Analyzing Investment Decisions and Financial Health via Ratio Analysis

VerifiedAdded on 2023/06/10

|10

|2559

|249

Case Study

AI Summary

This case study solution focuses on business finance, specifically investment appraisal and ratio analysis. The investment appraisal section evaluates a project's suitability using the payback period, net present value (NPV), and internal rate of return (IRR) methods, advising Jessica Ltd. on its investment decision. The financial ratio analysis calculates and interprets key ratios such as current ratio, quick ratio, debt-equity ratio, interest coverage ratio, stock turnover ratio, debtors turnover ratio, creditors turnover ratio, and net profit ratio for Omega Ltd., providing insights into the company's liquidity, solvency, efficiency, and profitability. Additionally, the study identifies and explains non-financial performance indicators like customer conversion rate, retention rate, customer satisfaction index, internal process efficiency, salary competitiveness ratio, and employee productivity rate. Finally, it evaluates the impact of Netflix's value-based pricing strategy on its brand value and profit margin. Desklib provides access to similar solved assignments and study tools for students.

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

MAIN BODY..................................................................................................................................3

2: A Case Study (a)..........................................................................................................................3

The Payback Period...........................................................................................................3

The Net Present Value.......................................................................................................3

The Internal Rate of Return...............................................................................................4

Advising on the suitability of the project....................................................................................4

(b).....................................................................................................................................................5

Calculating Ratios..............................................................................................................5

Identifying and Explaining the non-financial performance indicators..............................7

Evaluating the Impact of Pricing Strategy on the Performance of Netflix........................8

REFERENCES................................................................................................................................1

MAIN BODY..................................................................................................................................3

2: A Case Study (a)..........................................................................................................................3

The Payback Period...........................................................................................................3

The Net Present Value.......................................................................................................3

The Internal Rate of Return...............................................................................................4

Advising on the suitability of the project....................................................................................4

(b).....................................................................................................................................................5

Calculating Ratios..............................................................................................................5

Identifying and Explaining the non-financial performance indicators..............................7

Evaluating the Impact of Pricing Strategy on the Performance of Netflix........................8

REFERENCES................................................................................................................................1

