BAO5524 Professional Auditing Assignment: BSL Audit Report 2018

VerifiedAdded on 2023/01/16

|21

|4626

|96

Report

AI Summary

This report provides a comprehensive analysis of the audit of Biofuel Solutions Ltd (BSL) for the year ended December 31, 2018. It begins with an introduction to auditing and assurance services, emphasizing their importance in business operations. The report includes a SWOT analysis to evaluate business risks, identifying operational, innovation, legal, and credit risks. It then details major risk areas, such as liquidity, debtor turnover, salaries, and share cancellations, supported by ratio analysis and financial data. Risk management strategies are proposed to address operational, credit, technological, and legal risks. The report also examines the strengths and weaknesses of BSL's purchase system, along with audit tests. Furthermore, it presents actions to address concerns raised, outlines audit procedures for important processing, and analyzes the audit of non-current assets. The report concludes with a summary of findings and recommendations, supported by references.

AUDITING ASSIGNMENT

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

(A) SWOT analysis and major risk factors................................................................................4

(i)- The results of a SWOT analysis on BSL to evaluate business risk;.................................4

(ii)- The major risk areas to be addressed in the audit of BSL for the year ended 31

December, 2018. Give reasons why the identified areas are considered to be high risk.......5

(B) Risk management strategies.................................................................................................8

(C) Strength and weakness in the purchase system of BSL.......................................................9

(D) Actions to be taken to address the concerns raised by Charlie Smith...............................12

(E) Audit procedure on important processing..........................................................................13

(F) Audit of non-current assets................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

2

Introduction................................................................................................................................3

(A) SWOT analysis and major risk factors................................................................................4

(i)- The results of a SWOT analysis on BSL to evaluate business risk;.................................4

(ii)- The major risk areas to be addressed in the audit of BSL for the year ended 31

December, 2018. Give reasons why the identified areas are considered to be high risk.......5

(B) Risk management strategies.................................................................................................8

(C) Strength and weakness in the purchase system of BSL.......................................................9

(D) Actions to be taken to address the concerns raised by Charlie Smith...............................12

(E) Audit procedure on important processing..........................................................................13

(F) Audit of non-current assets................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

2

Introduction

Auditing and assurance service has become an important factor for every business

organisation in order to manage its business operations by analysing results. Auditing

services include various steps that are undertaken taken collectively to conclude the findings

in the audit report. In this case, Biofuel Solutions Ltd (BSL) is the business organisation

undertaken base in this report. Various aspects of auditing and assurance have been analysed

in this report. Firstly, business risk by conducting a SWOT analysis and major risk factors

has been analysed in this report. Audit procedures to overcome those identified major risk

areas have been undertaken in this report. Next section of the report consists of an analysis of

purchase and payment system of BSL. Next section of this report deals with the identification

of programmed and manual application controls that can be placed in the accounting system

to minimise risk. In the last section, non-current assets have been analysed under different

audit procedures.

3

Auditing and assurance service has become an important factor for every business

organisation in order to manage its business operations by analysing results. Auditing

services include various steps that are undertaken taken collectively to conclude the findings

in the audit report. In this case, Biofuel Solutions Ltd (BSL) is the business organisation

undertaken base in this report. Various aspects of auditing and assurance have been analysed

in this report. Firstly, business risk by conducting a SWOT analysis and major risk factors

has been analysed in this report. Audit procedures to overcome those identified major risk

areas have been undertaken in this report. Next section of the report consists of an analysis of

purchase and payment system of BSL. Next section of this report deals with the identification

of programmed and manual application controls that can be placed in the accounting system

to minimise risk. In the last section, non-current assets have been analysed under different

audit procedures.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

AUDIT PLANNING MEMORANDUM

(A) SWOT analysis and major risk factors

(i)- The results of a SWOT analysis on BSL to evaluate business risk;

Strength

Biofuel Solutions Ltd technology-oriented

company since they use technology to create

personal-care products and raw materials for

chemical companies. Therefore it can be

analysed that innovation is their main strength

in business operations.

Use of advanced accounting system that will

cut costing and there less are less human errors.

Strength of Biofuel Solutions Ltd is that they

have their own fixed assets therefore it has

base for expansion operations.

Weakness

Expensive product i.e. fuel and need to

manage cost effectiveness to beat the

competition. Biofuel Solutions Ltd has to

incurre major cost and expenses to operate

their business because their expenses are

technology driven.

There are operational weaknesses in the

business operations of BSL Ltd as there are

many checkpoints in processing transactions.

(Operations risk)

Apart from advanced system in the operation,

Biofuel Solutions Ltd also has very complex

acclounting system that creats ambiguity in

employees and auditors.

