Professional Judgement and Asset Impairment Analysis: ALTIUM LIMITED

VerifiedAdded on 2023/01/18

|11

|2581

|33

Report

AI Summary

This report provides an in-depth analysis of professional judgement in accounting, specifically focusing on asset impairment within ALTIUM LIMITED. It examines how accountants use their skills and experience to make critical decisions regarding accounting policies and estimates, especially concerning the impairment of assets like goodwill and other intangible assets. The report highlights the implications of unreasonable professional judgement on users of financial information and explores the treatment of various assets, including goodwill and trade receivables. It discusses the estimation methods used to determine impairments and the importance of relevant disclosures. Furthermore, it aligns professional judgement on impairments with the objectives of general-purpose financial statements, emphasizing the need for clear and understandable information for all users. The report also provides detailed financial data from ALTIUM LIMITED's annual reports, including write-downs, reconciliations, and the annual testing of goodwill for impairment. The author recommends increased disclosures on the basis of provisions for doubtful debts to enhance transparency and assist stakeholders in making informed decisions.

PROFESIONAL JUDGEMENT AND IMPAIRMENT 1

UNIVERSITY NAME

STUDENT NAME

STUDENT ID

COURSE

DATE.

UNIVERSITY NAME

STUDENT NAME

STUDENT ID

COURSE

DATE.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PROFESIONAL JUDGEMENT AND IMPAIRMENT 2

EXECUTIVE SUMMARY

The purpose of this research is to discuss the issue of professional judgement of accountants of

ALTIUM LIMITED regarding impairments of assets.it critically analyses how an accountant

uses their professional judgement in determination of various accounting decisions regarding

policies and rules governing impairments.it also examine how accountants treat various assets

such as goodwill and other intangible assets. This report also points out the implications that

unreasonable professional judgement can bring to the users of financial information.

It describes how to make various provisions regarding trade receivables. Accountant uses

professional judgement in determination of amount to be provided for doubtful debts.it is noted

that ALTIUM LIMITED has between 30-90 days’ terms of accounts receivables.

It also discusses how professional judgment regarding the determination of impairments will

assist the users of those financial information in making various decisions such as investment

decision.

EXECUTIVE SUMMARY

The purpose of this research is to discuss the issue of professional judgement of accountants of

ALTIUM LIMITED regarding impairments of assets.it critically analyses how an accountant

uses their professional judgement in determination of various accounting decisions regarding

policies and rules governing impairments.it also examine how accountants treat various assets

such as goodwill and other intangible assets. This report also points out the implications that

unreasonable professional judgement can bring to the users of financial information.

It describes how to make various provisions regarding trade receivables. Accountant uses

professional judgement in determination of amount to be provided for doubtful debts.it is noted

that ALTIUM LIMITED has between 30-90 days’ terms of accounts receivables.

It also discusses how professional judgment regarding the determination of impairments will

assist the users of those financial information in making various decisions such as investment

decision.

PROFESIONAL JUDGEMENT AND IMPAIRMENT 3

Table of Contents

INTRODUCTION.......................................................................................................................................4

PROFESSIONAL JUDGEMENT...............................................................................................................4

IMPLICATIONS TO USERS OF ACCOUNTING INFORMATION IF PROFESSIONAL

JUDGEMENT HAS NOT BEEN MADE IN THE MOST REASONABLE MANNER.............................5

IMPAIRMENT............................................................................................................................................5

ASSETS IMPAIRED..................................................................................................................................6

GOODWILL AND OTHER INTANGIBLE ASSETS................................................................................6

ESTIMATION USED TO DETERMINE IMPAIRMENT.........................................................................6

AMOUNT OF WRITE-DOWNS AND RECONCILIATION THEREOFF................................................7

DISCLOSURE ON IMPAIRMENT TEST.................................................................................................7

HOW PROFESSIONAL JUDGEMENT ON IMPAIRMENTS ALIGN WITH OBJECTIVES OF

GENERAL PURPOSE FINANCIAL STATETEMENTS..........................................................................9

CONCLUSION...........................................................................................................................................9

REFERENCES..............................................................................................................................................10

Table of Contents

INTRODUCTION.......................................................................................................................................4

PROFESSIONAL JUDGEMENT...............................................................................................................4

IMPLICATIONS TO USERS OF ACCOUNTING INFORMATION IF PROFESSIONAL

JUDGEMENT HAS NOT BEEN MADE IN THE MOST REASONABLE MANNER.............................5

IMPAIRMENT............................................................................................................................................5

ASSETS IMPAIRED..................................................................................................................................6

GOODWILL AND OTHER INTANGIBLE ASSETS................................................................................6

ESTIMATION USED TO DETERMINE IMPAIRMENT.........................................................................6

AMOUNT OF WRITE-DOWNS AND RECONCILIATION THEREOFF................................................7

DISCLOSURE ON IMPAIRMENT TEST.................................................................................................7

HOW PROFESSIONAL JUDGEMENT ON IMPAIRMENTS ALIGN WITH OBJECTIVES OF

GENERAL PURPOSE FINANCIAL STATETEMENTS..........................................................................9

CONCLUSION...........................................................................................................................................9

REFERENCES..............................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PROFESIONAL JUDGEMENT AND IMPAIRMENT 4

INTRODUCTION.

