University of Greenwich: FINA1082 Coursework - Finance Analysis Report

VerifiedAdded on 2022/08/18

|19

|3990

|288

Report

AI Summary

This report analyzes the financial performance of Duronic PLC, a UK-based radio manufacturer, as part of a Principles of Finance coursework assignment. The analysis begins with the calculation of the Weighted Average Cost of Capital (WACC), considering the cost of equity, preference shares, and debt, ultimately determining the most appropriate cost of capital for evaluating a potential project. The report then calculates the Net Present Value (NPV) of the project at different discount rates, assessing its viability based on positive NPV outcomes. Furthermore, the report extends to the valuation of Walmart Inc. and Sysco Corp. using the Dividend Discount Model (DDM), determining their intrinsic values and providing recommendations for buying or selling the stocks based on the comparison of intrinsic values to current market prices. The report concludes with a discussion of stakeholder conflicts, dividend policies, and the Modigliani and Miller dividend policy theory, offering insights into corporate finance and investment decisions.

Running head: REPORT 0

PRINCIPLE OF FINANCE

MARCH 11, 2020

STUDENT DETAILS:

PRINCIPLE OF FINANCE

MARCH 11, 2020

STUDENT DETAILS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Contents

Answer one:.................................................................................................................................................2

1. Calculation of average cost of capital for evaluation of project of Duronic plc. –...........................2

2. Calculation of Net present value @ 5.16% -....................................................................................3

3. Calculation of Net present value @6% -..........................................................................................4

Answer two:................................................................................................................................................5

1. Calculation of intrinsic value of Walmart Inc. and Sysco Corp. -....................................................5

2. Valuation and assumption of dividend discount model –.................................................................8

3. Suggestions for buying or selling –..................................................................................................9

Answer three:............................................................................................................................................10

References.................................................................................................................................................14

Appendix...................................................................................................................................................16

Contents

Answer one:.................................................................................................................................................2

1. Calculation of average cost of capital for evaluation of project of Duronic plc. –...........................2

2. Calculation of Net present value @ 5.16% -....................................................................................3

3. Calculation of Net present value @6% -..........................................................................................4

Answer two:................................................................................................................................................5

1. Calculation of intrinsic value of Walmart Inc. and Sysco Corp. -....................................................5

2. Valuation and assumption of dividend discount model –.................................................................8

3. Suggestions for buying or selling –..................................................................................................9

Answer three:............................................................................................................................................10

References.................................................................................................................................................14

Appendix...................................................................................................................................................16

