Chapter 4 Process Costing Solutions: Exercises and Problems Analysis

VerifiedAdded on 2021/09/02

|53

|9865

|196

Homework Assignment

AI Summary

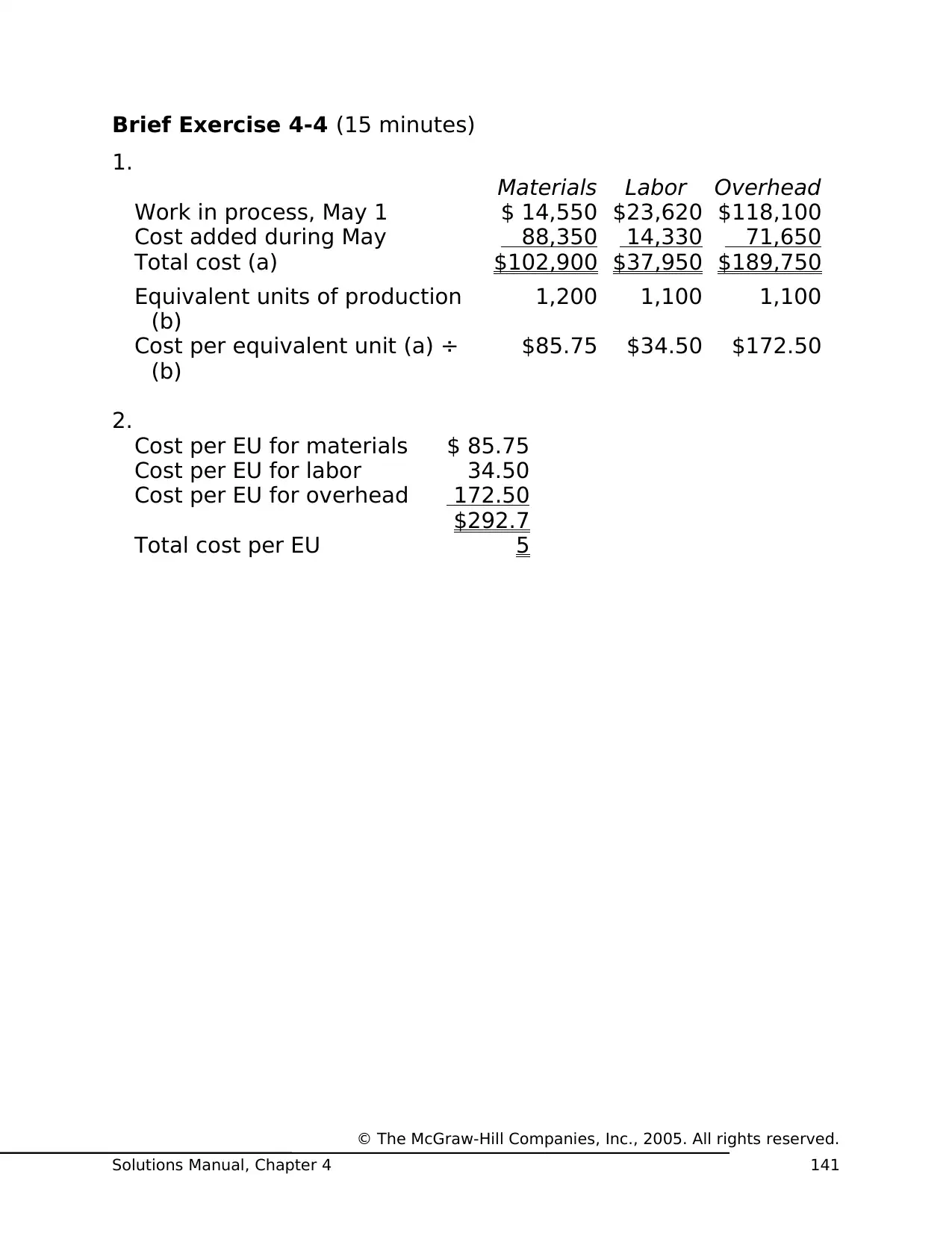

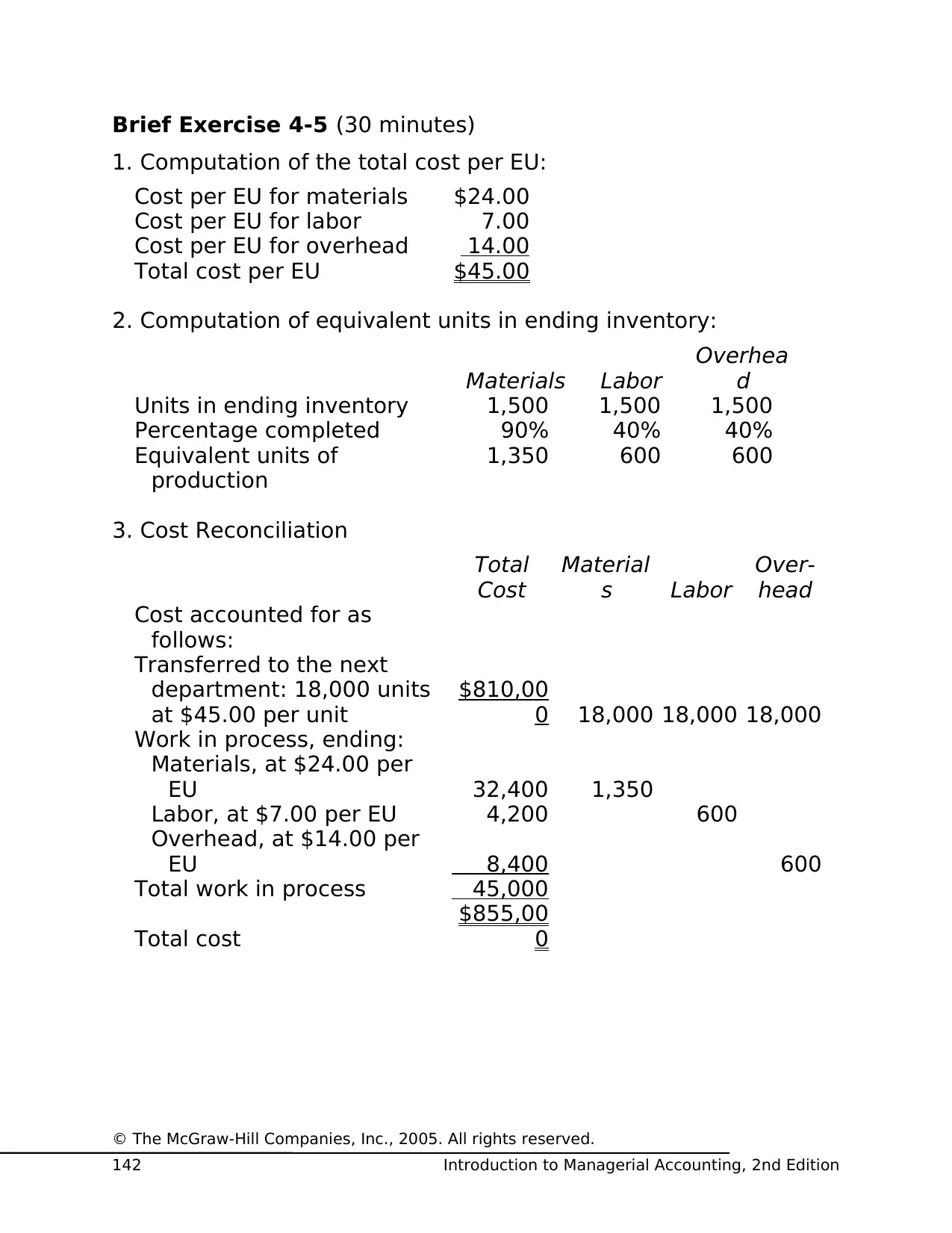