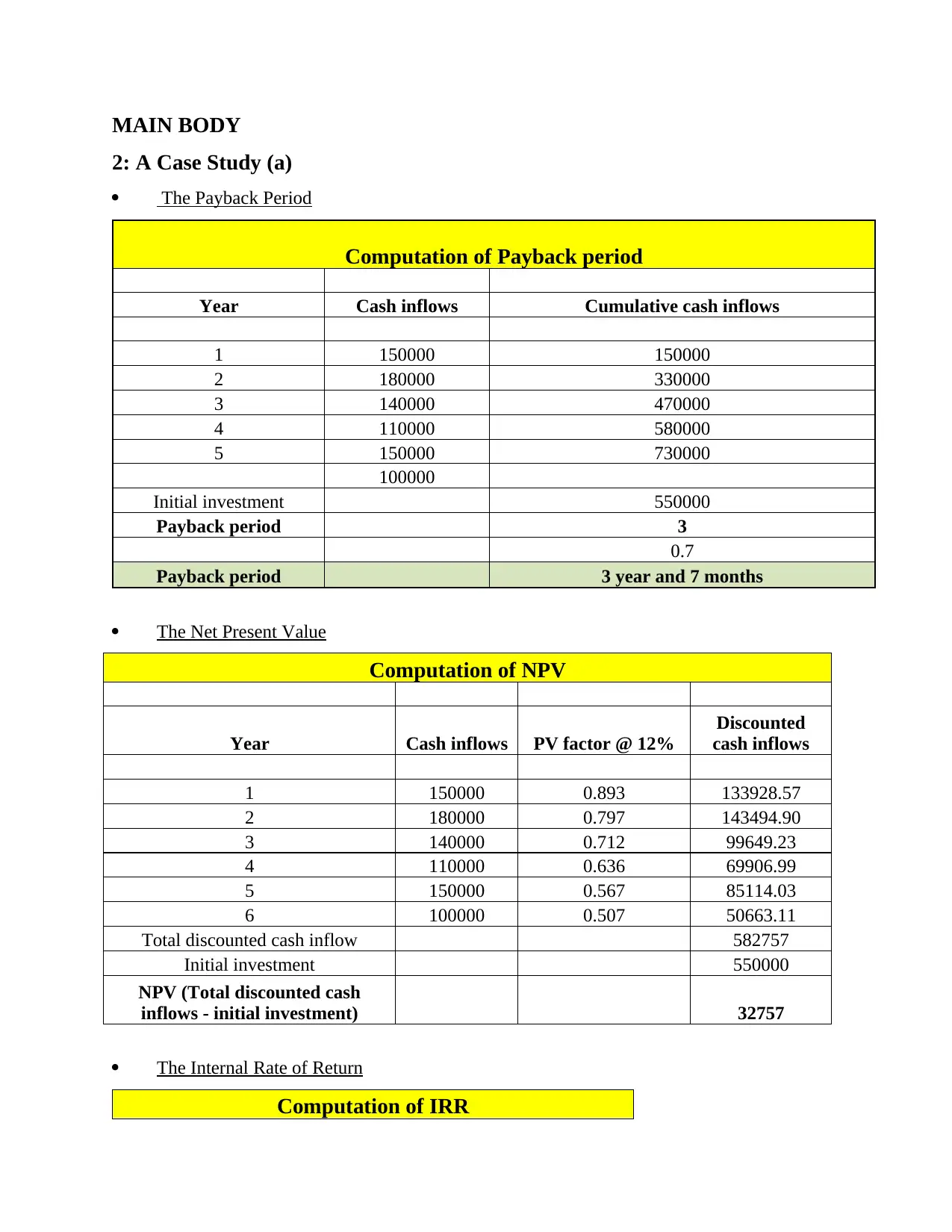

MAIN BODY

2: A Case Study (a)

The Payback Period

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 150000 150000

2 180000 330000

3 140000 470000

4 110000 580000

5 150000 730000

100000

Initial investment 550000

Payback period 3

0.7

Payback period 3 year and 7 months

The Net Present Value

Computation of NPV

Year Cash inflows PV factor @ 12%

Discounted

cash inflows

1 150000 0.893 133928.57

2 180000 0.797 143494.90

3 140000 0.712 99649.23

4 110000 0.636 69906.99

5 150000 0.567 85114.03

6 100000 0.507 50663.11

Total discounted cash inflow 582757

Initial investment 550000

NPV (Total discounted cash

inflows - initial investment) 32757

The Internal Rate of Return

Computation of IRR

2: A Case Study (a)

The Payback Period

Computation of Payback period

Year Cash inflows Cumulative cash inflows

1 150000 150000

2 180000 330000

3 140000 470000

4 110000 580000

5 150000 730000

100000

Initial investment 550000

Payback period 3

0.7

Payback period 3 year and 7 months

The Net Present Value

Computation of NPV

Year Cash inflows PV factor @ 12%

Discounted

cash inflows

1 150000 0.893 133928.57

2 180000 0.797 143494.90

3 140000 0.712 99649.23

4 110000 0.636 69906.99

5 150000 0.567 85114.03

6 100000 0.507 50663.11

Total discounted cash inflow 582757

Initial investment 550000

NPV (Total discounted cash

inflows - initial investment) 32757

The Internal Rate of Return

Computation of IRR

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Year Cash inflows

0 -550000

1 150000

2 180000

3 140000

4 110000

5 150000

6 100000

Internal rate of return (IRR) 14%

Advising on the suitability of the project

Analysing the suitability of project based on the three capital budgeting techniques

namely, payback period, net present value and internal rate of return. The payback period

calculation computes the period as 3 years 7 months. It means that the initial investment value of

£550,000 will be recovered by the company from the inflows the investment will generate in 3

years and 7 months. £470,000 will be covered from the returns in the three years and rest

£80,000 will be generated in the 4th year’s profits. The company will be able to reinvest the

initial amount in some other project after the payback period (Broomhead and et.al., 2021). The

net present value helps to select a project on the basis of the value that comes from its

computation. The time value of money means that the money is of more worth when received

earlier rather than on a future date. Net present value of the investment plan is £32,757; the result

is positive (Baum, Crosby and Devaney, 2021). The result is calculated by subtracting the initial

investment amount from the sum total of all the cash inflows over the life of project at the

discounted value. Result is positive it means that the discounted value or the present value of all

the future cash inflows is greater than the initial amount required to be invested. Lastly, the

project viability was computed through the IRR method of capital budgeting (Wijnen and et.al.,

2020). The IRR is the rate at which the net present value of the future benefits of the investment

is equal to the net present value of the initial cost. The rate at which the NPV becomes zero.

Internal Rate of Return is computed as 14%.

It is advisory for the Jessica Ltd to invest in the project as the net present value of the

investment is positive. The payback period is also good. The investment will cover its fixed cost

in the initial 3.7 years and afterwards the firm will start earning profits. Further the internal rate

0 -550000

1 150000

2 180000

3 140000

4 110000

5 150000

6 100000

Internal rate of return (IRR) 14%

Advising on the suitability of the project

Analysing the suitability of project based on the three capital budgeting techniques

namely, payback period, net present value and internal rate of return. The payback period

calculation computes the period as 3 years 7 months. It means that the initial investment value of

£550,000 will be recovered by the company from the inflows the investment will generate in 3

years and 7 months. £470,000 will be covered from the returns in the three years and rest

£80,000 will be generated in the 4th year’s profits. The company will be able to reinvest the

initial amount in some other project after the payback period (Broomhead and et.al., 2021). The

net present value helps to select a project on the basis of the value that comes from its

computation. The time value of money means that the money is of more worth when received

earlier rather than on a future date. Net present value of the investment plan is £32,757; the result

is positive (Baum, Crosby and Devaney, 2021). The result is calculated by subtracting the initial

investment amount from the sum total of all the cash inflows over the life of project at the

discounted value. Result is positive it means that the discounted value or the present value of all

the future cash inflows is greater than the initial amount required to be invested. Lastly, the

project viability was computed through the IRR method of capital budgeting (Wijnen and et.al.,

2020). The IRR is the rate at which the net present value of the future benefits of the investment

is equal to the net present value of the initial cost. The rate at which the NPV becomes zero.

