Analysis of Tax Obstacles in Cross-Border Private Equity Investments

VerifiedAdded on 2020/04/15

|48

|15987

|67

Report

AI Summary

This report delves into the tax obstacles encountered in cross-border private equity investments, with a specific focus on the jurisdictions of Luxembourg and Ireland. The introduction highlights the growing significance of private equity funds, particularly in supporting Small and Medium Enterprises (SMEs) in Europe, and the challenges posed by the financial crisis. The report examines the benefits and regulation of private equity investment funds, including different types, organizational frameworks, and the roles of investors, funds, and management firms. It analyzes the tax treatment of these funds, including ideal jurisdictions, with detailed discussions on Luxembourg and Ireland. The core of the report addresses key tax issues, such as double taxation arising from inconsistent tax treatments across countries and withholding tax relief obstacles. Furthermore, it explores the tax implications of the Alternative Investment Fund Managers Directive (AIFMD), including its aim, scope, and impact on residency and domestic tax developments. The report concludes by summarizing findings and suggesting potential solutions to the identified tax restrictions, aiming to enhance understanding of the tax landscape for cross-border private equity investments.

TAX OBSTACLES TO CROSS-BORDER INVESTMENTS THROUGH PRIVATE EQUITY

INVESTMENT FUNDS FOCUSING ON LUXEMBOURG AND IRELAND

Name of the Student:

Name of the University:

Author’s Note:

INVESTMENT FUNDS FOCUSING ON LUXEMBOURG AND IRELAND

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

I. Introduction..........................................................................................................3

II. Private equity investment funds and their tax treatment............................................5

2.1 Background........................................................................................................5

2.1.1 Explanation and the benefits of private equity investment funds............................5

2.1.2 Regulation of private equity investment funds.....................................................6

2.1.3 Types of private equity investment funds............................................................8

2.1.4 Organizational Framework of a private equity investment fund.............................9

2.1.5 Analysis of the functions performed by the investors, the fund and the management

firm/fund manager..................................................................................................13

2.2 Tax Treatment of private equity investment funds................................................15

2.2.1 Taxes payable by the private equity funds........................................................15

2.2.2 Ideal jurisdiction for creating private equity investment fund.............................15

2.2.3 Luxembourg as a private equity investment fund jurisdiction.............................17

The Part III UCI Law and the CIF Law....................................................................18

3.2.4 Ireland as a private equity investment fund jurisdiction.....................................22

3.2.5 Conclusion..................................................................................................26

IV. Main Tax issues related to cross-border private equity investments......................27

4.2Double taxation caused by mismatch in tax treatment of investment funds by different

countries...........................................................................................................28

4.3 Withholding tax relief obstacles.....................................................................30

V. Tax implications of the Alternative Investment Fund Managers Directive...........32

5.1 Aim, scope and impact of the Alternative Investment Fund Managers Directive.32

1

I. Introduction..........................................................................................................3

II. Private equity investment funds and their tax treatment............................................5

2.1 Background........................................................................................................5

2.1.1 Explanation and the benefits of private equity investment funds............................5

2.1.2 Regulation of private equity investment funds.....................................................6

2.1.3 Types of private equity investment funds............................................................8

2.1.4 Organizational Framework of a private equity investment fund.............................9

2.1.5 Analysis of the functions performed by the investors, the fund and the management

firm/fund manager..................................................................................................13

2.2 Tax Treatment of private equity investment funds................................................15

2.2.1 Taxes payable by the private equity funds........................................................15

2.2.2 Ideal jurisdiction for creating private equity investment fund.............................15

2.2.3 Luxembourg as a private equity investment fund jurisdiction.............................17

The Part III UCI Law and the CIF Law....................................................................18

3.2.4 Ireland as a private equity investment fund jurisdiction.....................................22

3.2.5 Conclusion..................................................................................................26

IV. Main Tax issues related to cross-border private equity investments......................27

4.2Double taxation caused by mismatch in tax treatment of investment funds by different

countries...........................................................................................................28

4.3 Withholding tax relief obstacles.....................................................................30

V. Tax implications of the Alternative Investment Fund Managers Directive...........32

5.1 Aim, scope and impact of the Alternative Investment Fund Managers Directive.32

1

5.2 Tax implications of the Alternative Investment Fund Managers Directive..........35

5.2.1 Issue of residency......................................................................................35

5.2.2 Domestic tax developments introduced as a part of the implementation of the AIFMD

............................................................................................................36

VI. Conclusion.................................................................................................38

Reference List and Bibliography........................................................................41

2

5.2.1 Issue of residency......................................................................................35

5.2.2 Domestic tax developments introduced as a part of the implementation of the AIFMD

............................................................................................................36

VI. Conclusion.................................................................................................38

Reference List and Bibliography........................................................................41

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

I. Introduction

In the current time period, there has been growth in the significance of investment funds

especially in the private equity funds. In the current era, several Europe based“Small and

Medium Enterprises” (SMEs) are having issues in generating income for the growth and

development. As cited by the “European Commission”, the strengthening of the credit

circumstances in the time of calamity has created entrance to difficulty in finance even in the

SMEs. In such scenario, the business capital and the private equity are the key sources which can

assist in addressing the requirements of the SMEs and thereby contributing to their

development1. The SMEs on the other hand can create economic development and generate new

jobs and help in the designing and the exploitation of new technologies and knowledge. For these

factors, the business capital and the private equity investments have a significantjob in the

enhancement of the economy in Europe and thereby require to be cultivating and giving

extensive extent of attention.

