Analyzing Profitability: Management Accounting Assignment Solution

VerifiedAdded on 2023/06/03

|5

|635

|173

Homework Assignment

AI Summary

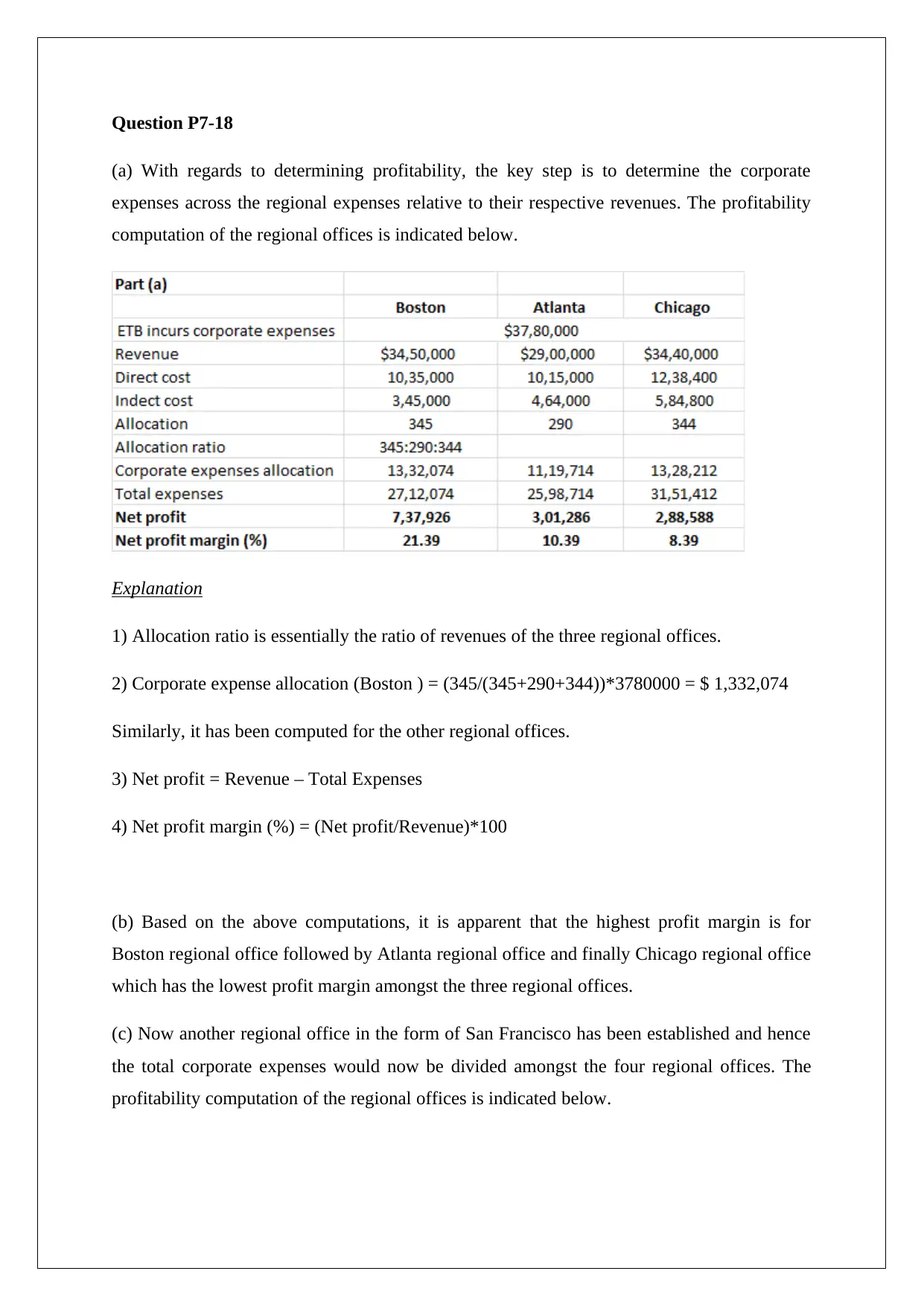

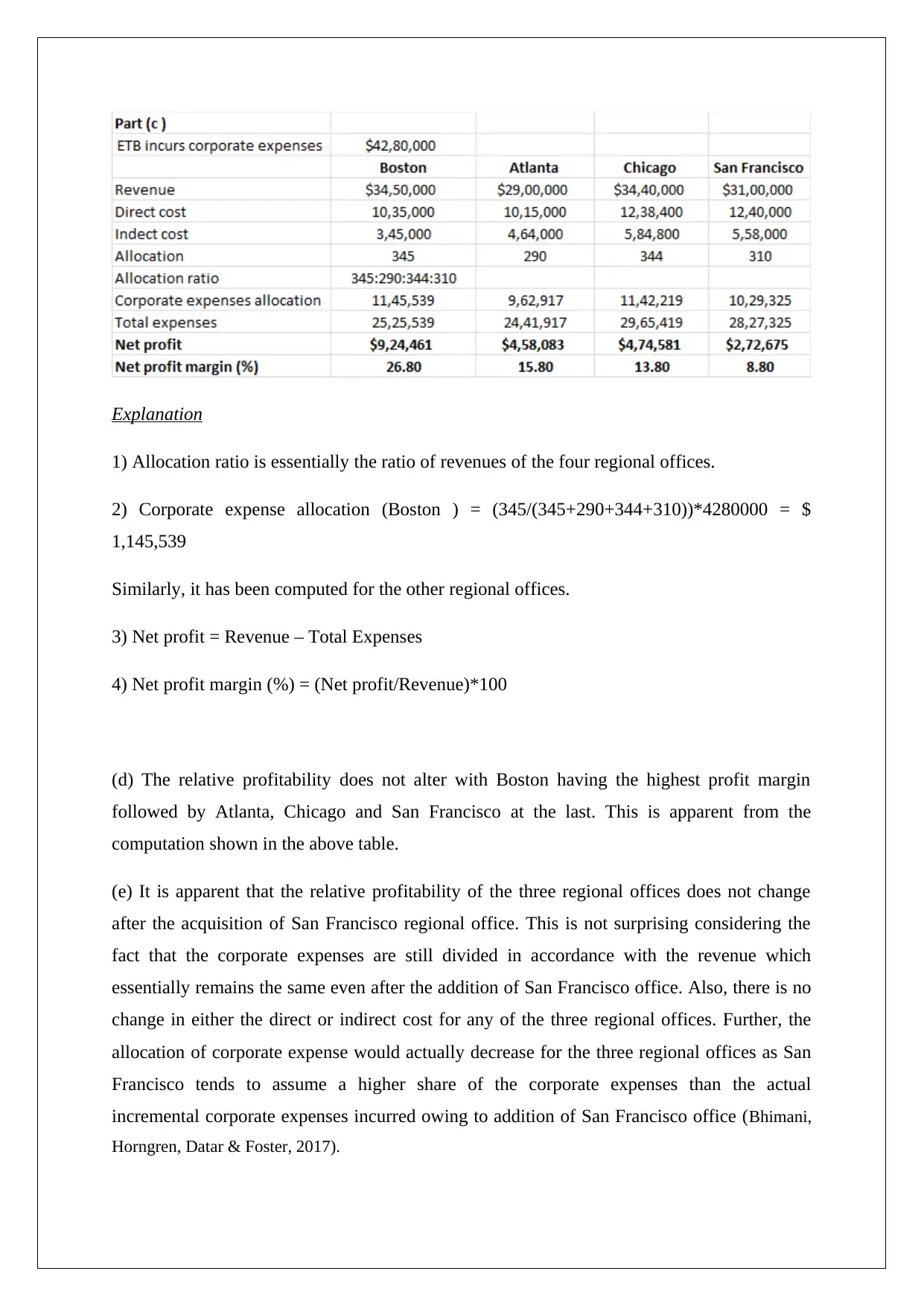

This assignment solution addresses a management accounting problem concerning the profitability analysis of regional offices. It begins by calculating the profitability of existing regional offices based on revenue and allocated corporate expenses, using a revenue-based allocation method. The solution then introduces a new regional office and recalculates profitability, demonstrating how the allocation of corporate expenses changes. The analysis highlights the potential inaccuracies of the current cost allocation method, showing how the allocation can misrepresent the profitability of individual offices. The solution also provides a detailed breakdown of the calculations, including the allocation ratios and net profit margins. Finally, it offers references from various accounting textbooks and resources to support the analysis and findings, emphasizing the importance of accurate cost allocation in determining profitability and making informed business decisions. This assignment highlights the critical role of financial analysis in assessing the performance of different business units and making strategic decisions.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.