Internal Rate of Return is computed as 14%.

It is advisory for the Jessica Ltd to invest in the project as the net present value of the

investment is positive. The payback period is also good. The investment will cover its fixed cost

in the initial 3.7 years and afterwards the firm will start earning profits. Further the internal rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of rate is also high. Higher the IRR better it is for the company. So based on these three

investment appraisal techniques it is advantageous for the firm to undertake its investment

decision.

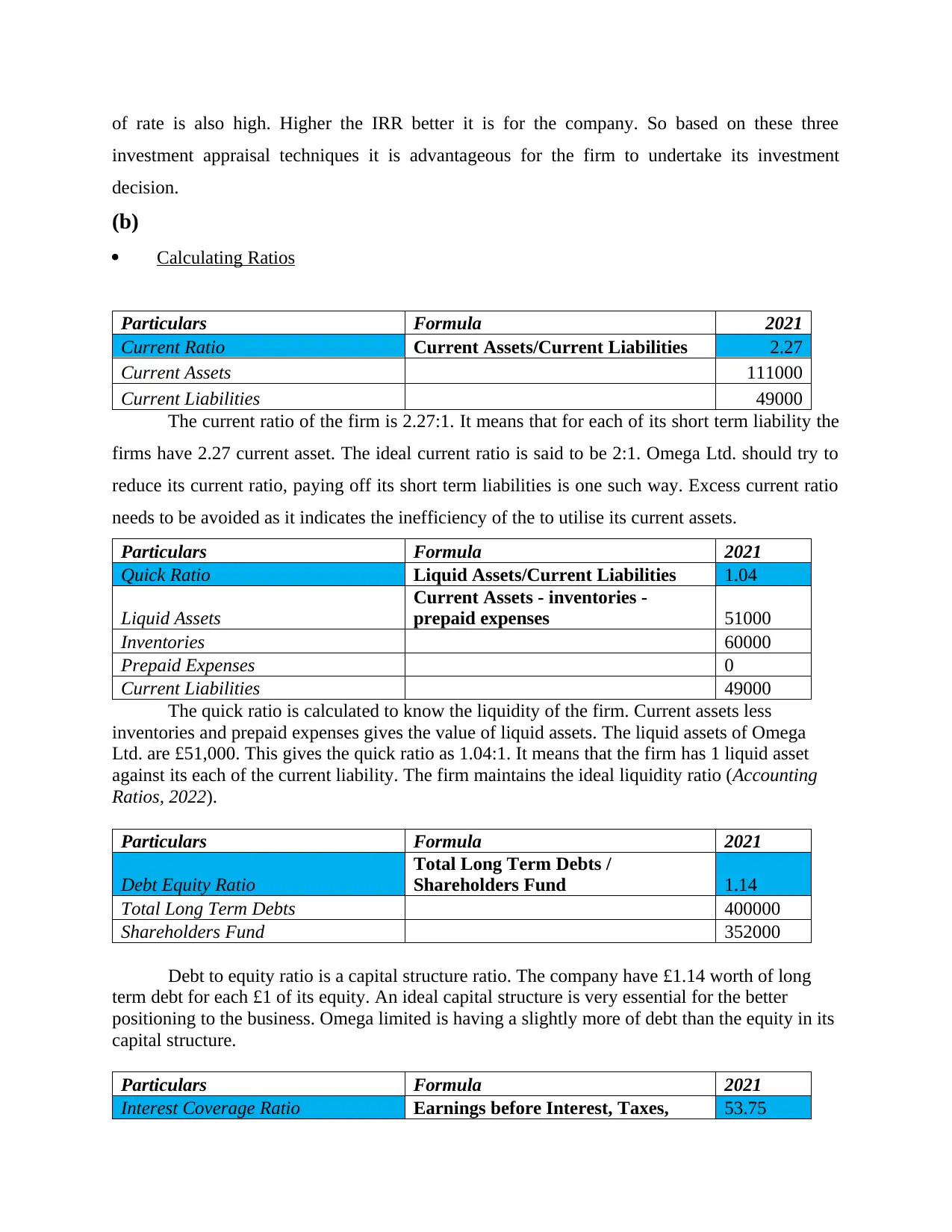

(b)

Calculating Ratios

Particulars Formula 2021

Current Ratio Current Assets/Current Liabilities 2.27

Current Assets 111000

Current Liabilities 49000

The current ratio of the firm is 2.27:1. It means that for each of its short term liability the

firms have 2.27 current asset. The ideal current ratio is said to be 2:1. Omega Ltd. should try to

reduce its current ratio, paying off its short term liabilities is one such way. Excess current ratio

needs to be avoided as it indicates the inefficiency of the to utilise its current assets.

