FNSACC301 - Process Financial Transactions and Extract Reports

VerifiedAdded on 2023/06/04

|16

|3308

|102

Homework Assignment

AI Summary

This document presents a comprehensive solution for the FNSACC301 assignment, focusing on processing financial transactions and extracting interim reports. The assignment covers a wide range of topics, including sales invoices, journal entries, ledger accounts, petty cash management, error correction, audit procedures, debtor and general ledgers, and bad debt write-offs. The solution provides detailed answers to short answer questions, practical examples, and journal entries, demonstrating how to handle various financial scenarios and maintain accurate records. The document emphasizes the importance of continuous improvement in financial systems and adhering to organizational policies and legislative requirements. It also explores methods for lodging cash and non-cash items with financial institutions, ensuring financial data security, and maintaining employee safety in the workplace.

1

NSACC301

Process Financial Transactions and

Extract interim Reports

NSACC301

Process Financial Transactions and

Extract interim Reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Answer 1....................................................................................................................................4

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................4

Answer 4....................................................................................................................................5

Answer 5....................................................................................................................................5

Answer 6....................................................................................................................................5

Answer 7....................................................................................................................................6

Answer 8....................................................................................................................................6

Answer 9....................................................................................................................................7

Answer 10..................................................................................................................................7

Answer 11..................................................................................................................................8

Answer 12..................................................................................................................................8

Answer 13..................................................................................................................................8

Answer 14 A& B........................................................................................................................9

Table 4: Company’s Ledger A/c................................................................................................9

Answer 15..................................................................................................................................9

Answer 16................................................................................................................................10

Lodging Cash with Financial Institutions............................................................................10

Lodging Non-Cash Items with Financial Institutions..........................................................10

Answer 17................................................................................................................................10

Answer 18................................................................................................................................10

Answer 19................................................................................................................................11

Answer 20................................................................................................................................12

Answer 21................................................................................................................................12

Answer 22................................................................................................................................12

Assessment 2............................................................................................................................14

Table of Contents

Answer 1....................................................................................................................................4

Answer 2....................................................................................................................................4

Answer 3....................................................................................................................................4

Answer 4....................................................................................................................................5

Answer 5....................................................................................................................................5

Answer 6....................................................................................................................................5

Answer 7....................................................................................................................................6

Answer 8....................................................................................................................................6

Answer 9....................................................................................................................................7

Answer 10..................................................................................................................................7

Answer 11..................................................................................................................................8

Answer 12..................................................................................................................................8

Answer 13..................................................................................................................................8

Answer 14 A& B........................................................................................................................9

Table 4: Company’s Ledger A/c................................................................................................9

Answer 15..................................................................................................................................9

Answer 16................................................................................................................................10

Lodging Cash with Financial Institutions............................................................................10

Lodging Non-Cash Items with Financial Institutions..........................................................10

Answer 17................................................................................................................................10

Answer 18................................................................................................................................10

Answer 19................................................................................................................................11

Answer 20................................................................................................................................12

Answer 21................................................................................................................................12

Answer 22................................................................................................................................12

Assessment 2............................................................................................................................14

3

References................................................................................................................................16

References................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

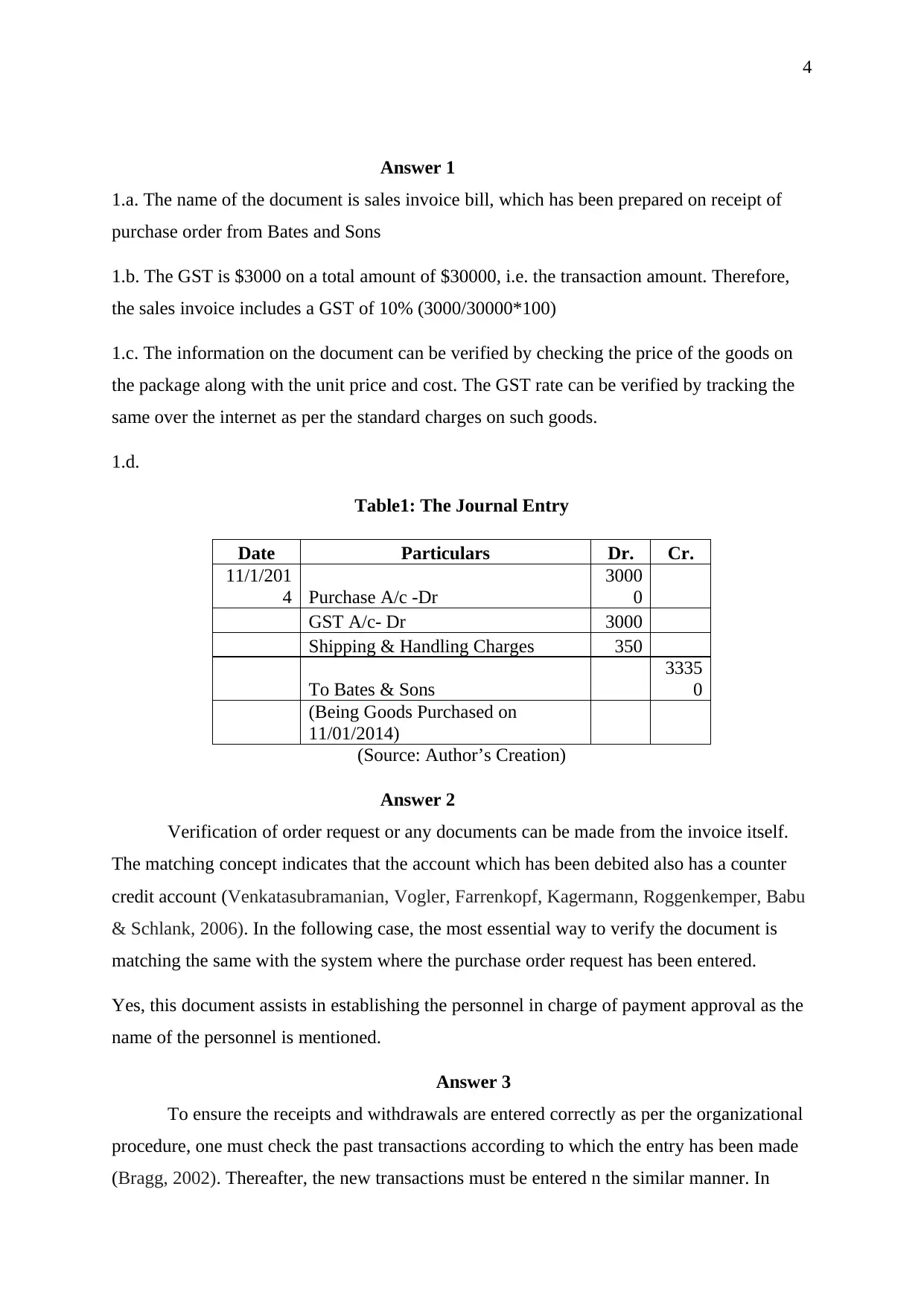

Answer 1

1.a. The name of the document is sales invoice bill, which has been prepared on receipt of

purchase order from Bates and Sons

1.b. The GST is $3000 on a total amount of $30000, i.e. the transaction amount. Therefore,

the sales invoice includes a GST of 10% (3000/30000*100)