Professional judgement is the use of skills and experience acquired from training. In accounting,

this is used in determination of accounting estimates and policies to be applied in determination

of various accounting decisions like measurement of impairments and calculation of fair values

of different assets.

PROFESSIONAL JUDGEMENT.

This involves use of knowledge, skills and experience amassed from long-term conduct of the

same job and from training through utilization of ethical codes relevant in the field and from

making some decisions such as accounting treatment of various transactions (Stefan, 2015, pg.

713).

Various companies would like to present their financial statements in the most impressive way

and in a way that can portray a good image of the company. To do this, companies must utilize

skills and experience of various accountants who can use skills and experience in determination

of various economic decisions affecting the company’s transactions.

When a professional judgement is used in making accounting decisions, relevant disclosures

must be adequately made and necessary documentations as to how various analysis and

conclusion were arrived at must be made.

It is applied when making some decisions in areas where there are some uncertainties and where

the elements concerned might have adverse effects on other parties. Professional judgement is

applied in various areas in accounting treatment and disclosures of various assumptions relating

to various economic transactions such as;

1. Accounting policies and estimates used in a particular transaction such as depreciable

useful life of a certain asset utilizes professional judgement of an accountant.

2. It is applicable in the determination of impairment of various assets, if such impairments

have happened and any provisions if any.

INTRODUCTION.

Professional judgement is the use of skills and experience acquired from training. In accounting,

this is used in determination of accounting estimates and policies to be applied in determination

of various accounting decisions like measurement of impairments and calculation of fair values

of different assets.

PROFESSIONAL JUDGEMENT.

This involves use of knowledge, skills and experience amassed from long-term conduct of the

same job and from training through utilization of ethical codes relevant in the field and from

making some decisions such as accounting treatment of various transactions (Stefan, 2015, pg.

713).

Various companies would like to present their financial statements in the most impressive way

and in a way that can portray a good image of the company. To do this, companies must utilize

skills and experience of various accountants who can use skills and experience in determination

of various economic decisions affecting the company’s transactions.

When a professional judgement is used in making accounting decisions, relevant disclosures

must be adequately made and necessary documentations as to how various analysis and

conclusion were arrived at must be made.

It is applied when making some decisions in areas where there are some uncertainties and where

the elements concerned might have adverse effects on other parties. Professional judgement is

applied in various areas in accounting treatment and disclosures of various assumptions relating

to various economic transactions such as;

1. Accounting policies and estimates used in a particular transaction such as depreciable

useful life of a certain asset utilizes professional judgement of an accountant.

2. It is applicable in the determination of impairment of various assets, if such impairments

have happened and any provisions if any.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PROFESIONAL JUDGEMENT AND IMPAIRMENT 5

3. Utilized in definition of “value” of various accounting items such as fair value, net

realizable value, replacement value etc. This is done through selection of one basis of

measurement either historical, FV, NRV or PV.

Experience and long term professional skills are highly applicable in professional

judgement as someone short of experience may not be able to make judgement

accurately.

Professional judgement is an important skill for accountants who prepares financial

statements more so under principle based accounting.

IMPLICATIONS TO USERS OF ACCOUNTING INFORMATION

IF PROFESSIONAL JUDGEMENT HAS NOT BEEN MADE IN

THE MOST REASONABLE MANNER.

If impairments of assets have not been determined in the most reasonable manner

and accurate carrying amount of the assets determined, it will lead to

misstatement of entity’s financial position. This might also have been transferred

into the income statement which will give a wrong picture to investors thus

making wrong investment decisions. This will affect them negatively (Trotman,

Tan & Ang, 2011, pg. 279).

Wrong picture of the company’s financial position will impact negatively to the

image of the organization as financiers such as lenders of funds will not be able to

make appropriate lending decisions (Linnenluecke , Birt, Lyon &Sidhu, 2015,

pg.921).

