Report on Principles of Financial Management: Task 1 and Task 2

VerifiedAdded on 2023/01/06

|18

|5444

|46

Report

AI Summary

This report provides a comprehensive overview of financial management principles, encompassing various aspects crucial for effective decision-making. It begins by exploring the factors, techniques, and approaches to sound decision-making, emphasizing the importance of both financial and non-financial information. The report then delves into stakeholder management, highlighting the significance of fostering positive relationships with various stakeholder groups and addressing their diverse interests. Furthermore, it examines the value of management accounting techniques, particularly in cost control, profit maximization, and the detection of fraudulent activities. The report also covers ethical decision-making processes, emphasizing the application of ethical principles in evaluating alternatives. In the second part, the report focuses on financial analysis, including ratio analysis and its role in assisting management in making informed decisions. Investment appraisal techniques are evaluated, underscoring their importance in financial decision-making and ensuring long-term sustainability. Recommendations for improving financial sustainability are also presented. The report concludes by emphasizing the critical role of financial data and strategic planning in achieving organizational success.

Principles of Financial

Management

1

Management

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.Factor, techniques and approaches to effective decision making........................................3

2. Stakeholder management....................................................................................................5

3. Value of management accounting techniques....................................................................6

4. Fraud detection and ethical decision making.....................................................................7

5. Reflection...........................................................................................................................8

Task 2...............................................................................................................................................9

1. Ratio Analysis....................................................................................................................9

2.Ratio analysis as assistance tool for management.............................................................12

3.Evaluation of investment appraisal techniques.................................................................12

4. Importance of techniques in financial decision making...................................................14

5.Financial decision support long-term sustainability..........................................................15

6. Recommendations to improve financial sustainability.....................................................16

Conclusion.....................................................................................................................................16

References......................................................................................................................................18

2

Introduction......................................................................................................................................3

Task 1...............................................................................................................................................3

1.Factor, techniques and approaches to effective decision making........................................3

2. Stakeholder management....................................................................................................5

3. Value of management accounting techniques....................................................................6

4. Fraud detection and ethical decision making.....................................................................7

5. Reflection...........................................................................................................................8

Task 2...............................................................................................................................................9

1. Ratio Analysis....................................................................................................................9

2.Ratio analysis as assistance tool for management.............................................................12

3.Evaluation of investment appraisal techniques.................................................................12

4. Importance of techniques in financial decision making...................................................14

5.Financial decision support long-term sustainability..........................................................15

6. Recommendations to improve financial sustainability.....................................................16

Conclusion.....................................................................................................................................16

References......................................................................................................................................18

2

Introduction

Part of accounting which that helps managers in managerial decision making is known as

management accounting. Managers use variety of techniques for better control and performance

management (Soderstrom, Soderstrom and Stewart, 2017). This report throw light on various

aspects of effective and ethical decision-making. Various stakeholders of business has varied

interests and seek different types of financial and non-financial information before reaching a

decision. These accounting techniques helps in reaching a conclusion by different stakeholder

groups. It is presentation of information in such a way that helps in cost control and profit and

value maximisation. It is helpful in avoiding conflicts and detecting mismanagement.

Financial data plays an important role in operational and strategic decision-making. This

report shows various techniques that are applied before taking working capital decisions as well

as long term investment decisions. This report also presents financial information in the form of

ratio calculation to show how financial performance is interpreted.

Task 1

1.Factor, techniques and approaches to effective decision making

Success or failure of an organisation depends on the quality of decision-making by the

management. Management uses both financial and non-financial information to arrive at any

decision. A decision is a course of action and conscious choice on the part of manager (Bryson,

2017). It is selecting a course of behaviour, out of a set of alternatives available to achieve a

desired result. Thus, decision-making can be said a part of planning function and base for

controlling function of management. Following are the various factors that have an effect over

decision-making: Organisation structure – Administrative and operational structure of an organisation

plays a huge role in deciding approach and technique taken by management for decision-

making. Management has to consider other factors as well such as availability of

adequate and accurate information, risk and impact of decision, time constraints, business

of the company, industry standing of the product and company, business environment,

etc. before taking any decision.

Personality of decision-maker – Personal habits and social and cultural influences over

management plays deciding role in selecting a course out of available options. For

3

Part of accounting which that helps managers in managerial decision making is known as

management accounting. Managers use variety of techniques for better control and performance

management (Soderstrom, Soderstrom and Stewart, 2017). This report throw light on various

aspects of effective and ethical decision-making. Various stakeholders of business has varied

interests and seek different types of financial and non-financial information before reaching a

decision. These accounting techniques helps in reaching a conclusion by different stakeholder

groups. It is presentation of information in such a way that helps in cost control and profit and

value maximisation. It is helpful in avoiding conflicts and detecting mismanagement.

Financial data plays an important role in operational and strategic decision-making. This

report shows various techniques that are applied before taking working capital decisions as well

as long term investment decisions. This report also presents financial information in the form of

ratio calculation to show how financial performance is interpreted.

Task 1

1.Factor, techniques and approaches to effective decision making

Success or failure of an organisation depends on the quality of decision-making by the

management. Management uses both financial and non-financial information to arrive at any

decision. A decision is a course of action and conscious choice on the part of manager (Bryson,

2017). It is selecting a course of behaviour, out of a set of alternatives available to achieve a

desired result. Thus, decision-making can be said a part of planning function and base for

controlling function of management. Following are the various factors that have an effect over

decision-making: Organisation structure – Administrative and operational structure of an organisation

plays a huge role in deciding approach and technique taken by management for decision-

making. Management has to consider other factors as well such as availability of

adequate and accurate information, risk and impact of decision, time constraints, business

of the company, industry standing of the product and company, business environment,

etc. before taking any decision.