1.c. The information on the document can be verified by checking the price of the goods on

the package along with the unit price and cost. The GST rate can be verified by tracking the

same over the internet as per the standard charges on such goods.

1.d.

Table1: The Journal Entry

Date Particulars Dr. Cr.

11/1/201

4 Purchase A/c -Dr

3000

0

GST A/c- Dr 3000

Shipping & Handling Charges 350

To Bates & Sons

3335

0

(Being Goods Purchased on

11/01/2014)

(Source: Author’s Creation)

Answer 2

Verification of order request or any documents can be made from the invoice itself.

The matching concept indicates that the account which has been debited also has a counter

credit account (Venkatasubramanian, Vogler, Farrenkopf, Kagermann, Roggenkemper, Babu

& Schlank, 2006). In the following case, the most essential way to verify the document is

matching the same with the system where the purchase order request has been entered.

Yes, this document assists in establishing the personnel in charge of payment approval as the

name of the personnel is mentioned.

Answer 3

To ensure the receipts and withdrawals are entered correctly as per the organizational

procedure, one must check the past transactions according to which the entry has been made

(Bragg, 2002). Thereafter, the new transactions must be entered n the similar manner. In

Answer 1

1.a. The name of the document is sales invoice bill, which has been prepared on receipt of

purchase order from Bates and Sons

1.b. The GST is $3000 on a total amount of $30000, i.e. the transaction amount. Therefore,

the sales invoice includes a GST of 10% (3000/30000*100)

1.c. The information on the document can be verified by checking the price of the goods on

the package along with the unit price and cost. The GST rate can be verified by tracking the

same over the internet as per the standard charges on such goods.

1.d.

Table1: The Journal Entry

Date Particulars Dr. Cr.

11/1/201

4 Purchase A/c -Dr

3000

0

GST A/c- Dr 3000

Shipping & Handling Charges 350

To Bates & Sons

3335

0

(Being Goods Purchased on

11/01/2014)

(Source: Author’s Creation)

Answer 2

Verification of order request or any documents can be made from the invoice itself.

The matching concept indicates that the account which has been debited also has a counter

credit account (Venkatasubramanian, Vogler, Farrenkopf, Kagermann, Roggenkemper, Babu

& Schlank, 2006). In the following case, the most essential way to verify the document is

matching the same with the system where the purchase order request has been entered.

Yes, this document assists in establishing the personnel in charge of payment approval as the

name of the personnel is mentioned.

Answer 3

To ensure the receipts and withdrawals are entered correctly as per the organizational

procedure, one must check the past transactions according to which the entry has been made

(Bragg, 2002). Thereafter, the new transactions must be entered n the similar manner. In

