BAO5524: Professional Auditing Report on Konekt Limited (2018)

VerifiedAdded on 2022/11/26

|18

|3862

|268

Report

AI Summary

This report presents a professional auditing analysis of Konekt Limited's 2018 financial statements. It examines key aspects, including an executive summary, key information, and the nature of the client's business. The report details the audit program, identifies potentially misstated account balances (sales, expenses, cash, intangible assets, and borrowings), and computes planning materiality. It also assesses audit risks associated with these accounts and applies the audit risk model to determine different types of risks. The analysis adheres to relevant auditing standards like ASA 300, ASA 315, ASA 320, and ASA 230, offering a comprehensive overview of the audit process and its application to Konekt Limited. The report aims to evaluate the fairness of the financial statements and provide insights into the audit procedures undertaken.

Running head: PROFESSIONAL AUDITING

Professional Auditing

Name of the Student:

Name of the University:

Author’s Note

Professional Auditing

Name of the Student:

Name of the University:

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

PROFESSIONAL AUDITING

Executive Summary

The main purpose of the assessment is to analyse the financial statement of Konekt Limited for

the year 2018 for analysing if there are any material misstatement in the financial statement of

the business. The assessment would also be ascertaining the risks which is related to the five

account balances as identified in the annual report of the business. The assessment would also be

checking the materiality of the items which are shown in the annual report of the business. The

assessment would also be computing the planning materiality of the business for assessing

whether the items which are shown in the annual report are free from material misstatement or

not. The assessment would also be applying audit risk model for assessing the three types of

risks of the business.

PROFESSIONAL AUDITING

Executive Summary

The main purpose of the assessment is to analyse the financial statement of Konekt Limited for

the year 2018 for analysing if there are any material misstatement in the financial statement of

the business. The assessment would also be ascertaining the risks which is related to the five

account balances as identified in the annual report of the business. The assessment would also be

checking the materiality of the items which are shown in the annual report of the business. The

assessment would also be computing the planning materiality of the business for assessing

whether the items which are shown in the annual report are free from material misstatement or

not. The assessment would also be applying audit risk model for assessing the three types of

risks of the business.

2

PROFESSIONAL AUDITING

Table of Contents

Introduction......................................................................................................................................3

Key Information...............................................................................................................................3

Nature of the Clients Business.....................................................................................................4

Audit Program.............................................................................................................................4

Identification of Materially Misstated Account Balances...........................................................5

Planning Materiality....................................................................................................................7

Audit Risks of the Selected Account Balances............................................................................9

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................15

PROFESSIONAL AUDITING

Table of Contents

Introduction......................................................................................................................................3

Key Information...............................................................................................................................3

Nature of the Clients Business.....................................................................................................4

Audit Program.............................................................................................................................4

Identification of Materially Misstated Account Balances...........................................................5

Planning Materiality....................................................................................................................7

Audit Risks of the Selected Account Balances............................................................................9

Conclusion.....................................................................................................................................14

Reference.......................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

PROFESSIONAL AUDITING

Introduction

The main purpose of the assessment is to analyse the business of Konekt ltd which is

engaged in providing health and risk management services in Australia. The analysis would be

conducted from the perspective of audit in order to asses if the financial statement is showing

true and fair view of the annual report of the business (Konekt.com.au. 2019). The report would

be forming an appropriate audit plan which would focus on collecting evidences on the basis of

which an audit opinion would be formed. The initial steps which are undertaken by the auditor

would be considered for collecting evidences and also proper application of relevant auditing

standards would also be shown in the report. In addition to this, five material accounts which are

shown in the annual report would be assessed in order to ensure that the balances which are

shown are free from material misstatement or not. The report would also be considering the audit

risks which are associated with the five balances which is shown in the annual report of the

business. The assessment would also be showing application of audit risk model to determine the

different risks which are applicable to the five accounts which are considered in the assessment.

Key Information

The first step which is really important if an auditor is conducting audit for a business is

planning the activities of audit process. Appropriate planning results in smooth conducting of the

process of auditing and the auditor is also able to collect important audit evidences relating to the

business. One of the key steps which the auditor of the company needs to undertake is

computation of planning materiality which would help the auditor determine if the financial

statements are showing accurate view of the results. The auditor needs to adhere to relevant

auditing standards during the course of audit and simultaneously apply audit procedure for the

PROFESSIONAL AUDITING

Introduction

The main purpose of the assessment is to analyse the business of Konekt ltd which is

engaged in providing health and risk management services in Australia. The analysis would be

conducted from the perspective of audit in order to asses if the financial statement is showing

true and fair view of the annual report of the business (Konekt.com.au. 2019). The report would

be forming an appropriate audit plan which would focus on collecting evidences on the basis of

which an audit opinion would be formed. The initial steps which are undertaken by the auditor

would be considered for collecting evidences and also proper application of relevant auditing

standards would also be shown in the report. In addition to this, five material accounts which are

shown in the annual report would be assessed in order to ensure that the balances which are

shown are free from material misstatement or not. The report would also be considering the audit

risks which are associated with the five balances which is shown in the annual report of the

business. The assessment would also be showing application of audit risk model to determine the

different risks which are applicable to the five accounts which are considered in the assessment.