Additionally, in the current period, the business capital and private equity in the

European market still functions lower than their actual prospective. The financial crisis has

revealed an unfavorable impact on the private equitymarket in Europe. The entire raising of fund

of the vehicles of private equity in the European Union has lowered in the year 2012 by 43%.

The overall investment in the companies in Europe has even declined and it can be observed that

“EUR 6.5 bn” was paid in the firms of Europe in the year 2012 along with a decline of 19% in

relation to the last year.

The financial atmosphere is a key reasonthat can reinforce and condense the development

of the venture capital and the equity sector that is private in nature. There has been an

observation that as the investment funds undertake investments in a pool of global organizations

and thereby develop several issues related to tax due to the interaction between jurisdiction of

taxing of the associated states, i.e the nation of the construction of the deposit and the nation

where the indented company functions and the nation of the investor2. To make sure the

1Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the

coordination of laws, regulations and administrative provisions relating to undertakings for

collective investment in transferable securities (UCITS);

2OECD revised public discussion draft, Interpretation and application of article 5 (permanent

establishment) of the OECD Model Tax Convention, 2011. Retrieved from:

http://www.oecd.org/ctp/treaties/PermanentEstablishment.pdf; 74

3

In the current time period, there has been growth in the significance of investment funds

especially in the private equity funds. In the current era, several Europe based“Small and

Medium Enterprises” (SMEs) are having issues in generating income for the growth and

development. As cited by the “European Commission”, the strengthening of the credit

circumstances in the time of calamity has created entrance to difficulty in finance even in the

SMEs. In such scenario, the business capital and the private equity are the key sources which can

assist in addressing the requirements of the SMEs and thereby contributing to their

development1. The SMEs on the other hand can create economic development and generate new

jobs and help in the designing and the exploitation of new technologies and knowledge. For these

factors, the business capital and the private equity investments have a significantjob in the

enhancement of the economy in Europe and thereby require to be cultivating and giving

extensive extent of attention.

Additionally, in the current period, the business capital and private equity in the

European market still functions lower than their actual prospective. The financial crisis has

revealed an unfavorable impact on the private equitymarket in Europe. The entire raising of fund

of the vehicles of private equity in the European Union has lowered in the year 2012 by 43%.

The overall investment in the companies in Europe has even declined and it can be observed that

“EUR 6.5 bn” was paid in the firms of Europe in the year 2012 along with a decline of 19% in

relation to the last year.

The financial atmosphere is a key reasonthat can reinforce and condense the development

of the venture capital and the equity sector that is private in nature. There has been an

observation that as the investment funds undertake investments in a pool of global organizations

and thereby develop several issues related to tax due to the interaction between jurisdiction of

taxing of the associated states, i.e the nation of the construction of the deposit and the nation

where the indented company functions and the nation of the investor2. To make sure the

1Directive 2009/65/EC of the European Parliament and of the Council of 13 July 2009 on the

coordination of laws, regulations and administrative provisions relating to undertakings for

collective investment in transferable securities (UCITS);

2OECD revised public discussion draft, Interpretation and application of article 5 (permanent

establishment) of the OECD Model Tax Convention, 2011. Retrieved from:

http://www.oecd.org/ctp/treaties/PermanentEstablishment.pdf; 74

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

enhancement of the investment region associated to private equity, the key obstacles of taxation

requires to be recognized and suitable answers requires to be discovered.

By locking at the general introductory assessment that is concerned with the character of

the operations of the equity funds that is under the Chapter I of this thesis, the researcher will

undertake a comparison of the treatment of taxes of the private equity funds by considering one

as the appropriate venture fund authority i.e. Ireland and Luxembourg as instances. In the

comingsection the researcher will concentrate on the issues of the claim of the tax agreement of

the personal equity funds that is essential for recognizing the key tax restrictions to the cross-

border personal investments that are equity in nature. In “Section IV”, the researcher will assess

the key research questions by highlighting the significant tax restrictions to the cross-border

personal equity investments. In general, the researcher will concentrate on the topic of unrelieved

double taxation that takes place due to the various classifications of the personal equity

investment fund tool by the various territories and with the creation of the risk of enduring

creation of the stakeholders in the nation in relation to the funds or the investors in the country of

the organization that has been targeted. Furthermore, the researcher will assess the restrictions

endured by the stakeholders of fund that is tax translucent when looking to receive a tax credit

with respect to the withheld tax in the nation of the firm that has been targeted. In the conclusive

section, the researcher will explain the present topics of the substitute fund sector, the current

incorporation of the “Alternative Investment Fund Managers Directive” which looks to attain

coordination of the managers of substitute venture funds and explicitly has a vital effect on the

business equity. Even though the Directive does not unswervingly control the tax problems of

the alternative venture funds, the researcher will disclose the implication of tax, the Directive had

and how much the nations are able to explain them theconjugal laws. By looking at the

performed assessment, the researcher will bring out the outcomes and give out prospective

solutions to the recognized restrictions.

4

requires to be recognized and suitable answers requires to be discovered.