IMPAIRMENT

This refers to a reduction in the carrying amount of an intangible asset such as goodwill

(Jackling, Howieson & Natoli, 2012, pg.340). GOODWILL for instance is tested for

goodwill impairment on an annual basis so as to ascertain the amount reduced in its

carrying amount from the start of the year to the end of the year. According to the

disclosure made by ALTIUM LIMITED, it states that goodwill is tested for impairment

annually. It is further disclosed that impairment of goodwill is taken into income

statement and are not reversed. Goodwill is not amortized but tested for impairment on an

annual basis.

3. Utilized in definition of “value” of various accounting items such as fair value, net

realizable value, replacement value etc. This is done through selection of one basis of

measurement either historical, FV, NRV or PV.

Experience and long term professional skills are highly applicable in professional

judgement as someone short of experience may not be able to make judgement

accurately.

Professional judgement is an important skill for accountants who prepares financial

statements more so under principle based accounting.

IMPLICATIONS TO USERS OF ACCOUNTING INFORMATION

IF PROFESSIONAL JUDGEMENT HAS NOT BEEN MADE IN

THE MOST REASONABLE MANNER.

If impairments of assets have not been determined in the most reasonable manner

and accurate carrying amount of the assets determined, it will lead to

misstatement of entity’s financial position. This might also have been transferred

into the income statement which will give a wrong picture to investors thus

making wrong investment decisions. This will affect them negatively (Trotman,

Tan & Ang, 2011, pg. 279).

Wrong picture of the company’s financial position will impact negatively to the

image of the organization as financiers such as lenders of funds will not be able to

make appropriate lending decisions (Linnenluecke , Birt, Lyon &Sidhu, 2015,

pg.921).

IMPAIRMENT

This refers to a reduction in the carrying amount of an intangible asset such as goodwill

(Jackling, Howieson & Natoli, 2012, pg.340). GOODWILL for instance is tested for

goodwill impairment on an annual basis so as to ascertain the amount reduced in its

carrying amount from the start of the year to the end of the year. According to the

disclosure made by ALTIUM LIMITED, it states that goodwill is tested for impairment

annually. It is further disclosed that impairment of goodwill is taken into income

statement and are not reversed. Goodwill is not amortized but tested for impairment on an

annual basis.