Key Information

The first step which is really important if an auditor is conducting audit for a business is

planning the activities of audit process. Appropriate planning results in smooth conducting of the

process of auditing and the auditor is also able to collect important audit evidences relating to the

business. One of the key steps which the auditor of the company needs to undertake is

computation of planning materiality which would help the auditor determine if the financial

statements are showing accurate view of the results. The auditor needs to adhere to relevant

auditing standards during the course of audit and simultaneously apply audit procedure for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

PROFESSIONAL AUDITING

purpose of collection important evidences for the business (Eilifsen and Messier Jr 2014). Some

other steps which are undertaken by the auditor of the business are analytical review, compliance

test of internal control, external confirmation, substantive tests but the same is dependent on the

audit program which is formulated by the auditor as the same determine timing and extent to

which the audit procedure is to be applied.

Nature of the Clients Business

The business which is considered for the purpose audit is Konekt Limited which is

private listed company operating in Australia and the company provides appropriate services to

the clients in relation to health and risk management services. The company is a developing

business as the same operates as a health and risk management business (Edgley 2014). The

focus of the management of the company is to create a workplace which would be safe and

secure. The management of the company operates with an objective to make the workplace a

safer place.

Audit Program

The audit program is formulated by the auditor at the initial stages of audit and includes

detailed steps and procedures which are to be undertaken by the auditor for the purpose of

ensuring that the audit process is smoothly undertaken. The audit program is also developed in

order to ensure that the annual reports of the business are prepared following all relevant

guidelines and regulations which are operating in the country. As per the provisions stated in

Para 7 of ASA 300 Planning an Audit of the Financial Report, the auditor needs to formulate

an appropriate plan at the initial stages of audit so that the auditing strategy appropriately sets out

scope, timing and direction of the audit (Auasb.gov.au. 2019). The audit program also states the

steps which are to be undertaken by the auditor for estimating the planning materiality of the

PROFESSIONAL AUDITING

purpose of collection important evidences for the business (Eilifsen and Messier Jr 2014). Some

other steps which are undertaken by the auditor of the business are analytical review, compliance

test of internal control, external confirmation, substantive tests but the same is dependent on the

audit program which is formulated by the auditor as the same determine timing and extent to

which the audit procedure is to be applied.

Nature of the Clients Business

The business which is considered for the purpose audit is Konekt Limited which is

private listed company operating in Australia and the company provides appropriate services to

the clients in relation to health and risk management services. The company is a developing

business as the same operates as a health and risk management business (Edgley 2014). The

focus of the management of the company is to create a workplace which would be safe and

secure. The management of the company operates with an objective to make the workplace a

safer place.

Audit Program

The audit program is formulated by the auditor at the initial stages of audit and includes

detailed steps and procedures which are to be undertaken by the auditor for the purpose of

ensuring that the audit process is smoothly undertaken. The audit program is also developed in

order to ensure that the annual reports of the business are prepared following all relevant

guidelines and regulations which are operating in the country. As per the provisions stated in

Para 7 of ASA 300 Planning an Audit of the Financial Report, the auditor needs to formulate

an appropriate plan at the initial stages of audit so that the auditing strategy appropriately sets out

scope, timing and direction of the audit (Auasb.gov.au. 2019). The audit program also states the

steps which are to be undertaken by the auditor for estimating the planning materiality of the

5

PROFESSIONAL AUDITING

business (Christensen et al. 2016). The financial report for 2018 is considered for the purpose of

assessing whether the same are showing true and fair view of the financial position or not. The

audit program also requires the auditor to adhere to provisions of ASA 230 Documentation,

which states that proper records need to be maintained by the business so that the auditor can

effectively incorporate in the working papers the figures, estimates and management

representation (Auasb.gov.au. 2019). It is also to be noted that the working papers also forms

part of the audit evidences as the same sets out the procedures and tests which are to be

conducted by the auditor for collecting appropriate audit evidences of the business.

