Principles and Practice of Management Accounting Report - Unit 5

VerifiedAdded on 2023/01/17

|24

|4963

|35

Report

AI Summary

This report analyzes management accounting principles, focusing on the case study of Alpha Ltd, a medium-sized pizza company. It explores different management accounting systems, including job costing, cost accounting, inventory management, and price optimization. The report delves into various management accounting reporting methods such as budget reports, performance reports, sales reports, and job cost reports. It also examines the application and benefits of these systems. Furthermore, the report compares and contrasts marginal and absorption costing techniques, providing income statements and reconciliation statements for each. It also investigates budgetary planning tools and their advantages and disadvantages. Finally, it compares how management accounting is used by organizations to respond to financial statements, providing a comprehensive understanding of the subject.

PRINCIPLES AND PRACTICE

OF MANAGEMENT

ACCOUNTING

OF MANAGEMENT

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Management accounting and requirement of different types of management accounting

systems.........................................................................................................................................1

P2 Different methods used for management accounting reporting.............................................1

Benefits and application of management accounting system......................................................2

LO2..................................................................................................................................................2

P3 Calculating costs under different management accounting techniques..................................2

LO3..................................................................................................................................................7

P4 Advantages and disadvantages of different types of budgetary planning tools......................7

LO4................................................................................................................................................10

P5 Comparing how management accounting is used by organisations for responding to

financial statements. ..................................................................................................................10

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Management accounting and requirement of different types of management accounting

systems.........................................................................................................................................1

P2 Different methods used for management accounting reporting.............................................1

Benefits and application of management accounting system......................................................2

LO2..................................................................................................................................................2

P3 Calculating costs under different management accounting techniques..................................2

LO3..................................................................................................................................................7

P4 Advantages and disadvantages of different types of budgetary planning tools......................7

LO4................................................................................................................................................10

P5 Comparing how management accounting is used by organisations for responding to

financial statements. ..................................................................................................................10

CONCLUSION .............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting implies for the presentation of accounting information which in

turn aid in the formulation of management policies that associated with daily activities. In the

context of business unit, management accounting is highly significant as it helps facilitates

planning, co-ordination and financial control to a great extent. By employing this firm can do

effectual evaluation of efficiency and effectiveness of different policies. Along with this, with

the help of management team can do proper forecast about future and thereby would become

able to make optimum use of monetary resources. This report is based on the case scenario of

medium sized organization namely Alpha Ltd which in turn involved in offering pizza to all age

groups. In this, report will furnish information about the essential requirements of varied

management accounting systems that available to the firm. Besides this, it will also shed light on

the extent to which reports aid in managerial decision making.

Report will also develop understanding about the concept of costing methods in relation

to absorption and marginal. Further, report also entails how effectual planning can be done in

monetary terms by referring management accounting tools. It will also provide deeper insight

about the techniques which assist in addressing financial problems prominently. The present

report will be providing the understanding about the requirements of different type of

management accounting systems. It will be providing information about the different methods

that are use in management accounting and reporting. It will also provide for different techniques

under which income statements are prepared by the organisation. Report will also provide for

the tools that are used in management accounting. It will be giving detailed understanding about

the management accounting.

LO1

P1 Management accounting and requirement of different types of management accounting

systems.

Management accounting places emphasis on analysing and evaluating business

transactions which in turn contributes in business decision making. There are several tools which

can be employed by Alpha Ltd for ensuring smooth functioning of the business operations and

functions. Management accounting refers to the process of making management accounts and

reports for providing timely and accurately financial as well as statistical information’s to

managers for making decisions for the business. The accounting is used by organisations to

1

Management accounting implies for the presentation of accounting information which in

turn aid in the formulation of management policies that associated with daily activities. In the

context of business unit, management accounting is highly significant as it helps facilitates

planning, co-ordination and financial control to a great extent. By employing this firm can do

effectual evaluation of efficiency and effectiveness of different policies. Along with this, with

the help of management team can do proper forecast about future and thereby would become

able to make optimum use of monetary resources. This report is based on the case scenario of

medium sized organization namely Alpha Ltd which in turn involved in offering pizza to all age

groups. In this, report will furnish information about the essential requirements of varied

management accounting systems that available to the firm. Besides this, it will also shed light on

the extent to which reports aid in managerial decision making.

Report will also develop understanding about the concept of costing methods in relation

to absorption and marginal. Further, report also entails how effectual planning can be done in

monetary terms by referring management accounting tools. It will also provide deeper insight

about the techniques which assist in addressing financial problems prominently. The present

report will be providing the understanding about the requirements of different type of

management accounting systems. It will be providing information about the different methods

that are use in management accounting and reporting. It will also provide for different techniques

under which income statements are prepared by the organisation. Report will also provide for

the tools that are used in management accounting. It will be giving detailed understanding about

the management accounting.

LO1

P1 Management accounting and requirement of different types of management accounting

systems.

Management accounting places emphasis on analysing and evaluating business

transactions which in turn contributes in business decision making. There are several tools which

can be employed by Alpha Ltd for ensuring smooth functioning of the business operations and

functions. Management accounting refers to the process of making management accounts and

reports for providing timely and accurately financial as well as statistical information’s to

managers for making decisions for the business. The accounting is used by organisations to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

