Project 1: Feedback, Forecast, and Examples of Accounting Info

VerifiedAdded on 2023/01/05

|13

|2978

|23

Report

AI Summary

This report analyzes the concepts of 'feedback value' and 'forecast value' in financial decision-making, highlighting their roles in improving user choices based on past performance and future predictions. It explains the significance of accounting relevance and predictive value in financial reporting, supported by an example of customer comments on corporate tax reports. The report then provides four examples of accounting information extracted from an annual report: the balance sheet, income statement, statement of cash flows, and ledger accounts. It details the components and functions of each, including how changes in accounts receivable, inventory value, and cash flows impact financial analysis. The report also covers the indirect and direct methods for calculating cash flow, and the ledger account's role in maintaining financial transaction records. The report emphasizes the interrelation of these elements in providing a comprehensive view of a company's financial health and performance.

Project 1

a) Discuss how ‘feedback value’ and ‘forecast value’ may assist users to make

better decision

Feedback value means the nature of the data that allows users to confirm or respond to wishes in

advance. It is unusual to expect a future business model without evaluating the exercises it has

done in the past. In this way, appreciation of the input is essential, if appropriate. The data can

influence the choice by altering or correcting the wishes of previous clan leaders. Customers

can't make the right choice if their data doesn't meet the criticism. The attached table shows

customer comments on the critique of estimated data on corporate tax reports.

Accounting relevance deals with the usefulness of financial information to users during the

decision making process. Obviously financial information that isn’t related to user’s decisions

isn’t useful to creditors or investors. That is why FASB committed to making financial reporting

relevant to the end users.

Predictive value refers to the fact that quality financial information can be used to base

predictions, forecasts, and projections on. Financial analysts and investors can use past financial

statements to chart performance trends and make predictions about future performance and

profitability.

Quality information has a feedback value when it can confirm or correct previous expectations.

In other words, users can examine financial information and confirm or adjust their predictions

made on previous performance trends. Based on this feedback, users can make future decisions.

b) Show four examples of accounting information from the annual report.

Balance Sheet

A corporate balance sheet indicates a firm's economic solidness. It lists short-term assets such as

cash, accounts receivable, inventories and short-term investments. Balance sheet is more like a

forecast of an organization’s balance sheet position at a predefined time, usually determined after

each quarter, half-year or year. The accounting relationship has two main headings: resources

and responsibilities. Responsibilities are responsibilities or commitments of an organization.

a) Discuss how ‘feedback value’ and ‘forecast value’ may assist users to make

better decision

Feedback value means the nature of the data that allows users to confirm or respond to wishes in

advance. It is unusual to expect a future business model without evaluating the exercises it has

done in the past. In this way, appreciation of the input is essential, if appropriate. The data can

influence the choice by altering or correcting the wishes of previous clan leaders. Customers

can't make the right choice if their data doesn't meet the criticism. The attached table shows

customer comments on the critique of estimated data on corporate tax reports.

Accounting relevance deals with the usefulness of financial information to users during the

decision making process. Obviously financial information that isn’t related to user’s decisions

isn’t useful to creditors or investors. That is why FASB committed to making financial reporting

relevant to the end users.

Predictive value refers to the fact that quality financial information can be used to base

predictions, forecasts, and projections on. Financial analysts and investors can use past financial

statements to chart performance trends and make predictions about future performance and

profitability.

Quality information has a feedback value when it can confirm or correct previous expectations.

In other words, users can examine financial information and confirm or adjust their predictions

made on previous performance trends. Based on this feedback, users can make future decisions.

b) Show four examples of accounting information from the annual report.

Balance Sheet

A corporate balance sheet indicates a firm's economic solidness. It lists short-term assets such as

cash, accounts receivable, inventories and short-term investments. Balance sheet is more like a

forecast of an organization’s balance sheet position at a predefined time, usually determined after

each quarter, half-year or year. The accounting relationship has two main headings: resources

and responsibilities. Responsibilities are responsibilities or commitments of an organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

How much the group owes its tenants. Responsibilities can be separated into current and long-

range responsibilities.

Another important page that has not yet been confirmed is the value of the investor or owner.

Resources are synonymous with adding to the responsibilities and value of owners. Owner value

is used when the group is a sole proprietor and investment value is used when the group is a

body corporate. It's called the book's estimate.

The Balance sheet is one of the three basic budget ratios and is essential for both fiscal

presentation and accounting. The cash register shows the total resources of the organization and

how those resources are funded, by way of duty or other value. Similarly, it can be referred to as

proof of total assets or as proof of a cash-related position. The accounting report is based on the

key condition: Assets = Liabilities + Equity.

In this capacity, the accounting report is divided into several parts (or areas). The left hand side

of the accounting report follows the integrity of an organization's resources. On the other hand,

the accounting report oversees the responsibilities of the organization and the value of its

investors. Resources and responsibilities are divided into two classes: current resources /

responsibilities and absent (long range) resources / responsibilities. Smaller registers, such as

Inventory, Cash, and Trade Payments, are established in the current range before illegal (or

absent, accounts, for example, Appliance, Property and Equipment (PP&E) ) and Long Term

Payments).

Income Statement

An organization's statement of profit and loss instructs a reader on the firm's profitability and

financial performance during a period such as a month, quarter or year.

Statement of Cash Flows

An organization's statement of cash flows provides details about the firm's cash inflows, or

receipts, and cash outflows, or payments, during a period. The statement of cash flows, or the

cash flow statement, is a budget summary that sums up the measure of money and money

counterparts entering and leaving an organization. The income proclamation (CFS) quantifies

how well an organization deals with its money position, which means how well the organization

produces money to pay its obligation commitments and asset its working costs. The income

range responsibilities.

