BUSM4617 Project Finance: APWater Project Finance Scheme Analysis

VerifiedAdded on 2023/06/10

|10

|1963

|428

Case Study

AI Summary

This case study analyzes the financial viability of the APWater project using various financial metrics such as IRR, Equity IRR, Debt-Service Coverage Ratio, CAPM, and WACC. The report evaluates three off-take agreements (CallWater, APWater, and NuWater) to determine the most suitable project for ABC Pty Ltd's special purpose vehicle. Through detailed calculations and analysis, the report recommends the APWater agreement due to its higher present value and IRR. The study also includes recommendations for improving cost expenditure. Desklib offers a wide range of solved assignments and project finance resources for students.

Project Finance Case

Study

Study

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The below report summarises that the Project B of APWater limited should be selected

by the ABC Pty Ltd. The report is formed for the special purpose vehicle (SPV) which has been

unified in Australia. The project can be selected by using the capital expenditure, cash inflows

and cash outflows.

The below report summarises that the Project B of APWater limited should be selected

by the ABC Pty Ltd. The report is formed for the special purpose vehicle (SPV) which has been

unified in Australia. The project can be selected by using the capital expenditure, cash inflows

and cash outflows.

Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

METHODOLOGY..........................................................................................................................4

DISCUSSION..................................................................................................................................4

Calculate the project IRR.............................................................................................................4

Calculate the Equity IRR.............................................................................................................5

Calculate Debt – service coverage ratio......................................................................................5

Calculate Expected return using the CAPM model.....................................................................6

Calculate WACC.........................................................................................................................7

Should the project go ahead using a project finance scheme? Give reasons...............................7

CONCLUSION................................................................................................................................7

RECOMMENDATIONS.................................................................................................................8

REFERENCES................................................................................................................................9

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION...........................................................................................................................4

METHODOLOGY..........................................................................................................................4

DISCUSSION..................................................................................................................................4

Calculate the project IRR.............................................................................................................4

Calculate the Equity IRR.............................................................................................................5

Calculate Debt – service coverage ratio......................................................................................5

Calculate Expected return using the CAPM model.....................................................................6

Calculate WACC.........................................................................................................................7

Should the project go ahead using a project finance scheme? Give reasons...............................7

CONCLUSION................................................................................................................................7

RECOMMENDATIONS.................................................................................................................8

REFERENCES................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Project Finance is the term that is widely used for projecting the cash flow of the company.

In this, the capital expenditure, cash inflows, and outflow are determined on the basis of the

return the company is getting. It helps in building the financial structure of the company by

enforcing the agreements. It is a very capital intensive project which helps in generating the

project as a source of funds for repaying the dues (Harvey, 2020). In the accompanying report,

ABC Pty Ltd is an organisation whose purpose is to form a special purpose vehicle (SPV) that

has to be incorporated in Australia. For this, the company has signed three different agreements

for supplying the treated water. The following report is prepared for finding out the IRR of the

project, Equity IRR, CAPM, WACC, debt – service coverage ratio. Moreover, at the end of the

report, the project which the company should select for financing is to be determined on the basis

of the certain computation that will be performed.

METHODOLOGY

The methodology that has been used for completing the purpose of the project is quantitative

secondary research. The data is collected through the secondary data collection method. The

economic parameters that are used in the report is internal rate of return, capital asset pricing

model. The weighted average cost of capital, and debt – service coverage ratios is computed.

DISCUSSION

Calculate the project IRR.

A matrix used to estimate the probability of potential investments in financial analysis is

termed an Internal rate of return (IRR). IRR is a discounted rate and in a discounted cash analysis

it makes the NPV of the multitude of incomes equivalent to nothing. It is the yearly pace of

development that a financial investor hopes to produce. Positioning different speculations or

projects can be utilized. When an investment option is being compared with others the one with

the highest IRR would be considered as the best option probably. It understands and compares

potential rates of annual return and is ideal for analyzing capital budgeting projects. The

calculation of IRR cannot be done easily it can only be done by using the trial and error method.

It focuses on the identification of the rate of discount. Despite having several methods to

identify, IRR is the ideal method for analyzing the potential return of the project.

Project Finance is the term that is widely used for projecting the cash flow of the company.