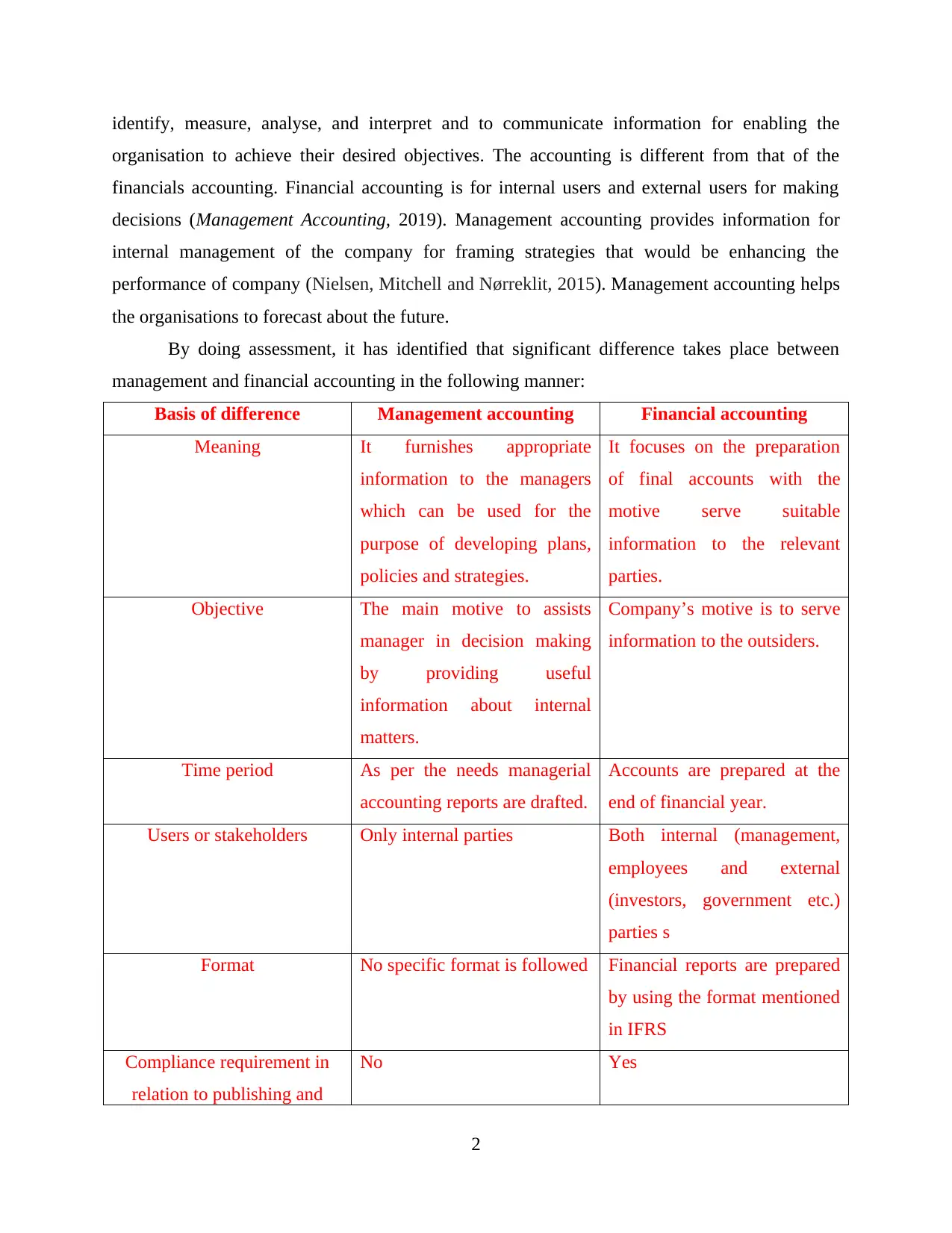

identify, measure, analyse, and interpret and to communicate information for enabling the

organisation to achieve their desired objectives. The accounting is different from that of the

financials accounting. Financial accounting is for internal users and external users for making

decisions (Management Accounting, 2019). Management accounting provides information for

internal management of the company for framing strategies that would be enhancing the

performance of company (Nielsen, Mitchell and Nørreklit, 2015). Management accounting helps

the organisations to forecast about the future.

By doing assessment, it has identified that significant difference takes place between

management and financial accounting in the following manner:

Basis of difference Management accounting Financial accounting

Meaning It furnishes appropriate

information to the managers

which can be used for the

purpose of developing plans,

policies and strategies.

It focuses on the preparation

of final accounts with the

motive serve suitable

information to the relevant

parties.

Objective The main motive to assists

manager in decision making

by providing useful

information about internal

matters.

Company’s motive is to serve

information to the outsiders.

Time period As per the needs managerial

accounting reports are drafted.

Accounts are prepared at the

end of financial year.

Users or stakeholders Only internal parties Both internal (management,

employees and external

(investors, government etc.)

parties s

Format No specific format is followed Financial reports are prepared

by using the format mentioned

in IFRS

Compliance requirement in

relation to publishing and

No Yes

2

organisation to achieve their desired objectives. The accounting is different from that of the

financials accounting. Financial accounting is for internal users and external users for making

decisions (Management Accounting, 2019). Management accounting provides information for

internal management of the company for framing strategies that would be enhancing the

performance of company (Nielsen, Mitchell and Nørreklit, 2015). Management accounting helps

the organisations to forecast about the future.

By doing assessment, it has identified that significant difference takes place between

management and financial accounting in the following manner:

Basis of difference Management accounting Financial accounting

Meaning It furnishes appropriate

information to the managers

which can be used for the

purpose of developing plans,

policies and strategies.

It focuses on the preparation

of final accounts with the

motive serve suitable

information to the relevant

parties.

Objective The main motive to assists

manager in decision making

by providing useful

information about internal

matters.

Company’s motive is to serve

information to the outsiders.

Time period As per the needs managerial

accounting reports are drafted.

Accounts are prepared at the

end of financial year.

Users or stakeholders Only internal parties Both internal (management,

employees and external

(investors, government etc.)

