BAO5524 Professional Auditing: Financial Audit of Pro Medicus Ltd

VerifiedAdded on 2022/08/20

|17

|4440

|13

Report

AI Summary

This report provides an analysis of Pro Medicus Ltd's financial statements from an auditing perspective, focusing on identifying key accounts susceptible to material misstatement. It references ASA 210 regarding audit engagement terms and ASA 300 for audit planning, including risk assessment and the collection of audit evidence. The report also discusses the concept of materiality, following ASA 320, and includes a computation of planning materiality. Key accounts like cost of sales, foreign currency gains/losses, receivables, accrued revenue, deferred tax assets, intangible assets, payables and share reserves are assessed for risk. The analysis concludes by considering the potential impact of identified risks on the company's financial position.

ASSIGNMENT

BAO5524 PROFESSIONAL AUDITING

REPORT

Penalty

- Exceeding the 3000 words limit: TWO (2) marks deduction.

- Exceeding the 30% similarity index limit: FOUR (4) marks deduction.

- Late submission: TWO (2) marks deduction per day including weekend.

Plagiarism

Plagiarism is defined as presenting someone else’s work, including the work of

other students, as one’s own. Any ideas or materials taken from another source

for either written or oral use must be fully acknowledged, unless the

information is common knowledge. All students are strongly advised to do the

following:

- goto http://wcf.vu.edu.au/GovernancePolicy/PDF/POA040915000.PDF

BAO5524 PROFESSIONAL AUDITING

REPORT

Penalty

- Exceeding the 3000 words limit: TWO (2) marks deduction.

- Exceeding the 30% similarity index limit: FOUR (4) marks deduction.

- Late submission: TWO (2) marks deduction per day including weekend.

Plagiarism

Plagiarism is defined as presenting someone else’s work, including the work of

other students, as one’s own. Any ideas or materials taken from another source

for either written or oral use must be fully acknowledged, unless the

information is common knowledge. All students are strongly advised to do the

following:

- goto http://wcf.vu.edu.au/GovernancePolicy/PDF/POA040915000.PDF

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- enter School of Accounting and Finance

- enter Student Resources

- read the PLAGIARISM POLICY.

Semester TRI3_ 2019

1. Executive summary

The assessment would be analysing the financial statements of Pro Medicus Ltd

which is engaged in imaging and medical management. The assessment would be

considering auditing aspect for the business and therefore would be identifying key

accounts which are shown in the financial statement of the company. The auditor

would be assessing the audit engagement by referring to the “ASA 210 Agreeing the

Terms of Audit Engagements” before accepting the audit of the business. The auditor

would be planning the audit procedures step by step considering the past trends and

this is done referring to “ASA 300 Planning an Audit of a Financial Report”. The

auditor would be assessing the risks which are associated with the business and also

point out steps which the auditor would be taking for collecting appropriate audit

evidences. The aspect of materiality would be considered for the purpose assessing

the risks which is associated with the business and therefore the provisions of “ASA

320 Materiality in Planning and Performing an Audit” would be followed. In

addition to this, the analysis would also be showing computation of planning

materiality for the business on the basis of which risk assessment would be done by

the auditor of the business. The assumptions which is considered by the senior

management for computing the planning materiality is also shown in the discussion

below. Furthermore, the analysis would also be presenting the impacts of the risks

accounts which have been identified earlier in the financial position of the business.

- enter Student Resources

- read the PLAGIARISM POLICY.

Semester TRI3_ 2019

1. Executive summary

The assessment would be analysing the financial statements of Pro Medicus Ltd

which is engaged in imaging and medical management. The assessment would be

considering auditing aspect for the business and therefore would be identifying key

accounts which are shown in the financial statement of the company. The auditor

would be assessing the audit engagement by referring to the “ASA 210 Agreeing the

Terms of Audit Engagements” before accepting the audit of the business. The auditor

would be planning the audit procedures step by step considering the past trends and

this is done referring to “ASA 300 Planning an Audit of a Financial Report”. The

auditor would be assessing the risks which are associated with the business and also

point out steps which the auditor would be taking for collecting appropriate audit

evidences. The aspect of materiality would be considered for the purpose assessing

the risks which is associated with the business and therefore the provisions of “ASA

320 Materiality in Planning and Performing an Audit” would be followed. In

addition to this, the analysis would also be showing computation of planning

materiality for the business on the basis of which risk assessment would be done by

the auditor of the business. The assumptions which is considered by the senior

management for computing the planning materiality is also shown in the discussion

below. Furthermore, the analysis would also be presenting the impacts of the risks

accounts which have been identified earlier in the financial position of the business.

2. Introduction

The main purpose of the assessment is to conduct an analysis on Pro Medicus

Company which is engaged in providing radiology information systems (RIS), Picture

Archiving and Communication Systems (PACS). The analysis would be conducted

from the perspective of audit and therefore the annual report of the company would be

considered for 2018 to check if everything is reported fairly and also identify accounts

which can be subjected to risks (Mio 2013). The different accounts which are

susceptible to risks of material misstatement would be identified. The audit

procedures which can be undertaken by the business would also be stated in details in

the assessment. The analysis would also be showing the level of risks which the

auditor would be facing while formulating an opinion on the financial presentation of

the company. In accordance with the provisions of “Para 9 of ASA 210 Agreeing the

Terms of Audit Engagements”, the auditor needs to agree to the terms and conditions

of the audit engagement with the management of the company. In the case of Pro

Medicus, the external auditor is in agreement with those charged with governance in

regards to the audit fee which is to be charged by the auditor and the same is set to be

$ 130,000. The terms of audit engagement has also been made clear in the audit

engagement letter which is provided by the auditor.

In order to effectively conduct audit for the business, proper planning and

strategy formulation is an important step which needs to be undertaken by the external

auditor. As per “Para 7 of ASA 300 Planning an Audit of a Financial Report”, an

effective strategy needs to be formulated or planned beforehand regarding the

procedures which is to be applied by the auditor and which accounts needs to be

analysed in details (Auasb.gov.au. 2020). The standard also states the timing, extent

and nature of audit evidences which needs to be collected for identifying material

misstatements. The audit evidences would give an idea regarding the overall risks

which is faced by the business and accordingly the auditor would provide his opinion

on thee presented annual report. The analysis would also be showing the estimation of

planning materiality for the business and how the same would assist in collection of

audit evidences. Further the assessment would be showing the impacts of the

identified risks accounts for the business.

