Performance Management and Control (ACC3MAC) Assignment: Budgeting

VerifiedAdded on 2022/09/14

|9

|1645

|40

Project

AI Summary

This project report details the process of product design and master budget preparation for a car navigation and location tracking system, proposed to address the needs of app cab drivers. The report outlines the product's design, vision, purposes, and goals, along with market research supporting its viability. It includes detailed cost estimations for materials, labor, and overhead, leading to the calculation of total product costs. A master budget is constructed, including raw materials, labor, and overhead budgets, projecting profitability based on estimated demand. The student reflects on the challenges and learning experiences gained through the assignment, emphasizing the practical application of financial planning and product development principles.

Running head: MANAGEMENT

Management

Name of the Student:

Name of the University:

Author’s Note:

Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Product design............................................................................................................................2

Proposed product....................................................................................................................2

Vision, purposes and goals of the business............................................................................3

Cost estimates.............................................................................................................................3

Production process and design of the product........................................................................3

Estimation of costs.................................................................................................................4

Master budget.............................................................................................................................5

Reflection...................................................................................................................................6

References and bibliography......................................................................................................8

Table of Contents

Introduction................................................................................................................................2

Product design............................................................................................................................2

Proposed product....................................................................................................................2

Vision, purposes and goals of the business............................................................................3

Cost estimates.............................................................................................................................3

Production process and design of the product........................................................................3

Estimation of costs.................................................................................................................4

Master budget.............................................................................................................................5

Reflection...................................................................................................................................6

References and bibliography......................................................................................................8

2MANAGEMENT

Introduction

Product designing and preparation of the master budget is the initial stage of

development and manufacturing of a product. In this report, the complete process of product

designing and preparation of master budget have been illustrated with the help of an example

of a new product. In the first part, the proposed product has been defined and its goals,

purposes have been outlined, and in the second part the costs and budget has been prepared

and explained (Kaplan and Atkinson 2015).

Product design

Proposed product

With revolution in technology, the automobile industry has been rapidly grown up.

The app cab service has also been increased worldwide with the revolution in technology and

development in the economy. Most of the app cab drivers use their phone for location

tracking and navigation. Therefore, there is a need of a highly automated location tracking

and navigation system in cars especially for the app cab drivers. The product proposed in this

report is a location tracking and navigation system with a display unit which can be fitted into

any type of cars. An abstract image of the proposed product has been attached below.

Introduction

Product designing and preparation of the master budget is the initial stage of

development and manufacturing of a product. In this report, the complete process of product

designing and preparation of master budget have been illustrated with the help of an example

of a new product. In the first part, the proposed product has been defined and its goals,

purposes have been outlined, and in the second part the costs and budget has been prepared

and explained (Kaplan and Atkinson 2015).

Product design

Proposed product

With revolution in technology, the automobile industry has been rapidly grown up.

The app cab service has also been increased worldwide with the revolution in technology and

development in the economy. Most of the app cab drivers use their phone for location

tracking and navigation. Therefore, there is a need of a highly automated location tracking

and navigation system in cars especially for the app cab drivers. The product proposed in this

report is a location tracking and navigation system with a display unit which can be fitted into

any type of cars. An abstract image of the proposed product has been attached below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT

It has been observed from various market researches that, some of the premium

automobile companies provide navigation system inbuilt with the cars, but in low priced

vehicle it is missing. Hence, a compatible location control and navigation system can be a

game changer in this case. It will have a security system too which sends notification to the

owner if anything happens with the car and locks the ignition automatically in that situation

(Dissanayake and Sinha 2015).

Vision, purposes and goals of the business

The vision of the business is to become the market leader in manufacturing and

selling car essentials and car accessories. The proposed product that is the location control

and navigation system with a security measure will help the company to go one step ahead in

accomplishing the vision of their business. The purpose of the business is to manufacture and

sell car accessories and car essentials to serve the customers with better experience in using

their cars and automobiles. The product has been proposed keeping in mind the vision and

purposes of the business and the goal of the business is to establish a brand in manufacturing

and selling car essentials and car accessories by serving their customers with unique and

technologically developed quality products.

Cost estimates

Production process and design of the product

The device has been designed to be compact and compatible for all the cars. It can be

mounted to the windshield by a vacuum mounting kit or it can be placed to the dashboard of

the car. The dimension of the devices would be of 4 inches by 5 inches and it will wait

approx 0.25kg. Most of the parts of the product will be outsourced and it will be assembled

in-house. The devise will have 4 inches by 4.5inches LED display which will be purchased

It has been observed from various market researches that, some of the premium

automobile companies provide navigation system inbuilt with the cars, but in low priced

vehicle it is missing. Hence, a compatible location control and navigation system can be a

game changer in this case. It will have a security system too which sends notification to the

owner if anything happens with the car and locks the ignition automatically in that situation

(Dissanayake and Sinha 2015).