parties s

Format No specific format is followed Financial reports are prepared

by using the format mentioned

in IFRS

Compliance requirement in

relation to publishing and

No Yes

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

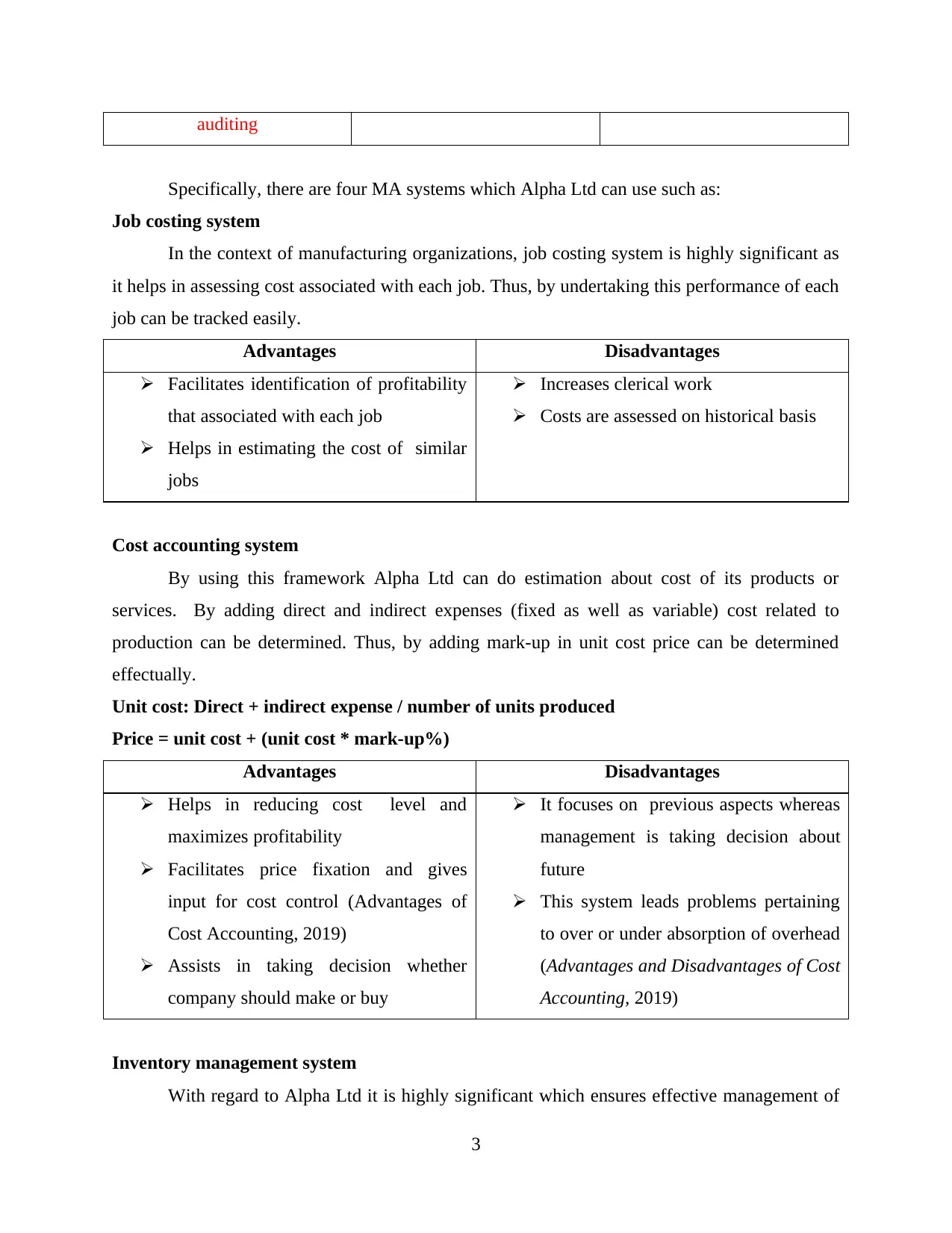

auditing

Specifically, there are four MA systems which Alpha Ltd can use such as:

Job costing system

In the context of manufacturing organizations, job costing system is highly significant as

it helps in assessing cost associated with each job. Thus, by undertaking this performance of each

job can be tracked easily.

Advantages Disadvantages

Facilitates identification of profitability

that associated with each job

Helps in estimating the cost of similar

jobs

Increases clerical work

Costs are assessed on historical basis

Cost accounting system

By using this framework Alpha Ltd can do estimation about cost of its products or

services. By adding direct and indirect expenses (fixed as well as variable) cost related to

production can be determined. Thus, by adding mark-up in unit cost price can be determined

effectually.

Unit cost: Direct + indirect expense / number of units produced

Price = unit cost + (unit cost * mark-up%)

Advantages Disadvantages

Helps in reducing cost level and

maximizes profitability

Facilitates price fixation and gives

input for cost control (Advantages of

Cost Accounting, 2019)

Assists in taking decision whether

company should make or buy

It focuses on previous aspects whereas

management is taking decision about

future

This system leads problems pertaining

to over or under absorption of overhead

(Advantages and Disadvantages of Cost

Accounting, 2019)

Inventory management system

With regard to Alpha Ltd it is highly significant which ensures effective management of

3

Specifically, there are four MA systems which Alpha Ltd can use such as:

Job costing system

In the context of manufacturing organizations, job costing system is highly significant as

it helps in assessing cost associated with each job. Thus, by undertaking this performance of each

job can be tracked easily.

Advantages Disadvantages

Facilitates identification of profitability

that associated with each job

Helps in estimating the cost of similar

jobs

Increases clerical work

Costs are assessed on historical basis

Cost accounting system

By using this framework Alpha Ltd can do estimation about cost of its products or

services. By adding direct and indirect expenses (fixed as well as variable) cost related to

production can be determined. Thus, by adding mark-up in unit cost price can be determined

effectually.

Unit cost: Direct + indirect expense / number of units produced

Price = unit cost + (unit cost * mark-up%)

Advantages Disadvantages

Helps in reducing cost level and

maximizes profitability

Facilitates price fixation and gives

input for cost control (Advantages of

Cost Accounting, 2019)

Assists in taking decision whether

company should make or buy

It focuses on previous aspects whereas

management is taking decision about

future

This system leads problems pertaining

to over or under absorption of overhead

(Advantages and Disadvantages of Cost

Accounting, 2019)

Inventory management system

With regard to Alpha Ltd it is highly significant which ensures effective management of

3

raw material and finished product. Hence, by undertaking EOQ, JIT system etc firm can

determine the level to which inventory need to be maintained within an organization. Along with

this, by taking into account LIFO, FIFO etc business unit ensure prominent management of stock

within an organization.

Advantages Disadvantages

Ensures uninterrupted production

activity within an organization

Facilitates savings in terms of time and

cost

Dependency on internet usage limits its

significance: System crash, malicious

hack

Reduction in the activity of physical

audit (Advantages & Disadvantages of

a Computerized Inventory Management

System, 2019)

Price optimization system

This software can be undertaken by the firm for assessing prices which will improve

profitability aspect in the near future. Moreover, it clearly shows prices that customers are ready

to pay for the company’s product’s or services. Thus, by setting suitable price company can

increase customer base and thereby profitability as well.