Identification of Materially Misstated Account Balances

The misstatements which affects the financial reports must be identified by the auditor of

the business as the same forms one of the main responsibilities of the auditor. The provisions of

para 5 of ASA 315 Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and Its Environment, states that it is the responsibility of the auditor

to apply risk assessment procedures for the purpose of identification of items which are most

susceptible to audit risks (Auasb.gov.au. 2019). In addition to this, the standard requires the

auditor to properly understand the nature of the business and thereby assess the major risks

which are faced by the auditor (Ruhnke and Schmidt 2014). The auditor of the business also

needs to be apply proper tests for evaluating the internal control system which is established in

the business. The auditor of the business needs to ensure that the financial statements are

showing true and fair view of the financial position of the business. The annual report of Konekt

Limited for the year 2018 is assessed and the key items which are identified as items which can

be misstated are explained below in details:

PROFESSIONAL AUDITING

business (Christensen et al. 2016). The financial report for 2018 is considered for the purpose of

assessing whether the same are showing true and fair view of the financial position or not. The

audit program also requires the auditor to adhere to provisions of ASA 230 Documentation,

which states that proper records need to be maintained by the business so that the auditor can

effectively incorporate in the working papers the figures, estimates and management

representation (Auasb.gov.au. 2019). It is also to be noted that the working papers also forms

part of the audit evidences as the same sets out the procedures and tests which are to be

conducted by the auditor for collecting appropriate audit evidences of the business.

Identification of Materially Misstated Account Balances

The misstatements which affects the financial reports must be identified by the auditor of

the business as the same forms one of the main responsibilities of the auditor. The provisions of

para 5 of ASA 315 Identifying and Assessing the Risks of Material Misstatement through

Understanding the Entity and Its Environment, states that it is the responsibility of the auditor

to apply risk assessment procedures for the purpose of identification of items which are most

susceptible to audit risks (Auasb.gov.au. 2019). In addition to this, the standard requires the

auditor to properly understand the nature of the business and thereby assess the major risks

which are faced by the auditor (Ruhnke and Schmidt 2014). The auditor of the business also

needs to be apply proper tests for evaluating the internal control system which is established in

the business. The auditor of the business needs to ensure that the financial statements are

showing true and fair view of the financial position of the business. The annual report of Konekt

Limited for the year 2018 is assessed and the key items which are identified as items which can

be misstated are explained below in details:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

PROFESSIONAL AUDITING

Sales: The profit and loss statement of the business shows the revenue which is generated

by the business from sales and the annual report for 2018 demonstrate that the sales of the

business have increased tremendously in 2018 in comparison to previous year figure. The

concern for the auditor in such a case is that the sales revenue which is presented in the

annual report might be overstated. This also signifies that the auditor needs to apply

proper substantive procedures for confirming or denying for presence of material

misstatement in the figure.

Total Expenses: The profit and loss statement which is prepared by the business also

represent the total expenses of the business which ultimately determines the profits which

is generated by the business. Some of the expenses such as depreciation, finance costs,

salaries and wages and other expenses significant rise which should be checked by the

auditor of the business for the purpose of assessing whether the financial statements are

showing true and fair view of the financial statements of the business. The auditor of the

business needs to consider the values of expenses which are shown in the financial

statements and judge whether the same are showing appropriate value or not.

Cash and Cash Equivalent: The cash balance which is presented in the annual report of

the business appropriately shows significant increase from the estimate which is shown

for the business in previous year. The auditor needs to check the value which is shown by

applying appropriate procedures (Tepalagul and Lin 2015). There is a chance that cash

balance might be misstated which would affect the financial position of the entire annual

report of the business. The auditor need to apply appropriate auditing procedure so as to

ensure that the financial statement is showing a true and fair view. In such a case, the

PROFESSIONAL AUDITING

Sales: The profit and loss statement of the business shows the revenue which is generated

by the business from sales and the annual report for 2018 demonstrate that the sales of the

business have increased tremendously in 2018 in comparison to previous year figure. The

concern for the auditor in such a case is that the sales revenue which is presented in the

annual report might be overstated. This also signifies that the auditor needs to apply

proper substantive procedures for confirming or denying for presence of material

misstatement in the figure.

Total Expenses: The profit and loss statement which is prepared by the business also

represent the total expenses of the business which ultimately determines the profits which

is generated by the business. Some of the expenses such as depreciation, finance costs,

salaries and wages and other expenses significant rise which should be checked by the

auditor of the business for the purpose of assessing whether the financial statements are

showing true and fair view of the financial statements of the business. The auditor of the

business needs to consider the values of expenses which are shown in the financial

statements and judge whether the same are showing appropriate value or not.