Vision, purposes and goals of the business

The vision of the business is to become the market leader in manufacturing and

selling car essentials and car accessories. The proposed product that is the location control

and navigation system with a security measure will help the company to go one step ahead in

accomplishing the vision of their business. The purpose of the business is to manufacture and

sell car accessories and car essentials to serve the customers with better experience in using

their cars and automobiles. The product has been proposed keeping in mind the vision and

purposes of the business and the goal of the business is to establish a brand in manufacturing

and selling car essentials and car accessories by serving their customers with unique and

technologically developed quality products.

Cost estimates

Production process and design of the product

The device has been designed to be compact and compatible for all the cars. It can be

mounted to the windshield by a vacuum mounting kit or it can be placed to the dashboard of

the car. The dimension of the devices would be of 4 inches by 5 inches and it will wait

approx 0.25kg. Most of the parts of the product will be outsourced and it will be assembled

in-house. The devise will have 4 inches by 4.5inches LED display which will be purchased

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT

from a local supplier. The electronic circuit will be assembled and installed in-house along

with a GPS tracker and a motion sensor (Rauch, Dallasega and Matt 2016).

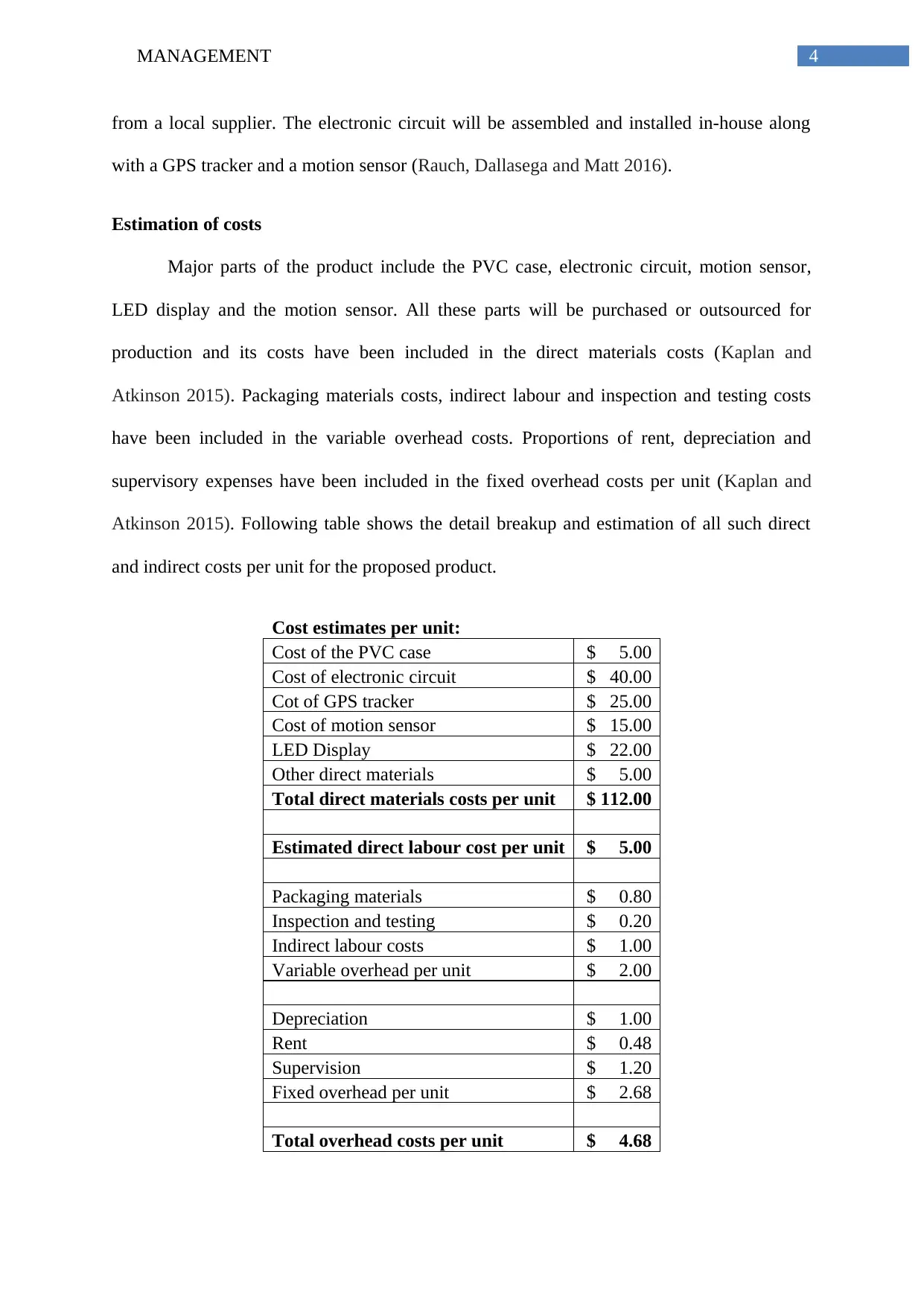

Estimation of costs

Major parts of the product include the PVC case, electronic circuit, motion sensor,

