Comprehensive Report: Australian Private Health Insurance Reforms 2017

VerifiedAdded on 2021/09/19

|14

|3289

|304

Report

AI Summary

This report provides a detailed analysis of the 2017 private health insurance reforms implemented by the Australian government. It examines the reforms' background, objectives, and the timeline of their implementation, including key dates and actions taken. The report delves into the critical aspects of the reforms, such as changes in the prostheses rules, the establishment of advisory committees, and legislative amendments. It also explores the impact of removing policy restrictions, improved consumer protection, and the introduction of standardized product categories. Furthermore, the report discusses the amendment rules of 2018 and the implications of the reforms on various aspects of health insurance coverage, including discounts for younger people, mental health treatment, and the removal of benefits for natural therapies. The report concludes with an overview of the reforms' impact on consumers and the healthcare landscape in Australia. The content is intended for students and researchers interested in healthcare policy.

Running head: PRIVATE HEALTH INSURANCE 2017 REFORMS

PRIVATE HEALTH INSURANCE 2017 REFORMS

Name of the student:

Name of the university:

Author note:

PRIVATE HEALTH INSURANCE 2017 REFORMS

Name of the student:

Name of the university:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1PRIVATE HEALTH INSURANCE 2017 REFORMS

Executive summary:

Last year in the month of October, the Australian government had announced a series of

reforms or changes in the healthcare policies in order to make them more affordable for the

Australians. This was introduced with an intention to make medical benefits accessible to all

citizens and ensure there is no medical or health related issues for the citizens.

The following report will highlight the different aspects that are associated to the

changing reforms. The description as well as the background of the reform will be studied in

details. The mechanisms and the compliance issues associated with the implementation of the

reform change will be studied in details in the following paragraphs. By the end of this report,

the reader will be able to have an in depth idea of the recent changing reforms in the health

insurance sector. The different stages of the life cycle of the reforms that are to be implemented

in the healthcare industry in Australia will be discussed in details in the following paragraph. By

the end of the report, the reader will have a clear understanding of the different aspects of the

reform implementation.

Executive summary:

Last year in the month of October, the Australian government had announced a series of

reforms or changes in the healthcare policies in order to make them more affordable for the

Australians. This was introduced with an intention to make medical benefits accessible to all

citizens and ensure there is no medical or health related issues for the citizens.

The following report will highlight the different aspects that are associated to the

changing reforms. The description as well as the background of the reform will be studied in

details. The mechanisms and the compliance issues associated with the implementation of the

reform change will be studied in details in the following paragraphs. By the end of this report,

the reader will be able to have an in depth idea of the recent changing reforms in the health

insurance sector. The different stages of the life cycle of the reforms that are to be implemented

in the healthcare industry in Australia will be discussed in details in the following paragraph. By

the end of the report, the reader will have a clear understanding of the different aspects of the

reform implementation.

2PRIVATE HEALTH INSURANCE 2017 REFORMS

Table of Contents

Introduction:....................................................................................................................................3

Critical analysis of the reforms:.......................................................................................................3

Timeline for implementation:......................................................................................................4

Factsheet for the reforms:............................................................................................................7

Private health insurance reforms: Amendment Rules 2018:.......................................................8

Impact of removing the policy restrictions:.................................................................................9

Improved protection for consumers and terminating the policies:..............................................9

Legislative amendments:...........................................................................................................10

Low priced health insurance products in the private segment:..................................................11

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

Table of Contents

Introduction:....................................................................................................................................3

Critical analysis of the reforms:.......................................................................................................3

Timeline for implementation:......................................................................................................4

Factsheet for the reforms:............................................................................................................7

Private health insurance reforms: Amendment Rules 2018:.......................................................8

Impact of removing the policy restrictions:.................................................................................9

Improved protection for consumers and terminating the policies:..............................................9

Legislative amendments:...........................................................................................................10

Low priced health insurance products in the private segment:..................................................11

Conclusion:....................................................................................................................................12

References:....................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3PRIVATE HEALTH INSURANCE 2017 REFORMS

Introduction:

Health Insurance can be defined as a kind of insurance which provides overall medical as

well as financial coverage for the policyholder in case of any medical emergencies. According to

the kind of policy owned by the policy owner, the different expenses associated to the treatment

of critical diseases, surgery expenses, hospital fees etc. are sponsored by the healthcare insurance

company.

In Australia, there are different health insurance companies that have different kinds of

health insurances available for students, senior citizens and other category of consumers that

offer great benefits for the users. In Australia, almost all the citizens including students, senior

citizens are covered for any medical illness under the healthcare division. Users can also

eliminate the private healthcare divisions in order to give themselves the provisions of a wider

range of healthcare insurance options. The two most important decisions of the healthcare

insurances, which are general treatment as well as hospital and the recent reforms that the

Australian government has implemented for the benefit of the Australian citizens, will be

discussed in details in the following paragraphs.

Critical analysis of the reforms:

Recently the Australian government has introduced certain reforms in order to make the

health insurances more affordable for the consumers. The analysis of the reform requires it to be

explained in a series of steps (Flahiff, 2014).

Introduction:

Health Insurance can be defined as a kind of insurance which provides overall medical as

well as financial coverage for the policyholder in case of any medical emergencies. According to

the kind of policy owned by the policy owner, the different expenses associated to the treatment

of critical diseases, surgery expenses, hospital fees etc. are sponsored by the healthcare insurance

company.