By locking at the general introductory assessment that is concerned with the character of

the operations of the equity funds that is under the Chapter I of this thesis, the researcher will

undertake a comparison of the treatment of taxes of the private equity funds by considering one

as the appropriate venture fund authority i.e. Ireland and Luxembourg as instances. In the

comingsection the researcher will concentrate on the issues of the claim of the tax agreement of

the personal equity funds that is essential for recognizing the key tax restrictions to the cross-

border personal investments that are equity in nature. In “Section IV”, the researcher will assess

the key research questions by highlighting the significant tax restrictions to the cross-border

personal equity investments. In general, the researcher will concentrate on the topic of unrelieved

double taxation that takes place due to the various classifications of the personal equity

investment fund tool by the various territories and with the creation of the risk of enduring

creation of the stakeholders in the nation in relation to the funds or the investors in the country of

the organization that has been targeted. Furthermore, the researcher will assess the restrictions

endured by the stakeholders of fund that is tax translucent when looking to receive a tax credit

with respect to the withheld tax in the nation of the firm that has been targeted. In the conclusive

section, the researcher will explain the present topics of the substitute fund sector, the current

incorporation of the “Alternative Investment Fund Managers Directive” which looks to attain

coordination of the managers of substitute venture funds and explicitly has a vital effect on the

business equity. Even though the Directive does not unswervingly control the tax problems of

the alternative venture funds, the researcher will disclose the implication of tax, the Directive had

and how much the nations are able to explain them theconjugal laws. By looking at the

performed assessment, the researcher will bring out the outcomes and give out prospective

solutions to the recognized restrictions.

4

II. Private equity investment funds and their tax treatment

2.1 Background

2.1.1 Explanation and the benefits of private equity investment funds:

The venture funds are fiscal mediators which gatherprofit from the financiersthat can be

corporations or individuals and connect them thereby undertake investments within extend of

ventures with the intention of accomplishing venture development and attaining gains for the

investors. The investors specifically in developed nations, observes it more beneficial to invest

their money in an indirect manner which means constructing their investments with the help of

communal investment tools rather than the frankly purchased shares in the organizations that

have been targeted3. There are several factors that make the funds an eye-catching tool from the

point of view of the investors in comparison to the direct investments, specifically,

Investment facilitation: It can be hard for the investors to select the precise goal for

venture due to lack of essential expertise, resources and time. This is the reason why it

has become easier to allocate the job of managing and selecting ventures to the skilled

investment fund managers.

Risk Spreading: The process of spreading of risk is attained with the help of the

categorization of investments undertaken by endowment. An aggregate investor can

generally give in order to capitalize in a small level of money. Therefore, it will become

tough for them to purchase any holdings in various organizations in a direct manner. The

investment of money with the help of funds permits the investors to be the shareholders

in various firms. The holding of shares of various organizations terminates the risk of

losing all the money of the investors with respect to the straight investments in scenarios

of insolvency of one of the marked organizations and reduces the danger in accordance to

the gain.

Lowering of expense for investors: The transaction cost of the investors on minor sales

and purchases of shares are specifically much bigger than as a fraction of the price of

every business deal than those for the fund that deals with huge amount.

The processesexplainedabove are applicable to the private equity investment funds.

3Commission staff working document of 30 April 2009 “Impact assessment” accompanying the

Proposal for a Directive of the European Parliament and of the Council on Alternative

Investment Fund Managers and amending Directives 2004/39/EC and 2009/…/EC;

5

2.1 Background

2.1.1 Explanation and the benefits of private equity investment funds:

The venture funds are fiscal mediators which gatherprofit from the financiersthat can be

corporations or individuals and connect them thereby undertake investments within extend of

ventures with the intention of accomplishing venture development and attaining gains for the

investors. The investors specifically in developed nations, observes it more beneficial to invest

their money in an indirect manner which means constructing their investments with the help of

communal investment tools rather than the frankly purchased shares in the organizations that

have been targeted3. There are several factors that make the funds an eye-catching tool from the

point of view of the investors in comparison to the direct investments, specifically,

Investment facilitation: It can be hard for the investors to select the precise goal for

venture due to lack of essential expertise, resources and time. This is the reason why it

has become easier to allocate the job of managing and selecting ventures to the skilled

investment fund managers.

Risk Spreading: The process of spreading of risk is attained with the help of the

categorization of investments undertaken by endowment. An aggregate investor can

generally give in order to capitalize in a small level of money. Therefore, it will become

tough for them to purchase any holdings in various organizations in a direct manner. The

investment of money with the help of funds permits the investors to be the shareholders

in various firms. The holding of shares of various organizations terminates the risk of

losing all the money of the investors with respect to the straight investments in scenarios

of insolvency of one of the marked organizations and reduces the danger in accordance to

the gain.

Lowering of expense for investors: The transaction cost of the investors on minor sales

and purchases of shares are specifically much bigger than as a fraction of the price of

every business deal than those for the fund that deals with huge amount.

The processesexplainedabove are applicable to the private equity investment funds.

3Commission staff working document of 30 April 2009 “Impact assessment” accompanying the

Proposal for a Directive of the European Parliament and of the Council on Alternative

Investment Fund Managers and amending Directives 2004/39/EC and 2009/…/EC;

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.1.2 Regulation of private equity investment funds

Conversely, to gain knowledge about the specifications of this kind of funds, it is

significant to differentiate decisionsfor the combined investments in the securities that are

transferable from the other activities for the purpose of combined investments which are called

the substitute investment funds4.

A “UCITS” fund is a Europe based product that is regulated by the Directive

2009/65/EC3” which is even known as the “UCITS IV Directive”. The aim of “UCIT IV

Directive is to permit for the funds that are open ended that invest in manageable securities to the

topic of similar regulations in every “Member State” that facilitates the fractious border offer of

the investments that contributes to the founding of the solitary investment fund market as a

section of the distinctmonetary European market. Due to these reasons, the “UCITS IV

Directive” looks “UCITS” having a passport that is of Europe in order to become profitable

throughout the European Union. The “UCITS”directive is reliant on the principle of solitary

license that explains that the “UCITS” that have the authority in single member state can sale

their units in other “Member State” without looking to put on for the approval in the later period.