Particulars Formula 2021

Quick Ratio Liquid Assets/Current Liabilities 1.04

Liquid Assets

Current Assets - inventories -

prepaid expenses 51000

Inventories 60000

Prepaid Expenses 0

Current Liabilities 49000

The quick ratio is calculated to know the liquidity of the firm. Current assets less

inventories and prepaid expenses gives the value of liquid assets. The liquid assets of Omega

Ltd. are £51,000. This gives the quick ratio as 1.04:1. It means that the firm has 1 liquid asset

against its each of the current liability. The firm maintains the ideal liquidity ratio (Accounting

Ratios, 2022).

Particulars Formula 2021

Debt Equity Ratio

Total Long Term Debts /

Shareholders Fund 1.14

Total Long Term Debts 400000

Shareholders Fund 352000

Debt to equity ratio is a capital structure ratio. The company have £1.14 worth of long

term debt for each £1 of its equity. An ideal capital structure is very essential for the better

positioning to the business. Omega limited is having a slightly more of debt than the equity in its

capital structure.

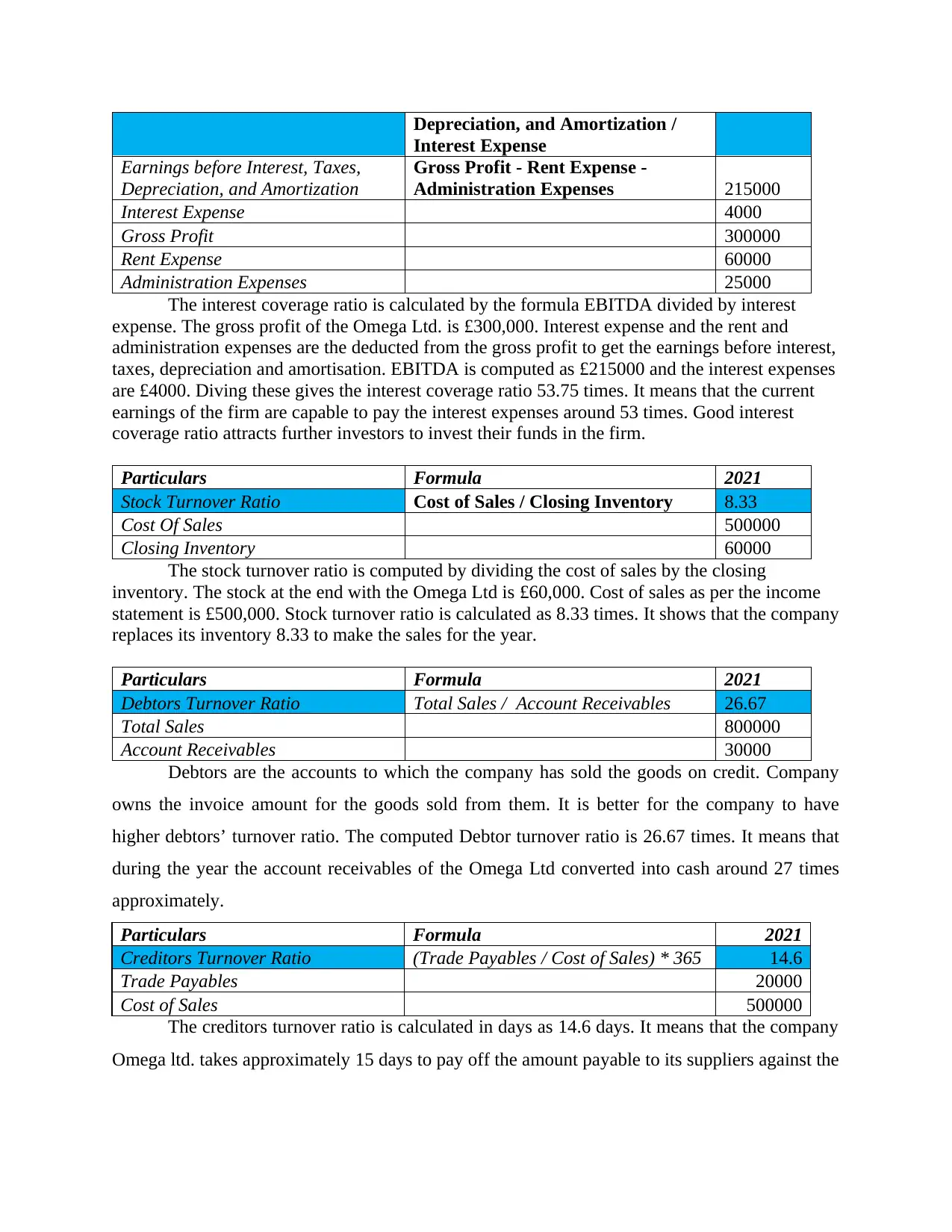

Particulars Formula 2021

Interest Coverage Ratio Earnings before Interest, Taxes, 53.75

investment appraisal techniques it is advantageous for the firm to undertake its investment

decision.