Advantages Disadvantages

Helps in taking appropriate pricing

decisions

Assists in building competitive edge

Time consuming exercise

High dependency on internet access

P2 Management accounting report methods

The different reporting method for accounting of management includes different types of

reports which are formulated for organization in order to manage the information relating to

company (Mata, Fialho and Eugénio, 2018). This reporting is very necessary because of the fact

that this records all the information in a systematic and clear manner which helps the manager in

taking effective decision. Thus, it is very necessary for Alpha Ltd to use these various kinds of

reporting system which are illustrated in connected points-

Report for budget- this is a type of managerial reporting under which the budget for the

4

determine the level to which inventory need to be maintained within an organization. Along with

this, by taking into account LIFO, FIFO etc business unit ensure prominent management of stock

within an organization.

Advantages Disadvantages

Ensures uninterrupted production

activity within an organization

Facilitates savings in terms of time and

cost

Dependency on internet usage limits its

significance: System crash, malicious

hack

Reduction in the activity of physical

audit (Advantages & Disadvantages of

a Computerized Inventory Management

System, 2019)

Price optimization system

This software can be undertaken by the firm for assessing prices which will improve

profitability aspect in the near future. Moreover, it clearly shows prices that customers are ready

to pay for the company’s product’s or services. Thus, by setting suitable price company can

increase customer base and thereby profitability as well.

Advantages Disadvantages

Helps in taking appropriate pricing

decisions

Assists in building competitive edge

Time consuming exercise

High dependency on internet access

P2 Management accounting report methods

The different reporting method for accounting of management includes different types of

reports which are formulated for organization in order to manage the information relating to

company (Mata, Fialho and Eugénio, 2018). This reporting is very necessary because of the fact

that this records all the information in a systematic and clear manner which helps the manager in

taking effective decision. Thus, it is very necessary for Alpha Ltd to use these various kinds of

reporting system which are illustrated in connected points-

Report for budget- this is a type of managerial reporting under which the budget for the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company is prepared. The budget is defined as the estimate of the income and expenses based on

the previous budgets. This is very helpful for the company in analysing the expenses which can

be incurred in future and for this the company take measures for solving this in advance. Also,

this will help the manager in analysing the areas where they can cut the cost and where to

improve the income sources.

Performance report- this is yet another type of performance report which can be

prepared in Alpha Ltd under which the performance of the employees is recorded. Current

discussion helps the manager in evaluting the performance of the employees as well as the

business. Thus, this helps the manager in deciding that who are better employees and how they

need to be retained within the company. Thus, assist business in analysing and making ways of

improvising working ability of the employees and the overall performance of the company.

Sales report- this is a kind of format which is prepared by Alpha Ltd under which all the

sales transactions are being recorded. This helps the management of the organization in

analysing the sources of revenues and how much revenue is calculated with this source. This is

necessary because this helps the manager in deciding that whether the sales revenue is enough

for the working of company are they have to invest in other sources as well.

Job cost report- this is a type of reporting under which all the expenses which are which

are incurred for a specific project are recorded. Also, the estimation of revenue is done from this

project in order to evaluate the profitability of the project (Commerford, Hatfield and Houston,

2018). This job costing report help the company in identifying and analysing the higher earning

areas of the business. This report is prepared with the motive of analysing the good project so

that time and money is not wasted on the projects which are of low profit margins.

Benefits and application of management accounting system

The management accounting is very beneficial for the company as this helps the

company in analysing and interpreting the financial information and then taking decision and

making policies and plans to manage the business. The management accounting system are

applied in business in order to record different transaction of business, plan and control and take

decisions and formulate different policies for the betterment of the company.

5

the previous budgets. This is very helpful for the company in analysing the expenses which can

be incurred in future and for this the company take measures for solving this in advance. Also,

this will help the manager in analysing the areas where they can cut the cost and where to

improve the income sources.

Performance report- this is yet another type of performance report which can be

prepared in Alpha Ltd under which the performance of the employees is recorded. Current

discussion helps the manager in evaluting the performance of the employees as well as the

business. Thus, this helps the manager in deciding that who are better employees and how they

need to be retained within the company. Thus, assist business in analysing and making ways of

improvising working ability of the employees and the overall performance of the company.

Sales report- this is a kind of format which is prepared by Alpha Ltd under which all the

sales transactions are being recorded. This helps the management of the organization in

analysing the sources of revenues and how much revenue is calculated with this source. This is

necessary because this helps the manager in deciding that whether the sales revenue is enough

for the working of company are they have to invest in other sources as well.

Job cost report- this is a type of reporting under which all the expenses which are which

are incurred for a specific project are recorded. Also, the estimation of revenue is done from this

project in order to evaluate the profitability of the project (Commerford, Hatfield and Houston,

2018). This job costing report help the company in identifying and analysing the higher earning

areas of the business. This report is prepared with the motive of analysing the good project so

that time and money is not wasted on the projects which are of low profit margins.

Benefits and application of management accounting system

The management accounting is very beneficial for the company as this helps the

company in analysing and interpreting the financial information and then taking decision and

making policies and plans to manage the business. The management accounting system are

applied in business in order to record different transaction of business, plan and control and take

decisions and formulate different policies for the betterment of the company.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