Cash and Cash Equivalent: The cash balance which is presented in the annual report of

the business appropriately shows significant increase from the estimate which is shown

for the business in previous year. The auditor needs to check the value which is shown by

applying appropriate procedures (Tepalagul and Lin 2015). There is a chance that cash

balance might be misstated which would affect the financial position of the entire annual

report of the business. The auditor need to apply appropriate auditing procedure so as to

ensure that the financial statement is showing a true and fair view. In such a case, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

PROFESSIONAL AUDITING

auditor also needs to check the internal control system in order to ensure that proper cash

management policies are implemented in the business of Konekt Limited.

Intangible Assets: The intangible assets of the business are also showing similar increase

in the value and therefore there is a chance the same might not be valued properly

following the provisions of AASB 138 Intangible assets. The financial statement would

be affected if improper value is shown in the balance sheet of the business (Gaynor et al.

2016). The auditor of the business needs to apply appropriate practice such as verification

of the asset in order to assess if the financial statement ate showing true and fair view or

not. The auditor of the business also needs to assess if there are any impairment charges

shown in the annual report of the business.

Borrowings: The annual report of 2018 shows that the business has indulged in

borrowings during the year for meeting the current obligations of the business. The

increase in the borrowings is done to add more leverage to the capital structure which is

used by the business. The auditor needs to check if the management has actually taken

the loan or not and if the same has been taken at the value which is represented in the

financial statements of the business. The interest expenses which is related to the

borrowings need to be checked by the auditor of the business.

Planning Materiality

The purpose of assessing the materiality of the items which are shown in the financial

statement is to identify misstatement which can affect the financial statement of the business. In

order to determine materiality of an item shown in the financial statement, the auditor needs to

consider the nature of item and complexity of the item which is shown in the annual report. The

auditor of the business needs to consider the materiality of each item which is shown in the

PROFESSIONAL AUDITING

auditor also needs to check the internal control system in order to ensure that proper cash

management policies are implemented in the business of Konekt Limited.

Intangible Assets: The intangible assets of the business are also showing similar increase

in the value and therefore there is a chance the same might not be valued properly

following the provisions of AASB 138 Intangible assets. The financial statement would

be affected if improper value is shown in the balance sheet of the business (Gaynor et al.

2016). The auditor of the business needs to apply appropriate practice such as verification

of the asset in order to assess if the financial statement ate showing true and fair view or

not. The auditor of the business also needs to assess if there are any impairment charges

shown in the annual report of the business.

Borrowings: The annual report of 2018 shows that the business has indulged in

borrowings during the year for meeting the current obligations of the business. The

increase in the borrowings is done to add more leverage to the capital structure which is

used by the business. The auditor needs to check if the management has actually taken

the loan or not and if the same has been taken at the value which is represented in the

financial statements of the business. The interest expenses which is related to the

borrowings need to be checked by the auditor of the business.

Planning Materiality

The purpose of assessing the materiality of the items which are shown in the financial

statement is to identify misstatement which can affect the financial statement of the business. In

order to determine materiality of an item shown in the financial statement, the auditor needs to

consider the nature of item and complexity of the item which is shown in the annual report. The

auditor of the business needs to consider the materiality of each item which is shown in the

8

PROFESSIONAL AUDITING

financial statement for the purpose of estimating whether the same are showing appropriate view

or not. The auditor needs to appropriately consider the provisions of ASA 320 Materiality for

the purpose of ascertaining the material items which are considered from the annual report of the

business (Auasb.gov.au. 2019). The auditor of the business also needs to apply the principle of

professional skepticism on all items which are shown in the financial statements of the business

so that the auditor can confirm or deny the presence of material misstatement in the annual report

of the business (Lee. et al. 2016).

The planning materiality of the items are computed in order to asses the performance

materiality of the account balances which are shown in the annual reports of the business. In

order to compute the planning materiality estimate for the business of Konekt Limited, the figure

of total revenue is considered which has shown tremendous increase over the last year. The

auditor considers 0.5% as the percentage on the basis of which the planning materiality amount

would be computed. The annual report of Konekt Limited for the year 2018 shows that the

management of the company has been able to enhance their revenue from previous year and the

same is shown to be $ 87,914,000. The equation which is shown below marks the process which

is used for the purpose of computing the planning materiality of the business.

Planning Materiality=Total Revenue∗0.5 %

¿ $ 87,914 , , 000∗0.5 %

¿ $ 439,570

The planning materiality of the business thus computed is shown to be $ 439,570 and this

estimate would be considered for computing the performance materiality of different items

which are shown in the annual reports of the business (Vaicekauskas and Mackevičius 2014).