REPORT 2

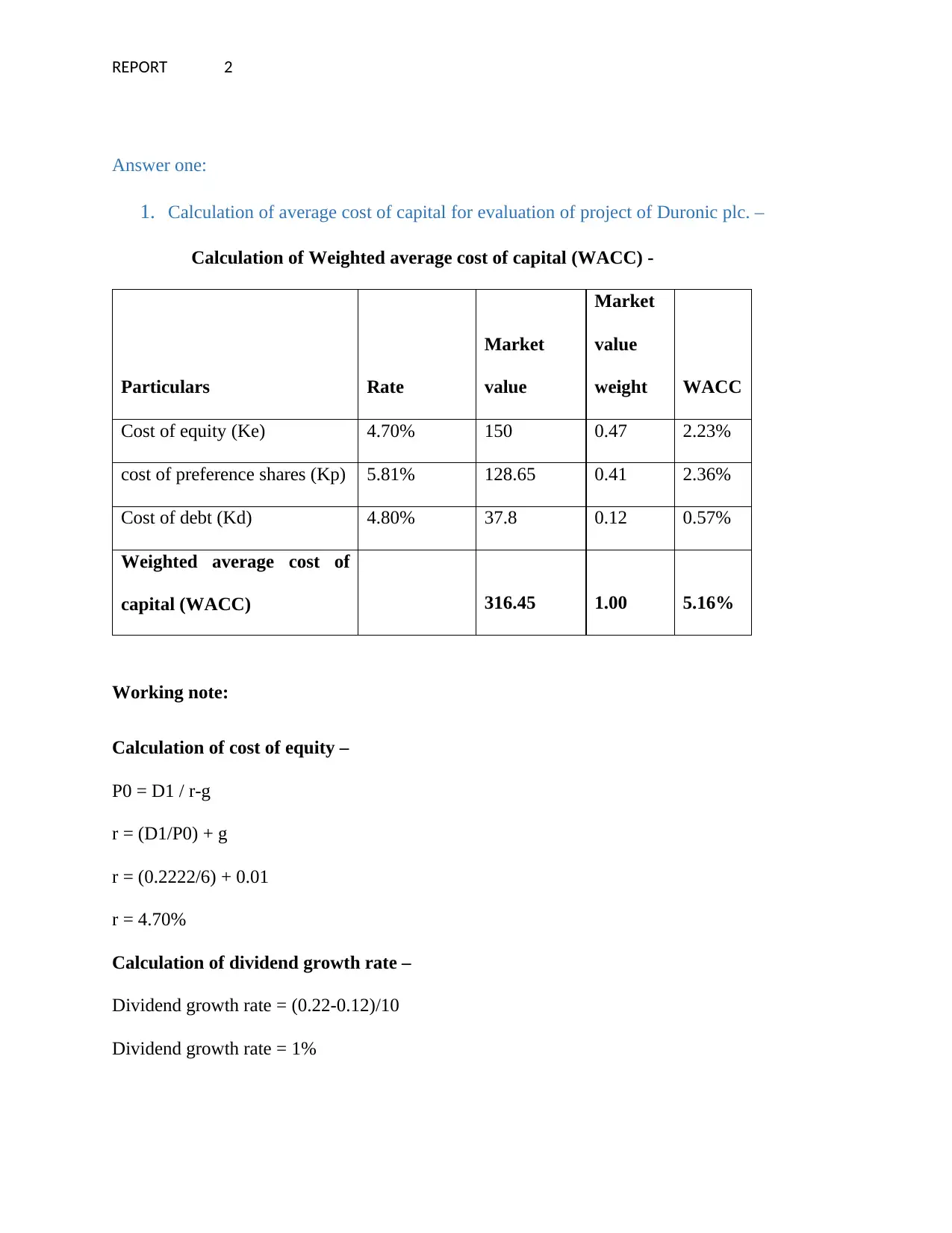

Answer one:

1. Calculation of average cost of capital for evaluation of project of Duronic plc. –

Calculation of Weighted average cost of capital (WACC) -

Particulars Rate

Market

value

Market

value

weight WACC

Cost of equity (Ke) 4.70% 150 0.47 2.23%

cost of preference shares (Kp) 5.81% 128.65 0.41 2.36%

Cost of debt (Kd) 4.80% 37.8 0.12 0.57%

Weighted average cost of

capital (WACC) 316.45 1.00 5.16%

Working note:

Calculation of cost of equity –

P0 = D1 / r-g

r = (D1/P0) + g

r = (0.2222/6) + 0.01

r = 4.70%

Calculation of dividend growth rate –

Dividend growth rate = (0.22-0.12)/10

Dividend growth rate = 1%

Answer one:

1. Calculation of average cost of capital for evaluation of project of Duronic plc. –

Calculation of Weighted average cost of capital (WACC) -

Particulars Rate

Market

value

Market

value

weight WACC

Cost of equity (Ke) 4.70% 150 0.47 2.23%

cost of preference shares (Kp) 5.81% 128.65 0.41 2.36%

Cost of debt (Kd) 4.80% 37.8 0.12 0.57%

Weighted average cost of

capital (WACC) 316.45 1.00 5.16%

Working note:

Calculation of cost of equity –

P0 = D1 / r-g

r = (D1/P0) + g

r = (0.2222/6) + 0.01

r = 4.70%

Calculation of dividend growth rate –

Dividend growth rate = (0.22-0.12)/10

Dividend growth rate = 1%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Calculation of preference shares-

Cost of preference shares (Kp) = Annual preference Dividend/market price per share

Cost of preference shares (Kp) = 0.09/1.55

Cost of preference shares (Kp) = 5.81%

Calculation of cost of debt -

Cost of debt (Kd) = Interest rate (1-tax)

Cost of debt (Kd) = 6% (1 - .20)

Cost of debt (Kd) = 4.80%

As per the view of CEO, the weighted average cost of capital should be 6%. On the other hand,

as per the view of project manager, the weighted average cost of capital should be 5.16%. It is

found that most appropriate cost of capital is 5.16%.The reason is that the company's WACC can

be used to estimate the expected costs for all of its financing. The high weighted average cost of

capital (high WACC) is normally the sign of higher risk related to the functions of company

(Khan, Javaid and Khan, 2018). The investor tends to need the additional return to

counterbalance additional risks. On the other hand, the concept behind making investment in the

undervalued stock is that price of the stock is more likely to increase over the period because this

is being sold for below worth (Santandrea, et. al, 2017). The project using less cost of capital will

be less risky. In this way, the most appropriate cost of capital is 5.16%.

2. Calculation of Net present value @ 5.16% - (Refer appendix 1)

From the calculation, it is found that net present value of company is $293.12. It is positive net

present value. The company should accept this project. The project having positive net present

Calculation of preference shares-

Cost of preference shares (Kp) = Annual preference Dividend/market price per share

Cost of preference shares (Kp) = 0.09/1.55

Cost of preference shares (Kp) = 5.81%

Calculation of cost of debt -

Cost of debt (Kd) = Interest rate (1-tax)

Cost of debt (Kd) = 6% (1 - .20)

Cost of debt (Kd) = 4.80%

As per the view of CEO, the weighted average cost of capital should be 6%. On the other hand,

as per the view of project manager, the weighted average cost of capital should be 5.16%. It is

found that most appropriate cost of capital is 5.16%.The reason is that the company's WACC can

be used to estimate the expected costs for all of its financing. The high weighted average cost of

capital (high WACC) is normally the sign of higher risk related to the functions of company

(Khan, Javaid and Khan, 2018). The investor tends to need the additional return to

counterbalance additional risks. On the other hand, the concept behind making investment in the

undervalued stock is that price of the stock is more likely to increase over the period because this

is being sold for below worth (Santandrea, et. al, 2017). The project using less cost of capital will

be less risky. In this way, the most appropriate cost of capital is 5.16%.

