Management Accounting Report: Variance and Production Analysis

VerifiedAdded on 2023/01/09

|11

|3090

|86

Report

AI Summary

This management accounting report examines the financial performance of XLG, a cleaning product manufacturer, focusing on variance analysis and production decisions. The report begins with an introduction to management accounting and its importance in decision-making, particularly for internal management. It then delves into Part A, which covers sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. The report provides calculations and critical analyses of these variances to assess the performance of managers. Part B of the report discusses the decision between in-house production and importing from Brazil, weighing the advantages and disadvantages of each option. The report includes detailed calculations, critical analysis, and a discussion of the merits and demerits of variance analysis. It also explores the implications of these decisions on supply chain management and overall company strategy, providing a comprehensive overview of the financial and operational considerations for XLG.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

PART A...........................................................................................................................................1

i) Sales Price variance and the sales volume contribution variance............................................1

ii) Material Price Planning Variance and the Material Price Operational Variance....................2

iii) Critical analysis of variances to analyse the performance of managers.................................3

PART B...........................................................................................................................................6

Report discussing over making in house production or to import from Brazil...........................6

REFERENCES................................................................................................................................9

TABLE OF CONTENTS................................................................................................................2

INTRODUTION..............................................................................................................................1

PART A...........................................................................................................................................1

i) Sales Price variance and the sales volume contribution variance............................................1

ii) Material Price Planning Variance and the Material Price Operational Variance....................2

iii) Critical analysis of variances to analyse the performance of managers.................................3

PART B...........................................................................................................................................6

Report discussing over making in house production or to import from Brazil...........................6

REFERENCES................................................................................................................................9

INTRODUTION

Management accounting is also called managerial accounting and is defined as the process

providing the financial information and the resources to managers in decision making. MA is

used mainly by internal management team of organisation and this makes it different from

financial accounting. MA focuses over accounting for providing information about the

operational business metric. It enables the manager to make effective decisions based on the

information provided by the company. Current report is based over XLG which is cleaning

product making company of Britain producing two cleaning agents. It has maintained leading

position in the market due to its solution famaQ. After the broke out of corona virus its

maximum sales were moved online. Also due to the pandemic prices of most of the goods have

risen. Report provides about the different variances to assess the efficient of managers. It also

wants to assess whether it should go for in-house making or to import it from Brazil only. Report

will enhance the understanding about variances and their importance in organisation.

PART A

i) Sales Price variance and the sales volume contribution variance

Sales price variance

The variance measures change in the sales revenues as result of the variance between

standard and actual selling prices. Actual sales could differ from the standard sales due to rise in

demand of the product. It can be due to several factors such as change in customer preference or

change in trend. It quantifies difference in the sales which results from different in the standard

price and market price.

Sales volume contribution variance

It measures the revenues brought in for company over actual sales volume against the

budgeted sales volume projections (D'Onza, Greco and Allegrini, 2016). It helps the business in

making more accurate estimate of revenues that products will be bringing in future.

Calculations

Sales and Contribution

X Y

Total Sales 595 595

Actual sales volume 850 750

Standard Sales Price 35 30

1

Management accounting is also called managerial accounting and is defined as the process

providing the financial information and the resources to managers in decision making. MA is

used mainly by internal management team of organisation and this makes it different from

financial accounting. MA focuses over accounting for providing information about the

operational business metric. It enables the manager to make effective decisions based on the

information provided by the company. Current report is based over XLG which is cleaning

product making company of Britain producing two cleaning agents. It has maintained leading

position in the market due to its solution famaQ. After the broke out of corona virus its

maximum sales were moved online. Also due to the pandemic prices of most of the goods have

risen. Report provides about the different variances to assess the efficient of managers. It also

wants to assess whether it should go for in-house making or to import it from Brazil only. Report

will enhance the understanding about variances and their importance in organisation.

PART A

i) Sales Price variance and the sales volume contribution variance

Sales price variance

The variance measures change in the sales revenues as result of the variance between

standard and actual selling prices. Actual sales could differ from the standard sales due to rise in

demand of the product. It can be due to several factors such as change in customer preference or

change in trend. It quantifies difference in the sales which results from different in the standard

price and market price.

Sales volume contribution variance

It measures the revenues brought in for company over actual sales volume against the

budgeted sales volume projections (D'Onza, Greco and Allegrini, 2016). It helps the business in

making more accurate estimate of revenues that products will be bringing in future.