The main purpose of the assessment is to conduct an analysis on Pro Medicus

Company which is engaged in providing radiology information systems (RIS), Picture

Archiving and Communication Systems (PACS). The analysis would be conducted

from the perspective of audit and therefore the annual report of the company would be

considered for 2018 to check if everything is reported fairly and also identify accounts

which can be subjected to risks (Mio 2013). The different accounts which are

susceptible to risks of material misstatement would be identified. The audit

procedures which can be undertaken by the business would also be stated in details in

the assessment. The analysis would also be showing the level of risks which the

auditor would be facing while formulating an opinion on the financial presentation of

the company. In accordance with the provisions of “Para 9 of ASA 210 Agreeing the

Terms of Audit Engagements”, the auditor needs to agree to the terms and conditions

of the audit engagement with the management of the company. In the case of Pro

Medicus, the external auditor is in agreement with those charged with governance in

regards to the audit fee which is to be charged by the auditor and the same is set to be

$ 130,000. The terms of audit engagement has also been made clear in the audit

engagement letter which is provided by the auditor.

In order to effectively conduct audit for the business, proper planning and

strategy formulation is an important step which needs to be undertaken by the external

auditor. As per “Para 7 of ASA 300 Planning an Audit of a Financial Report”, an

effective strategy needs to be formulated or planned beforehand regarding the

procedures which is to be applied by the auditor and which accounts needs to be

analysed in details (Auasb.gov.au. 2020). The standard also states the timing, extent

and nature of audit evidences which needs to be collected for identifying material

misstatements. The audit evidences would give an idea regarding the overall risks

which is faced by the business and accordingly the auditor would provide his opinion

on thee presented annual report. The analysis would also be showing the estimation of

planning materiality for the business and how the same would assist in collection of

audit evidences. Further the assessment would be showing the impacts of the

identified risks accounts for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Key information

a) Our understanding of the client

The business of Pro Medicus is considered for the purpose of analysis and the

same would be conducted from the perspective of audit of a business. The

company is known to provide IT solutions and radiology information system. The

company has experience in assisting the clients perform medical care for patients

and the business also streamlined healthcare management practices for the benefit

of its customers. The strength of the business is client visualization and providing

useful information which is considered to be best provided service by the

company (Promed.com.au. 2020). The company has recently listed in ASX for the

purpose of expanding its market value and thereby achieving more growth in its

operations. In order to understand the reporting framework which is followed by

the business, the annual report of the company would be considered for the year

2018. The different items which are recorded would be analysed so that any risk

which may be present can be identified. It is important to know regarding the

nature of operations of the client mainly because of ensuring that the entity has

followed all legal regulations which is applicable to the business as per the

requirements of “ASA 250 Consideration of Laws and Regulations in an Audit

of a Financial Report”. This is one of the criteria which are followed by the

auditor before he accepts the audit of the company.

As per the provisions which are stated in ASA 315, the auditor needs to

appropriately consider the business environment and the nature of operations

before commencing the audit for the company. This is considered to be important

as the same gives insights to the auditor regarding the important matters which are

material (Auasb.gov.au. 2020). The auditor needs to gain ample knowledge of the

workings of the business and also in the process identifies key accounts which are

most susceptible to risks of misstatement. Furthermore, an understanding of the

nature of the operations of business also assists the auditor in documentation

process as per “ASA 230 Audit Documentation” which is considered to be

important for future reference.

b) Our assessment of significant accounts

The financial statements of Pro Medicus are considered for the identification

of key accounts which can have material misstatement affecting the financial

position of the business as a whole. In order to identify key items from the

financial statements, the concept of materiality should be given importance

(Baldacchino, Tabone and Demanuele 2017). As per “Para 5 of ASA 320

Materiality in Planning and Performing an Audit”, the concept of materiality is

not only important in the planning stage but also in the stage of performing the

audit as the same guides the auditor regarding which items are material and where

more audit procedures would be applicable (Auasb.gov.au. 2020). In order to

assess the materiality for any items, the professional judgement of the auditor is

applicable on the basis of which performance materiality would be computed.

The key accounts which are considered for the purpose of risk assessment

considering the provisions of ASA 320 are provided below in table format:

Account Name Movements Type of Risk

Cost of Sales Declined in comparison

to previous year

The auditor needs to

assess the reason for the

a) Our understanding of the client

The business of Pro Medicus is considered for the purpose of analysis and the

same would be conducted from the perspective of audit of a business. The

company is known to provide IT solutions and radiology information system. The

company has experience in assisting the clients perform medical care for patients

and the business also streamlined healthcare management practices for the benefit

of its customers. The strength of the business is client visualization and providing

useful information which is considered to be best provided service by the

company (Promed.com.au. 2020). The company has recently listed in ASX for the

purpose of expanding its market value and thereby achieving more growth in its

operations. In order to understand the reporting framework which is followed by

the business, the annual report of the company would be considered for the year

2018. The different items which are recorded would be analysed so that any risk

which may be present can be identified. It is important to know regarding the

nature of operations of the client mainly because of ensuring that the entity has

followed all legal regulations which is applicable to the business as per the

requirements of “ASA 250 Consideration of Laws and Regulations in an Audit

of a Financial Report”. This is one of the criteria which are followed by the

auditor before he accepts the audit of the company.

As per the provisions which are stated in ASA 315, the auditor needs to

appropriately consider the business environment and the nature of operations

before commencing the audit for the company. This is considered to be important

as the same gives insights to the auditor regarding the important matters which are

material (Auasb.gov.au. 2020). The auditor needs to gain ample knowledge of the

workings of the business and also in the process identifies key accounts which are

most susceptible to risks of misstatement. Furthermore, an understanding of the

nature of the operations of business also assists the auditor in documentation

process as per “ASA 230 Audit Documentation” which is considered to be

important for future reference.

b) Our assessment of significant accounts

The financial statements of Pro Medicus are considered for the identification

of key accounts which can have material misstatement affecting the financial

position of the business as a whole. In order to identify key items from the

financial statements, the concept of materiality should be given importance

(Baldacchino, Tabone and Demanuele 2017). As per “Para 5 of ASA 320

Materiality in Planning and Performing an Audit”, the concept of materiality is

not only important in the planning stage but also in the stage of performing the

audit as the same guides the auditor regarding which items are material and where

more audit procedures would be applicable (Auasb.gov.au. 2020). In order to

assess the materiality for any items, the professional judgement of the auditor is

applicable on the basis of which performance materiality would be computed.

