Justifying Capital Investment: Project A or B? A Financial Analysis

VerifiedAdded on 2020/06/04

|13

|3552

|155

Report

AI Summary

This report presents a capital budgeting analysis comparing two mutually exclusive projects, Project A and Project B, for Tissue Co. The analysis employs various investment appraisal techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), payback period, and Accounting Rate of Return (ARR), to determine the more financially viable project. The report includes profit and loss statements, cash flow statements, and calculations for each method. The discounting rate is calculated, and a detailed evaluation of each project is provided, leading to a recommendation for Tissue Co. to invest in Project A due to its higher NPV, IRR, and profitability index, despite the quicker payback period of Project A. The report highlights the importance of capital budgeting techniques in making informed investment decisions, considering the time value of money and the risks associated with each project.

Justify and validate whether or not to

proceed with one of two mutually exclusive

projects (Project A or Project B)

proceed with one of two mutually exclusive

projects (Project A or Project B)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................1

Business and project overview.....................................................................................................1

P&L statement and cash flow statement......................................................................................2

Discounting rate...........................................................................................................................3

Capital budgeting analysis...........................................................................................................4

CONCLUSION................................................................................................................................9

LIST OF REFERNCES.................................................................................................................10

INDEX OF TABLES

Table 1 Profit and loss statement of Project A...............................................................................2

Table 2Profit and loss statement of Project B................................................................................2

Table 3 Cash flow statement for Project A....................................................................................2

Table 4Cash flow statement for Project B.....................................................................................3

Table 5 Calculation of net present value for project A...................................................................5

Table 6 Calculation of net present value for project B...................................................................5

Table 7 Calulation of payback period for project A.......................................................................6

Table 8 Calulation of payback period for project B.......................................................................6

Table 9 Calculation of internal rate of return for project A............................................................6

Table 10 Calculation of internal rate of return for project for project B........................................7

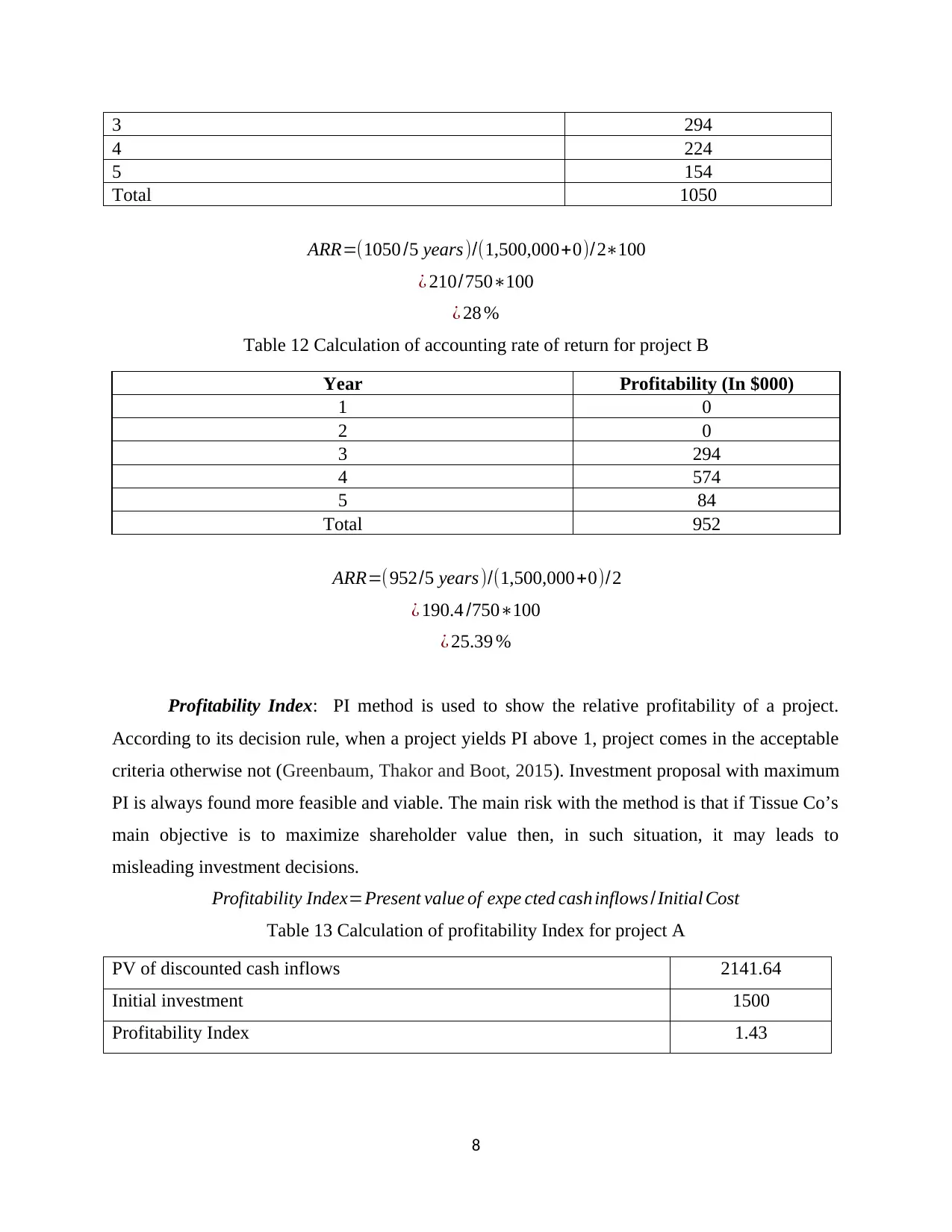

Table 11 Calculation of accounting rate of return for project A....................................................7

Table 12 Calculation of accounting rate of return for project B.....................................................8

Table 13 Calculation of profitability Index for project A...............................................................8

Table 14 Calculation of profitability Index for project B...............................................................8

EXECUTIVE SUMMARY.............................................................................................................1

Business and project overview.....................................................................................................1

P&L statement and cash flow statement......................................................................................2

Discounting rate...........................................................................................................................3

Capital budgeting analysis...........................................................................................................4

CONCLUSION................................................................................................................................9

LIST OF REFERNCES.................................................................................................................10

INDEX OF TABLES

Table 1 Profit and loss statement of Project A...............................................................................2

Table 2Profit and loss statement of Project B................................................................................2

Table 3 Cash flow statement for Project A....................................................................................2

Table 4Cash flow statement for Project B.....................................................................................3

Table 5 Calculation of net present value for project A...................................................................5

Table 6 Calculation of net present value for project B...................................................................5

Table 7 Calulation of payback period for project A.......................................................................6

Table 8 Calulation of payback period for project B.......................................................................6

