Professional Practice Taxation Exam: UOW, Income Tax & GST

VerifiedAdded on 2023/06/18

|8

|717

|377

Homework Assignment

AI Summary

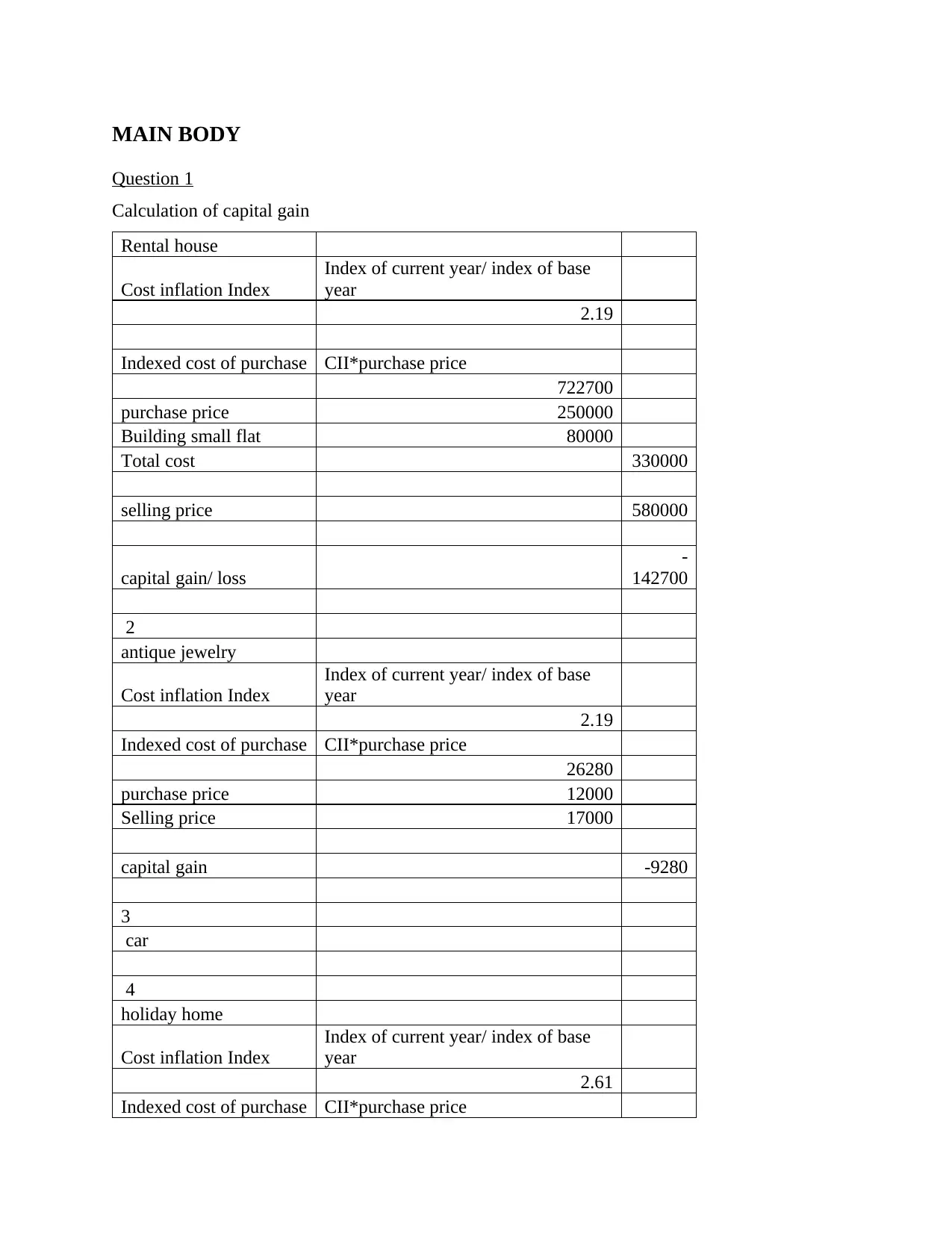

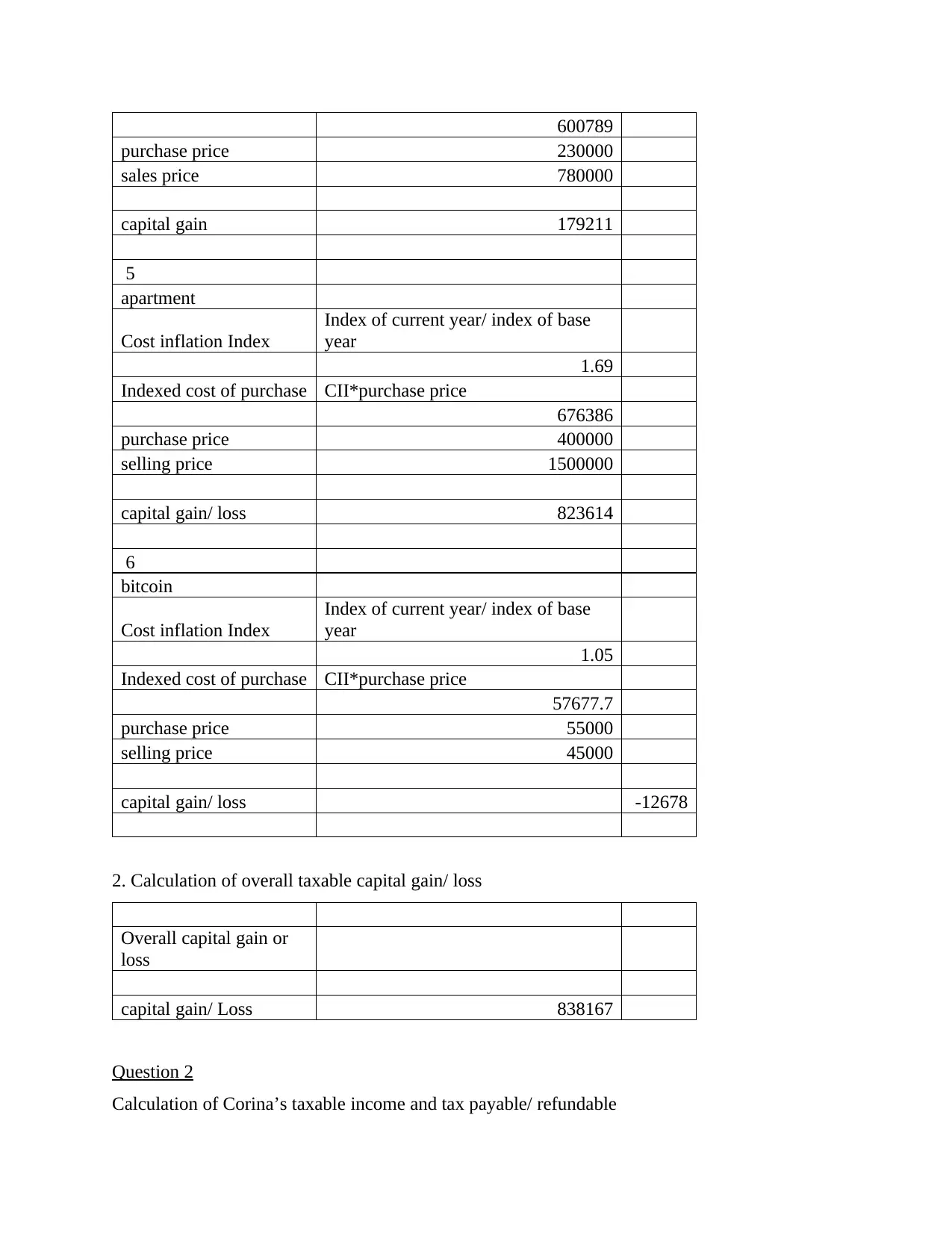

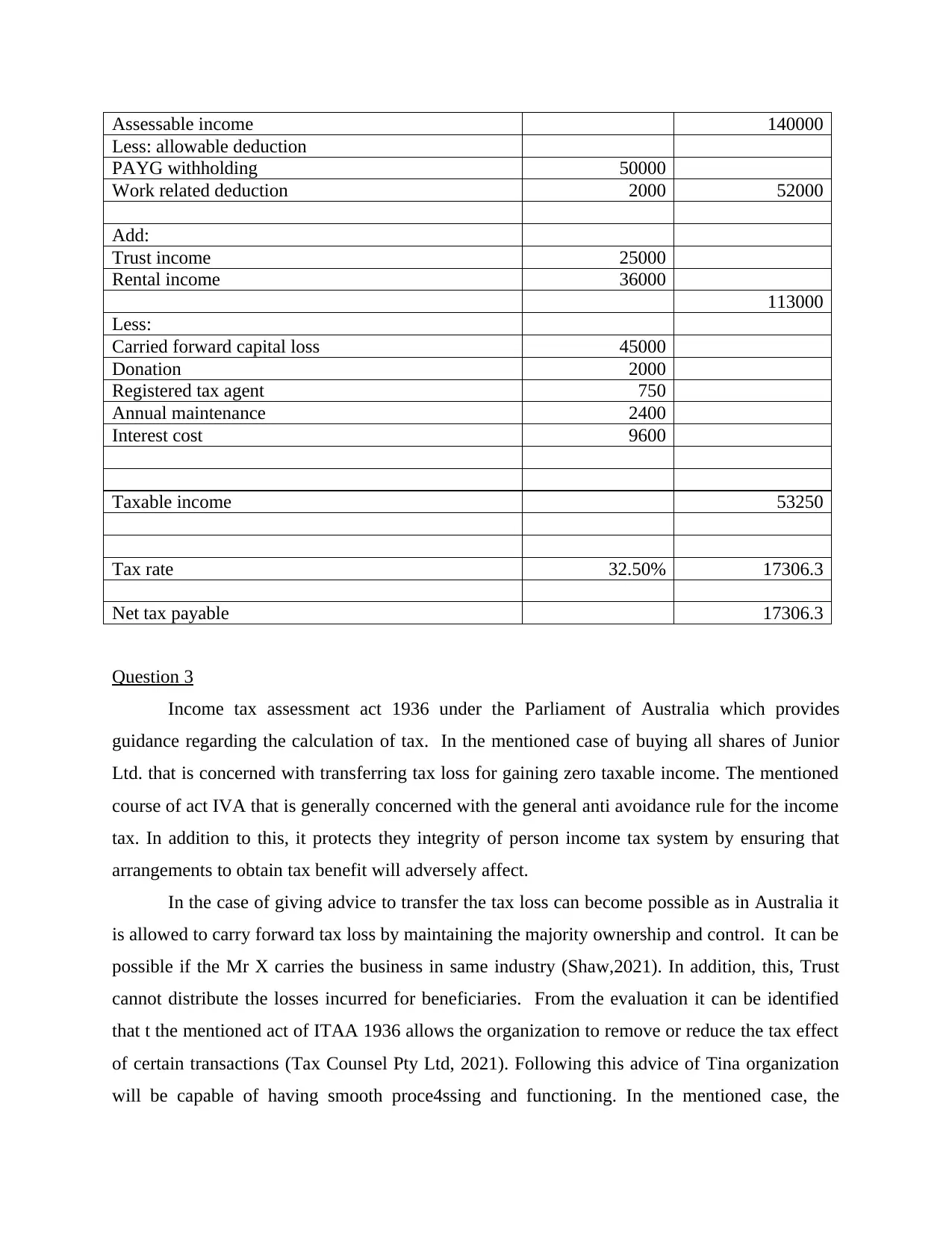