Opportunities

There are high gross margins that can be

retained for future business growth. Because

of high turnover of Biofuel Solutions Ltd,

their earned profit is also high and some

portion from profit can be saved for future

growth.

Threads

Technological changes- Industrial

biotechnology company. Change in

technology can be thread for Biofuel

Solutions Ltd as well. Rapid development of

technology in competitors business lead to

higher competitive thread.

4

(A) SWOT analysis and major risk factors

(i)- The results of a SWOT analysis on BSL to evaluate business risk;

Strength

Biofuel Solutions Ltd technology-oriented

company since they use technology to create

personal-care products and raw materials for

chemical companies. Therefore it can be

analysed that innovation is their main strength

in business operations.

Use of advanced accounting system that will

cut costing and there less are less human errors.

Strength of Biofuel Solutions Ltd is that they

have their own fixed assets therefore it has

base for expansion operations.

Weakness

Expensive product i.e. fuel and need to

manage cost effectiveness to beat the

competition. Biofuel Solutions Ltd has to

incurre major cost and expenses to operate

their business because their expenses are

technology driven.

There are operational weaknesses in the

business operations of BSL Ltd as there are

many checkpoints in processing transactions.

(Operations risk)

Apart from advanced system in the operation,

Biofuel Solutions Ltd also has very complex

acclounting system that creats ambiguity in

employees and auditors.

Opportunities

There are high gross margins that can be

retained for future business growth. Because

of high turnover of Biofuel Solutions Ltd,

their earned profit is also high and some

portion from profit can be saved for future

growth.