In this, the capital expenditure, cash inflows, and outflow are determined on the basis of the

return the company is getting. It helps in building the financial structure of the company by

enforcing the agreements. It is a very capital intensive project which helps in generating the

project as a source of funds for repaying the dues (Harvey, 2020). In the accompanying report,

ABC Pty Ltd is an organisation whose purpose is to form a special purpose vehicle (SPV) that

has to be incorporated in Australia. For this, the company has signed three different agreements

for supplying the treated water. The following report is prepared for finding out the IRR of the

project, Equity IRR, CAPM, WACC, debt – service coverage ratio. Moreover, at the end of the

report, the project which the company should select for financing is to be determined on the basis

of the certain computation that will be performed.

METHODOLOGY

The methodology that has been used for completing the purpose of the project is quantitative

secondary research. The data is collected through the secondary data collection method. The

economic parameters that are used in the report is internal rate of return, capital asset pricing

model. The weighted average cost of capital, and debt – service coverage ratios is computed.

DISCUSSION

Calculate the project IRR.

A matrix used to estimate the probability of potential investments in financial analysis is

termed an Internal rate of return (IRR). IRR is a discounted rate and in a discounted cash analysis

it makes the NPV of the multitude of incomes equivalent to nothing. It is the yearly pace of

development that a financial investor hopes to produce. Positioning different speculations or

projects can be utilized. When an investment option is being compared with others the one with

the highest IRR would be considered as the best option probably. It understands and compares

potential rates of annual return and is ideal for analyzing capital budgeting projects. The

calculation of IRR cannot be done easily it can only be done by using the trial and error method.

It focuses on the identification of the rate of discount. Despite having several methods to

identify, IRR is the ideal method for analyzing the potential return of the project.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