Personality of decision-maker – Personal habits and social and cultural influences over

management plays deciding role in selecting a course out of available options. For

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

example, intelligence and cognitive constraints of managers, their prejudices and risk

appetite, etc. influence the process of rational decision-making.

Approaches to decision-making

There are various approaches for effective decision-making. Few are below mentioned: Autocratic approach – Such approach is found where decisions are completely taken at

top level of management. This approach is suitable when there is urgency to make a

decision and involving a lot of people may prove counterproductive. This type of

decision-making is found in companies which are rigid in organisational structure and

have strict command chain.

Democratic approach – This approach invites participation and seek consensus.

Whenever a decision is to be taken which is going to impact a lot of people or which is

having a huge risk. Different people give different ideas and then votes are invited on it.

Decision which is approved by majority is taken as final decision (Malakouti, Rezaei and

Shahijan, 2017). These additional inputs help in finding innovative ideas to reduce or

eliminate risk and encourage employee development but this approach is very time

consuming and is not fit for urgent decisions.

Techniques of decision-making

Management use various techniques such as marginal cost analysis, cost benefit analysis,

operations research, linear programming, network analysis, co-effectiveness analysis, etc. Few

techniques of decision-making are following: Marginal Cost Analysis – This technique is also known as marginal costing. In it,

additional revenues from producing one extra unit are compared with additional cost

incurred to produce it. Profit is maximum at the point of production, where marginal

revenue and cost are at same level i.e. break even point.

Operations Research – It is defined as a scientific method to study business problems in

such a way that provides quantitative information to management for reaching a

conclusion (Odero, Ochara and Quenum, 2017). Its purpose is to provide managers with

scientific basis to solve operational issues rather than based on intuition or past

experience. For example, Inventory models to control level of inventory, linear

programming for allocation of work, sequencing theory, etc.

4

appetite, etc. influence the process of rational decision-making.

Approaches to decision-making

There are various approaches for effective decision-making. Few are below mentioned: Autocratic approach – Such approach is found where decisions are completely taken at

top level of management. This approach is suitable when there is urgency to make a

decision and involving a lot of people may prove counterproductive. This type of

decision-making is found in companies which are rigid in organisational structure and

have strict command chain.

Democratic approach – This approach invites participation and seek consensus.

Whenever a decision is to be taken which is going to impact a lot of people or which is

having a huge risk. Different people give different ideas and then votes are invited on it.

Decision which is approved by majority is taken as final decision (Malakouti, Rezaei and

Shahijan, 2017). These additional inputs help in finding innovative ideas to reduce or

eliminate risk and encourage employee development but this approach is very time

consuming and is not fit for urgent decisions.

Techniques of decision-making

Management use various techniques such as marginal cost analysis, cost benefit analysis,

operations research, linear programming, network analysis, co-effectiveness analysis, etc. Few

techniques of decision-making are following: Marginal Cost Analysis – This technique is also known as marginal costing. In it,

additional revenues from producing one extra unit are compared with additional cost

incurred to produce it. Profit is maximum at the point of production, where marginal

revenue and cost are at same level i.e. break even point.

Operations Research – It is defined as a scientific method to study business problems in

such a way that provides quantitative information to management for reaching a

conclusion (Odero, Ochara and Quenum, 2017). Its purpose is to provide managers with

scientific basis to solve operational issues rather than based on intuition or past

experience. For example, Inventory models to control level of inventory, linear

programming for allocation of work, sequencing theory, etc.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Stakeholder management

Stakeholders are those parties or group that have stake or interest in projects and business

undertaken by company. They can be both external and internal to company. Internal

stakeholders include shareholders, employees, management, etc. while external stakeholders

include suppliers, customers, government, etc. Managing stakeholders is fostering good

relationship with various pressure groups of an organisation (Freeman, 2017). It involves the

process of identifying stakeholders, assessing their expectations and planning and implementing

various strategies to maintain quality of relationship. Good stakeholder management helps

company in reducing costs and maximising value. It also helps company in gaining goodwill,

competitive advantage and social license to operate.

Various stakeholder have variety of interests and expectations from a company. These

varied expectations often result in conflicts. For example, management seeks high profit and thus

in bid to reduce cost, may be less willing to pay good salary packages or plans to lay off staff.

This will not go well in employees. Thus, it is important for managers to develop a good

stakeholder management plan. A good plan outlines appropriate strategies to effectively engage

various stakeholders and minimise the risk of conflict. First step in a plan is to identify various

stakeholders and their interest in the concerned project. Next step is to determine their influence

on the organisational decision-making. Then, priority among stakeholders shall be identified and

5

Illustration 1: Stakeholder

Management, 2019

Stakeholders are those parties or group that have stake or interest in projects and business

undertaken by company. They can be both external and internal to company. Internal

stakeholders include shareholders, employees, management, etc. while external stakeholders

include suppliers, customers, government, etc. Managing stakeholders is fostering good

relationship with various pressure groups of an organisation (Freeman, 2017). It involves the

process of identifying stakeholders, assessing their expectations and planning and implementing

various strategies to maintain quality of relationship. Good stakeholder management helps

company in reducing costs and maximising value. It also helps company in gaining goodwill,

competitive advantage and social license to operate.

Various stakeholder have variety of interests and expectations from a company. These

varied expectations often result in conflicts. For example, management seeks high profit and thus

in bid to reduce cost, may be less willing to pay good salary packages or plans to lay off staff.

This will not go well in employees. Thus, it is important for managers to develop a good

stakeholder management plan. A good plan outlines appropriate strategies to effectively engage

various stakeholders and minimise the risk of conflict. First step in a plan is to identify various

stakeholders and their interest in the concerned project. Next step is to determine their influence

on the organisational decision-making. Then, priority among stakeholders shall be identified and

5

Illustration 1: Stakeholder

Management, 2019

based on priority, appropriate way to engage with them shall be identified. Final step is to

develop and implement a plan based on the consultation with various stakeholders.