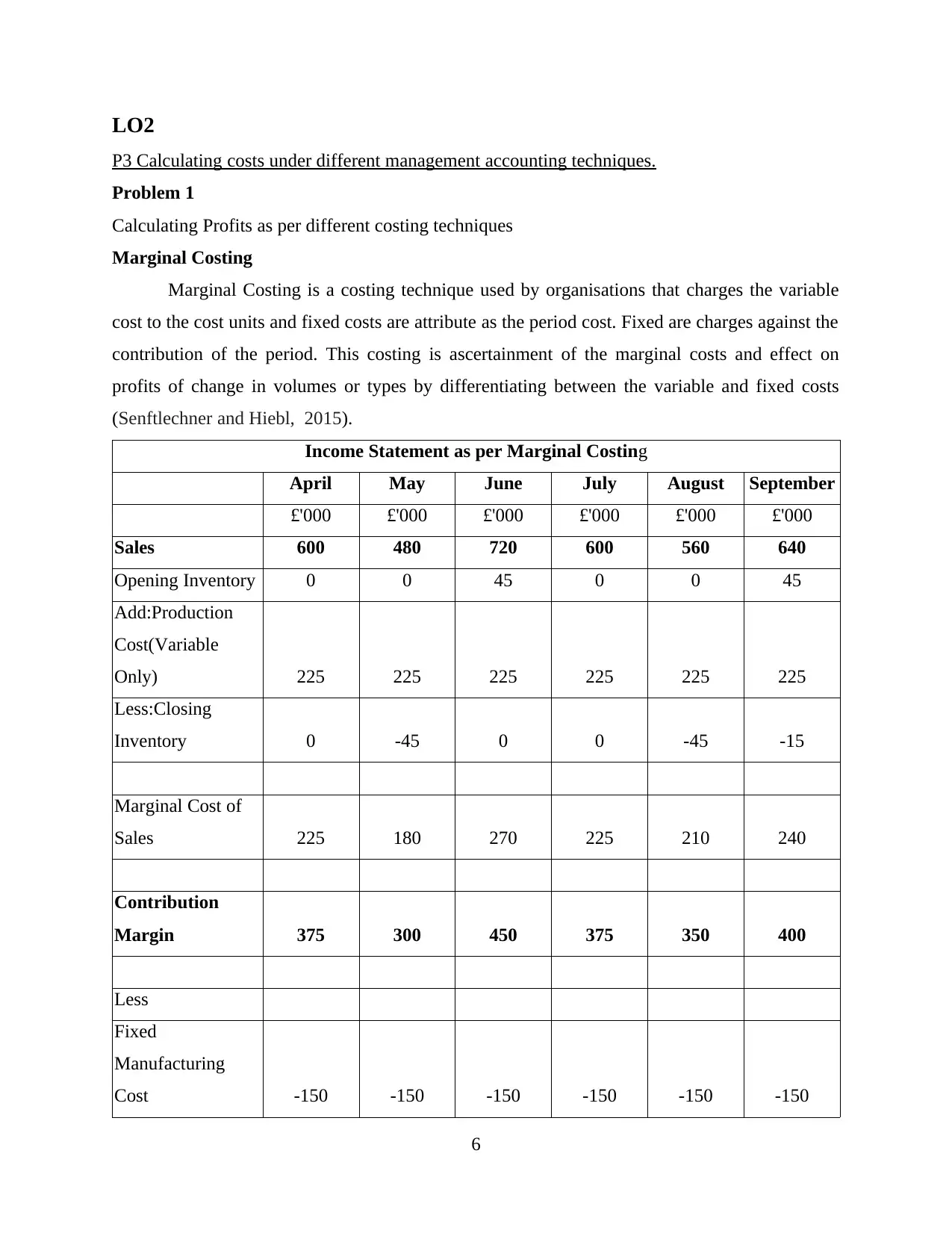

LO2

P3 Calculating costs under different management accounting techniques.

Problem 1

Calculating Profits as per different costing techniques

Marginal Costing

Marginal Costing is a costing technique used by organisations that charges the variable

cost to the cost units and fixed costs are attribute as the period cost. Fixed are charges against the

contribution of the period. This costing is ascertainment of the marginal costs and effect on

profits of change in volumes or types by differentiating between the variable and fixed costs

(Senftlechner and Hiebl, 2015).

Income Statement as per Marginal Costing

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Opening Inventory 0 0 45 0 0 45

Add:Production

Cost(Variable

Only) 225 225 225 225 225 225

Less:Closing

Inventory 0 -45 0 0 -45 -15

Marginal Cost of

Sales 225 180 270 225 210 240

Contribution

Margin 375 300 450 375 350 400

Less

Fixed

Manufacturing

Cost -150 -150 -150 -150 -150 -150

6

P3 Calculating costs under different management accounting techniques.

Problem 1

Calculating Profits as per different costing techniques

Marginal Costing

Marginal Costing is a costing technique used by organisations that charges the variable

cost to the cost units and fixed costs are attribute as the period cost. Fixed are charges against the

contribution of the period. This costing is ascertainment of the marginal costs and effect on

profits of change in volumes or types by differentiating between the variable and fixed costs

(Senftlechner and Hiebl, 2015).

Income Statement as per Marginal Costing

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Opening Inventory 0 0 45 0 0 45