Calculations

Sales and Contribution

X Y

Total Sales 595 595

Actual sales volume 850 750

Standard Sales Price 35 30

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Actual Sales price 45 37

Standard Margin 25 20

Sales Price Variance

(Actual price * Actual units sold) - (Standard price * Actual

units sold)

(45*850)-

(35*595)

(37*750)-

(30*595)

17425 9900

(Actual Price - Standard price) * Actual unit (45-35)*850 (37-30)*750

8500 5250

Sales volume contribution variance

Actual sales units -Budgeted sales units * Standard unit

profit

(850 - 595) *

25

( 750 -

595 )*20

6375 3100

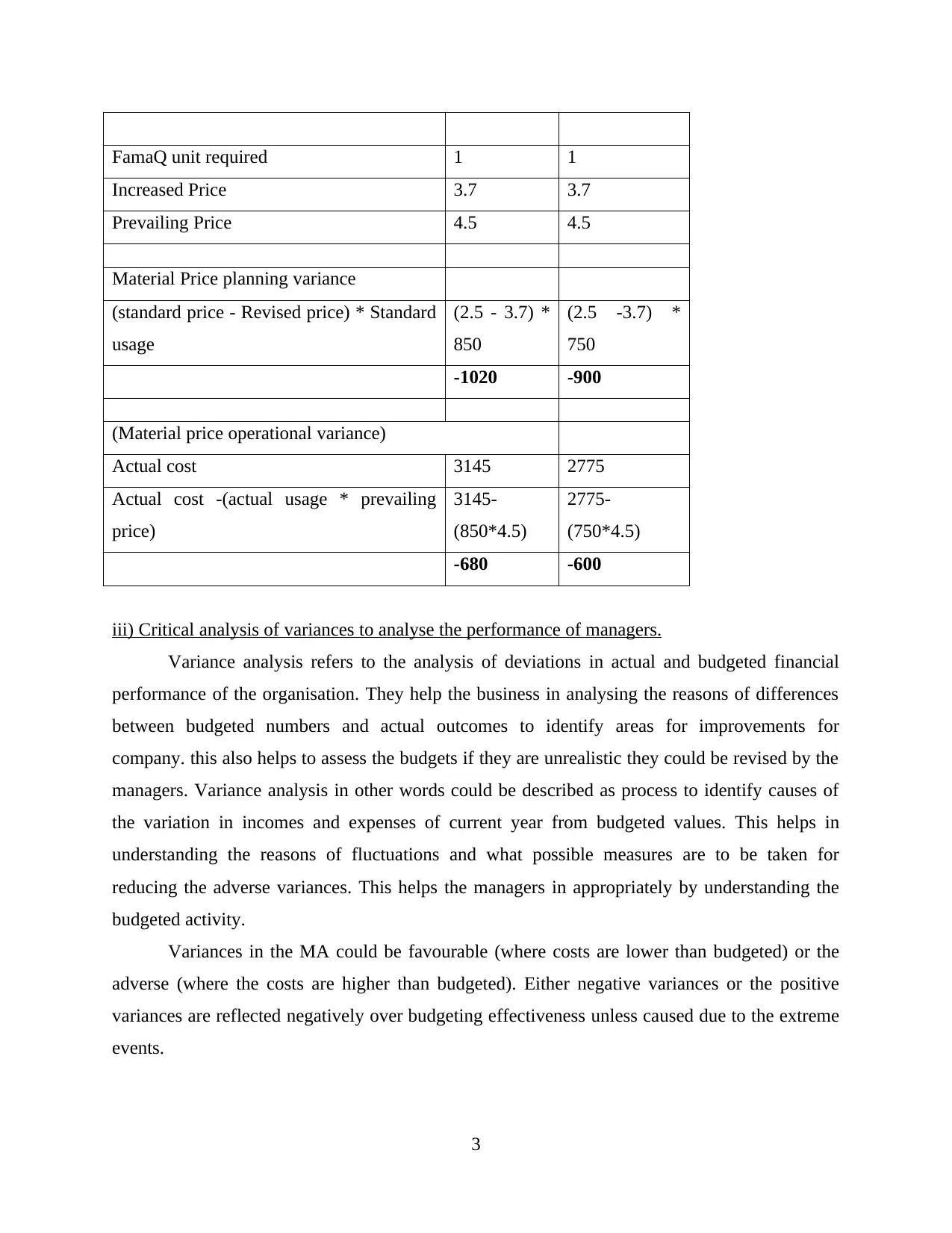

ii) Material Price Planning Variance and the Material Price Operational Variance.