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

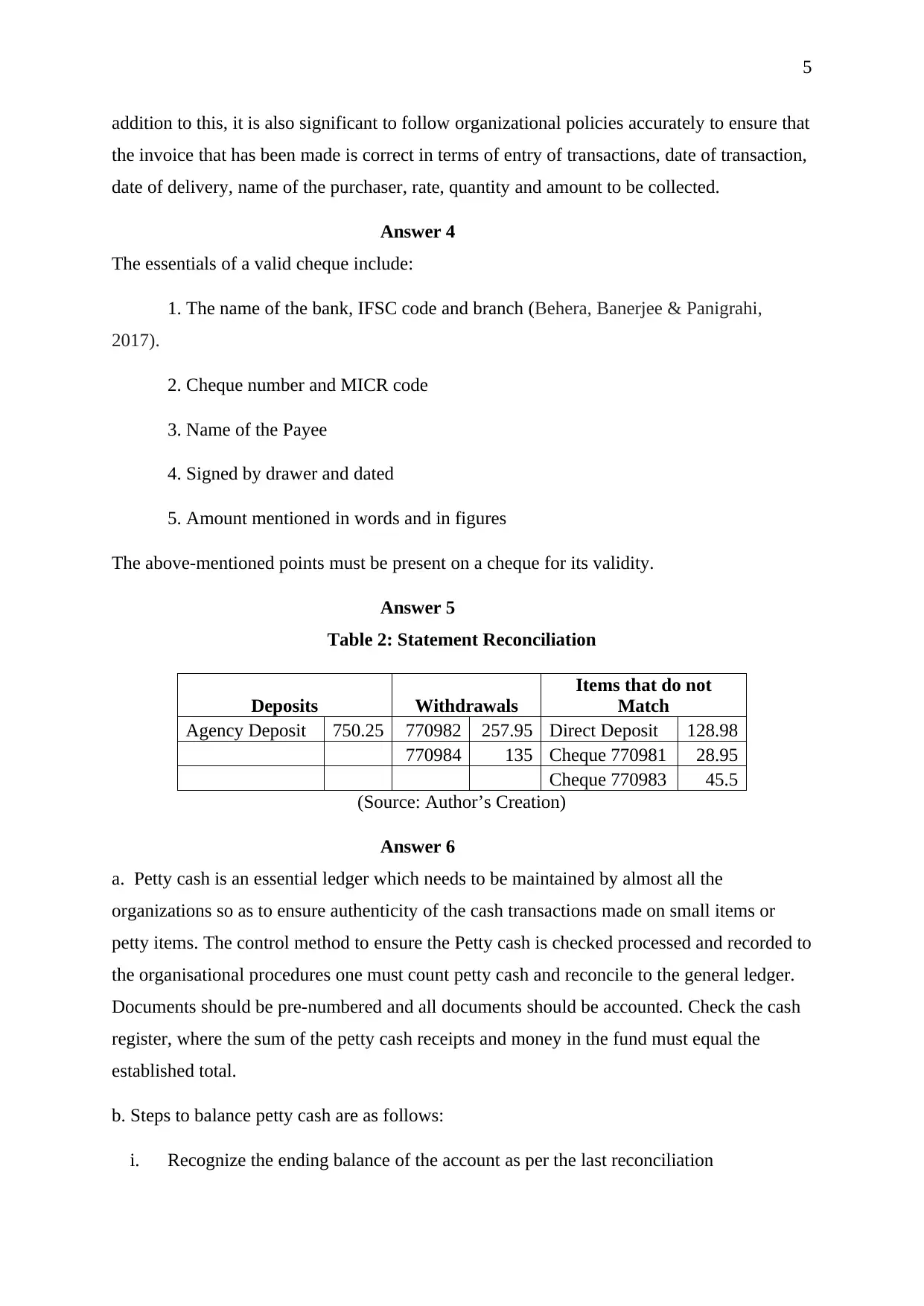

addition to this, it is also significant to follow organizational policies accurately to ensure that

the invoice that has been made is correct in terms of entry of transactions, date of transaction,

date of delivery, name of the purchaser, rate, quantity and amount to be collected.

Answer 4

The essentials of a valid cheque include:

1. The name of the bank, IFSC code and branch (Behera, Banerjee & Panigrahi,

2017).

2. Cheque number and MICR code

3. Name of the Payee

4. Signed by drawer and dated

5. Amount mentioned in words and in figures

The above-mentioned points must be present on a cheque for its validity.

Answer 5

Table 2: Statement Reconciliation

Deposits Withdrawals

Items that do not

Match

Agency Deposit 750.25 770982 257.95 Direct Deposit 128.98

770984 135 Cheque 770981 28.95

Cheque 770983 45.5

(Source: Author’s Creation)

Answer 6

a. Petty cash is an essential ledger which needs to be maintained by almost all the

organizations so as to ensure authenticity of the cash transactions made on small items or

petty items. The control method to ensure the Petty cash is checked processed and recorded to

the organisational procedures one must count petty cash and reconcile to the general ledger.

Documents should be pre-numbered and all documents should be accounted. Check the cash

register, where the sum of the petty cash receipts and money in the fund must equal the

established total.

b. Steps to balance petty cash are as follows:

i. Recognize the ending balance of the account as per the last reconciliation

addition to this, it is also significant to follow organizational policies accurately to ensure that

the invoice that has been made is correct in terms of entry of transactions, date of transaction,

date of delivery, name of the purchaser, rate, quantity and amount to be collected.

Answer 4

The essentials of a valid cheque include:

1. The name of the bank, IFSC code and branch (Behera, Banerjee & Panigrahi,

2017).

2. Cheque number and MICR code

3. Name of the Payee

4. Signed by drawer and dated

5. Amount mentioned in words and in figures

The above-mentioned points must be present on a cheque for its validity.

Answer 5

Table 2: Statement Reconciliation

Deposits Withdrawals

Items that do not

Match

Agency Deposit 750.25 770982 257.95 Direct Deposit 128.98

770984 135 Cheque 770981 28.95

Cheque 770983 45.5

(Source: Author’s Creation)

Answer 6

a. Petty cash is an essential ledger which needs to be maintained by almost all the

organizations so as to ensure authenticity of the cash transactions made on small items or

petty items. The control method to ensure the Petty cash is checked processed and recorded to

the organisational procedures one must count petty cash and reconcile to the general ledger.

Documents should be pre-numbered and all documents should be accounted. Check the cash

register, where the sum of the petty cash receipts and money in the fund must equal the

established total.

b. Steps to balance petty cash are as follows:

i. Recognize the ending balance of the account as per the last reconciliation

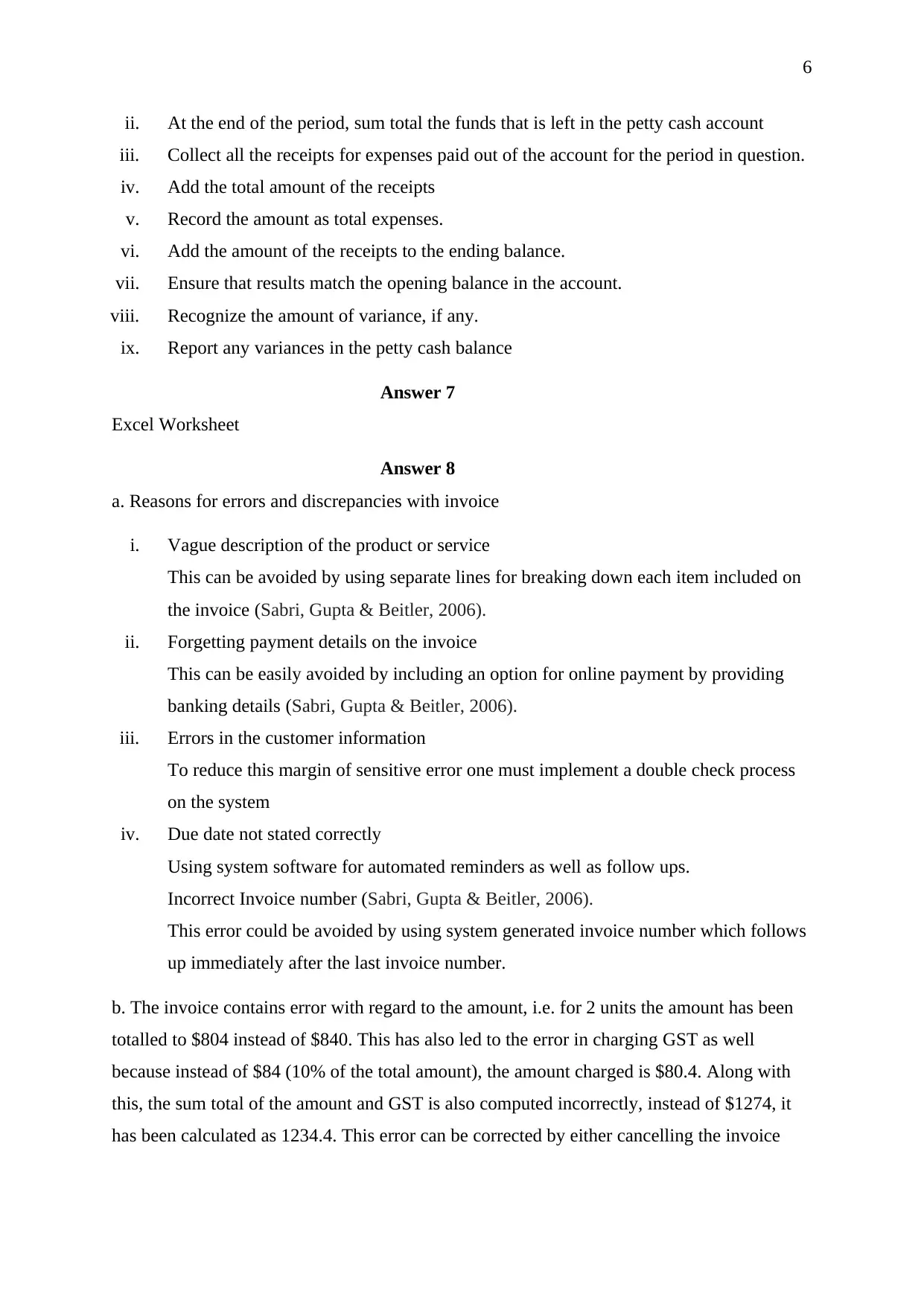

6

ii. At the end of the period, sum total the funds that is left in the petty cash account

iii. Collect all the receipts for expenses paid out of the account for the period in question.

iv. Add the total amount of the receipts

v. Record the amount as total expenses.

vi. Add the amount of the receipts to the ending balance.

vii. Ensure that results match the opening balance in the account.

viii. Recognize the amount of variance, if any.

ix. Report any variances in the petty cash balance

Answer 7

Excel Worksheet

Answer 8

a. Reasons for errors and discrepancies with invoice

i. Vague description of the product or service

This can be avoided by using separate lines for breaking down each item included on

the invoice (Sabri, Gupta & Beitler, 2006).

ii. Forgetting payment details on the invoice

This can be easily avoided by including an option for online payment by providing

banking details (Sabri, Gupta & Beitler, 2006).

iii. Errors in the customer information

To reduce this margin of sensitive error one must implement a double check process

on the system

iv. Due date not stated correctly

Using system software for automated reminders as well as follow ups.

Incorrect Invoice number (Sabri, Gupta & Beitler, 2006).

This error could be avoided by using system generated invoice number which follows

up immediately after the last invoice number.

b. The invoice contains error with regard to the amount, i.e. for 2 units the amount has been

totalled to $804 instead of $840. This has also led to the error in charging GST as well

because instead of $84 (10% of the total amount), the amount charged is $80.4. Along with

this, the sum total of the amount and GST is also computed incorrectly, instead of $1274, it

has been calculated as 1234.4. This error can be corrected by either cancelling the invoice

ii. At the end of the period, sum total the funds that is left in the petty cash account

iii. Collect all the receipts for expenses paid out of the account for the period in question.

iv. Add the total amount of the receipts

v. Record the amount as total expenses.

vi. Add the amount of the receipts to the ending balance.

vii. Ensure that results match the opening balance in the account.

viii. Recognize the amount of variance, if any.

ix. Report any variances in the petty cash balance

Answer 7

Excel Worksheet

Answer 8

a. Reasons for errors and discrepancies with invoice

i. Vague description of the product or service

This can be avoided by using separate lines for breaking down each item included on

the invoice (Sabri, Gupta & Beitler, 2006).

ii. Forgetting payment details on the invoice

This can be easily avoided by including an option for online payment by providing

banking details (Sabri, Gupta & Beitler, 2006).

iii. Errors in the customer information

To reduce this margin of sensitive error one must implement a double check process

on the system

iv. Due date not stated correctly

Using system software for automated reminders as well as follow ups.

Incorrect Invoice number (Sabri, Gupta & Beitler, 2006).

This error could be avoided by using system generated invoice number which follows

up immediately after the last invoice number.

b. The invoice contains error with regard to the amount, i.e. for 2 units the amount has been

totalled to $804 instead of $840. This has also led to the error in charging GST as well

because instead of $84 (10% of the total amount), the amount charged is $80.4. Along with

this, the sum total of the amount and GST is also computed incorrectly, instead of $1274, it

has been calculated as 1234.4. This error can be corrected by either cancelling the invoice

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

and generating a new one with correct figures, or by generating another invoice with the

balance figure. The first alternative option seems to be more accurate.

Answer 9

The 5 reasons for filing invoices and related documents to be important for audit purpose are

as follows:

1. The invoices and other related documents include the basic facts with regard to the

transaction, which includes the date when the transactions occurred, to whom the transaction

was made, the quantity sold and bought and the amount charged for it.

2. These documents serve as evidences for the financial transactions that have occurred.

3. These evidences can become records for verification of accurateness of the transactions for

audit purpose (Lanza, 2009).

4. Well-kept records generally shortens the length of time required for completing the audit

process.