LED display and the motion sensor. All these parts will be purchased or outsourced for

production and its costs have been included in the direct materials costs (Kaplan and

Atkinson 2015). Packaging materials costs, indirect labour and inspection and testing costs

have been included in the variable overhead costs. Proportions of rent, depreciation and

supervisory expenses have been included in the fixed overhead costs per unit (Kaplan and

Atkinson 2015). Following table shows the detail breakup and estimation of all such direct

and indirect costs per unit for the proposed product.

Cost estimates per unit:

Cost of the PVC case $ 5.00

Cost of electronic circuit $ 40.00

Cot of GPS tracker $ 25.00

Cost of motion sensor $ 15.00

LED Display $ 22.00

Other direct materials $ 5.00

Total direct materials costs per unit $ 112.00

Estimated direct labour cost per unit $ 5.00

Packaging materials $ 0.80

Inspection and testing $ 0.20

Indirect labour costs $ 1.00

Variable overhead per unit $ 2.00

Depreciation $ 1.00

Rent $ 0.48

Supervision $ 1.20

Fixed overhead per unit $ 2.68

Total overhead costs per unit $ 4.68

from a local supplier. The electronic circuit will be assembled and installed in-house along

with a GPS tracker and a motion sensor (Rauch, Dallasega and Matt 2016).

Estimation of costs

Major parts of the product include the PVC case, electronic circuit, motion sensor,

LED display and the motion sensor. All these parts will be purchased or outsourced for

production and its costs have been included in the direct materials costs (Kaplan and

Atkinson 2015). Packaging materials costs, indirect labour and inspection and testing costs

have been included in the variable overhead costs. Proportions of rent, depreciation and

supervisory expenses have been included in the fixed overhead costs per unit (Kaplan and

Atkinson 2015). Following table shows the detail breakup and estimation of all such direct

and indirect costs per unit for the proposed product.

Cost estimates per unit:

Cost of the PVC case $ 5.00

Cost of electronic circuit $ 40.00

Cot of GPS tracker $ 25.00

Cost of motion sensor $ 15.00

LED Display $ 22.00

Other direct materials $ 5.00

Total direct materials costs per unit $ 112.00

Estimated direct labour cost per unit $ 5.00

Packaging materials $ 0.80

Inspection and testing $ 0.20

Indirect labour costs $ 1.00

Variable overhead per unit $ 2.00

Depreciation $ 1.00

Rent $ 0.48

Supervision $ 1.20

Fixed overhead per unit $ 2.68

Total overhead costs per unit $ 4.68

5MANAGEMENT

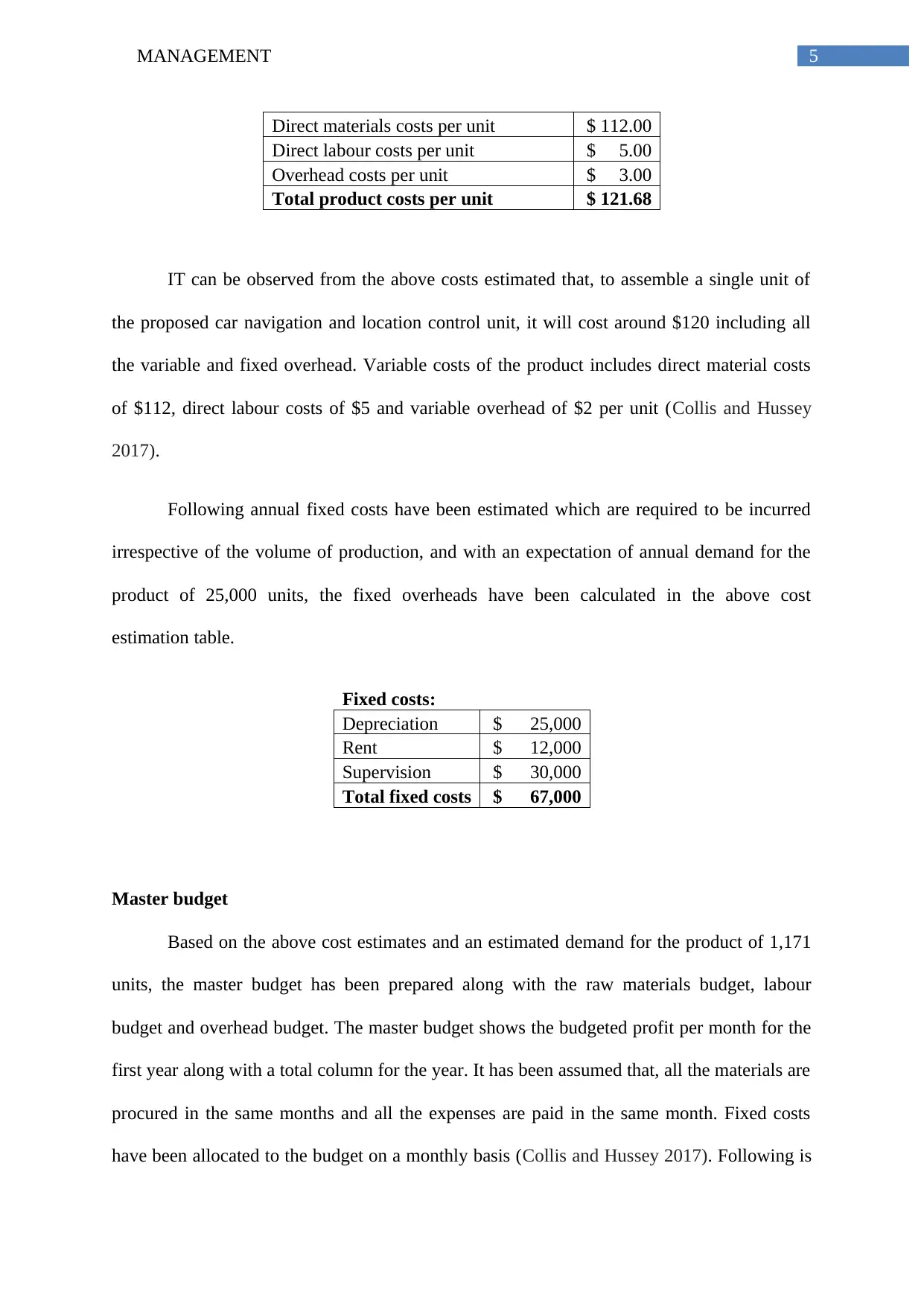

Direct materials costs per unit $ 112.00

Direct labour costs per unit $ 5.00

Overhead costs per unit $ 3.00

Total product costs per unit $ 121.68

IT can be observed from the above costs estimated that, to assemble a single unit of

the proposed car navigation and location control unit, it will cost around $120 including all

the variable and fixed overhead. Variable costs of the product includes direct material costs

of $112, direct labour costs of $5 and variable overhead of $2 per unit (Collis and Hussey

2017).

Following annual fixed costs have been estimated which are required to be incurred

irrespective of the volume of production, and with an expectation of annual demand for the

product of 25,000 units, the fixed overheads have been calculated in the above cost

estimation table.

Fixed costs:

Depreciation $ 25,000

Rent $ 12,000

Supervision $ 30,000

Total fixed costs $ 67,000

Master budget

Based on the above cost estimates and an estimated demand for the product of 1,171

units, the master budget has been prepared along with the raw materials budget, labour

budget and overhead budget. The master budget shows the budgeted profit per month for the

first year along with a total column for the year. It has been assumed that, all the materials are

procured in the same months and all the expenses are paid in the same month. Fixed costs

have been allocated to the budget on a monthly basis (Collis and Hussey 2017). Following is

Direct materials costs per unit $ 112.00

Direct labour costs per unit $ 5.00

Overhead costs per unit $ 3.00

Total product costs per unit $ 121.68

IT can be observed from the above costs estimated that, to assemble a single unit of

the proposed car navigation and location control unit, it will cost around $120 including all

the variable and fixed overhead. Variable costs of the product includes direct material costs

of $112, direct labour costs of $5 and variable overhead of $2 per unit (Collis and Hussey

2017).

Following annual fixed costs have been estimated which are required to be incurred

irrespective of the volume of production, and with an expectation of annual demand for the

product of 25,000 units, the fixed overheads have been calculated in the above cost

estimation table.

Fixed costs:

Depreciation $ 25,000

Rent $ 12,000

Supervision $ 30,000

Total fixed costs $ 67,000

Master budget

Based on the above cost estimates and an estimated demand for the product of 1,171

units, the master budget has been prepared along with the raw materials budget, labour

budget and overhead budget. The master budget shows the budgeted profit per month for the

first year along with a total column for the year. It has been assumed that, all the materials are

procured in the same months and all the expenses are paid in the same month. Fixed costs

have been allocated to the budget on a monthly basis (Collis and Hussey 2017). Following is