Add:Production

Cost(Variable

Only) 225 225 225 225 225 225

Less:Closing

Inventory 0 -45 0 0 -45 -15

Marginal Cost of

Sales 225 180 270 225 210 240

Contribution

Margin 375 300 450 375 350 400

Less

Fixed

Manufacturing

Cost -150 -150 -150 -150 -150 -150

6

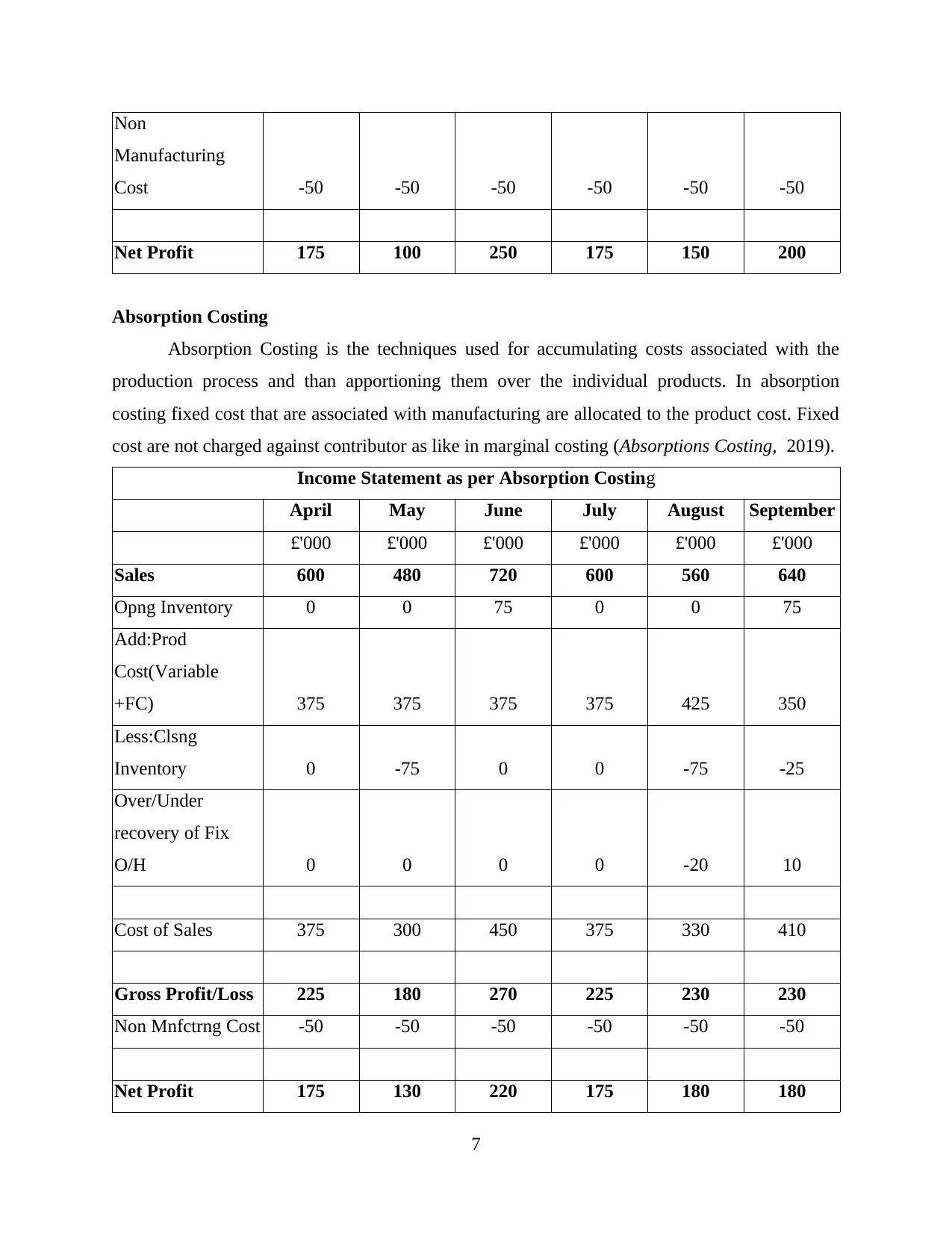

Non

Manufacturing

Cost -50 -50 -50 -50 -50 -50

Net Profit 175 100 250 175 150 200

Absorption Costing

Absorption Costing is the techniques used for accumulating costs associated with the

production process and than apportioning them over the individual products. In absorption

costing fixed cost that are associated with manufacturing are allocated to the product cost. Fixed

cost are not charged against contributor as like in marginal costing (Absorptions Costing, 2019).

Income Statement as per Absorption Costing

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Opng Inventory 0 0 75 0 0 75

Add:Prod

Cost(Variable

+FC) 375 375 375 375 425 350

Less:Clsng

Inventory 0 -75 0 0 -75 -25

Over/Under

recovery of Fix

O/H 0 0 0 0 -20 10

Cost of Sales 375 300 450 375 330 410

Gross Profit/Loss 225 180 270 225 230 230

Non Mnfctrng Cost -50 -50 -50 -50 -50 -50

Net Profit 175 130 220 175 180 180

7

Manufacturing

Cost -50 -50 -50 -50 -50 -50

Net Profit 175 100 250 175 150 200

Absorption Costing

Absorption Costing is the techniques used for accumulating costs associated with the

production process and than apportioning them over the individual products. In absorption

costing fixed cost that are associated with manufacturing are allocated to the product cost. Fixed

cost are not charged against contributor as like in marginal costing (Absorptions Costing, 2019).