5. The records maintained gives better information regarding the financial position.

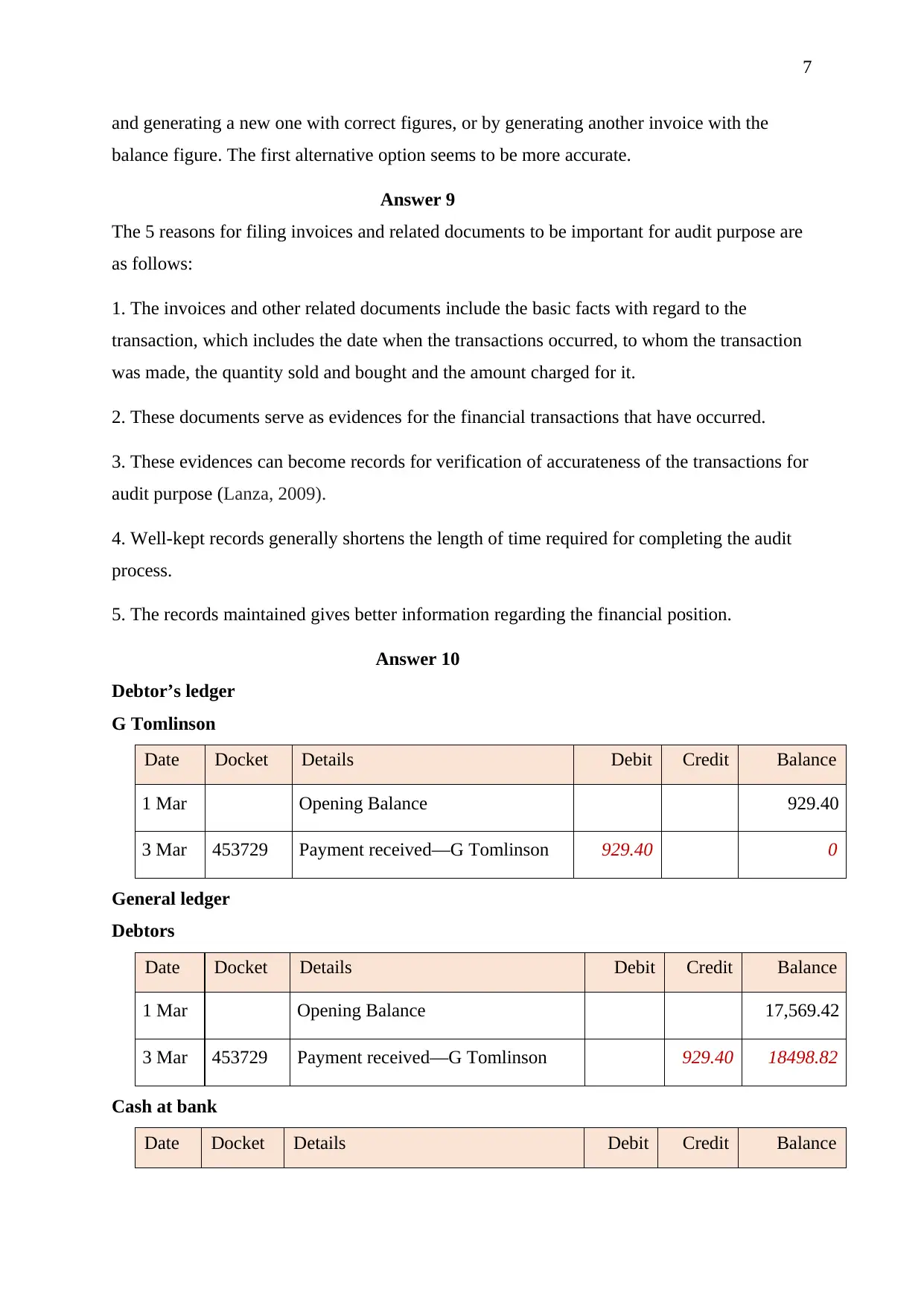

Answer 10

Debtor’s ledger

G Tomlinson

Date Docket Details Debit Credit Balance

1 Mar Opening Balance 929.40

3 Mar 453729 Payment received—G Tomlinson 929.40 0

General ledger

Debtors

Date Docket Details Debit Credit Balance

1 Mar Opening Balance 17,569.42

3 Mar 453729 Payment received—G Tomlinson 929.40 18498.82

Cash at bank

Date Docket Details Debit Credit Balance

and generating a new one with correct figures, or by generating another invoice with the

balance figure. The first alternative option seems to be more accurate.

Answer 9

The 5 reasons for filing invoices and related documents to be important for audit purpose are

as follows:

1. The invoices and other related documents include the basic facts with regard to the

transaction, which includes the date when the transactions occurred, to whom the transaction

was made, the quantity sold and bought and the amount charged for it.

2. These documents serve as evidences for the financial transactions that have occurred.

3. These evidences can become records for verification of accurateness of the transactions for

audit purpose (Lanza, 2009).

4. Well-kept records generally shortens the length of time required for completing the audit

process.

5. The records maintained gives better information regarding the financial position.

Answer 10

Debtor’s ledger

G Tomlinson

Date Docket Details Debit Credit Balance

1 Mar Opening Balance 929.40

3 Mar 453729 Payment received—G Tomlinson 929.40 0

General ledger

Debtors

Date Docket Details Debit Credit Balance

1 Mar Opening Balance 17,569.42

3 Mar 453729 Payment received—G Tomlinson 929.40 18498.82

Cash at bank

Date Docket Details Debit Credit Balance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