The substitutes of “UCITS”, “AIFs” in general are inclusive of the hedge and private

equity investment finance and real estate are the focus of the thesis. The another investment

funds can be explained as a tool for the purpose of combined investment that gathers the assets

from various stakeholders in order to empower in such assets with respect to a specific approach

for the profit of the investors and it does not function a commerce that is outside business sector

and even does not succeed as “UCITS”5. These frameworks like the holding organizations and

securitization tools can be clearly omitted from the definition of “AIF”.

With respect to “UCITS”, the “AIFs” are not controlled by the “UCITS IV Directive” as

it does not require having a passport of Europe and therefore is not able to market in a free

manner in the European Union. On the contrary to “UCITS”, there is no management for “AIFs”

within the European Union; in one pole there exists nations which implement a distinct

4OECD Income and Capital Model Tax Convention and Commentary, as of 22 July 2010;

5EVCA comments on the discussion draft on “Interpretation and application of article 5

(permanent establishment) of the OECD Model Tax Convention”, 8 February 2012. Retrieved

from: http://www.oecd.org/ctp/treaties/49637906.pdf;

6

Conversely, to gain knowledge about the specifications of this kind of funds, it is

significant to differentiate decisionsfor the combined investments in the securities that are

transferable from the other activities for the purpose of combined investments which are called

the substitute investment funds4.

A “UCITS” fund is a Europe based product that is regulated by the Directive

2009/65/EC3” which is even known as the “UCITS IV Directive”. The aim of “UCIT IV

Directive is to permit for the funds that are open ended that invest in manageable securities to the

topic of similar regulations in every “Member State” that facilitates the fractious border offer of

the investments that contributes to the founding of the solitary investment fund market as a

section of the distinctmonetary European market. Due to these reasons, the “UCITS IV

Directive” looks “UCITS” having a passport that is of Europe in order to become profitable

throughout the European Union. The “UCITS”directive is reliant on the principle of solitary

license that explains that the “UCITS” that have the authority in single member state can sale

their units in other “Member State” without looking to put on for the approval in the later period.

The substitutes of “UCITS”, “AIFs” in general are inclusive of the hedge and private

equity investment finance and real estate are the focus of the thesis. The another investment

funds can be explained as a tool for the purpose of combined investment that gathers the assets

from various stakeholders in order to empower in such assets with respect to a specific approach

for the profit of the investors and it does not function a commerce that is outside business sector

and even does not succeed as “UCITS”5. These frameworks like the holding organizations and

securitization tools can be clearly omitted from the definition of “AIF”.

With respect to “UCITS”, the “AIFs” are not controlled by the “UCITS IV Directive” as

it does not require having a passport of Europe and therefore is not able to market in a free

manner in the European Union. On the contrary to “UCITS”, there is no management for “AIFs”

within the European Union; in one pole there exists nations which implement a distinct

4OECD Income and Capital Model Tax Convention and Commentary, as of 22 July 2010;

5EVCA comments on the discussion draft on “Interpretation and application of article 5

(permanent establishment) of the OECD Model Tax Convention”, 8 February 2012. Retrieved

from: http://www.oecd.org/ctp/treaties/49637906.pdf;

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

lawmaking for the “AIFs” that controls specifically in the lawfulaspect of the funds, the investor

rights and incorporates special regimes of taxes6. At the other pole, certain nations put down to

the funds the benefit of selecting their permissible form and the stipulations that are in

association with their investors which has been generated.

The reason that “AIFs” are regulated fewer than the “UCITS”or even omitted by the

administrator from the guideline can be defined by the factor that generally do not have an

increased intensity ofdirective. “AIFs”dissimilarto “UCITS” does not pact with the common

public investing that attracts specific qualified investors like the richpeople and even in asset

organizations. The extent of their operations needs utmostelasticity of structuring and a restricted

revelation. In the current period regulations of “AIFs” at the European Union point is

accomplished at the extent of the investment managers with the help of the “Directive” on the

guideline of optional investment managers. Thecomponent is constructed even in Chapter V of

the current thesis.

A personal equity fund may be explained as a kind of equity venture within the personal

organizations that have not been disclosed with a stock exchange. The private equity is

differentiated by their venture framework that is active in nature in which it looks to deliver the

operational enhancements within their organizations over the previouscertain years.

The personal equity fund is different UCITS with respect to the kind of stakeholders and

the sort of ventures and their strategies of the firm. Generally the personal equity ventures are

reticent for the investors who are well informed and on the other hand the investors of UCITS

can be inclusive of the full continuum of the type of investors. By looking at the type of

investments, the private equity ventures may undertake investments in any kind of property

whereas the investments of the funds of UCITS shall only consist of the manageable securities

and the instruments of the wealth market that have admitted to or have been dealt on market that

is regulated of the units that is permitted UCITS or the other collective investment undertakings

and the deposits with the financial derivative tools in the credit organizations. The UCITS

6OECD public discussion draft, the granting of treaty benefits with respect to the income of

collective investment vehicles, 2010. Retrieved from:

http://www.oecd.org/tax/treaties/45359261.pdf;

7

rights and incorporates special regimes of taxes6. At the other pole, certain nations put down to

the funds the benefit of selecting their permissible form and the stipulations that are in

association with their investors which has been generated.