PROFESSIONAL AUDITING

financial statement for the purpose of estimating whether the same are showing appropriate view

or not. The auditor needs to appropriately consider the provisions of ASA 320 Materiality for

the purpose of ascertaining the material items which are considered from the annual report of the

business (Auasb.gov.au. 2019). The auditor of the business also needs to apply the principle of

professional skepticism on all items which are shown in the financial statements of the business

so that the auditor can confirm or deny the presence of material misstatement in the annual report

of the business (Lee. et al. 2016).

The planning materiality of the items are computed in order to asses the performance

materiality of the account balances which are shown in the annual reports of the business. In

order to compute the planning materiality estimate for the business of Konekt Limited, the figure

of total revenue is considered which has shown tremendous increase over the last year. The

auditor considers 0.5% as the percentage on the basis of which the planning materiality amount

would be computed. The annual report of Konekt Limited for the year 2018 shows that the

management of the company has been able to enhance their revenue from previous year and the

same is shown to be $ 87,914,000. The equation which is shown below marks the process which

is used for the purpose of computing the planning materiality of the business.

Planning Materiality=Total Revenue∗0.5 %

¿ $ 87,914 , , 000∗0.5 %

¿ $ 439,570

The planning materiality of the business thus computed is shown to be $ 439,570 and this

estimate would be considered for computing the performance materiality of different items

which are shown in the annual reports of the business (Vaicekauskas and Mackevičius 2014).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

PROFESSIONAL AUDITING

The planning materiality estimate effectively allows the auditor of the business to assess material

items and thereby form an opinion on the basis of the same.