The key accounts which are considered for the purpose of risk assessment

considering the provisions of ASA 320 are provided below in table format:

Account Name Movements Type of Risk

Cost of Sales Declined in comparison

to previous year

The auditor needs to

assess the reason for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

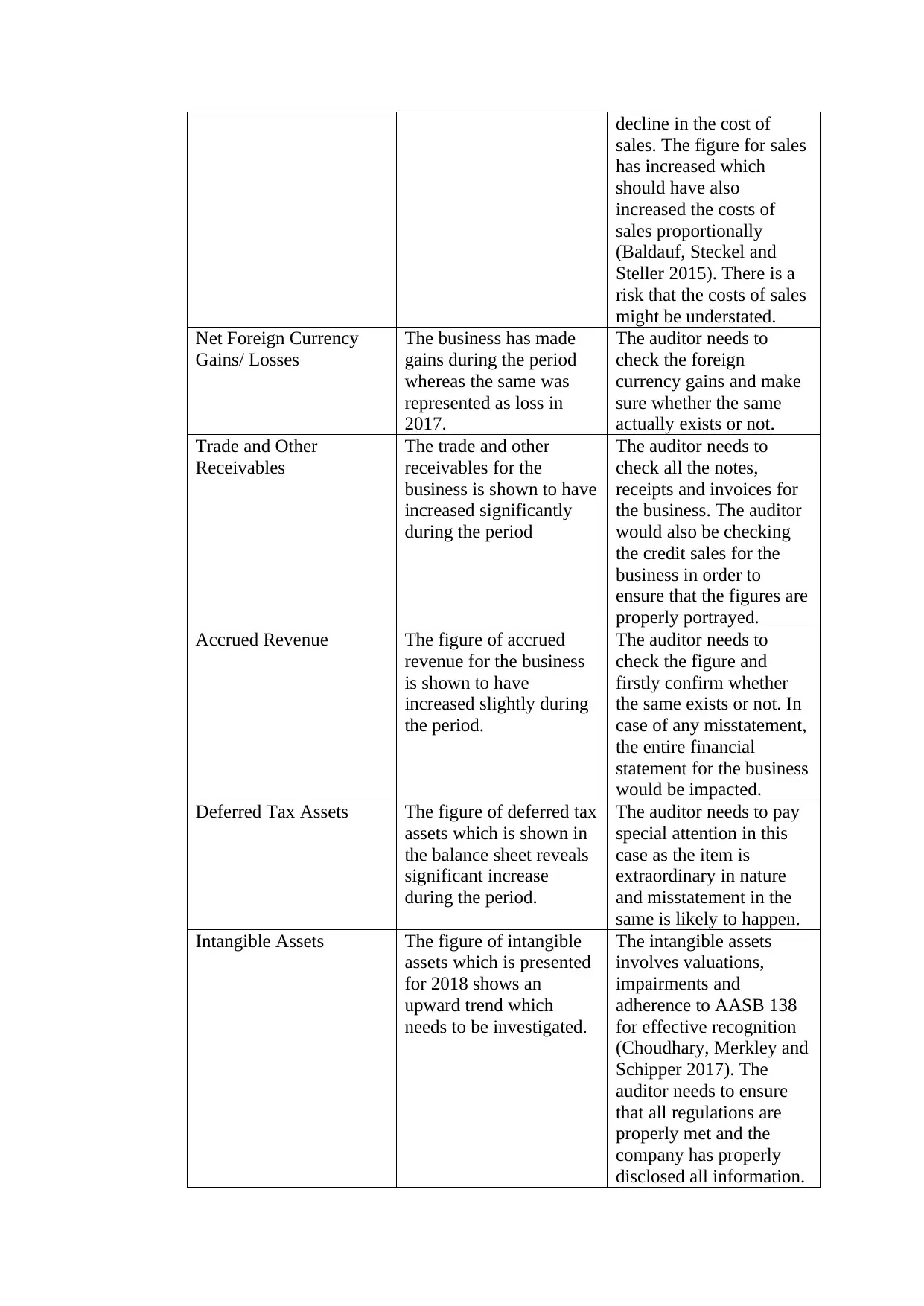

decline in the cost of

sales. The figure for sales

has increased which

should have also

increased the costs of

sales proportionally

(Baldauf, Steckel and

Steller 2015). There is a

risk that the costs of sales

might be understated.