2. Calculation of Net present value @ 5.16% - (Refer appendix 1)

From the calculation, it is found that net present value of company is $293.12. It is positive net

present value. The company should accept this project. The project having positive net present

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

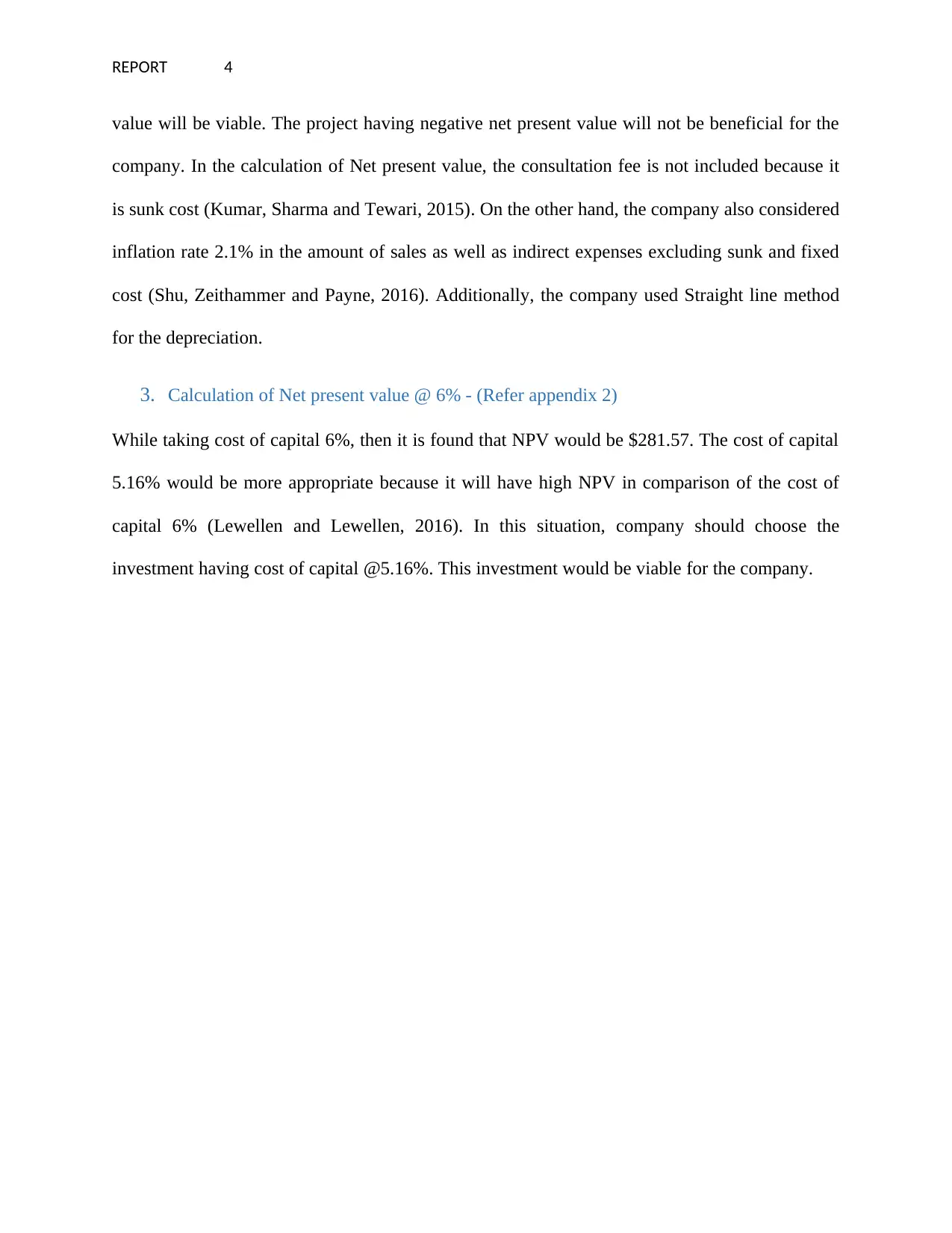

REPORT 4

value will be viable. The project having negative net present value will not be beneficial for the

company. In the calculation of Net present value, the consultation fee is not included because it

is sunk cost (Kumar, Sharma and Tewari, 2015). On the other hand, the company also considered

inflation rate 2.1% in the amount of sales as well as indirect expenses excluding sunk and fixed

cost (Shu, Zeithammer and Payne, 2016). Additionally, the company used Straight line method

for the depreciation.

3. Calculation of Net present value @ 6% - (Refer appendix 2)

While taking cost of capital 6%, then it is found that NPV would be $281.57. The cost of capital

5.16% would be more appropriate because it will have high NPV in comparison of the cost of

capital 6% (Lewellen and Lewellen, 2016). In this situation, company should choose the

investment having cost of capital @5.16%. This investment would be viable for the company.

value will be viable. The project having negative net present value will not be beneficial for the

company. In the calculation of Net present value, the consultation fee is not included because it

is sunk cost (Kumar, Sharma and Tewari, 2015). On the other hand, the company also considered

inflation rate 2.1% in the amount of sales as well as indirect expenses excluding sunk and fixed

cost (Shu, Zeithammer and Payne, 2016). Additionally, the company used Straight line method

for the depreciation.