Table 9 Calculation of internal rate of return for project A............................................................6

Table 10 Calculation of internal rate of return for project for project B........................................7

Table 11 Calculation of accounting rate of return for project A....................................................7

Table 12 Calculation of accounting rate of return for project B.....................................................8

Table 13 Calculation of profitability Index for project A...............................................................8

Table 14 Calculation of profitability Index for project B...............................................................8

EXECUTIVE SUMMARY

In business world, many-times, firm need to incur capital expenditures to purchase new

machinery, property, plant, acquire new technology, expansion projects and other. All of such

projects need huge capital; therefore, rational decisions needs to be made, otherwise,

inappropriate decisions may bring business into significant trouble. Capital budgeting also called

investment appraisal methods are used by companies to judge how well various projects seems

viable and justifiable for the enterprise and found acceptable (Baum and Crosby, 2014). Tissue

Co. is a private firm that gained success in the market by producing & selling toilet paper from

past 10 year. Currently, it is looking to add a new product to its existing offerings but firm has

limited capital. Therefore, out of two project proposals, A & B, business can only put money in

one of these which seems more worthy. Thus, the aim of the report is to apply investment

appraisal techniques like ARR, payback, internal rate of return and Net present value to choose

the best one. After applying the necessary capital budgeting techniques, project A found worthy

due to greater NPV, IRR above the cost of capital and higher profitability Index. Despite this,

payback period method discovers quick recovery of initial investment in project A. Hence, it is

better to recommend Tissue Co. to undertake investment in project A.

Business and project overview

Company has two proposals available presented by Manager A and Manager B. Project A

is about launching just a fragranced toilet paper and current procedure followed by Tissue Co. is

already well arranged to produce such paper with the exception of slightly modifications and a

new machine to add fragrance. In order to purchase new machinery, entity will need to arrange

funds worth $1.5 million which has no resale value and will be completely scrap after 5 year.

However, project B is about launching a new kind of paper that is thicker and have a soft

surface but will be disposed easily when it soaked in water. Thus, both the projects are different

from each other, as in first, Tissue Co. just need to purchase a new machine whereas in later, it

will also need to carry out research & development which costs $0.5 million to determine that

which kind of paper is in great demand in the market. However, new machine purchase will

incur cost of $1 million. However, on the other side, fragranced toilet paper already exists in

heavy demand. Despite this, manager B also believed that on such project, firm will also incur

1

In business world, many-times, firm need to incur capital expenditures to purchase new

machinery, property, plant, acquire new technology, expansion projects and other. All of such

projects need huge capital; therefore, rational decisions needs to be made, otherwise,

inappropriate decisions may bring business into significant trouble. Capital budgeting also called

investment appraisal methods are used by companies to judge how well various projects seems

viable and justifiable for the enterprise and found acceptable (Baum and Crosby, 2014). Tissue

Co. is a private firm that gained success in the market by producing & selling toilet paper from

past 10 year. Currently, it is looking to add a new product to its existing offerings but firm has

limited capital. Therefore, out of two project proposals, A & B, business can only put money in

one of these which seems more worthy. Thus, the aim of the report is to apply investment

appraisal techniques like ARR, payback, internal rate of return and Net present value to choose

the best one. After applying the necessary capital budgeting techniques, project A found worthy

due to greater NPV, IRR above the cost of capital and higher profitability Index. Despite this,

payback period method discovers quick recovery of initial investment in project A. Hence, it is

better to recommend Tissue Co. to undertake investment in project A.

Business and project overview

Company has two proposals available presented by Manager A and Manager B. Project A

is about launching just a fragranced toilet paper and current procedure followed by Tissue Co. is

already well arranged to produce such paper with the exception of slightly modifications and a

new machine to add fragrance. In order to purchase new machinery, entity will need to arrange

funds worth $1.5 million which has no resale value and will be completely scrap after 5 year.

However, project B is about launching a new kind of paper that is thicker and have a soft

surface but will be disposed easily when it soaked in water. Thus, both the projects are different

from each other, as in first, Tissue Co. just need to purchase a new machine whereas in later, it

will also need to carry out research & development which costs $0.5 million to determine that

which kind of paper is in great demand in the market. However, new machine purchase will

incur cost of $1 million. However, on the other side, fragranced toilet paper already exists in

heavy demand. Despite this, manager B also believed that on such project, firm will also incur