Material Price Planning Variance

Planning variance are used for measuring extent to which original standards are required

to be adjusted for reflecting the changes in operational conditions between current situation and

one envisaged at time of calculating the standards.

Material Price Operational Variance

Operational variances indicate extent to which the attainable targets are achieved. The

operational variance is calculated after planning variances are established and this is more

realistic manner of assessing (Marzlin Marzuki and Ismail, 2019). Both the variances play an

important role in assessing the performance of company and its managers.

Calculations

Material Price

X Y

Actual sales volume 850 750

Standard Price 2.5 2.5

2

Standard Margin 25 20

Sales Price Variance

(Actual price * Actual units sold) - (Standard price * Actual

units sold)

(45*850)-

(35*595)

(37*750)-

(30*595)

17425 9900

(Actual Price - Standard price) * Actual unit (45-35)*850 (37-30)*750

8500 5250

Sales volume contribution variance

Actual sales units -Budgeted sales units * Standard unit

profit

(850 - 595) *

25

( 750 -

595 )*20

6375 3100

ii) Material Price Planning Variance and the Material Price Operational Variance.

Material Price Planning Variance

Planning variance are used for measuring extent to which original standards are required

to be adjusted for reflecting the changes in operational conditions between current situation and

one envisaged at time of calculating the standards.

Material Price Operational Variance

Operational variances indicate extent to which the attainable targets are achieved. The

operational variance is calculated after planning variances are established and this is more

realistic manner of assessing (Marzlin Marzuki and Ismail, 2019). Both the variances play an

important role in assessing the performance of company and its managers.

Calculations

Material Price

X Y

Actual sales volume 850 750

Standard Price 2.5 2.5

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FamaQ unit required 1 1

Increased Price 3.7 3.7

Prevailing Price 4.5 4.5

Material Price planning variance

(standard price - Revised price) * Standard

usage

(2.5 - 3.7) *

850

(2.5 -3.7) *

750

-1020 -900

(Material price operational variance)

Actual cost 3145 2775

Actual cost -(actual usage * prevailing

price)

3145-

(850*4.5)

2775-

(750*4.5)

-680 -600

iii) Critical analysis of variances to analyse the performance of managers.

Variance analysis refers to the analysis of deviations in actual and budgeted financial

performance of the organisation. They help the business in analysing the reasons of differences

between budgeted numbers and actual outcomes to identify areas for improvements for

company. this also helps to assess the budgets if they are unrealistic they could be revised by the

managers. Variance analysis in other words could be described as process to identify causes of

the variation in incomes and expenses of current year from budgeted values. This helps in

understanding the reasons of fluctuations and what possible measures are to be taken for

reducing the adverse variances. This helps the managers in appropriately by understanding the

budgeted activity.

Variances in the MA could be favourable (where costs are lower than budgeted) or the

adverse (where the costs are higher than budgeted). Either negative variances or the positive

variances are reflected negatively over budgeting effectiveness unless caused due to the extreme

events.

3

Increased Price 3.7 3.7

Prevailing Price 4.5 4.5

Material Price planning variance

(standard price - Revised price) * Standard

usage

(2.5 - 3.7) *

850

(2.5 -3.7) *

750

-1020 -900

(Material price operational variance)

Actual cost 3145 2775

Actual cost -(actual usage * prevailing

price)

3145-

(850*4.5)

2775-

(750*4.5)

-680 -600

iii) Critical analysis of variances to analyse the performance of managers.

Variance analysis refers to the analysis of deviations in actual and budgeted financial

performance of the organisation. They help the business in analysing the reasons of differences

between budgeted numbers and actual outcomes to identify areas for improvements for

company. this also helps to assess the budgets if they are unrealistic they could be revised by the

managers. Variance analysis in other words could be described as process to identify causes of

the variation in incomes and expenses of current year from budgeted values. This helps in

understanding the reasons of fluctuations and what possible measures are to be taken for

reducing the adverse variances. This helps the managers in appropriately by understanding the

budgeted activity.

Variances in the MA could be favourable (where costs are lower than budgeted) or the

adverse (where the costs are higher than budgeted). Either negative variances or the positive

variances are reflected negatively over budgeting effectiveness unless caused due to the extreme

events.