The reason that “AIFs” are regulated fewer than the “UCITS”or even omitted by the

administrator from the guideline can be defined by the factor that generally do not have an

increased intensity ofdirective. “AIFs”dissimilarto “UCITS” does not pact with the common

public investing that attracts specific qualified investors like the richpeople and even in asset

organizations. The extent of their operations needs utmostelasticity of structuring and a restricted

revelation. In the current period regulations of “AIFs” at the European Union point is

accomplished at the extent of the investment managers with the help of the “Directive” on the

guideline of optional investment managers. Thecomponent is constructed even in Chapter V of

the current thesis.

A personal equity fund may be explained as a kind of equity venture within the personal

organizations that have not been disclosed with a stock exchange. The private equity is

differentiated by their venture framework that is active in nature in which it looks to deliver the

operational enhancements within their organizations over the previouscertain years.

The personal equity fund is different UCITS with respect to the kind of stakeholders and

the sort of ventures and their strategies of the firm. Generally the personal equity ventures are

reticent for the investors who are well informed and on the other hand the investors of UCITS

can be inclusive of the full continuum of the type of investors. By looking at the type of

investments, the private equity ventures may undertake investments in any kind of property

whereas the investments of the funds of UCITS shall only consist of the manageable securities

and the instruments of the wealth market that have admitted to or have been dealt on market that

is regulated of the units that is permitted UCITS or the other collective investment undertakings

and the deposits with the financial derivative tools in the credit organizations. The UCITS

6OECD public discussion draft, the granting of treaty benefits with respect to the income of

collective investment vehicles, 2010. Retrieved from:

http://www.oecd.org/tax/treaties/45359261.pdf;

7

business strategy looks at the investments that are increasingly profitable in nature in specific

kinds of assets that have been explained earlier in order to allocate the income to the investors or

purchasing of the units at the request of the investors7. The personal equity investment strategy

additionally, in certain scenarios is focused in order to nurture development and establish extra

goodwill in the firm that has been targeted like for example with the enhancement of innovative

technologies and products, growth of the working fund by taking a product that is existent in the

new market, ownership resolution and the management problems with the main aim to sell the

targeted organization after certain years for an increased price and to create profit for the investor

fund.

2.1.3 Types of private equity investment funds

The personal equity investments can be classified into the following kinds:

Leveraged buyout funds: Conventionally they gain power of the ranks with the help of the

majority of the ownership and representation of the board for the companies that are undervalued

or have matured as underperforming. The funds that are buyout have specifically required to

influence their equity investments in debt bankrolling and even more which are concerned with

the capability of a firm to create sustainable cash flow than the venture capital funds.

Venture capital funds: These kinds of funds acquire least amount of stakes in a start-up or

relatively young private organizations with a prospective development that are driven

specifically by the technological development and give both management skills and equity

capital. It is common for an investment capital investment fund to take as a scenario within their

asset which gains position on the boards of the directors of a firm that has been targeted, which is

useful for giving out management skills for supervising the investment8.

Growth equity funds: They undertake investments in latter stages in the IPO organizations and

even in the PIPE transactions with the private organizations. The private equity funds can

undertake investments in various firms by overlooking their size but most of the companies that

has been targeted for the private equity funds that are “SMEs” are 83% of the private equity

funds that have been made into the “SMEs”.

7Commission staff working document of 30 April 2009 “Impact assessment” accompanying the

Proposal for a Directive of the European Parliament and of the Council on Alternative

Investment Fund Managers and amending Directives 2004/39/EC and 2009/…/EC;

8Luxembourg law of 17 December 2010 on Undertakings for Collective Investment;

8

kinds of assets that have been explained earlier in order to allocate the income to the investors or

purchasing of the units at the request of the investors7. The personal equity investment strategy

additionally, in certain scenarios is focused in order to nurture development and establish extra

goodwill in the firm that has been targeted like for example with the enhancement of innovative

technologies and products, growth of the working fund by taking a product that is existent in the

new market, ownership resolution and the management problems with the main aim to sell the

targeted organization after certain years for an increased price and to create profit for the investor

fund.

2.1.3 Types of private equity investment funds

The personal equity investments can be classified into the following kinds:

Leveraged buyout funds: Conventionally they gain power of the ranks with the help of the

majority of the ownership and representation of the board for the companies that are undervalued

or have matured as underperforming. The funds that are buyout have specifically required to

influence their equity investments in debt bankrolling and even more which are concerned with

the capability of a firm to create sustainable cash flow than the venture capital funds.

Venture capital funds: These kinds of funds acquire least amount of stakes in a start-up or

relatively young private organizations with a prospective development that are driven

specifically by the technological development and give both management skills and equity

capital. It is common for an investment capital investment fund to take as a scenario within their

asset which gains position on the boards of the directors of a firm that has been targeted, which is

useful for giving out management skills for supervising the investment8.

Growth equity funds: They undertake investments in latter stages in the IPO organizations and

even in the PIPE transactions with the private organizations. The private equity funds can

undertake investments in various firms by overlooking their size but most of the companies that

has been targeted for the private equity funds that are “SMEs” are 83% of the private equity

funds that have been made into the “SMEs”.