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT

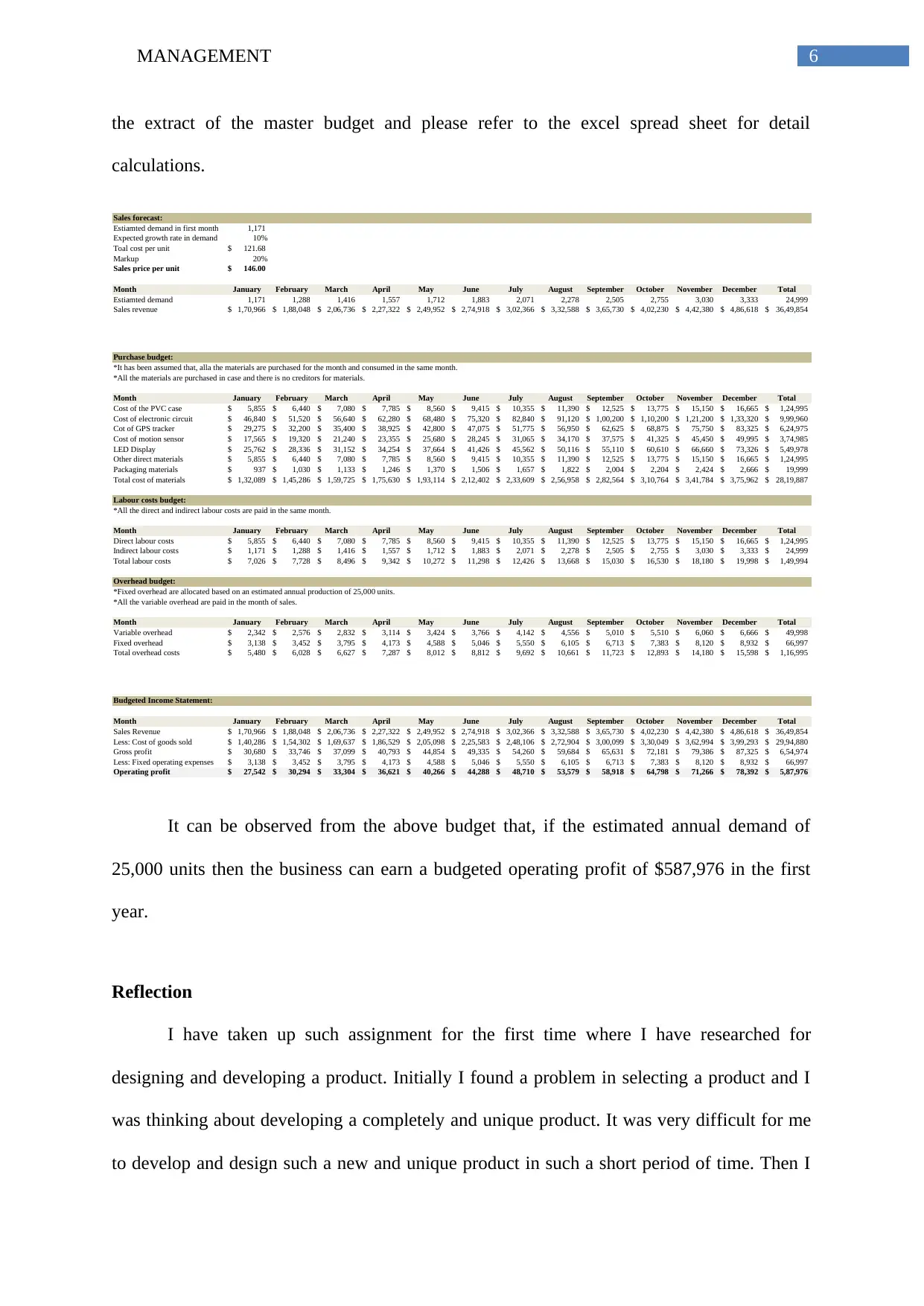

the extract of the master budget and please refer to the excel spread sheet for detail

calculations.

Sales forecast:

Estiamted demand in first month 1,171

Expected growth rate in demand 10%

Toal cost per unit 121.68$

Markup 20%

Sales price per unit 146.00$

Month January February March April May June July August September October November December Total

Estiamted demand 1,171 1,288 1,416 1,557 1,712 1,883 2,071 2,278 2,505 2,755 3,030 3,333 24,999

Sales revenue 1,70,966$ 1,88,048$ 2,06,736$ 2,27,322$ 2,49,952$ 2,74,918$ 3,02,366$ 3,32,588$ 3,65,730$ 4,02,230$ 4,42,380$ 4,86,618$ 36,49,854$

Purchase budget:

*It has been assumed that, alla the materials are purchased for the month and consumed in the same month.

*All the materials are purchased in case and there is no creditors for materials.