In Australia, there are different health insurance companies that have different kinds of

health insurances available for students, senior citizens and other category of consumers that

offer great benefits for the users. In Australia, almost all the citizens including students, senior

citizens are covered for any medical illness under the healthcare division. Users can also

eliminate the private healthcare divisions in order to give themselves the provisions of a wider

range of healthcare insurance options. The two most important decisions of the healthcare

insurances, which are general treatment as well as hospital and the recent reforms that the

Australian government has implemented for the benefit of the Australian citizens, will be

discussed in details in the following paragraphs.

Critical analysis of the reforms:

Recently the Australian government has introduced certain reforms in order to make the

health insurances more affordable for the consumers. The analysis of the reform requires it to be

explained in a series of steps (Flahiff, 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4PRIVATE HEALTH INSURANCE 2017 REFORMS

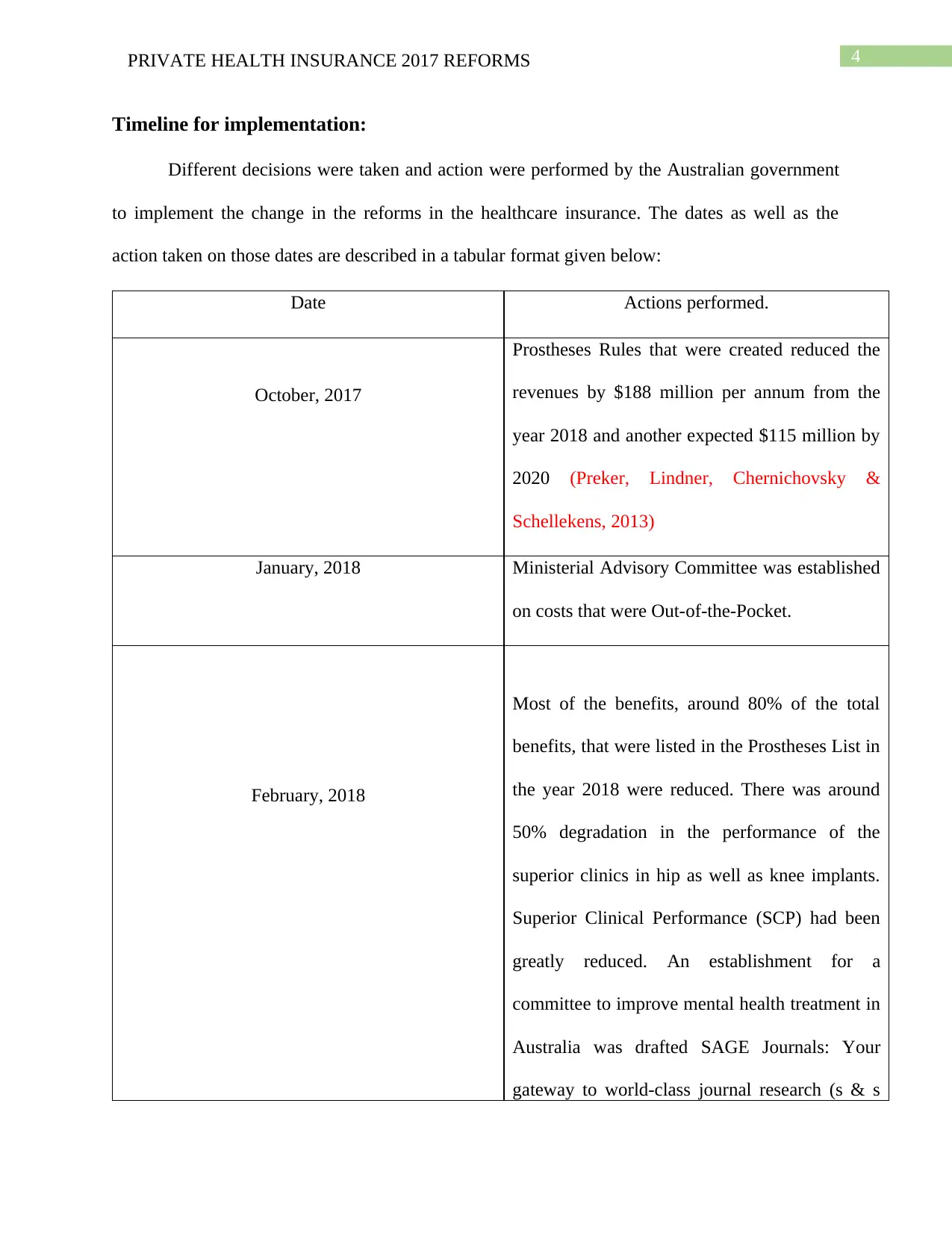

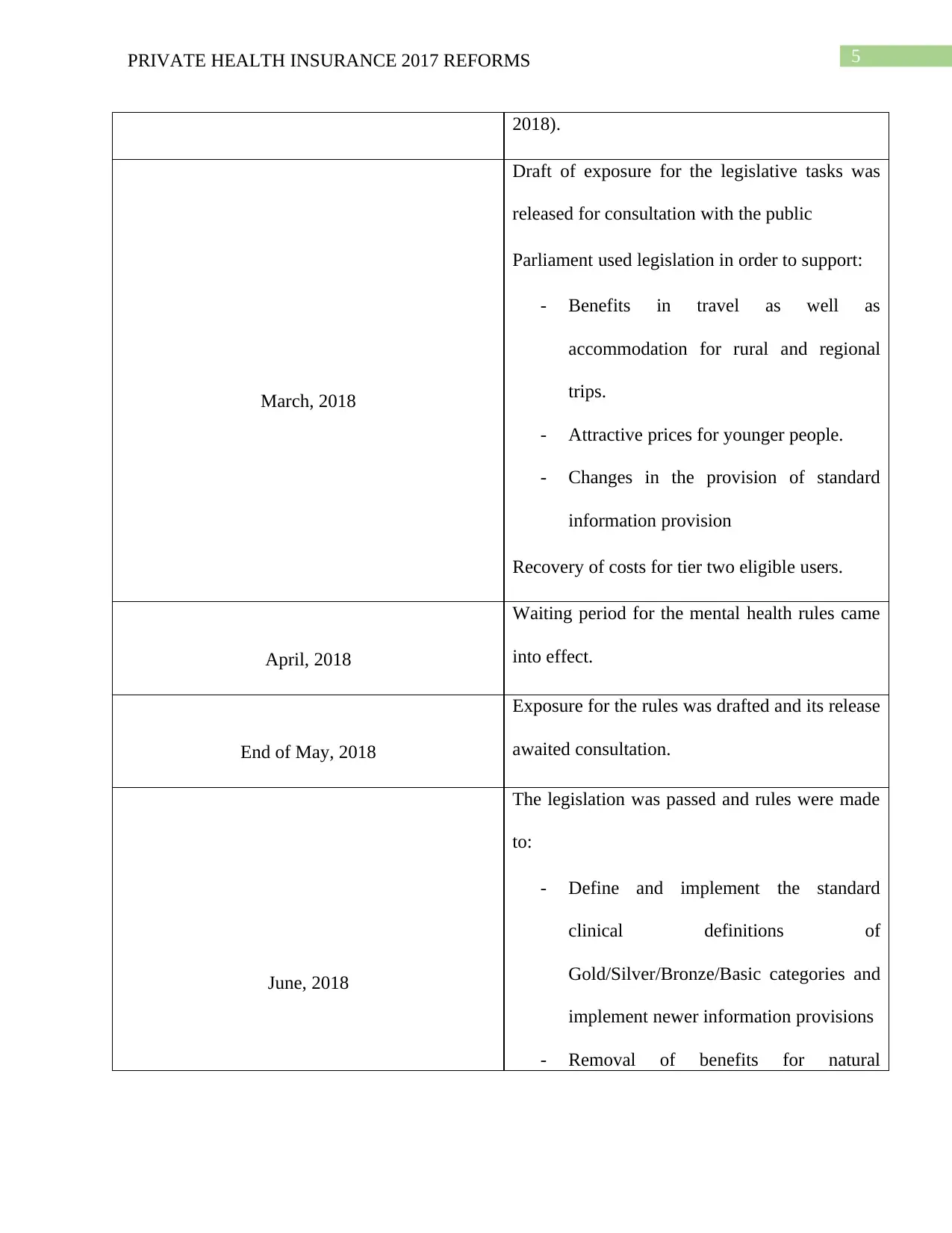

Timeline for implementation:

Different decisions were taken and action were performed by the Australian government

to implement the change in the reforms in the healthcare insurance. The dates as well as the

action taken on those dates are described in a tabular format given below:

Date Actions performed.

October, 2017

Prostheses Rules that were created reduced the

revenues by $188 million per annum from the

year 2018 and another expected $115 million by

2020 (Preker, Lindner, Chernichovsky &

Schellekens, 2013)

January, 2018 Ministerial Advisory Committee was established

on costs that were Out-of-the-Pocket.

February, 2018

Most of the benefits, around 80% of the total

benefits, that were listed in the Prostheses List in