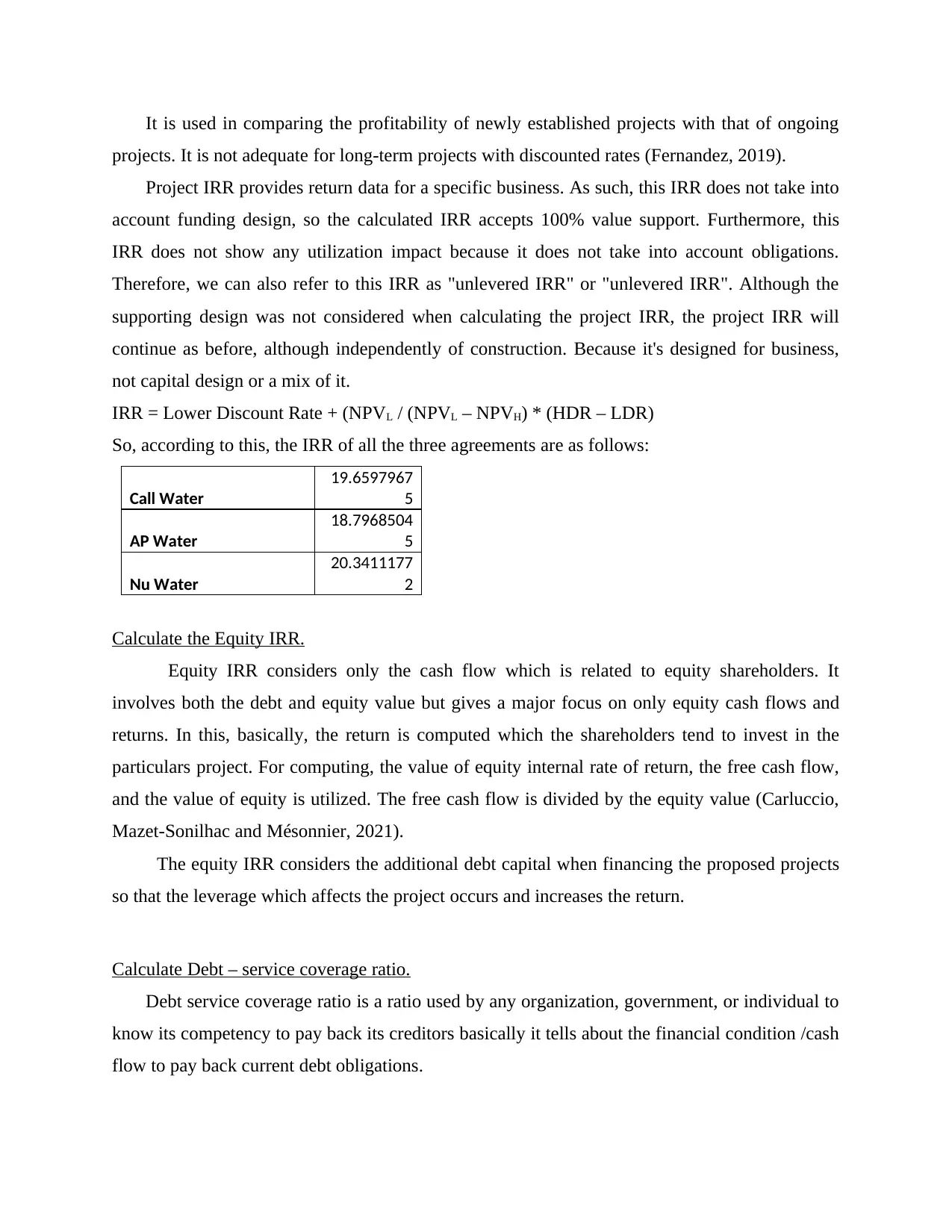

It is used in comparing the profitability of newly established projects with that of ongoing

projects. It is not adequate for long-term projects with discounted rates (Fernandez, 2019).

Project IRR provides return data for a specific business. As such, this IRR does not take into

account funding design, so the calculated IRR accepts 100% value support. Furthermore, this

IRR does not show any utilization impact because it does not take into account obligations.

Therefore, we can also refer to this IRR as "unlevered IRR" or "unlevered IRR". Although the

supporting design was not considered when calculating the project IRR, the project IRR will

continue as before, although independently of construction. Because it's designed for business,

not capital design or a mix of it.

IRR = Lower Discount Rate + (NPVL / (NPVL – NPVH) * (HDR – LDR)

So, according to this, the IRR of all the three agreements are as follows:

Call Water

19.6597967

5

AP Water

18.7968504

5

Nu Water

20.3411177

2

Calculate the Equity IRR.

Equity IRR considers only the cash flow which is related to equity shareholders. It

involves both the debt and equity value but gives a major focus on only equity cash flows and

returns. In this, basically, the return is computed which the shareholders tend to invest in the

particulars project. For computing, the value of equity internal rate of return, the free cash flow,

and the value of equity is utilized. The free cash flow is divided by the equity value (Carluccio,

Mazet-Sonilhac and Mésonnier, 2021).

The equity IRR considers the additional debt capital when financing the proposed projects

so that the leverage which affects the project occurs and increases the return.

Calculate Debt – service coverage ratio.

Debt service coverage ratio is a ratio used by any organization, government, or individual to

know its competency to pay back its creditors basically it tells about the financial condition /cash

flow to pay back current debt obligations.

projects. It is not adequate for long-term projects with discounted rates (Fernandez, 2019).

Project IRR provides return data for a specific business. As such, this IRR does not take into

account funding design, so the calculated IRR accepts 100% value support. Furthermore, this

IRR does not show any utilization impact because it does not take into account obligations.

Therefore, we can also refer to this IRR as "unlevered IRR" or "unlevered IRR". Although the

supporting design was not considered when calculating the project IRR, the project IRR will

continue as before, although independently of construction. Because it's designed for business,

not capital design or a mix of it.

IRR = Lower Discount Rate + (NPVL / (NPVL – NPVH) * (HDR – LDR)

So, according to this, the IRR of all the three agreements are as follows:

Call Water

19.6597967

5

AP Water

18.7968504

5

Nu Water

20.3411177

2

Calculate the Equity IRR.

Equity IRR considers only the cash flow which is related to equity shareholders. It

involves both the debt and equity value but gives a major focus on only equity cash flows and

returns. In this, basically, the return is computed which the shareholders tend to invest in the

particulars project. For computing, the value of equity internal rate of return, the free cash flow,

and the value of equity is utilized. The free cash flow is divided by the equity value (Carluccio,

Mazet-Sonilhac and Mésonnier, 2021).

The equity IRR considers the additional debt capital when financing the proposed projects

so that the leverage which affects the project occurs and increases the return.

Calculate Debt – service coverage ratio.