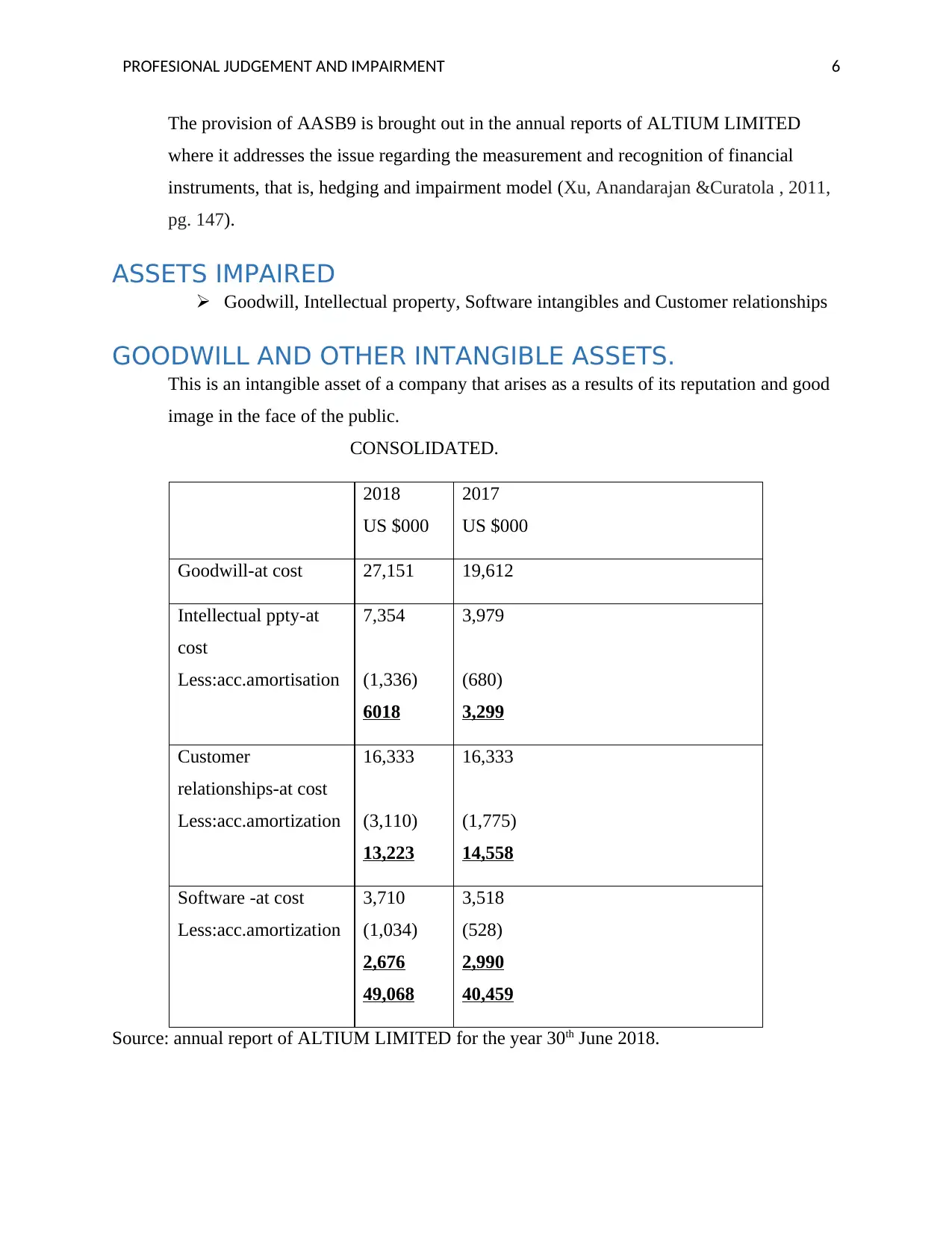

PROFESIONAL JUDGEMENT AND IMPAIRMENT 6

The provision of AASB9 is brought out in the annual reports of ALTIUM LIMITED

where it addresses the issue regarding the measurement and recognition of financial

instruments, that is, hedging and impairment model (Xu, Anandarajan &Curatola , 2011,

pg. 147).

ASSETS IMPAIRED

Goodwill, Intellectual property, Software intangibles and Customer relationships

GOODWILL AND OTHER INTANGIBLE ASSETS.

This is an intangible asset of a company that arises as a results of its reputation and good

image in the face of the public.

CONSOLIDATED.

2018

US $000

2017

US $000

Goodwill-at cost 27,151 19,612

Intellectual ppty-at

cost

Less:acc.amortisation

7,354

(1,336)

6018

3,979

(680)

3,299

Customer

relationships-at cost

Less:acc.amortization

16,333

(3,110)

13,223

16,333

(1,775)

14,558

Software -at cost

Less:acc.amortization

3,710

(1,034)

2,676

49,068

3,518

(528)

2,990

40,459

Source: annual report of ALTIUM LIMITED for the year 30th June 2018.

The provision of AASB9 is brought out in the annual reports of ALTIUM LIMITED

where it addresses the issue regarding the measurement and recognition of financial

instruments, that is, hedging and impairment model (Xu, Anandarajan &Curatola , 2011,

pg. 147).

ASSETS IMPAIRED

Goodwill, Intellectual property, Software intangibles and Customer relationships

GOODWILL AND OTHER INTANGIBLE ASSETS.

This is an intangible asset of a company that arises as a results of its reputation and good

image in the face of the public.

CONSOLIDATED.

2018

US $000

2017

US $000

Goodwill-at cost 27,151 19,612

Intellectual ppty-at

cost

Less:acc.amortisation

7,354

(1,336)

6018

3,979

(680)

3,299

Customer

relationships-at cost

Less:acc.amortization

16,333

(3,110)

13,223

16,333

(1,775)

14,558

Software -at cost

Less:acc.amortization

3,710

(1,034)

2,676

49,068

3,518

(528)

2,990

40,459

Source: annual report of ALTIUM LIMITED for the year 30th June 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PROFESIONAL JUDGEMENT AND IMPAIRMENT 7