the year 2018 were reduced. There was around

50% degradation in the performance of the

superior clinics in hip as well as knee implants.

Superior Clinical Performance (SCP) had been

greatly reduced. An establishment for a

committee to improve mental health treatment in

Australia was drafted SAGE Journals: Your

gateway to world-class journal research (s & s

Timeline for implementation:

Different decisions were taken and action were performed by the Australian government

to implement the change in the reforms in the healthcare insurance. The dates as well as the

action taken on those dates are described in a tabular format given below:

Date Actions performed.

October, 2017

Prostheses Rules that were created reduced the

revenues by $188 million per annum from the

year 2018 and another expected $115 million by

2020 (Preker, Lindner, Chernichovsky &

Schellekens, 2013)

January, 2018 Ministerial Advisory Committee was established

on costs that were Out-of-the-Pocket.

February, 2018

Most of the benefits, around 80% of the total

benefits, that were listed in the Prostheses List in

the year 2018 were reduced. There was around

50% degradation in the performance of the

superior clinics in hip as well as knee implants.

Superior Clinical Performance (SCP) had been

greatly reduced. An establishment for a

committee to improve mental health treatment in

Australia was drafted SAGE Journals: Your

gateway to world-class journal research (s & s

5PRIVATE HEALTH INSURANCE 2017 REFORMS

2018).

March, 2018

Draft of exposure for the legislative tasks was

released for consultation with the public

Parliament used legislation in order to support:

- Benefits in travel as well as

accommodation for rural and regional

trips.

- Attractive prices for younger people.

- Changes in the provision of standard

information provision

Recovery of costs for tier two eligible users.

April, 2018

Waiting period for the mental health rules came

into effect.