(b)

Calculating Ratios

Particulars Formula 2021

Current Ratio Current Assets/Current Liabilities 2.27

Current Assets 111000

Current Liabilities 49000

The current ratio of the firm is 2.27:1. It means that for each of its short term liability the

firms have 2.27 current asset. The ideal current ratio is said to be 2:1. Omega Ltd. should try to

reduce its current ratio, paying off its short term liabilities is one such way. Excess current ratio

needs to be avoided as it indicates the inefficiency of the to utilise its current assets.

Particulars Formula 2021

Quick Ratio Liquid Assets/Current Liabilities 1.04

Liquid Assets

Current Assets - inventories -

prepaid expenses 51000

Inventories 60000

Prepaid Expenses 0

Current Liabilities 49000

The quick ratio is calculated to know the liquidity of the firm. Current assets less

inventories and prepaid expenses gives the value of liquid assets. The liquid assets of Omega

Ltd. are £51,000. This gives the quick ratio as 1.04:1. It means that the firm has 1 liquid asset

against its each of the current liability. The firm maintains the ideal liquidity ratio (Accounting

Ratios, 2022).

Particulars Formula 2021

Debt Equity Ratio

Total Long Term Debts /

Shareholders Fund 1.14

Total Long Term Debts 400000

Shareholders Fund 352000

Debt to equity ratio is a capital structure ratio. The company have £1.14 worth of long

term debt for each £1 of its equity. An ideal capital structure is very essential for the better

positioning to the business. Omega limited is having a slightly more of debt than the equity in its

capital structure.

Particulars Formula 2021

Interest Coverage Ratio Earnings before Interest, Taxes, 53.75

Depreciation, and Amortization /

Interest Expense

Earnings before Interest, Taxes,

Depreciation, and Amortization

Gross Profit - Rent Expense -

Administration Expenses 215000

Interest Expense 4000

Gross Profit 300000

Rent Expense 60000

Administration Expenses 25000

The interest coverage ratio is calculated by the formula EBITDA divided by interest

expense. The gross profit of the Omega Ltd. is £300,000. Interest expense and the rent and

administration expenses are the deducted from the gross profit to get the earnings before interest,

taxes, depreciation and amortisation. EBITDA is computed as £215000 and the interest expenses

are £4000. Diving these gives the interest coverage ratio 53.75 times. It means that the current

earnings of the firm are capable to pay the interest expenses around 53 times. Good interest

coverage ratio attracts further investors to invest their funds in the firm.

Particulars Formula 2021

Stock Turnover Ratio Cost of Sales / Closing Inventory 8.33

Cost Of Sales 500000

Closing Inventory 60000

The stock turnover ratio is computed by dividing the cost of sales by the closing

inventory. The stock at the end with the Omega Ltd is £60,000. Cost of sales as per the income

statement is £500,000. Stock turnover ratio is calculated as 8.33 times. It shows that the company

replaces its inventory 8.33 to make the sales for the year.

Particulars Formula 2021

Debtors Turnover Ratio Total Sales / Account Receivables 26.67

Total Sales 800000

Account Receivables 30000

Debtors are the accounts to which the company has sold the goods on credit. Company

owns the invoice amount for the goods sold from them. It is better for the company to have

higher debtors’ turnover ratio. The computed Debtor turnover ratio is 26.67 times. It means that

during the year the account receivables of the Omega Ltd converted into cash around 27 times

approximately.

Particulars Formula 2021

Creditors Turnover Ratio (Trade Payables / Cost of Sales) * 365 14.6

Trade Payables 20000

Cost of Sales 500000

The creditors turnover ratio is calculated in days as 14.6 days. It means that the company

Omega ltd. takes approximately 15 days to pay off the amount payable to its suppliers against the

Interest Expense

Earnings before Interest, Taxes,

Depreciation, and Amortization

Gross Profit - Rent Expense -

Administration Expenses 215000

Interest Expense 4000

Gross Profit 300000

Rent Expense 60000

Administration Expenses 25000

The interest coverage ratio is calculated by the formula EBITDA divided by interest

expense. The gross profit of the Omega Ltd. is £300,000. Interest expense and the rent and

administration expenses are the deducted from the gross profit to get the earnings before interest,

taxes, depreciation and amortisation. EBITDA is computed as £215000 and the interest expenses

are £4000. Diving these gives the interest coverage ratio 53.75 times. It means that the current

earnings of the firm are capable to pay the interest expenses around 53 times. Good interest

coverage ratio attracts further investors to invest their funds in the firm.

Particulars Formula 2021

Stock Turnover Ratio Cost of Sales / Closing Inventory 8.33

Cost Of Sales 500000

Closing Inventory 60000

The stock turnover ratio is computed by dividing the cost of sales by the closing

inventory. The stock at the end with the Omega Ltd is £60,000. Cost of sales as per the income

statement is £500,000. Stock turnover ratio is calculated as 8.33 times. It shows that the company

replaces its inventory 8.33 to make the sales for the year.