Another important page that has not yet been confirmed is the value of the investor or owner.

Resources are synonymous with adding to the responsibilities and value of owners. Owner value

is used when the group is a sole proprietor and investment value is used when the group is a

body corporate. It's called the book's estimate.

The Balance sheet is one of the three basic budget ratios and is essential for both fiscal

presentation and accounting. The cash register shows the total resources of the organization and

how those resources are funded, by way of duty or other value. Similarly, it can be referred to as

proof of total assets or as proof of a cash-related position. The accounting report is based on the

key condition: Assets = Liabilities + Equity.

In this capacity, the accounting report is divided into several parts (or areas). The left hand side

of the accounting report follows the integrity of an organization's resources. On the other hand,

the accounting report oversees the responsibilities of the organization and the value of its

investors. Resources and responsibilities are divided into two classes: current resources /

responsibilities and absent (long range) resources / responsibilities. Smaller registers, such as

Inventory, Cash, and Trade Payments, are established in the current range before illegal (or

absent, accounts, for example, Appliance, Property and Equipment (PP&E) ) and Long Term

Payments).

Income Statement

An organization's statement of profit and loss instructs a reader on the firm's profitability and

financial performance during a period such as a month, quarter or year.

Statement of Cash Flows

An organization's statement of cash flows provides details about the firm's cash inflows, or

receipts, and cash outflows, or payments, during a period. The statement of cash flows, or the

cash flow statement, is a budget summary that sums up the measure of money and money

counterparts entering and leaving an organization. The income proclamation (CFS) quantifies

how well an organization deals with its money position, which means how well the organization

produces money to pay its obligation commitments and asset its working costs. The income

articulation supplements the monetary record and pay explanation and is a required piece of an

organization's monetary reports since 1987.

The CFS permits speculators to see how an organization's tasks are running, where its cash is

coming from, and how cash is being spent. The CFS is significant since it assists speculators

with deciding if an organization is on a strong monetary balance. Banks, then again, can utilize

the CFS to decide how much money is accessible (alluded to as liquidity) for the organization to

finance its working costs and pay its obligations.

It's critical to take note of that the CFS is particular from the pay proclamation and asset report

since it does exclude the measure of future approaching and active money that has been recorded

using a loan. Along these lines, money isn't equivalent to overall gain, which on the pay

explanation and monetary record incorporates money deals and deals made using a loan.

On account of an exchanging portfolio or a venture organization, receipts from the offer of

credits, obligation, or value instruments are likewise included. While setting up an income

articulation under the backhanded technique, deterioration, amortization, conceded expense,

additions or misfortunes related with a noncurrent resource, and profits or income got from

certain contributing exercises are likewise included. Nonetheless, buys or deals of long haul

resources are excluded from working exercises.

Income is determined by making certain acclimations to net gain by adding or deducting

contrasts in income, costs, and credit exchanges (showing up on the accounting report and pay

explanation) coming about because of exchanges that happen starting with one period then onto

the next. These changes are made on the grounds that non-money things are determined into total

compensation (pay articulation) and all out resources and liabilities (monetary record). Along

these lines, on the grounds that not all exchanges include real money things, numerous things

must be reconsidered when ascertaining income from activities. Therefore, there are two

techniques for computing income: the immediate strategy and the aberrant strategy.

Direct Cash Flow Method

The immediate strategy includes all the different kinds of money installments and receipts,

including money paid to providers, money receipts from clients, and money paid out in

organization's monetary reports since 1987.

The CFS permits speculators to see how an organization's tasks are running, where its cash is

coming from, and how cash is being spent. The CFS is significant since it assists speculators

with deciding if an organization is on a strong monetary balance. Banks, then again, can utilize

the CFS to decide how much money is accessible (alluded to as liquidity) for the organization to

finance its working costs and pay its obligations.

It's critical to take note of that the CFS is particular from the pay proclamation and asset report

since it does exclude the measure of future approaching and active money that has been recorded

using a loan. Along these lines, money isn't equivalent to overall gain, which on the pay

explanation and monetary record incorporates money deals and deals made using a loan.

On account of an exchanging portfolio or a venture organization, receipts from the offer of

credits, obligation, or value instruments are likewise included. While setting up an income

articulation under the backhanded technique, deterioration, amortization, conceded expense,

additions or misfortunes related with a noncurrent resource, and profits or income got from

certain contributing exercises are likewise included. Nonetheless, buys or deals of long haul

resources are excluded from working exercises.

Income is determined by making certain acclimations to net gain by adding or deducting

contrasts in income, costs, and credit exchanges (showing up on the accounting report and pay

explanation) coming about because of exchanges that happen starting with one period then onto

the next. These changes are made on the grounds that non-money things are determined into total

compensation (pay articulation) and all out resources and liabilities (monetary record). Along

these lines, on the grounds that not all exchanges include real money things, numerous things

must be reconsidered when ascertaining income from activities. Therefore, there are two

techniques for computing income: the immediate strategy and the aberrant strategy.

Direct Cash Flow Method

The immediate strategy includes all the different kinds of money installments and receipts,

including money paid to providers, money receipts from clients, and money paid out in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compensations. These figures are determined by utilizing the start and finishing adjusts of an

assortment of business accounts and inspecting the net diminishing or expansion in the records.

Indirect Cash Flow Method

With the backhanded technique, income from working exercises is determined by first removing

the net gain from an organization's pay explanation. Since an organization's pay proclamation is

set up on a gathering premise, income is possibly perceived when it is acquired and not when it

is gotten. Total compensation is certainly not a precise portrayal of net income from working

exercises, so it gets important to change profit before revenue and duties (EBIT) for things that

influence net gain, despite the fact that no genuine money has yet been gotten or paid against

them. The roundabout technique additionally makes changes in accordance with add back non-

working exercises that don't influence an organization's working income.