Debt service coverage ratio is a ratio used by any organization, government, or individual to

know its competency to pay back its creditors basically it tells about the financial condition /cash

flow to pay back current debt obligations.

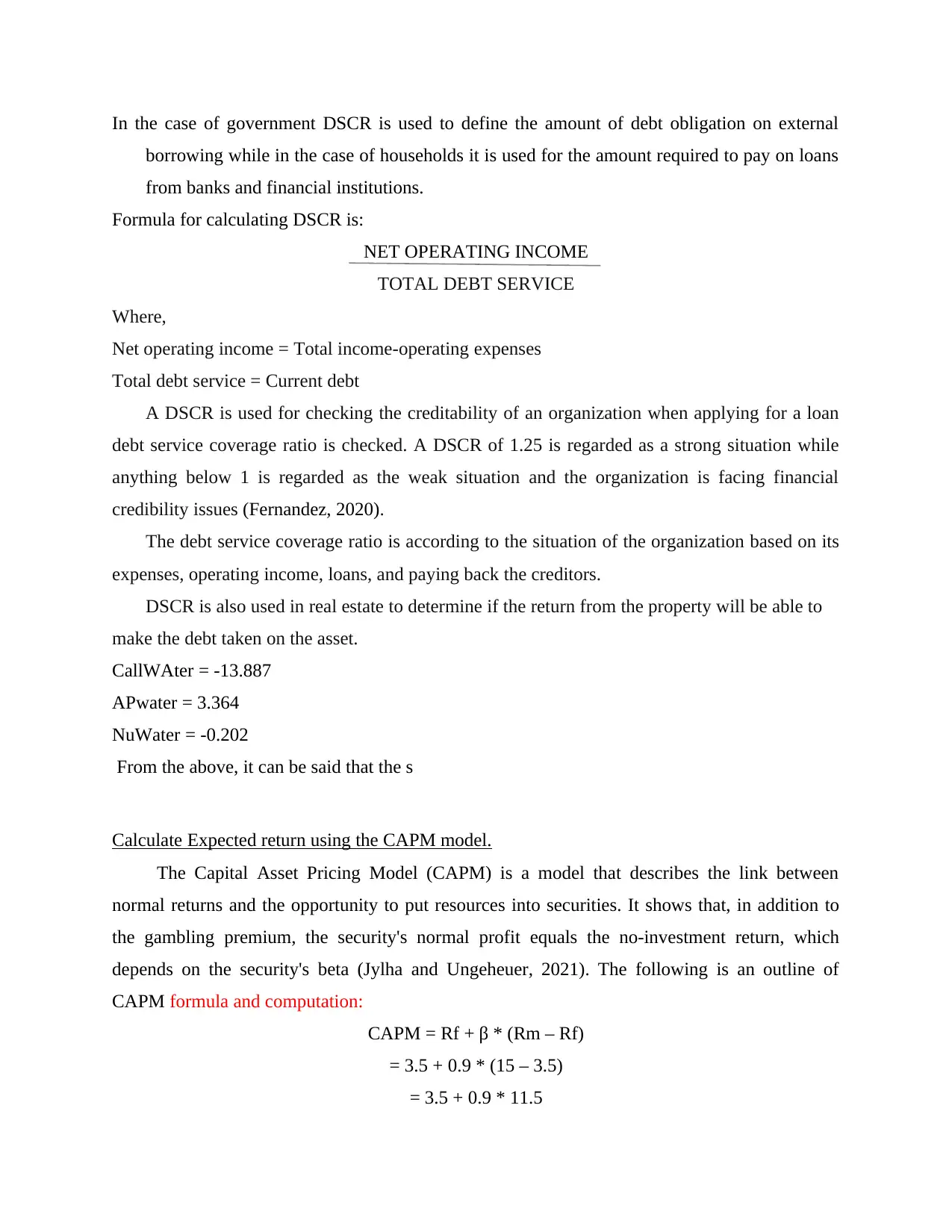

In the case of government DSCR is used to define the amount of debt obligation on external

borrowing while in the case of households it is used for the amount required to pay on loans

from banks and financial institutions.