Particulars Formula 2021

Debtors Turnover Ratio Total Sales / Account Receivables 26.67

Total Sales 800000

Account Receivables 30000

Debtors are the accounts to which the company has sold the goods on credit. Company

owns the invoice amount for the goods sold from them. It is better for the company to have

higher debtors’ turnover ratio. The computed Debtor turnover ratio is 26.67 times. It means that

during the year the account receivables of the Omega Ltd converted into cash around 27 times

approximately.

Particulars Formula 2021

Creditors Turnover Ratio (Trade Payables / Cost of Sales) * 365 14.6

Trade Payables 20000

Cost of Sales 500000

The creditors turnover ratio is calculated in days as 14.6 days. It means that the company

Omega ltd. takes approximately 15 days to pay off the amount payable to its suppliers against the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

goods purchased by the company on credit. Every firm tries to increase this ratio in number of

days. As more the duration available to pay for the creditors better it is for the business.

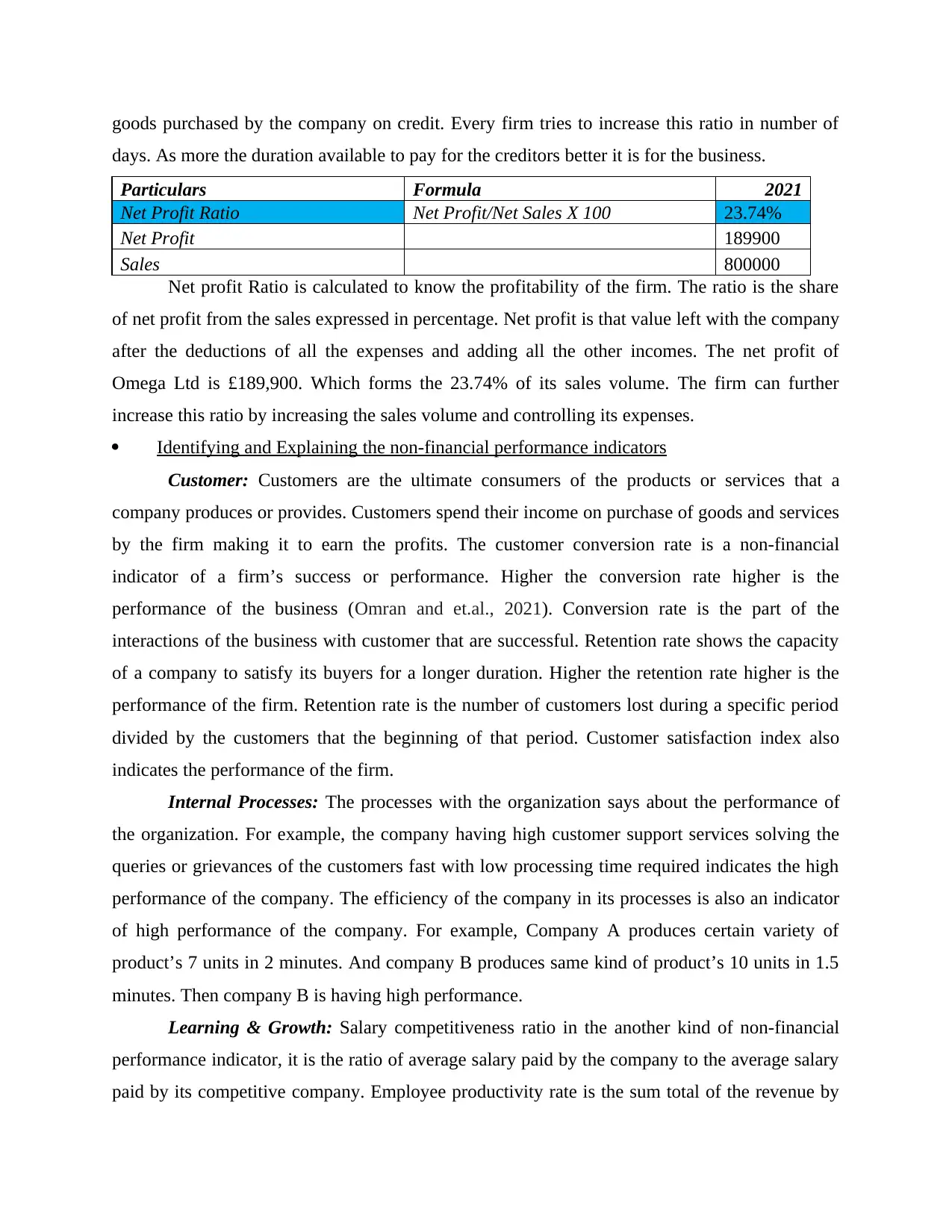

Particulars Formula 2021

Net Profit Ratio Net Profit/Net Sales X 100 23.74%

Net Profit 189900

Sales 800000

Net profit Ratio is calculated to know the profitability of the firm. The ratio is the share

of net profit from the sales expressed in percentage. Net profit is that value left with the company

after the deductions of all the expenses and adding all the other incomes. The net profit of

Omega Ltd is £189,900. Which forms the 23.74% of its sales volume. The firm can further

increase this ratio by increasing the sales volume and controlling its expenses.