For instance, deterioration isn't generally a money cost; it is a sum that is deducted from the

absolute estimation of a resource that has recently been represented. That is the reason it is added

once more into net deals for computing income.

Accounts Receivable and Cash Flow

Changes in records receivable (AR) on the asset report starting with one bookkeeping period

then onto the next must likewise be reflected in income. On the off chance that records of sales

diminish, this infers that more money has entered the organization from clients taking care of

their credit accounts—the sum by which AR has diminished is then added to net deals. On the

off chance that debt claims increments starting with one bookkeeping period then onto the next,

the measure of the expansion must be deducted from net deals in light of the fact that, despite the

fact that the sums spoke to in AR are income, they are not money.

Inventory Value and Cash Flow

An expansion in stock, then again, signals that an organization has gone through more cash to

buy more crude materials. In the event that the stock was paid with money, the expansion in the

estimation of stock is deducted from net deals. A decline in stock would be added to net deals.

On the off chance that stock was bought on layaway, an expansion in records payable would

assortment of business accounts and inspecting the net diminishing or expansion in the records.

Indirect Cash Flow Method

With the backhanded technique, income from working exercises is determined by first removing

the net gain from an organization's pay explanation. Since an organization's pay proclamation is

set up on a gathering premise, income is possibly perceived when it is acquired and not when it

is gotten. Total compensation is certainly not a precise portrayal of net income from working

exercises, so it gets important to change profit before revenue and duties (EBIT) for things that

influence net gain, despite the fact that no genuine money has yet been gotten or paid against

them. The roundabout technique additionally makes changes in accordance with add back non-

working exercises that don't influence an organization's working income.

For instance, deterioration isn't generally a money cost; it is a sum that is deducted from the

absolute estimation of a resource that has recently been represented. That is the reason it is added

once more into net deals for computing income.

Accounts Receivable and Cash Flow

Changes in records receivable (AR) on the asset report starting with one bookkeeping period

then onto the next must likewise be reflected in income. On the off chance that records of sales

diminish, this infers that more money has entered the organization from clients taking care of

their credit accounts—the sum by which AR has diminished is then added to net deals. On the

off chance that debt claims increments starting with one bookkeeping period then onto the next,

the measure of the expansion must be deducted from net deals in light of the fact that, despite the

fact that the sums spoke to in AR are income, they are not money.

Inventory Value and Cash Flow

An expansion in stock, then again, signals that an organization has gone through more cash to

buy more crude materials. In the event that the stock was paid with money, the expansion in the

estimation of stock is deducted from net deals. A decline in stock would be added to net deals.

On the off chance that stock was bought on layaway, an expansion in records payable would

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

happen on the accounting report, and the measure of the increment from one year to the next

would be added to net deals.

A similar rationale remains constant for charges payable, compensations payable, and prepaid

protection. On the off chance that something has been paid off, at that point the distinction in the

worth owed starting with one year then onto the next must be deducted from total compensation.

In the event that there is a sum that is as yet owed, at that point any distinctions should be added

to net profit.

Cash from Investing Activities

Contributing exercises incorporate any sources and employments of money from an

organization's ventures. A buy or offer of a resource, credits made to merchants or got from

clients, or any installments identified with a consolidation or securing is remembered for this

classification. So, changes in gear, resources, or ventures identify with money from investing.3

Generally, money changes from contributing are a "money out" thing, since money is utilized to

purchase new gear, structures, or transient resources, for example, attractive protections. In any

case, when an organization strips a resource, the exchange is considered "money in" for

computing money from contributing.

Cash from Financing Activities

Money from financing exercises incorporates the wellsprings of money from speculators or

banks, just as the employments of money paid to investors. Installment of profits, installments

for stock repurchases, and the reimbursement of obligation head (credits) are remembered for

this class.

Changes in real money from financing are "money in" when capital is raised, and they're "money

out" when profits are paid. Consequently, if an organization gives an attach to the general

population, the organization gets money financing; be that as it may, when premium is paid to

bondholders, the organization is decreasing its money.

Ledger book

would be added to net deals.

A similar rationale remains constant for charges payable, compensations payable, and prepaid

protection. On the off chance that something has been paid off, at that point the distinction in the

worth owed starting with one year then onto the next must be deducted from total compensation.

In the event that there is a sum that is as yet owed, at that point any distinctions should be added

to net profit.

Cash from Investing Activities

Contributing exercises incorporate any sources and employments of money from an

organization's ventures. A buy or offer of a resource, credits made to merchants or got from

clients, or any installments identified with a consolidation or securing is remembered for this

classification. So, changes in gear, resources, or ventures identify with money from investing.3

Generally, money changes from contributing are a "money out" thing, since money is utilized to

purchase new gear, structures, or transient resources, for example, attractive protections. In any

case, when an organization strips a resource, the exchange is considered "money in" for

computing money from contributing.

Cash from Financing Activities

Money from financing exercises incorporates the wellsprings of money from speculators or

banks, just as the employments of money paid to investors. Installment of profits, installments

for stock repurchases, and the reimbursement of obligation head (credits) are remembered for

this class.

Changes in real money from financing are "money in" when capital is raised, and they're "money

out" when profits are paid. Consequently, if an organization gives an attach to the general

population, the organization gets money financing; be that as it may, when premium is paid to

bondholders, the organization is decreasing its money.

