ACCG224: Financial Accounting and Reporting - Impairment Analysis

VerifiedAdded on 2022/12/14

|13

|838

|424

Report

AI Summary

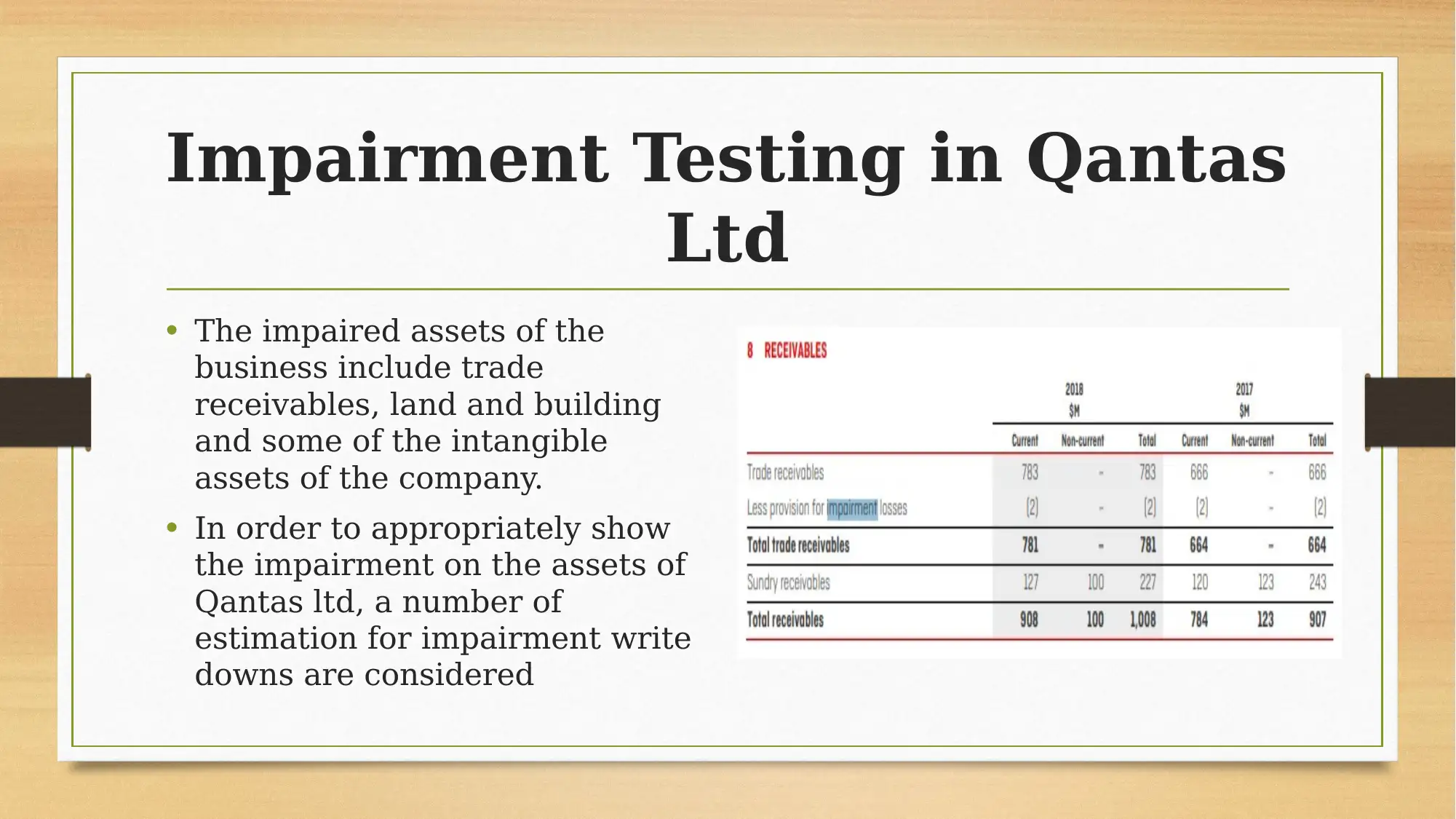

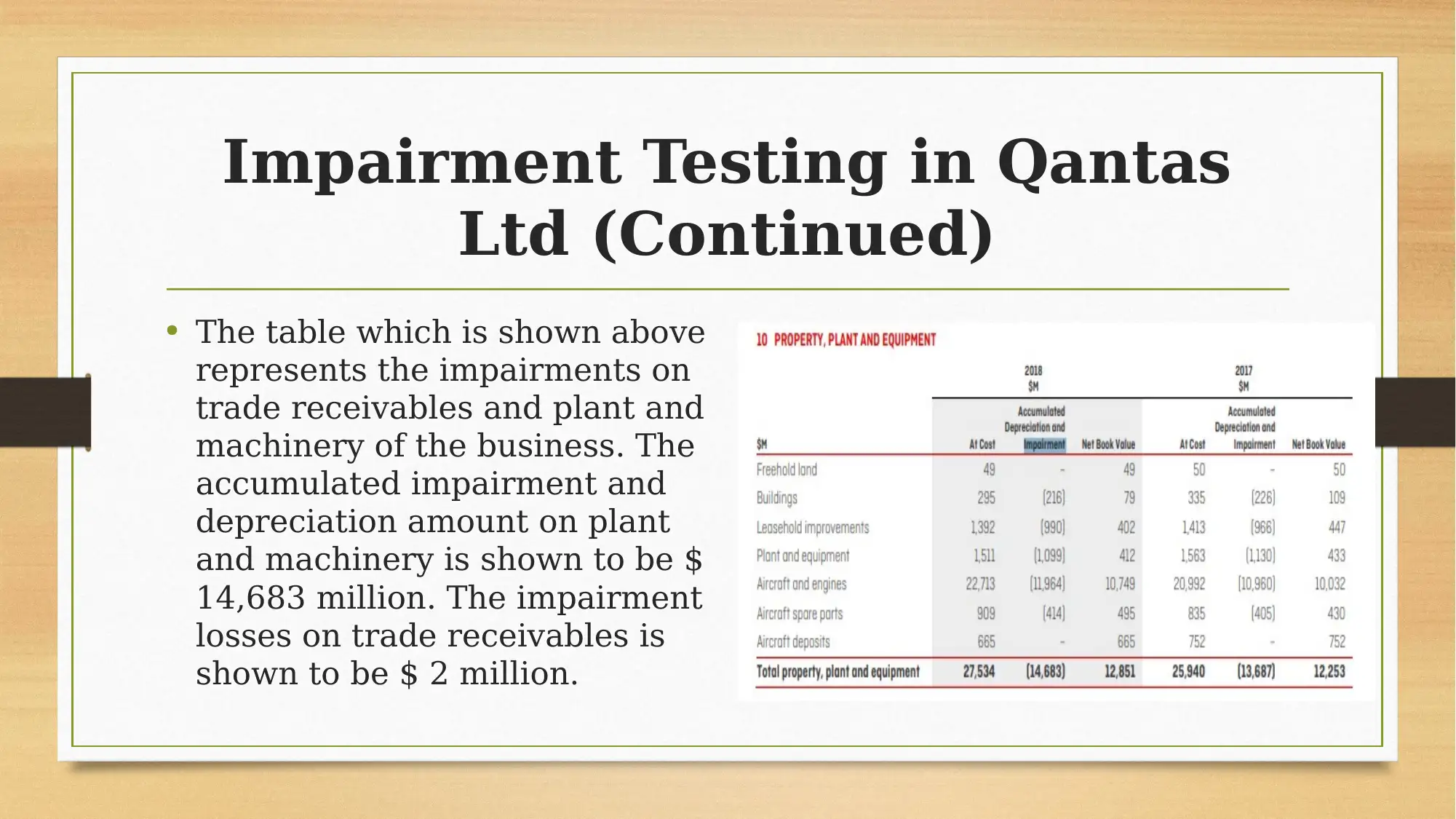

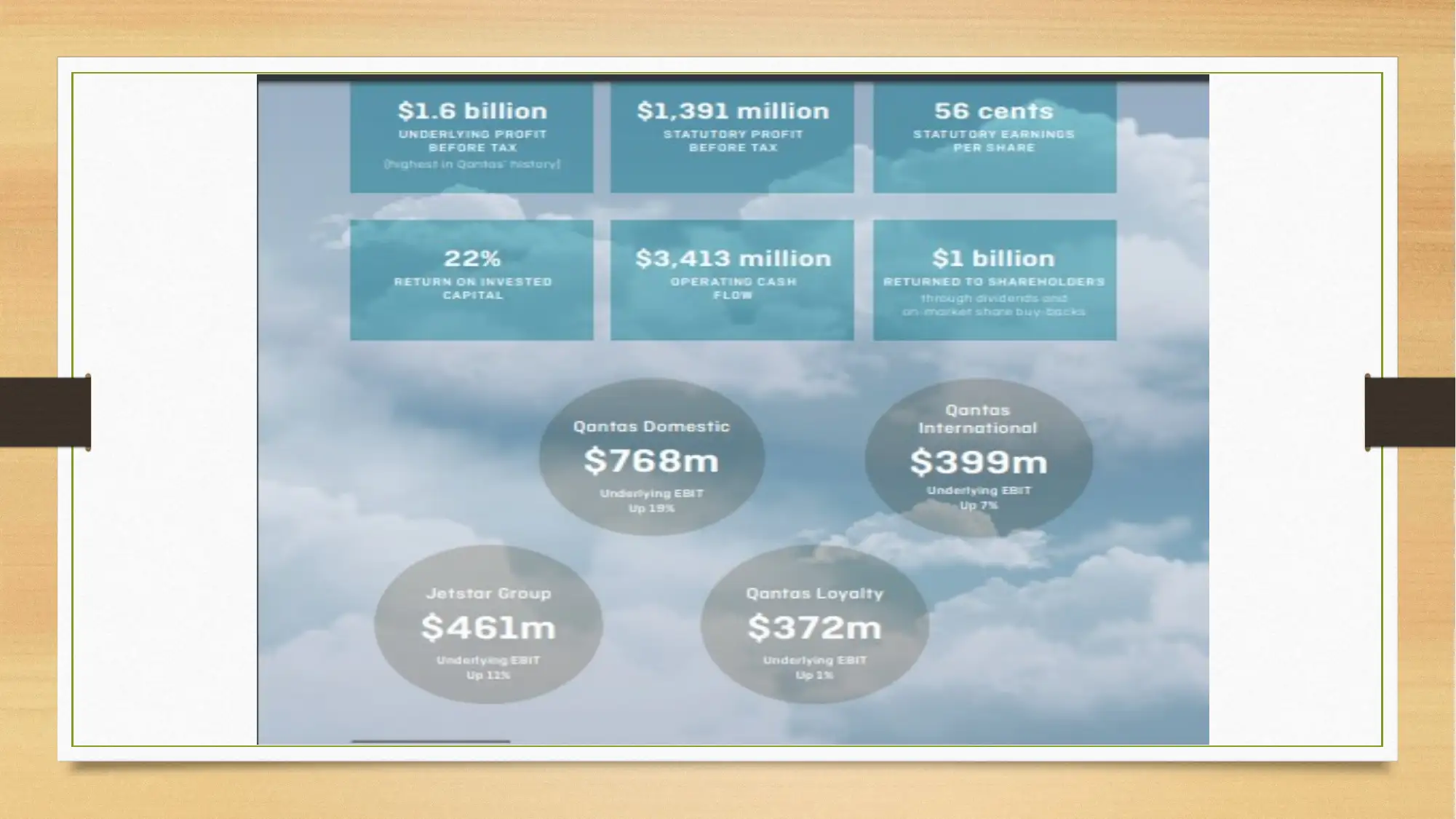

This report analyzes the application of professional judgment in financial accounting, focusing on impairment testing within Qantas Ltd. It examines the significance of professional judgment in ensuring the quality of financial reports and its implications on decision-making by stakeholders. The report delves into the impairment testing procedures, including trade receivables, land, building, and intangible assets, and considers the estimation for impairment write-downs. It also explores the requirements of the Australian Securities and Investments Commission (ASIC) regarding cash flow assumptions, fair value determination, and the identification of Cash Generating Units (CGUs). Furthermore, the report discusses the principles of the general-purpose financial reporting framework and evaluates the application of these principles by Qantas Ltd, highlighting the importance of detailed disclosures in cases of asset impairments. The conclusion emphasizes the crucial role of professional judgment in maintaining the integrity of financial reports and suggests areas for improved disclosure in impairment testing.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.