Formula for calculating DSCR is:

NET OPERATING INCOME

TOTAL DEBT SERVICE

Where,

Net operating income = Total income-operating expenses

Total debt service = Current debt

A DSCR is used for checking the creditability of an organization when applying for a loan

debt service coverage ratio is checked. A DSCR of 1.25 is regarded as a strong situation while

anything below 1 is regarded as the weak situation and the organization is facing financial

credibility issues (Fernandez, 2020).

The debt service coverage ratio is according to the situation of the organization based on its

expenses, operating income, loans, and paying back the creditors.

DSCR is also used in real estate to determine if the return from the property will be able to

make the debt taken on the asset.

CallWAter = -13.887

APwater = 3.364

NuWater = -0.202

From the above, it can be said that the s

Calculate Expected return using the CAPM model.

The Capital Asset Pricing Model (CAPM) is a model that describes the link between

normal returns and the opportunity to put resources into securities. It shows that, in addition to

the gambling premium, the security's normal profit equals the no-investment return, which

depends on the security's beta (Jylha and Ungeheuer, 2021). The following is an outline of

CAPM formula and computation:

CAPM = Rf + β * (Rm – Rf)

= 3.5 + 0.9 * (15 – 3.5)

= 3.5 + 0.9 * 11.5

borrowing while in the case of households it is used for the amount required to pay on loans

from banks and financial institutions.

Formula for calculating DSCR is:

NET OPERATING INCOME

TOTAL DEBT SERVICE

Where,

Net operating income = Total income-operating expenses

Total debt service = Current debt

A DSCR is used for checking the creditability of an organization when applying for a loan

debt service coverage ratio is checked. A DSCR of 1.25 is regarded as a strong situation while

anything below 1 is regarded as the weak situation and the organization is facing financial

credibility issues (Fernandez, 2020).

The debt service coverage ratio is according to the situation of the organization based on its

expenses, operating income, loans, and paying back the creditors.

DSCR is also used in real estate to determine if the return from the property will be able to

make the debt taken on the asset.

CallWAter = -13.887

APwater = 3.364

NuWater = -0.202

From the above, it can be said that the s

Calculate Expected return using the CAPM model.

The Capital Asset Pricing Model (CAPM) is a model that describes the link between

normal returns and the opportunity to put resources into securities. It shows that, in addition to

the gambling premium, the security's normal profit equals the no-investment return, which

depends on the security's beta (Jylha and Ungeheuer, 2021). The following is an outline of

CAPM formula and computation:

CAPM = Rf + β * (Rm – Rf)

= 3.5 + 0.9 * (15 – 3.5)