3. Value of management accounting techniques

Primary objective of management is to maximise value of business. Thus, it aims to

increase profit and control cost. Cost control includes determining various ways for completing

each operation in more economical manner (Collis and Hussey, 2017). It involves setting

standards and then comparing actual results against such standards. It helps in achieving

optimum cost level which improves profitability and increases competitiveness. Company

produces a product according to standard operating methods deployed such as budgetary

controls, detailed standard costs, etc. Budgetary control is a tool of management accounting

practice wherein with the use of multiple budgets, managers perform planning and controlling

functions. Budgets plans are formulated for a given period of time in numerical terms. It serves

as a base for controlling and monitoring where in standards are compared with actual results to

ascertain deviations and implement corrective actions. It helps in maximum utilisation of

resources. Other than budgets, standard costing is another prominent tool used for cost control. It

establishes target costs to be achieved under given working conditions. These standard cost are

then compared with actual cost to measure and analyse variances. This helps in fixing

responsibility for non-standard performance and focus attention on areas which require cost

improvement. It can also help management in fixing selling price and performance based

incentives for employees.

Other than cost control, profit maximisation is the way to increase shareholders' value.

Management accountants performs various operations to identify those ways in which business

can improve its revenue (Cooper, 2017). Managers use various managerial reports, performance

metrics, revenue projections, budgets, cash forecasts, etc. to make informed decisions. These

informations also help management in taking other important strategic decisions such as new

projects, capital investments, change in marketing policy, change in revenue projections, etc. For

this, managers use various accounting techniques such as ratios, key performance indicators,

Management Information Systems, financial modelling, etc. Data-backed financial reporting and

control ensures that management is making accurate decisions to maximise future returns and

minimise uncertainty and risk.

6

develop and implement a plan based on the consultation with various stakeholders.

3. Value of management accounting techniques

Primary objective of management is to maximise value of business. Thus, it aims to

increase profit and control cost. Cost control includes determining various ways for completing

each operation in more economical manner (Collis and Hussey, 2017). It involves setting

standards and then comparing actual results against such standards. It helps in achieving

optimum cost level which improves profitability and increases competitiveness. Company

produces a product according to standard operating methods deployed such as budgetary

controls, detailed standard costs, etc. Budgetary control is a tool of management accounting

practice wherein with the use of multiple budgets, managers perform planning and controlling

functions. Budgets plans are formulated for a given period of time in numerical terms. It serves

as a base for controlling and monitoring where in standards are compared with actual results to

ascertain deviations and implement corrective actions. It helps in maximum utilisation of

resources. Other than budgets, standard costing is another prominent tool used for cost control. It

establishes target costs to be achieved under given working conditions. These standard cost are

then compared with actual cost to measure and analyse variances. This helps in fixing

responsibility for non-standard performance and focus attention on areas which require cost

improvement. It can also help management in fixing selling price and performance based

incentives for employees.

Other than cost control, profit maximisation is the way to increase shareholders' value.

Management accountants performs various operations to identify those ways in which business

can improve its revenue (Cooper, 2017). Managers use various managerial reports, performance

metrics, revenue projections, budgets, cash forecasts, etc. to make informed decisions. These

informations also help management in taking other important strategic decisions such as new

projects, capital investments, change in marketing policy, change in revenue projections, etc. For

this, managers use various accounting techniques such as ratios, key performance indicators,

Management Information Systems, financial modelling, etc. Data-backed financial reporting and

control ensures that management is making accurate decisions to maximise future returns and

minimise uncertainty and risk.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4. Fraud detection and ethical decision making

Intentional deception or concealment of truth to gain unfair personal advantage or

unauthorised benefits. For example, misappropriation of company's funds, supplies or assets by

an employee or a group of employees, insider trading, leaking confidential information of

company to competitors, etc.. It is risk that threatens all types and sizes of firms (Dong, Liao and

Zhang, 2018). An early detection of actual or expected fraud is called fraud detection. Fraud

detection technique can be either proactive or reactive and also, either manual or automated. To

effectively manage fraud risk, a proper corporate governance structure shall be in place. There

shall be effective policies and procedures for fraud assessment, prevention, detection and

investigation. Multiple parties play role in fraud risk management such as board of directors and

management, internal audit committee, external independent auditor, etc. Management these

days use artificial intelligence to design their fraud detection programs. Fraud Analytics is

combination of technology and human interactions for early detections of fraudulent

transactions. Techniques such as sampling, ad-hoc, continuous analysis, etc. are used for

analysis. Companies also use methods like social network analysis, social customer relationship

management, etc. for data analytics.

Ethical decision-making refers to the process of applying ethics such as justice, virtue,

common good, etc. while evaluating and choosing among various alternatives present for

decision-making. It is far more than doing the right thing (Bagozzi, Sekerka and Sguera, 2018).

It is using ethical means to achieve just end. It is taking decisions according to legal policies and

procedures. There are various approaches to ethical decision-making such as utilitarian approach,

rights approach, fairness approach, common good approach, virtue approach, etc. Utilitarian

approach tries to produce the greatest good to the maximum people. It believes in ethical end

with no regard to nature of means. Rights approach intends to treat people fairly and respect

dignity and rights of everyone. Fairness approach asks to treat everyone with equally irrespective

of their position in organisation. Approach of common good says that leaders should protect the

well-being of their team. It encourages compassion for fellow team in leaders. Virtue approach

asks leaders to take decisions on the basis of universally ethical values such as honesty, courage,

sympathy, patience, justice, fairness, etc. Ethical decisions generate and sustain trust for

company and helps company increase its goodwill.