3

Variance analysis helps the management in effective budgeting activities that the

management wishes for having lower deviations from planned budgets. Lower deviations leads

the managers in making detailed as well as forward looking the budgetary decisions. it works as

the control mechanism (Zhang, 2017). Carrying out analysis of the significant deviations over

essential items help company for knowing the issues and also helps management for looking into

the possible manner about the deviations that could be avoided.

The variance analysis helps the managers in allocation of the roles and responsibilities

and also engages the control mechanism over the departments where it is most required. For

instance if the labour efficiency variances are seen unfavourable or the procurement of the raw

materials cost variance is also unfavourable, management could enhance the control over

departments for increasing the efficiency.

Merits and demerits of the variance analysis

Process of the variance analysis is easy and the simple. This refers to the act of

comparing the actual with the standards. Managers set the standards with which the actual

performance is judged. Standard setting is aspect of the budgetary control where management

accountants express the professional knowledge and skills for preventing the harm and using

budgeting process.

It helps in measuring performance. Some managers may only see the adverse and

favourable variances as good or bad. The variance analysis is the good tool for assessing the

manager’s performance. Managers are required to take care of the business ensuring that they do

not make costly mistakes and the assumptions that could cause the company to suffer losses.

Responsibility accounting is also a phrase used for describing how managers will be held

accountable for the decisions taken by them. Company is structured in the segments and

managers have the responsibility of ensuring that the resources are allocated effectively and

efficiently among different departments (Maas, chaltegger and Crutzen, 2016). As variance

analysis is made on items or department basis it makes it easy for the managers to held

accountable for the material deviations from the planned activities. Great care is to be exercised

using the variance analysis for the responsibility accounting.

Material or significant variances draw attention of the management to the areas where the

planned activities differ from the actual outcomes. Great care is required to be taken while using

the variance analysis as a management tool and not using it too dogmatically.

4

management wishes for having lower deviations from planned budgets. Lower deviations leads

the managers in making detailed as well as forward looking the budgetary decisions. it works as

the control mechanism (Zhang, 2017). Carrying out analysis of the significant deviations over

essential items help company for knowing the issues and also helps management for looking into

the possible manner about the deviations that could be avoided.

The variance analysis helps the managers in allocation of the roles and responsibilities

and also engages the control mechanism over the departments where it is most required. For

instance if the labour efficiency variances are seen unfavourable or the procurement of the raw

materials cost variance is also unfavourable, management could enhance the control over

departments for increasing the efficiency.

Merits and demerits of the variance analysis

Process of the variance analysis is easy and the simple. This refers to the act of

comparing the actual with the standards. Managers set the standards with which the actual

performance is judged. Standard setting is aspect of the budgetary control where management

accountants express the professional knowledge and skills for preventing the harm and using

budgeting process.

It helps in measuring performance. Some managers may only see the adverse and

favourable variances as good or bad. The variance analysis is the good tool for assessing the

manager’s performance. Managers are required to take care of the business ensuring that they do

not make costly mistakes and the assumptions that could cause the company to suffer losses.

Responsibility accounting is also a phrase used for describing how managers will be held

accountable for the decisions taken by them. Company is structured in the segments and

managers have the responsibility of ensuring that the resources are allocated effectively and

efficiently among different departments (Maas, chaltegger and Crutzen, 2016). As variance

analysis is made on items or department basis it makes it easy for the managers to held

accountable for the material deviations from the planned activities. Great care is to be exercised

using the variance analysis for the responsibility accounting.

Material or significant variances draw attention of the management to the areas where the

planned activities differ from the actual outcomes. Great care is required to be taken while using

the variance analysis as a management tool and not using it too dogmatically.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Along with the advantages it also has limitations. The variance analysis though helps in

identifying the areas of variations or deviations from the budgeted figures. It does not tells the

users about the actual reasons or causes about the variances. After identifying the variances

further investigation is also required by the managers that lead to them to take suboptimal

decisions (Otley, 2016). First reaction of the decision makers could be for praising the buyers

who are responsible for purchasing the materials from cheaper sources than the anticipated &

reprimand the managers that are responsible for using materials

Market prices leading the material prices to rise. Setting incorrect materials prices and

managers buying the inferior quality of the goods which eventually leads to use of increased

materials than budgeted makes variance analysis a disadvantage. If the managers are not able to

use the information derived from variance analysis they will not be able to achieve the desired

results.