Threads

Technological changes- Industrial

biotechnology company. Change in

technology can be thread for Biofuel

Solutions Ltd as well. Rapid development of

technology in competitors business lead to

higher competitive thread.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

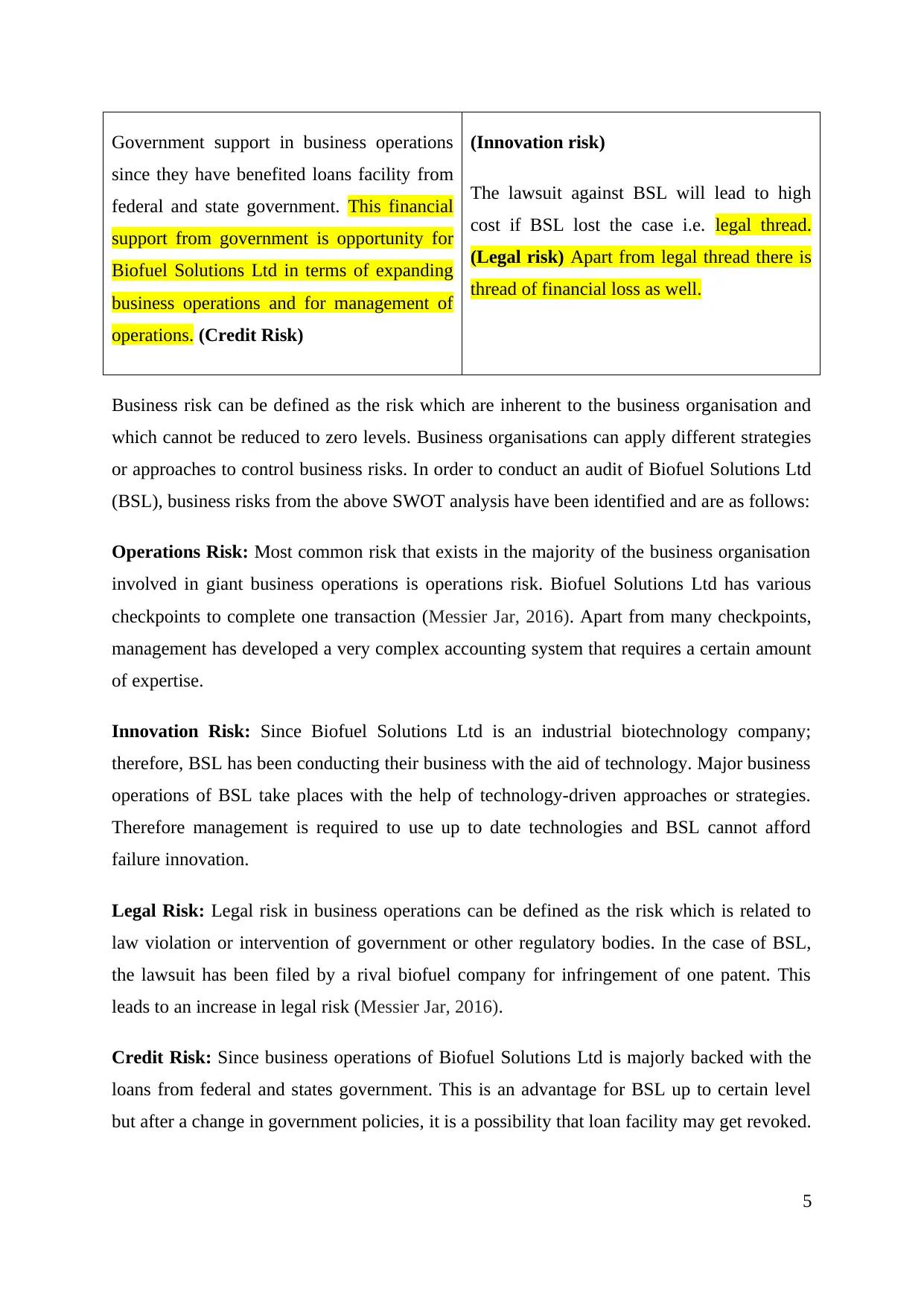

Government support in business operations

since they have benefited loans facility from

federal and state government. This financial

support from government is opportunity for

Biofuel Solutions Ltd in terms of expanding

business operations and for management of

operations. (Credit Risk)

(Innovation risk)

The lawsuit against BSL will lead to high

cost if BSL lost the case i.e. legal thread.

(Legal risk) Apart from legal thread there is

thread of financial loss as well.

Business risk can be defined as the risk which are inherent to the business organisation and

which cannot be reduced to zero levels. Business organisations can apply different strategies

or approaches to control business risks. In order to conduct an audit of Biofuel Solutions Ltd

(BSL), business risks from the above SWOT analysis have been identified and are as follows:

Operations Risk: Most common risk that exists in the majority of the business organisation

involved in giant business operations is operations risk. Biofuel Solutions Ltd has various

checkpoints to complete one transaction (Messier Jar, 2016). Apart from many checkpoints,

management has developed a very complex accounting system that requires a certain amount

of expertise.

Innovation Risk: Since Biofuel Solutions Ltd is an industrial biotechnology company;

therefore, BSL has been conducting their business with the aid of technology. Major business

operations of BSL take places with the help of technology-driven approaches or strategies.

Therefore management is required to use up to date technologies and BSL cannot afford

failure innovation.

Legal Risk: Legal risk in business operations can be defined as the risk which is related to

law violation or intervention of government or other regulatory bodies. In the case of BSL,

the lawsuit has been filed by a rival biofuel company for infringement of one patent. This

leads to an increase in legal risk (Messier Jar, 2016).

Credit Risk: Since business operations of Biofuel Solutions Ltd is majorly backed with the

loans from federal and states government. This is an advantage for BSL up to certain level

but after a change in government policies, it is a possibility that loan facility may get revoked.

5

since they have benefited loans facility from

federal and state government. This financial

support from government is opportunity for

Biofuel Solutions Ltd in terms of expanding

business operations and for management of

operations. (Credit Risk)

(Innovation risk)

The lawsuit against BSL will lead to high

cost if BSL lost the case i.e. legal thread.

(Legal risk) Apart from legal thread there is

thread of financial loss as well.

Business risk can be defined as the risk which are inherent to the business organisation and

which cannot be reduced to zero levels. Business organisations can apply different strategies

or approaches to control business risks. In order to conduct an audit of Biofuel Solutions Ltd

(BSL), business risks from the above SWOT analysis have been identified and are as follows:

Operations Risk: Most common risk that exists in the majority of the business organisation

involved in giant business operations is operations risk. Biofuel Solutions Ltd has various

checkpoints to complete one transaction (Messier Jar, 2016). Apart from many checkpoints,

management has developed a very complex accounting system that requires a certain amount

of expertise.

Innovation Risk: Since Biofuel Solutions Ltd is an industrial biotechnology company;

therefore, BSL has been conducting their business with the aid of technology. Major business

operations of BSL take places with the help of technology-driven approaches or strategies.

Therefore management is required to use up to date technologies and BSL cannot afford

failure innovation.

Legal Risk: Legal risk in business operations can be defined as the risk which is related to

law violation or intervention of government or other regulatory bodies. In the case of BSL,

the lawsuit has been filed by a rival biofuel company for infringement of one patent. This

leads to an increase in legal risk (Messier Jar, 2016).

Credit Risk: Since business operations of Biofuel Solutions Ltd is majorly backed with the

loans from federal and states government. This is an advantage for BSL up to certain level

but after a change in government policies, it is a possibility that loan facility may get revoked.