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

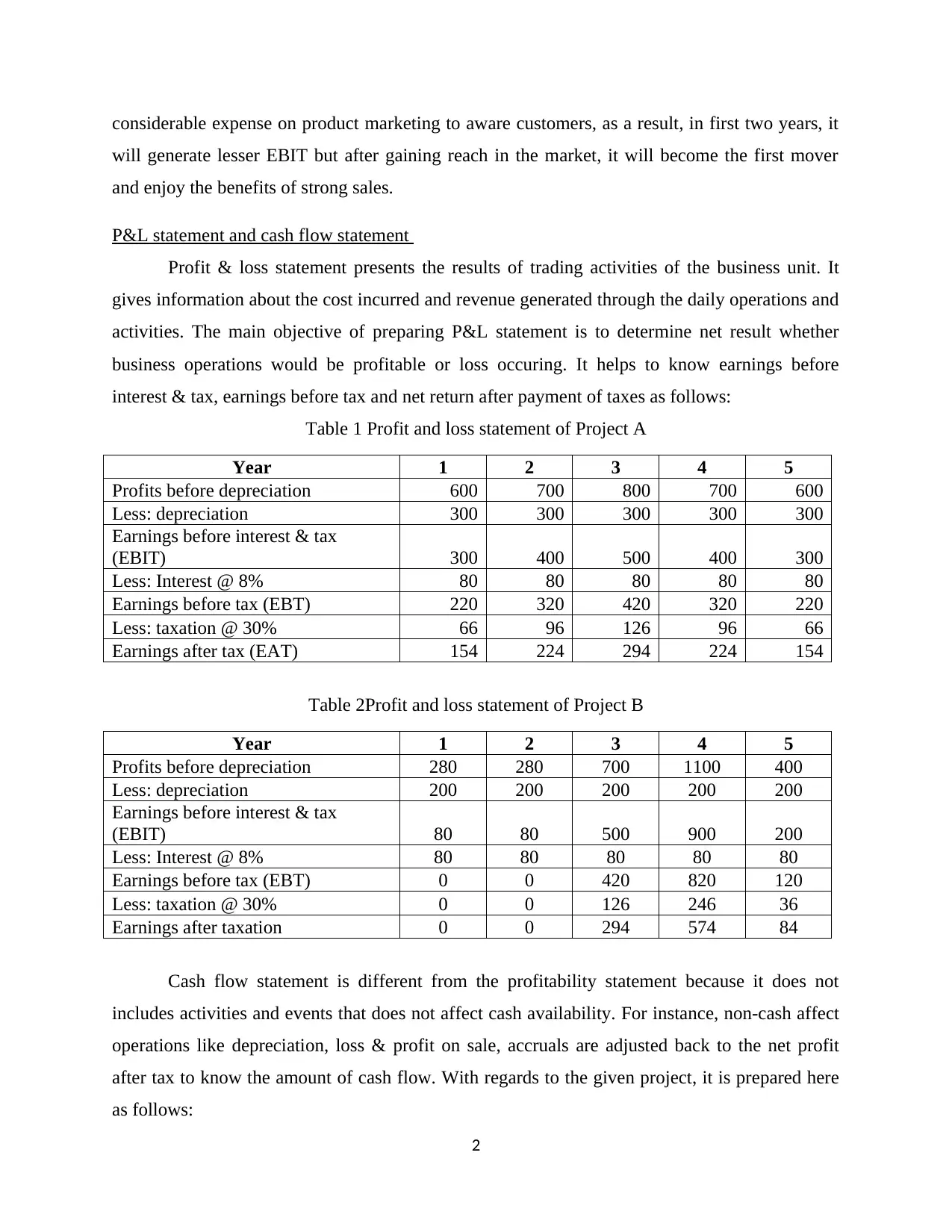

considerable expense on product marketing to aware customers, as a result, in first two years, it

will generate lesser EBIT but after gaining reach in the market, it will become the first mover

and enjoy the benefits of strong sales.

P&L statement and cash flow statement

Profit & loss statement presents the results of trading activities of the business unit. It

gives information about the cost incurred and revenue generated through the daily operations and

activities. The main objective of preparing P&L statement is to determine net result whether

business operations would be profitable or loss occuring. It helps to know earnings before

interest & tax, earnings before tax and net return after payment of taxes as follows:

Table 1 Profit and loss statement of Project A

Year 1 2 3 4 5

Profits before depreciation 600 700 800 700 600

Less: depreciation 300 300 300 300 300

Earnings before interest & tax

(EBIT) 300 400 500 400 300

Less: Interest @ 8% 80 80 80 80 80

Earnings before tax (EBT) 220 320 420 320 220

Less: taxation @ 30% 66 96 126 96 66

Earnings after tax (EAT) 154 224 294 224 154

Table 2Profit and loss statement of Project B

Year 1 2 3 4 5

Profits before depreciation 280 280 700 1100 400

Less: depreciation 200 200 200 200 200

Earnings before interest & tax

(EBIT) 80 80 500 900 200

Less: Interest @ 8% 80 80 80 80 80

Earnings before tax (EBT) 0 0 420 820 120

Less: taxation @ 30% 0 0 126 246 36

Earnings after taxation 0 0 294 574 84

Cash flow statement is different from the profitability statement because it does not

includes activities and events that does not affect cash availability. For instance, non-cash affect

operations like depreciation, loss & profit on sale, accruals are adjusted back to the net profit

after tax to know the amount of cash flow. With regards to the given project, it is prepared here

as follows:

2

will generate lesser EBIT but after gaining reach in the market, it will become the first mover

and enjoy the benefits of strong sales.

P&L statement and cash flow statement

Profit & loss statement presents the results of trading activities of the business unit. It

gives information about the cost incurred and revenue generated through the daily operations and

activities. The main objective of preparing P&L statement is to determine net result whether

business operations would be profitable or loss occuring. It helps to know earnings before

interest & tax, earnings before tax and net return after payment of taxes as follows:

Table 1 Profit and loss statement of Project A

Year 1 2 3 4 5

Profits before depreciation 600 700 800 700 600

Less: depreciation 300 300 300 300 300

Earnings before interest & tax

(EBIT) 300 400 500 400 300

Less: Interest @ 8% 80 80 80 80 80

Earnings before tax (EBT) 220 320 420 320 220

Less: taxation @ 30% 66 96 126 96 66

Earnings after tax (EAT) 154 224 294 224 154

Table 2Profit and loss statement of Project B

Year 1 2 3 4 5

Profits before depreciation 280 280 700 1100 400

Less: depreciation 200 200 200 200 200

Earnings before interest & tax

(EBIT) 80 80 500 900 200

Less: Interest @ 8% 80 80 80 80 80

Earnings before tax (EBT) 0 0 420 820 120

Less: taxation @ 30% 0 0 126 246 36

Earnings after taxation 0 0 294 574 84

Cash flow statement is different from the profitability statement because it does not

includes activities and events that does not affect cash availability. For instance, non-cash affect

operations like depreciation, loss & profit on sale, accruals are adjusted back to the net profit

after tax to know the amount of cash flow. With regards to the given project, it is prepared here

as follows:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table 3 Cash flow statement for Project A

Year 1 2 3 4 5

Profit after tax as per P&L statement 154 224 294 224 154

Add: Non-cash expenditures

Depreciation 300 300 300 300 300

Accrued interest 40 40 40 40 40

Add: Increase in current assets

Accounts receivables 50 67 83 67 50

Inventory 30 40 50 40 30

Less: Decrease in accounts payable 43 57 72 57 43

Cash flow from operating activities 457 514 573 514 457

Table 4Cash flow statement for Project B

Year 1 2 3 4 5

Profit after tax as per P&L statement 0 0 294 574 84

Add: Non-cash expenditures

Depreciation 200 200 200 200 200

Accrued interest 40 40 40 40 40

Add: Increase in current assets

Accounts receivables 10 10 100 250 30

Inventory 30 30 188 338 75

Less: Decrease in accounts payable 30 30 188 338 75

Cash flow from operating activities 230 230 434 564 294

Discounting rate

In capital budgeting method, discounting cash flow (DCF) analysis plays an important

role in valuing a project or assets considering the time value of currency. In such methods,

estimated cash inflows for the project life are discounted using a cost of capital so as to use their

current or present values (PVs). Time value of Money (TVM) concept works on the logic that it

is worthier to receive money today instead of receiving it later because, by investing money

today helps to get an interest tomorrow. Here, selecting a discounting factor is one of the most

important requirements; it can be either the bank’s interest rate or weighted average cost of

capital. Here, with reference to the given project proposals, A & B, both of these are financed

through debt capital. On debt interest, taxation authorities render tax shields means tax is charged

after payment of an interest obligation (Eliasson and Börjesson, 2014). Therefore, it can be said

that cost of debt is computed after tax payment using following formula, as follows:

3

Year 1 2 3 4 5

Profit after tax as per P&L statement 154 224 294 224 154

Add: Non-cash expenditures

Depreciation 300 300 300 300 300

Accrued interest 40 40 40 40 40

Add: Increase in current assets

Accounts receivables 50 67 83 67 50

Inventory 30 40 50 40 30

Less: Decrease in accounts payable 43 57 72 57 43

Cash flow from operating activities 457 514 573 514 457

Table 4Cash flow statement for Project B

Year 1 2 3 4 5

Profit after tax as per P&L statement 0 0 294 574 84

Add: Non-cash expenditures

Depreciation 200 200 200 200 200

Accrued interest 40 40 40 40 40

Add: Increase in current assets

Accounts receivables 10 10 100 250 30

Inventory 30 30 188 338 75

Less: Decrease in accounts payable 30 30 188 338 75

Cash flow from operating activities 230 230 434 564 294

Discounting rate

In capital budgeting method, discounting cash flow (DCF) analysis plays an important

role in valuing a project or assets considering the time value of currency. In such methods,

estimated cash inflows for the project life are discounted using a cost of capital so as to use their

current or present values (PVs). Time value of Money (TVM) concept works on the logic that it

is worthier to receive money today instead of receiving it later because, by investing money

today helps to get an interest tomorrow. Here, selecting a discounting factor is one of the most

important requirements; it can be either the bank’s interest rate or weighted average cost of

capital. Here, with reference to the given project proposals, A & B, both of these are financed

through debt capital. On debt interest, taxation authorities render tax shields means tax is charged

after payment of an interest obligation (Eliasson and Börjesson, 2014). Therefore, it can be said

that cost of debt is computed after tax payment using following formula, as follows:

3

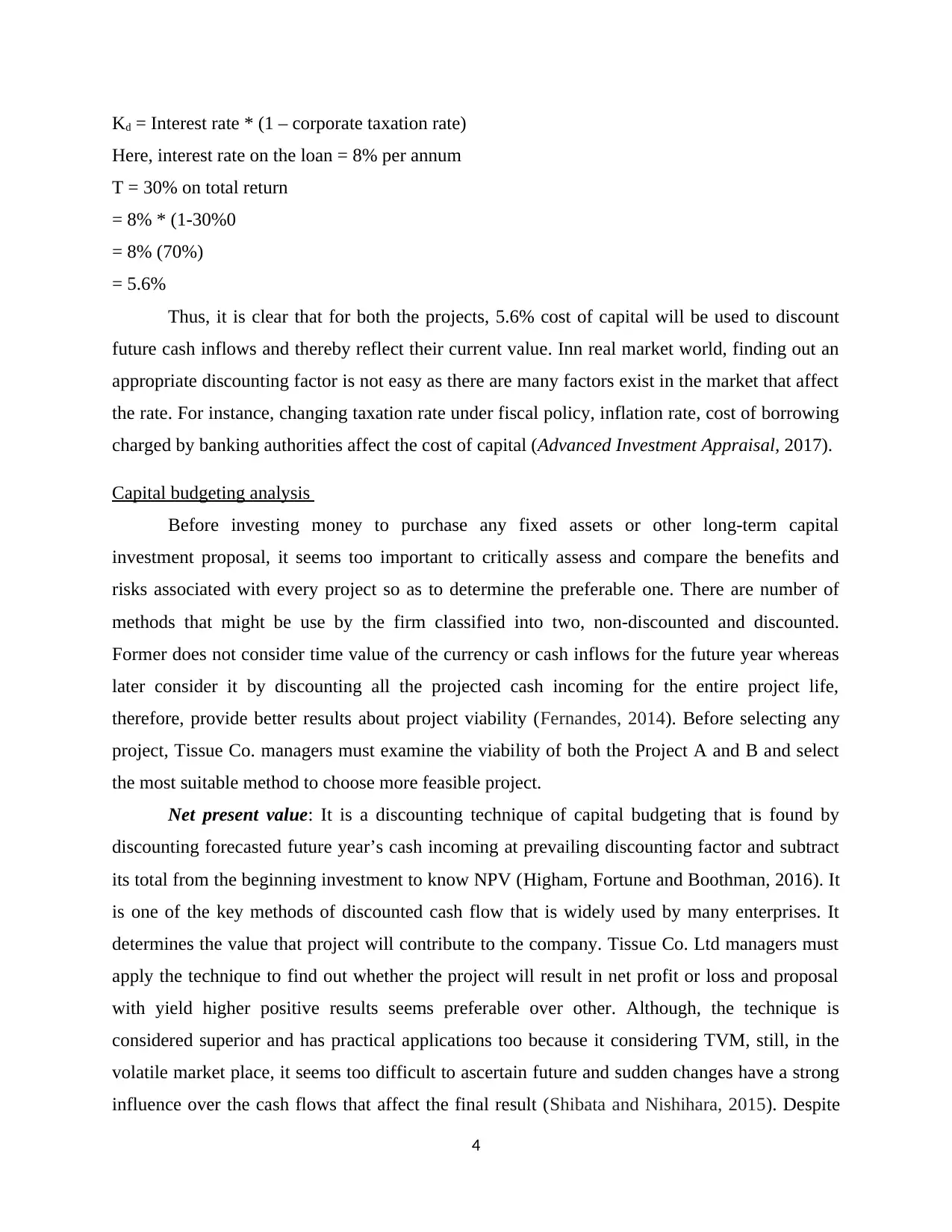

Kd = Interest rate * (1 – corporate taxation rate)

Here, interest rate on the loan = 8% per annum

T = 30% on total return

= 8% * (1-30%0

= 8% (70%)

= 5.6%

Thus, it is clear that for both the projects, 5.6% cost of capital will be used to discount

future cash inflows and thereby reflect their current value. Inn real market world, finding out an

appropriate discounting factor is not easy as there are many factors exist in the market that affect

the rate. For instance, changing taxation rate under fiscal policy, inflation rate, cost of borrowing

charged by banking authorities affect the cost of capital (Advanced Investment Appraisal, 2017).

Capital budgeting analysis

Before investing money to purchase any fixed assets or other long-term capital

investment proposal, it seems too important to critically assess and compare the benefits and

risks associated with every project so as to determine the preferable one. There are number of

methods that might be use by the firm classified into two, non-discounted and discounted.

Former does not consider time value of the currency or cash inflows for the future year whereas

later consider it by discounting all the projected cash incoming for the entire project life,

therefore, provide better results about project viability (Fernandes, 2014). Before selecting any

project, Tissue Co. managers must examine the viability of both the Project A and B and select

the most suitable method to choose more feasible project.

