University Finance Report: Project and Innovation Accounting Analysis

VerifiedAdded on 2023/06/03

|7

|1049

|85

Report

AI Summary

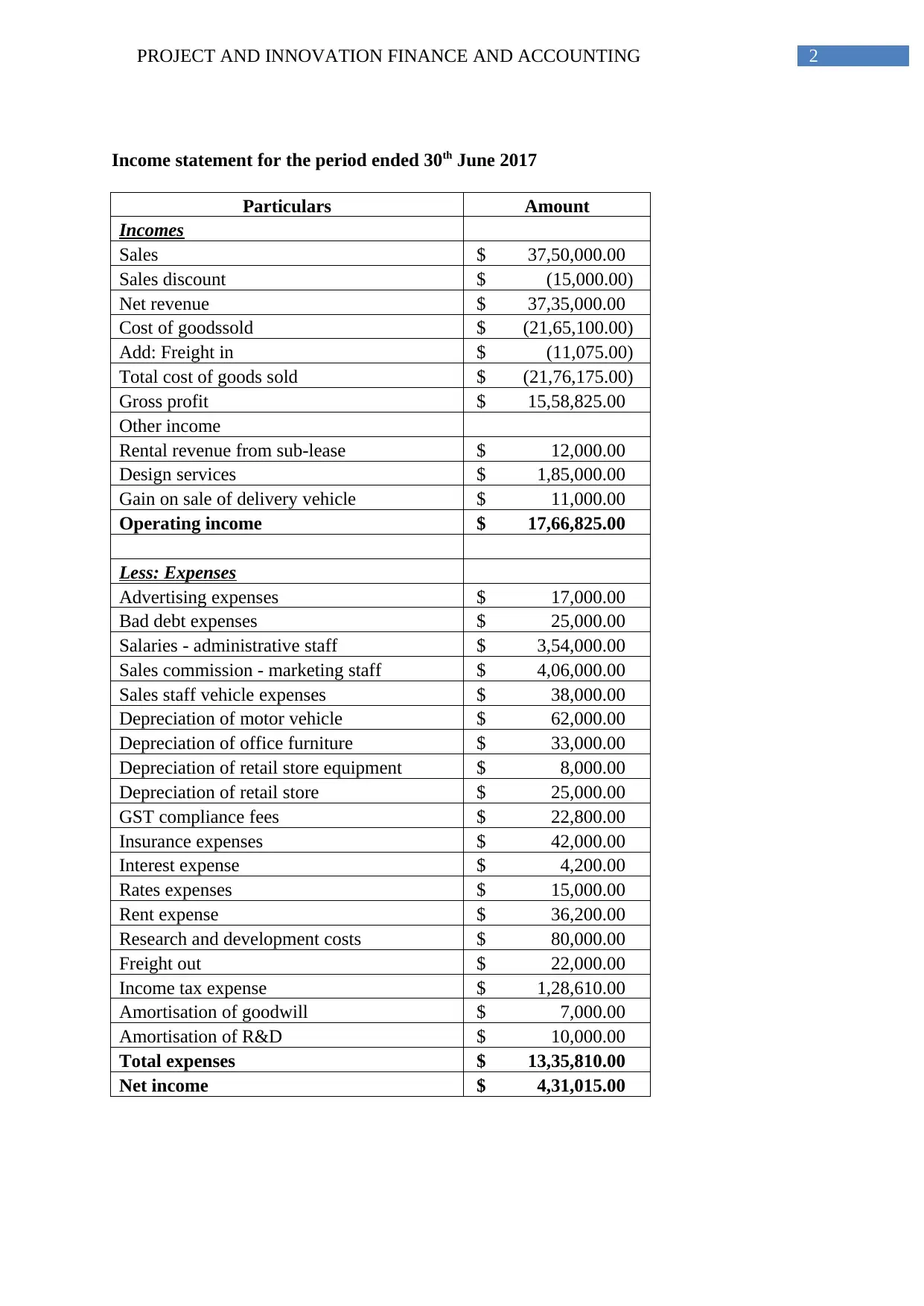

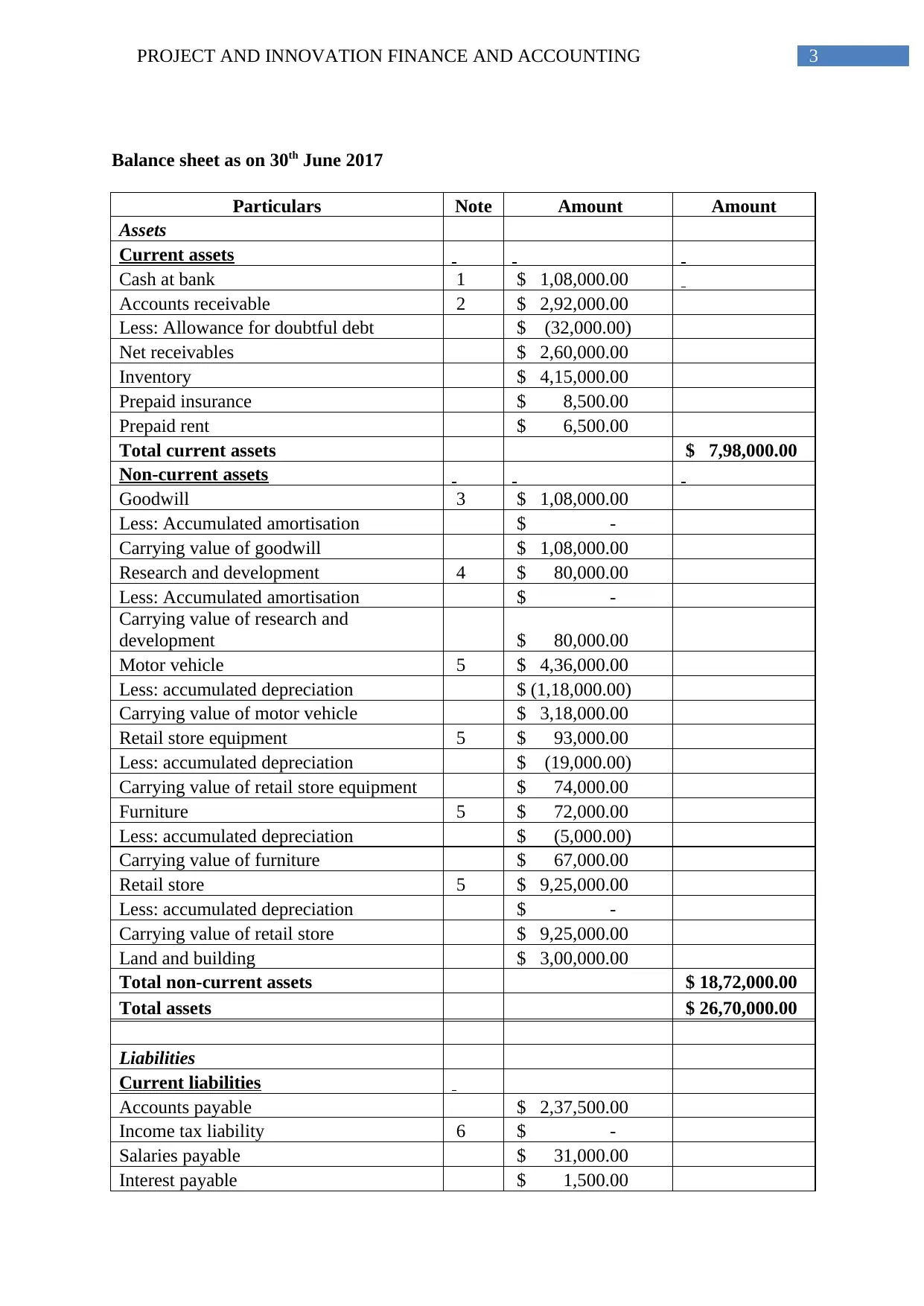

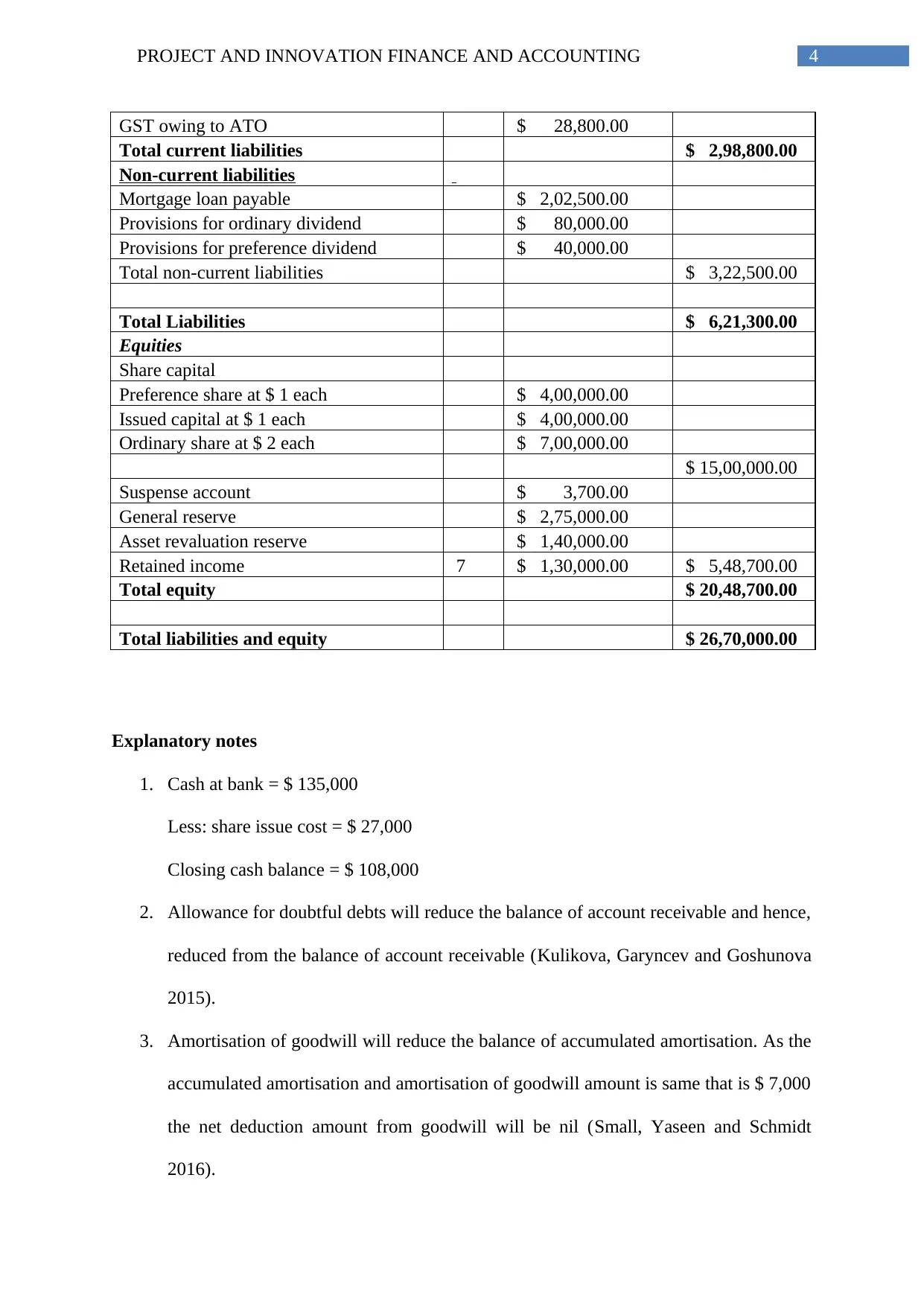

This report provides a comprehensive analysis of project and innovation finance and accounting. It includes an income statement for the period ending June 30, 2017, detailing sales, cost of goods sold, gross profit, other income, operating income, expenses, and net income. The balance sheet as of June 30, 2017, presents assets (current and non-current), liabilities (current and non-current), and equity. Explanatory notes clarify key accounting treatments such as allowance for doubtful debts, amortization of goodwill and R&D, depreciation, and income tax liability. The report references several sources, including articles discussing depreciation methods, doubtful debts, deferred tax liabilities, and the amortization of intangible assets.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.