3. Calculation of Net present value @ 6% - (Refer appendix 2)

While taking cost of capital 6%, then it is found that NPV would be $281.57. The cost of capital

5.16% would be more appropriate because it will have high NPV in comparison of the cost of

capital 6% (Lewellen and Lewellen, 2016). In this situation, company should choose the

investment having cost of capital @5.16%. This investment would be viable for the company.

REPORT 5

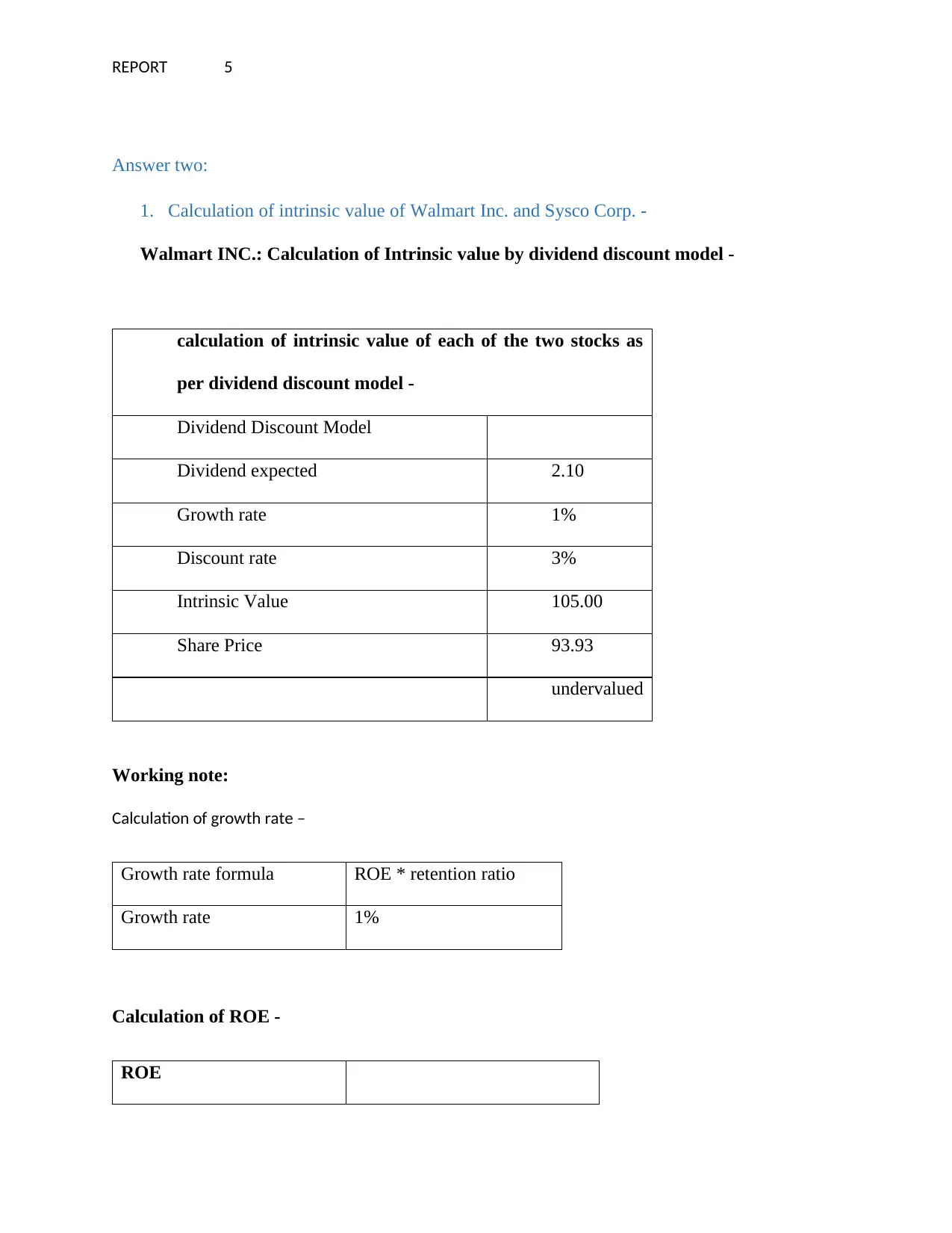

Answer two:

1. Calculation of intrinsic value of Walmart Inc. and Sysco Corp. -

Walmart INC.: Calculation of Intrinsic value by dividend discount model -

calculation of intrinsic value of each of the two stocks as

per dividend discount model -

Dividend Discount Model

Dividend expected 2.10

Growth rate 1%

Discount rate 3%

Intrinsic Value 105.00

Share Price 93.93

undervalued

Working note:

Calculation of growth rate –

Growth rate formula ROE * retention ratio

Growth rate 1%

Calculation of ROE -

ROE

Answer two:

1. Calculation of intrinsic value of Walmart Inc. and Sysco Corp. -

Walmart INC.: Calculation of Intrinsic value by dividend discount model -

calculation of intrinsic value of each of the two stocks as

per dividend discount model -

Dividend Discount Model

Dividend expected 2.10

Growth rate 1%

Discount rate 3%

Intrinsic Value 105.00

Share Price 93.93

undervalued

Working note:

Calculation of growth rate –

Growth rate formula ROE * retention ratio

Growth rate 1%

Calculation of ROE -

ROE

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

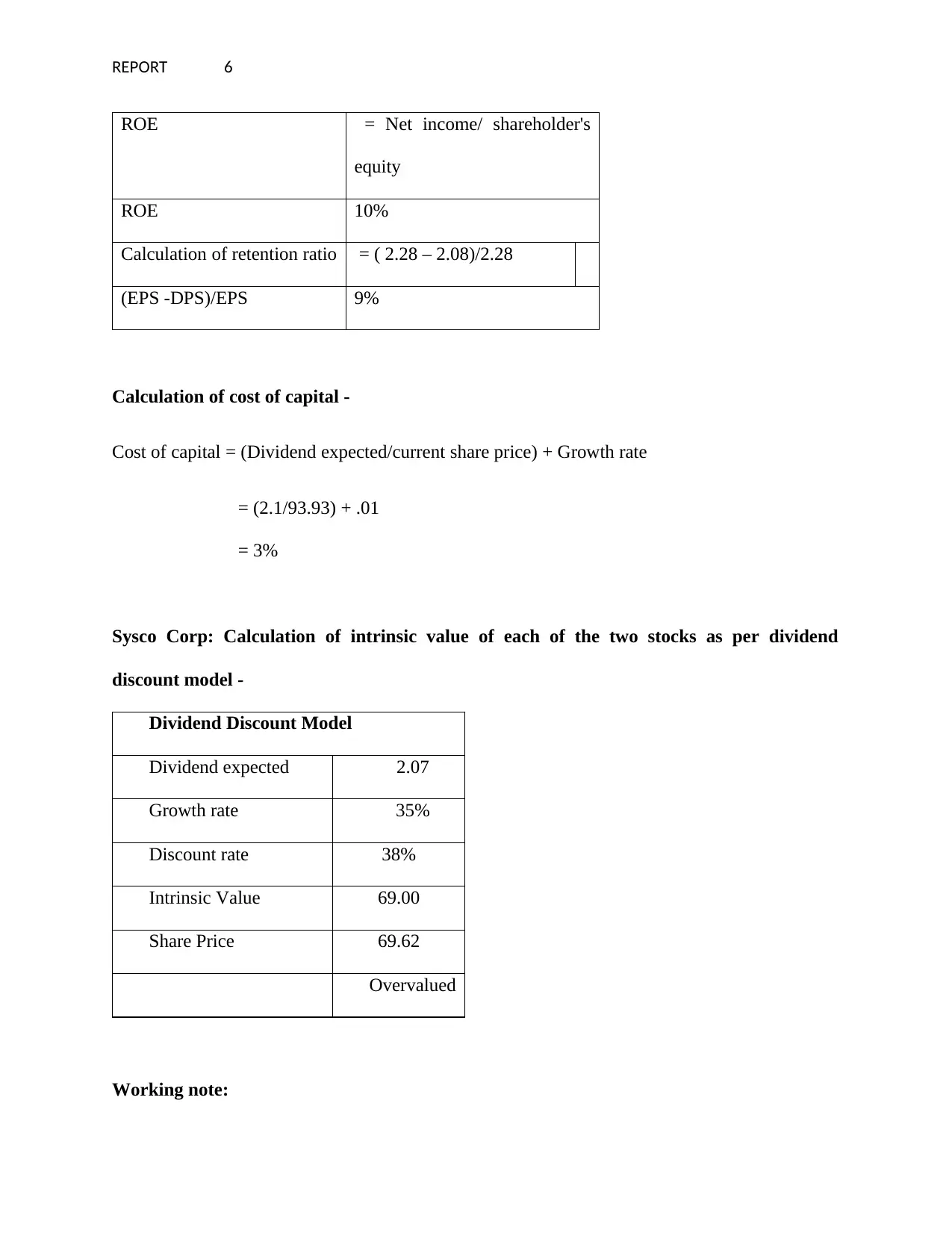

ROE = Net income/ shareholder's

equity

ROE 10%

Calculation of retention ratio = ( 2.28 – 2.08)/2.28

(EPS -DPS)/EPS 9%

Calculation of cost of capital -

Cost of capital = (Dividend expected/current share price) + Growth rate

= (2.1/93.93) + .01

= 3%

Sysco Corp: Calculation of intrinsic value of each of the two stocks as per dividend

discount model -

Working note:

Dividend Discount Model

Dividend expected 2.07

Growth rate 35%

Discount rate 38%

Intrinsic Value 69.00

Share Price 69.62

Overvalued

ROE = Net income/ shareholder's

equity

ROE 10%

Calculation of retention ratio = ( 2.28 – 2.08)/2.28

(EPS -DPS)/EPS 9%

Calculation of cost of capital -

Cost of capital = (Dividend expected/current share price) + Growth rate

= (2.1/93.93) + .01

= 3%

Sysco Corp: Calculation of intrinsic value of each of the two stocks as per dividend

discount model -

Working note:

Dividend Discount Model

Dividend expected 2.07

Growth rate 35%

Discount rate 38%

Intrinsic Value 69.00

Share Price 69.62

Overvalued

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

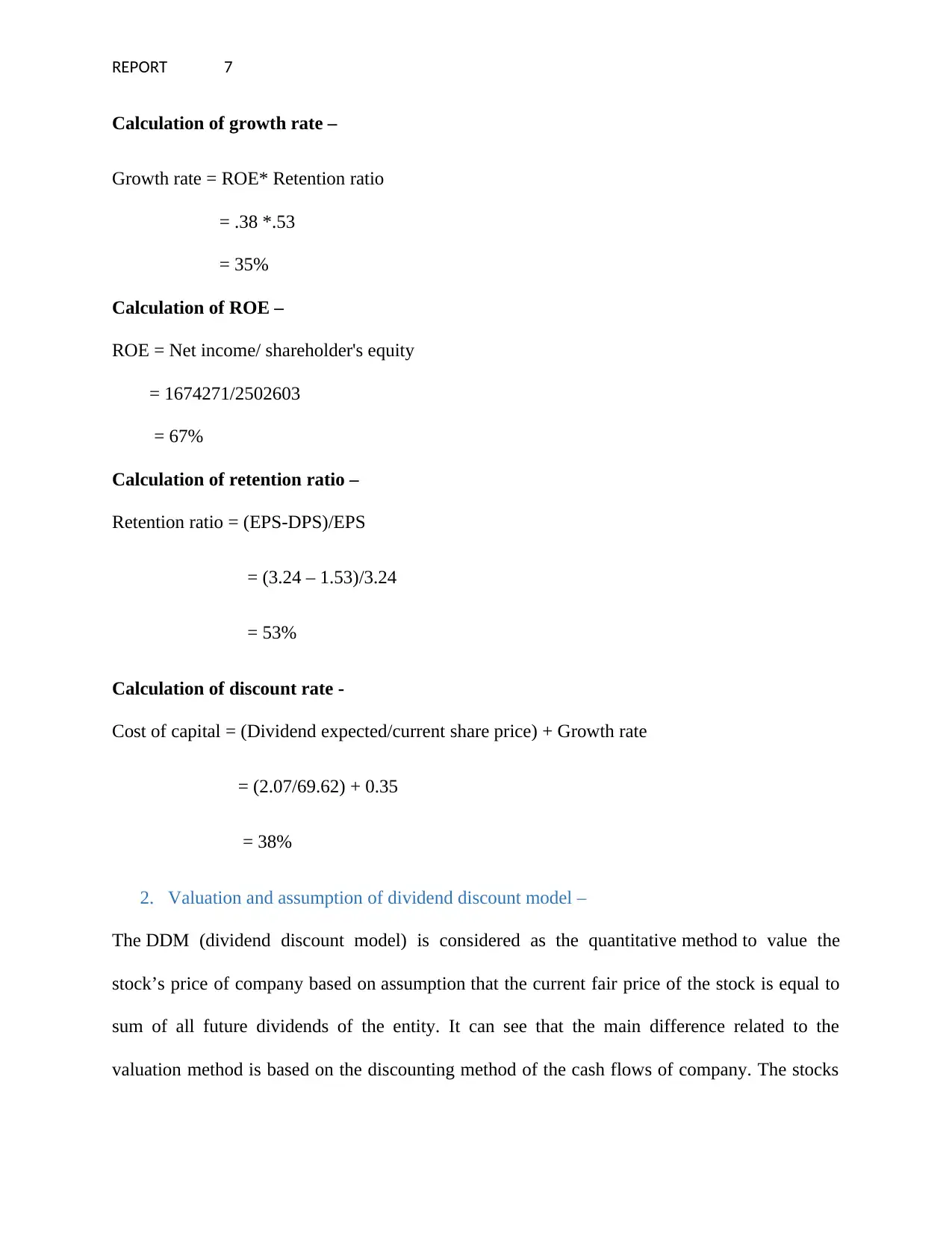

Calculation of growth rate –

Growth rate = ROE* Retention ratio

= .38 *.53

= 35%

Calculation of ROE –

ROE = Net income/ shareholder's equity

= 1674271/2502603

= 67%

Calculation of retention ratio –

Retention ratio = (EPS-DPS)/EPS

= (3.24 – 1.53)/3.24

= 53%

Calculation of discount rate -

Cost of capital = (Dividend expected/current share price) + Growth rate

= (2.07/69.62) + 0.35

= 38%

2. Valuation and assumption of dividend discount model –

The DDM (dividend discount model) is considered as the quantitative method to value the

stock’s price of company based on assumption that the current fair price of the stock is equal to

sum of all future dividends of the entity. It can see that the main difference related to the

valuation method is based on the discounting method of the cash flows of company. The stocks