Net present value: It is a discounting technique of capital budgeting that is found by

discounting forecasted future year’s cash incoming at prevailing discounting factor and subtract

its total from the beginning investment to know NPV (Higham, Fortune and Boothman, 2016). It

is one of the key methods of discounted cash flow that is widely used by many enterprises. It

determines the value that project will contribute to the company. Tissue Co. Ltd managers must

apply the technique to find out whether the project will result in net profit or loss and proposal

with yield higher positive results seems preferable over other. Although, the technique is

considered superior and has practical applications too because it considering TVM, still, in the

volatile market place, it seems too difficult to ascertain future and sudden changes have a strong

influence over the cash flows that affect the final result (Shibata and Nishihara, 2015). Despite

4

Here, interest rate on the loan = 8% per annum

T = 30% on total return

= 8% * (1-30%0

= 8% (70%)

= 5.6%

Thus, it is clear that for both the projects, 5.6% cost of capital will be used to discount

future cash inflows and thereby reflect their current value. Inn real market world, finding out an

appropriate discounting factor is not easy as there are many factors exist in the market that affect

the rate. For instance, changing taxation rate under fiscal policy, inflation rate, cost of borrowing

charged by banking authorities affect the cost of capital (Advanced Investment Appraisal, 2017).

Capital budgeting analysis

Before investing money to purchase any fixed assets or other long-term capital

investment proposal, it seems too important to critically assess and compare the benefits and

risks associated with every project so as to determine the preferable one. There are number of

methods that might be use by the firm classified into two, non-discounted and discounted.

Former does not consider time value of the currency or cash inflows for the future year whereas

later consider it by discounting all the projected cash incoming for the entire project life,

therefore, provide better results about project viability (Fernandes, 2014). Before selecting any

project, Tissue Co. managers must examine the viability of both the Project A and B and select

the most suitable method to choose more feasible project.

Net present value: It is a discounting technique of capital budgeting that is found by

discounting forecasted future year’s cash incoming at prevailing discounting factor and subtract

its total from the beginning investment to know NPV (Higham, Fortune and Boothman, 2016). It

is one of the key methods of discounted cash flow that is widely used by many enterprises. It

determines the value that project will contribute to the company. Tissue Co. Ltd managers must

apply the technique to find out whether the project will result in net profit or loss and proposal

with yield higher positive results seems preferable over other. Although, the technique is

considered superior and has practical applications too because it considering TVM, still, in the

volatile market place, it seems too difficult to ascertain future and sudden changes have a strong

influence over the cash flows that affect the final result (Shibata and Nishihara, 2015). Despite

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this, this method favours using the same rate of discounting for the entire life, however, in the

volatile market, it does not seem justifiable (Li and Trutnevyte, 2017).

NPV =Present value of future cash inflows – PV of cash outgoings/investment

Table 5 Calculation of net present value for project A

Year

Cash inflows (In

$000) Discounting rate

PV of discounted cash

flows

(In $000)

1 457 0.9470 432.77

2 514 0.8968 460.93

3 573 0.8492 486.59

4 514 0.8042 413.34

5 457 0.7615 348.01

Present value (PV) of discounted cash inflows (DCF) 2141.64

Less: Beginning investment 1500

Net present value 641.64

Table 6 Calculation of net present value for project B

Year

Cash inflows (In

$000) Discounting rate

PV of discounted cash

flows

(In $000)

1 230 0.9470 217.80

2 230 0.8968 206.25

3 434 0.8492 368.55

4 564 0.8042 453.55

5 294 0.7615 223.89

Present value (PV) of discounted cash inflows (DCF) 1470.04

Less: Beginning investment 1500

Net present value -29.96

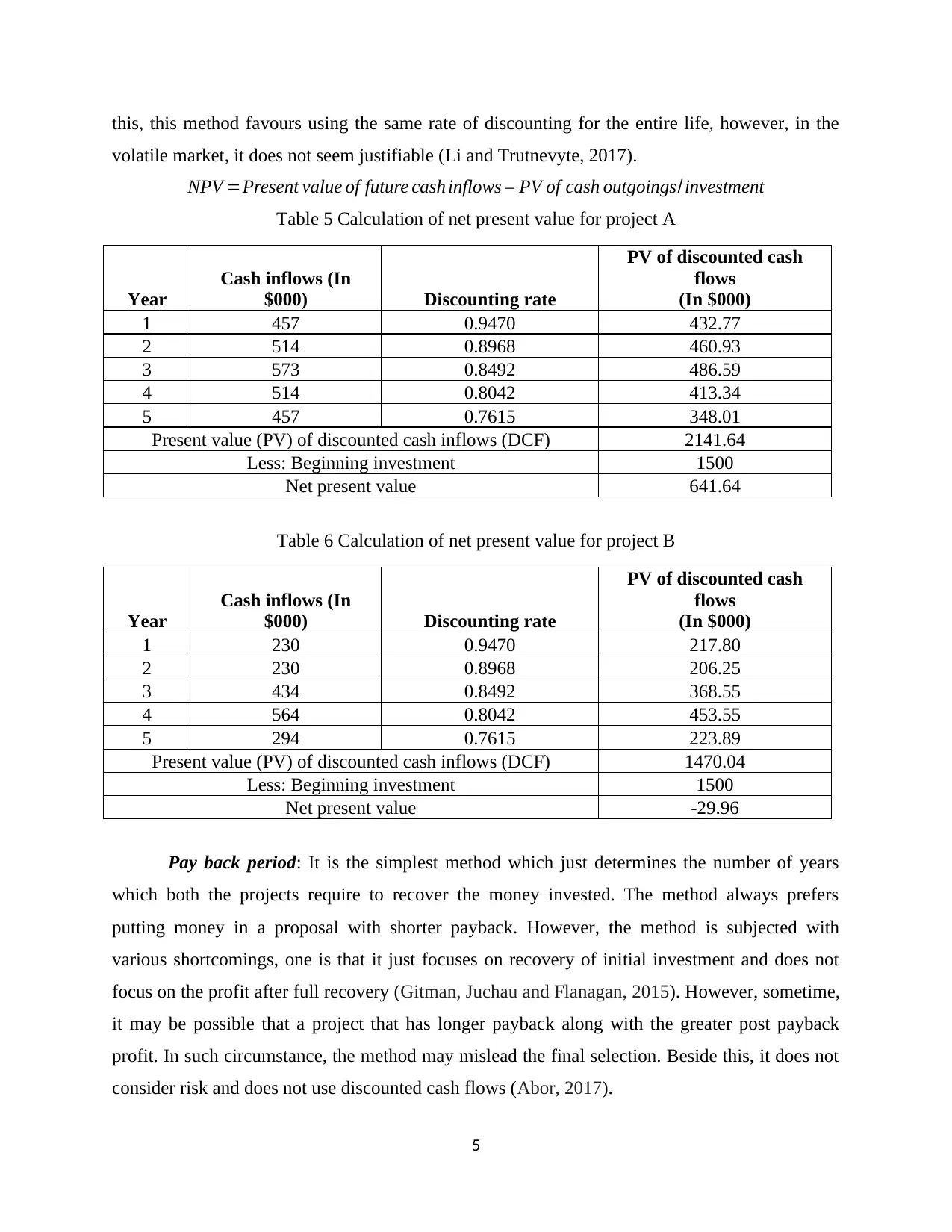

Pay back period: It is the simplest method which just determines the number of years