7

Intentional deception or concealment of truth to gain unfair personal advantage or

unauthorised benefits. For example, misappropriation of company's funds, supplies or assets by

an employee or a group of employees, insider trading, leaking confidential information of

company to competitors, etc.. It is risk that threatens all types and sizes of firms (Dong, Liao and

Zhang, 2018). An early detection of actual or expected fraud is called fraud detection. Fraud

detection technique can be either proactive or reactive and also, either manual or automated. To

effectively manage fraud risk, a proper corporate governance structure shall be in place. There

shall be effective policies and procedures for fraud assessment, prevention, detection and

investigation. Multiple parties play role in fraud risk management such as board of directors and

management, internal audit committee, external independent auditor, etc. Management these

days use artificial intelligence to design their fraud detection programs. Fraud Analytics is

combination of technology and human interactions for early detections of fraudulent

transactions. Techniques such as sampling, ad-hoc, continuous analysis, etc. are used for

analysis. Companies also use methods like social network analysis, social customer relationship

management, etc. for data analytics.

Ethical decision-making refers to the process of applying ethics such as justice, virtue,

common good, etc. while evaluating and choosing among various alternatives present for

decision-making. It is far more than doing the right thing (Bagozzi, Sekerka and Sguera, 2018).

It is using ethical means to achieve just end. It is taking decisions according to legal policies and

procedures. There are various approaches to ethical decision-making such as utilitarian approach,

rights approach, fairness approach, common good approach, virtue approach, etc. Utilitarian

approach tries to produce the greatest good to the maximum people. It believes in ethical end

with no regard to nature of means. Rights approach intends to treat people fairly and respect

dignity and rights of everyone. Fairness approach asks to treat everyone with equally irrespective

of their position in organisation. Approach of common good says that leaders should protect the

well-being of their team. It encourages compassion for fellow team in leaders. Virtue approach

asks leaders to take decisions on the basis of universally ethical values such as honesty, courage,

sympathy, patience, justice, fairness, etc. Ethical decisions generate and sustain trust for

company and helps company increase its goodwill.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Reflection

From the above report, I understood that effective decision-making plays a significant

role in success of an organisation. Quality of decision making is must in a good manager (Tseng,

Chiu and Liang, 2018). There are various factors that influence the decisions of managers. Those

factors could be external to organisation such as industry, market and environment or internal

such as business size, products or personal beliefs of management. Managers follow different

approaches to take decisions. Some managers believe in one-manship while others follows

participative and democratic style of decision-making. No manager follow single approach all

the time and changes as per the need of situation. They use various techniques such as marginal

cost analysis, cost benefit analysis, operations research, linear programming, etc. to reach

decisions that can form the basis of financial decision-making. A business has many stakeholders

and their varied interest out of the business often results in conflicts. These conflicts arises

several issues in making informed business decisions. Managers then identify various

stakeholders and their level of interest and influence. They have to be prioritised as per the

influence they can wield on company. Accordingly managers enter into discussion with them and

then decide on final strategies.

Basic objective of management is to maximise business profit. For it, either they can

increase revenue from present sources such as by increasing sales of existing products in same

market or by creating new revenue sources such as introducing existing products in new markets

or introducing altogether new product. They use various performance metrics and forecasts to

identify sources that can help increase revenue (Jiao and et.al., 2018.). Other than increasing

revenue, company can control cost to increase profit. Managers undertake various techniques

such as multiple budgets, standard costing, etc. to assess variances in targeted costs and actual

costs. Cost control also helps in maximum utilisation of resources as well. Many-a-times, it is

seen that people intentionally deceive company for their personal benefits. Such fraudulent

practises are not only illegal but also unethical. That's why companies shall have effective

corporate governance plan to mitigate fraud risk. Ethical decision making by management helps

in eliminating such frauds and improve business sustainability.

8

From the above report, I understood that effective decision-making plays a significant

role in success of an organisation. Quality of decision making is must in a good manager (Tseng,

Chiu and Liang, 2018). There are various factors that influence the decisions of managers. Those

factors could be external to organisation such as industry, market and environment or internal

such as business size, products or personal beliefs of management. Managers follow different

approaches to take decisions. Some managers believe in one-manship while others follows

participative and democratic style of decision-making. No manager follow single approach all

the time and changes as per the need of situation. They use various techniques such as marginal

cost analysis, cost benefit analysis, operations research, linear programming, etc. to reach

decisions that can form the basis of financial decision-making. A business has many stakeholders

and their varied interest out of the business often results in conflicts. These conflicts arises

several issues in making informed business decisions. Managers then identify various

stakeholders and their level of interest and influence. They have to be prioritised as per the

influence they can wield on company. Accordingly managers enter into discussion with them and

then decide on final strategies.

Basic objective of management is to maximise business profit. For it, either they can

increase revenue from present sources such as by increasing sales of existing products in same

market or by creating new revenue sources such as introducing existing products in new markets

or introducing altogether new product. They use various performance metrics and forecasts to

identify sources that can help increase revenue (Jiao and et.al., 2018.). Other than increasing

revenue, company can control cost to increase profit. Managers undertake various techniques

such as multiple budgets, standard costing, etc. to assess variances in targeted costs and actual

costs. Cost control also helps in maximum utilisation of resources as well. Many-a-times, it is

seen that people intentionally deceive company for their personal benefits. Such fraudulent

practises are not only illegal but also unethical. That's why companies shall have effective

corporate governance plan to mitigate fraud risk. Ethical decision making by management helps

in eliminating such frauds and improve business sustainability.

8

Task 2

1. Ratio Analysis

In this segment, it is understood that ratio analysis is performed to measure and interpret

results obtained from financial statements and it is further used to provide assistance to managers

in drawing appropriate strategies for future (Abor, 2017). Following is further explanation of

various ratios and how they are practically implemented by taking example of real company i.e.

Lookers plc.