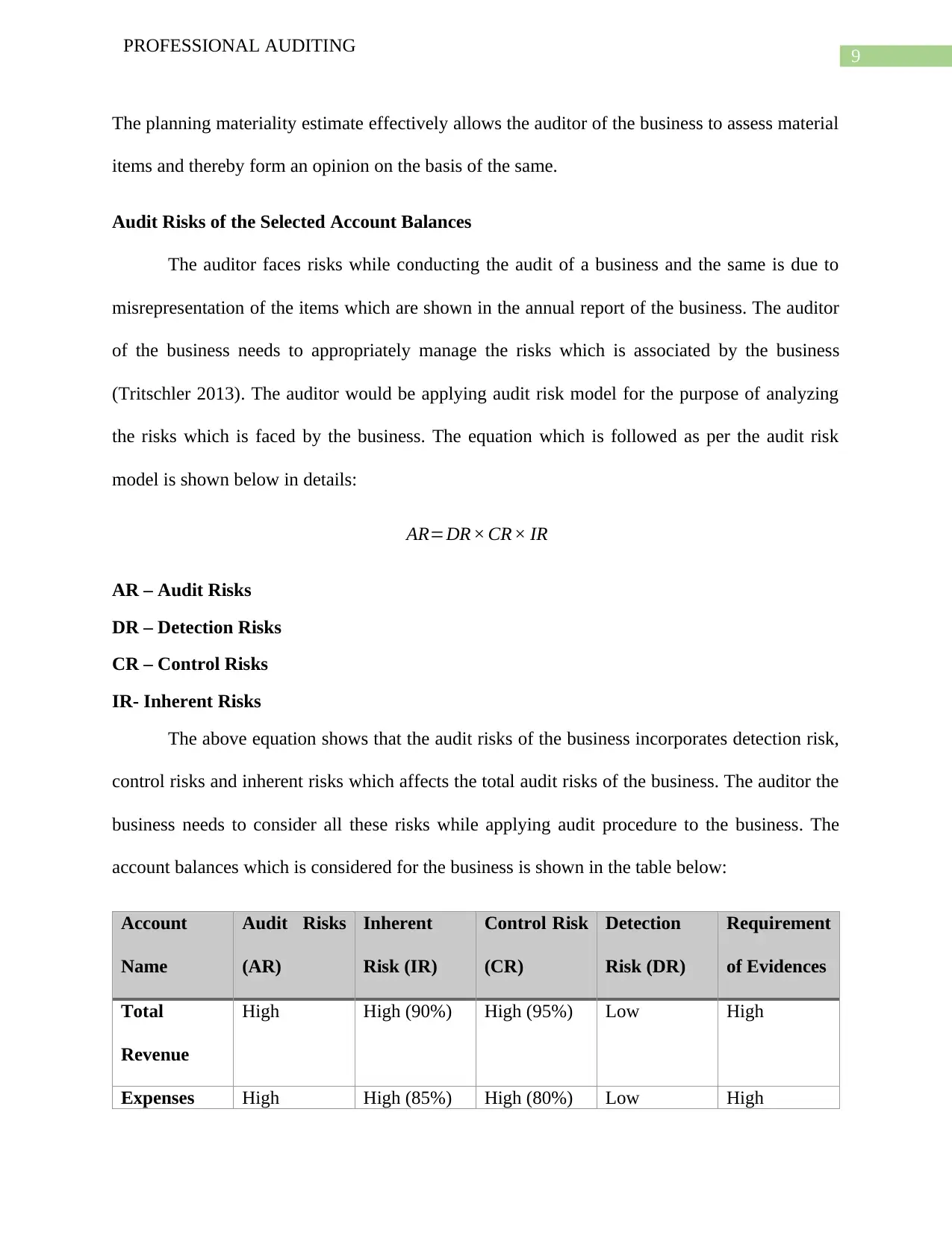

Audit Risks of the Selected Account Balances

The auditor faces risks while conducting the audit of a business and the same is due to

misrepresentation of the items which are shown in the annual report of the business. The auditor

of the business needs to appropriately manage the risks which is associated by the business

(Tritschler 2013). The auditor would be applying audit risk model for the purpose of analyzing

the risks which is faced by the business. The equation which is followed as per the audit risk

model is shown below in details:

AR=DR × CR× IR

AR – Audit Risks

DR – Detection Risks

CR – Control Risks

IR- Inherent Risks

The above equation shows that the audit risks of the business incorporates detection risk,

control risks and inherent risks which affects the total audit risks of the business. The auditor the

business needs to consider all these risks while applying audit procedure to the business. The

account balances which is considered for the business is shown in the table below:

Account

Name

Audit Risks

(AR)

Inherent

Risk (IR)

Control Risk

(CR)

Detection

Risk (DR)

Requirement

of Evidences

Total

Revenue

High High (90%) High (95%) Low High

Expenses High High (85%) High (80%) Low High

PROFESSIONAL AUDITING

The planning materiality estimate effectively allows the auditor of the business to assess material

items and thereby form an opinion on the basis of the same.

Audit Risks of the Selected Account Balances

The auditor faces risks while conducting the audit of a business and the same is due to

misrepresentation of the items which are shown in the annual report of the business. The auditor

of the business needs to appropriately manage the risks which is associated by the business

(Tritschler 2013). The auditor would be applying audit risk model for the purpose of analyzing

the risks which is faced by the business. The equation which is followed as per the audit risk

model is shown below in details:

AR=DR × CR× IR

AR – Audit Risks

DR – Detection Risks

CR – Control Risks

IR- Inherent Risks

The above equation shows that the audit risks of the business incorporates detection risk,

control risks and inherent risks which affects the total audit risks of the business. The auditor the

business needs to consider all these risks while applying audit procedure to the business. The

account balances which is considered for the business is shown in the table below:

Account

Name

Audit Risks

(AR)

Inherent

Risk (IR)

Control Risk

(CR)

Detection

Risk (DR)

