Financial Decision Making Report: Project Appraisal and Costing

VerifiedAdded on 2021/02/19

|7

|1674

|124

Report

AI Summary

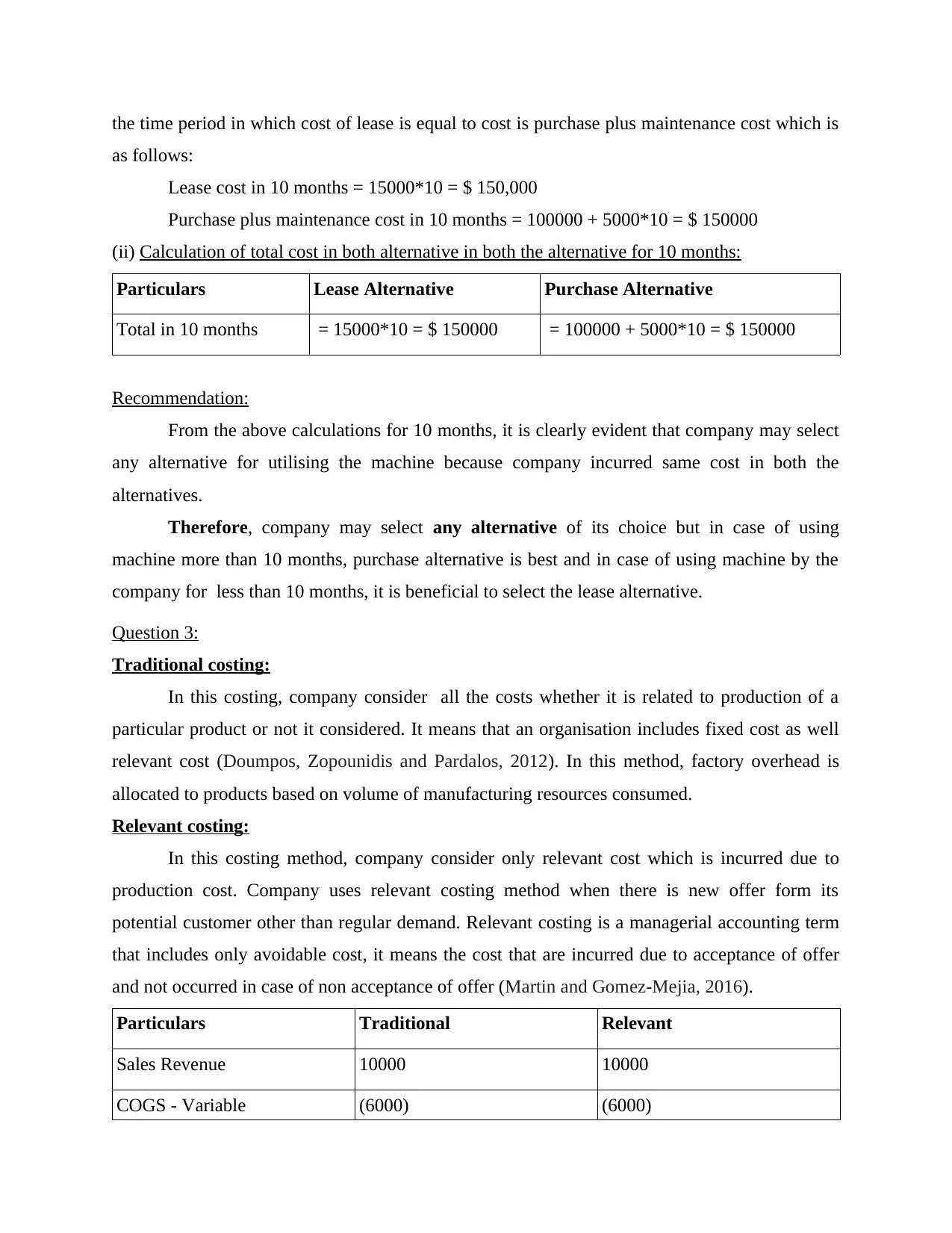

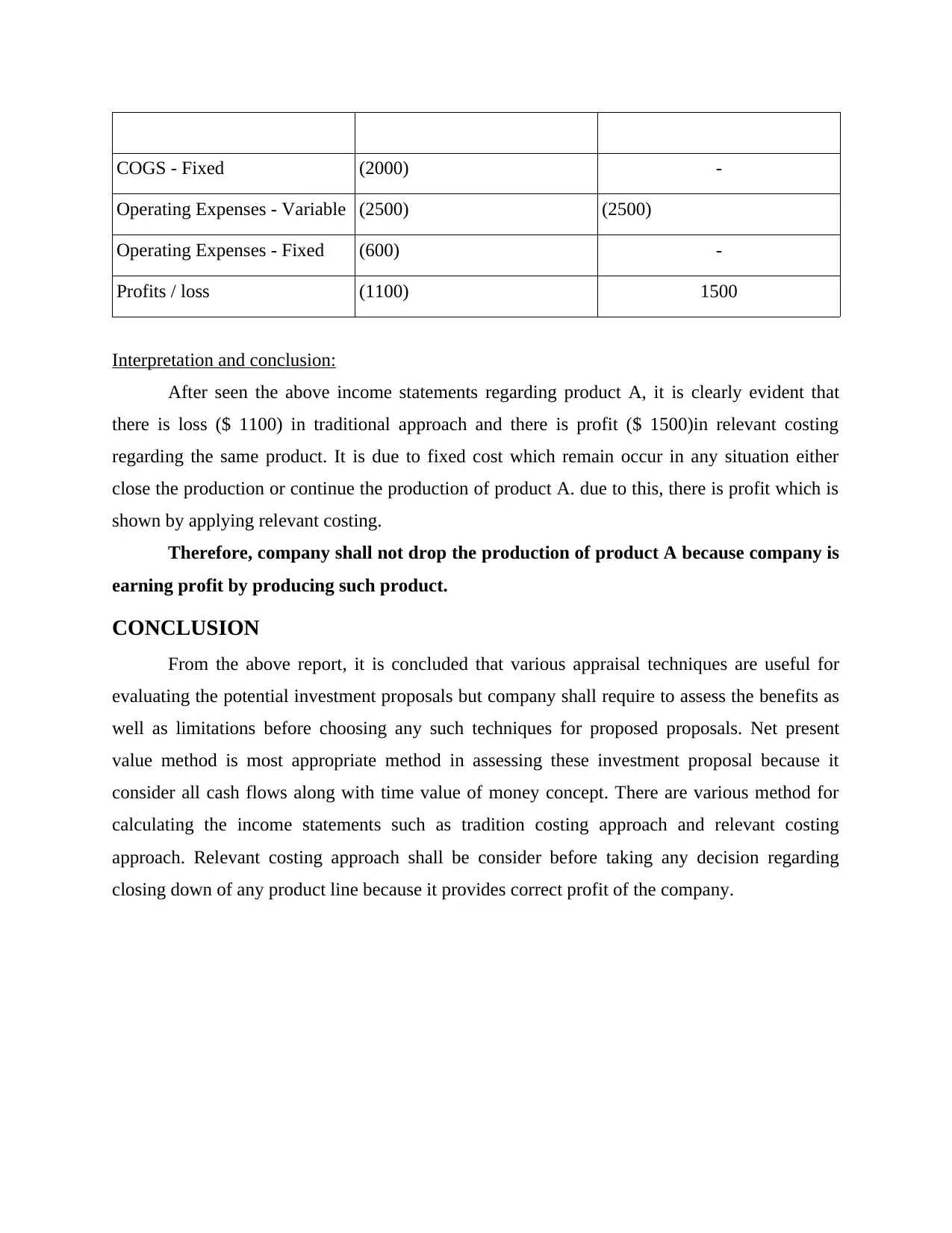

This report provides a comprehensive overview of financial decision-making processes. It delves into various project appraisal techniques, such as payback period, net present value (NPV), and internal rate of return (IRR), discussing their advantages and disadvantages. The report further analyzes a lease versus purchase decision, providing a numerical example to determine the optimal time frame for each option. Additionally, it explores the concepts of traditional costing and relevant costing, offering a comparative analysis with a numerical illustration to demonstrate their impact on profit calculation and decision-making. The conclusion emphasizes the importance of evaluating appraisal techniques and considering relevant costs for sound financial decisions.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.