Cost Accounting Report: Proposal Profit Analysis, BEP

VerifiedAdded on 2020/10/22

|11

|2568

|275

Report

AI Summary

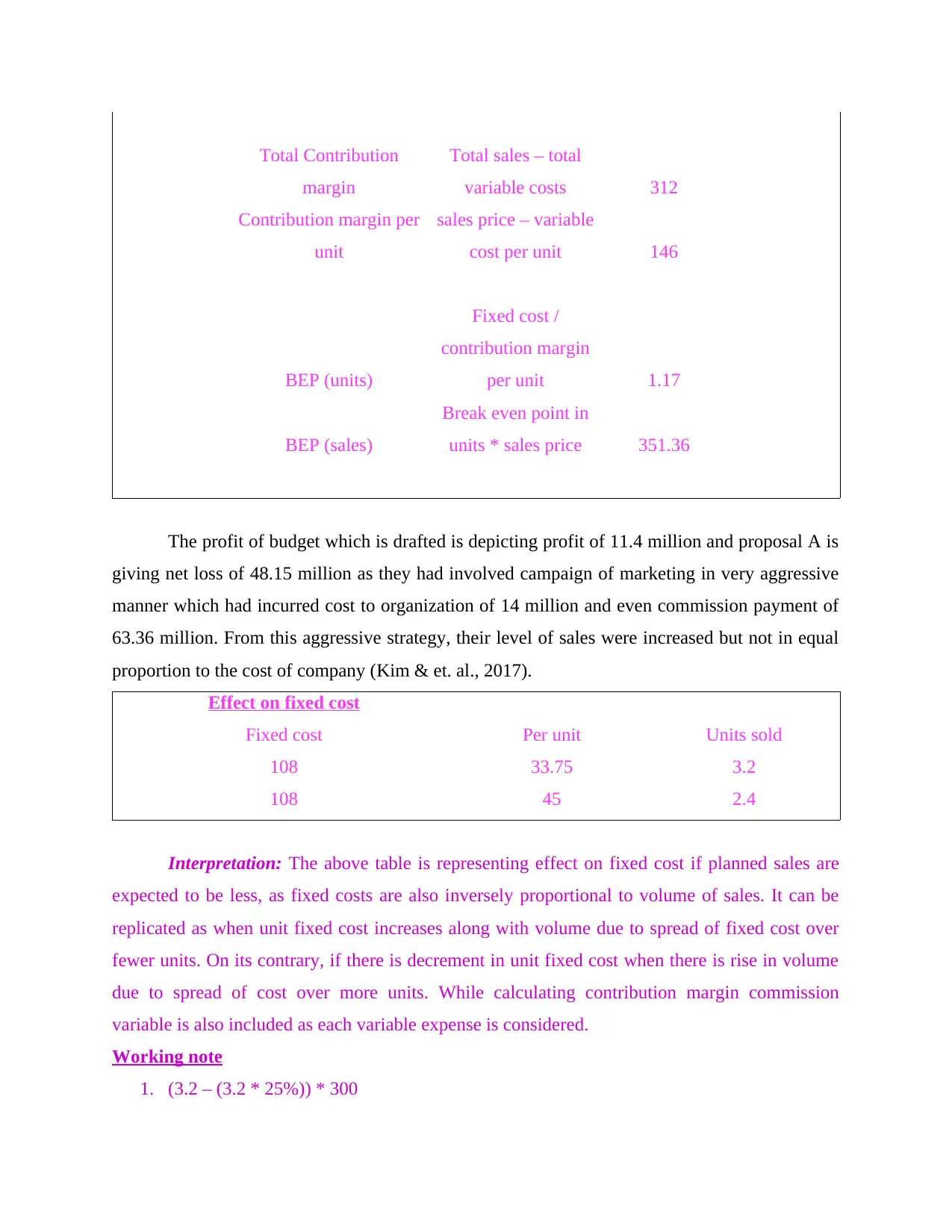

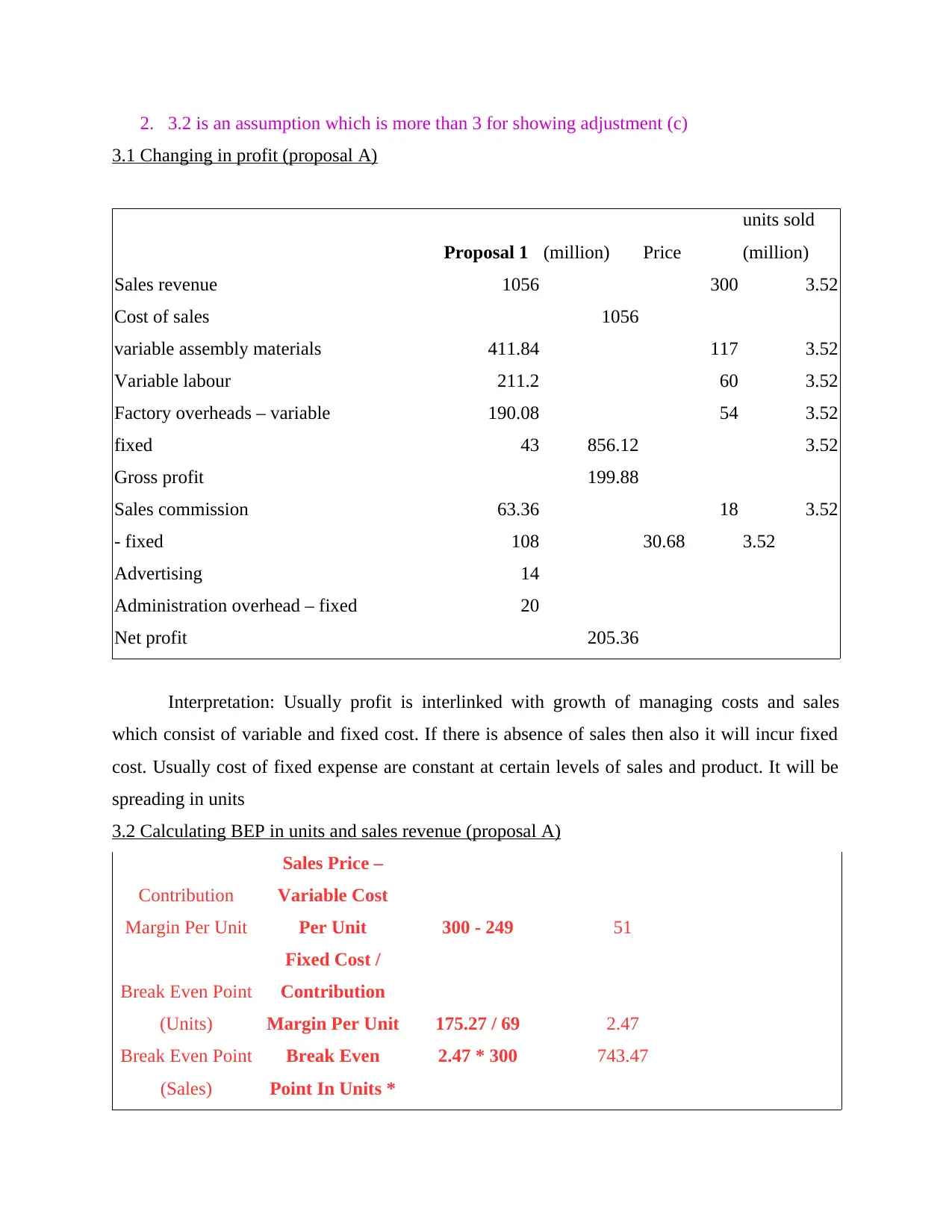

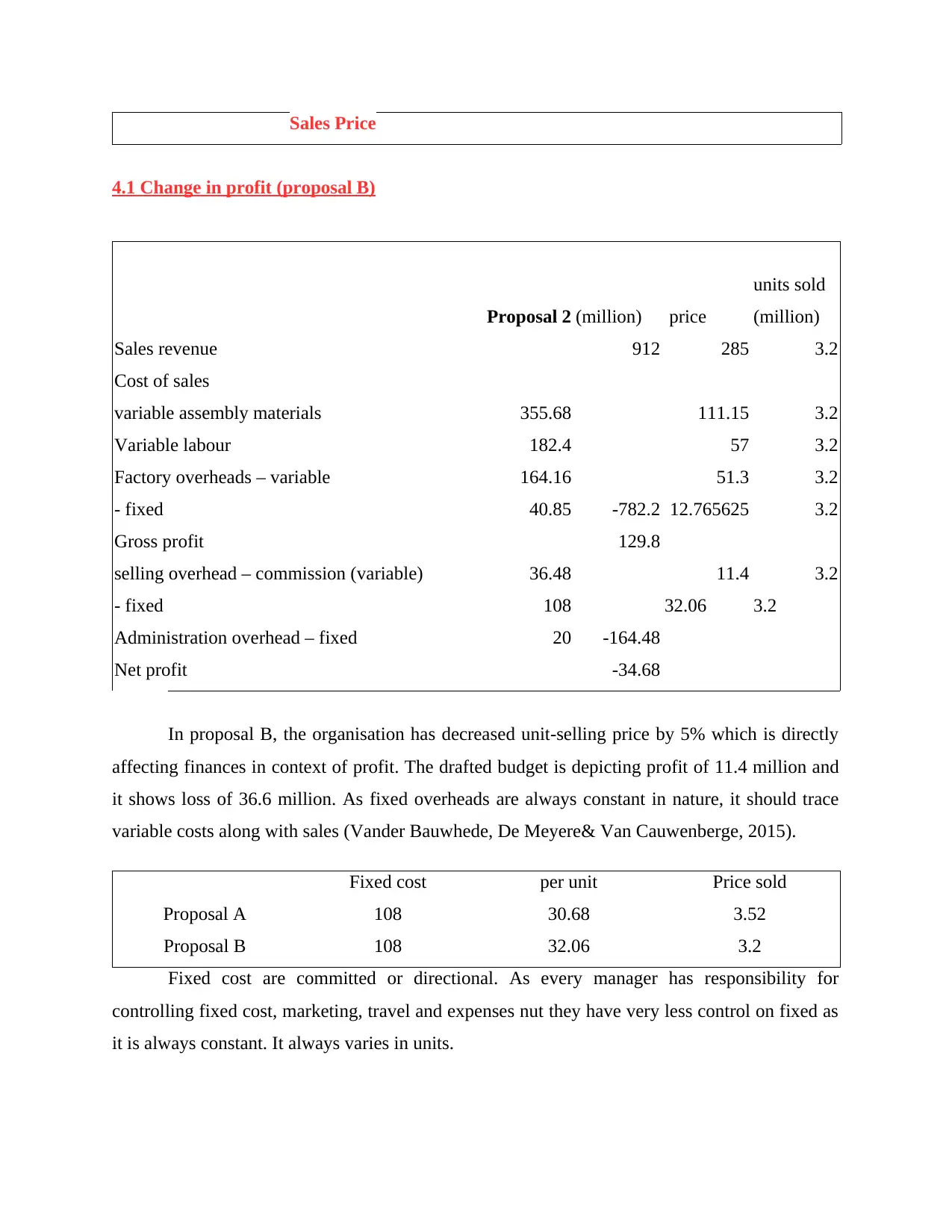