Income Statement as per Absorption Costing

April May June July August September

£'000 £'000 £'000 £'000 £'000 £'000

Sales 600 480 720 600 560 640

Opng Inventory 0 0 75 0 0 75

Add:Prod

Cost(Variable

+FC) 375 375 375 375 425 350

Less:Clsng

Inventory 0 -75 0 0 -75 -25

Over/Under

recovery of Fix

O/H 0 0 0 0 -20 10

Cost of Sales 375 300 450 375 330 410

Gross Profit/Loss 225 180 270 225 230 230

Non Mnfctrng Cost -50 -50 -50 -50 -50 -50

Net Profit 175 130 220 175 180 180

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

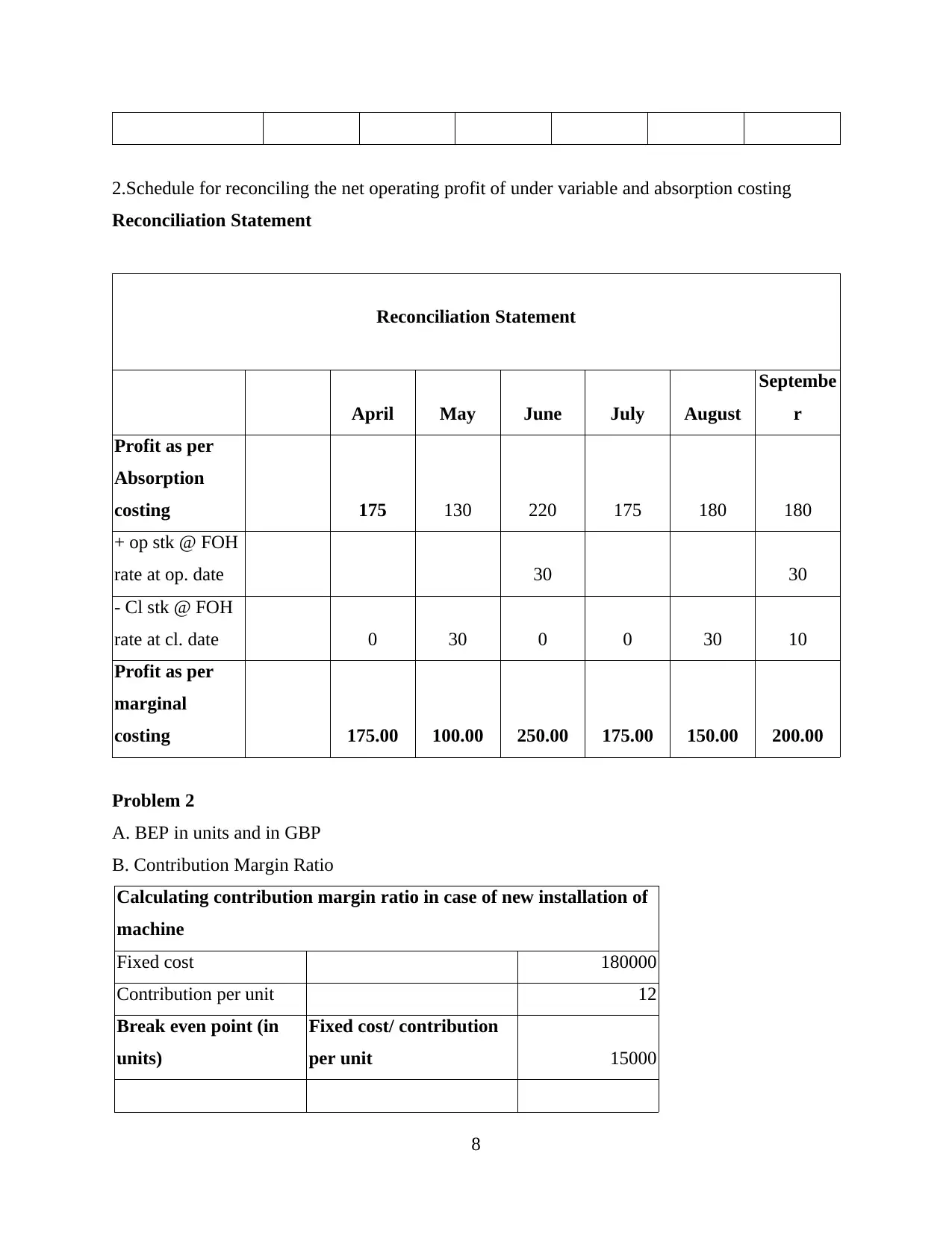

2.Schedule for reconciling the net operating profit of under variable and absorption costing

Reconciliation Statement

Reconciliation Statement

April May June July August

Septembe

r

Profit as per

Absorption

costing 175 130 220 175 180 180

+ op stk @ FOH

rate at op. date 30 30

- Cl stk @ FOH

rate at cl. date 0 30 0 0 30 10

Profit as per

marginal

costing 175.00 100.00 250.00 175.00 150.00 200.00

Problem 2

A. BEP in units and in GBP

B. Contribution Margin Ratio

Calculating contribution margin ratio in case of new installation of

machine

Fixed cost 180000

Contribution per unit 12

Break even point (in

units)

Fixed cost/ contribution

per unit 15000

8

Reconciliation Statement

Reconciliation Statement

April May June July August

Septembe

r

Profit as per

Absorption

costing 175 130 220 175 180 180

+ op stk @ FOH

rate at op. date 30 30

- Cl stk @ FOH

rate at cl. date 0 30 0 0 30 10

Profit as per

marginal

costing 175.00 100.00 250.00 175.00 150.00 200.00

Problem 2

A. BEP in units and in GBP

B. Contribution Margin Ratio

Calculating contribution margin ratio in case of new installation of

machine

Fixed cost 180000

Contribution per unit 12

Break even point (in

units)

Fixed cost/ contribution

per unit 15000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

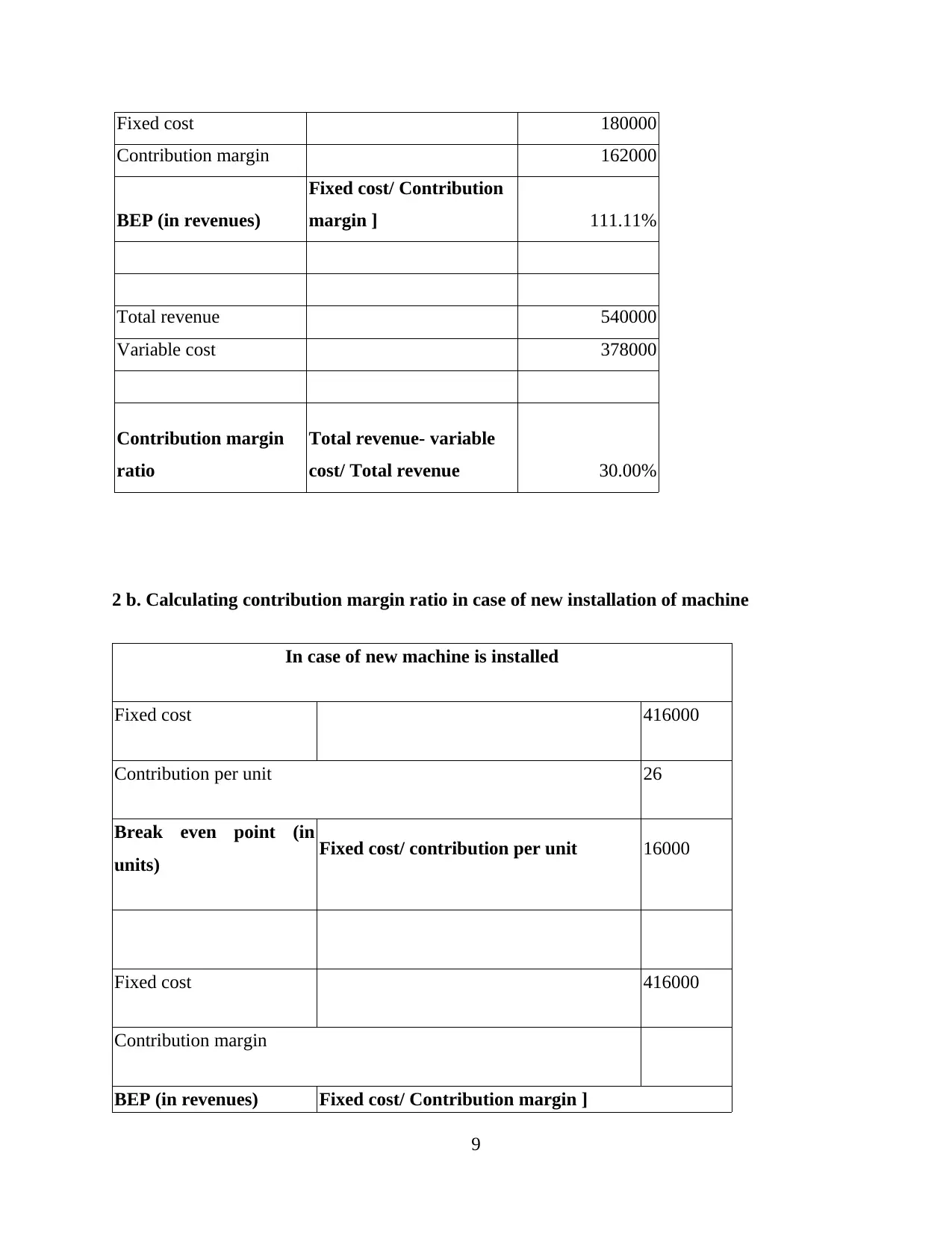

Fixed cost 180000

Contribution margin 162000

BEP (in revenues)