7Commission staff working document of 30 April 2009 “Impact assessment” accompanying the

Proposal for a Directive of the European Parliament and of the Council on Alternative

Investment Fund Managers and amending Directives 2004/39/EC and 2009/…/EC;

8Luxembourg law of 17 December 2010 on Undertakings for Collective Investment;

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

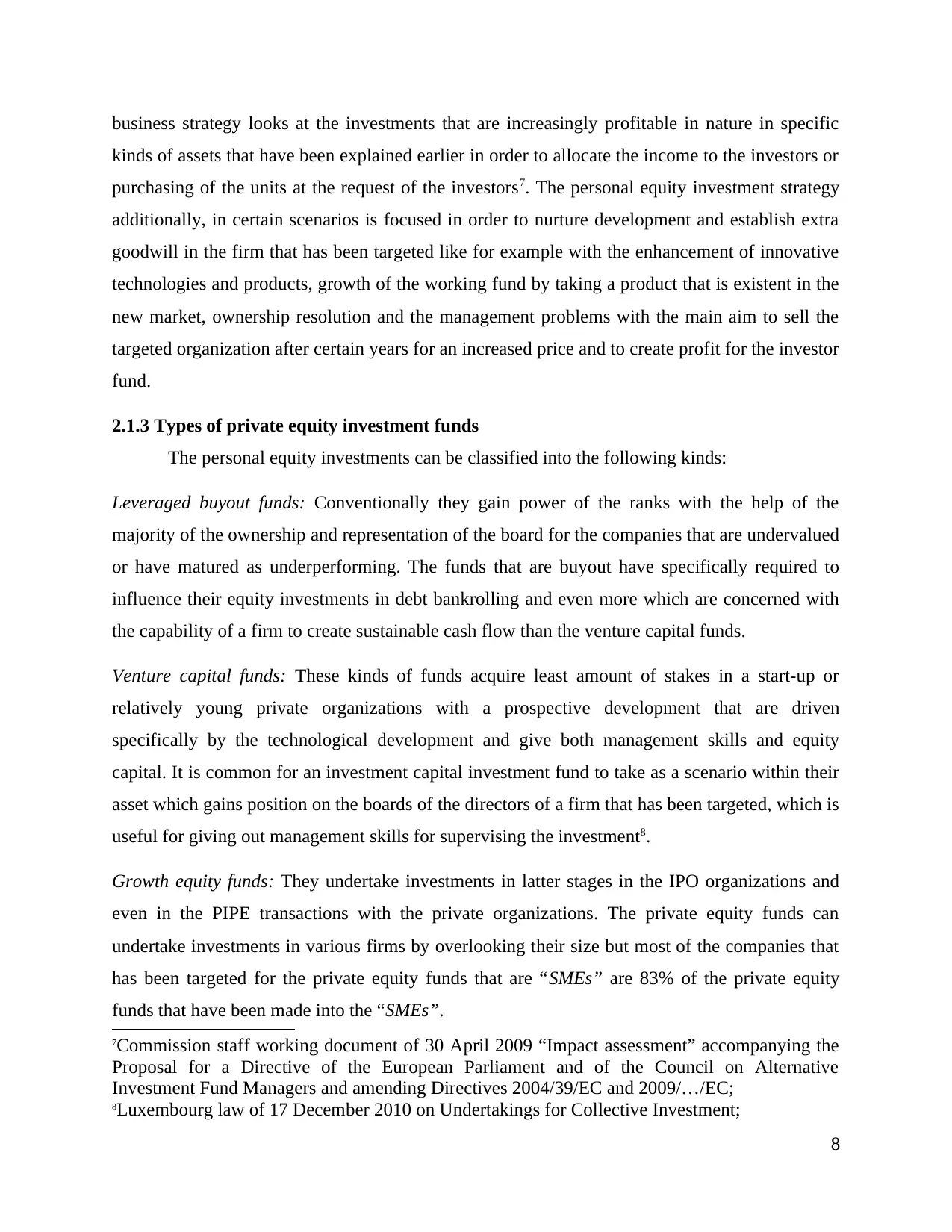

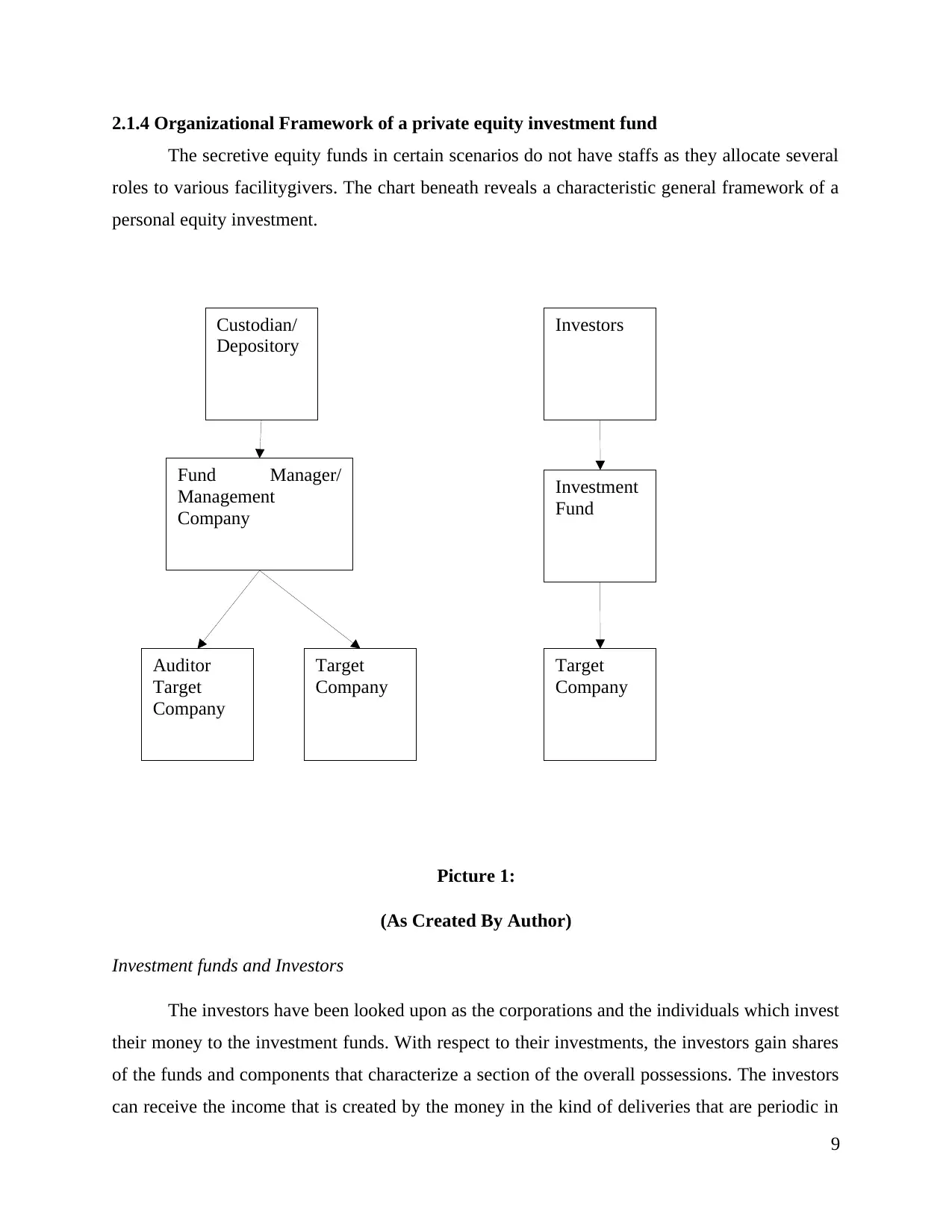

Custodian/

Depository

Fund Manager/

Management

Company

Target

Company

Target

Company

Auditor

Target

Company

Investors

Investment

Fund

2.1.4 Organizational Framework of a private equity investment fund

The secretive equity funds in certain scenarios do not have staffs as they allocate several

roles to various facilitygivers. The chart beneath reveals a characteristic general framework of a

personal equity investment.

Picture 1:

(As Created By Author)

Investment funds and Investors

The investors have been looked upon as the corporations and the individuals which invest

their money to the investment funds. With respect to their investments, the investors gain shares

of the funds and components that characterize a section of the overall possessions. The investors

can receive the income that is created by the money in the kind of deliveries that are periodic in

9

Depository

Fund Manager/

Management

Company

Target

Company

Target

Company

Auditor

Target

Company

Investors

Investment

Fund

2.1.4 Organizational Framework of a private equity investment fund

The secretive equity funds in certain scenarios do not have staffs as they allocate several

roles to various facilitygivers. The chart beneath reveals a characteristic general framework of a

personal equity investment.

Picture 1:

(As Created By Author)

Investment funds and Investors

The investors have been looked upon as the corporations and the individuals which invest

their money to the investment funds. With respect to their investments, the investors gain shares

of the funds and components that characterize a section of the overall possessions. The investors

can receive the income that is created by the money in the kind of deliveries that are periodic in

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

nature or the kind of principal gains from the substitution of the asset of the funds9. The