which both the projects require to recover the money invested. The method always prefers

putting money in a proposal with shorter payback. However, the method is subjected with

various shortcomings, one is that it just focuses on recovery of initial investment and does not

focus on the profit after full recovery (Gitman, Juchau and Flanagan, 2015). However, sometime,

it may be possible that a project that has longer payback along with the greater post payback

profit. In such circumstance, the method may mislead the final selection. Beside this, it does not

consider risk and does not use discounted cash flows (Abor, 2017).

5

volatile market, it does not seem justifiable (Li and Trutnevyte, 2017).

NPV =Present value of future cash inflows – PV of cash outgoings/investment

Table 5 Calculation of net present value for project A

Year

Cash inflows (In

$000) Discounting rate

PV of discounted cash

flows

(In $000)

1 457 0.9470 432.77

2 514 0.8968 460.93

3 573 0.8492 486.59

4 514 0.8042 413.34

5 457 0.7615 348.01

Present value (PV) of discounted cash inflows (DCF) 2141.64

Less: Beginning investment 1500

Net present value 641.64

Table 6 Calculation of net present value for project B

Year

Cash inflows (In

$000) Discounting rate

PV of discounted cash

flows

(In $000)

1 230 0.9470 217.80

2 230 0.8968 206.25

3 434 0.8492 368.55

4 564 0.8042 453.55

5 294 0.7615 223.89

Present value (PV) of discounted cash inflows (DCF) 1470.04

Less: Beginning investment 1500

Net present value -29.96

Pay back period: It is the simplest method which just determines the number of years

which both the projects require to recover the money invested. The method always prefers

putting money in a proposal with shorter payback. However, the method is subjected with

various shortcomings, one is that it just focuses on recovery of initial investment and does not

focus on the profit after full recovery (Gitman, Juchau and Flanagan, 2015). However, sometime,

it may be possible that a project that has longer payback along with the greater post payback

profit. In such circumstance, the method may mislead the final selection. Beside this, it does not

consider risk and does not use discounted cash flows (Abor, 2017).

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Payback period in equal cash inflows over the project life:

= Initial investment/Yearly cash inflows

Payback period in unequal cash inflows over the project life:

= Number of years prior to full recovery + unrecovered cost remaining/Cash flow during full

recovery year

Table 7 Calulation of payback period for project A

Year Cash flows (In $000)

Cumulative cash

inflows (In $000)

1 457 457

2 514 971

3 573 1544

4 514 2058

5 457 2515

Payback period

= 2 years + (1,544 – 1,500)/695

= 2.08

Table 8 Calulation of payback period for project B

Year Cash flows (In $000)

Cumulative cash

inflows (In $000)

1 230 230

2 230 460

3 434 894

4 564 1458

5 294 1752

Payback period

= 4 years + (1,752-1,500) / 1,064

= 4.45 years

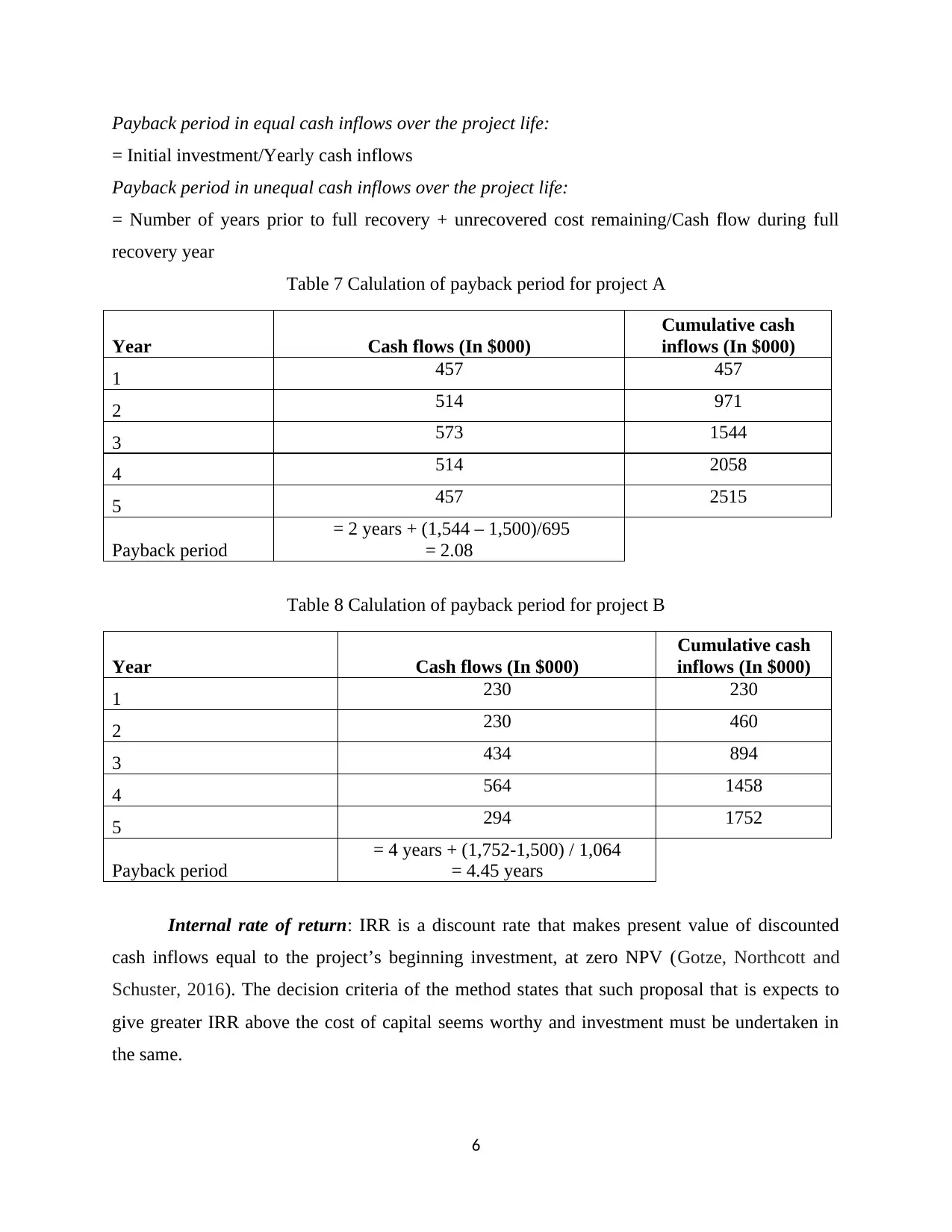

Internal rate of return: IRR is a discount rate that makes present value of discounted

cash inflows equal to the project’s beginning investment, at zero NPV (Gotze, Northcott and

Schuster, 2016). The decision criteria of the method states that such proposal that is expects to

give greater IRR above the cost of capital seems worthy and investment must be undertaken in

the same.