End of May, 2018

Exposure for the rules was drafted and its release

awaited consultation.

June, 2018

The legislation was passed and rules were made

to:

- Define and implement the standard

clinical definitions of

Gold/Silver/Bronze/Basic categories and

implement newer information provisions

- Removal of benefits for natural

2018).

March, 2018

Draft of exposure for the legislative tasks was

released for consultation with the public

Parliament used legislation in order to support:

- Benefits in travel as well as

accommodation for rural and regional

trips.

- Attractive prices for younger people.

- Changes in the provision of standard

information provision

Recovery of costs for tier two eligible users.

April, 2018

Waiting period for the mental health rules came

into effect.

End of May, 2018

Exposure for the rules was drafted and its release

awaited consultation.

June, 2018

The legislation was passed and rules were made

to:

- Define and implement the standard

clinical definitions of

Gold/Silver/Bronze/Basic categories and

implement newer information provisions

- Removal of benefits for natural

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

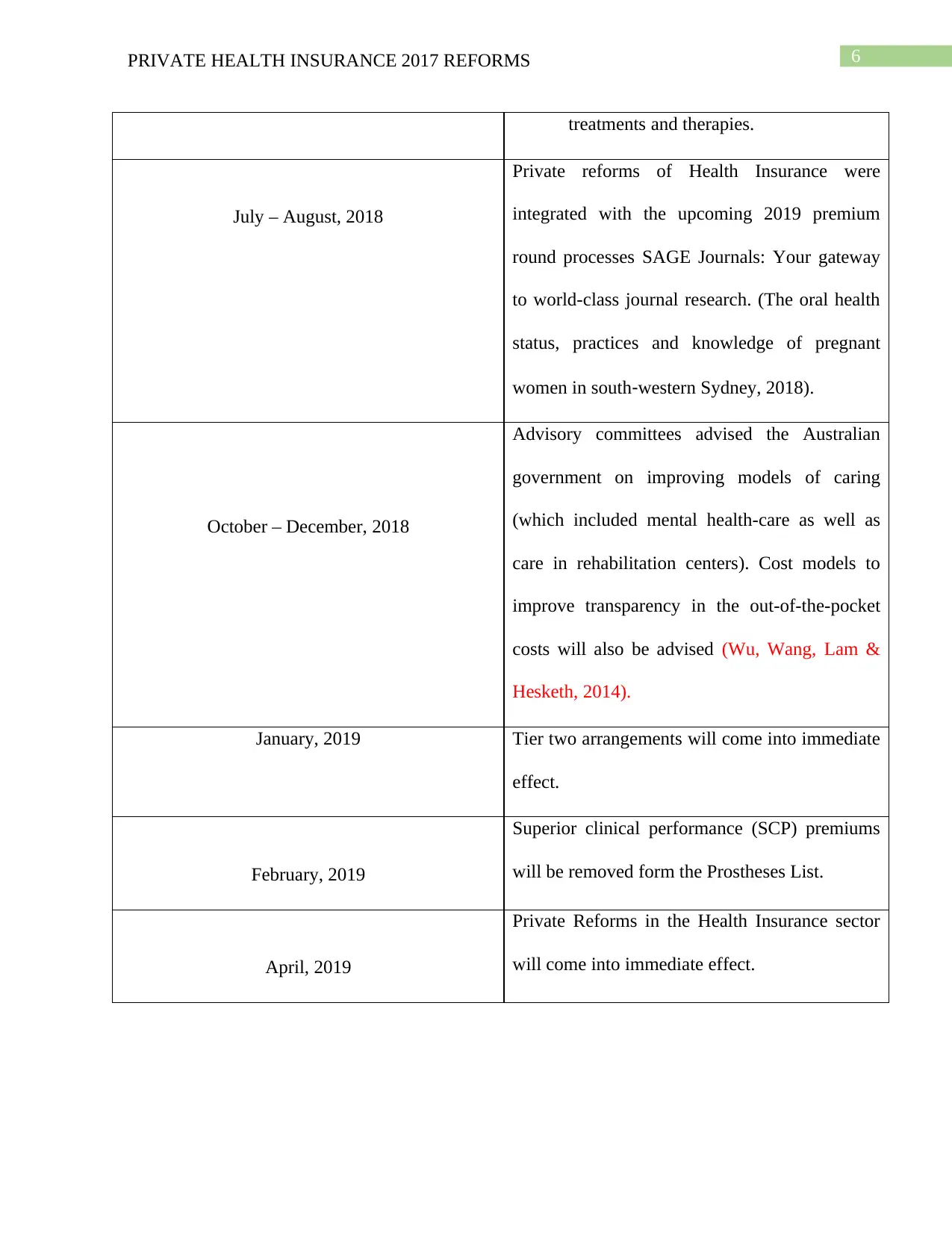

6PRIVATE HEALTH INSURANCE 2017 REFORMS

treatments and therapies.

July – August, 2018

Private reforms of Health Insurance were

integrated with the upcoming 2019 premium

round processes SAGE Journals: Your gateway

to world-class journal research. (The oral health

status, practices and knowledge of pregnant

women in south‐western Sydney, 2018).

October – December, 2018

Advisory committees advised the Australian

government on improving models of caring

(which included mental health-care as well as

care in rehabilitation centers). Cost models to

improve transparency in the out-of-the-pocket

costs will also be advised (Wu, Wang, Lam &

Hesketh, 2014).

January, 2019 Tier two arrangements will come into immediate

effect.