5

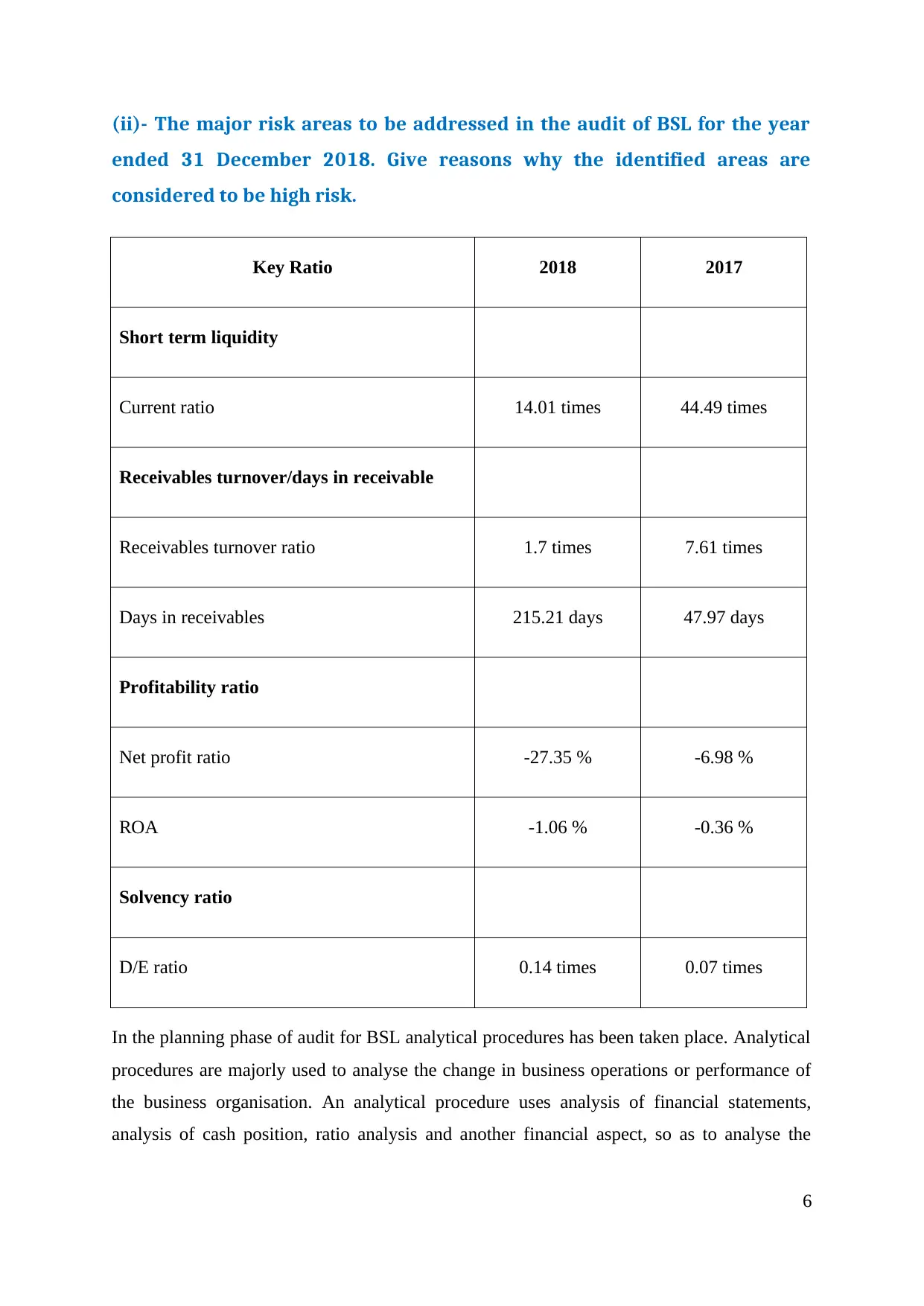

(ii)- The major risk areas to be addressed in the audit of BSL for the year

ended 31 December 2018. Give reasons why the identified areas are

considered to be high risk.

Key Ratio 2018 2017

Short term liquidity

Current ratio 14.01 times 44.49 times

Receivables turnover/days in receivable

Receivables turnover ratio 1.7 times 7.61 times

Days in receivables 215.21 days 47.97 days

Profitability ratio

Net profit ratio -27.35 % -6.98 %

ROA -1.06 % -0.36 %

Solvency ratio

D/E ratio 0.14 times 0.07 times

In the planning phase of audit for BSL analytical procedures has been taken place. Analytical

procedures are majorly used to analyse the change in business operations or performance of

the business organisation. An analytical procedure uses analysis of financial statements,

analysis of cash position, ratio analysis and another financial aspect, so as to analyse the

6

ended 31 December 2018. Give reasons why the identified areas are

considered to be high risk.