Profitability ratios: It is that category of financial metrics that are used by managers to analyse

a business ability to engender earnings in comparison with operating costs, assets or

shareholder's equity within a specific period of time. Under this class of ratios, following

calculations are made:

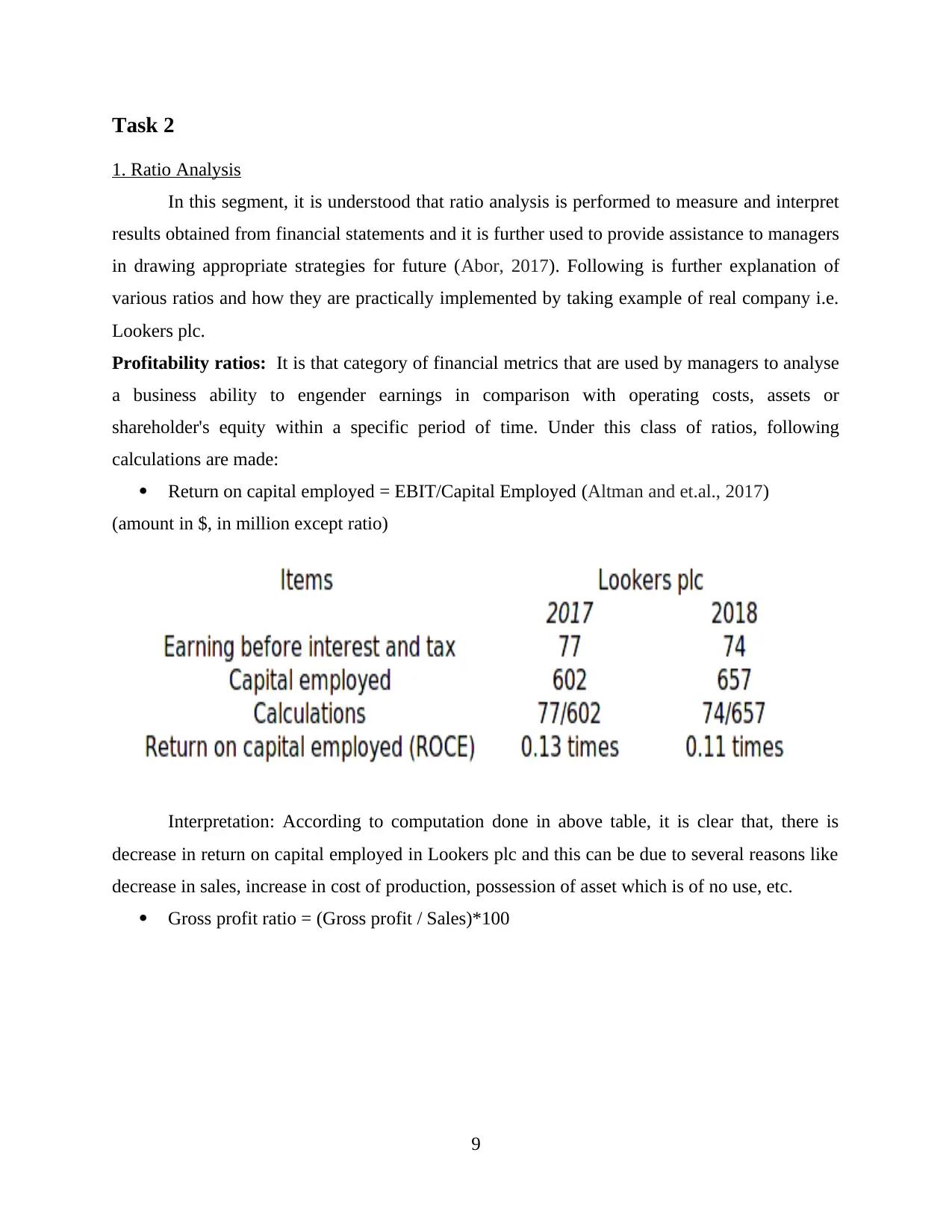

Return on capital employed = EBIT/Capital Employed (Altman and et.al., 2017)

(amount in $, in million except ratio)

Interpretation: According to computation done in above table, it is clear that, there is

decrease in return on capital employed in Lookers plc and this can be due to several reasons like

decrease in sales, increase in cost of production, possession of asset which is of no use, etc.

Gross profit ratio = (Gross profit / Sales)*100

9

1. Ratio Analysis

In this segment, it is understood that ratio analysis is performed to measure and interpret

results obtained from financial statements and it is further used to provide assistance to managers

in drawing appropriate strategies for future (Abor, 2017). Following is further explanation of

various ratios and how they are practically implemented by taking example of real company i.e.

Lookers plc.

Profitability ratios: It is that category of financial metrics that are used by managers to analyse

a business ability to engender earnings in comparison with operating costs, assets or

shareholder's equity within a specific period of time. Under this class of ratios, following

calculations are made:

Return on capital employed = EBIT/Capital Employed (Altman and et.al., 2017)

(amount in $, in million except ratio)

Interpretation: According to computation done in above table, it is clear that, there is

decrease in return on capital employed in Lookers plc and this can be due to several reasons like

decrease in sales, increase in cost of production, possession of asset which is of no use, etc.