= 3.5 + 0.9 * 11.5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

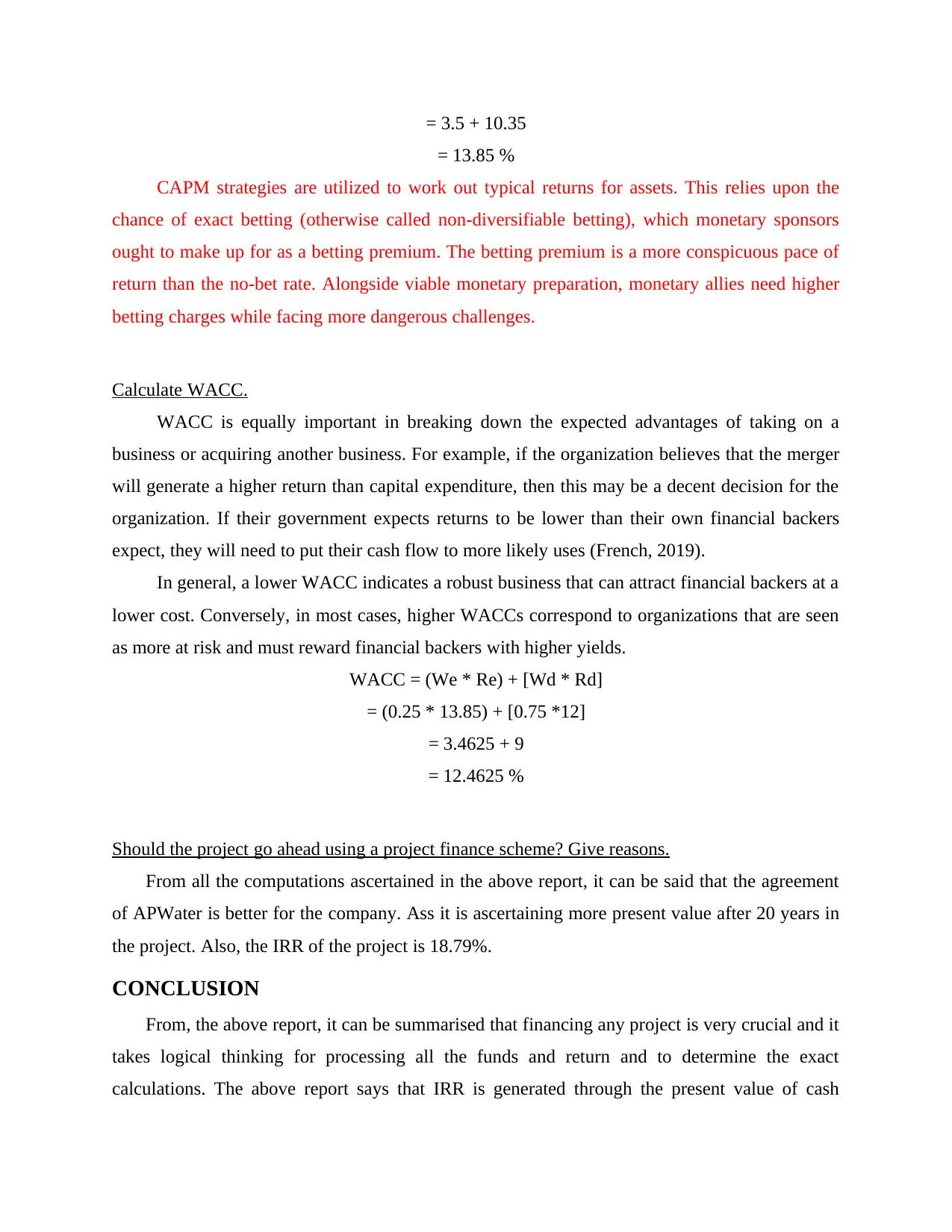

= 3.5 + 10.35

= 13.85 %

CAPM strategies are utilized to work out typical returns for assets. This relies upon the

chance of exact betting (otherwise called non-diversifiable betting), which monetary sponsors

ought to make up for as a betting premium. The betting premium is a more conspicuous pace of

return than the no-bet rate. Alongside viable monetary preparation, monetary allies need higher

betting charges while facing more dangerous challenges.

Calculate WACC.

WACC is equally important in breaking down the expected advantages of taking on a

business or acquiring another business. For example, if the organization believes that the merger

will generate a higher return than capital expenditure, then this may be a decent decision for the

organization. If their government expects returns to be lower than their own financial backers

expect, they will need to put their cash flow to more likely uses (French, 2019).

In general, a lower WACC indicates a robust business that can attract financial backers at a

lower cost. Conversely, in most cases, higher WACCs correspond to organizations that are seen

as more at risk and must reward financial backers with higher yields.

WACC = (We * Re) + [Wd * Rd]

= (0.25 * 13.85) + [0.75 *12]

= 3.4625 + 9

= 12.4625 %

Should the project go ahead using a project finance scheme? Give reasons.

From all the computations ascertained in the above report, it can be said that the agreement

of APWater is better for the company. Ass it is ascertaining more present value after 20 years in

the project. Also, the IRR of the project is 18.79%.

CONCLUSION

From, the above report, it can be summarised that financing any project is very crucial and it

takes logical thinking for processing all the funds and return and to determine the exact

calculations. The above report says that IRR is generated through the present value of cash

= 13.85 %

CAPM strategies are utilized to work out typical returns for assets. This relies upon the

chance of exact betting (otherwise called non-diversifiable betting), which monetary sponsors

ought to make up for as a betting premium. The betting premium is a more conspicuous pace of

return than the no-bet rate. Alongside viable monetary preparation, monetary allies need higher

betting charges while facing more dangerous challenges.

Calculate WACC.

WACC is equally important in breaking down the expected advantages of taking on a

business or acquiring another business. For example, if the organization believes that the merger

will generate a higher return than capital expenditure, then this may be a decent decision for the

organization. If their government expects returns to be lower than their own financial backers

expect, they will need to put their cash flow to more likely uses (French, 2019).