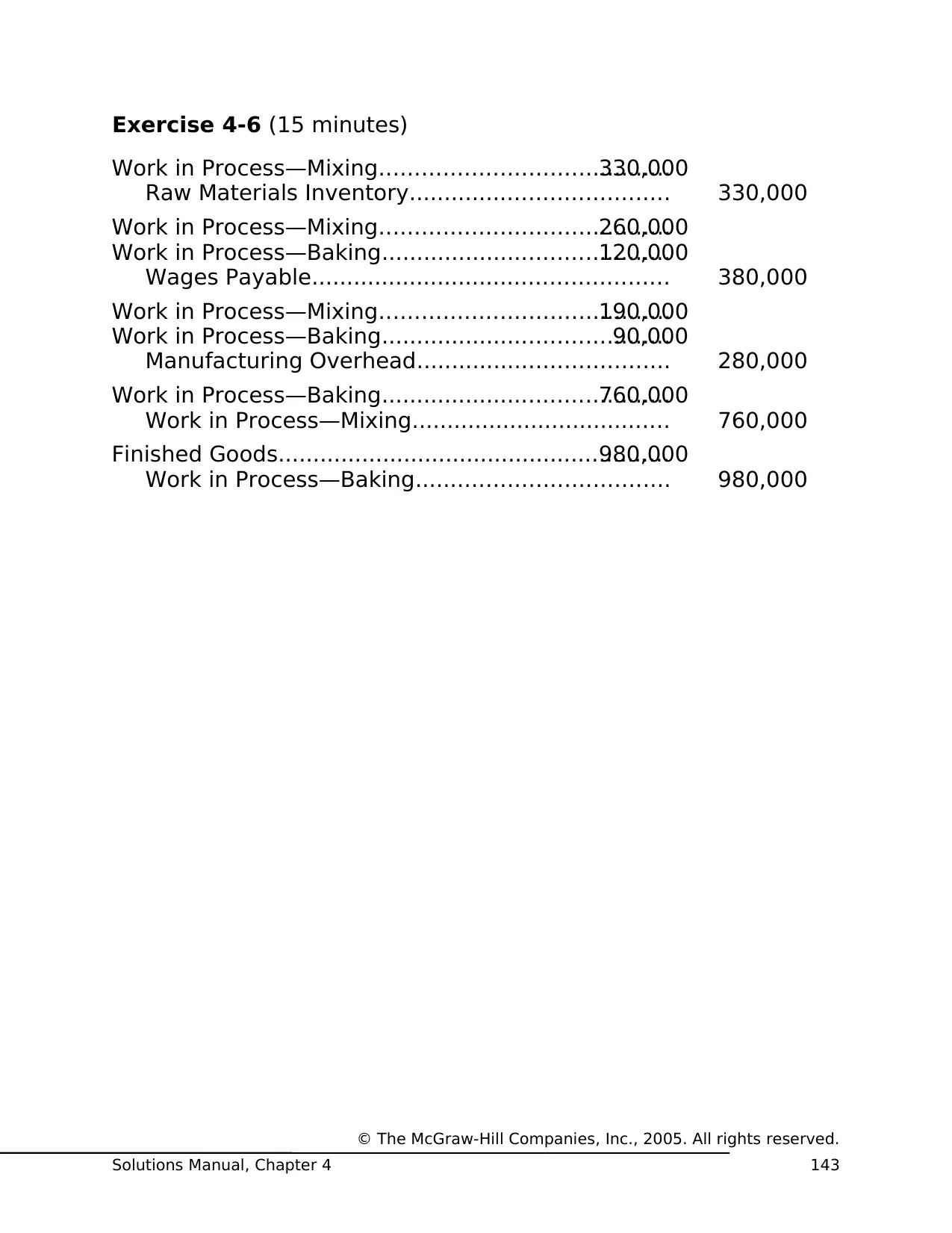

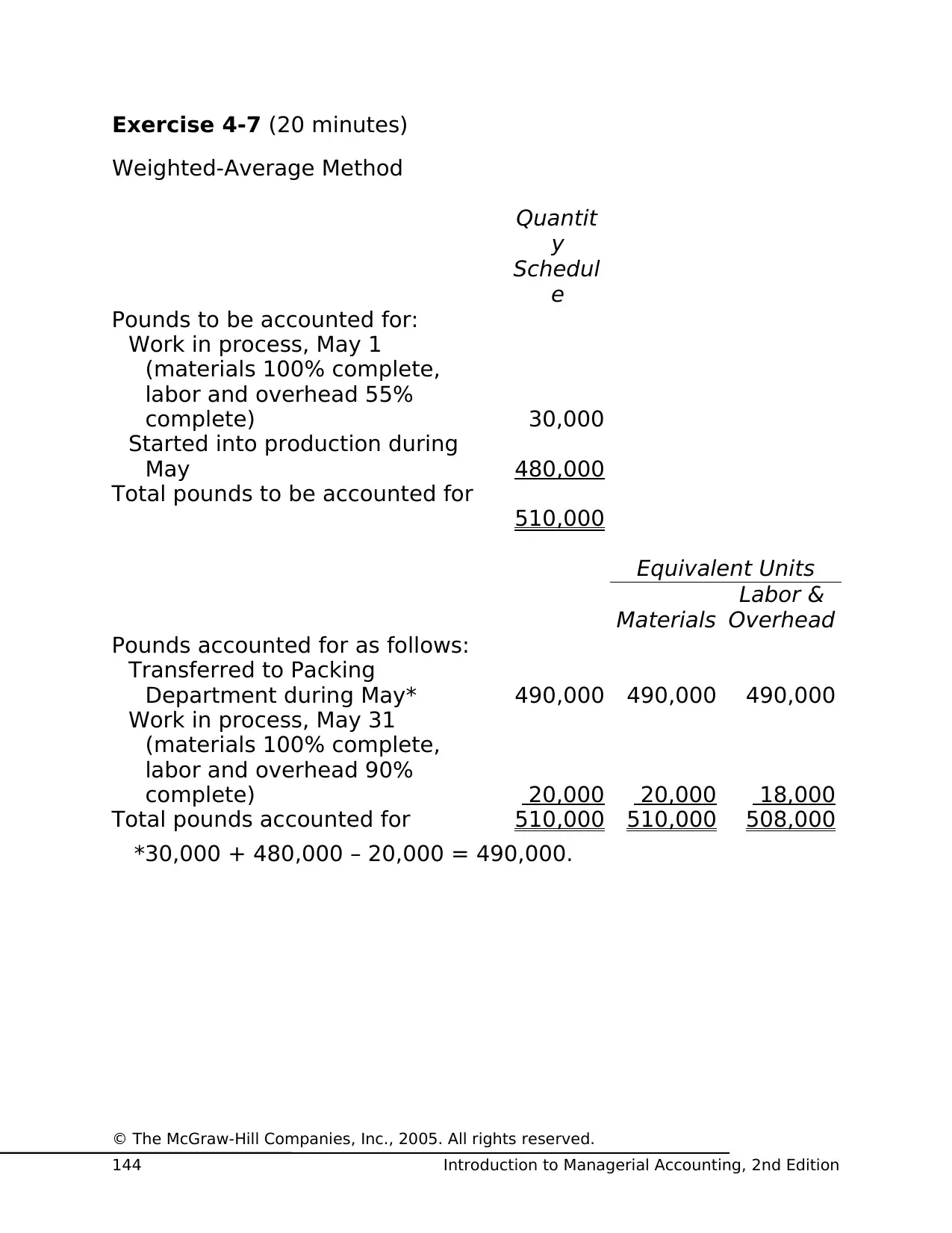

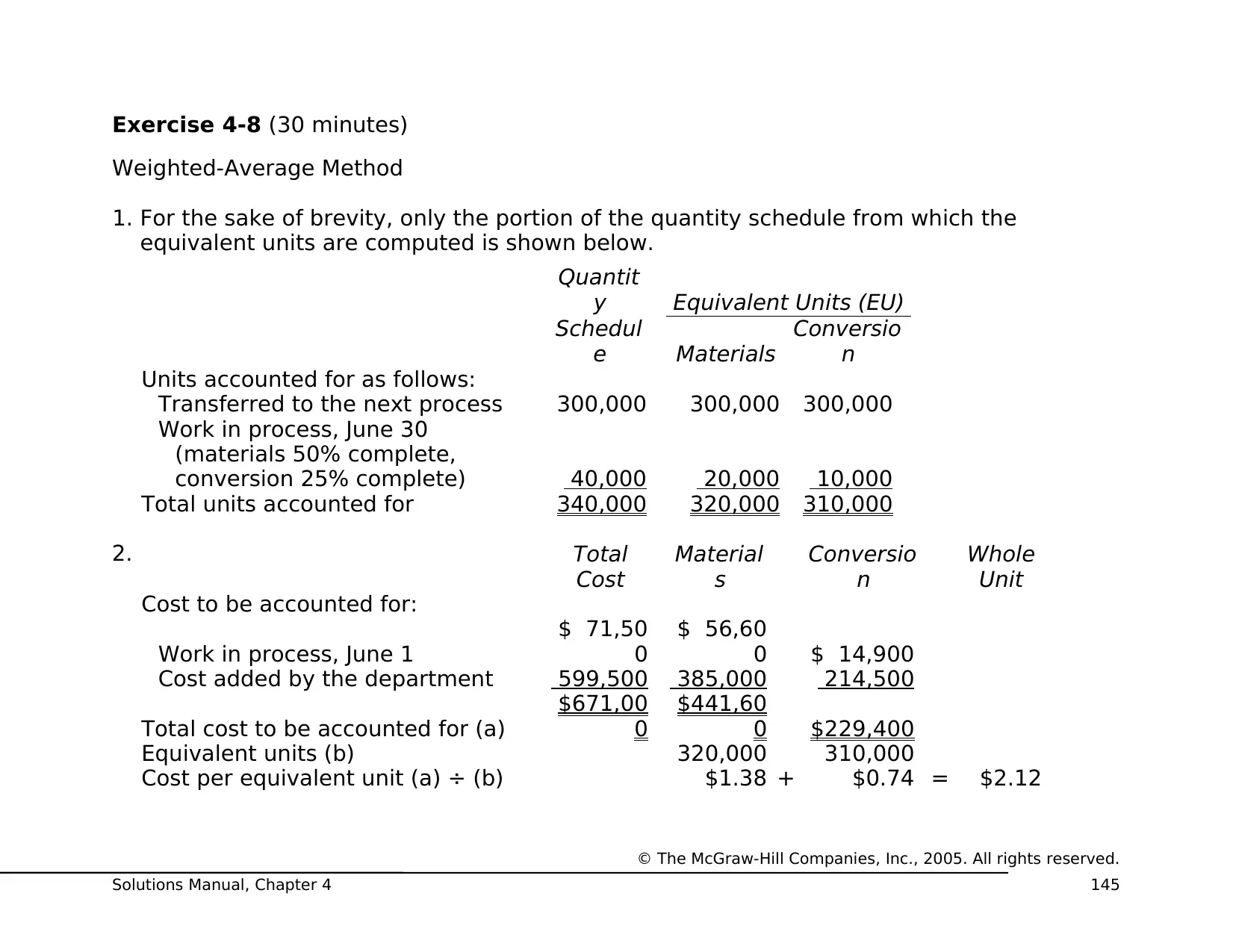

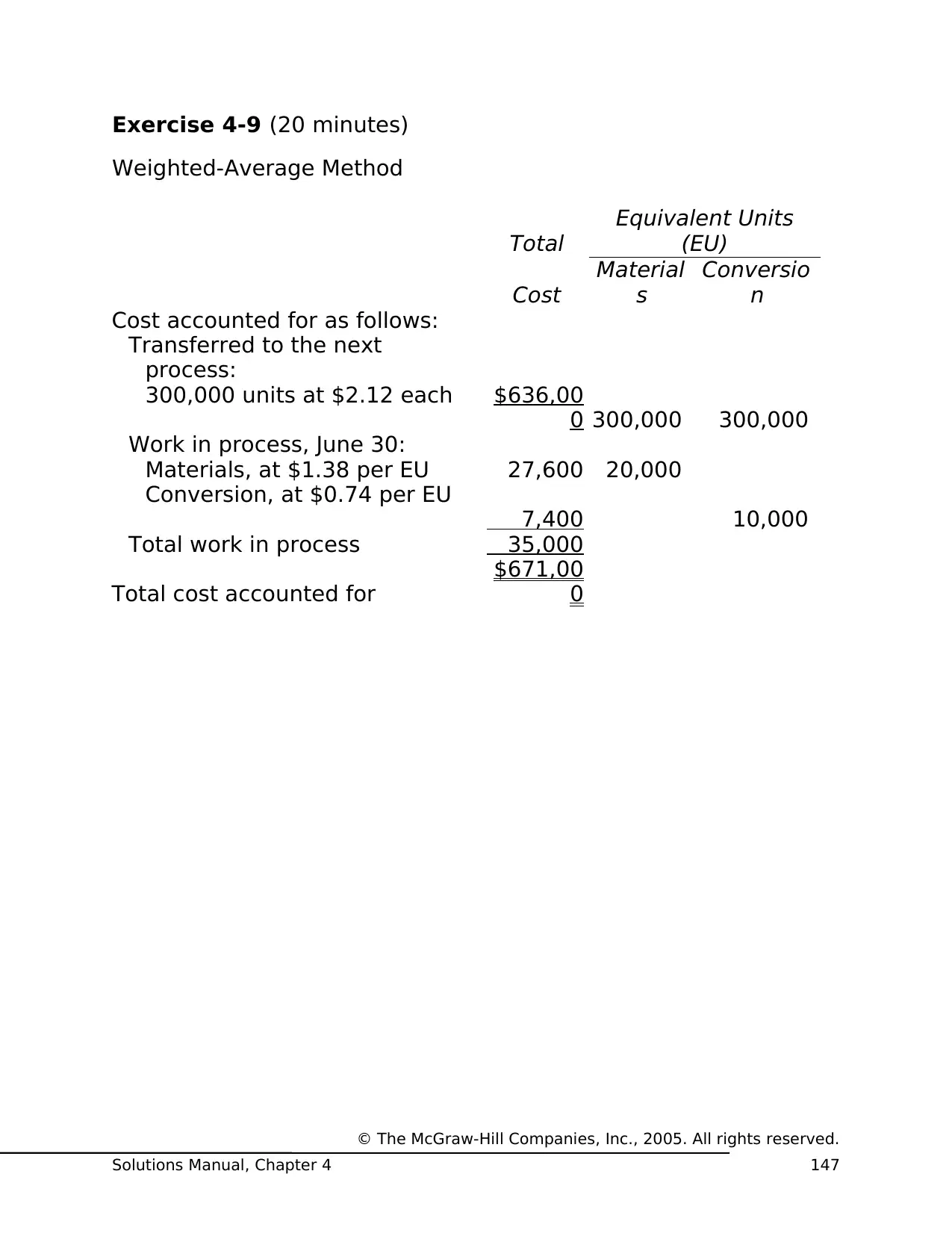

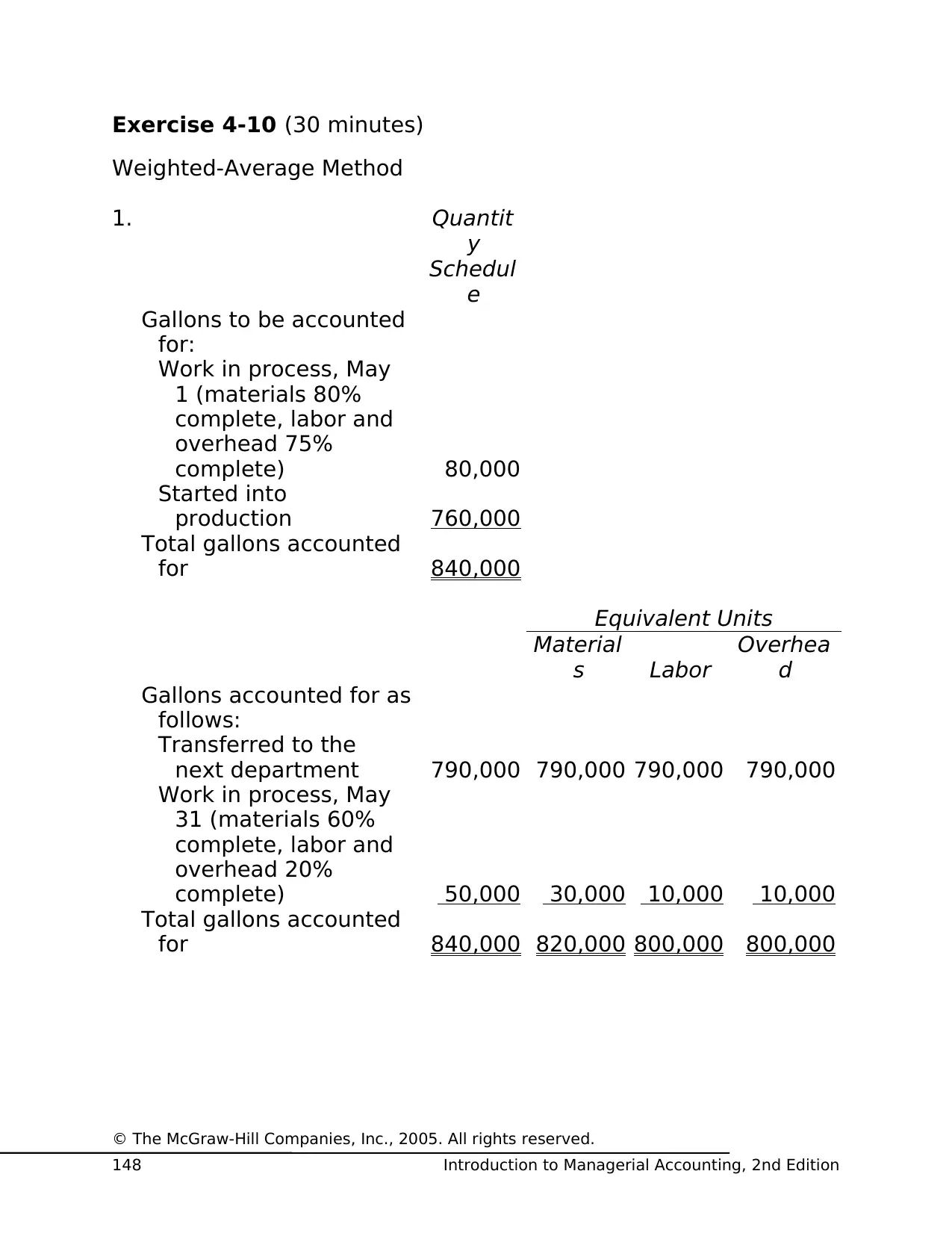

This document offers a comprehensive set of solutions to various exercises and problems related to process costing, specifically focusing on Chapter 4. The solutions cover key concepts such as the application of process costing systems, cost accumulation by department, and the calculation of equivalent units of production under the weighted-average method. The document includes journal entries for recording costs, quantity schedules for tracking units, and detailed calculations of cost per equivalent unit. It also addresses the transfer of costs between departments and the reconciliation of costs. The solutions are presented in a clear and organized manner, providing a step-by-step approach to understanding and solving process costing problems, which is a crucial aspect of cost accounting and finance. The solutions cover topics such as materials, labor, and overhead costs, along with their impact on work in process and finished goods inventories. The document is designed to help students grasp the practical application of process costing principles.

1 out of 53

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.