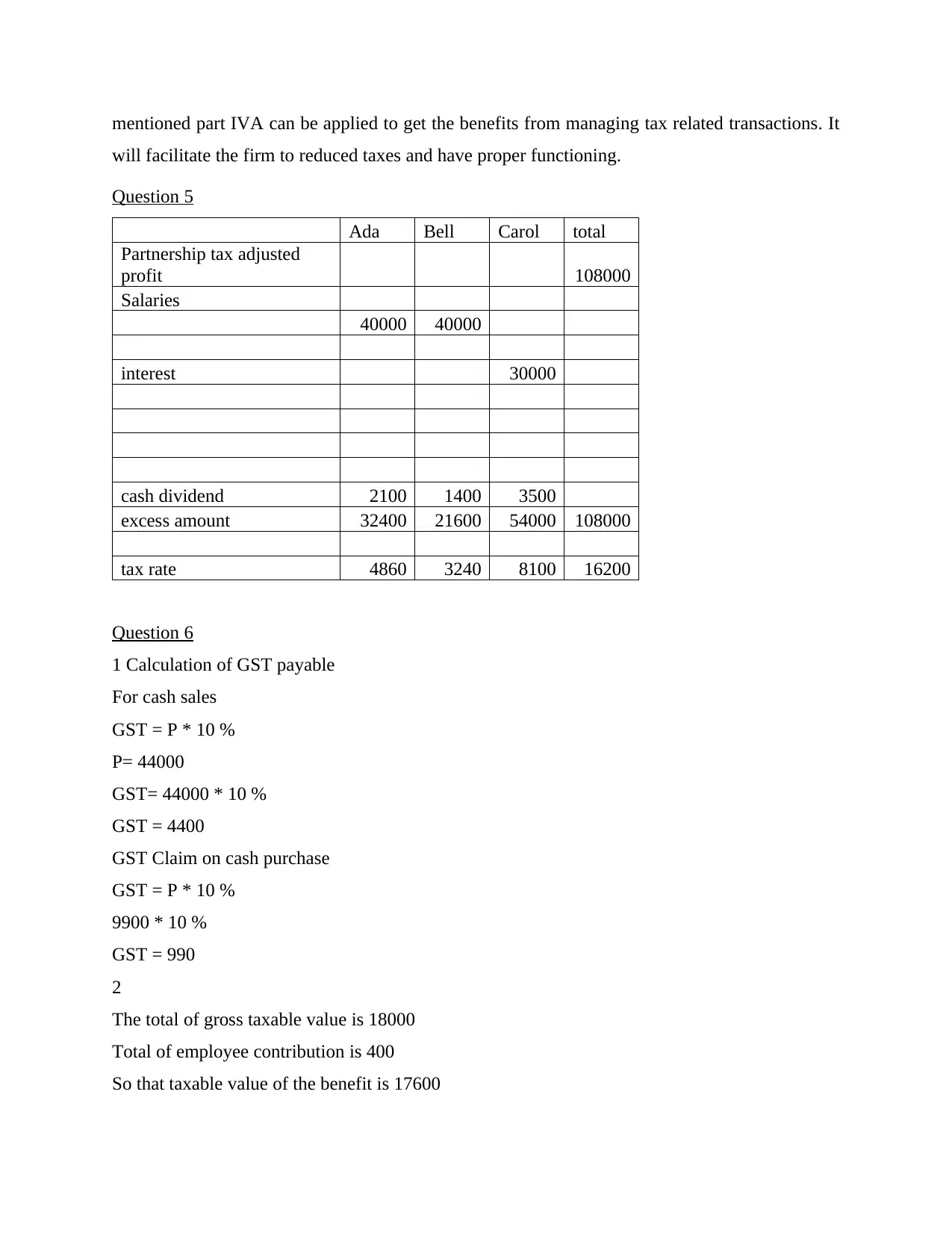

This document provides solutions to a professional practice taxation exam, covering various aspects of income tax assessment, capital gains, and GST calculations. It includes calculations for capital gains on rental properties, antique jewelry, holiday homes, apartments, and Bitcoin, as well as the calculation of overall taxable capital gain/loss. The document further details Corina’s taxable income and tax payable, referencing the Income Tax Assessment Act 1936 and its implications on tax loss transfers. Additionally, it addresses partnership tax adjusted profit and GST payable on cash sales and purchases. Desklib offers a wide range of past papers and solved assignments to support students in their studies.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.