Gross profit ratio = (Gross profit / Sales)*100

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

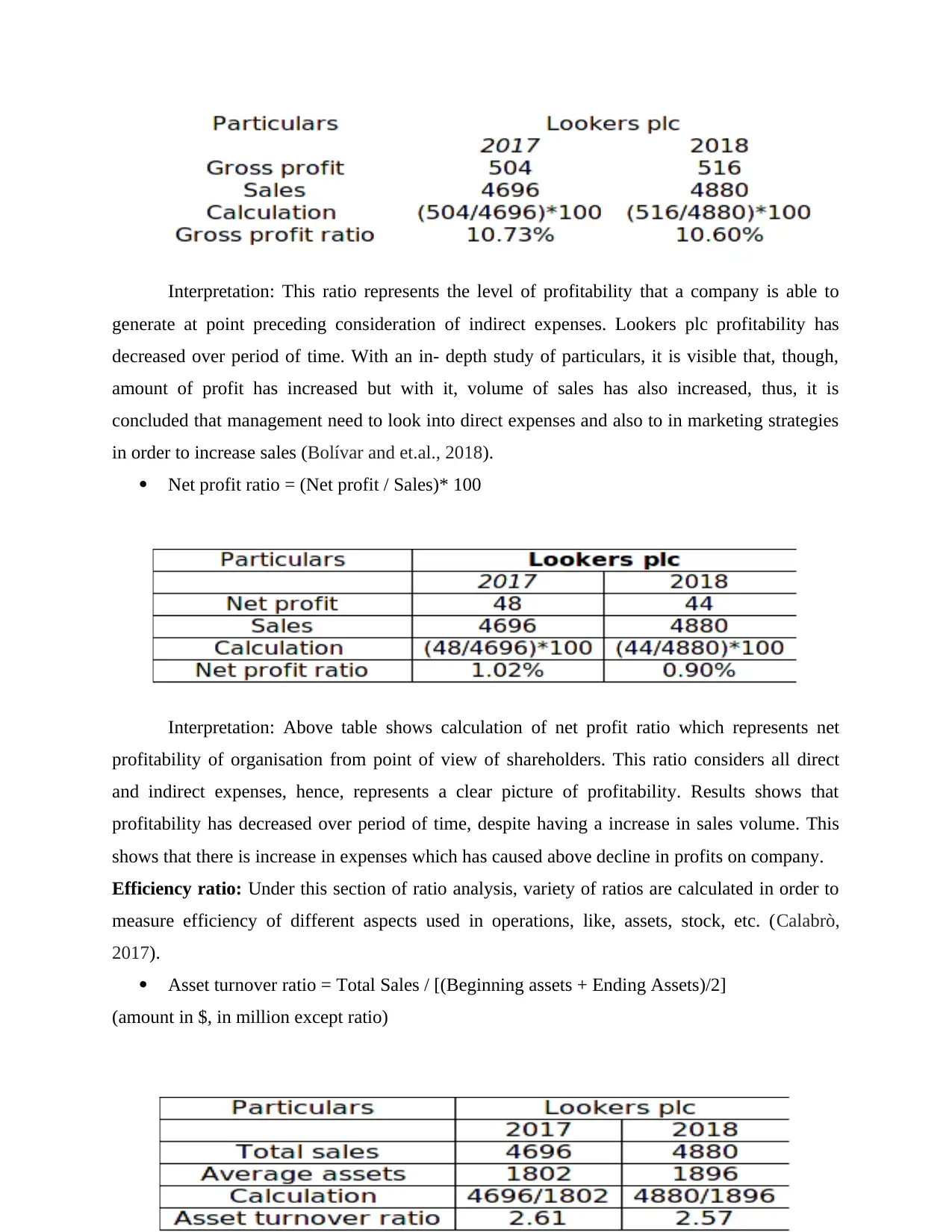

Interpretation: This ratio represents the level of profitability that a company is able to

generate at point preceding consideration of indirect expenses. Lookers plc profitability has

decreased over period of time. With an in- depth study of particulars, it is visible that, though,

amount of profit has increased but with it, volume of sales has also increased, thus, it is

concluded that management need to look into direct expenses and also to in marketing strategies

in order to increase sales (Bolívar and et.al., 2018).

Net profit ratio = (Net profit / Sales)* 100

Interpretation: Above table shows calculation of net profit ratio which represents net

profitability of organisation from point of view of shareholders. This ratio considers all direct

and indirect expenses, hence, represents a clear picture of profitability. Results shows that

profitability has decreased over period of time, despite having a increase in sales volume. This

shows that there is increase in expenses which has caused above decline in profits on company.

Efficiency ratio: Under this section of ratio analysis, variety of ratios are calculated in order to

measure efficiency of different aspects used in operations, like, assets, stock, etc. (Calabrò,

2017).

Asset turnover ratio = Total Sales / [(Beginning assets + Ending Assets)/2]

(amount in $, in million except ratio)

10

generate at point preceding consideration of indirect expenses. Lookers plc profitability has

decreased over period of time. With an in- depth study of particulars, it is visible that, though,

amount of profit has increased but with it, volume of sales has also increased, thus, it is

concluded that management need to look into direct expenses and also to in marketing strategies

in order to increase sales (Bolívar and et.al., 2018).

Net profit ratio = (Net profit / Sales)* 100

Interpretation: Above table shows calculation of net profit ratio which represents net

profitability of organisation from point of view of shareholders. This ratio considers all direct

and indirect expenses, hence, represents a clear picture of profitability. Results shows that

profitability has decreased over period of time, despite having a increase in sales volume. This

shows that there is increase in expenses which has caused above decline in profits on company.

Efficiency ratio: Under this section of ratio analysis, variety of ratios are calculated in order to

measure efficiency of different aspects used in operations, like, assets, stock, etc. (Calabrò,

2017).