Requirement

of Evidences

Total

Revenue

High High (90%) High (95%) Low High

Expenses High High (85%) High (80%) Low High

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

PROFESSIONAL AUDITING

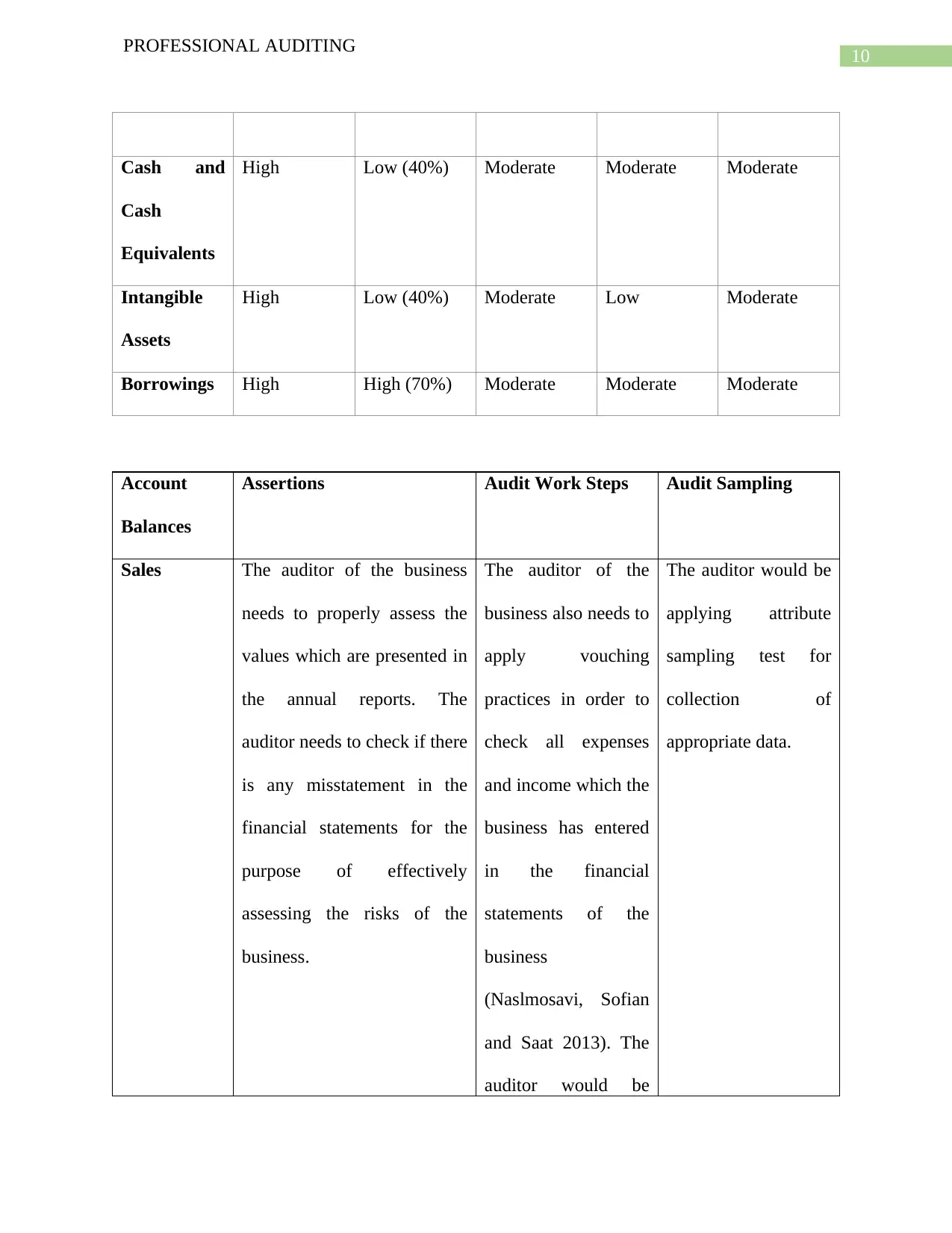

Cash and

Cash

Equivalents

High Low (40%) Moderate Moderate Moderate

Intangible

Assets

High Low (40%) Moderate Low Moderate

Borrowings High High (70%) Moderate Moderate Moderate

Account

Balances

Assertions Audit Work Steps Audit Sampling

Sales The auditor of the business

needs to properly assess the

values which are presented in

the annual reports. The

auditor needs to check if there

is any misstatement in the

financial statements for the

purpose of effectively

assessing the risks of the

business.

The auditor of the

business also needs to

apply vouching

practices in order to

check all expenses

and income which the

business has entered

in the financial

statements of the

business

(Naslmosavi, Sofian

and Saat 2013). The

auditor would be

The auditor would be

applying attribute

sampling test for

collection of

appropriate data.

PROFESSIONAL AUDITING

Cash and

Cash

Equivalents

High Low (40%) Moderate Moderate Moderate

Intangible

Assets

High Low (40%) Moderate Low Moderate

Borrowings High High (70%) Moderate Moderate Moderate

Account

Balances

Assertions Audit Work Steps Audit Sampling

Sales The auditor of the business

needs to properly assess the

values which are presented in

the annual reports. The

auditor needs to check if there

is any misstatement in the

financial statements for the

purpose of effectively

assessing the risks of the

business.

The auditor of the

business also needs to

apply vouching

practices in order to

check all expenses

and income which the

business has entered

in the financial

statements of the

business

(Naslmosavi, Sofian

and Saat 2013). The

auditor would be

The auditor would be

applying attribute

sampling test for

collection of

appropriate data.

