AF102 Introduction to Accounting: Product Costing Analysis Assignment

VerifiedAdded on 2022/12/15

|7

|905

|248

Homework Assignment

AI Summary

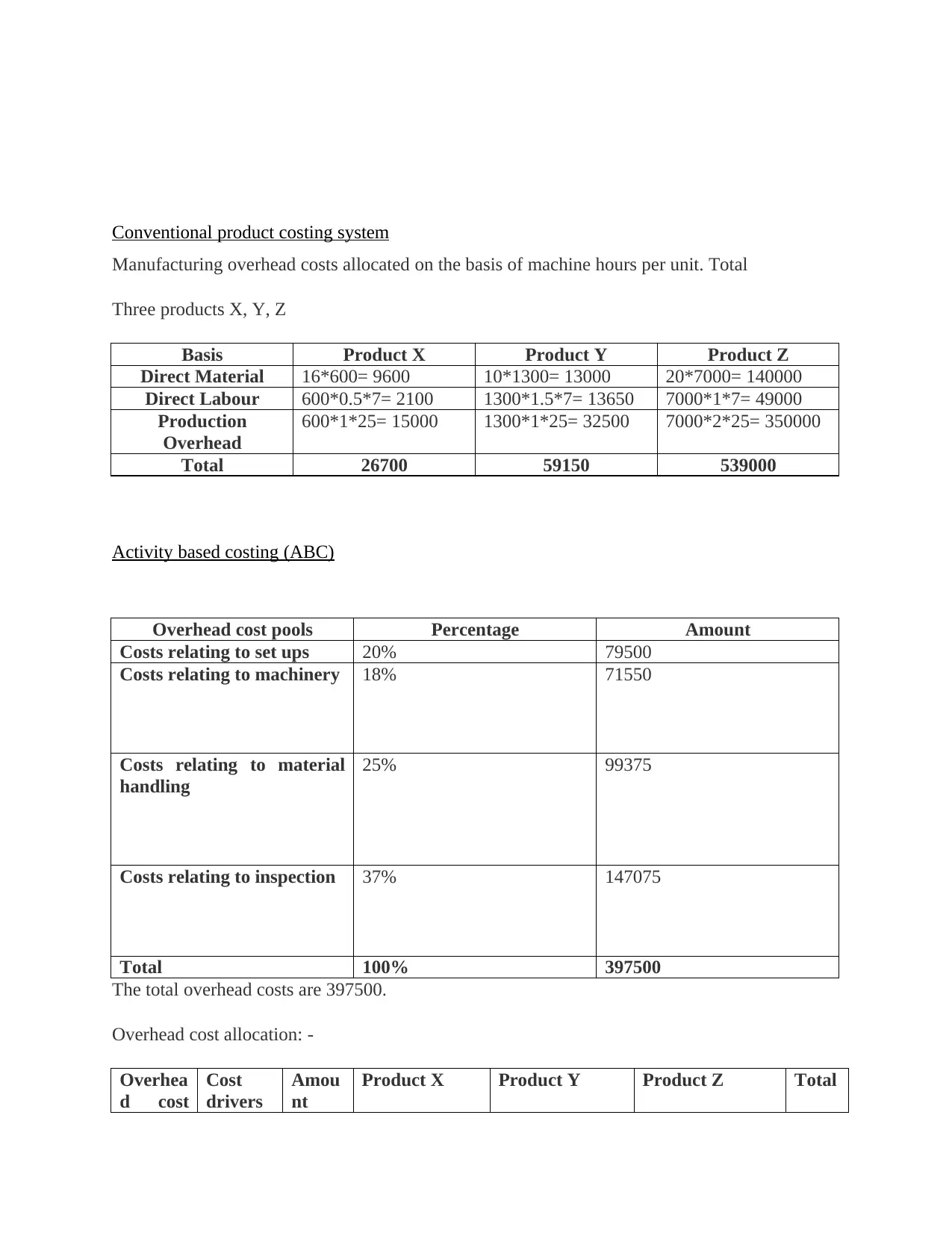

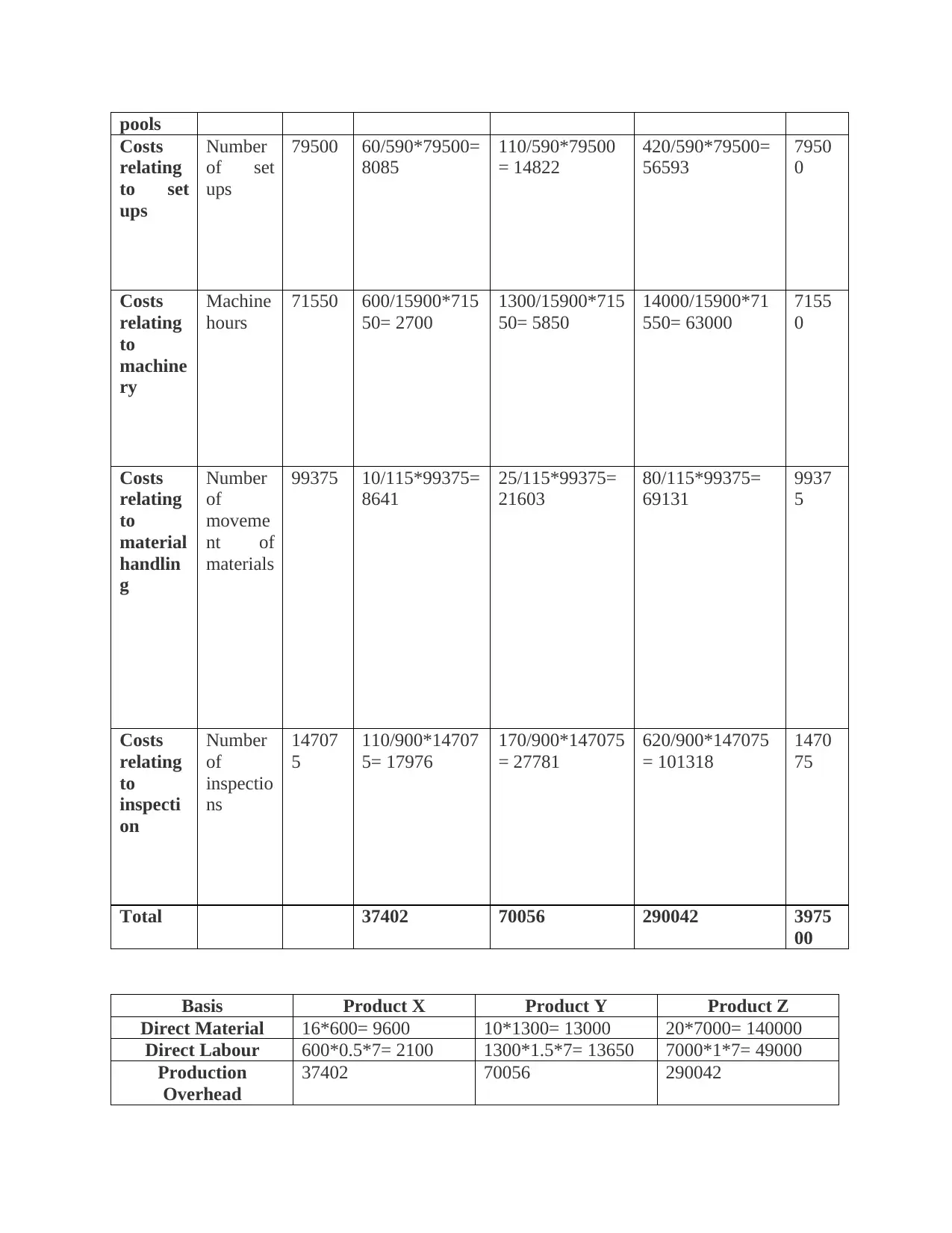

This assignment focuses on product costing methods, specifically comparing conventional product costing with activity-based costing (ABC). The solution includes calculations of cost per unit for three products (X, Y, Z) using both methods. It defines volume-based drivers and assesses the reasons for differences in per-unit costs between the two approaches. The assignment also explores activity-based management. The document provides detailed calculations of overhead allocation, including overhead cost pools and cost drivers for the ABC method. The student analyzes the impact of different costing methods on product profitability and decision-making. The analysis highlights how the choice of costing method affects the allocation of overhead costs and the resulting cost per unit for each product, which is crucial for informed business decisions.

1 out of 7

Related Documents

![Management Accounting: Costing Analysis of Office Desks - [Company]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fjv%2Fc197923795a34b81bdce50f667d18d4c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.