Identifying and Explaining the non-financial performance indicators

Customer: Customers are the ultimate consumers of the products or services that a

company produces or provides. Customers spend their income on purchase of goods and services

by the firm making it to earn the profits. The customer conversion rate is a non-financial

indicator of a firm’s success or performance. Higher the conversion rate higher is the

performance of the business (Omran and et.al., 2021). Conversion rate is the part of the

interactions of the business with customer that are successful. Retention rate shows the capacity

of a company to satisfy its buyers for a longer duration. Higher the retention rate higher is the

performance of the firm. Retention rate is the number of customers lost during a specific period

divided by the customers that the beginning of that period. Customer satisfaction index also

indicates the performance of the firm.

Internal Processes: The processes with the organization says about the performance of

the organization. For example, the company having high customer support services solving the

queries or grievances of the customers fast with low processing time required indicates the high

performance of the company. The efficiency of the company in its processes is also an indicator

of high performance of the company. For example, Company A produces certain variety of

product’s 7 units in 2 minutes. And company B produces same kind of product’s 10 units in 1.5

minutes. Then company B is having high performance.

Learning & Growth: Salary competitiveness ratio in the another kind of non-financial

performance indicator, it is the ratio of average salary paid by the company to the average salary

paid by its competitive company. Employee productivity rate is the sum total of the revenue by

days. As more the duration available to pay for the creditors better it is for the business.

Particulars Formula 2021

Net Profit Ratio Net Profit/Net Sales X 100 23.74%

Net Profit 189900

Sales 800000

Net profit Ratio is calculated to know the profitability of the firm. The ratio is the share

of net profit from the sales expressed in percentage. Net profit is that value left with the company

after the deductions of all the expenses and adding all the other incomes. The net profit of

Omega Ltd is £189,900. Which forms the 23.74% of its sales volume. The firm can further

increase this ratio by increasing the sales volume and controlling its expenses.

Identifying and Explaining the non-financial performance indicators

Customer: Customers are the ultimate consumers of the products or services that a

company produces or provides. Customers spend their income on purchase of goods and services

by the firm making it to earn the profits. The customer conversion rate is a non-financial

indicator of a firm’s success or performance. Higher the conversion rate higher is the

performance of the business (Omran and et.al., 2021). Conversion rate is the part of the

interactions of the business with customer that are successful. Retention rate shows the capacity

of a company to satisfy its buyers for a longer duration. Higher the retention rate higher is the

performance of the firm. Retention rate is the number of customers lost during a specific period

divided by the customers that the beginning of that period. Customer satisfaction index also

indicates the performance of the firm.

Internal Processes: The processes with the organization says about the performance of

the organization. For example, the company having high customer support services solving the

queries or grievances of the customers fast with low processing time required indicates the high

performance of the company. The efficiency of the company in its processes is also an indicator

of high performance of the company. For example, Company A produces certain variety of

product’s 7 units in 2 minutes. And company B produces same kind of product’s 10 units in 1.5

minutes. Then company B is having high performance.

Learning & Growth: Salary competitiveness ratio in the another kind of non-financial

performance indicator, it is the ratio of average salary paid by the company to the average salary

paid by its competitive company. Employee productivity rate is the sum total of the revenue by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the company divided by the total number of employees (Mjongwana and Kamala, 2018). A high

value of salary competitiveness ratio and employee productivity rate indicates that the firm is a

high performing one. Turnover rate of the highest performer personnel in the company is less it

means that the company is performing well. The time taken by the company on an average to

hire new person at the place of the previous left, died, promoted or transferred employee is low

that means the performance of the company is reliable and good. These were some of the non-

financial indicators that are used or can be used to measure the performance of a firm.

Evaluating the Impact of Pricing Strategy on the Performance of Netflix

Value Based Pricing strategy is used by the Netflix. The meaning of value based pricing

strategy is that the price of the services that products offered by the company are based on the

value that is perceived by its customers. The pricing strategy is focussed on the customer and the

respective believes of the customers regarding the worth of the product. The strategy is used by

the company as the product offered by the company is highly differentiated from the products

that its competitors offers to the market (Cherla, Howard and Mossialos, 2021). Services

provided by the company are of high quality. Thus the pricing strategy is useful for the company.

The impacts of the value based pricing strategy on the company are the brand value of the

company increased largely because of its pricing strategy. Setting up of the price high instantly

increases the value of the brand. This increased brand value results in the high value

perseverance by the customers. The reason is that the high value creates the mind among the

customer that product is of higher quality. Impacting the company positively through better

brand value. Another impact of the value based pricing strategy is that the profit margin of the

company increases. It is assumed that the customers are ready to pay more for the services of the

company by the value based pricing strategy being followed. Setting up of prices higher

ultimately linked with the high customer perceived value means that the profits earnings of the

company increases imposing a positive impact. The negative impact of this pricing strategy over

the company is that by selling the products or services at the highest possible price requires the

providence of higher quality products (Kumar and Sun, 2020). Thus the production cost

increases. Another negative impact that the firm faces is the high level of increasing competition

in the industry. Thus the pricing strategy have both weaknesses and strengths.

value of salary competitiveness ratio and employee productivity rate indicates that the firm is a

high performing one. Turnover rate of the highest performer personnel in the company is less it

means that the company is performing well. The time taken by the company on an average to

hire new person at the place of the previous left, died, promoted or transferred employee is low

that means the performance of the company is reliable and good. These were some of the non-

financial indicators that are used or can be used to measure the performance of a firm.