Month January February March April May June July August September October November December Total

Cost of the PVC case 5,855$ 6,440$ 7,080$ 7,785$ 8,560$ 9,415$ 10,355$ 11,390$ 12,525$ 13,775$ 15,150$ 16,665$ 1,24,995$

Cost of electronic circuit 46,840$ 51,520$ 56,640$ 62,280$ 68,480$ 75,320$ 82,840$ 91,120$ 1,00,200$ 1,10,200$ 1,21,200$ 1,33,320$ 9,99,960$

Cot of GPS tracker 29,275$ 32,200$ 35,400$ 38,925$ 42,800$ 47,075$ 51,775$ 56,950$ 62,625$ 68,875$ 75,750$ 83,325$ 6,24,975$

Cost of motion sensor 17,565$ 19,320$ 21,240$ 23,355$ 25,680$ 28,245$ 31,065$ 34,170$ 37,575$ 41,325$ 45,450$ 49,995$ 3,74,985$

LED Display 25,762$ 28,336$ 31,152$ 34,254$ 37,664$ 41,426$ 45,562$ 50,116$ 55,110$ 60,610$ 66,660$ 73,326$ 5,49,978$

Other direct materials 5,855$ 6,440$ 7,080$ 7,785$ 8,560$ 9,415$ 10,355$ 11,390$ 12,525$ 13,775$ 15,150$ 16,665$ 1,24,995$

Packaging materials 937$ 1,030$ 1,133$ 1,246$ 1,370$ 1,506$ 1,657$ 1,822$ 2,004$ 2,204$ 2,424$ 2,666$ 19,999$

Total cost of materials 1,32,089$ 1,45,286$ 1,59,725$ 1,75,630$ 1,93,114$ 2,12,402$ 2,33,609$ 2,56,958$ 2,82,564$ 3,10,764$ 3,41,784$ 3,75,962$ 28,19,887$

Labour costs budget:

*All the direct and indirect labour costs are paid in the same month.

Month January February March April May June July August September October November December Total

Direct labour costs 5,855$ 6,440$ 7,080$ 7,785$ 8,560$ 9,415$ 10,355$ 11,390$ 12,525$ 13,775$ 15,150$ 16,665$ 1,24,995$

Indirect labour costs 1,171$ 1,288$ 1,416$ 1,557$ 1,712$ 1,883$ 2,071$ 2,278$ 2,505$ 2,755$ 3,030$ 3,333$ 24,999$

Total labour costs 7,026$ 7,728$ 8,496$ 9,342$ 10,272$ 11,298$ 12,426$ 13,668$ 15,030$ 16,530$ 18,180$ 19,998$ 1,49,994$

Overhead budget:

*Fixed overhead are allocated based on an estimated annual production of 25,000 units.

*All the variable overhead are paid in the month of sales.

Month January February March April May June July August September October November December Total

Variable overhead 2,342$ 2,576$ 2,832$ 3,114$ 3,424$ 3,766$ 4,142$ 4,556$ 5,010$ 5,510$ 6,060$ 6,666$ 49,998$

Fixed overhead 3,138$ 3,452$ 3,795$ 4,173$ 4,588$ 5,046$ 5,550$ 6,105$ 6,713$ 7,383$ 8,120$ 8,932$ 66,997$

Total overhead costs 5,480$ 6,028$ 6,627$ 7,287$ 8,012$ 8,812$ 9,692$ 10,661$ 11,723$ 12,893$ 14,180$ 15,598$ 1,16,995$

Budgeted Income Statement:

Month January February March April May June July August September October November December Total

Sales Revenue 1,70,966$ 1,88,048$ 2,06,736$ 2,27,322$ 2,49,952$ 2,74,918$ 3,02,366$ 3,32,588$ 3,65,730$ 4,02,230$ 4,42,380$ 4,86,618$ 36,49,854$

Less: Cost of goods sold 1,40,286$ 1,54,302$ 1,69,637$ 1,86,529$ 2,05,098$ 2,25,583$ 2,48,106$ 2,72,904$ 3,00,099$ 3,30,049$ 3,62,994$ 3,99,293$ 29,94,880$

Gross profit 30,680$ 33,746$ 37,099$ 40,793$ 44,854$ 49,335$ 54,260$ 59,684$ 65,631$ 72,181$ 79,386$ 87,325$ 6,54,974$

Less: Fixed operating expenses 3,138$ 3,452$ 3,795$ 4,173$ 4,588$ 5,046$ 5,550$ 6,105$ 6,713$ 7,383$ 8,120$ 8,932$ 66,997$

Operating profit 27,542$ 30,294$ 33,304$ 36,621$ 40,266$ 44,288$ 48,710$ 53,579$ 58,918$ 64,798$ 71,266$ 78,392$ 5,87,976$

It can be observed from the above budget that, if the estimated annual demand of

25,000 units then the business can earn a budgeted operating profit of $587,976 in the first

year.

Reflection

I have taken up such assignment for the first time where I have researched for

designing and developing a product. Initially I found a problem in selecting a product and I

was thinking about developing a completely and unique product. It was very difficult for me

to develop and design such a new and unique product in such a short period of time. Then I

the extract of the master budget and please refer to the excel spread sheet for detail

calculations.