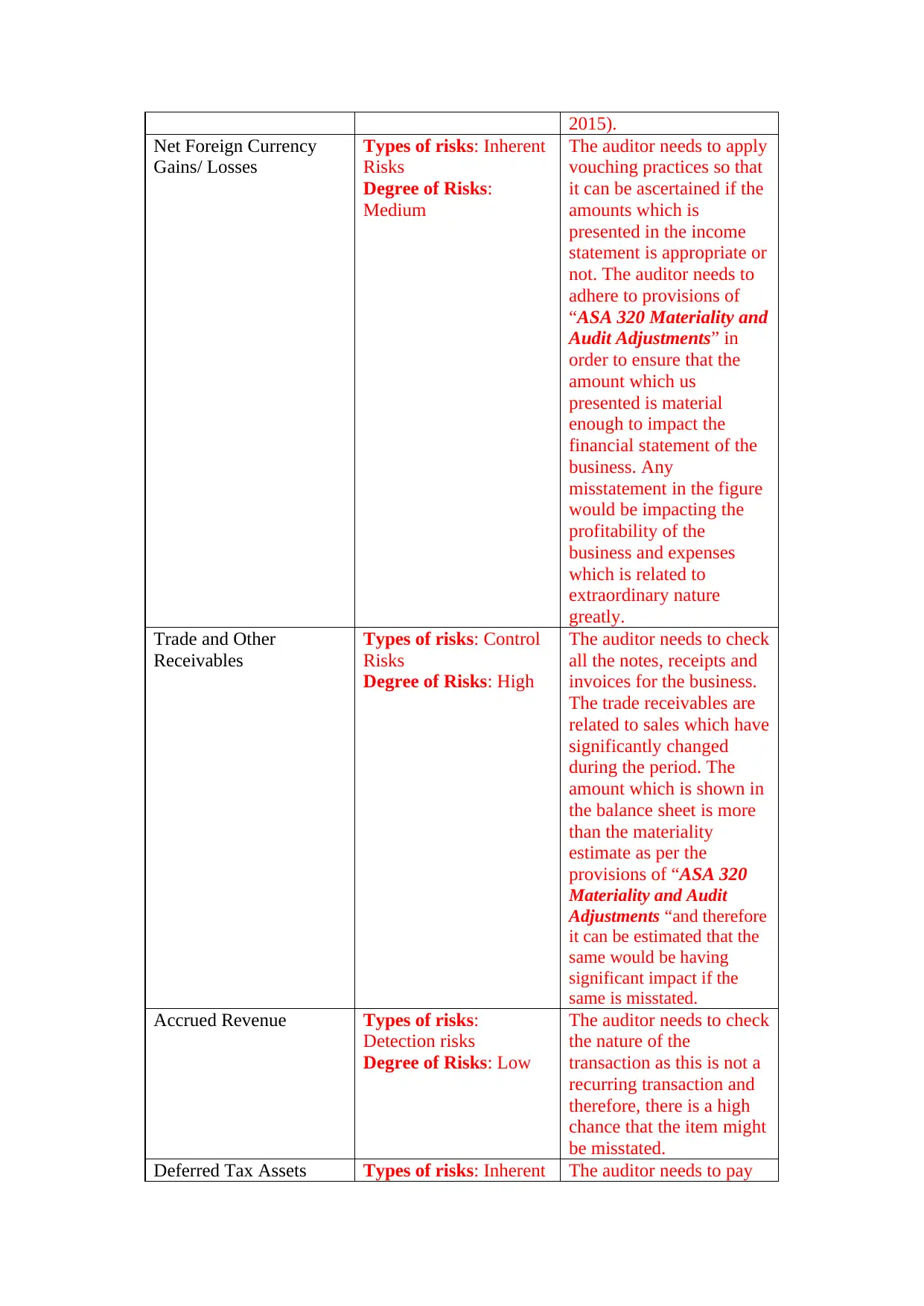

Net Foreign Currency

Gains/ Losses

The business has made

gains during the period

whereas the same was

represented as loss in

2017.

The auditor needs to

check the foreign

currency gains and make

sure whether the same

actually exists or not.

Trade and Other

Receivables

The trade and other

receivables for the

business is shown to have

increased significantly

during the period

The auditor needs to

check all the notes,

receipts and invoices for

the business. The auditor

would also be checking

the credit sales for the

business in order to

ensure that the figures are

properly portrayed.

Accrued Revenue The figure of accrued

revenue for the business

is shown to have

increased slightly during

the period.

The auditor needs to

check the figure and

firstly confirm whether

the same exists or not. In

case of any misstatement,

the entire financial

statement for the business

would be impacted.

Deferred Tax Assets The figure of deferred tax

assets which is shown in

the balance sheet reveals

significant increase

during the period.

The auditor needs to pay

special attention in this

case as the item is

extraordinary in nature

and misstatement in the

same is likely to happen.

Intangible Assets The figure of intangible

assets which is presented

for 2018 shows an

upward trend which

needs to be investigated.

The intangible assets

involves valuations,

impairments and

adherence to AASB 138

for effective recognition

(Choudhary, Merkley and

Schipper 2017). The

auditor needs to ensure

that all regulations are

properly met and the

company has properly

disclosed all information.

sales. The figure for sales

has increased which

should have also

increased the costs of

sales proportionally

(Baldauf, Steckel and

Steller 2015). There is a

risk that the costs of sales

might be understated.

Net Foreign Currency

Gains/ Losses

The business has made

gains during the period

whereas the same was

represented as loss in

2017.

The auditor needs to

check the foreign

currency gains and make

sure whether the same

actually exists or not.

Trade and Other

Receivables

The trade and other

receivables for the

business is shown to have

increased significantly

during the period

The auditor needs to

check all the notes,

receipts and invoices for

the business. The auditor

would also be checking

the credit sales for the

business in order to

ensure that the figures are

properly portrayed.

Accrued Revenue The figure of accrued

revenue for the business

is shown to have

increased slightly during

the period.

The auditor needs to

check the figure and

firstly confirm whether

the same exists or not. In

case of any misstatement,

the entire financial

statement for the business

would be impacted.

Deferred Tax Assets The figure of deferred tax

assets which is shown in

the balance sheet reveals

significant increase

during the period.

The auditor needs to pay

special attention in this

case as the item is

extraordinary in nature

and misstatement in the

same is likely to happen.

Intangible Assets The figure of intangible

assets which is presented

for 2018 shows an

upward trend which

needs to be investigated.

The intangible assets

involves valuations,

impairments and

adherence to AASB 138

for effective recognition

(Choudhary, Merkley and

Schipper 2017). The

auditor needs to ensure

that all regulations are

properly met and the

company has properly

disclosed all information.