Calculation of growth rate –

Growth rate = ROE* Retention ratio

= .38 *.53

= 35%

Calculation of ROE –

ROE = Net income/ shareholder's equity

= 1674271/2502603

= 67%

Calculation of retention ratio –

Retention ratio = (EPS-DPS)/EPS

= (3.24 – 1.53)/3.24

= 53%

Calculation of discount rate -

Cost of capital = (Dividend expected/current share price) + Growth rate

= (2.07/69.62) + 0.35

= 38%

2. Valuation and assumption of dividend discount model –

The DDM (dividend discount model) is considered as the quantitative method to value the

stock’s price of company based on assumption that the current fair price of the stock is equal to

sum of all future dividends of the entity. It can see that the main difference related to the

valuation method is based on the discounting method of the cash flows of company. The stocks

REPORT 8

are finally worth no more than what this would render investor in future dividend along with

current dividend. It is stated by the financial theory that the value of the stocks is worth all of

upcoming cash flows expected to be made by an entity, discounted by the proper risk adjusted

rate. As per the dividend discount model, the dividend is considered as cash flow that is returned

to company’s shareholders. It is essential to know the concept of time value of money (TVM) as

well as discounting. According to the dividend discount model (DDM), one can calculate the

value of dividend payment that someone thinks the stock would throw-off in the periods ahead.

The dividend discount model states that –

P0 = D1

r

Here, P0 = price in year zero, having no dividend growth

D1 = payment of future dividend

r = Discount rate

Further, the dividend discount model is has various assumptions. As per the above discussion in

relation to the assumptions, there are also assumptions in relation to the growth rate, rate of tax

as well as rate of interest. Most of the factors are beyond regulation of the investor. This factor

too reduce the model’s validity. The assumption that the growth rate in dividend has to be

endless over the period is very critical assumption to be, particularly provided the volatility of

earning (Porter and South-Winter, 2017).

are finally worth no more than what this would render investor in future dividend along with

current dividend. It is stated by the financial theory that the value of the stocks is worth all of

upcoming cash flows expected to be made by an entity, discounted by the proper risk adjusted

rate. As per the dividend discount model, the dividend is considered as cash flow that is returned

to company’s shareholders. It is essential to know the concept of time value of money (TVM) as

well as discounting. According to the dividend discount model (DDM), one can calculate the

value of dividend payment that someone thinks the stock would throw-off in the periods ahead.

The dividend discount model states that –

P0 = D1

r

Here, P0 = price in year zero, having no dividend growth

D1 = payment of future dividend

r = Discount rate

Further, the dividend discount model is has various assumptions. As per the above discussion in

relation to the assumptions, there are also assumptions in relation to the growth rate, rate of tax

as well as rate of interest. Most of the factors are beyond regulation of the investor. This factor

too reduce the model’s validity. The assumption that the growth rate in dividend has to be

endless over the period is very critical assumption to be, particularly provided the volatility of

earning (Porter and South-Winter, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

3. Suggestions for buying or selling –

From the above calculation, it is found that the intrinsic value of Walmart Inc. is $105. It can see

that current share price is $93.93. It is evident that the market price can be meaningfully lower or

higher in comparison of intrinsic value of the stocks. The intrinsic value of shares is more than

the current share price. In this way, the shares are undervalued. In this way, the undervalued

stocks are described as the stock that are selling at the price suggestively below what is assumed

to be the intrinsic value. Therefore, the undervalued shares should be purchased. The reason is

that purchase the undervalued stock means the risk of losing money is decreased, also in the

condition when the company is not doing well.

Further, it is found that intrinsic value of Sysco Corp is $69. On the other hand, the current share

price of the company is $69.62. It means the shares are overvalued. It can see that the overvalued

shares should be sold. The reason is that the overvalued stock is likely to experience the price

reduction and return to the level that better reflects the financial position of company (Kumar,

Sharma and Tewari, 2015).

3. Suggestions for buying or selling –

From the above calculation, it is found that the intrinsic value of Walmart Inc. is $105. It can see

that current share price is $93.93. It is evident that the market price can be meaningfully lower or

higher in comparison of intrinsic value of the stocks. The intrinsic value of shares is more than

the current share price. In this way, the shares are undervalued. In this way, the undervalued

stocks are described as the stock that are selling at the price suggestively below what is assumed

to be the intrinsic value. Therefore, the undervalued shares should be purchased. The reason is

that purchase the undervalued stock means the risk of losing money is decreased, also in the

condition when the company is not doing well.

Further, it is found that intrinsic value of Sysco Corp is $69. On the other hand, the current share

price of the company is $69.62. It means the shares are overvalued. It can see that the overvalued

shares should be sold. The reason is that the overvalued stock is likely to experience the price

reduction and return to the level that better reflects the financial position of company (Kumar,

Sharma and Tewari, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

Answer three:

The confliction between stakeholders as well as managers is biggest issue to be considered in

entity. The analysts does not consider the dividend policies to address the agency issue between

minority shareholders and managers. As per the substitute model, the cash dividend can be

considered as alternative of legal security of the investor. The organisations are likely to

discharge higher dividend at the time of disorganization of legal security of the shareholders. The

quality of governance is enhanced while the minority shareholders influence the managers for

making payment of cash dividend. Though, while dividend is used in different governance

mechanism, then the constant role of dividend will be reduced.