6

= Initial investment/Yearly cash inflows

Payback period in unequal cash inflows over the project life:

= Number of years prior to full recovery + unrecovered cost remaining/Cash flow during full

recovery year

Table 7 Calulation of payback period for project A

Year Cash flows (In $000)

Cumulative cash

inflows (In $000)

1 457 457

2 514 971

3 573 1544

4 514 2058

5 457 2515

Payback period

= 2 years + (1,544 – 1,500)/695

= 2.08

Table 8 Calulation of payback period for project B

Year Cash flows (In $000)

Cumulative cash

inflows (In $000)

1 230 230

2 230 460

3 434 894

4 564 1458

5 294 1752

Payback period

= 4 years + (1,752-1,500) / 1,064

= 4.45 years

Internal rate of return: IRR is a discount rate that makes present value of discounted

cash inflows equal to the project’s beginning investment, at zero NPV (Gotze, Northcott and

Schuster, 2016). The decision criteria of the method states that such proposal that is expects to

give greater IRR above the cost of capital seems worthy and investment must be undertaken in

the same.

6

Table 9 Calculation of internal rate of return for project A

Year Cash inflows (In $000)

Beginning investment -1500

1 457

2 514

3 573

4 514

5 457

IRR ( Calculated in Excel) 20%

Table 10 Calculation of internal rate of return for project for project B

Year Cash inflows (In $000)

Beginning investment -1500

1 230

2 230

3 434

4 564

5 294

IRR ( Calculated in Excel) 5%

Accounting rate of return: It measures average profit percentage on the average

investment made by the company. With such method, the main thing is that it uses accounting

return, earning after taxes and by this, non-cash items like accruals, depreciation and loss/profit

on disposal is taken into consideration (Locatelli, Invernizzi and Mancini, 2016). Moreover,

similar to payback, cash flows are not subjected to cost of capital hence, it ignores time value of

money.

ARR=Average net income / Average investment∗100

Table 11 Calculation of accounting rate of return for project A

Year Profitability (In $000)

1 154

2 224

7

Year Cash inflows (In $000)

Beginning investment -1500

1 457

2 514

3 573

4 514

5 457

IRR ( Calculated in Excel) 20%

Table 10 Calculation of internal rate of return for project for project B

Year Cash inflows (In $000)

Beginning investment -1500

1 230

2 230

3 434

4 564

5 294

IRR ( Calculated in Excel) 5%

Accounting rate of return: It measures average profit percentage on the average

investment made by the company. With such method, the main thing is that it uses accounting

return, earning after taxes and by this, non-cash items like accruals, depreciation and loss/profit

on disposal is taken into consideration (Locatelli, Invernizzi and Mancini, 2016). Moreover,

similar to payback, cash flows are not subjected to cost of capital hence, it ignores time value of

money.

ARR=Average net income / Average investment∗100

Table 11 Calculation of accounting rate of return for project A

Year Profitability (In $000)

1 154

2 224

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3 294

4 224

5 154

Total 1050

ARR=(1050 /5 years )/(1,500,000+0)/2∗100

¿ 210/750∗100

¿ 28 %

Table 12 Calculation of accounting rate of return for project B

Year Profitability (In $000)

1 0

2 0

3 294

4 574

5 84

Total 952

ARR=(952/5 years)/(1,500,000+0)/2

¿ 190.4 /750∗100

¿ 25.39 %

Profitability Index: PI method is used to show the relative profitability of a project.

According to its decision rule, when a project yields PI above 1, project comes in the acceptable

criteria otherwise not (Greenbaum, Thakor and Boot, 2015). Investment proposal with maximum

PI is always found more feasible and viable. The main risk with the method is that if Tissue Co’s

main objective is to maximize shareholder value then, in such situation, it may leads to

misleading investment decisions.

Profitability Index=Present value of expe cted cash inflows /Initial Cost

Table 13 Calculation of profitability Index for project A

PV of discounted cash inflows 2141.64

Initial investment 1500

Profitability Index 1.43

8

4 224

5 154

Total 1050

ARR=(1050 /5 years )/(1,500,000+0)/2∗100

¿ 210/750∗100

¿ 28 %

Table 12 Calculation of accounting rate of return for project B

Year Profitability (In $000)

1 0

2 0

3 294

4 574

5 84

Total 952

ARR=(952/5 years)/(1,500,000+0)/2

¿ 190.4 /750∗100

¿ 25.39 %

Profitability Index: PI method is used to show the relative profitability of a project.

According to its decision rule, when a project yields PI above 1, project comes in the acceptable

criteria otherwise not (Greenbaum, Thakor and Boot, 2015). Investment proposal with maximum

PI is always found more feasible and viable. The main risk with the method is that if Tissue Co’s

main objective is to maximize shareholder value then, in such situation, it may leads to

misleading investment decisions.