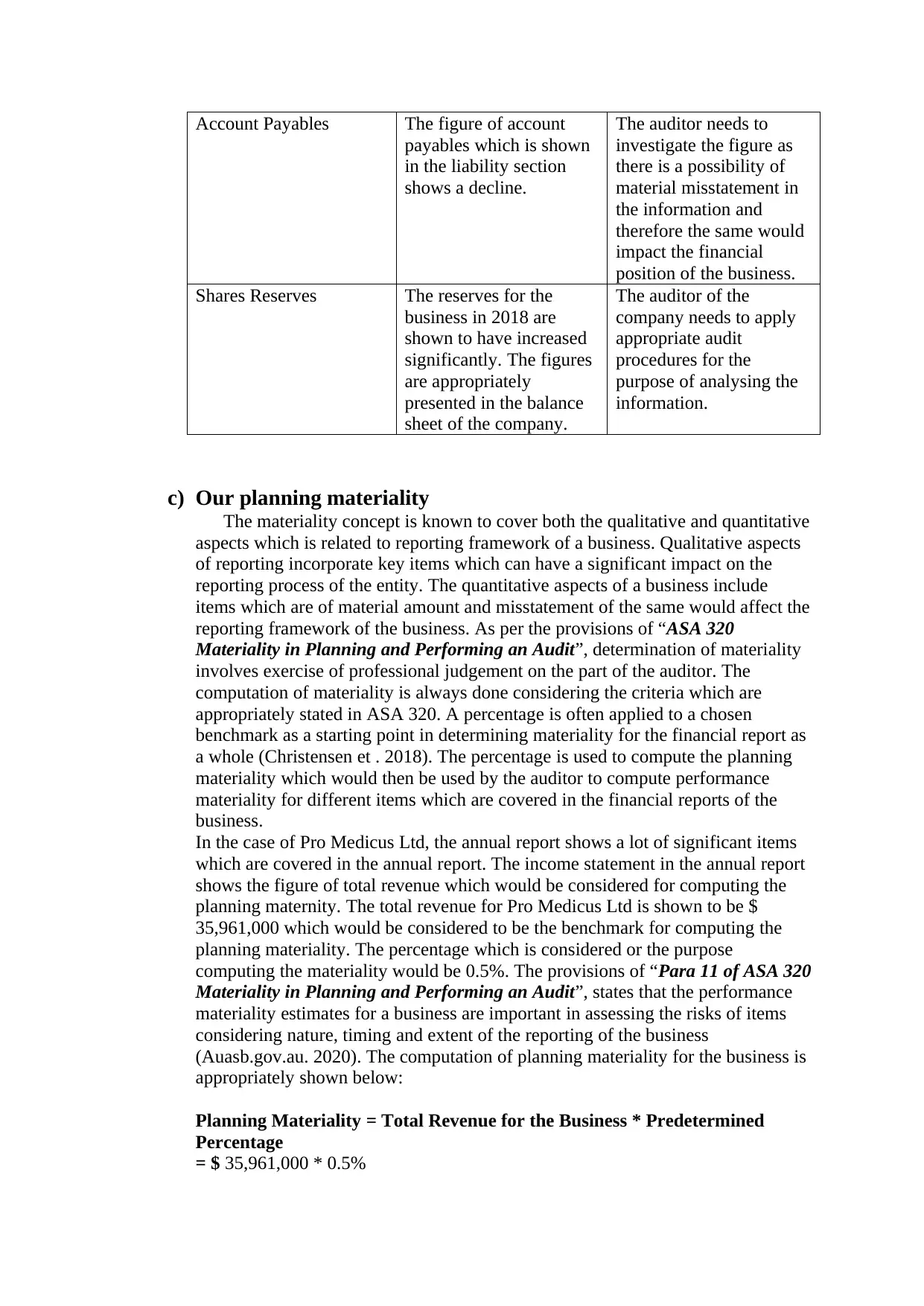

Account Payables The figure of account

payables which is shown

in the liability section

shows a decline.

The auditor needs to

investigate the figure as

there is a possibility of

material misstatement in

the information and

therefore the same would

impact the financial

position of the business.

Shares Reserves The reserves for the

business in 2018 are

shown to have increased

significantly. The figures

are appropriately

presented in the balance

sheet of the company.

The auditor of the

company needs to apply

appropriate audit

procedures for the

purpose of analysing the

information.

c) Our planning materiality

The materiality concept is known to cover both the qualitative and quantitative

aspects which is related to reporting framework of a business. Qualitative aspects

of reporting incorporate key items which can have a significant impact on the

reporting process of the entity. The quantitative aspects of a business include

items which are of material amount and misstatement of the same would affect the

reporting framework of the business. As per the provisions of “ASA 320

Materiality in Planning and Performing an Audit”, determination of materiality

involves exercise of professional judgement on the part of the auditor. The

computation of materiality is always done considering the criteria which are

appropriately stated in ASA 320. A percentage is often applied to a chosen

benchmark as a starting point in determining materiality for the financial report as

a whole (Christensen et . 2018). The percentage is used to compute the planning

materiality which would then be used by the auditor to compute performance

materiality for different items which are covered in the financial reports of the

business.

In the case of Pro Medicus Ltd, the annual report shows a lot of significant items

which are covered in the annual report. The income statement in the annual report

shows the figure of total revenue which would be considered for computing the

planning maternity. The total revenue for Pro Medicus Ltd is shown to be $

35,961,000 which would be considered to be the benchmark for computing the

planning materiality. The percentage which is considered or the purpose

computing the materiality would be 0.5%. The provisions of “Para 11 of ASA 320

Materiality in Planning and Performing an Audit”, states that the performance

materiality estimates for a business are important in assessing the risks of items

considering nature, timing and extent of the reporting of the business

(Auasb.gov.au. 2020). The computation of planning materiality for the business is

appropriately shown below:

Planning Materiality = Total Revenue for the Business * Predetermined

Percentage

= $ 35,961,000 * 0.5%

payables which is shown

in the liability section

shows a decline.

The auditor needs to

investigate the figure as

there is a possibility of

material misstatement in

the information and

therefore the same would

impact the financial

position of the business.

Shares Reserves The reserves for the

business in 2018 are

shown to have increased

significantly. The figures

are appropriately

presented in the balance

sheet of the company.

The auditor of the

company needs to apply

appropriate audit

procedures for the

purpose of analysing the

information.

c) Our planning materiality

The materiality concept is known to cover both the qualitative and quantitative

aspects which is related to reporting framework of a business. Qualitative aspects

of reporting incorporate key items which can have a significant impact on the

reporting process of the entity. The quantitative aspects of a business include

items which are of material amount and misstatement of the same would affect the

reporting framework of the business. As per the provisions of “ASA 320

Materiality in Planning and Performing an Audit”, determination of materiality

involves exercise of professional judgement on the part of the auditor. The

computation of materiality is always done considering the criteria which are

appropriately stated in ASA 320. A percentage is often applied to a chosen

benchmark as a starting point in determining materiality for the financial report as

a whole (Christensen et . 2018). The percentage is used to compute the planning

materiality which would then be used by the auditor to compute performance

materiality for different items which are covered in the financial reports of the

business.