1 Mar Opening Balance 125,851.65

3 Mar 453729 Payment received—G Tomlinson 929.40 126781.05

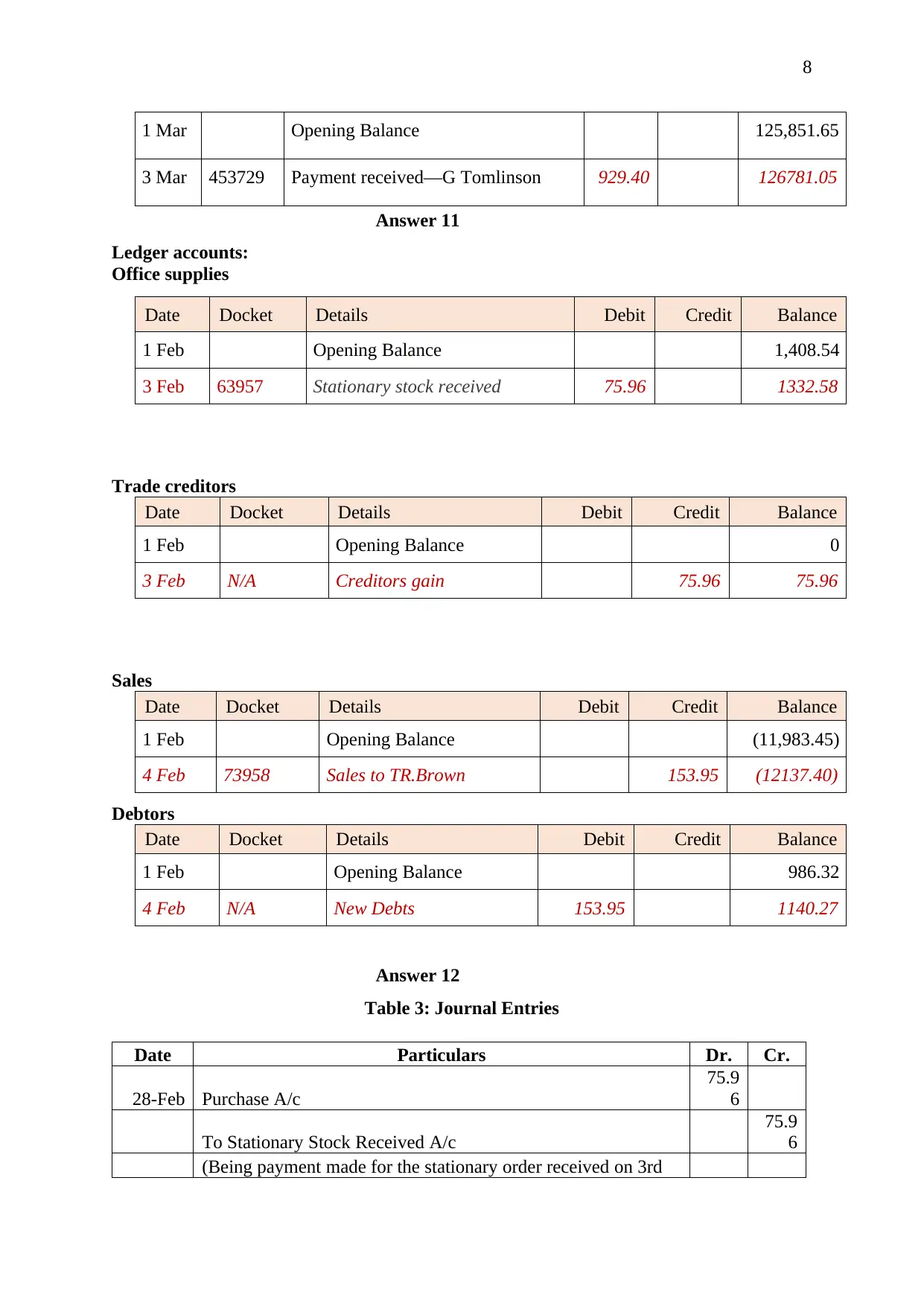

Answer 11

Ledger accounts:

Office supplies

Date Docket Details Debit Credit Balance

1 Feb Opening Balance 1,408.54

3 Feb 63957 Stationary stock received 75.96 1332.58

Trade creditors

Date Docket Details Debit Credit Balance

1 Feb Opening Balance 0

3 Feb N/A Creditors gain 75.96 75.96

Sales

Date Docket Details Debit Credit Balance

1 Feb Opening Balance (11,983.45)

4 Feb 73958 Sales to TR.Brown 153.95 (12137.40)

Debtors

Date Docket Details Debit Credit Balance

1 Feb Opening Balance 986.32

4 Feb N/A New Debts 153.95 1140.27

Answer 12

Table 3: Journal Entries

Date Particulars Dr. Cr.

28-Feb Purchase A/c

75.9

6

To Stationary Stock Received A/c

75.9

6

(Being payment made for the stationary order received on 3rd

1 Mar Opening Balance 125,851.65

3 Mar 453729 Payment received—G Tomlinson 929.40 126781.05

Answer 11

Ledger accounts:

Office supplies

Date Docket Details Debit Credit Balance

1 Feb Opening Balance 1,408.54

3 Feb 63957 Stationary stock received 75.96 1332.58

Trade creditors

Date Docket Details Debit Credit Balance

1 Feb Opening Balance 0

3 Feb N/A Creditors gain 75.96 75.96

Sales

Date Docket Details Debit Credit Balance

1 Feb Opening Balance (11,983.45)

4 Feb 73958 Sales to TR.Brown 153.95 (12137.40)

Debtors

Date Docket Details Debit Credit Balance

1 Feb Opening Balance 986.32

4 Feb N/A New Debts 153.95 1140.27

Answer 12

Table 3: Journal Entries

Date Particulars Dr. Cr.

28-Feb Purchase A/c

75.9

6

To Stationary Stock Received A/c

75.9

6

(Being payment made for the stationary order received on 3rd

9

Feb)

(Source: Author’s Creation)

Answer 13

Table 4: Sales Journal

Date Account Debited

Invoice

No. Amount

4-Jul John Green 6 2200

5-Jul John Green 7 2000

5-Jul Peter Brown 8 1100

7-Jul John Squires 9 125.9

31-Jul Total Transferred to Sales A/c 5425.9

(Source: Author’s Creation)

Table 5:Sales A/c

Date Description Amount Date Description Amount

- - - 31-Jul

Accounts

Receivable 5425.9

Accounts Receivable

Date Description Amount Date Description Amount

31-Jul Sales A/c 5425.9 - - -

(Source: Author’s Creation)

Answer 14 A& B

Table 4: Company’s Ledger A/c

Date Description

Amoun

t Date Description

Amoun

t

1/2/2015

Kmart Service

Station 365

5/2/201

5 Richardson 1300

28/2/2015 Bank A/c 1335

Profit & Loss

A/c 400

Answer 15

A continuous improvement or updating strategy implemented in an organization is the

process and policies that enables the management to stay focused on improving the activities

done on regular basis. Systems could be regularly maintained by means of updating the

software at periodic intervals. The importance of ensuring that the related systems in a

Feb)

(Source: Author’s Creation)

Answer 13

Table 4: Sales Journal

Date Account Debited

Invoice

No. Amount

4-Jul John Green 6 2200

5-Jul John Green 7 2000

5-Jul Peter Brown 8 1100

7-Jul John Squires 9 125.9

31-Jul Total Transferred to Sales A/c 5425.9

(Source: Author’s Creation)

Table 5:Sales A/c

Date Description Amount Date Description Amount

- - - 31-Jul

Accounts

Receivable 5425.9

Accounts Receivable

Date Description Amount Date Description Amount

31-Jul Sales A/c 5425.9 - - -

(Source: Author’s Creation)

Answer 14 A& B

Table 4: Company’s Ledger A/c

Date Description

Amoun

t Date Description

Amoun

t

1/2/2015

Kmart Service

Station 365

5/2/201

5 Richardson 1300

28/2/2015 Bank A/c 1335

Profit & Loss

A/c 400

Answer 15

A continuous improvement or updating strategy implemented in an organization is the

process and policies that enables the management to stay focused on improving the activities

done on regular basis. Systems could be regularly maintained by means of updating the

software at periodic intervals. The importance of ensuring that the related systems in a

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

workplace are continuously updated is that it helps the management to prevent breakdown or

system hang, which might cause system failure, loss of productivity, hamper the proficiency

of the workforce, loss of capital and may other business losses. In addition to this,

Fagerholm, Guinea, Mäenpää and Münch (2017) in their work have contended that the

significance of continuous updating helps the organization to increased productivity, effective

software systems helps in keeping the workforce up to date with the modifications and

additions made thereof.

