Professional Practice Taxation 6: Assignment Solution Analysis

VerifiedAdded on 2020/03/16

|9

|1393

|47

Homework Assignment

AI Summary

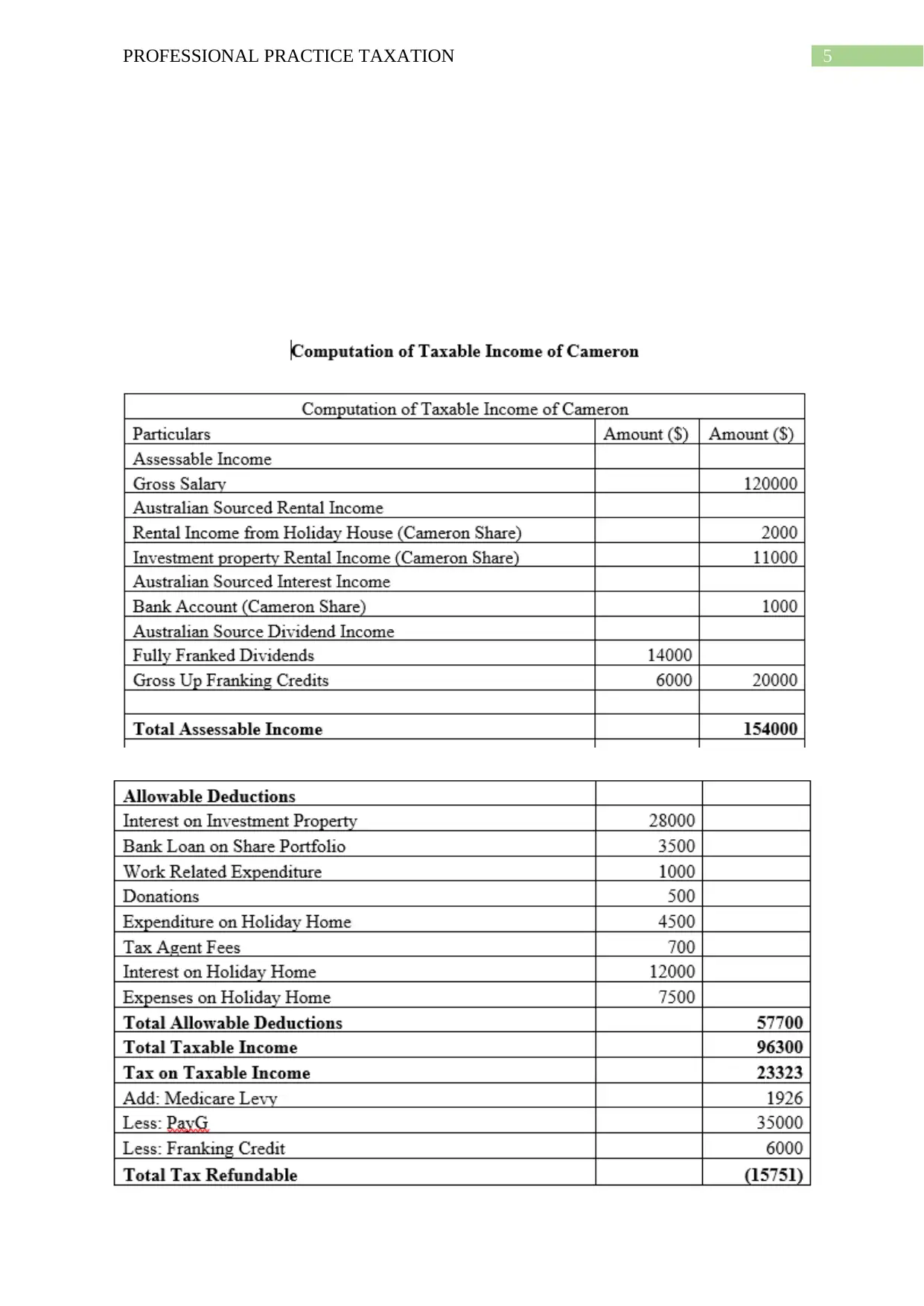

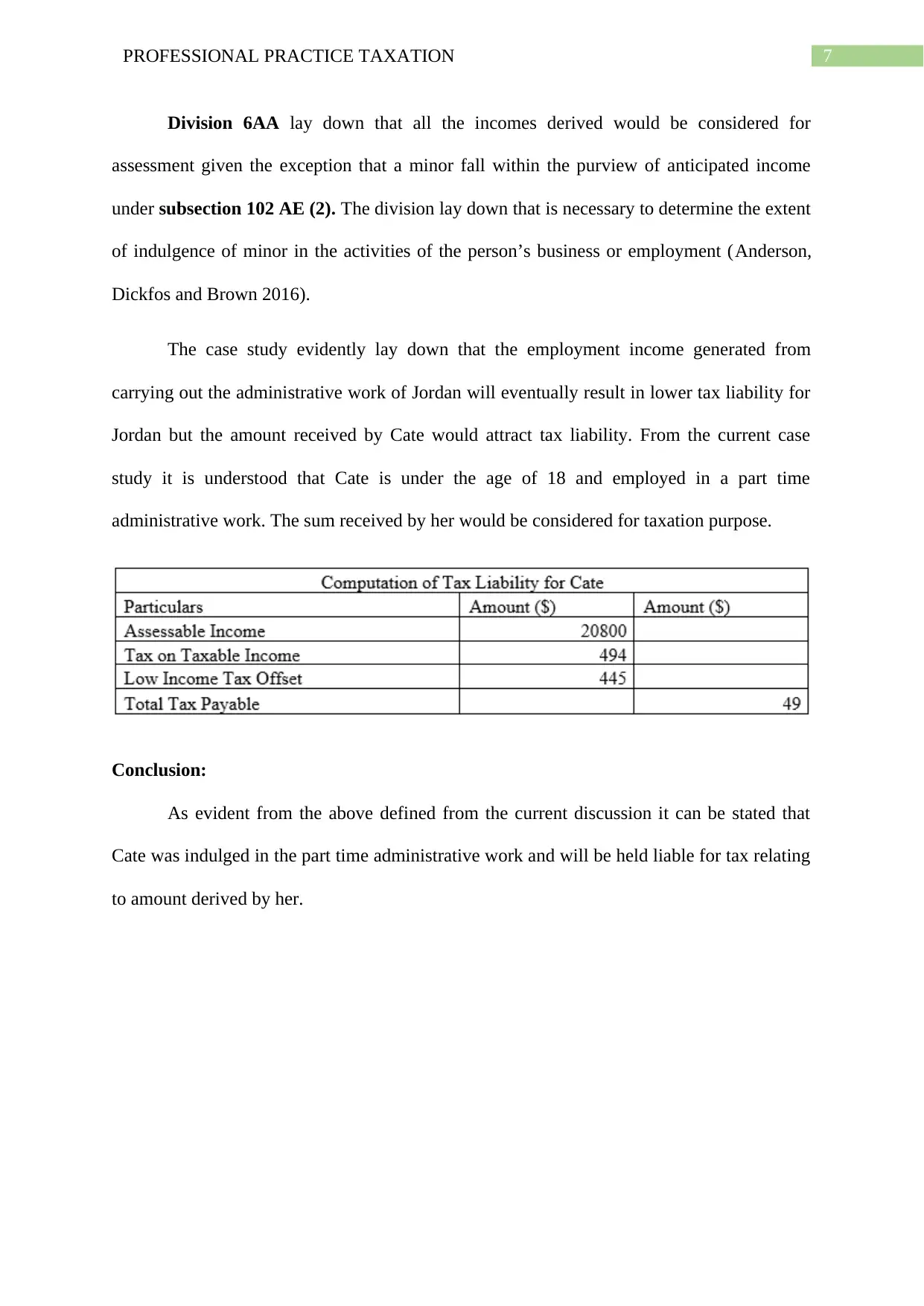

This document presents a comprehensive solution to a professional practice taxation assignment, addressing the calculation of net tax payable for individuals and analyzing the tax implications of various financial transactions. The assignment delves into issues such as the deductibility of travel expenses, superannuation contributions, child care expenses, and private living expenses, referencing relevant legislation, including the ITAA 1997, and case law, such as TR 95/9, FC of T v Hayley (1958), and TD 92/154. The solution also examines the tax liability of a minor employed for part-time administrative work, considering relevant taxation rulings and divisions of the ITAA. The analysis covers the determination of assessable income, allowable deductions, and the application of tax rules to specific scenarios, providing a detailed breakdown of the tax implications for both individuals and businesses. The assignment emphasizes the importance of understanding tax regulations and their practical application in real-world financial situations.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.