February, 2019

Superior clinical performance (SCP) premiums

will be removed form the Prostheses List.

April, 2019

Private Reforms in the Health Insurance sector

will come into immediate effect.

treatments and therapies.

July – August, 2018

Private reforms of Health Insurance were

integrated with the upcoming 2019 premium

round processes SAGE Journals: Your gateway

to world-class journal research. (The oral health

status, practices and knowledge of pregnant

women in south‐western Sydney, 2018).

October – December, 2018

Advisory committees advised the Australian

government on improving models of caring

(which included mental health-care as well as

care in rehabilitation centers). Cost models to

improve transparency in the out-of-the-pocket

costs will also be advised (Wu, Wang, Lam &

Hesketh, 2014).

January, 2019 Tier two arrangements will come into immediate

effect.

February, 2019

Superior clinical performance (SCP) premiums

will be removed form the Prostheses List.

April, 2019

Private Reforms in the Health Insurance sector

will come into immediate effect.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7PRIVATE HEALTH INSURANCE 2017 REFORMS

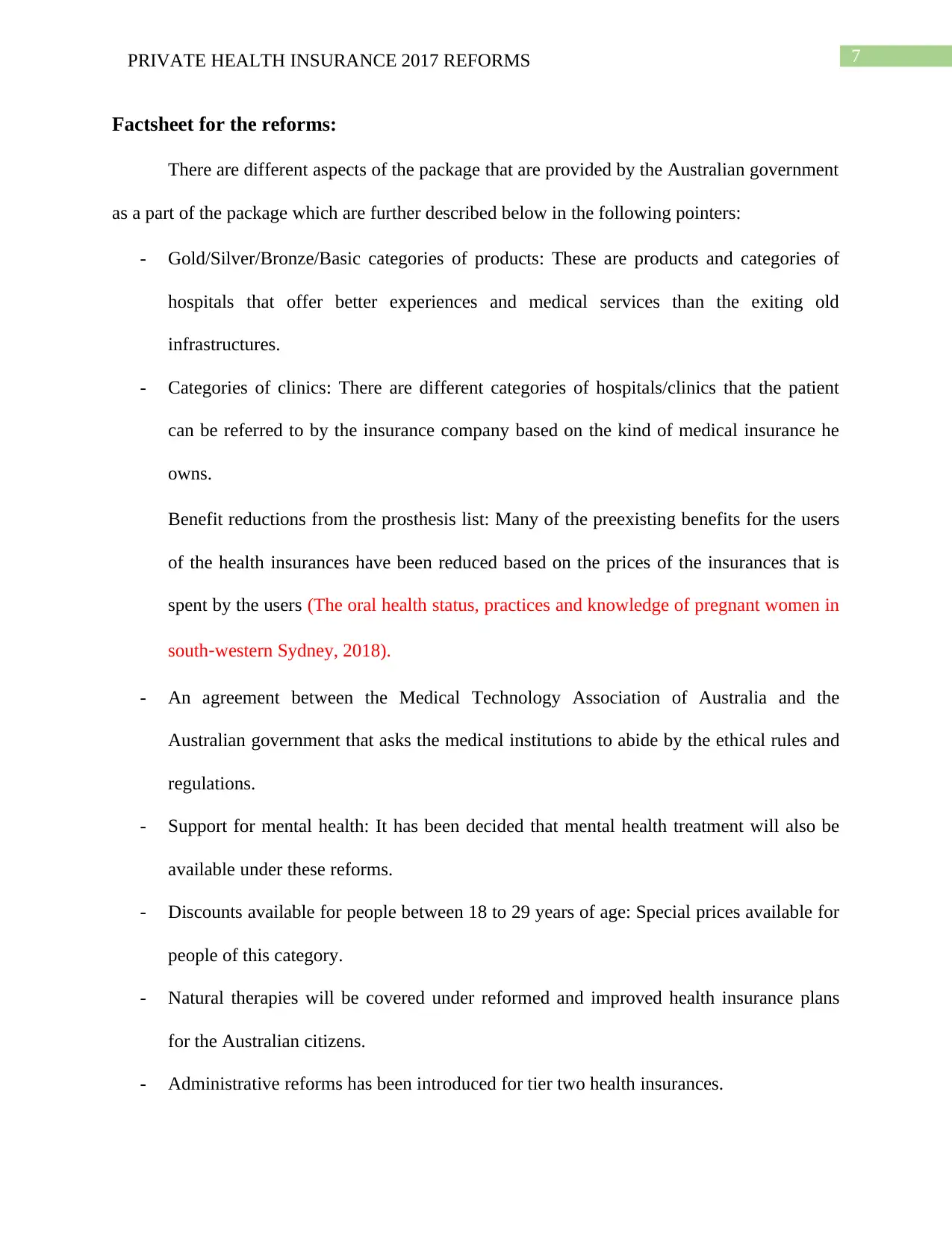

Factsheet for the reforms:

There are different aspects of the package that are provided by the Australian government

as a part of the package which are further described below in the following pointers:

- Gold/Silver/Bronze/Basic categories of products: These are products and categories of

hospitals that offer better experiences and medical services than the exiting old

infrastructures.

- Categories of clinics: There are different categories of hospitals/clinics that the patient

can be referred to by the insurance company based on the kind of medical insurance he

owns.