Sales forecast:

Estiamted demand in first month 1,171

Expected growth rate in demand 10%

Toal cost per unit 121.68$

Markup 20%

Sales price per unit 146.00$

Month January February March April May June July August September October November December Total

Estiamted demand 1,171 1,288 1,416 1,557 1,712 1,883 2,071 2,278 2,505 2,755 3,030 3,333 24,999

Sales revenue 1,70,966$ 1,88,048$ 2,06,736$ 2,27,322$ 2,49,952$ 2,74,918$ 3,02,366$ 3,32,588$ 3,65,730$ 4,02,230$ 4,42,380$ 4,86,618$ 36,49,854$

Purchase budget:

*It has been assumed that, alla the materials are purchased for the month and consumed in the same month.

*All the materials are purchased in case and there is no creditors for materials.

Month January February March April May June July August September October November December Total

Cost of the PVC case 5,855$ 6,440$ 7,080$ 7,785$ 8,560$ 9,415$ 10,355$ 11,390$ 12,525$ 13,775$ 15,150$ 16,665$ 1,24,995$

Cost of electronic circuit 46,840$ 51,520$ 56,640$ 62,280$ 68,480$ 75,320$ 82,840$ 91,120$ 1,00,200$ 1,10,200$ 1,21,200$ 1,33,320$ 9,99,960$

Cot of GPS tracker 29,275$ 32,200$ 35,400$ 38,925$ 42,800$ 47,075$ 51,775$ 56,950$ 62,625$ 68,875$ 75,750$ 83,325$ 6,24,975$

Cost of motion sensor 17,565$ 19,320$ 21,240$ 23,355$ 25,680$ 28,245$ 31,065$ 34,170$ 37,575$ 41,325$ 45,450$ 49,995$ 3,74,985$

LED Display 25,762$ 28,336$ 31,152$ 34,254$ 37,664$ 41,426$ 45,562$ 50,116$ 55,110$ 60,610$ 66,660$ 73,326$ 5,49,978$

Other direct materials 5,855$ 6,440$ 7,080$ 7,785$ 8,560$ 9,415$ 10,355$ 11,390$ 12,525$ 13,775$ 15,150$ 16,665$ 1,24,995$

Packaging materials 937$ 1,030$ 1,133$ 1,246$ 1,370$ 1,506$ 1,657$ 1,822$ 2,004$ 2,204$ 2,424$ 2,666$ 19,999$

Total cost of materials 1,32,089$ 1,45,286$ 1,59,725$ 1,75,630$ 1,93,114$ 2,12,402$ 2,33,609$ 2,56,958$ 2,82,564$ 3,10,764$ 3,41,784$ 3,75,962$ 28,19,887$

Labour costs budget:

*All the direct and indirect labour costs are paid in the same month.

Month January February March April May June July August September October November December Total

Direct labour costs 5,855$ 6,440$ 7,080$ 7,785$ 8,560$ 9,415$ 10,355$ 11,390$ 12,525$ 13,775$ 15,150$ 16,665$ 1,24,995$

Indirect labour costs 1,171$ 1,288$ 1,416$ 1,557$ 1,712$ 1,883$ 2,071$ 2,278$ 2,505$ 2,755$ 3,030$ 3,333$ 24,999$

Total labour costs 7,026$ 7,728$ 8,496$ 9,342$ 10,272$ 11,298$ 12,426$ 13,668$ 15,030$ 16,530$ 18,180$ 19,998$ 1,49,994$

Overhead budget:

*Fixed overhead are allocated based on an estimated annual production of 25,000 units.

*All the variable overhead are paid in the month of sales.

Month January February March April May June July August September October November December Total

Variable overhead 2,342$ 2,576$ 2,832$ 3,114$ 3,424$ 3,766$ 4,142$ 4,556$ 5,010$ 5,510$ 6,060$ 6,666$ 49,998$

Fixed overhead 3,138$ 3,452$ 3,795$ 4,173$ 4,588$ 5,046$ 5,550$ 6,105$ 6,713$ 7,383$ 8,120$ 8,932$ 66,997$

Total overhead costs 5,480$ 6,028$ 6,627$ 7,287$ 8,012$ 8,812$ 9,692$ 10,661$ 11,723$ 12,893$ 14,180$ 15,598$ 1,16,995$

Budgeted Income Statement:

Month January February March April May June July August September October November December Total

Sales Revenue 1,70,966$ 1,88,048$ 2,06,736$ 2,27,322$ 2,49,952$ 2,74,918$ 3,02,366$ 3,32,588$ 3,65,730$ 4,02,230$ 4,42,380$ 4,86,618$ 36,49,854$