Key Ratio 2018 2017

Short term liquidity

Current ratio 14.01 times 44.49 times

Receivables turnover/days in receivable

Receivables turnover ratio 1.7 times 7.61 times

Days in receivables 215.21 days 47.97 days

Profitability ratio

Net profit ratio -27.35 % -6.98 %

ROA -1.06 % -0.36 %

Solvency ratio

D/E ratio 0.14 times 0.07 times

In the planning phase of audit for BSL analytical procedures has been taken place. Analytical

procedures are majorly used to analyse the change in business operations or performance of

the business organisation. An analytical procedure uses analysis of financial statements,

analysis of cash position, ratio analysis and another financial aspect, so as to analyse the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

change in business position and performance. The main objective of analytical procedures is

to identify major risk areas that need more focus while auditing. In the case of BSL, the

following are major risk areas that have been identified using analytical procedures:

Major Risk area REASON

1-Liquidity position

(Majorly current

assets)

From the analysis of the statement of financial position and ratio

analysis, it can be analysed that the current ratio of BSL has been

drastically decreased to 14.04 times in 2018 from 44.49 times in

2017. The main reason behind the decline in liquidity position is a

drastic decrease in cash and cash equivalents in 2018. In 2018,

there is a decrease in cash because of the decrease in cash from

operating activities during the year (Cohen and Simnett, 2014).

Because of this change, liquidity becomes a major risk area and

cash and cash equivalent balance needs to be a focus on. It can be

observed that Biofuel Solutions Ltd has very high current ratio

which means investment in current assets are very high as

compared to current obligations. During audit process, current

assets should be investigate in detail.

2- Debtor or

operating area

With the help of an analytical review, it is analysed that days in

receivable of BSL has been significantly increased in 2018 as

compared to 2017. In 2017, days in receivable were 47 days but in

2018 it is 215.21. A day in receivable is the operational ratio that

measures average no of days in which cash from debtors has been

collected in a reporting year (Cohen and Simnett, 2014). This can

be clearly analysed that the operational efficiency of BSL in 2018

in terms of collecting cash from debtors is the major risk factor.

Therefore whole performing audit, debtors needs to be analysed by

using different techniques like external communication, preparing

age debtors and other audit procedures.

7

to identify major risk areas that need more focus while auditing. In the case of BSL, the

following are major risk areas that have been identified using analytical procedures:

Major Risk area REASON

1-Liquidity position

(Majorly current

assets)

From the analysis of the statement of financial position and ratio

analysis, it can be analysed that the current ratio of BSL has been

drastically decreased to 14.04 times in 2018 from 44.49 times in

2017. The main reason behind the decline in liquidity position is a

drastic decrease in cash and cash equivalents in 2018. In 2018,

there is a decrease in cash because of the decrease in cash from

operating activities during the year (Cohen and Simnett, 2014).

Because of this change, liquidity becomes a major risk area and

cash and cash equivalent balance needs to be a focus on. It can be

observed that Biofuel Solutions Ltd has very high current ratio

which means investment in current assets are very high as

compared to current obligations. During audit process, current

assets should be investigate in detail.

2- Debtor or

operating area

With the help of an analytical review, it is analysed that days in

receivable of BSL has been significantly increased in 2018 as

compared to 2017. In 2017, days in receivable were 47 days but in

2018 it is 215.21. A day in receivable is the operational ratio that

measures average no of days in which cash from debtors has been

collected in a reporting year (Cohen and Simnett, 2014). This can

be clearly analysed that the operational efficiency of BSL in 2018

in terms of collecting cash from debtors is the major risk factor.

Therefore whole performing audit, debtors needs to be analysed by

using different techniques like external communication, preparing

age debtors and other audit procedures.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