Ledger book

Ledger Account is a diary where an organization keeps up the information of the relative

multitude of exchanges and budget summary. Organization's overall record account is

coordinated under the overall record with the asset report grouped in various records like

resources, Accounts receivable, creditor liability, investors, liabilities, values, incomes, charges,

costs, benefit, misfortune, reserves, advances, bonds, stocks, compensations, compensation, and

so forth In this article, we will study Ledger Account organization and models, kinds of the

record, record posting, and we will likewise give record account layout in dominate, google

bookkeeping page, and PDF design.

Record is a book that contains the records. Any fiscal summary identified with the monetary

situation of the organization arises just from the records. Along these lines, this record is known

as the chief book. Thus, the consequence of this is that it is important to relate all the data for any

record accessible is from the record. This book of records is the main book for any business and

that is the reason it is known as the lord, everything being equal. Additionally, the record book is

otherwise called the book of the last section. The Ledger account is thought about the book that

has all the bookkeeping data of the organization.

Anyplace you go, you will discover this example as it were. Likewise, in record accounts, this

example is utilized for composing the passages of the bookkeeping. Moreover, record accounts

likewise incorporate the record posting.

At whatever point an exchange happens it is signified and recorded in the diary as the diary

section. Besides, this section is posted again in their separate diary accounts. This is done from

the diary under the twofold section rule. This is known as the record posting. There are a few

standards which you need to stick to while composing the diary sections for the accompanying

records.

multitude of exchanges and budget summary. Organization's overall record account is

coordinated under the overall record with the asset report grouped in various records like

resources, Accounts receivable, creditor liability, investors, liabilities, values, incomes, charges,

costs, benefit, misfortune, reserves, advances, bonds, stocks, compensations, compensation, and

so forth In this article, we will study Ledger Account organization and models, kinds of the

record, record posting, and we will likewise give record account layout in dominate, google

bookkeeping page, and PDF design.

Record is a book that contains the records. Any fiscal summary identified with the monetary

situation of the organization arises just from the records. Along these lines, this record is known

as the chief book. Thus, the consequence of this is that it is important to relate all the data for any

record accessible is from the record. This book of records is the main book for any business and

that is the reason it is known as the lord, everything being equal. Additionally, the record book is

otherwise called the book of the last section. The Ledger account is thought about the book that

has all the bookkeeping data of the organization.

Anyplace you go, you will discover this example as it were. Likewise, in record accounts, this

example is utilized for composing the passages of the bookkeeping. Moreover, record accounts

likewise incorporate the record posting.

At whatever point an exchange happens it is signified and recorded in the diary as the diary

section. Besides, this section is posted again in their separate diary accounts. This is done from

the diary under the twofold section rule. This is known as the record posting. There are a few

standards which you need to stick to while composing the diary sections for the accompanying