Benefit reductions from the prosthesis list: Many of the preexisting benefits for the users

of the health insurances have been reduced based on the prices of the insurances that is

spent by the users (The oral health status, practices and knowledge of pregnant women in

south‐western Sydney, 2018).

- An agreement between the Medical Technology Association of Australia and the

Australian government that asks the medical institutions to abide by the ethical rules and

regulations.

- Support for mental health: It has been decided that mental health treatment will also be

available under these reforms.

- Discounts available for people between 18 to 29 years of age: Special prices available for

people of this category.

- Natural therapies will be covered under reformed and improved health insurance plans

for the Australian citizens.

- Administrative reforms has been introduced for tier two health insurances.

Factsheet for the reforms:

There are different aspects of the package that are provided by the Australian government

as a part of the package which are further described below in the following pointers:

- Gold/Silver/Bronze/Basic categories of products: These are products and categories of

hospitals that offer better experiences and medical services than the exiting old

infrastructures.

- Categories of clinics: There are different categories of hospitals/clinics that the patient

can be referred to by the insurance company based on the kind of medical insurance he

owns.

Benefit reductions from the prosthesis list: Many of the preexisting benefits for the users

of the health insurances have been reduced based on the prices of the insurances that is

spent by the users (The oral health status, practices and knowledge of pregnant women in

south‐western Sydney, 2018).

- An agreement between the Medical Technology Association of Australia and the

Australian government that asks the medical institutions to abide by the ethical rules and

regulations.

- Support for mental health: It has been decided that mental health treatment will also be

available under these reforms.

- Discounts available for people between 18 to 29 years of age: Special prices available for

people of this category.

- Natural therapies will be covered under reformed and improved health insurance plans

for the Australian citizens.

- Administrative reforms has been introduced for tier two health insurances.

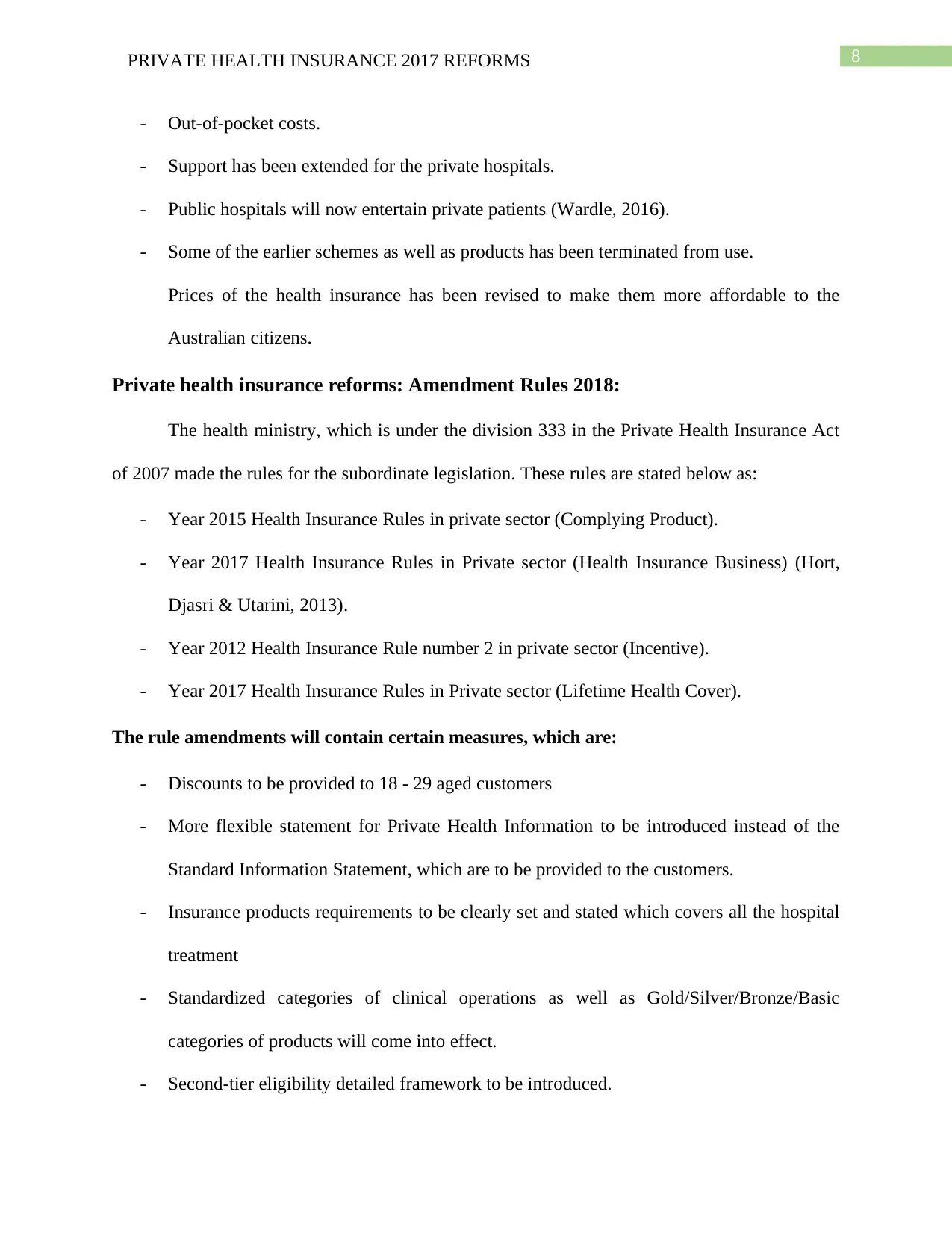

8PRIVATE HEALTH INSURANCE 2017 REFORMS

- Out-of-pocket costs.