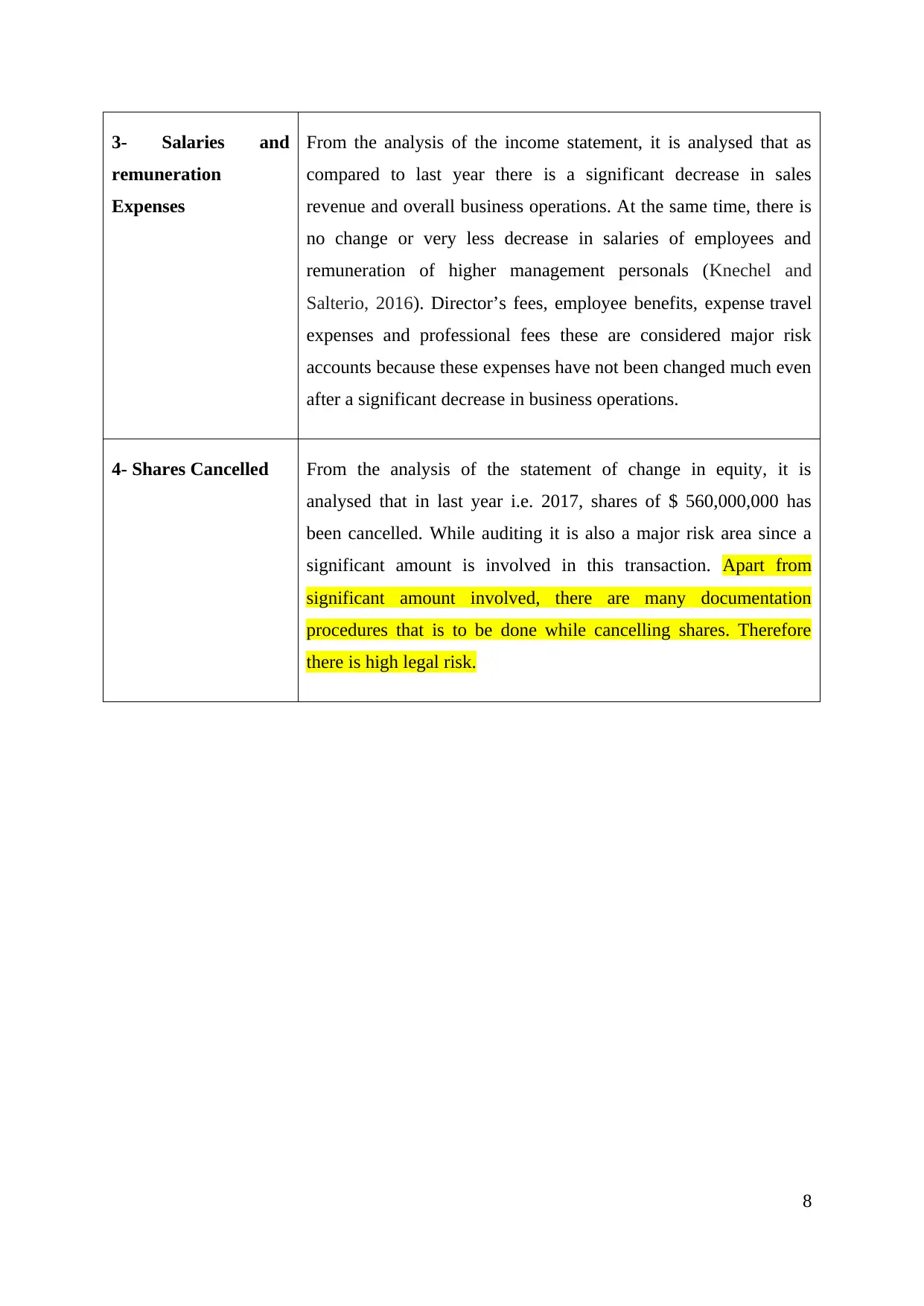

3- Salaries and

remuneration

Expenses

From the analysis of the income statement, it is analysed that as

compared to last year there is a significant decrease in sales

revenue and overall business operations. At the same time, there is

no change or very less decrease in salaries of employees and

remuneration of higher management personals (Knechel and

Salterio, 2016). Director’s fees, employee benefits, expense travel

expenses and professional fees these are considered major risk

accounts because these expenses have not been changed much even

after a significant decrease in business operations.

4- Shares Cancelled From the analysis of the statement of change in equity, it is

analysed that in last year i.e. 2017, shares of $ 560,000,000 has

been cancelled. While auditing it is also a major risk area since a

significant amount is involved in this transaction. Apart from

significant amount involved, there are many documentation

procedures that is to be done while cancelling shares. Therefore

there is high legal risk.

8

remuneration

Expenses

From the analysis of the income statement, it is analysed that as

compared to last year there is a significant decrease in sales

revenue and overall business operations. At the same time, there is

no change or very less decrease in salaries of employees and

remuneration of higher management personals (Knechel and

Salterio, 2016). Director’s fees, employee benefits, expense travel

expenses and professional fees these are considered major risk

accounts because these expenses have not been changed much even

after a significant decrease in business operations.

4- Shares Cancelled From the analysis of the statement of change in equity, it is

analysed that in last year i.e. 2017, shares of $ 560,000,000 has

been cancelled. While auditing it is also a major risk area since a

significant amount is involved in this transaction. Apart from

significant amount involved, there are many documentation

procedures that is to be done while cancelling shares. Therefore

there is high legal risk.