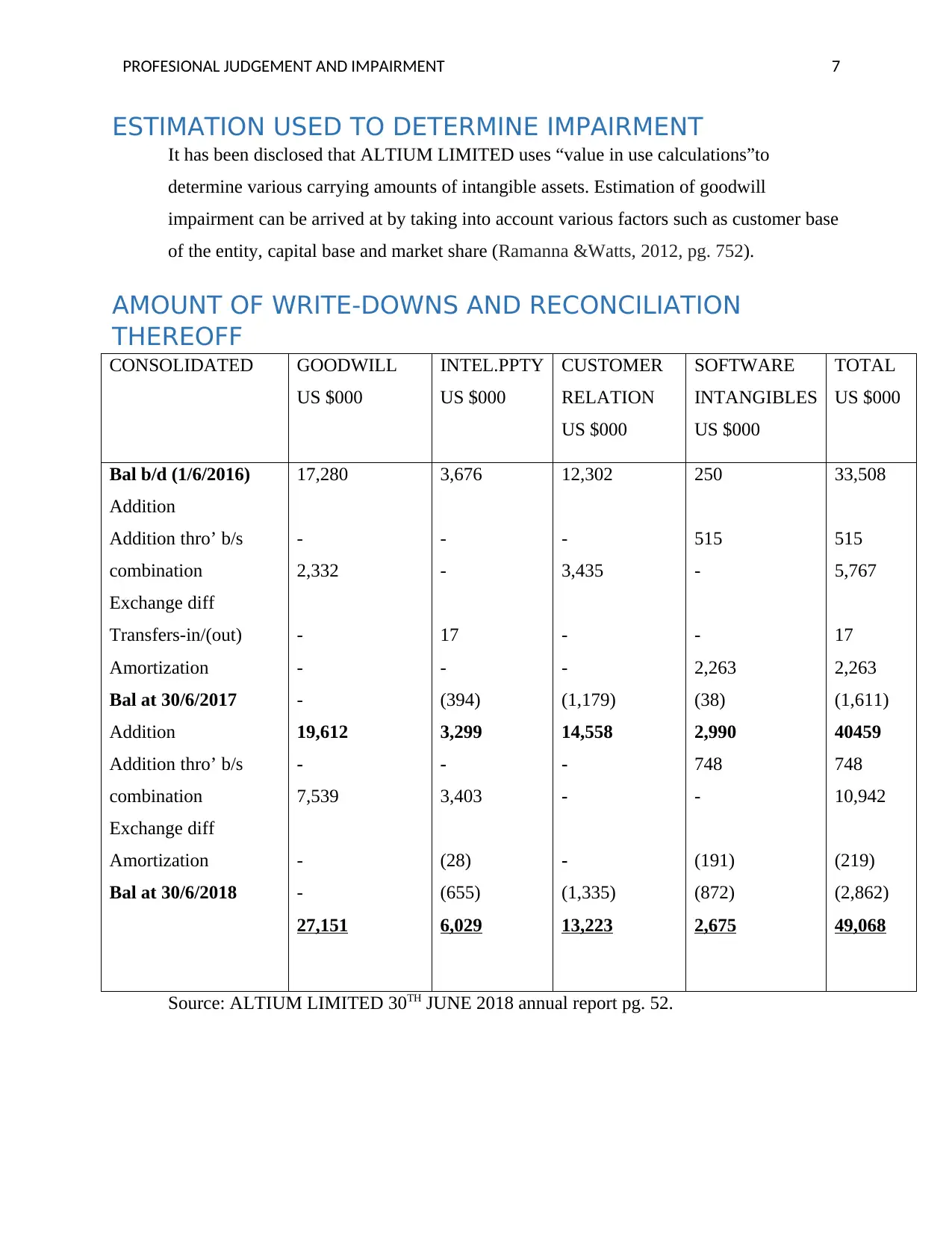

ESTIMATION USED TO DETERMINE IMPAIRMENT

It has been disclosed that ALTIUM LIMITED uses “value in use calculations”to

determine various carrying amounts of intangible assets. Estimation of goodwill

impairment can be arrived at by taking into account various factors such as customer base

of the entity, capital base and market share (Ramanna &Watts, 2012, pg. 752).

AMOUNT OF WRITE-DOWNS AND RECONCILIATION

THEREOFF

CONSOLIDATED GOODWILL

US $000

INTEL.PPTY

US $000

CUSTOMER

RELATION

US $000

SOFTWARE

INTANGIBLES

US $000

TOTAL

US $000

Bal b/d (1/6/2016)

Addition

Addition thro’ b/s

combination

Exchange diff

Transfers-in/(out)

Amortization

Bal at 30/6/2017

Addition

Addition thro’ b/s

combination

Exchange diff

Amortization

Bal at 30/6/2018

17,280

-

2,332

-

-

-

19,612

-

7,539

-

-

27,151

3,676

-

-

17

-

(394)

3,299

-

3,403

(28)

(655)

6,029

12,302

-

3,435

-

-

(1,179)

14,558

-

-

-

(1,335)

13,223

250

515

-

-

2,263

(38)

2,990

748

-

(191)

(872)

2,675

33,508

515

5,767

17

2,263

(1,611)

40459

748

10,942

(219)

(2,862)

49,068

Source: ALTIUM LIMITED 30TH JUNE 2018 annual report pg. 52.

ESTIMATION USED TO DETERMINE IMPAIRMENT

It has been disclosed that ALTIUM LIMITED uses “value in use calculations”to

determine various carrying amounts of intangible assets. Estimation of goodwill

impairment can be arrived at by taking into account various factors such as customer base

of the entity, capital base and market share (Ramanna &Watts, 2012, pg. 752).