records.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

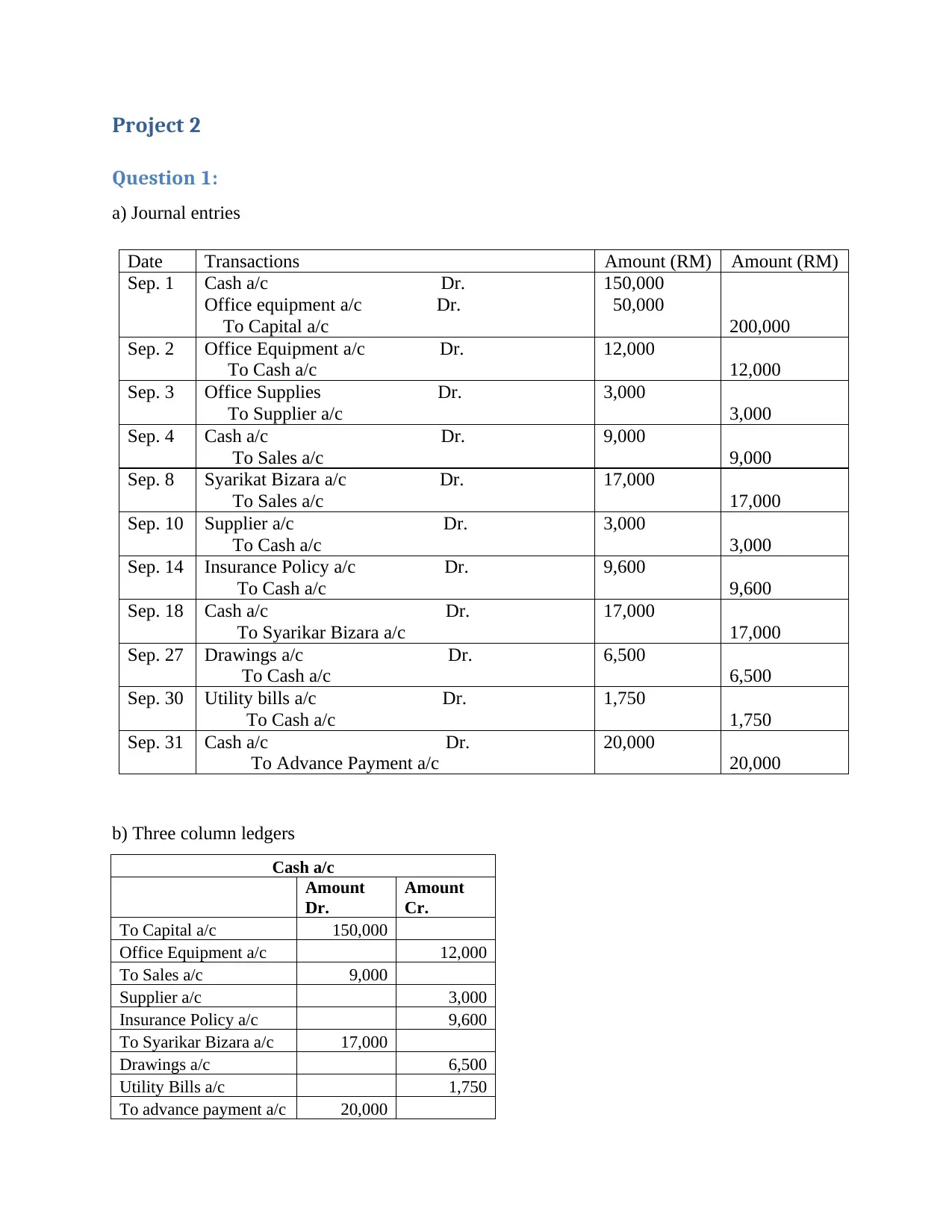

Project 2

Question 1:

a) Journal entries

Date Transactions Amount (RM) Amount (RM)

Sep. 1 Cash a/c Dr.

Office equipment a/c Dr.

To Capital a/c

150,000

50,000

200,000

Sep. 2 Office Equipment a/c Dr.

To Cash a/c

12,000

12,000

Sep. 3 Office Supplies Dr.

To Supplier a/c

3,000

3,000

Sep. 4 Cash a/c Dr.

To Sales a/c

9,000

9,000

Sep. 8 Syarikat Bizara a/c Dr.

To Sales a/c

17,000

17,000

Sep. 10 Supplier a/c Dr.

To Cash a/c

3,000

3,000

Sep. 14 Insurance Policy a/c Dr.

To Cash a/c

9,600

9,600

Sep. 18 Cash a/c Dr.

To Syarikar Bizara a/c

17,000

17,000

Sep. 27 Drawings a/c Dr.

To Cash a/c

6,500

6,500

Sep. 30 Utility bills a/c Dr.

To Cash a/c

1,750

1,750

Sep. 31 Cash a/c Dr.

To Advance Payment a/c

20,000

20,000

b) Three column ledgers

Cash a/c

Amount

Dr.

Amount

Cr.

To Capital a/c 150,000

Office Equipment a/c 12,000

To Sales a/c 9,000

Supplier a/c 3,000

Insurance Policy a/c 9,600

To Syarikar Bizara a/c 17,000

Drawings a/c 6,500

Utility Bills a/c 1,750

To advance payment a/c 20,000

Question 1:

a) Journal entries

Date Transactions Amount (RM) Amount (RM)

Sep. 1 Cash a/c Dr.

Office equipment a/c Dr.

To Capital a/c

150,000

50,000

200,000

Sep. 2 Office Equipment a/c Dr.

To Cash a/c

12,000

12,000

Sep. 3 Office Supplies Dr.

To Supplier a/c

3,000

3,000

Sep. 4 Cash a/c Dr.

To Sales a/c

9,000

9,000

Sep. 8 Syarikat Bizara a/c Dr.

To Sales a/c

17,000

17,000

Sep. 10 Supplier a/c Dr.

To Cash a/c

3,000

3,000

Sep. 14 Insurance Policy a/c Dr.

To Cash a/c

9,600

9,600

Sep. 18 Cash a/c Dr.

To Syarikar Bizara a/c

17,000

17,000

Sep. 27 Drawings a/c Dr.

To Cash a/c

6,500

6,500

Sep. 30 Utility bills a/c Dr.

To Cash a/c

1,750

1,750

Sep. 31 Cash a/c Dr.

To Advance Payment a/c

20,000

20,000

b) Three column ledgers

Cash a/c

Amount

Dr.

Amount

Cr.