In general, a lower WACC indicates a robust business that can attract financial backers at a

lower cost. Conversely, in most cases, higher WACCs correspond to organizations that are seen

as more at risk and must reward financial backers with higher yields.

WACC = (We * Re) + [Wd * Rd]

= (0.25 * 13.85) + [0.75 *12]

= 3.4625 + 9

= 12.4625 %

Should the project go ahead using a project finance scheme? Give reasons.

From all the computations ascertained in the above report, it can be said that the agreement

of APWater is better for the company. Ass it is ascertaining more present value after 20 years in

the project. Also, the IRR of the project is 18.79%.

CONCLUSION

From, the above report, it can be summarised that financing any project is very crucial and it

takes logical thinking for processing all the funds and return and to determine the exact

calculations. The above report says that IRR is generated through the present value of cash

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inflows and outflows considering the discounted rate of return. Further, The WACC and CAPM

model is calculated with the help of the cost of capital and the value of market return given.

RECOMMENDATIONS

The suggestions that can be given to ABC Water Pty Limited is that the costs of expenditure

should be improvised. It will be beneficial for the company and for the project as well.

model is calculated with the help of the cost of capital and the value of market return given.

RECOMMENDATIONS

The suggestions that can be given to ABC Water Pty Limited is that the costs of expenditure

should be improvised. It will be beneficial for the company and for the project as well.

REFERENCES

Books and Journals

Carluccio, J., Mazet-Sonilhac, C. and Mésonnier, J.S., 2021. Private firms, corporate investment

and the WACC: evidence from France. The European Journal of Finance, pp.1-25.

Chung, J.H., 2020, November. Debt/Equity Tradeoff Model for Revenue Based DBFOM PPP

Transportation Infrastructure: Case Study of I-95 (VA) Express Lanes. In Construction

Research Congress 2020: Project Management and Controls, Materials, and

Contracts (pp. 1177-1185). Reston, VA: American Society of Civil Engineers.

Fernandez, P., 2019. wacc and capm according to utilities regulators: Confusions, errors and

inconsistencies. Errors and Inconsistencies (February 19, 2019).

Fernandez, P., 2020. The Most Common Error in Valuations using WACC. Available at SSRN

3512739.

French, N., 2019. Property investment: gearing and the equity rate of return. Journal of Property

Investment & Finance.

Harvey, L.D., 2020. Clarifications of and improvements to the equations used to calculate the

levelized cost of electricity (LCOE), and comments on the weighted average cost of

capital (WACC). Energy, 207, p.118340.

Jylha, P. and Ungeheuer, M., 2021. Growth Expectations out of WACC. Available at SSRN

3618612.

Magni, C.A. and Cuthbert, J., 2018. Some problems of the IRR in measuring PEI performance

and how to solve it with the pure-investment AIRR. Journal of Performance

Measurement, 22(2), pp.39-50.

Books and Journals

Carluccio, J., Mazet-Sonilhac, C. and Mésonnier, J.S., 2021. Private firms, corporate investment

and the WACC: evidence from France. The European Journal of Finance, pp.1-25.

Chung, J.H., 2020, November. Debt/Equity Tradeoff Model for Revenue Based DBFOM PPP

Transportation Infrastructure: Case Study of I-95 (VA) Express Lanes. In Construction

Research Congress 2020: Project Management and Controls, Materials, and

Contracts (pp. 1177-1185). Reston, VA: American Society of Civil Engineers.

Fernandez, P., 2019. wacc and capm according to utilities regulators: Confusions, errors and

inconsistencies. Errors and Inconsistencies (February 19, 2019).

Fernandez, P., 2020. The Most Common Error in Valuations using WACC. Available at SSRN

3512739.

French, N., 2019. Property investment: gearing and the equity rate of return. Journal of Property

Investment & Finance.

Harvey, L.D., 2020. Clarifications of and improvements to the equations used to calculate the

levelized cost of electricity (LCOE), and comments on the weighted average cost of

capital (WACC). Energy, 207, p.118340.

Jylha, P. and Ungeheuer, M., 2021. Growth Expectations out of WACC. Available at SSRN

3618612.

Magni, C.A. and Cuthbert, J., 2018. Some problems of the IRR in measuring PEI performance

and how to solve it with the pure-investment AIRR. Journal of Performance

Measurement, 22(2), pp.39-50.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.