Answer 16

Lodging Cash with Financial Institutions

1. An organization can lodge deposit of cash with financial institutions by either

transferring the money in electronic form (Tyson, 2015).

2. Agent of the organization can lodge cash by visiting the institution and filling the cash

deposit sheet and submit the same for the necessary action.

3. Another way to lodge cash with the financial institution is by mobile transfer. Due to

advancement in technology, there are a number of people who have opted for such

facilities and now transfer funds through mobile banking apps for the purpose of

lodging cash without any delay, compared to the manual system of cash deposit.

Lodging Non-Cash Items with Financial Institutions

1. For non-cash items, the company can either fill up a cheque or a demand draft deposit

slip and submit the same at the nearby branch.

2. The non-cash items can be deposited by online transaction system which is available

at the website of the Financial institutions (Tyson, 2015).

3. Another way to lodge non-cash item is through agents appointed by the company.

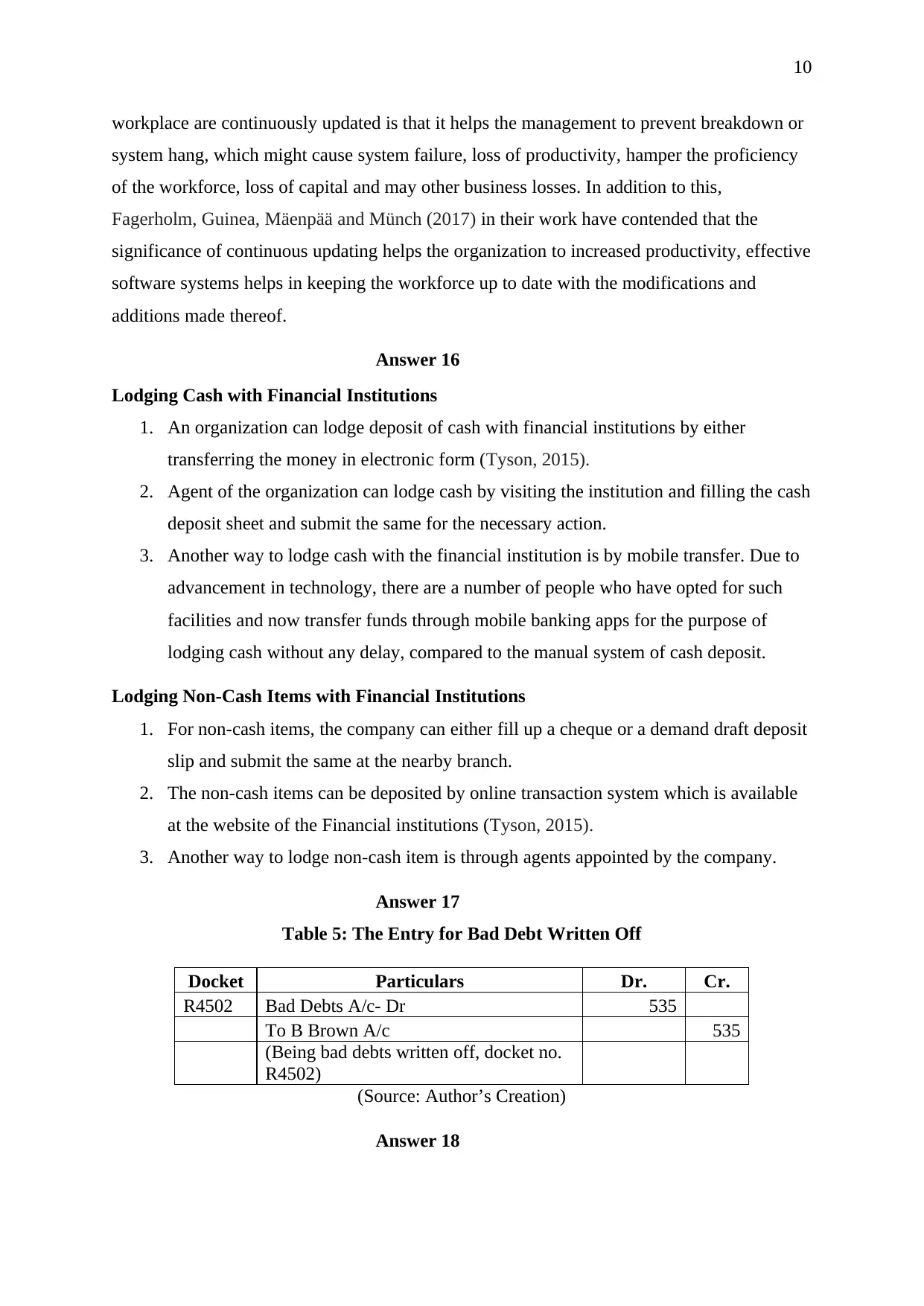

Answer 17

Table 5: The Entry for Bad Debt Written Off

Docket Particulars Dr. Cr.

R4502 Bad Debts A/c- Dr 535

To B Brown A/c 535

(Being bad debts written off, docket no.

R4502)

(Source: Author’s Creation)

Answer 18

workplace are continuously updated is that it helps the management to prevent breakdown or

system hang, which might cause system failure, loss of productivity, hamper the proficiency

of the workforce, loss of capital and may other business losses. In addition to this,

Fagerholm, Guinea, Mäenpää and Münch (2017) in their work have contended that the

significance of continuous updating helps the organization to increased productivity, effective

software systems helps in keeping the workforce up to date with the modifications and

additions made thereof.

Answer 16

Lodging Cash with Financial Institutions

1. An organization can lodge deposit of cash with financial institutions by either

transferring the money in electronic form (Tyson, 2015).

2. Agent of the organization can lodge cash by visiting the institution and filling the cash

deposit sheet and submit the same for the necessary action.

3. Another way to lodge cash with the financial institution is by mobile transfer. Due to

advancement in technology, there are a number of people who have opted for such

facilities and now transfer funds through mobile banking apps for the purpose of

lodging cash without any delay, compared to the manual system of cash deposit.