Another drawback of the variance analysis is that it takes considerable amount of time in

examining effect of variances because of which corrective actions are often delayed. Monitoring

the tools result in big lag time and applications of the control measure are significantly delayed.

Other performance measure is the sensitivity that determines variations in output could be

attributed to the variations in output. The sensitivity analysis determines effects of variations

between actual outcomes from planned activities.

It plays a critical role in measuring the performance of the managers as they are the

people who actually operates the business and ensures that the desired goals and objectives of the

company are achieved. Managers take decisions as per the prevailing conditions in the market to

ensure that the maximum benefits are caused to the company. it has to make informed decisions

after analysing all the factors that could influence the results. Effectiveness of the management

decisions could be identified from the variations in budgeted and actual outcomes. The cost

variances may be unfavourable if the sales variance is highly favourable as compared with the

cost variances (Hiebl and Richter, 2018). The results show the efficiency of management to

operate the business in changing environment by taking effective decisions. There should be

overall benefit caused to the company due to the decisions that are taken in different situations.

5

identifying the areas of variations or deviations from the budgeted figures. It does not tells the

users about the actual reasons or causes about the variances. After identifying the variances

further investigation is also required by the managers that lead to them to take suboptimal

decisions (Otley, 2016). First reaction of the decision makers could be for praising the buyers

who are responsible for purchasing the materials from cheaper sources than the anticipated &

reprimand the managers that are responsible for using materials

Market prices leading the material prices to rise. Setting incorrect materials prices and

managers buying the inferior quality of the goods which eventually leads to use of increased

materials than budgeted makes variance analysis a disadvantage. If the managers are not able to

use the information derived from variance analysis they will not be able to achieve the desired

results.

Another drawback of the variance analysis is that it takes considerable amount of time in

examining effect of variances because of which corrective actions are often delayed. Monitoring

the tools result in big lag time and applications of the control measure are significantly delayed.

Other performance measure is the sensitivity that determines variations in output could be

attributed to the variations in output. The sensitivity analysis determines effects of variations

between actual outcomes from planned activities.

It plays a critical role in measuring the performance of the managers as they are the

people who actually operates the business and ensures that the desired goals and objectives of the

company are achieved. Managers take decisions as per the prevailing conditions in the market to

ensure that the maximum benefits are caused to the company. it has to make informed decisions

after analysing all the factors that could influence the results. Effectiveness of the management

decisions could be identified from the variations in budgeted and actual outcomes. The cost

variances may be unfavourable if the sales variance is highly favourable as compared with the

cost variances (Hiebl and Richter, 2018). The results show the efficiency of management to

operate the business in changing environment by taking effective decisions. There should be

overall benefit caused to the company due to the decisions that are taken in different situations.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PART B

Report discussing over making in house production or to import from Brazil

Deciding over setting up manufacturing of own is key of structuring the supply chain.

Business is unique and decision making that are right for the company and its stage are vital. In

manufacturing world companies required to make choices between purchasing the products or

making in house. Many of the countries purchases products or outsource services for saving

money. Advantages and disadvantage of the outsourcing and in house production are different

for the companies. It should take decisions as per the circumstances and situation faced by it and

the scenarios that will bring maximum benefits to it.

In the present case XLG is planning to make in house production of famaQ as the imports

after the pandemic has risen. It wants to analyse which would be more beneficial for the

company whether to produce by own or to import from Brazil only.

In-house Production

On in house production XLG will be having complete control of the process from starting

to the finish. It will give more flexibility of adoption when it is seen fit. It is useful specially

when company is proposing to respond to market more quickly and making consumer led

modifications to the product and without going through other company or anyone else.

In house manufacturing will enable the company to have quick as well as seamless process

between the engineering, design production or product development. It could closely control the

activities and processes of the in-house production. Supply chain managers could access all the

departments adequately and for making immediate contact when required. The process of

manufacturing could be speeded up form prototype onwards (Hopper and Bui, 2016). The speed

will be making it easier for the company to customise the products as per customers. It will

reduce the in between cost of company such as tax and transportation.

However it will also required the management to also look over the production of another

product apart from the main products for which the production is being made. When production

is in-house quality of the products could be ensured to be best. Quality is often sacrificed by the

suppliers when making short purchases or when negotiations in prices are made. preventing the

other cost company could produce the product inhouse of higher quality,

6

Report discussing over making in house production or to import from Brazil

Deciding over setting up manufacturing of own is key of structuring the supply chain.