- Support has been extended for the private hospitals.

- Public hospitals will now entertain private patients (Wardle, 2016).

- Some of the earlier schemes as well as products has been terminated from use.

Prices of the health insurance has been revised to make them more affordable to the

Australian citizens.

Private health insurance reforms: Amendment Rules 2018:

The health ministry, which is under the division 333 in the Private Health Insurance Act

of 2007 made the rules for the subordinate legislation. These rules are stated below as:

- Year 2015 Health Insurance Rules in private sector (Complying Product).

- Year 2017 Health Insurance Rules in Private sector (Health Insurance Business) (Hort,

Djasri & Utarini, 2013).

- Year 2012 Health Insurance Rule number 2 in private sector (Incentive).

- Year 2017 Health Insurance Rules in Private sector (Lifetime Health Cover).

The rule amendments will contain certain measures, which are:

- Discounts to be provided to 18 - 29 aged customers

- More flexible statement for Private Health Information to be introduced instead of the

Standard Information Statement, which are to be provided to the customers.

- Insurance products requirements to be clearly set and stated which covers all the hospital

treatment

- Standardized categories of clinical operations as well as Gold/Silver/Bronze/Basic

categories of products will come into effect.

- Second-tier eligibility detailed framework to be introduced.

- Out-of-pocket costs.

- Support has been extended for the private hospitals.

- Public hospitals will now entertain private patients (Wardle, 2016).

- Some of the earlier schemes as well as products has been terminated from use.

Prices of the health insurance has been revised to make them more affordable to the

Australian citizens.

Private health insurance reforms: Amendment Rules 2018:

The health ministry, which is under the division 333 in the Private Health Insurance Act

of 2007 made the rules for the subordinate legislation. These rules are stated below as:

- Year 2015 Health Insurance Rules in private sector (Complying Product).

- Year 2017 Health Insurance Rules in Private sector (Health Insurance Business) (Hort,

Djasri & Utarini, 2013).

- Year 2012 Health Insurance Rule number 2 in private sector (Incentive).

- Year 2017 Health Insurance Rules in Private sector (Lifetime Health Cover).

The rule amendments will contain certain measures, which are:

- Discounts to be provided to 18 - 29 aged customers

- More flexible statement for Private Health Information to be introduced instead of the

Standard Information Statement, which are to be provided to the customers.

- Insurance products requirements to be clearly set and stated which covers all the hospital

treatment

- Standardized categories of clinical operations as well as Gold/Silver/Bronze/Basic

categories of products will come into effect.

- Second-tier eligibility detailed framework to be introduced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9PRIVATE HEALTH INSURANCE 2017 REFORMS

- Natural therapies coverage has to be removed.

- Clarify the protection schemes to be clarified to the customers (Hall, 2015).

Impact of removing the policy restrictions:

Around 25% of users who have insurance coverage for private hospitals insurance

purchase restricted coverage plans which are applied to other categories other than psychiatric

care in hospitals, rehabilitation as well as care in the palliative unit.Proposals were no longer

considered to allow the different insurers in private health sector to offer restricted coverage for

other categories of clinical benefits. Categories such as psychiatric care, palliative care as well as

rehabilitation were only allowed. Modelling in the Deloitte’s format shows that restrictions

removal would help in increasing the rate of draw for medium level products by around 10%,

which would in turn be converted to the premium channels (Willis, Reynolds & Keleher, 2016).

The Ombudsman of health insurance in the private sector has said that restrictions

removal can be harmful since, as it would be removing the access to choose doctors. The

prosthesis benefits of the present insurance holders would also be affected under this scheme.

Its importance lies in the fact that, people residing in the rural areas where it is difficult to access

the private hospitals will have the flexibility and provisions to now access them more easily and

the expenses will be covered under the policy. Retaining restrictions in rehabilitation as well as

palliative care in the Silver, Bronze as well as the Basic tiers, can protect the customers from a

rapid increase in the premium cases. This in turn will protect the policy holders will be protected

from the detrimental changes in the product lines (Osborn, Squires, Doty, Sarnak & Schneider,

2016).

- Natural therapies coverage has to be removed.

- Clarify the protection schemes to be clarified to the customers (Hall, 2015).

Impact of removing the policy restrictions:

Around 25% of users who have insurance coverage for private hospitals insurance

purchase restricted coverage plans which are applied to other categories other than psychiatric

care in hospitals, rehabilitation as well as care in the palliative unit.Proposals were no longer

considered to allow the different insurers in private health sector to offer restricted coverage for

other categories of clinical benefits. Categories such as psychiatric care, palliative care as well as

rehabilitation were only allowed. Modelling in the Deloitte’s format shows that restrictions

removal would help in increasing the rate of draw for medium level products by around 10%,

which would in turn be converted to the premium channels (Willis, Reynolds & Keleher, 2016).

The Ombudsman of health insurance in the private sector has said that restrictions

removal can be harmful since, as it would be removing the access to choose doctors. The

prosthesis benefits of the present insurance holders would also be affected under this scheme.