investment funds generally comprises of the financial assets that have been acquired by the fund

with the help of the fund that is gained from investors along with the prospective cash reserves.

Fund manager/ Management Company

The management firm or even the account manager is the individual or the entity that

generally makes the money to be generated so it generally accomplishes the roles of the

promoters or the fund originator.

The management of the reserve can be undertaken with the help of the external managers

of a management firm or by the fund itself that is in the legal aspect can allow the in-house

administration and the place where the stakeholders look to not to choose an exterior

administered firm. For instance, Luxembourg SICAFs and SICAVs that is generated in the

corporate aspect must both be selected a managing firm or allocate itself as a self-administered

asset firm10. Conversely, the reserved equity funds generated in the lucid form like for example

Irish bonds and the “CCFS” that are needed to select an exterior administration company.

The firm is the entity that manages the equity funds as a general business which increases

the capital from various investors with an idea to invest in the money for the profit of those

financiers with respect to an explained investment policy. In reality, management firms generally

manage various investment funds. The management firm functions with respect to the service

agreement that has been contracted with the financiers. During the time of the center

management, the endowment generally incorporates administration team that consists of entities

who have competent expertise11.

The characteristics of the operations of the fund managers of the management firm are

inclusive of the following:

9P. Behrens, Residence of Companies under Tax Treaties and EC Law, G. Maisto edition, fifth

volume in the IBFD "EC and International Tax Law Series", IBFD Publications BV, 2009;

10Luxembourg law of 15 June 2004 relating to the Investment Company in Risk Capital (SICAR)

as amended by the law of 24 October 2008;

11The Luxembourg Bill of law No.6471 of 24 August 2012 transposing the AIFMD;

10

investment funds generally comprises of the financial assets that have been acquired by the fund

with the help of the fund that is gained from investors along with the prospective cash reserves.