AMOUNT OF WRITE-DOWNS AND RECONCILIATION

THEREOFF

CONSOLIDATED GOODWILL

US $000

INTEL.PPTY

US $000

CUSTOMER

RELATION

US $000

SOFTWARE

INTANGIBLES

US $000

TOTAL

US $000

Bal b/d (1/6/2016)

Addition

Addition thro’ b/s

combination

Exchange diff

Transfers-in/(out)

Amortization

Bal at 30/6/2017

Addition

Addition thro’ b/s

combination

Exchange diff

Amortization

Bal at 30/6/2018

17,280

-

2,332

-

-

-

19,612

-

7,539

-

-

27,151

3,676

-

-

17

-

(394)

3,299

-

3,403

(28)

(655)

6,029

12,302

-

3,435

-

-

(1,179)

14,558

-

-

-

(1,335)

13,223

250

515

-

-

2,263

(38)

2,990

748

-

(191)

(872)

2,675

33,508

515

5,767

17

2,263

(1,611)

40459

748

10,942

(219)

(2,862)

49,068

Source: ALTIUM LIMITED 30TH JUNE 2018 annual report pg. 52.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PROFESIONAL JUDGEMENT AND IMPAIRMENT 8

DISCLOSURE ON IMPAIRMENT TEST

It has been fully disclosed by the company that goodwill is annually reviewed or tested for any

impairment so that excess book value is not to carried.

(C) Based on the above write downs in values, reasonable professional judgement and due care

has been adhered to in the determination of such values and relevant disclosures. According to

the requirements of professional judgement, there must be a level of consistency with regard to

items under question and relevant disclosures must be made accordingly (Nguyen, Hooper

&Sinclair, 2013, pg.480).

It is noted that, ALTIUM LIMITED has made various disclosures regarding impairment of

various assets, for instance they have disclosed to the public that they have applied “value in use

calculation” to determine carrying amounts of various intangible assets.

It is further noted that, goodwill is annually tested for impairment (Chalmers, Godfrey

&Webster, 2011, pg. 646). This fact has been sufficiently disclosed in the report so that other

interested parties can understand the information contained in the annual reports better.

They have further indicated that their terms regarding receivables range between 30-60 days.

This has been clearly disclosed.

According to the information in the above table extracted from the books of ALTIUM

LIMITED, goodwill is seen to be rising, for instance goodwill b/d from 2016 is 17280 and there

is goodwill gained as a results of business combination (note 30) of 2,332. this has led to an

increase in goodwill to US $ 19,612 in 2017.It is also noted that there is an increment of US

$7,539 in the course of 2018.This is also as a results of addition from business combination. In

the event that businesses combine, goodwill is revalued to ascertain their carrying amount and in

the case above, it shows that accountants have used their professional judgements to establish

goodwill for business combination in the respective years.

Intellectual property has been impaired from US $ 3,676 in 2016 to US $ 3,299 in 2017.This is

due to amortization value of US $ 394.It increased in value in 2018 due to addition from business

combination of US $ 3403 resulting to a new value of US $ 6,019 in 2018.

DISCLOSURE ON IMPAIRMENT TEST

It has been fully disclosed by the company that goodwill is annually reviewed or tested for any

impairment so that excess book value is not to carried.

(C) Based on the above write downs in values, reasonable professional judgement and due care

has been adhered to in the determination of such values and relevant disclosures. According to

the requirements of professional judgement, there must be a level of consistency with regard to

items under question and relevant disclosures must be made accordingly (Nguyen, Hooper

&Sinclair, 2013, pg.480).

It is noted that, ALTIUM LIMITED has made various disclosures regarding impairment of

various assets, for instance they have disclosed to the public that they have applied “value in use

calculation” to determine carrying amounts of various intangible assets.

It is further noted that, goodwill is annually tested for impairment (Chalmers, Godfrey

&Webster, 2011, pg. 646). This fact has been sufficiently disclosed in the report so that other

interested parties can understand the information contained in the annual reports better.

They have further indicated that their terms regarding receivables range between 30-60 days.

This has been clearly disclosed.

According to the information in the above table extracted from the books of ALTIUM

LIMITED, goodwill is seen to be rising, for instance goodwill b/d from 2016 is 17280 and there

is goodwill gained as a results of business combination (note 30) of 2,332. this has led to an

increase in goodwill to US $ 19,612 in 2017.It is also noted that there is an increment of US

$7,539 in the course of 2018.This is also as a results of addition from business combination. In

the event that businesses combine, goodwill is revalued to ascertain their carrying amount and in

the case above, it shows that accountants have used their professional judgements to establish

goodwill for business combination in the respective years.