Asset turnover ratio = Total Sales / [(Beginning assets + Ending Assets)/2]

(amount in $, in million except ratio)

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

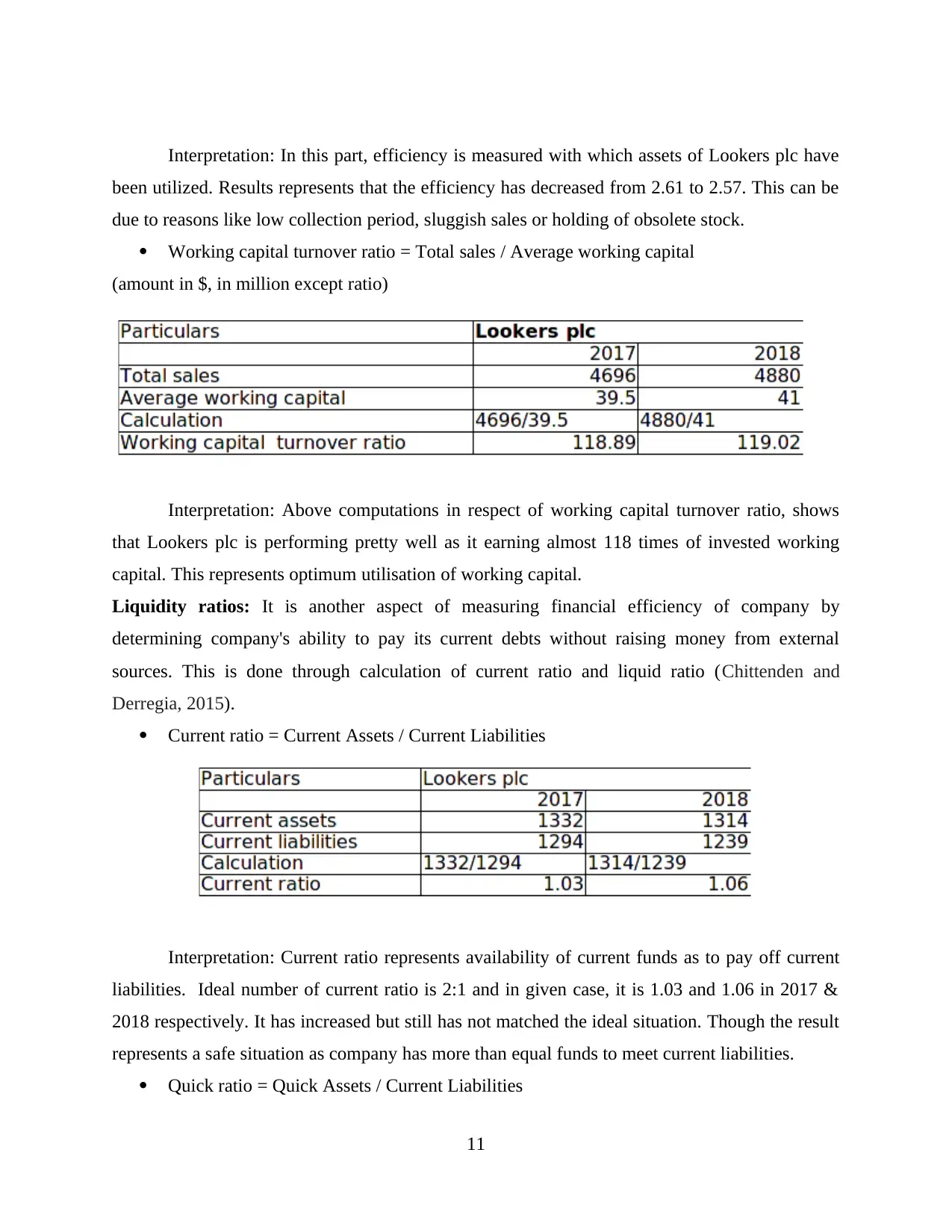

Interpretation: In this part, efficiency is measured with which assets of Lookers plc have

been utilized. Results represents that the efficiency has decreased from 2.61 to 2.57. This can be

due to reasons like low collection period, sluggish sales or holding of obsolete stock.

Working capital turnover ratio = Total sales / Average working capital

(amount in $, in million except ratio)

Interpretation: Above computations in respect of working capital turnover ratio, shows

that Lookers plc is performing pretty well as it earning almost 118 times of invested working

capital. This represents optimum utilisation of working capital.

Liquidity ratios: It is another aspect of measuring financial efficiency of company by

determining company's ability to pay its current debts without raising money from external

sources. This is done through calculation of current ratio and liquid ratio (Chittenden and

Derregia, 2015).

Current ratio = Current Assets / Current Liabilities

Interpretation: Current ratio represents availability of current funds as to pay off current

liabilities. Ideal number of current ratio is 2:1 and in given case, it is 1.03 and 1.06 in 2017 &

2018 respectively. It has increased but still has not matched the ideal situation. Though the result

represents a safe situation as company has more than equal funds to meet current liabilities.

Quick ratio = Quick Assets / Current Liabilities

11

been utilized. Results represents that the efficiency has decreased from 2.61 to 2.57. This can be

due to reasons like low collection period, sluggish sales or holding of obsolete stock.

Working capital turnover ratio = Total sales / Average working capital

(amount in $, in million except ratio)

Interpretation: Above computations in respect of working capital turnover ratio, shows

that Lookers plc is performing pretty well as it earning almost 118 times of invested working

capital. This represents optimum utilisation of working capital.

Liquidity ratios: It is another aspect of measuring financial efficiency of company by

determining company's ability to pay its current debts without raising money from external

sources. This is done through calculation of current ratio and liquid ratio (Chittenden and

Derregia, 2015).

Current ratio = Current Assets / Current Liabilities

Interpretation: Current ratio represents availability of current funds as to pay off current

liabilities. Ideal number of current ratio is 2:1 and in given case, it is 1.03 and 1.06 in 2017 &

2018 respectively. It has increased but still has not matched the ideal situation. Though the result

represents a safe situation as company has more than equal funds to meet current liabilities.