Business is unique and decision making that are right for the company and its stage are vital. In

manufacturing world companies required to make choices between purchasing the products or

making in house. Many of the countries purchases products or outsource services for saving

money. Advantages and disadvantage of the outsourcing and in house production are different

for the companies. It should take decisions as per the circumstances and situation faced by it and

the scenarios that will bring maximum benefits to it.

In the present case XLG is planning to make in house production of famaQ as the imports

after the pandemic has risen. It wants to analyse which would be more beneficial for the

company whether to produce by own or to import from Brazil only.

In-house Production

On in house production XLG will be having complete control of the process from starting

to the finish. It will give more flexibility of adoption when it is seen fit. It is useful specially

when company is proposing to respond to market more quickly and making consumer led

modifications to the product and without going through other company or anyone else.

In house manufacturing will enable the company to have quick as well as seamless process

between the engineering, design production or product development. It could closely control the

activities and processes of the in-house production. Supply chain managers could access all the

departments adequately and for making immediate contact when required. The process of

manufacturing could be speeded up form prototype onwards (Hopper and Bui, 2016). The speed

will be making it easier for the company to customise the products as per customers. It will

reduce the in between cost of company such as tax and transportation.

However it will also required the management to also look over the production of another

product apart from the main products for which the production is being made. When production

is in-house quality of the products could be ensured to be best. Quality is often sacrificed by the

suppliers when making short purchases or when negotiations in prices are made. preventing the

other cost company could produce the product inhouse of higher quality,

6

Producing famaQ in-house will also avoid management costs. It will control the issues of public

relations. It will not be required to depend over outside supplier for the essential product without

which the main product could not be made.

Buying from Brazil

On the other labour cost has always been major part in the manufacturing process. When the

goods are purchased directly from outside managers is not required to take responsibilities and

costs involved to hire staff. In house production requires knowledge and expertise regarding

particular product. Company will not be required to appoint additional staff and the managers to

carryout the production process. Production process requires company to undertake number of

responsibilities. They have to take of whole process from procuring raw materials, monitoring

and control of process and operations to the finished products.

When goods are purchased from outside company is only required to pay focus over ensuing

quality and price of acquiring the products. It is not required to take other responsibilities. In

production even small operations require people to run them smoothly which could be

detrimental drain over business accounts. Also, there are other savings that are made when the

products are sold from outside in terms of the general overheads. It is more expensive to have the

manufacturing facility and meeting all bills. It includes utility expenses, maintenance, insurance

and license.

With management efficiency flexibility could also be achieved in buying. Contractors or

suppliers specialise in bespoke and could easily adapt for the alterations and customisations to

the products as per requirements. Company by making adequate research could identify the

suppliers that are providing the materials with best deals for company. Buying in business in

business is not limited to only economic or the logistic decisions (Cooper, Ezzamel and Qu,

2017). Company buying products out of the area of expertise provides the company with the

required space for growing.

Company could buy from the suppliers as per their requirements, company in short

requirements will make reduced purchases and seeing the demand it can also make bulk

purchases. While in in-house production company producing below the estimated limit will not

be able to cover its cost and in cases of increased demand it might not have the required capacity.

In such situations cost of in-house production will rise at more faster speed wiping out the profits

of core business activities. It has to acquire all the facilities to manufacture the products such as

7

relations. It will not be required to depend over outside supplier for the essential product without

which the main product could not be made.

Buying from Brazil

On the other labour cost has always been major part in the manufacturing process. When the

goods are purchased directly from outside managers is not required to take responsibilities and

costs involved to hire staff. In house production requires knowledge and expertise regarding

particular product. Company will not be required to appoint additional staff and the managers to

carryout the production process. Production process requires company to undertake number of

responsibilities. They have to take of whole process from procuring raw materials, monitoring

and control of process and operations to the finished products.

When goods are purchased from outside company is only required to pay focus over ensuing

quality and price of acquiring the products. It is not required to take other responsibilities. In

production even small operations require people to run them smoothly which could be

detrimental drain over business accounts. Also, there are other savings that are made when the

products are sold from outside in terms of the general overheads. It is more expensive to have the

manufacturing facility and meeting all bills. It includes utility expenses, maintenance, insurance

and license.

With management efficiency flexibility could also be achieved in buying. Contractors or

suppliers specialise in bespoke and could easily adapt for the alterations and customisations to

the products as per requirements. Company by making adequate research could identify the

suppliers that are providing the materials with best deals for company. Buying in business in

business is not limited to only economic or the logistic decisions (Cooper, Ezzamel and Qu,

2017). Company buying products out of the area of expertise provides the company with the

required space for growing.