Intellectual property has been impaired from US $ 3,676 in 2016 to US $ 3,299 in 2017.This is

due to amortization value of US $ 394.It increased in value in 2018 due to addition from business

combination of US $ 3403 resulting to a new value of US $ 6,019 in 2018.

PROFESIONAL JUDGEMENT AND IMPAIRMENT 9

Customer relation increased from US $ 12,302 in 2016 to US $ 14,558 in 2017 due to addition

through business combination resulting to an increase in value in 2017.in the course of 2018,

amortization resulted to decrease in the value of customer relation to US $ 13,223. this lead to an

impairment write-down of US $ 1,335.

Software intangible was US $ 2,990 in 2017 and amortization led to decrease in value to US $

2,675 in 2018.This indicate that accountants have used their professional judgement in

determination of this.

HOW PROFESSIONAL JUDGEMENT ON IMPAIRMENTS

ALIGN WITH OBJECTIVES OF GENERAL PURPOSE

FINANCIAL STATETEMENTS

General purpose financial statements are basically prepared to provide information to users of

financial reports who do not have skills and expertise on how to prepare financial statements

(Caramanis &Dedoulis, 2011, pg.240). These users solely rely on the statements that are

prepared by the entity (Donelson, McInnis &Mergenthaler, 2012, pg., 1250). Therefore, the

entity should prepare their financial information in the best way that can be read and understood

by an ordinary person. Relevant disclosures relating to various methods used such as basis of

depreciation and impairments of assets should be adequately disclosed. In the case of ALTIUM

LIMITED, relevant disclosures on impairments of assets have been sufficiently disclosed

including how impairment of goodwill is determined. This will greatly improve the information

required by users of these financial statements (Alexander & Alon, 2017, pg. 270). This shows

how professional judgement relating to impairment align with the objective of general purpose

financial statements.

CONCLUSION.

In conclusion, accountants responsible for the preparation of financial statements of ALTIUM

LIMITED should increase their disclosures regarding basis of provisions of doubtful debts as it

is not very clear on how they have arrived at it.Accountants of ALTIUM limited have used their

professional judgements in the determination of provisions made on accounts receivables and

full disclosure relating to the same has not been made fully so that third parties interested on the

information can make relevant decision based those disclosures. I therefore recommend that

accountants of ALTIUM LIMITED should make full disclosure regarding any method adopted

Customer relation increased from US $ 12,302 in 2016 to US $ 14,558 in 2017 due to addition

through business combination resulting to an increase in value in 2017.in the course of 2018,

amortization resulted to decrease in the value of customer relation to US $ 13,223. this lead to an

impairment write-down of US $ 1,335.

Software intangible was US $ 2,990 in 2017 and amortization led to decrease in value to US $

2,675 in 2018.This indicate that accountants have used their professional judgement in

determination of this.

HOW PROFESSIONAL JUDGEMENT ON IMPAIRMENTS

ALIGN WITH OBJECTIVES OF GENERAL PURPOSE

FINANCIAL STATETEMENTS

General purpose financial statements are basically prepared to provide information to users of

financial reports who do not have skills and expertise on how to prepare financial statements

(Caramanis &Dedoulis, 2011, pg.240). These users solely rely on the statements that are

prepared by the entity (Donelson, McInnis &Mergenthaler, 2012, pg., 1250). Therefore, the

entity should prepare their financial information in the best way that can be read and understood

by an ordinary person. Relevant disclosures relating to various methods used such as basis of

depreciation and impairments of assets should be adequately disclosed. In the case of ALTIUM

LIMITED, relevant disclosures on impairments of assets have been sufficiently disclosed

including how impairment of goodwill is determined. This will greatly improve the information

required by users of these financial statements (Alexander & Alon, 2017, pg. 270). This shows

how professional judgement relating to impairment align with the objective of general purpose

financial statements.

CONCLUSION.

In conclusion, accountants responsible for the preparation of financial statements of ALTIUM

LIMITED should increase their disclosures regarding basis of provisions of doubtful debts as it

is not very clear on how they have arrived at it.Accountants of ALTIUM limited have used their

professional judgements in the determination of provisions made on accounts receivables and

full disclosure relating to the same has not been made fully so that third parties interested on the

information can make relevant decision based those disclosures. I therefore recommend that

accountants of ALTIUM LIMITED should make full disclosure regarding any method adopted

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PROFESIONAL JUDGEMENT AND IMPAIRMENT 10

in determination of any accounting policy and rules such as impairments of intangible assets

(Devalle &Rizzato, 2012, pg.104)

REFERENCES.

Alexander, D. and Alon, A., 2017. Layering of IFRS and dual institutionality of accounting

standards in Belarus. Accounting in Europe, 14(3), pp.261-278.