To Capital a/c 150,000

Office Equipment a/c 12,000

To Sales a/c 9,000

Supplier a/c 3,000

Insurance Policy a/c 9,600

To Syarikar Bizara a/c 17,000

Drawings a/c 6,500

Utility Bills a/c 1,750

To advance payment a/c 20,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

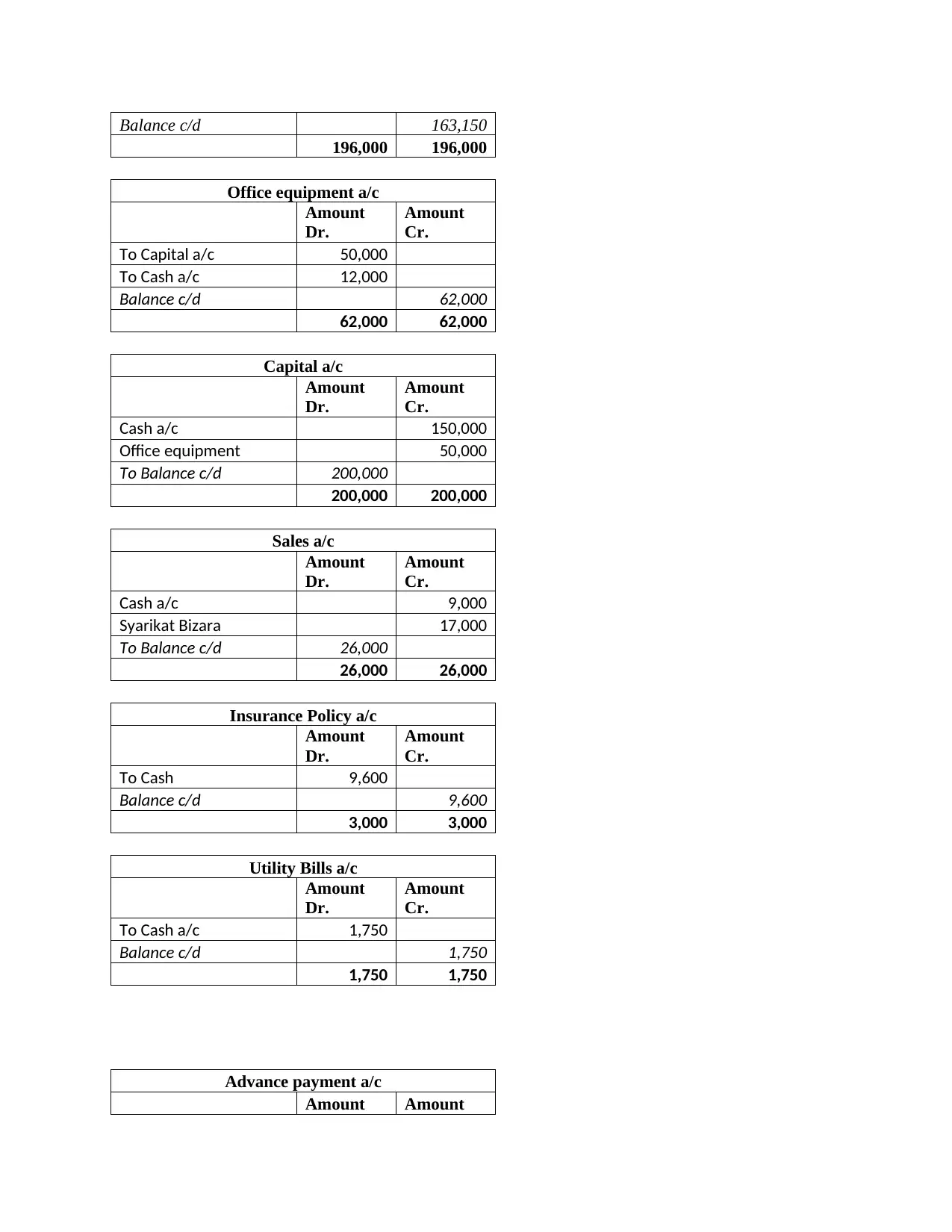

Balance c/d 163,150

196,000 196,000

Office equipment a/c

Amount

Dr.

Amount

Cr.

To Capital a/c 50,000

To Cash a/c 12,000

Balance c/d 62,000

62,000 62,000

Capital a/c

Amount

Dr.

Amount

Cr.

Cash a/c 150,000

Office equipment 50,000

To Balance c/d 200,000

200,000 200,000

Sales a/c

Amount

Dr.

Amount

Cr.

Cash a/c 9,000

Syarikat Bizara 17,000

To Balance c/d 26,000

26,000 26,000

Insurance Policy a/c

Amount

Dr.

Amount

Cr.

To Cash 9,600

Balance c/d 9,600

3,000 3,000

Utility Bills a/c

Amount

Dr.

Amount

Cr.

To Cash a/c 1,750

Balance c/d 1,750

1,750 1,750

Advance payment a/c

Amount Amount

196,000 196,000

Office equipment a/c

Amount

Dr.

Amount

Cr.

To Capital a/c 50,000

To Cash a/c 12,000

Balance c/d 62,000

62,000 62,000

Capital a/c

Amount

Dr.

Amount

Cr.

Cash a/c 150,000

Office equipment 50,000

To Balance c/d 200,000

200,000 200,000

Sales a/c

Amount

Dr.

Amount

Cr.

Cash a/c 9,000

Syarikat Bizara 17,000

To Balance c/d 26,000

26,000 26,000

Insurance Policy a/c

Amount

Dr.

Amount

Cr.

To Cash 9,600

Balance c/d 9,600

3,000 3,000

Utility Bills a/c

Amount

Dr.

Amount

Cr.

To Cash a/c 1,750

Balance c/d 1,750

1,750 1,750

Advance payment a/c

Amount Amount

Dr. Cr.

Cash 20,000

To Balance c/d 20,000

20,000 20,000

c) Trial Balance as at 30th September 2020

Trial Balance as at 30th September 2020

Amount Dr. Amount Cr.

Cash a/c 163,150

Office Equipment a/c 62,000

Capital 200,000

Sales 26,000

Insurance Policy 9,600

Drawings 6,500

Utility Bills 1,750

Advance payment 20,000

Office suppliers 3,000

246,000 246,000

Question 2

a)

Adjusting entries Amount (RM) Amount (RM)

Supplies expense a/c Dr.

To Revenue a/c

37,800

37,800

Depreciation a/c Dr.

To Accumulated dep. Motor vehicles a/c

36,900

36,900

Cash Dr.

To Unbilled revenue

15,975

15,975

Unearned revenue Dr.

To Revenue

32,400

32,400

Utility expense Dr.