Profitability Index=Present value of expe cted cash inflows /Initial Cost

Table 13 Calculation of profitability Index for project A

PV of discounted cash inflows 2141.64

Initial investment 1500

Profitability Index 1.43

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

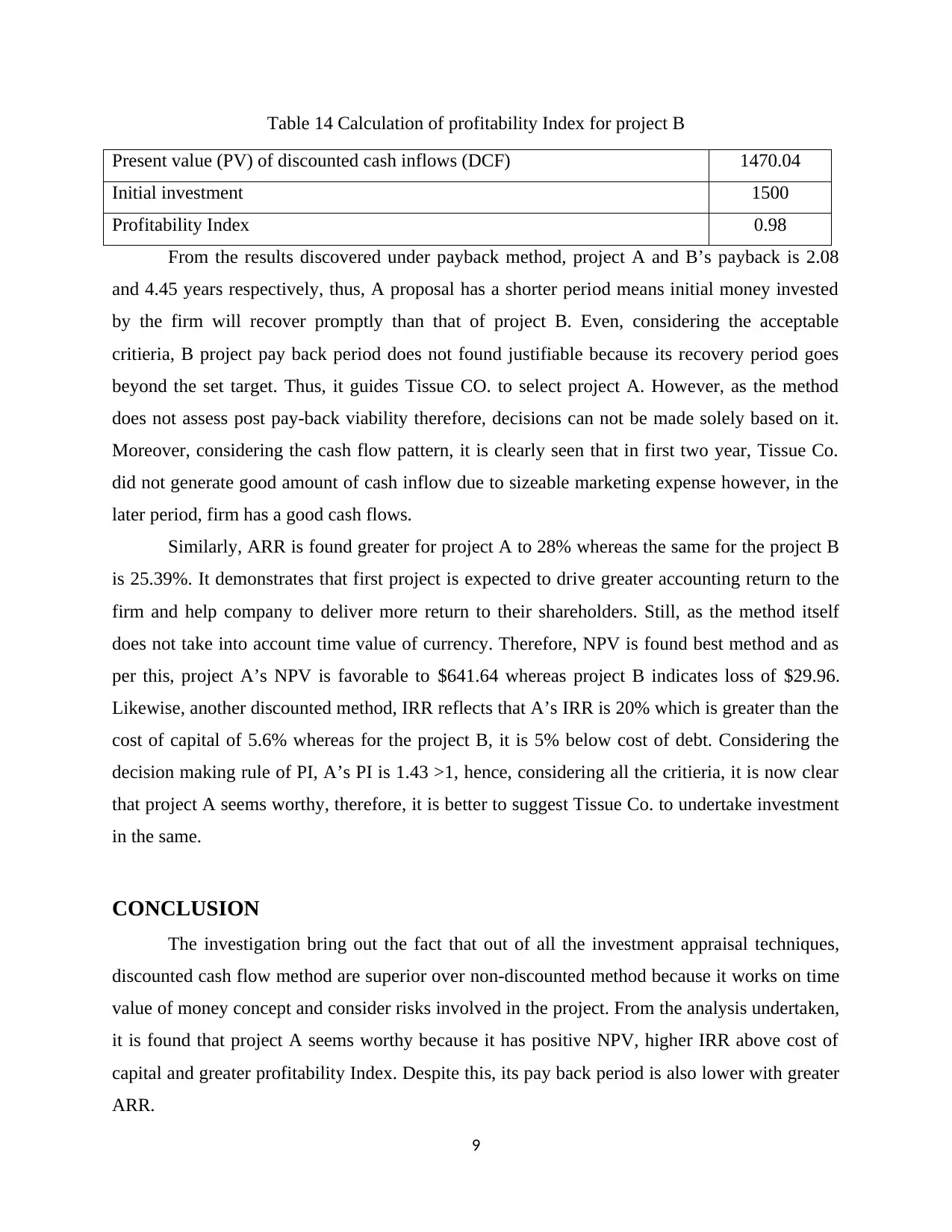

Table 14 Calculation of profitability Index for project B

Present value (PV) of discounted cash inflows (DCF) 1470.04

Initial investment 1500

Profitability Index 0.98

From the results discovered under payback method, project A and B’s payback is 2.08

and 4.45 years respectively, thus, A proposal has a shorter period means initial money invested

by the firm will recover promptly than that of project B. Even, considering the acceptable

critieria, B project pay back period does not found justifiable because its recovery period goes

beyond the set target. Thus, it guides Tissue CO. to select project A. However, as the method

does not assess post pay-back viability therefore, decisions can not be made solely based on it.

Moreover, considering the cash flow pattern, it is clearly seen that in first two year, Tissue Co.

did not generate good amount of cash inflow due to sizeable marketing expense however, in the

later period, firm has a good cash flows.

Similarly, ARR is found greater for project A to 28% whereas the same for the project B

is 25.39%. It demonstrates that first project is expected to drive greater accounting return to the

firm and help company to deliver more return to their shareholders. Still, as the method itself

does not take into account time value of currency. Therefore, NPV is found best method and as

per this, project A’s NPV is favorable to $641.64 whereas project B indicates loss of $29.96.

Likewise, another discounted method, IRR reflects that A’s IRR is 20% which is greater than the

cost of capital of 5.6% whereas for the project B, it is 5% below cost of debt. Considering the

decision making rule of PI, A’s PI is 1.43 >1, hence, considering all the critieria, it is now clear

that project A seems worthy, therefore, it is better to suggest Tissue Co. to undertake investment

in the same.

CONCLUSION

The investigation bring out the fact that out of all the investment appraisal techniques,

discounted cash flow method are superior over non-discounted method because it works on time

value of money concept and consider risks involved in the project. From the analysis undertaken,

it is found that project A seems worthy because it has positive NPV, higher IRR above cost of

capital and greater profitability Index. Despite this, its pay back period is also lower with greater

ARR.

9

Present value (PV) of discounted cash inflows (DCF) 1470.04

Initial investment 1500

Profitability Index 0.98

From the results discovered under payback method, project A and B’s payback is 2.08

and 4.45 years respectively, thus, A proposal has a shorter period means initial money invested

by the firm will recover promptly than that of project B. Even, considering the acceptable

critieria, B project pay back period does not found justifiable because its recovery period goes

beyond the set target. Thus, it guides Tissue CO. to select project A. However, as the method

does not assess post pay-back viability therefore, decisions can not be made solely based on it.

Moreover, considering the cash flow pattern, it is clearly seen that in first two year, Tissue Co.

did not generate good amount of cash inflow due to sizeable marketing expense however, in the

later period, firm has a good cash flows.

Similarly, ARR is found greater for project A to 28% whereas the same for the project B

is 25.39%. It demonstrates that first project is expected to drive greater accounting return to the

firm and help company to deliver more return to their shareholders. Still, as the method itself

does not take into account time value of currency. Therefore, NPV is found best method and as

per this, project A’s NPV is favorable to $641.64 whereas project B indicates loss of $29.96.

Likewise, another discounted method, IRR reflects that A’s IRR is 20% which is greater than the

cost of capital of 5.6% whereas for the project B, it is 5% below cost of debt. Considering the

decision making rule of PI, A’s PI is 1.43 >1, hence, considering all the critieria, it is now clear

that project A seems worthy, therefore, it is better to suggest Tissue Co. to undertake investment

in the same.

CONCLUSION

The investigation bring out the fact that out of all the investment appraisal techniques,

discounted cash flow method are superior over non-discounted method because it works on time

value of money concept and consider risks involved in the project. From the analysis undertaken,

it is found that project A seems worthy because it has positive NPV, higher IRR above cost of

capital and greater profitability Index. Despite this, its pay back period is also lower with greater

ARR.

9

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.