Fund manager/ Management Company

The management firm or even the account manager is the individual or the entity that

generally makes the money to be generated so it generally accomplishes the roles of the

promoters or the fund originator.

The management of the reserve can be undertaken with the help of the external managers

of a management firm or by the fund itself that is in the legal aspect can allow the in-house

administration and the place where the stakeholders look to not to choose an exterior

administered firm. For instance, Luxembourg SICAFs and SICAVs that is generated in the

corporate aspect must both be selected a managing firm or allocate itself as a self-administered

asset firm10. Conversely, the reserved equity funds generated in the lucid form like for example

Irish bonds and the “CCFS” that are needed to select an exterior administration company.

The firm is the entity that manages the equity funds as a general business which increases

the capital from various investors with an idea to invest in the money for the profit of those

financiers with respect to an explained investment policy. In reality, management firms generally

manage various investment funds. The management firm functions with respect to the service

agreement that has been contracted with the financiers. During the time of the center

management, the endowment generally incorporates administration team that consists of entities

who have competent expertise11.

The characteristics of the operations of the fund managers of the management firm are

inclusive of the following:

9P. Behrens, Residence of Companies under Tax Treaties and EC Law, G. Maisto edition, fifth

volume in the IBFD "EC and International Tax Law Series", IBFD Publications BV, 2009;

10Luxembourg law of 15 June 2004 relating to the Investment Company in Risk Capital (SICAR)

as amended by the law of 24 October 2008;

11The Luxembourg Bill of law No.6471 of 24 August 2012 transposing the AIFMD;

10

Servicing the investors of the funds by explaining the strategies and objectives of the

investment, sustaining the research, investment assessment, evaluation and recognition

of the prospective investment opportunities, selection of the portfolio and undertaking

the transactions related to the investment.

Administration operations that is inclusive of the fund assessment and pricing, managing

and functioning the accounts of the funds that is inclusive of the income that is received

and the losses and the gains that has been realized, liaison with the auditor and

custodian. Due to these facilities, the administration firm is given a fee for management.

The management company personnel and even the endowment managers generally get a

remuneration fee that is reliant on the presentation of the endowment that is called the approved

interest. Carried interest permits the personnel of the endowment organizations or the center

managers of the funds to receive a part in the profit that is created by the investment of the

funds12. Generally in additional to the administration services, the administration organizations

function as the ventureconsultant of the fund that provides the goal organizations and the fund

with the consultancy services with respect to an investment consultative contract. For these

services, the administration firm gains fees that are additional in nature.

Custodian (depository)

The custodian is accountable for the management of the assets that are available in the

funds. This is inclusive of the safeguarding of the assets of the funds and the daily supervision of

the assets that is dependent on the instructions that have been established from the administration

firm or the endowment manager until they struggle with the legitimate reports. In aarrangement

that dematerialized in nature, the asset of the funds are recorded in the minimal ownership of the

stockpile and it has been observed that in a materialized process, the certificates are held

physically with the cooperation or approval of the depository13. This is constructed in order to

restrict the assaulting of the investment assets by the administration firm or by the management

executives. For their facilities the collection levies a fee that is reliant on the proportion of the

ordinary net assets of the funds.

12OECD public discussion draft, Clarification of the meaning of “Beneficial owner” in the OECD

Model Tax Convention, 2011. Retrieved from: http://www.oecd.org/ctp/treaties/47643872.pdf;

13Report of the EC Expert Group, on removing tax obstacles to cross-border Venture Capital

Investments, 2010. Retrieved from: http://ec.europa.eu/venture-capital/index_en.htm;

11

investment, sustaining the research, investment assessment, evaluation and recognition

of the prospective investment opportunities, selection of the portfolio and undertaking

the transactions related to the investment.

Administration operations that is inclusive of the fund assessment and pricing, managing

and functioning the accounts of the funds that is inclusive of the income that is received

and the losses and the gains that has been realized, liaison with the auditor and

custodian. Due to these facilities, the administration firm is given a fee for management.

The management company personnel and even the endowment managers generally get a

remuneration fee that is reliant on the presentation of the endowment that is called the approved

interest. Carried interest permits the personnel of the endowment organizations or the center

managers of the funds to receive a part in the profit that is created by the investment of the

funds12. Generally in additional to the administration services, the administration organizations

function as the ventureconsultant of the fund that provides the goal organizations and the fund

with the consultancy services with respect to an investment consultative contract. For these

services, the administration firm gains fees that are additional in nature.

Custodian (depository)

The custodian is accountable for the management of the assets that are available in the

funds. This is inclusive of the safeguarding of the assets of the funds and the daily supervision of

the assets that is dependent on the instructions that have been established from the administration

firm or the endowment manager until they struggle with the legitimate reports. In aarrangement

that dematerialized in nature, the asset of the funds are recorded in the minimal ownership of the

stockpile and it has been observed that in a materialized process, the certificates are held

physically with the cooperation or approval of the depository13. This is constructed in order to

restrict the assaulting of the investment assets by the administration firm or by the management

executives. For their facilities the collection levies a fee that is reliant on the proportion of the

ordinary net assets of the funds.

12OECD public discussion draft, Clarification of the meaning of “Beneficial owner” in the OECD

Model Tax Convention, 2011. Retrieved from: http://www.oecd.org/ctp/treaties/47643872.pdf;

13Report of the EC Expert Group, on removing tax obstacles to cross-border Venture Capital

Investments, 2010. Retrieved from: http://ec.europa.eu/venture-capital/index_en.htm;

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 48

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.