To o/s expenses

400

400

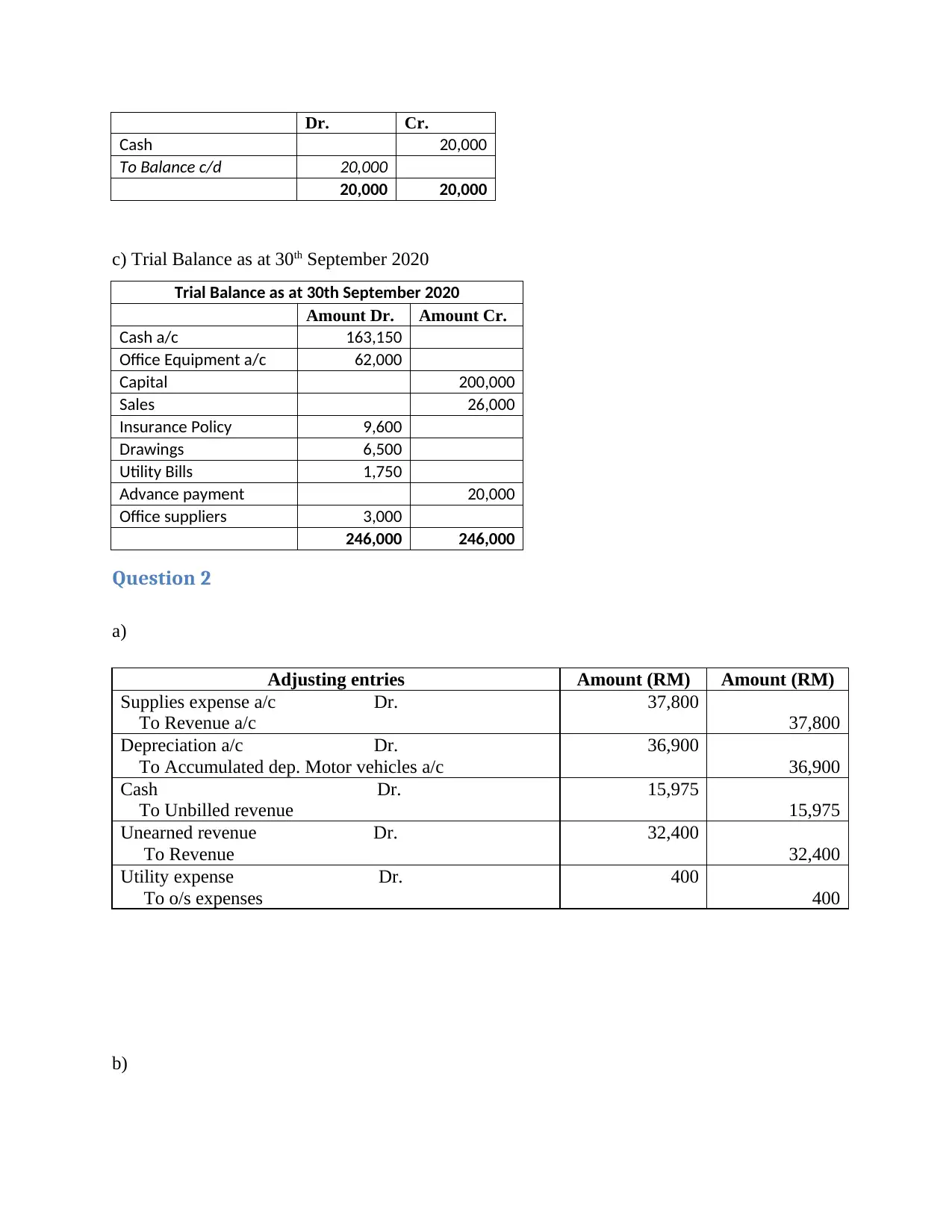

b)

Cash 20,000

To Balance c/d 20,000

20,000 20,000

c) Trial Balance as at 30th September 2020

Trial Balance as at 30th September 2020

Amount Dr. Amount Cr.

Cash a/c 163,150

Office Equipment a/c 62,000

Capital 200,000

Sales 26,000

Insurance Policy 9,600

Drawings 6,500

Utility Bills 1,750

Advance payment 20,000

Office suppliers 3,000

246,000 246,000

Question 2

a)

Adjusting entries Amount (RM) Amount (RM)

Supplies expense a/c Dr.

To Revenue a/c

37,800

37,800

Depreciation a/c Dr.

To Accumulated dep. Motor vehicles a/c

36,900

36,900

Cash Dr.

To Unbilled revenue

15,975

15,975

Unearned revenue Dr.

To Revenue

32,400

32,400

Utility expense Dr.