In the case of Pro Medicus Ltd, the annual report shows a lot of significant items

which are covered in the annual report. The income statement in the annual report

shows the figure of total revenue which would be considered for computing the

planning maternity. The total revenue for Pro Medicus Ltd is shown to be $

35,961,000 which would be considered to be the benchmark for computing the

planning materiality. The percentage which is considered or the purpose

computing the materiality would be 0.5%. The provisions of “Para 11 of ASA 320

Materiality in Planning and Performing an Audit”, states that the performance

materiality estimates for a business are important in assessing the risks of items

considering nature, timing and extent of the reporting of the business

(Auasb.gov.au. 2020). The computation of planning materiality for the business is

appropriately shown below:

Planning Materiality = Total Revenue for the Business * Predetermined

Percentage

= $ 35,961,000 * 0.5%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= $ 179,805

The planning materiality for the business is computed above and the same is

shown to be $ 179,805 for the period. This figure would be considered by the

auditor for assessing the performance materiality for the business (Christensen,

Glover and Wood 2013). Any amount which is lower than the figure of planning

materiality would not be considered to be material for the analysis of risks. In

accordance to “Para 5 of ASA 320 Materiality in Planning and Performing an

Audit”, the auditor needs to apply the concept of materiality in both planning and

performing the audit, and in evaluating the effect of identified misstatements on

the audit (Auasb.gov.au. 2020). Therefore, it can be said that the auditor of the

company is accurate in his approach to appropriately portray the computation of

Planning Materiality of the business.

The planning materiality for the business is computed above and the same is

shown to be $ 179,805 for the period. This figure would be considered by the

auditor for assessing the performance materiality for the business (Christensen,

Glover and Wood 2013). Any amount which is lower than the figure of planning

materiality would not be considered to be material for the analysis of risks. In

accordance to “Para 5 of ASA 320 Materiality in Planning and Performing an

Audit”, the auditor needs to apply the concept of materiality in both planning and

performing the audit, and in evaluating the effect of identified misstatements on

the audit (Auasb.gov.au. 2020). Therefore, it can be said that the auditor of the

company is accurate in his approach to appropriately portray the computation of

Planning Materiality of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

d) Our assessment of what can go wrong

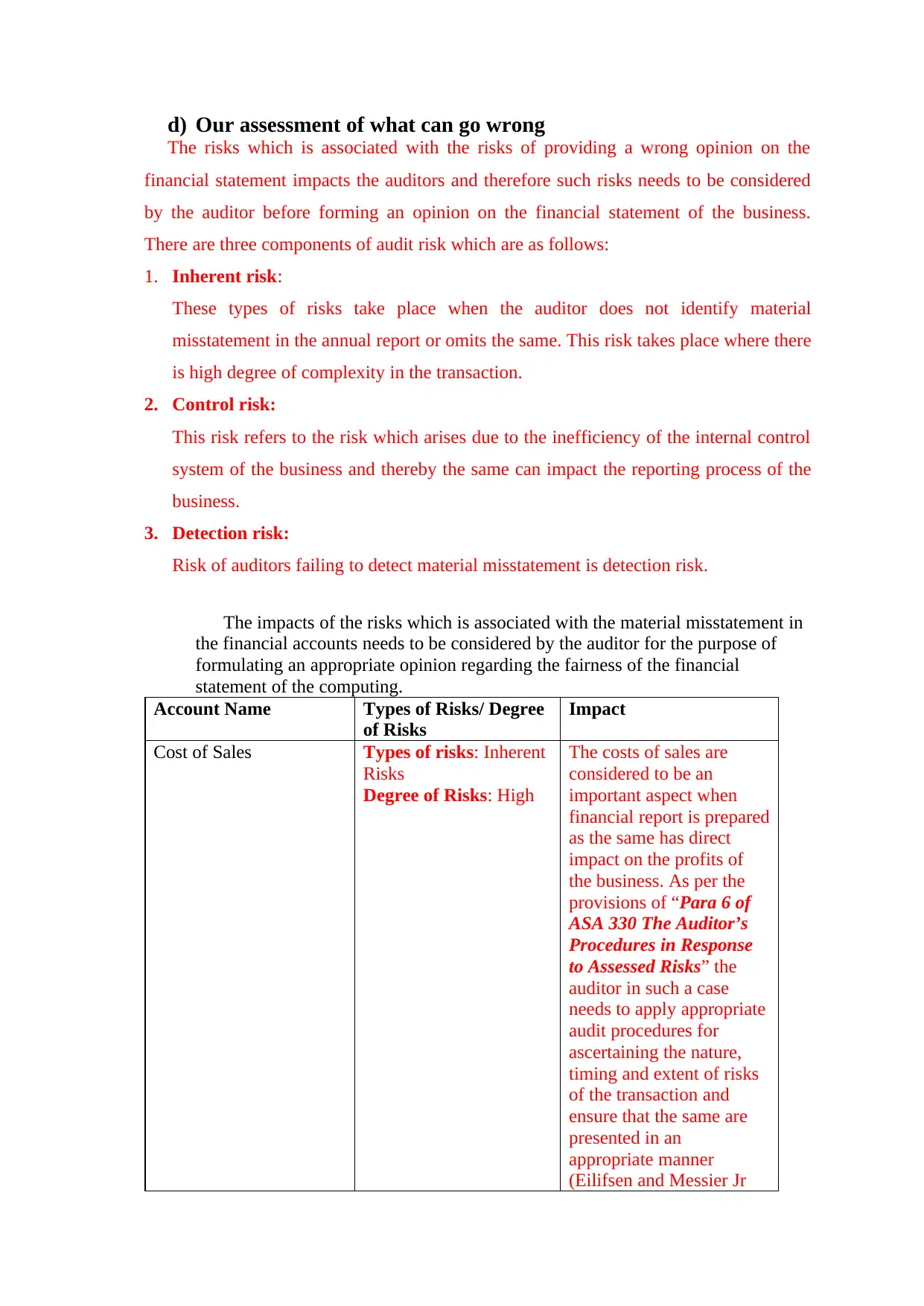

The risks which is associated with the risks of providing a wrong opinion on the

financial statement impacts the auditors and therefore such risks needs to be considered

by the auditor before forming an opinion on the financial statement of the business.

There are three components of audit risk which are as follows:

1. Inherent risk:

These types of risks take place when the auditor does not identify material

misstatement in the annual report or omits the same. This risk takes place where there

is high degree of complexity in the transaction.

2. Control risk:

This risk refers to the risk which arises due to the inefficiency of the internal control

system of the business and thereby the same can impact the reporting process of the

business.

3. Detection risk:

Risk of auditors failing to detect material misstatement is detection risk.

The impacts of the risks which is associated with the material misstatement in

the financial accounts needs to be considered by the auditor for the purpose of

formulating an appropriate opinion regarding the fairness of the financial

statement of the computing.

