FIN 601 - Principles of Finance: Financial Analysis of GlaxoSmithKline

VerifiedAdded on 2022/09/01

|21

|3499

|17

Report

AI Summary

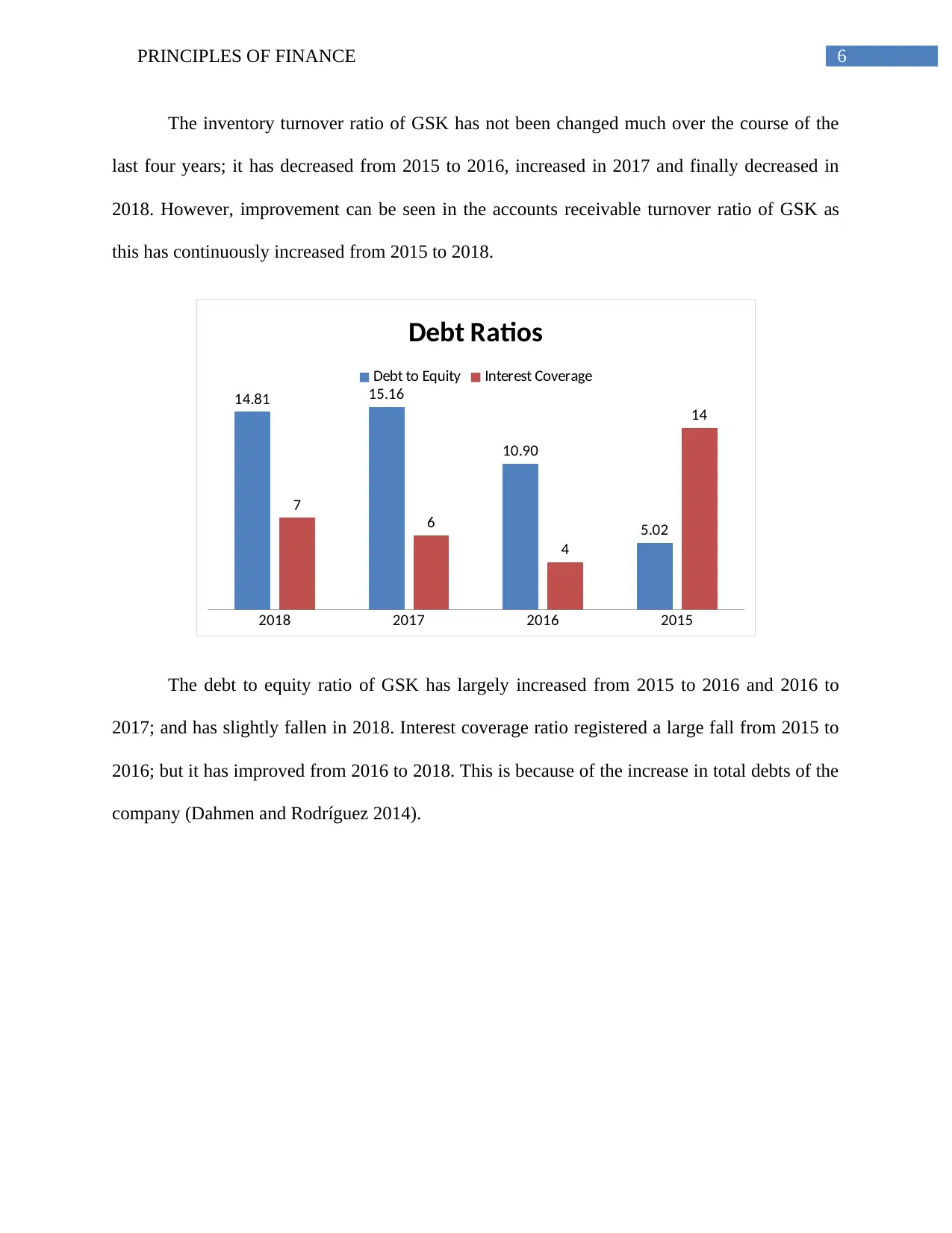

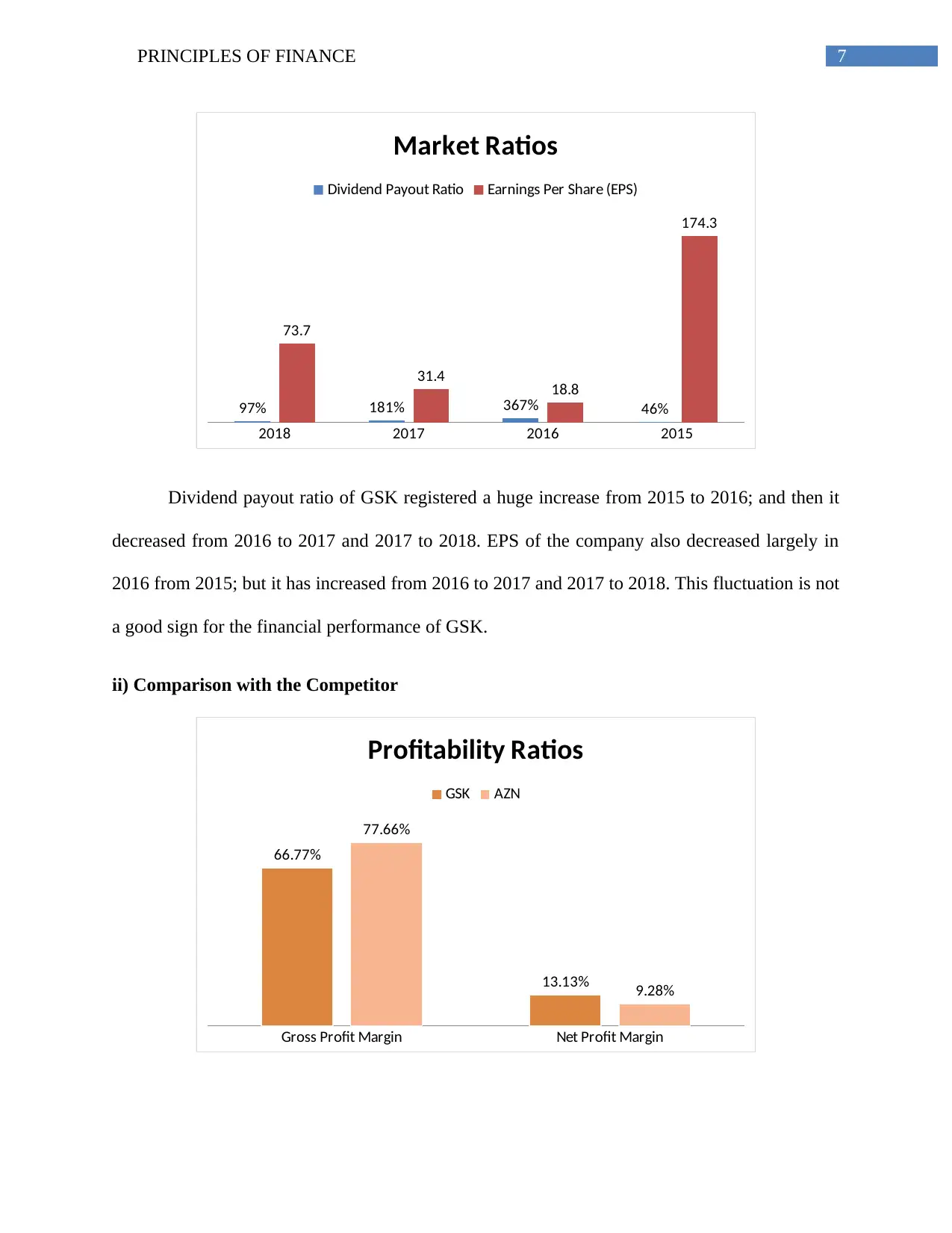

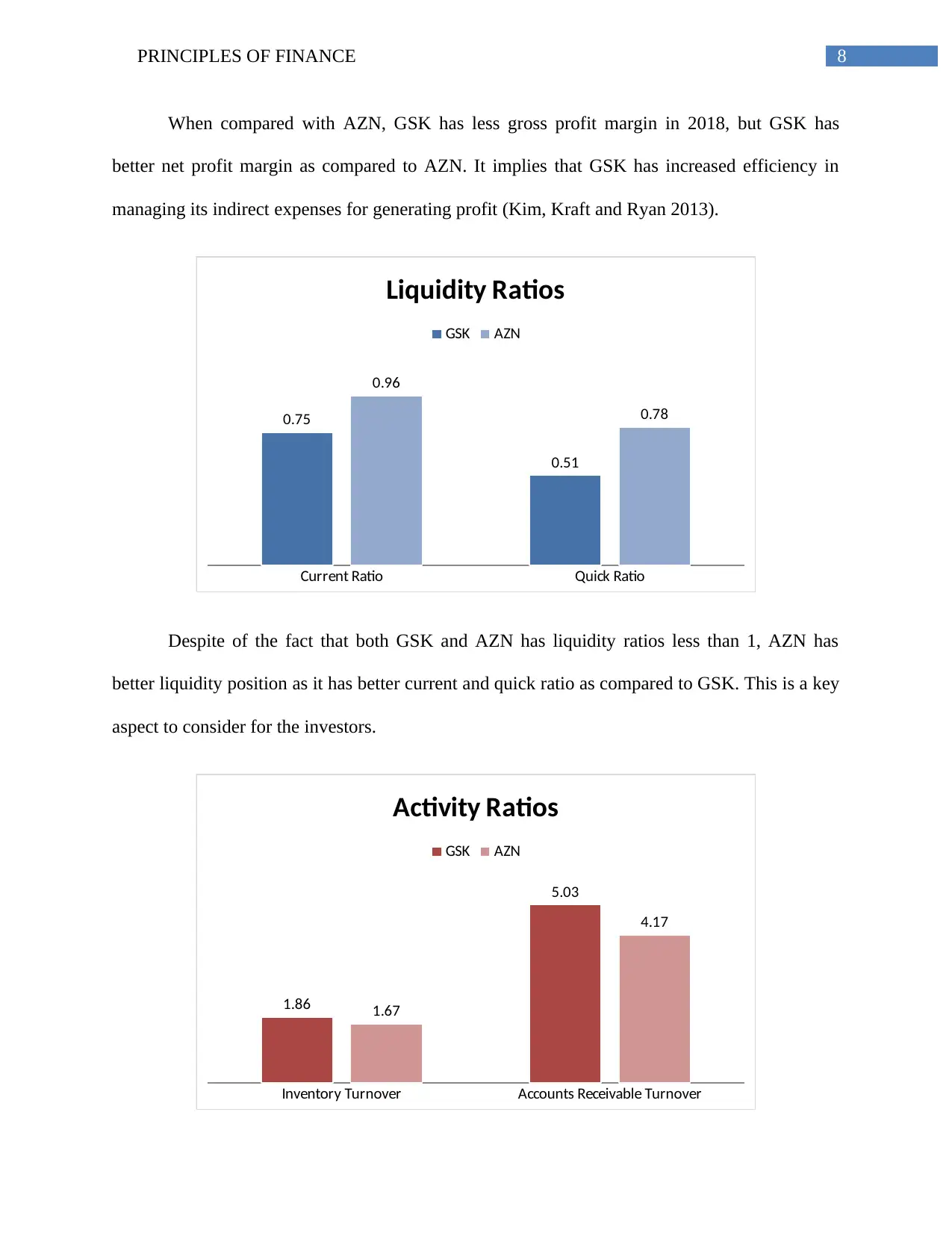

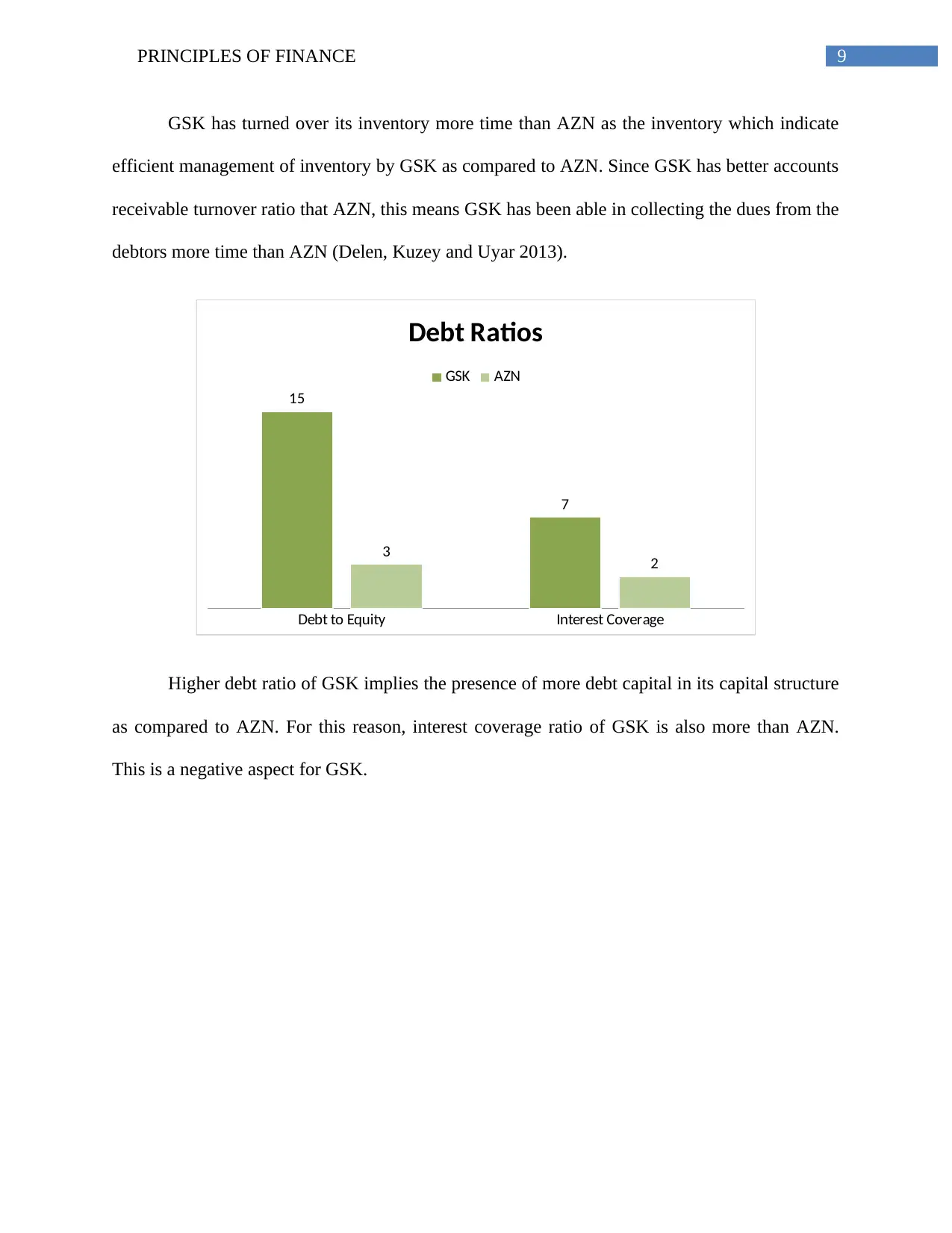

This report provides a comprehensive financial analysis of GlaxoSmithKline (GSK), a major multinational pharmaceutical company. It utilizes ratio analysis, including gross profit margin, net profit margin, current ratio, quick ratio, inventory turnover, accounts receivable turnover, and debt-to-equity ratio, to evaluate GSK's performance over a four-year period (2015-2018). The report compares GSK's financial health with its competitor AstraZeneca (AZN), highlighting key differences in profitability, liquidity, and debt management. Furthermore, trend analysis is employed to assess revenue, cost of sales, operating income, and net profit trends. The analysis reveals GSK's strengths and weaknesses, offering an investor's perspective and concluding with recommendations to enhance future financial performance, such as improving liquidity and managing debt. The report also acknowledges the limitations of ratio and trend analysis, considering factors like inflation and the aggregation of financial data.

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.