The theories based on dividend policies were argued to explain the validation in relation to

dividend payment by the corporation. The top-level management of the companies have different

views in between payment of dividend or reinvestment of the profit on business. Even those

companies that make payment of dividend do nt seem to have stationary formula to determine

the pay-out ratio. Abel (2018) explained that the dividend is periodic payment to equity

shareholders that together with capital gain is return for making investment in the stock of

company. Further, Mishan (2015) claimed that this is not easy to render empirical test on the rate

of return as well as dividend allocation policy. Hypothetically, the companies having high

dividend pay out also get high rate of return. For explaining the main arguments in relation to the

payment of dividend by companies, it is essential to understand the Modigliani and Merton

Miller dividend policy theory.

Answer three:

The confliction between stakeholders as well as managers is biggest issue to be considered in

entity. The analysts does not consider the dividend policies to address the agency issue between

minority shareholders and managers. As per the substitute model, the cash dividend can be

considered as alternative of legal security of the investor. The organisations are likely to

discharge higher dividend at the time of disorganization of legal security of the shareholders. The

quality of governance is enhanced while the minority shareholders influence the managers for

making payment of cash dividend. Though, while dividend is used in different governance

mechanism, then the constant role of dividend will be reduced.

The theories based on dividend policies were argued to explain the validation in relation to

dividend payment by the corporation. The top-level management of the companies have different

views in between payment of dividend or reinvestment of the profit on business. Even those

companies that make payment of dividend do nt seem to have stationary formula to determine

the pay-out ratio. Abel (2018) explained that the dividend is periodic payment to equity

shareholders that together with capital gain is return for making investment in the stock of

company. Further, Mishan (2015) claimed that this is not easy to render empirical test on the rate

of return as well as dividend allocation policy. Hypothetically, the companies having high

dividend pay out also get high rate of return. For explaining the main arguments in relation to the

payment of dividend by companies, it is essential to understand the Modigliani and Merton

Miller dividend policy theory.

REPORT 11

Franco Modigliani and Merton Miller proposed MM approach in 1961. It is advised by them that

the capital profit as well as dividend is equal while the investors consider return on investment. It

is evident that the earning is direct result of the investment policy of corporation. It can have

influence on the corporate values. Therefore, the MM approach states that if investor knows the

decision related to investment considered by the company, then the investors are not required to

take dividend policy related decisions. It is also stated by the theory that the investor needs to

keep own cash inflow irrespective of whether the stock pays dividend or not. Modigliani and

Miller claimed the dividend distribution to the shareholder as irrelevant as stock’s prices reduces

because of the allocation of the dividend. It is implied by MM theory that the cost of debt is

equivalent to cost of equity. Additionally, the cost of capital is not influenced by leverage.

According to this theory, there is no flotation or transaction cost. In addition, there is also no

influence of investor on share’s market value. Furthermore, this theory also assumes that the tax

is not exist in relation to the investment policy. It also state that the company does not change

their investment policy. No changes have been made in risk as well as the return in relation to

upcoming financing.

The assumptions of MM approach are not rationally solid. For this reason, this approach is

criticized. The assumption of no tax and no floating cost is impossible in the present world.

However, the external as well as internal financing are not same. In this way, the MM approach

of dividend policy is the stimulating as well as remarkable theory for the share’s valuation. These

famous methods believe in the irrelevancy of dividend. However, the policy su ers fromff

different significant restrictions. Therefore, this is critiqued related to the assumptions. Further,

Modigliani and Miller raised questions in 1960. They asked that whether the corporations

allocate dividend consistently at the premium over those with niggardly pay-out (Zolfani,

Franco Modigliani and Merton Miller proposed MM approach in 1961. It is advised by them that

the capital profit as well as dividend is equal while the investors consider return on investment. It

is evident that the earning is direct result of the investment policy of corporation. It can have

influence on the corporate values. Therefore, the MM approach states that if investor knows the

decision related to investment considered by the company, then the investors are not required to

take dividend policy related decisions. It is also stated by the theory that the investor needs to

keep own cash inflow irrespective of whether the stock pays dividend or not. Modigliani and

Miller claimed the dividend distribution to the shareholder as irrelevant as stock’s prices reduces

because of the allocation of the dividend. It is implied by MM theory that the cost of debt is

equivalent to cost of equity. Additionally, the cost of capital is not influenced by leverage.

According to this theory, there is no flotation or transaction cost. In addition, there is also no

influence of investor on share’s market value. Furthermore, this theory also assumes that the tax

is not exist in relation to the investment policy. It also state that the company does not change

their investment policy. No changes have been made in risk as well as the return in relation to

upcoming financing.

The assumptions of MM approach are not rationally solid. For this reason, this approach is

criticized. The assumption of no tax and no floating cost is impossible in the present world.

However, the external as well as internal financing are not same. In this way, the MM approach

of dividend policy is the stimulating as well as remarkable theory for the share’s valuation. These

famous methods believe in the irrelevancy of dividend. However, the policy su ers fromff

different significant restrictions. Therefore, this is critiqued related to the assumptions. Further,

Modigliani and Miller raised questions in 1960. They asked that whether the corporations

allocate dividend consistently at the premium over those with niggardly pay-out (Zolfani,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.