To o/s expenses

400

400

b)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

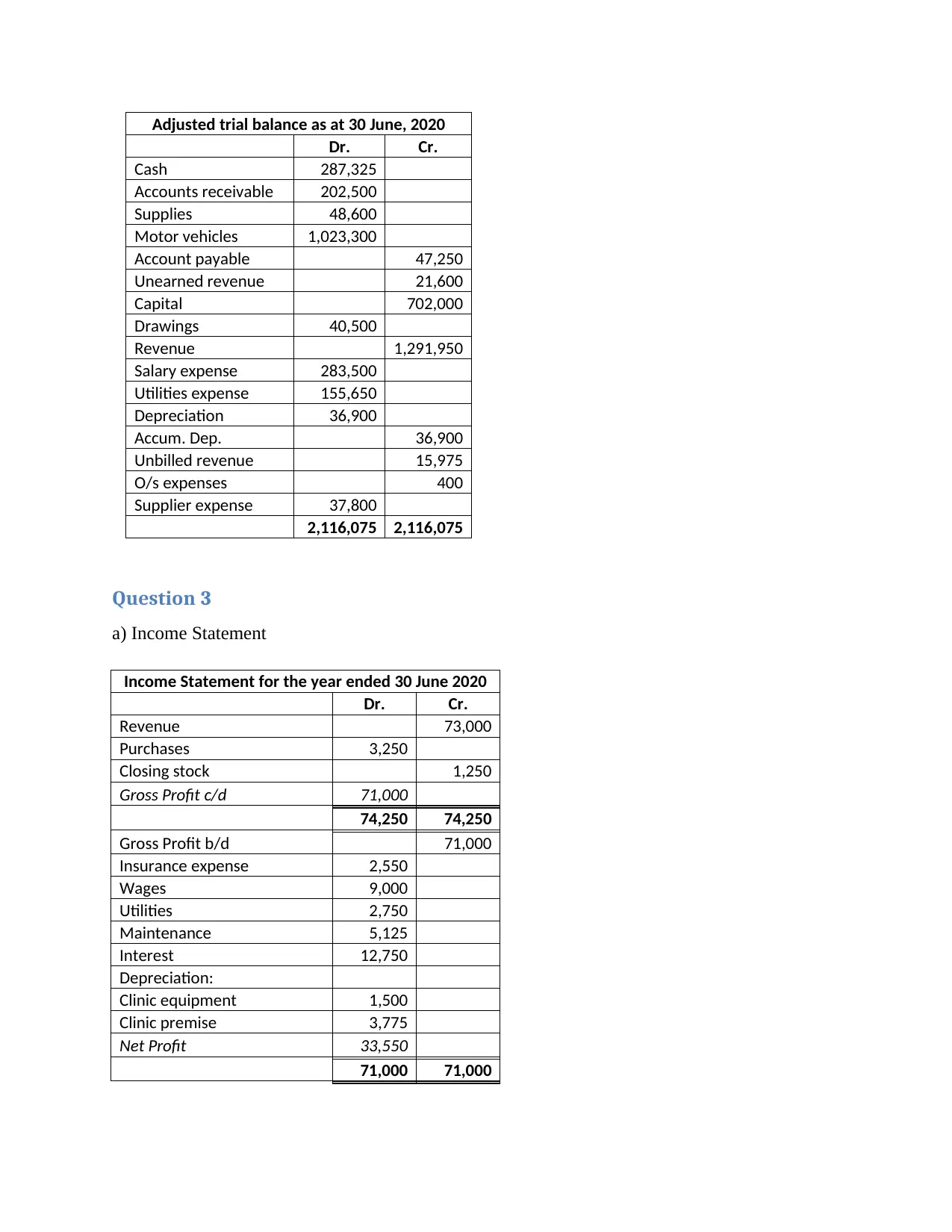

Adjusted trial balance as at 30 June, 2020

Dr. Cr.

Cash 287,325

Accounts receivable 202,500

Supplies 48,600

Motor vehicles 1,023,300

Account payable 47,250

Unearned revenue 21,600

Capital 702,000

Drawings 40,500

Revenue 1,291,950

Salary expense 283,500

Utilities expense 155,650

Depreciation 36,900

Accum. Dep. 36,900

Unbilled revenue 15,975

O/s expenses 400

Supplier expense 37,800

2,116,075 2,116,075

Question 3

a) Income Statement

Income Statement for the year ended 30 June 2020

Dr. Cr.

Revenue 73,000

Purchases 3,250

Closing stock 1,250

Gross Profit c/d 71,000

74,250 74,250

Gross Profit b/d 71,000

Insurance expense 2,550

Wages 9,000

Utilities 2,750

Maintenance 5,125

Interest 12,750

Depreciation:

Clinic equipment 1,500

Clinic premise 3,775

Net Profit 33,550

71,000 71,000

Dr. Cr.

Cash 287,325

Accounts receivable 202,500

Supplies 48,600

Motor vehicles 1,023,300

Account payable 47,250

Unearned revenue 21,600

Capital 702,000

Drawings 40,500

Revenue 1,291,950

Salary expense 283,500

Utilities expense 155,650

Depreciation 36,900

Accum. Dep. 36,900

Unbilled revenue 15,975

O/s expenses 400

Supplier expense 37,800

2,116,075 2,116,075

Question 3

a) Income Statement

Income Statement for the year ended 30 June 2020

Dr. Cr.

Revenue 73,000

Purchases 3,250

Closing stock 1,250

Gross Profit c/d 71,000

74,250 74,250

Gross Profit b/d 71,000

Insurance expense 2,550

Wages 9,000

Utilities 2,750

Maintenance 5,125

Interest 12,750

Depreciation:

Clinic equipment 1,500

Clinic premise 3,775

Net Profit 33,550

71,000 71,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Owner’s equity

Statement of owner's equity for the

year ended 30 June 2020

Capital

129,65

0

Retained earnings 32,300

Owner's equity

161,95

0

161,95

0

161,95

0

c) Balance sheet

Balance sheet as at 30 June 2020

Assets

Fixed Assets:

Clinic Equipment 10,650

Less: Accumulated Dep. 4,500 6,150

Clinic Premise

144,75

0

Less: Accumulated Dep. 14,375 130,375

Land 138,500

Total Fixed assets 275,025

Current Assets:

Cash 11,400

Accounts receivable 3,500

Stock 1,250

Prepaid Insurance 3,150

Total Current assets 19,300

Total Assets

294,32

5

Equity's and Liabilities

Total equity (Calculated) 161,950

Fixed Liabilities

Notes Payable 127,000

Current Liabilities:

Wages payable 2,625

Interest payable 2,750

Statement of owner's equity for the

year ended 30 June 2020

Capital

129,65

0

Retained earnings 32,300

Owner's equity

161,95

0

161,95

0

161,95

0

c) Balance sheet

Balance sheet as at 30 June 2020

Assets

Fixed Assets:

Clinic Equipment 10,650

Less: Accumulated Dep. 4,500 6,150

Clinic Premise

144,75

0

Less: Accumulated Dep. 14,375 130,375

Land 138,500

Total Fixed assets 275,025

Current Assets:

Cash 11,400

Accounts receivable 3,500

Stock 1,250

Prepaid Insurance 3,150

Total Current assets 19,300

Total Assets

294,32

5

Equity's and Liabilities

Total equity (Calculated) 161,950

Fixed Liabilities

Notes Payable 127,000

Current Liabilities:

Wages payable 2,625

Interest payable 2,750

Total Liabilities

294,32

5

294,32

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.