8

(B) Risk management strategies

Operational risk- One of the primary weakness of this organization is that overall cost of

operation in this organization is higher than other competitors in the market and it is

distracting the organization to gain a competitive advantage in the industry. Management of

the organization is required to adopt cost management strategies such as controlling indirect

cost to that are adding minimum value to business organization.

Audit procedure- auditor of the company should conduct a comparative analysis of the cost

elements to evaluate whether the increase in cost in in proportion to the increase in revenue or

not. If not then it can be said that overall efficiency of management is decreasing.

Credit risk- Liquidity position of the company is decreasing as compared to the year 2017

and management is required to invest in marketable securities to decrease liquidity risk.

Availability of current assets and quick assets should always be higher as compared to current

liabilities.

Auditor of the company should evaluate past trend of current ratio and compare it with other

business organization in same industry. this will be help in identifying whether business

organization has a risk of credit due to shortage of current assets or not.

Technological risk- Management of the organization should invest in the use of Advanced

technology to compete with other organizations as it is operating in the biotech industry

which is highly technological competitive.

Auditor is required to analyse whether business organization is using latest technology in

their IT infrastructure of not. In addition to that technology used for production of products

and providing services to customers should also be analysed and compared with competitors

in market.

Legal risk- BSL is required to establish a separate legal department that will be focused on

the identification and following all the legislative requirements that are applicable on a

business operation to protect any negative impact of a legal risk.

9

Operational risk- One of the primary weakness of this organization is that overall cost of

operation in this organization is higher than other competitors in the market and it is

distracting the organization to gain a competitive advantage in the industry. Management of

the organization is required to adopt cost management strategies such as controlling indirect

cost to that are adding minimum value to business organization.

Audit procedure- auditor of the company should conduct a comparative analysis of the cost

elements to evaluate whether the increase in cost in in proportion to the increase in revenue or

not. If not then it can be said that overall efficiency of management is decreasing.

Credit risk- Liquidity position of the company is decreasing as compared to the year 2017

and management is required to invest in marketable securities to decrease liquidity risk.

Availability of current assets and quick assets should always be higher as compared to current

liabilities.

Auditor of the company should evaluate past trend of current ratio and compare it with other

business organization in same industry. this will be help in identifying whether business

organization has a risk of credit due to shortage of current assets or not.

Technological risk- Management of the organization should invest in the use of Advanced

technology to compete with other organizations as it is operating in the biotech industry

which is highly technological competitive.

Auditor is required to analyse whether business organization is using latest technology in

their IT infrastructure of not. In addition to that technology used for production of products

and providing services to customers should also be analysed and compared with competitors

in market.

Legal risk- BSL is required to establish a separate legal department that will be focused on

the identification and following all the legislative requirements that are applicable on a

business operation to protect any negative impact of a legal risk.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditors should themselves identify all the legislature that might be application on business

organization and compared it with the legislature followed by management. In addition to

that rules and regulation followed by organization with respect to each legislature should also

be examined by auditor.

10

organization and compared it with the legislature followed by management. In addition to

that rules and regulation followed by organization with respect to each legislature should also

be examined by auditor.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(C) Strength and weakness in the purchase system of BSL

Strength of purchase system along with audit test

Advanced ordering of raw material- According to the purchase system of this organization

management of the company is making 3 months advance order in order to make sure that

effective discounts are received on bulk orders. This type of system will help in insurance

that the cost of direct expenses is controlled and gross profit is maintained. Management of

the company can also save cost on transportation as normal transportation cost would be

required in this scenario rather than excess to transportation cost that might be required in

case of an emergency.

Audit test- Auditor of the company should compare the prices charged by the supplier for

advanced ordering as compared to normal ordering price (Cohen and Simnett, 2014). This

comparison will help in understanding whether this practice of the organization is actually

beneficial or not.

Computerized process- Entire process of recording raw material received by the

organization is done with the help of computers. This type of practice will definitely help in

maintaining the accuracy and relevancy of accounting processes. Chances of human error are

reduced significantly with the help of computerized process (Messier Jr, 2016). Delivery

cards are also generated with the help of a computer which will also reduce the risk of errors

while recording or making payments.

Audit test- Auditor of the organization is required to use test data to identify whether the

master file used for processing and recording of inventory is accurate or not. This data then

will be compared with the actual data processed by the computer system.

Manually checking the details of delivery notes- According to the rules and regulations in

the purchase system of this organization, all the accounts payable are sent to the clerk at the

head office of the company. It is the responsibility of the clerk to check the details of the

invoice in accordance with the delivery note received from the warehouse. This will help in

ensuring that there are no discrepancies between the delivery note and invoice made for

payment. This will help in making sure that no access payment is made to any supplier

(William Jr, Glover and Prawitt, 2016).