Account Name Types of Risks/ Degree

of Risks

Impact

Cost of Sales Types of risks: Inherent

Risks

Degree of Risks: High

The costs of sales are

considered to be an

important aspect when

financial report is prepared

as the same has direct

impact on the profits of

the business. As per the

provisions of “Para 6 of

ASA 330 The Auditor’s

Procedures in Response

to Assessed Risks” the

auditor in such a case

needs to apply appropriate

audit procedures for

ascertaining the nature,

timing and extent of risks

of the transaction and

ensure that the same are

presented in an

appropriate manner

(Eilifsen and Messier Jr

The risks which is associated with the risks of providing a wrong opinion on the

financial statement impacts the auditors and therefore such risks needs to be considered

by the auditor before forming an opinion on the financial statement of the business.

There are three components of audit risk which are as follows:

1. Inherent risk:

These types of risks take place when the auditor does not identify material

misstatement in the annual report or omits the same. This risk takes place where there

is high degree of complexity in the transaction.

2. Control risk:

This risk refers to the risk which arises due to the inefficiency of the internal control

system of the business and thereby the same can impact the reporting process of the

business.

3. Detection risk:

Risk of auditors failing to detect material misstatement is detection risk.

The impacts of the risks which is associated with the material misstatement in

the financial accounts needs to be considered by the auditor for the purpose of

formulating an appropriate opinion regarding the fairness of the financial

statement of the computing.

Account Name Types of Risks/ Degree

of Risks

Impact

Cost of Sales Types of risks: Inherent

Risks

Degree of Risks: High

The costs of sales are

considered to be an

important aspect when

financial report is prepared

as the same has direct

impact on the profits of

the business. As per the

provisions of “Para 6 of

ASA 330 The Auditor’s

Procedures in Response

to Assessed Risks” the

auditor in such a case

needs to apply appropriate

audit procedures for

ascertaining the nature,

timing and extent of risks

of the transaction and

ensure that the same are

presented in an

appropriate manner

(Eilifsen and Messier Jr

2015).

Net Foreign Currency

Gains/ Losses

Types of risks: Inherent

Risks

Degree of Risks:

Medium

The auditor needs to apply

vouching practices so that

it can be ascertained if the

amounts which is

presented in the income

statement is appropriate or

not. The auditor needs to

adhere to provisions of

“ASA 320 Materiality and

Audit Adjustments” in

order to ensure that the

amount which us

presented is material

enough to impact the

financial statement of the

business. Any

misstatement in the figure

would be impacting the

profitability of the

business and expenses

which is related to

extraordinary nature

greatly.

Trade and Other

Receivables

Types of risks: Control

Risks

Degree of Risks: High

The auditor needs to check

all the notes, receipts and

invoices for the business.

The trade receivables are

related to sales which have

significantly changed

during the period. The

amount which is shown in

the balance sheet is more

than the materiality

estimate as per the

provisions of “ASA 320

Materiality and Audit

Adjustments “and therefore

it can be estimated that the

same would be having

significant impact if the

same is misstated.

Accrued Revenue Types of risks:

Detection risks

Degree of Risks: Low

The auditor needs to check

the nature of the

transaction as this is not a

recurring transaction and

therefore, there is a high

chance that the item might

be misstated.

Deferred Tax Assets Types of risks: Inherent The auditor needs to pay

Net Foreign Currency

Gains/ Losses

Types of risks: Inherent

Risks

Degree of Risks:

Medium

The auditor needs to apply

vouching practices so that

it can be ascertained if the

amounts which is

presented in the income

statement is appropriate or

not. The auditor needs to

adhere to provisions of

“ASA 320 Materiality and

Audit Adjustments” in

order to ensure that the

amount which us

presented is material

enough to impact the

financial statement of the

business. Any

misstatement in the figure

would be impacting the

profitability of the

business and expenses

which is related to

extraordinary nature

greatly.

Trade and Other

Receivables

Types of risks: Control

Risks

Degree of Risks: High

The auditor needs to check

all the notes, receipts and

invoices for the business.

The trade receivables are

related to sales which have

significantly changed

during the period. The

amount which is shown in

the balance sheet is more

than the materiality

estimate as per the

provisions of “ASA 320

Materiality and Audit

Adjustments “and therefore

it can be estimated that the

same would be having

significant impact if the

same is misstated.

Accrued Revenue Types of risks:

Detection risks

Degree of Risks: Low

The auditor needs to check

the nature of the

transaction as this is not a

recurring transaction and

therefore, there is a high

chance that the item might

be misstated.

Deferred Tax Assets Types of risks: Inherent The auditor needs to pay

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Risks

Degree of Risks: High

special attention in this

case as the item is

extraordinary in nature

and misstatement in the

same is likely to happen.

The provisions of ASA

220 Quality Control for

Audits of Historical

Financial Information,

can be referred in terms of

the business has any

values in the past for such

types of transactions.