Fixed cost/ Contribution

margin ] 111.11%

Total revenue 540000

Variable cost 378000

Contribution margin

ratio

Total revenue- variable

cost/ Total revenue 30.00%

2 b. Calculating contribution margin ratio in case of new installation of machine

In case of new machine is installed

Fixed cost 416000

Contribution per unit 26

Break even point (in

units) Fixed cost/ contribution per unit 16000

Fixed cost 416000

Contribution margin

BEP (in revenues) Fixed cost/ Contribution margin ]

9

Contribution margin 162000

BEP (in revenues)

Fixed cost/ Contribution

margin ] 111.11%

Total revenue 540000

Variable cost 378000

Contribution margin

ratio

Total revenue- variable

cost/ Total revenue 30.00%

2 b. Calculating contribution margin ratio in case of new installation of machine

In case of new machine is installed

Fixed cost 416000

Contribution per unit 26

Break even point (in

units) Fixed cost/ contribution per unit 16000

Fixed cost 416000

Contribution margin

BEP (in revenues) Fixed cost/ Contribution margin ]

9

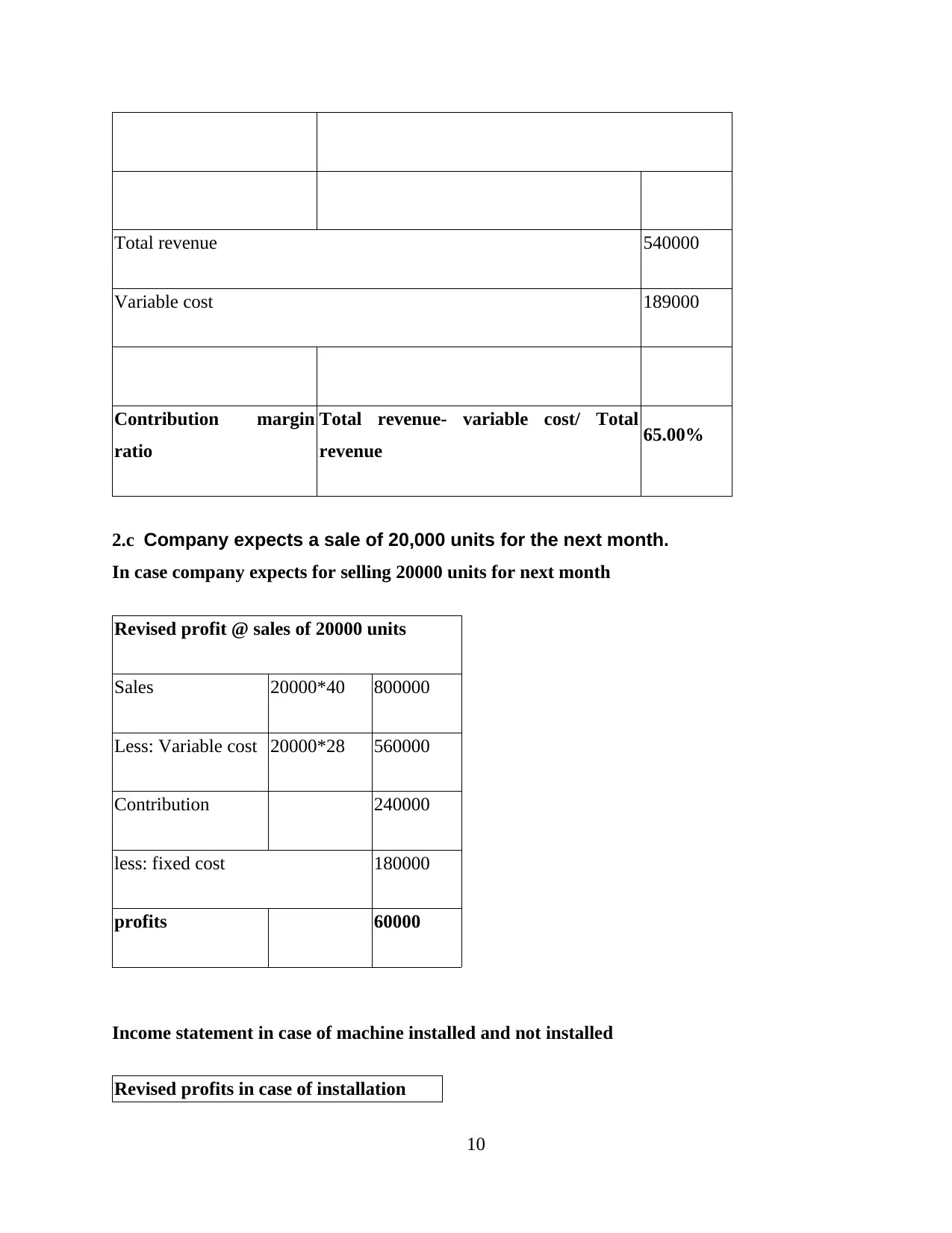

Total revenue 540000

Variable cost 189000

Contribution margin

ratio

Total revenue- variable cost/ Total

revenue 65.00%

2.c Company expects a sale of 20,000 units for the next month.

In case company expects for selling 20000 units for next month

Revised profit @ sales of 20000 units

Sales 20000*40 800000

Less: Variable cost 20000*28 560000

Contribution 240000

less: fixed cost 180000

profits 60000

Income statement in case of machine installed and not installed

Revised profits in case of installation

10

Variable cost 189000

Contribution margin

ratio

Total revenue- variable cost/ Total

revenue 65.00%

2.c Company expects a sale of 20,000 units for the next month.

In case company expects for selling 20000 units for next month

Revised profit @ sales of 20000 units

Sales 20000*40 800000

Less: Variable cost 20000*28 560000

Contribution 240000

less: fixed cost 180000

profits 60000

Income statement in case of machine installed and not installed

Revised profits in case of installation

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.