Less: Cost of goods sold 1,40,286$ 1,54,302$ 1,69,637$ 1,86,529$ 2,05,098$ 2,25,583$ 2,48,106$ 2,72,904$ 3,00,099$ 3,30,049$ 3,62,994$ 3,99,293$ 29,94,880$

Gross profit 30,680$ 33,746$ 37,099$ 40,793$ 44,854$ 49,335$ 54,260$ 59,684$ 65,631$ 72,181$ 79,386$ 87,325$ 6,54,974$

Less: Fixed operating expenses 3,138$ 3,452$ 3,795$ 4,173$ 4,588$ 5,046$ 5,550$ 6,105$ 6,713$ 7,383$ 8,120$ 8,932$ 66,997$

Operating profit 27,542$ 30,294$ 33,304$ 36,621$ 40,266$ 44,288$ 48,710$ 53,579$ 58,918$ 64,798$ 71,266$ 78,392$ 5,87,976$

It can be observed from the above budget that, if the estimated annual demand of

25,000 units then the business can earn a budgeted operating profit of $587,976 in the first

year.

Reflection

I have taken up such assignment for the first time where I have researched for

designing and developing a product. Initially I found a problem in selecting a product and I

was thinking about developing a completely and unique product. It was very difficult for me

to develop and design such a new and unique product in such a short period of time. Then I

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT

went for searching for products which can be remodelled or redesigned with a completely

new dimension and purposes. I found potential for the product car navigation system and

location tracker including a security system. Writing about the vision, purposes and goals of

the business was easy for me but I found a great problem in researching about the designing

and manufacturing process of the product. Hence, I decided to outsource all the parts of the

product and developed the cost estimates and budgets accordingly. I have worked with excel

before and it was easy for me to prepare a master budget along with the details calculations

and breakups. Overall the assignment has given me ample opportunity to enhance my

knowledge and skill in developing and designing products and making budgets and estimates

for that.

went for searching for products which can be remodelled or redesigned with a completely

new dimension and purposes. I found potential for the product car navigation system and

location tracker including a security system. Writing about the vision, purposes and goals of

the business was easy for me but I found a great problem in researching about the designing

and manufacturing process of the product. Hence, I decided to outsource all the parts of the

product and developed the cost estimates and budgets accordingly. I have worked with excel

before and it was easy for me to prepare a master budget along with the details calculations

and breakups. Overall the assignment has given me ample opportunity to enhance my

knowledge and skill in developing and designing products and making budgets and estimates

for that.

8MANAGEMENT

References and bibliography

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

da Silva, G.C. and Kaminski, P.C., 2016. Selection of virtual and physical prototypes in the

product development process. The international journal of advanced manufacturing

technology, 84(5-8), pp.1513-1530.

Dissanayake, G. and Sinha, P., 2015. An examination of the product development process for

fashion remanufacturing. Resources, Conservation and Recycling, 104, pp.94-102.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kumar, S., Luthra, S., Govindan, K., Kumar, N. and Haleem, A., 2016. Barriers in green lean

six sigma product development process: an ISM approach. Production Planning &

Control, 27(7-8), pp.604-620.

Kyei, E., Kwaning, C.O. and Francis, D., 2015. Budgets and Budgetary Control as a

Management Tool for Ghana Metropolitan Assemblies. Journal of Finance and

Accounting, 3(5), p.159.

Nelson, A.T. and Miller, P.B., 2014. Modern management accounting. Australasian.

Accounting, Business and Finance Journal, 8, p.2.

Rauch, E., Dallasega, P. and Matt, D.T., 2016. The way from lean product development

(LPD) to smart product development (SPD). Procedia CIRP, 50, pp.26-31.

References and bibliography

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

da Silva, G.C. and Kaminski, P.C., 2016. Selection of virtual and physical prototypes in the

product development process. The international journal of advanced manufacturing

technology, 84(5-8), pp.1513-1530.

Dissanayake, G. and Sinha, P., 2015. An examination of the product development process for

fashion remanufacturing. Resources, Conservation and Recycling, 104, pp.94-102.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kumar, S., Luthra, S., Govindan, K., Kumar, N. and Haleem, A., 2016. Barriers in green lean

six sigma product development process: an ISM approach. Production Planning &

Control, 27(7-8), pp.604-620.

Kyei, E., Kwaning, C.O. and Francis, D., 2015. Budgets and Budgetary Control as a

Management Tool for Ghana Metropolitan Assemblies. Journal of Finance and

Accounting, 3(5), p.159.

Nelson, A.T. and Miller, P.B., 2014. Modern management accounting. Australasian.

Accounting, Business and Finance Journal, 8, p.2.

Rauch, E., Dallasega, P. and Matt, D.T., 2016. The way from lean product development

(LPD) to smart product development (SPD). Procedia CIRP, 50, pp.26-31.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.