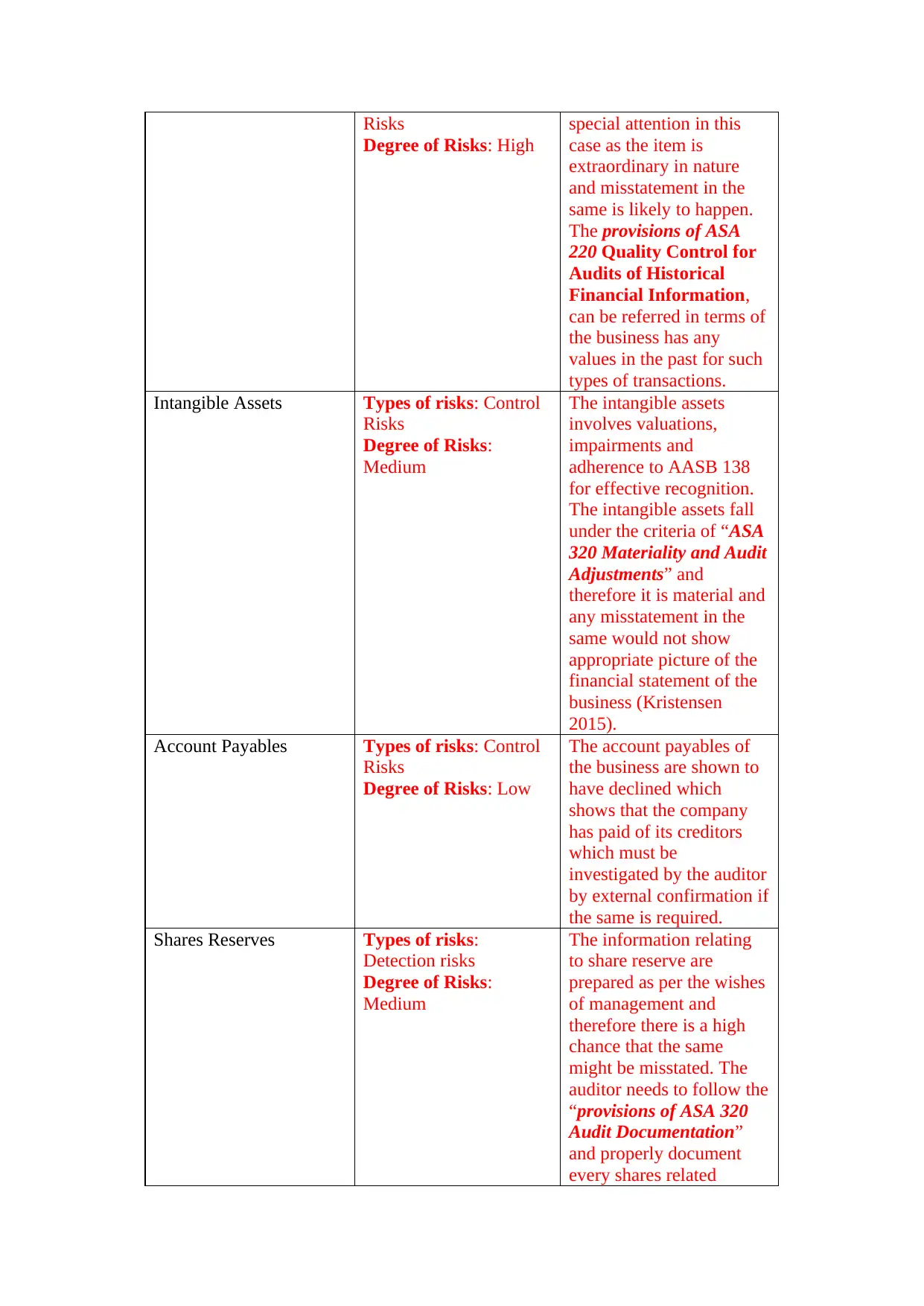

Intangible Assets Types of risks: Control

Risks

Degree of Risks:

Medium

The intangible assets

involves valuations,

impairments and

adherence to AASB 138

for effective recognition.

The intangible assets fall

under the criteria of “ASA

320 Materiality and Audit

Adjustments” and

therefore it is material and

any misstatement in the

same would not show

appropriate picture of the

financial statement of the

business (Kristensen

2015).

Account Payables Types of risks: Control

Risks

Degree of Risks: Low

The account payables of

the business are shown to

have declined which

shows that the company

has paid of its creditors

which must be

investigated by the auditor

by external confirmation if

the same is required.

Shares Reserves Types of risks:

Detection risks

Degree of Risks:

Medium

The information relating

to share reserve are

prepared as per the wishes

of management and

therefore there is a high

chance that the same

might be misstated. The

auditor needs to follow the

“provisions of ASA 320

Audit Documentation”

and properly document

every shares related

Degree of Risks: High

special attention in this

case as the item is

extraordinary in nature

and misstatement in the

same is likely to happen.

The provisions of ASA

220 Quality Control for

Audits of Historical

Financial Information,

can be referred in terms of

the business has any

values in the past for such

types of transactions.

Intangible Assets Types of risks: Control

Risks

Degree of Risks:

Medium

The intangible assets

involves valuations,

impairments and

adherence to AASB 138

for effective recognition.

The intangible assets fall

under the criteria of “ASA

320 Materiality and Audit

Adjustments” and

therefore it is material and

any misstatement in the

same would not show

appropriate picture of the

financial statement of the

business (Kristensen

2015).

Account Payables Types of risks: Control

Risks

Degree of Risks: Low

The account payables of

the business are shown to

have declined which

shows that the company

has paid of its creditors

which must be

investigated by the auditor

by external confirmation if

the same is required.

Shares Reserves Types of risks:

Detection risks

Degree of Risks:

Medium

The information relating

to share reserve are

prepared as per the wishes

of management and

therefore there is a high

chance that the same

might be misstated. The

auditor needs to follow the

“provisions of ASA 320

Audit Documentation”

and properly document

every shares related

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information such as issue

price, call made.

price, call made.

Conclusion

The above discussion appropriately shows the process of auditing for the business of

Pro Medicus Ltd while considering the annual report of the business for the year 2018.

The analysis shows the eight account balances which are most subjected to risks and the

respective audit procedures which can be taken by the auditor for accumulating audit

evidences in such a circumstance. The analysis shows application of “ASA 320 Audit

Documentation” and “ASA 320 Materiality and Audit Adjustments” for the purpose of

determining which information is to be documented and what is to be considered from the

perspective of materiality. In addition to this, the planning materiality for Pro Medicus ltd

is also compute considering the provision stated in “ASA 320 Materiality and Audit

Adjustments”. The analysis further shows the computation of materiality estimates which

is done considering the total revenue which is generated by the business during 2018. The

percentage which is considered is 0.5% on the basis of which planning materiality for the

business is computed. The analysis also shows impacts of material misstatement which is

present in the financial reports on the overall financial position of the business. The

discussion also shows the audit procedure which the auditor can undertake following

relevant auditing standards for forming an opinion on the financial statement of the

business.

The above discussion appropriately shows the process of auditing for the business of

Pro Medicus Ltd while considering the annual report of the business for the year 2018.

The analysis shows the eight account balances which are most subjected to risks and the

respective audit procedures which can be taken by the auditor for accumulating audit

evidences in such a circumstance. The analysis shows application of “ASA 320 Audit

Documentation” and “ASA 320 Materiality and Audit Adjustments” for the purpose of

determining which information is to be documented and what is to be considered from the

perspective of materiality. In addition to this, the planning materiality for Pro Medicus ltd

is also compute considering the provision stated in “ASA 320 Materiality and Audit

Adjustments”. The analysis further shows the computation of materiality estimates which

is done considering the total revenue which is generated by the business during 2018. The

percentage which is considered is 0.5% on the basis of which planning materiality for the

business is computed. The analysis also shows impacts of material misstatement which is

present in the financial reports on the overall financial position of the business. The

discussion also shows the audit procedure which the auditor can undertake following

relevant auditing standards for forming an opinion on the financial statement of the

business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.