11

Strength of purchase system along with audit test

Advanced ordering of raw material- According to the purchase system of this organization

management of the company is making 3 months advance order in order to make sure that

effective discounts are received on bulk orders. This type of system will help in insurance

that the cost of direct expenses is controlled and gross profit is maintained. Management of

the company can also save cost on transportation as normal transportation cost would be

required in this scenario rather than excess to transportation cost that might be required in

case of an emergency.

Audit test- Auditor of the company should compare the prices charged by the supplier for

advanced ordering as compared to normal ordering price (Cohen and Simnett, 2014). This

comparison will help in understanding whether this practice of the organization is actually

beneficial or not.

Computerized process- Entire process of recording raw material received by the

organization is done with the help of computers. This type of practice will definitely help in

maintaining the accuracy and relevancy of accounting processes. Chances of human error are

reduced significantly with the help of computerized process (Messier Jr, 2016). Delivery

cards are also generated with the help of a computer which will also reduce the risk of errors

while recording or making payments.

Audit test- Auditor of the organization is required to use test data to identify whether the

master file used for processing and recording of inventory is accurate or not. This data then

will be compared with the actual data processed by the computer system.

Manually checking the details of delivery notes- According to the rules and regulations in

the purchase system of this organization, all the accounts payable are sent to the clerk at the

head office of the company. It is the responsibility of the clerk to check the details of the

invoice in accordance with the delivery note received from the warehouse. This will help in

ensuring that there are no discrepancies between the delivery note and invoice made for

payment. This will help in making sure that no access payment is made to any supplier

(William Jr, Glover and Prawitt, 2016).

11

Audit test- Auditor of the company should himself/ herself check the accuracy of this is tattoo

by comparing past invoices and delivery note received from the warehouse on a sample basis.

Authorization of payment made to supplier- any payment made in excess of $20000 is

required to be sent by the financial controller to managing director for authorization. This

type of authorization process is very essential in any business organization as it helps in

maintaining transparency and accountability in business processes (Knechel and Salterio,

2016).

Audit test- sample of 25% to should be taken by the auditor to check whether approval is

given on all the samples cheques selected for payment to suppliers that are exceeding the

amount of $20000.

Weaknesses of the payment system-

Estimation of production level- Warehouse manager is responsible for making an order of

raw material to the supplier but there are no established rules and regulations that are required

to be followed by this warehouse manager for estimation of production level.

The negative impact of this weakness- inaccurate estimation of production level will result in

excess or lower production level. Excess production will definitely increase the overall cost

of production due to higher inventory management cost (Farooq and De Villiers, 2016). On

the other hand production level lower than demand will result in a loss of opportunity for

profit.

Audit test- Auditor is required to compare the production level in a particular accounting

period and demand for such a product in the market. Accuracy of estimations made by the

warehouse manager will be identified with the help of this test.

Lack of Documentation- Documentation is one of the most important parts of a business

organization in order to maintain accountability and transparency. In the payment system

described by this organization, no record is kept regarding the order made for raw material to

approved suppliers as orders are made over the phone. It is very important to issue a purchase

order to the supplier for ordering raw material as it will help in maintaining an audit trail in a

business organization (Wong and Millington, 2014).

12

by comparing past invoices and delivery note received from the warehouse on a sample basis.

Authorization of payment made to supplier- any payment made in excess of $20000 is

required to be sent by the financial controller to managing director for authorization. This

type of authorization process is very essential in any business organization as it helps in

maintaining transparency and accountability in business processes (Knechel and Salterio,

2016).

Audit test- sample of 25% to should be taken by the auditor to check whether approval is

given on all the samples cheques selected for payment to suppliers that are exceeding the

amount of $20000.

Weaknesses of the payment system-

Estimation of production level- Warehouse manager is responsible for making an order of

raw material to the supplier but there are no established rules and regulations that are required

to be followed by this warehouse manager for estimation of production level.

The negative impact of this weakness- inaccurate estimation of production level will result in

excess or lower production level. Excess production will definitely increase the overall cost

of production due to higher inventory management cost (Farooq and De Villiers, 2016). On

the other hand production level lower than demand will result in a loss of opportunity for

profit.

Audit test- Auditor is required to compare the production level in a particular accounting

period and demand for such a product in the market. Accuracy of estimations made by the

warehouse manager will be identified with the help of this test.

Lack of Documentation- Documentation is one of the most important parts of a business

organization in order to maintain accountability and transparency. In the payment system

described by this organization, no record is kept regarding the order made for raw material to

approved suppliers as orders are made over the phone. It is very important to issue a purchase

order to the supplier for ordering raw material as it will help in maintaining an audit trail in a

business organization (Wong and Millington, 2014).

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.