Cost Accounting Assignment: Analyzing Production and Variances

VerifiedAdded on 2021/01/02

|6

|832

|378

Homework Assignment

AI Summary

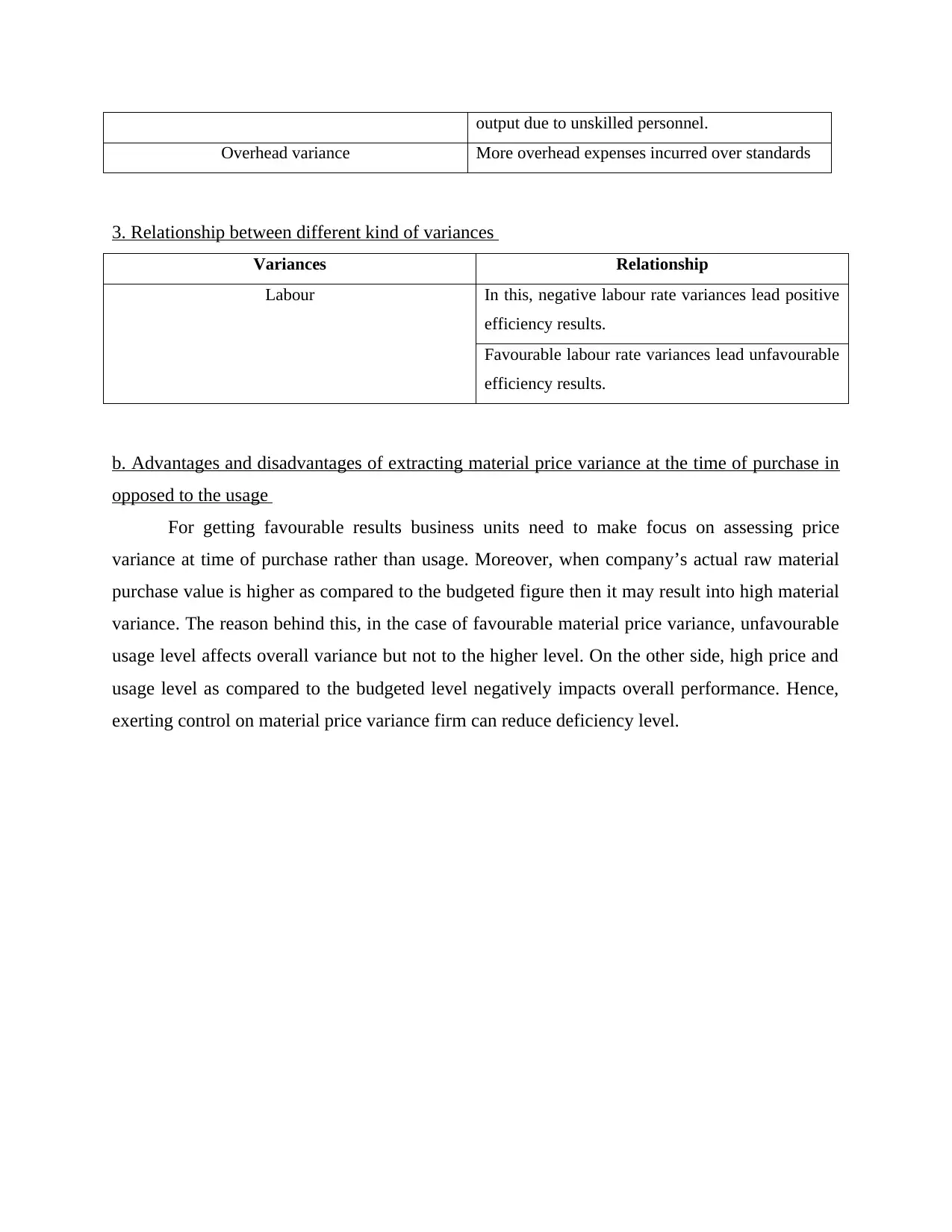

This assignment solution addresses key concepts in cost accounting, focusing on production and service cost centers, budgetary control, and break-even analysis. It defines and differentiates production and service cost centers, explaining cost apportionment methods. The benefits of a budgetary control system are outlined, along with assumptions related to break-even analysis. The solution further explores variance analysis, presenting different variance headings (material, labor, and overhead) and explaining the reasons behind their occurrence. It also examines the relationships between various types of variances and discusses the advantages and disadvantages of calculating material price variance at the time of purchase versus usage. The document includes references to relevant academic sources.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.