Lodging Non-Cash Items with Financial Institutions

1. For non-cash items, the company can either fill up a cheque or a demand draft deposit

slip and submit the same at the nearby branch.

2. The non-cash items can be deposited by online transaction system which is available

at the website of the Financial institutions (Tyson, 2015).

3. Another way to lodge non-cash item is through agents appointed by the company.

Answer 17

Table 5: The Entry for Bad Debt Written Off

Docket Particulars Dr. Cr.

R4502 Bad Debts A/c- Dr 535

To B Brown A/c 535

(Being bad debts written off, docket no.

R4502)

(Source: Author’s Creation)

Answer 18

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

In the era of globalization, there are a number of organizations that have been

established all over the world. Due to rise in competition in the world market the employers

have adopted diverse techniques and process to retain their employees. However, there are a

number of safety precautions that have been dealt with in the legislation and many

organizations too have adopted programs and strategies for ensuring protection of health,

safety and welfare of their employees. The safety precautions that can be taken by the

employees according to the legislative requirements and the organisational policies and

procedures are as follows:

1. Following all banking laws- many of the financial institutions are required to take

very explicit security steps, for the purpose of ensuring that the financial

information’s are protected appropriately

2. Scrutinization of employment practices- It is the responsibility of the employers

to hire professionals who are able to perform their duties accurately and with

little risk of mistakes or errors because failure to enter any transaction precisely

might lead to financial loss to the institution.

3. Instituting a strong security system- It is the duty of the employers and the

employees of the financial institutions to take safeguard against loss of financial

data. It may include instituting diverse safes as well as implementation of digital

security systems.

4. Keeping the security personnel at all times- The financial institutions have been

regarded as the financial hub for the cash and non-cash items deposited by

individuals as well as corporations. Therefore, it is necessary for the employers to

maintain safety and security at all times. This may include hiring security guards,

cyber security experts, as well as other relevant systems so as to ensure safety.

Employers and employees have rights and responsibilities under Work, Health and

Safety Legislation. The Security Regulations in the financial services industry is of immense

importance as per legislative requirements. According to the point of view of the scholar

(Rejda, 2011), despite of advanced security systems and strategies, there has always remained

a chance of insurance risks. It is the responsibility of both the employers and the employees

to have a complete knowledge with regard to such safety precautions. Therefore, there are a

number of business insurance which can be protect the employers and the employees of

financial institutions, namely, commercial property insurance, cyber liability insurance,

umbrella insurance and many others.

In the era of globalization, there are a number of organizations that have been

established all over the world. Due to rise in competition in the world market the employers

have adopted diverse techniques and process to retain their employees. However, there are a

number of safety precautions that have been dealt with in the legislation and many

organizations too have adopted programs and strategies for ensuring protection of health,

safety and welfare of their employees. The safety precautions that can be taken by the

employees according to the legislative requirements and the organisational policies and

procedures are as follows:

1. Following all banking laws- many of the financial institutions are required to take

very explicit security steps, for the purpose of ensuring that the financial

information’s are protected appropriately

2. Scrutinization of employment practices- It is the responsibility of the employers

to hire professionals who are able to perform their duties accurately and with

little risk of mistakes or errors because failure to enter any transaction precisely

might lead to financial loss to the institution.

3. Instituting a strong security system- It is the duty of the employers and the

employees of the financial institutions to take safeguard against loss of financial

data. It may include instituting diverse safes as well as implementation of digital

security systems.

4. Keeping the security personnel at all times- The financial institutions have been

regarded as the financial hub for the cash and non-cash items deposited by

individuals as well as corporations. Therefore, it is necessary for the employers to

maintain safety and security at all times. This may include hiring security guards,

cyber security experts, as well as other relevant systems so as to ensure safety.

Employers and employees have rights and responsibilities under Work, Health and

Safety Legislation. The Security Regulations in the financial services industry is of immense

importance as per legislative requirements. According to the point of view of the scholar

(Rejda, 2011), despite of advanced security systems and strategies, there has always remained

a chance of insurance risks. It is the responsibility of both the employers and the employees

to have a complete knowledge with regard to such safety precautions. Therefore, there are a

number of business insurance which can be protect the employers and the employees of

financial institutions, namely, commercial property insurance, cyber liability insurance,

umbrella insurance and many others.

12

Answer 19

When money is deposited at a bank, the bank-teller checks the cash, cheques as well

as the credit card details for the purpose of ensuring that it balances. The bank-teller then

stamps the copy of the deposit as well as tear-off the leaflet attached to the deposit slip, which

serves as an evidence with regard to the deposit that has been made. The stamped deposit slip

will serve as the proof of lodgement. According to the point of view of the scholar German,

(2006), the proof of lodgement must be presented at the accounts section where it is be

checked as well as filed. The scholar in his work have emphasized that proof of lodgement is

an important document as it serves as a proof and evidence thereby making it an appropriate

record on the part of the bank as well as on the part of the depositors.

Answer 20

Worksheet

31st March

Debit Credit

Balance Sheet Accounts:

Accounts Receivable

Accounts Payable

Cash $7.58

Revenue and Expense Accounts:

Bad Debt Expense 150.00

Office Supplies

Bank Charges $7.58

Total

Answer 21

Based upon the instructions that has been provided, a complete cash and credit journal has

ben prepared in the excel sheet, that would be used for preparing the general ledger. Every

Answer 19

When money is deposited at a bank, the bank-teller checks the cash, cheques as well

as the credit card details for the purpose of ensuring that it balances. The bank-teller then

stamps the copy of the deposit as well as tear-off the leaflet attached to the deposit slip, which

serves as an evidence with regard to the deposit that has been made. The stamped deposit slip

will serve as the proof of lodgement. According to the point of view of the scholar German,

(2006), the proof of lodgement must be presented at the accounts section where it is be

checked as well as filed. The scholar in his work have emphasized that proof of lodgement is

an important document as it serves as a proof and evidence thereby making it an appropriate

record on the part of the bank as well as on the part of the depositors.

Answer 20

Worksheet

31st March

Debit Credit

Balance Sheet Accounts:

Accounts Receivable

Accounts Payable

Cash $7.58

Revenue and Expense Accounts:

Bad Debt Expense 150.00

Office Supplies

Bank Charges $7.58

Total

Answer 21

Based upon the instructions that has been provided, a complete cash and credit journal has

ben prepared in the excel sheet, that would be used for preparing the general ledger. Every

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.