Analysis of ABC Ltd. Production: A Business Case Study Solution

VerifiedAdded on 2023/01/20

|7

|1676

|39

Case Study

AI Summary

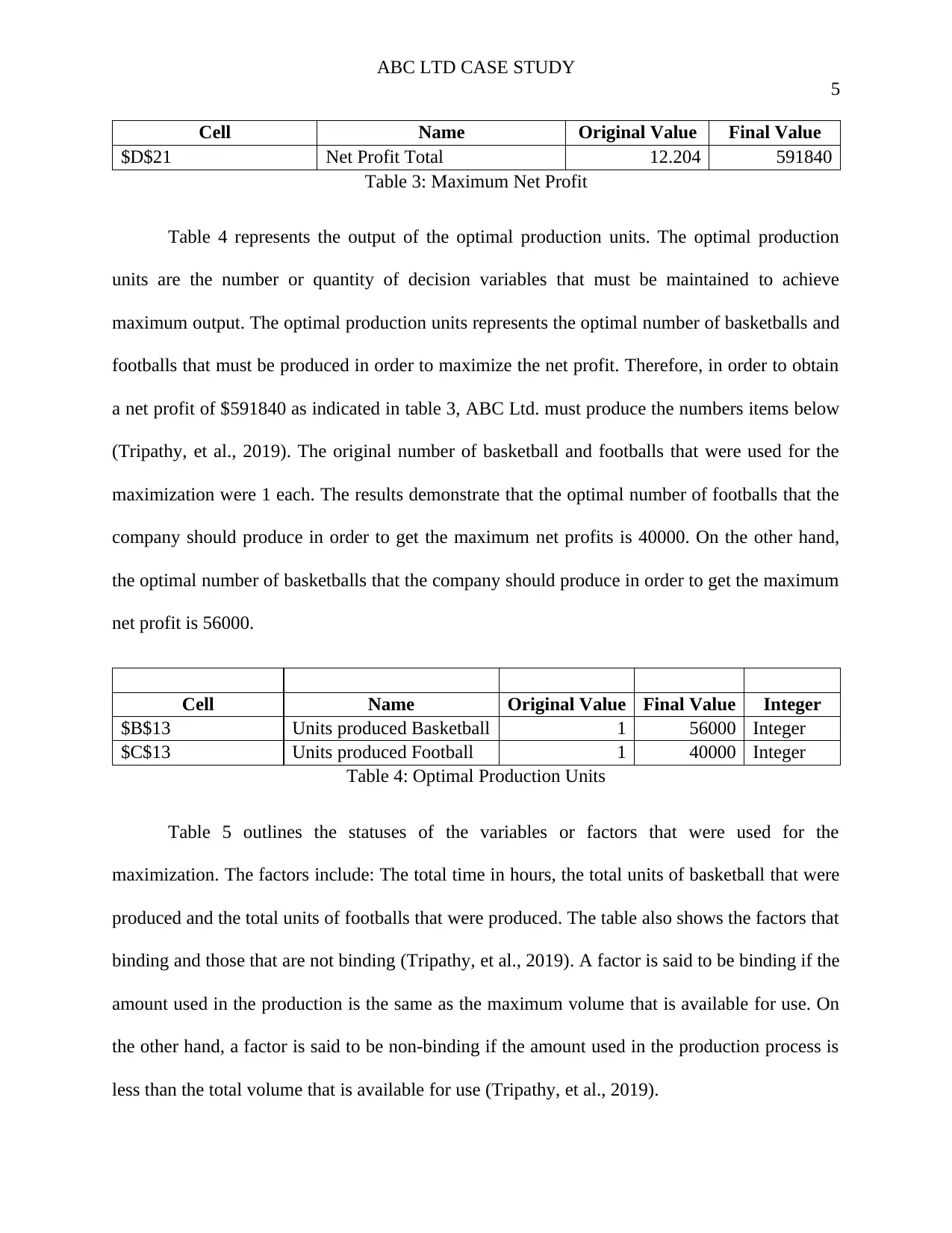

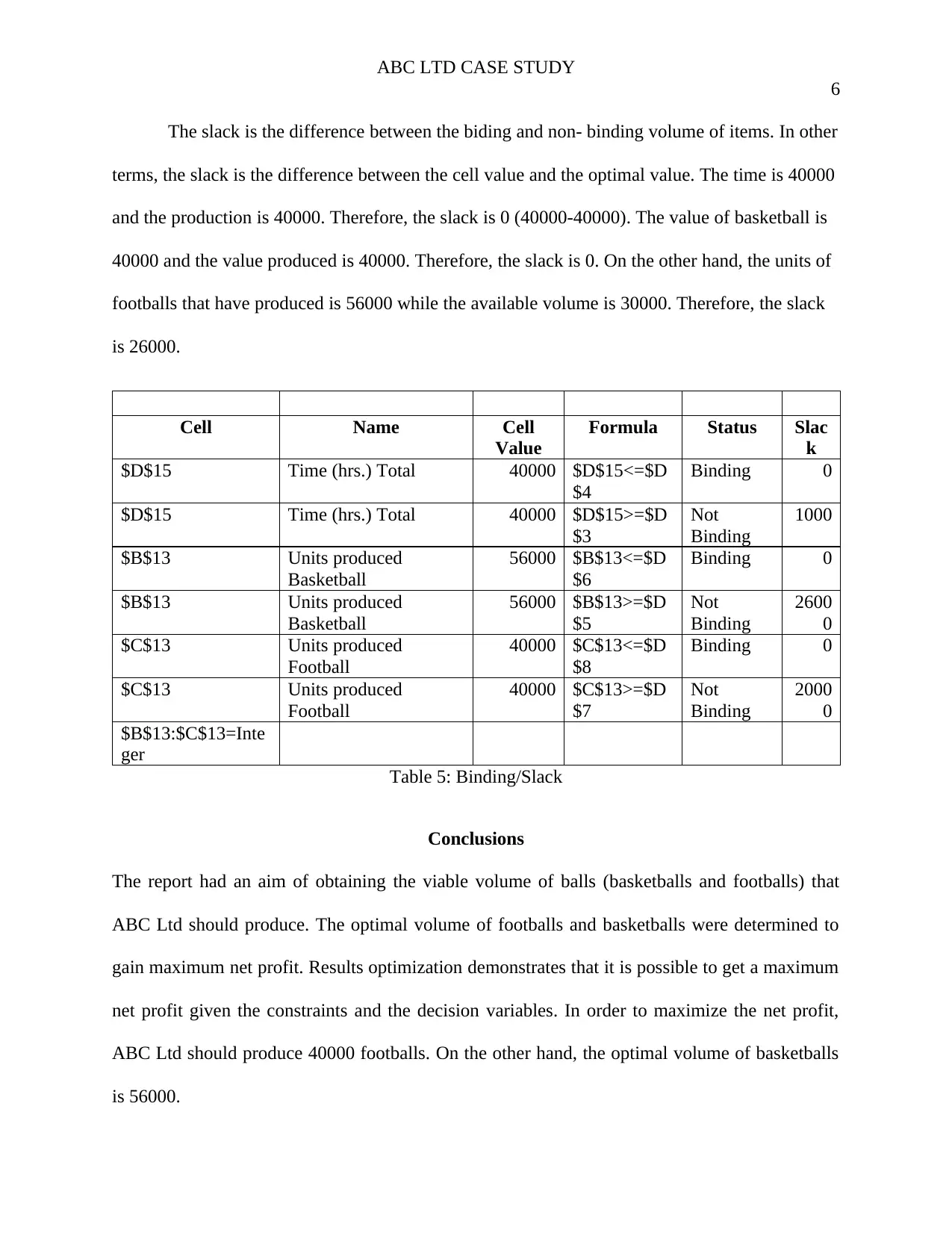

This case study analyzes ABC Ltd., a sports equipment manufacturer, aiming to optimize the production of footballs and basketballs to maximize net profit. Using linear programming and Excel Solver, the analysis considers constraints such as machine hours, material costs, and labor costs. The solution determines the optimal production quantities: 40,000 footballs and 56,000 basketballs, resulting in a maximum net profit of $591,840. The report highlights the significant increase in profit compared to the original production levels and provides insights into binding and non-binding constraints, offering recommendations for resource allocation and future profitability. The findings demonstrate the effectiveness of linear optimization in enhancing the company's financial performance.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.