Its importance lies in the fact that, people residing in the rural areas where it is difficult to access

the private hospitals will have the flexibility and provisions to now access them more easily and

the expenses will be covered under the policy. Retaining restrictions in rehabilitation as well as

palliative care in the Silver, Bronze as well as the Basic tiers, can protect the customers from a

rapid increase in the premium cases. This in turn will protect the policy holders will be protected

from the detrimental changes in the product lines (Osborn, Squires, Doty, Sarnak & Schneider,

2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10PRIVATE HEALTH INSURANCE 2017 REFORMS

Improved protection for consumers and terminating the policies:

Requirements will be introduced by the Australian government wherein the insurers have

to properly inform the adults and the insurance provider about their possible planes termination

of any particular product or transfer to a new product. Health insurers Australia already have

different kinds of products, which are not available for the new policyholders, and they should be

able to decide whether to make them available to the new policyholders to ensure a flexibility in

their working. The policyholders should also be able to decide if they want to close an old

existing product (Mossialos, Wenzl, Osborn & Sarnak, 2016).

If an insurer does not want to terminate a product, the following has to be provided

by them:

- New policy details

- Difference amount between the terminating and the new policy opted has to be paid.

- Relevant details about waiting periods relevant details that apply for the new product has

to be considered by the user.

It is important since a transparency will be maintained at the time of transfer of policy. The users

will be informed that not all aspects of the old policy will be covered under the new one.

Consumers will be immensely benefitted from this scheme since they will have a clear

understanding of the new policy and will have the provision to decide whether to transfer their

policies. This will also help the consumers to compare the different health insurance policies and

understand in details about the coverage they offer before choosing a particular product (Schoen,

Osborn, Squires, & Doty, 2013).

Improved protection for consumers and terminating the policies:

Requirements will be introduced by the Australian government wherein the insurers have

to properly inform the adults and the insurance provider about their possible planes termination

of any particular product or transfer to a new product. Health insurers Australia already have

different kinds of products, which are not available for the new policyholders, and they should be

able to decide whether to make them available to the new policyholders to ensure a flexibility in

their working. The policyholders should also be able to decide if they want to close an old

existing product (Mossialos, Wenzl, Osborn & Sarnak, 2016).

If an insurer does not want to terminate a product, the following has to be provided

by them:

- New policy details

- Difference amount between the terminating and the new policy opted has to be paid.

- Relevant details about waiting periods relevant details that apply for the new product has

to be considered by the user.

It is important since a transparency will be maintained at the time of transfer of policy. The users

will be informed that not all aspects of the old policy will be covered under the new one.

Consumers will be immensely benefitted from this scheme since they will have a clear

understanding of the new policy and will have the provision to decide whether to transfer their

policies. This will also help the consumers to compare the different health insurance policies and

understand in details about the coverage they offer before choosing a particular product (Schoen,

Osborn, Squires, & Doty, 2013).

11PRIVATE HEALTH INSURANCE 2017 REFORMS

Legislative amendments:

On the 28th of March 2018, three bills were introduced in form of a package and was

presented to the parliament. It implemented certain reforms to make the health insurances

simpler as well as affordable for the customers:

- Amendment Bill of legislation in the Health Insurance of private sector in the year 2018.

- A Newer Taxation System, which was the amendment of the Medicare levy surcharge –

benefits and passing of the “private health insurance policies excess levels” bill in the

year 2018 (Mason, 2013).

- Medicare Levy Amendment for Medicare, which was the “private health insurance

policies excess levels”, Bill passed in the year 2018.

The Amendment Bill of Legislation in the Private sector of Health Insurance of 2018

contains some primary amendments. It is expected that the senate will support them in the

Parliamentary sitting of 2018 spring. Some of these amendments are:

- Strengthening of the powers held by the Ombudsman of the Health Insurance in the

Private sector.

- Better access to travel as well as accommodation benefits for the users.

- improving transparency in providing information to the consumers

- Offering discounts to users of age group of 18-29 (Li & Powdthavee, 2015).

Low priced health insurance products in the private segment:

Low priced products that are low priced play an important role in health insurance of

private segment which are rated by the community since it is beneficial for the users who have a

fixed income. It is also helpful for people wanting to have access to private medical institutions

from rural and interior areas. Users aged between 18-29 have the provision to purchase low

Legislative amendments:

On the 28th of March 2018, three bills were introduced in form of a package and was

presented to the parliament. It implemented certain reforms to make the health insurances

simpler as well as affordable for the customers:

- Amendment Bill of legislation in the Health Insurance of private sector in the year 2018.

- A Newer Taxation System, which was the amendment of the Medicare levy surcharge –

benefits and passing of the “private health insurance policies excess levels” bill in the

year 2018 (Mason, 2013).

- Medicare Levy Amendment for Medicare, which was the “private health insurance

policies excess levels”, Bill passed in the year 2018.

The Amendment Bill of Legislation in the Private sector of Health Insurance of 2018

contains some primary amendments. It is expected that the senate will support them in the

Parliamentary sitting of 2018 spring. Some of these amendments are:

- Strengthening of the powers held by the Ombudsman of the Health Insurance in the

Private sector.

- Better access to travel as well as accommodation benefits for the users.

- improving transparency in providing information to the consumers

- Offering discounts to users of age group of 18-29 (Li & Powdthavee, 2015).

Low priced health insurance products in the private segment:

Low priced products that are low priced play an important role in health insurance of

private segment which are rated by the community since it is beneficial for the users who have a

fixed income. It is also helpful for people wanting to have access to private medical institutions

from rural and interior areas. Users aged between 18-29 have the provision to purchase low

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.