Company could buy from the suppliers as per their requirements, company in short

requirements will make reduced purchases and seeing the demand it can also make bulk

purchases. While in in-house production company producing below the estimated limit will not

be able to cover its cost and in cases of increased demand it might not have the required capacity.

In such situations cost of in-house production will rise at more faster speed wiping out the profits

of core business activities. It has to acquire all the facilities to manufacture the products such as

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

equipments and machinery and keep proper record of inventory of production which will also

increase the staff and management cost.

As per the current scenario XLG is having famaQ at 3.7 where the in-house production will

cost 3. The prices are high due to the reason of pandemic as previously it was available only at

2.5 which is lower than making. Company is required to focus over the core product as demand

is proposed to increase by 45%. Making will split the focus of management which could decline

the quality of cleaning products. After the pandemic price of fama may fall and company may

get it price lower than making it in-house. Therefore it is suggested that XLG should continue

importing famaQ from Brazil as it will be more beneficial for the company. As, it has already

increased the prices of X & Y due to the increase in price of famaQ it will not face decline in

profit margins.

CONCLUSIONS

From the above report it could be concluded that variance has a critical role in management

accounting. Using this, managers can identify the variations between budgeted and acual figures

and take corrective measures for reducing the same. It enables the management to make

allocation of resources more effectively for increasing the productivity and efficiency of

company.

8

increase the staff and management cost.

As per the current scenario XLG is having famaQ at 3.7 where the in-house production will

cost 3. The prices are high due to the reason of pandemic as previously it was available only at

2.5 which is lower than making. Company is required to focus over the core product as demand

is proposed to increase by 45%. Making will split the focus of management which could decline

the quality of cleaning products. After the pandemic price of fama may fall and company may

get it price lower than making it in-house. Therefore it is suggested that XLG should continue

importing famaQ from Brazil as it will be more beneficial for the company. As, it has already

increased the prices of X & Y due to the increase in price of famaQ it will not face decline in

profit margins.

CONCLUSIONS

From the above report it could be concluded that variance has a critical role in management

accounting. Using this, managers can identify the variations between budgeted and acual figures

and take corrective measures for reducing the same. It enables the management to make

allocation of resources more effectively for increasing the productivity and efficiency of

company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner

Production. 136.pp.237-248.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31. pp.45-62.

Hiebl, M.R. and Richter, J.F., 2018. Response rates in management accounting survey

research. Journal of Management Accounting Research.30(2). pp.59-79.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31.pp.10-30.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.34(2).pp.991-1025.

D'Onza, G., Greco, G. and Allegrini, M., 2016. Full cost accounting in the analysis of separated

waste collection efficiency: A methodological proposal. Journal of environmental

management.167. pp.59-65.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN. p.15.

Zhang, C., 2017. The Application of Variance Analysis in FP&A Organizations: Survey

Evidence and Recommendations for Enhancement. Journal of Accounting and

Finance. 17(8).pp.54-70.

9

Books and Journals

Maas, K., Schaltegger, S. and Crutzen, N., 2016. Integrating corporate sustainability assessment,

management accounting, control, and reporting. Journal of Cleaner

Production. 136.pp.237-248.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research.31. pp.45-62.

Hiebl, M.R. and Richter, J.F., 2018. Response rates in management accounting survey

research. Journal of Management Accounting Research.30(2). pp.59-79.

Hopper, T. and Bui, B., 2016. Has management accounting research been critical?. Management

Accounting Research. 31.pp.10-30.

Cooper, D.J., Ezzamel, M. and Qu, S.Q., 2017. Popularizing a management accounting idea: The

case of the balanced scorecard. Contemporary Accounting Research.34(2).pp.991-1025.

D'Onza, G., Greco, G. and Allegrini, M., 2016. Full cost accounting in the analysis of separated

waste collection efficiency: A methodological proposal. Journal of environmental

management.167. pp.59-65.

Marzlin Marzuki, N.A.R. and Ismail, J., 2019. Benefits and limitations of variance analysis in

management accounting. ACCOUNTING BULLETIN. p.15.

Zhang, C., 2017. The Application of Variance Analysis in FP&A Organizations: Survey

Evidence and Recommendations for Enhancement. Journal of Accounting and

Finance. 17(8).pp.54-70.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.