Evaluating the Impact of Pricing Strategy on the Performance of Netflix

Value Based Pricing strategy is used by the Netflix. The meaning of value based pricing

strategy is that the price of the services that products offered by the company are based on the

value that is perceived by its customers. The pricing strategy is focussed on the customer and the

respective believes of the customers regarding the worth of the product. The strategy is used by

the company as the product offered by the company is highly differentiated from the products

that its competitors offers to the market (Cherla, Howard and Mossialos, 2021). Services

provided by the company are of high quality. Thus the pricing strategy is useful for the company.

The impacts of the value based pricing strategy on the company are the brand value of the

company increased largely because of its pricing strategy. Setting up of the price high instantly

increases the value of the brand. This increased brand value results in the high value

perseverance by the customers. The reason is that the high value creates the mind among the

customer that product is of higher quality. Impacting the company positively through better

brand value. Another impact of the value based pricing strategy is that the profit margin of the

company increases. It is assumed that the customers are ready to pay more for the services of the

company by the value based pricing strategy being followed. Setting up of prices higher

ultimately linked with the high customer perceived value means that the profits earnings of the

company increases imposing a positive impact. The negative impact of this pricing strategy over

the company is that by selling the products or services at the highest possible price requires the

providence of higher quality products (Kumar and Sun, 2020). Thus the production cost

increases. Another negative impact that the firm faces is the high level of increasing competition

in the industry. Thus the pricing strategy have both weaknesses and strengths.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Broomhead, S. C. and et.al., 2021. EHealth Investment Appraisal in Africa: A Scoping

Review. INQUIRY: The Journal of Health Care Organization, Provision, and

Financing. 58. p.00469580211059999.

Cherla, A., Howard, N. and Mossialos, E., 2021. The ‘Netflix plus model’: can subscription

financing improve access to medicines in low-and middle-income countries?. Health

Economics, Policy and Law. 16(2). pp.113-123.

Kumar, V. and Sun, Y., 2020. Designing Pricing Strategy for Operational and Technological

Transformation. Management Science. 66(6). pp.2706-2734.

Mjongwana, A. and Kamala, P. N., 2018. Non-financial performance measurement by small and

medium sized enterprises operating in the hotel industry in the city of Cape

Town. African Journal of Hospitality, Tourism and Leisure. 7(1). pp.1-26.

Omran, M. and et.al., 2021. Non-financial performance measures disclosure, quality strategy,

and organizational financial performance: a mediating model. Total Quality Management

& Business Excellence, 32(5-6), pp.652-675.

Wijnen, B. F. and et.al., 2020. Implementing interventions to reduce work-related stress among

health-care workers: An investment appraisal from the employer’s

perspective. International Archives of Occupational and Environmental Health. 93(1).

pp.123-132.

Online

Accounting Ratios. 2022. [Online]. Available through: <

https://corporatefinanceinstitute.com/resources/knowledge/accounting/accounting-

ratios/>

1

Books and Journals

Baum, A. E., Crosby, N. and Devaney, S., 2021. Property investment appraisal. John Wiley &

Sons.

Broomhead, S. C. and et.al., 2021. EHealth Investment Appraisal in Africa: A Scoping

Review. INQUIRY: The Journal of Health Care Organization, Provision, and

Financing. 58. p.00469580211059999.

Cherla, A., Howard, N. and Mossialos, E., 2021. The ‘Netflix plus model’: can subscription

financing improve access to medicines in low-and middle-income countries?. Health

Economics, Policy and Law. 16(2). pp.113-123.

Kumar, V. and Sun, Y., 2020. Designing Pricing Strategy for Operational and Technological

Transformation. Management Science. 66(6). pp.2706-2734.

Mjongwana, A. and Kamala, P. N., 2018. Non-financial performance measurement by small and

medium sized enterprises operating in the hotel industry in the city of Cape

Town. African Journal of Hospitality, Tourism and Leisure. 7(1). pp.1-26.

Omran, M. and et.al., 2021. Non-financial performance measures disclosure, quality strategy,

and organizational financial performance: a mediating model. Total Quality Management

& Business Excellence, 32(5-6), pp.652-675.

Wijnen, B. F. and et.al., 2020. Implementing interventions to reduce work-related stress among

health-care workers: An investment appraisal from the employer’s

perspective. International Archives of Occupational and Environmental Health. 93(1).

pp.123-132.

Online

Accounting Ratios. 2022. [Online]. Available through: <

https://corporatefinanceinstitute.com/resources/knowledge/accounting/accounting-

ratios/>

1

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.