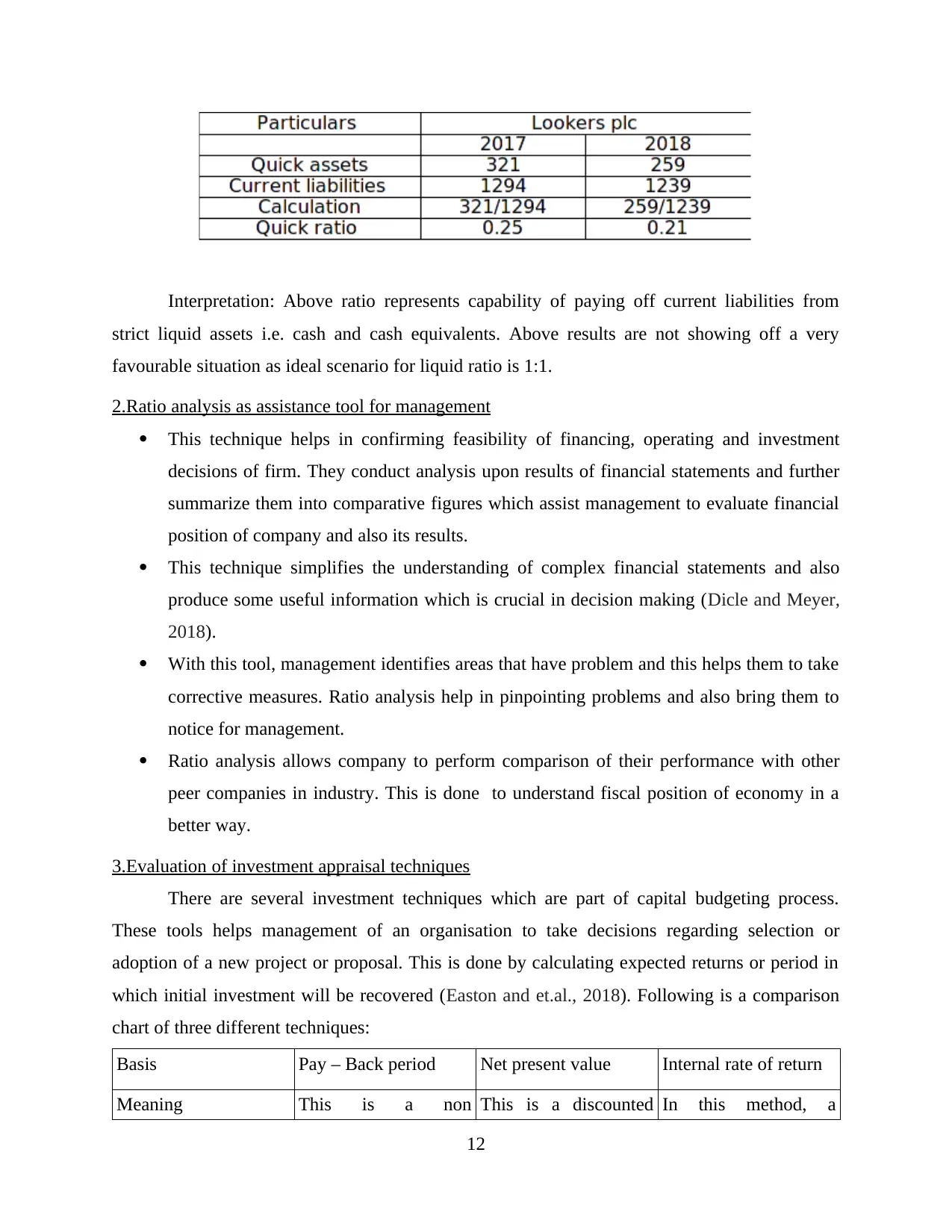

Quick ratio = Quick Assets / Current Liabilities

11

Interpretation: Above ratio represents capability of paying off current liabilities from

strict liquid assets i.e. cash and cash equivalents. Above results are not showing off a very

favourable situation as ideal scenario for liquid ratio is 1:1.

2.Ratio analysis as assistance tool for management

This technique helps in confirming feasibility of financing, operating and investment

decisions of firm. They conduct analysis upon results of financial statements and further

summarize them into comparative figures which assist management to evaluate financial

position of company and also its results.

This technique simplifies the understanding of complex financial statements and also

produce some useful information which is crucial in decision making (Dicle and Meyer,

2018).

With this tool, management identifies areas that have problem and this helps them to take

corrective measures. Ratio analysis help in pinpointing problems and also bring them to

notice for management.

Ratio analysis allows company to perform comparison of their performance with other

peer companies in industry. This is done to understand fiscal position of economy in a

better way.

3.Evaluation of investment appraisal techniques

There are several investment techniques which are part of capital budgeting process.

These tools helps management of an organisation to take decisions regarding selection or

adoption of a new project or proposal. This is done by calculating expected returns or period in

which initial investment will be recovered (Easton and et.al., 2018). Following is a comparison

chart of three different techniques:

Basis Pay – Back period Net present value Internal rate of return

Meaning This is a non This is a discounted In this method, a

12

strict liquid assets i.e. cash and cash equivalents. Above results are not showing off a very

favourable situation as ideal scenario for liquid ratio is 1:1.

2.Ratio analysis as assistance tool for management

This technique helps in confirming feasibility of financing, operating and investment

decisions of firm. They conduct analysis upon results of financial statements and further

summarize them into comparative figures which assist management to evaluate financial

position of company and also its results.

This technique simplifies the understanding of complex financial statements and also

produce some useful information which is crucial in decision making (Dicle and Meyer,

2018).

With this tool, management identifies areas that have problem and this helps them to take

corrective measures. Ratio analysis help in pinpointing problems and also bring them to

notice for management.

Ratio analysis allows company to perform comparison of their performance with other

peer companies in industry. This is done to understand fiscal position of economy in a

better way.

3.Evaluation of investment appraisal techniques

There are several investment techniques which are part of capital budgeting process.

These tools helps management of an organisation to take decisions regarding selection or

adoption of a new project or proposal. This is done by calculating expected returns or period in

which initial investment will be recovered (Easton and et.al., 2018). Following is a comparison

chart of three different techniques:

Basis Pay – Back period Net present value Internal rate of return

Meaning This is a non This is a discounted In this method, a

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.