ALTIUM LIMITED annual report for 30th June

2018<https://www.altium.com/resources/investor-announcement/2018_annual_report-

2018_final.pdf>

Caramanis, C. and Dedoulis, E., 2011. Accounting and Auditing Practices. In Business and

management practices in Greece (pp. 236-255). Palgrave Macmillan, London.

Chalmers, K.G., Godfrey, J.M. and Webster, J.C., 2011. Does a goodwill impairment regime

better reflect the underlying economic attributes of goodwill? Accounting & Finance, 51(3),

pp.634-660.

Devalle, A. and Rizzato, F., 2012. The quality of mandatory disclosure: the impairment of

goodwill. An empirical analysis of European listed companies. Procedia Economics and

Finance, 2, pp.101-108.

Donelson, D.C., McInnis, J.M. and Mergenthaler, R.D., 2012. Rules-based accounting standards

and litigation. The Accounting Review, 87(4), pp.1247-1279.

Jackling, B., Howieson, B. and Natoli, R., 2012. Some implications of IFRS adoption for

accounting education. Australian Accounting Review, 22(4), pp.331-340.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries: implications

for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Nguyen, L., Hooper, K. and Sinclair, R., 2013. Conservatism versus change in the Vietnamese

accounting field. Corporate Ownership & Control, 11(1), pp.471-482.

Ramanna, K. and Watts, R.L., 2012. Evidence on the use of unverifiable estimates in required

goodwill impairment. Review of Accounting Studies, 17(4), pp.749-780.

in determination of any accounting policy and rules such as impairments of intangible assets

(Devalle &Rizzato, 2012, pg.104)

REFERENCES.

Alexander, D. and Alon, A., 2017. Layering of IFRS and dual institutionality of accounting

standards in Belarus. Accounting in Europe, 14(3), pp.261-278.

ALTIUM LIMITED annual report for 30th June

2018<https://www.altium.com/resources/investor-announcement/2018_annual_report-

2018_final.pdf>

Caramanis, C. and Dedoulis, E., 2011. Accounting and Auditing Practices. In Business and

management practices in Greece (pp. 236-255). Palgrave Macmillan, London.

Chalmers, K.G., Godfrey, J.M. and Webster, J.C., 2011. Does a goodwill impairment regime

better reflect the underlying economic attributes of goodwill? Accounting & Finance, 51(3),

pp.634-660.

Devalle, A. and Rizzato, F., 2012. The quality of mandatory disclosure: the impairment of

goodwill. An empirical analysis of European listed companies. Procedia Economics and

Finance, 2, pp.101-108.

Donelson, D.C., McInnis, J.M. and Mergenthaler, R.D., 2012. Rules-based accounting standards

and litigation. The Accounting Review, 87(4), pp.1247-1279.

Jackling, B., Howieson, B. and Natoli, R., 2012. Some implications of IFRS adoption for

accounting education. Australian Accounting Review, 22(4), pp.331-340.

Linnenluecke, M.K., Birt, J., Lyon, J. and Sidhu, B.K., 2015. Planetary boundaries: implications

for asset impairment. Accounting & Finance, 55(4), pp.911-929.

Nguyen, L., Hooper, K. and Sinclair, R., 2013. Conservatism versus change in the Vietnamese

accounting field. Corporate Ownership & Control, 11(1), pp.471-482.

Ramanna, K. and Watts, R.L., 2012. Evidence on the use of unverifiable estimates in required

goodwill impairment. Review of Accounting Studies, 17(4), pp.749-780.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PROFESIONAL JUDGEMENT AND IMPAIRMENT 11

Stefan-Duicu, V.M., 2015. The Accountant Professional as a Current User of Professional

Judgment. Challenges of the Knowledge Society, p.713.

Trotman, K.T., Tan, H.C. and Ang, N., 2011. Fifty‐year overview of judgment and decision‐

making research in accounting. Accounting & Finance, 51(1), pp.278-360.

Xu, W., Anandarajan, A. and Curatola, A., 2011. The value relevance of goodwill

impairment. Research in Accounting Regulation, 23(2), pp.145-148.

Stefan-Duicu, V.M., 2015. The Accountant Professional as a Current User of Professional

Judgment. Challenges of the Knowledge Society, p.713.

Trotman, K.T., Tan, H.C. and Ang, N., 2011. Fifty‐year overview of judgment and decision‐

making research in accounting. Accounting & Finance, 51(1), pp.278-360.

Xu, W., Anandarajan, A. and Curatola, A., 2011. The value relevance of goodwill

impairment. Research in Accounting Regulation, 23(2), pp.145-148.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.