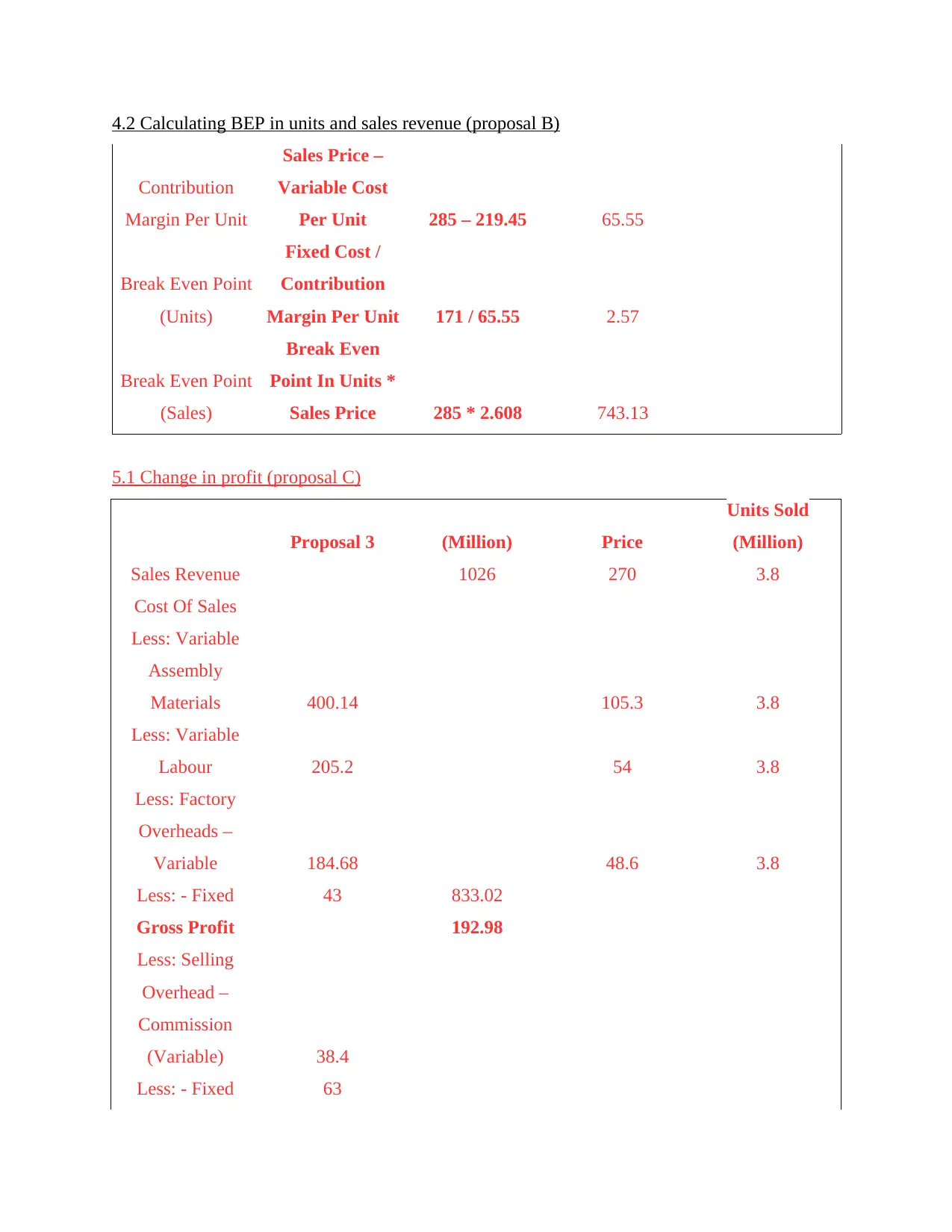

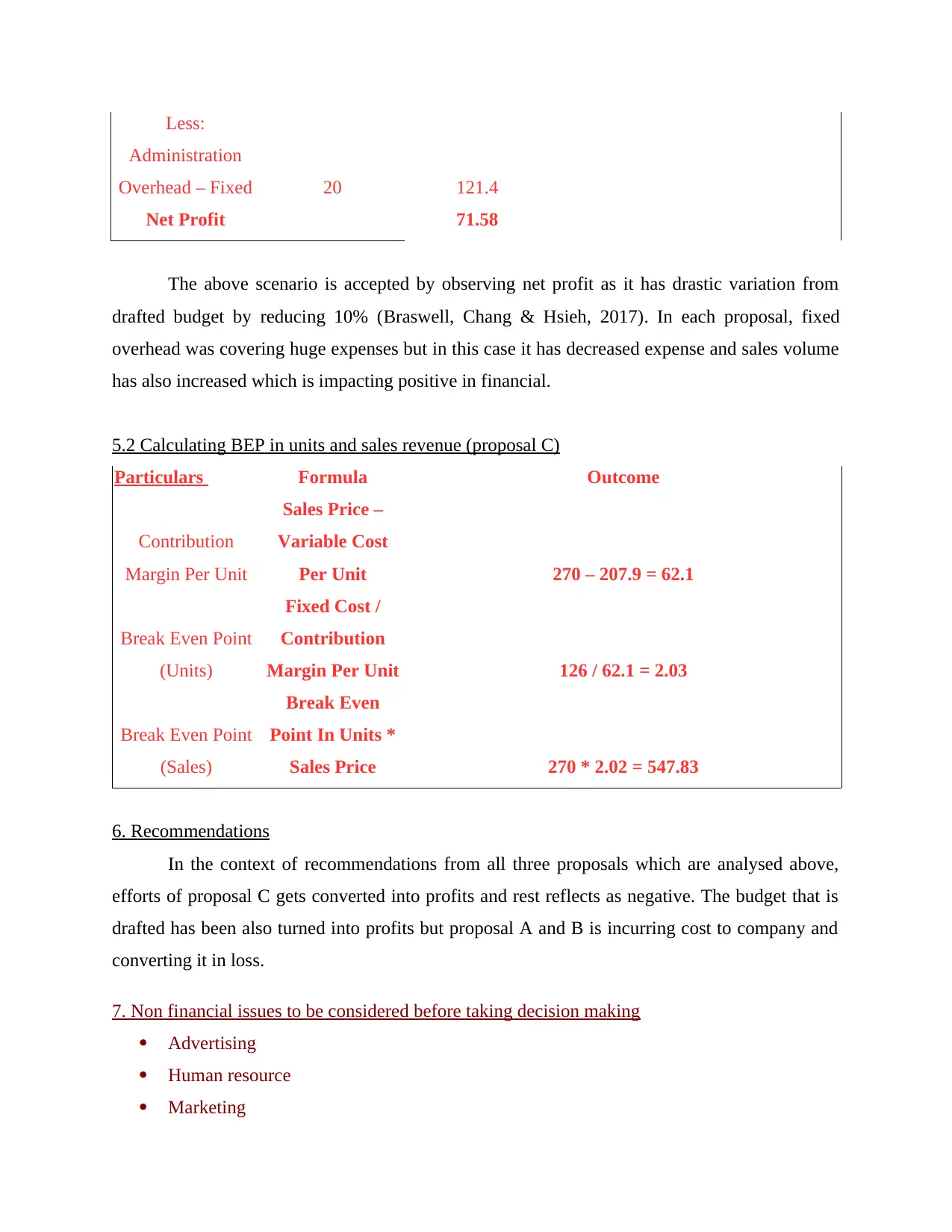

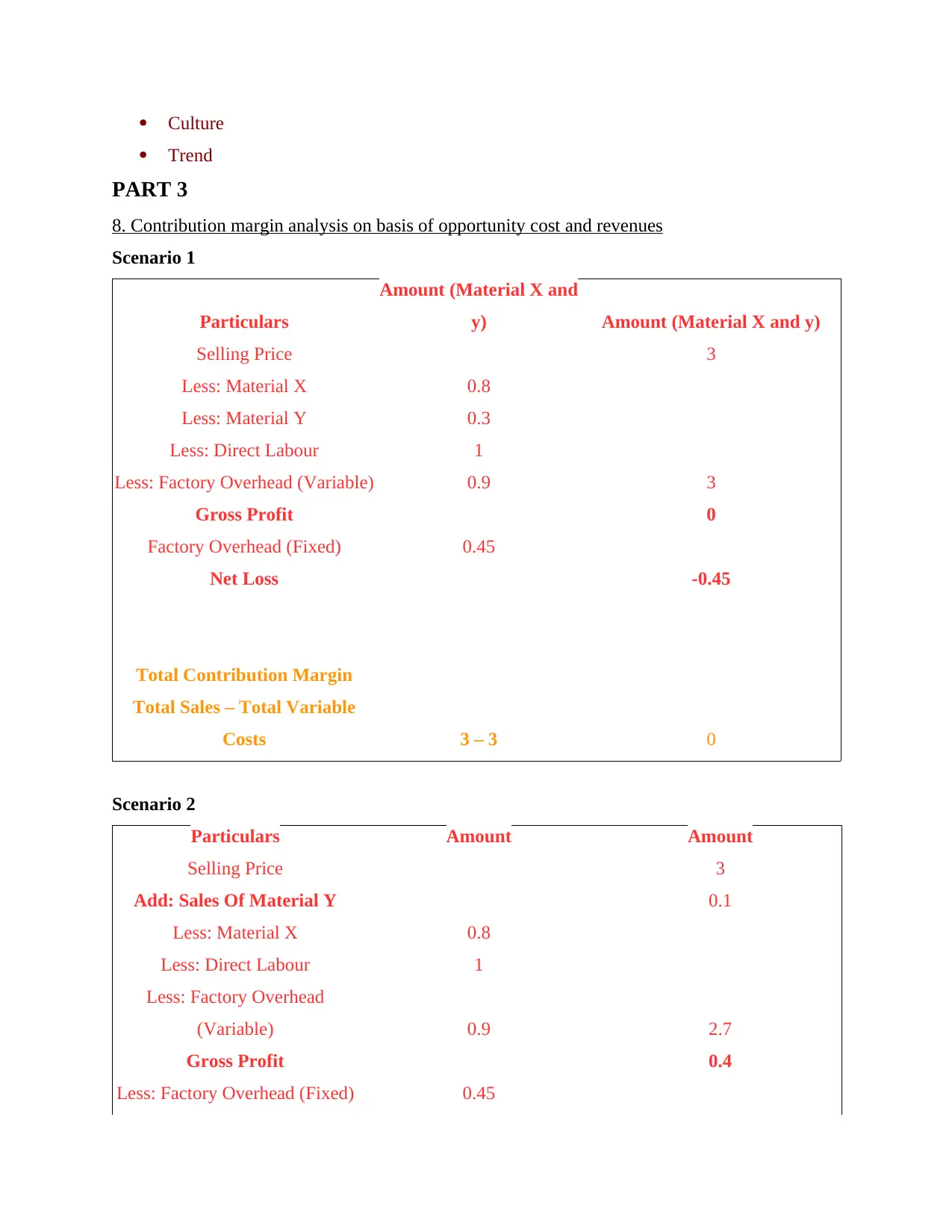

This cost accounting report presents a comprehensive analysis of three proposals (A, B, and C) along with a base budget, evaluating their impact on profitability and break-even points (BEP). The report meticulously calculates changes in profit, BEP in units, and sales revenue for each proposal. It examines the effects of fixed and variable costs, contribution margins, and the influence of factors like sales commissions and advertising. The analysis includes detailed interpretations of financial data, working notes, and a contribution margin analysis based on opportunity cost and revenues. The report concludes with recommendations, highlighting Proposal C as the most profitable, and considers non-financial issues like advertising, human resources, and marketing. It provides a deep dive into financial decision-making, considering fixed costs and their impact on profit margins, and provides a detailed look at how changes in sales prices and costs affect the overall financial performance, offering a practical guide to cost accounting principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.