11

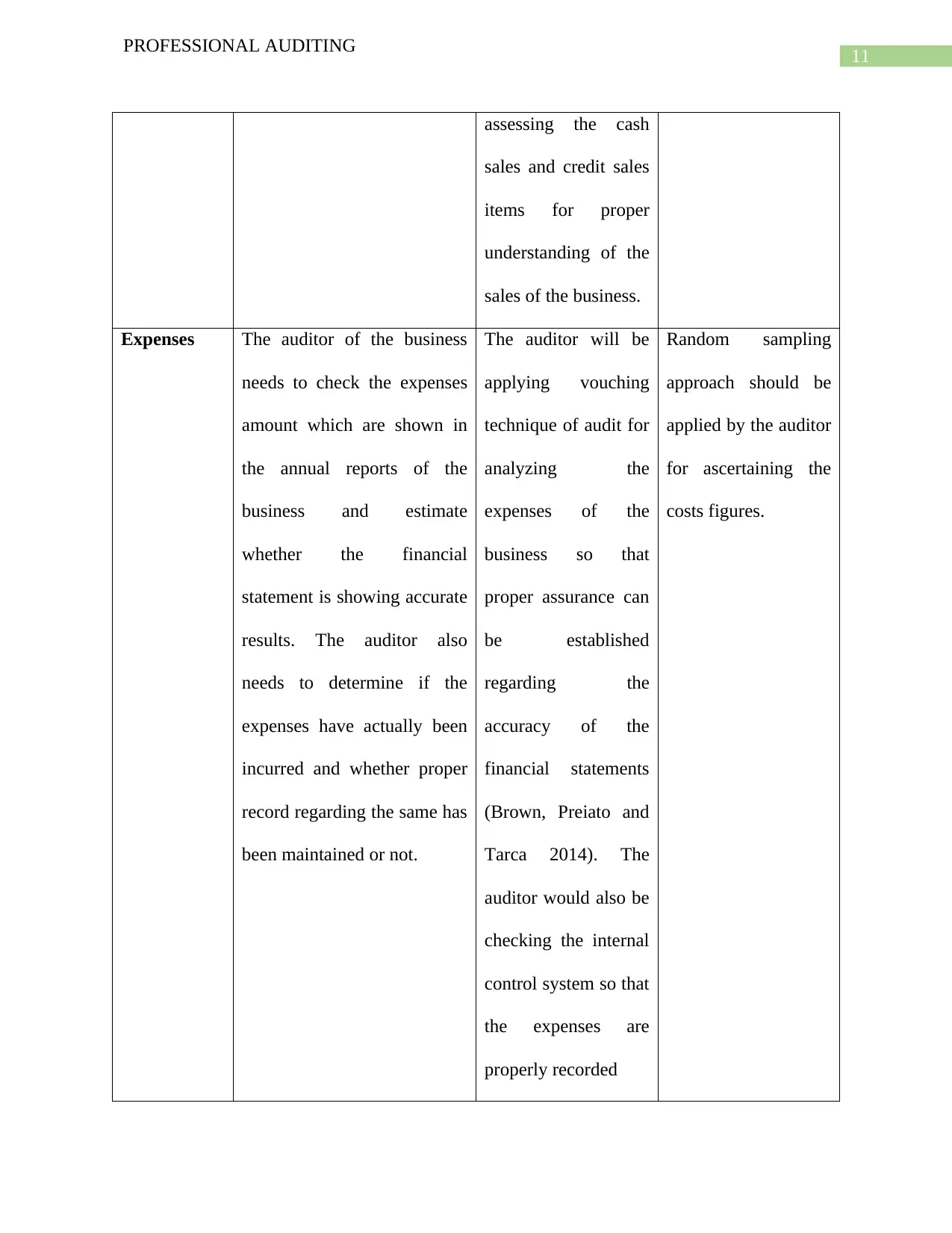

PROFESSIONAL AUDITING

assessing the cash

sales and credit sales

items for proper

understanding of the

sales of the business.

Expenses The auditor of the business

needs to check the expenses

amount which are shown in

the annual reports of the

business and estimate

whether the financial

statement is showing accurate

results. The auditor also

needs to determine if the

expenses have actually been

incurred and whether proper

record regarding the same has

been maintained or not.

The auditor will be

applying vouching

technique of audit for

analyzing the

expenses of the

business so that

proper assurance can

be established

regarding the

accuracy of the

financial statements

(Brown, Preiato and

Tarca 2014). The

auditor would also be

checking the internal

control system so that

the expenses are

properly recorded

Random sampling

approach should be

applied by the auditor

for ascertaining the

costs figures.

PROFESSIONAL AUDITING

assessing the cash

sales and credit sales

items for proper

understanding of the

sales of the business.

Expenses The auditor of the business

needs to check the expenses

amount which are shown in

the annual reports of the

business and estimate

whether the financial

statement is showing accurate

results. The auditor also

needs to determine if the

expenses have actually been

incurred and whether proper

record regarding the same has

been maintained or not.

The auditor will be

applying vouching

technique of audit for

analyzing the

expenses of the

business so that

proper assurance can

be established

regarding the

accuracy of the

financial statements

(Brown, Preiato and

Tarca 2014). The

auditor would also be

checking the internal

control system so that

the expenses are

properly recorded

Random sampling

approach should be

applied by the auditor

for ascertaining the

costs figures.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.