Financial Analysis and Investment Project Valuation - FIN301

VerifiedAdded on 2021/02/02

|10

|2388

|118

Homework Assignment

AI Summary

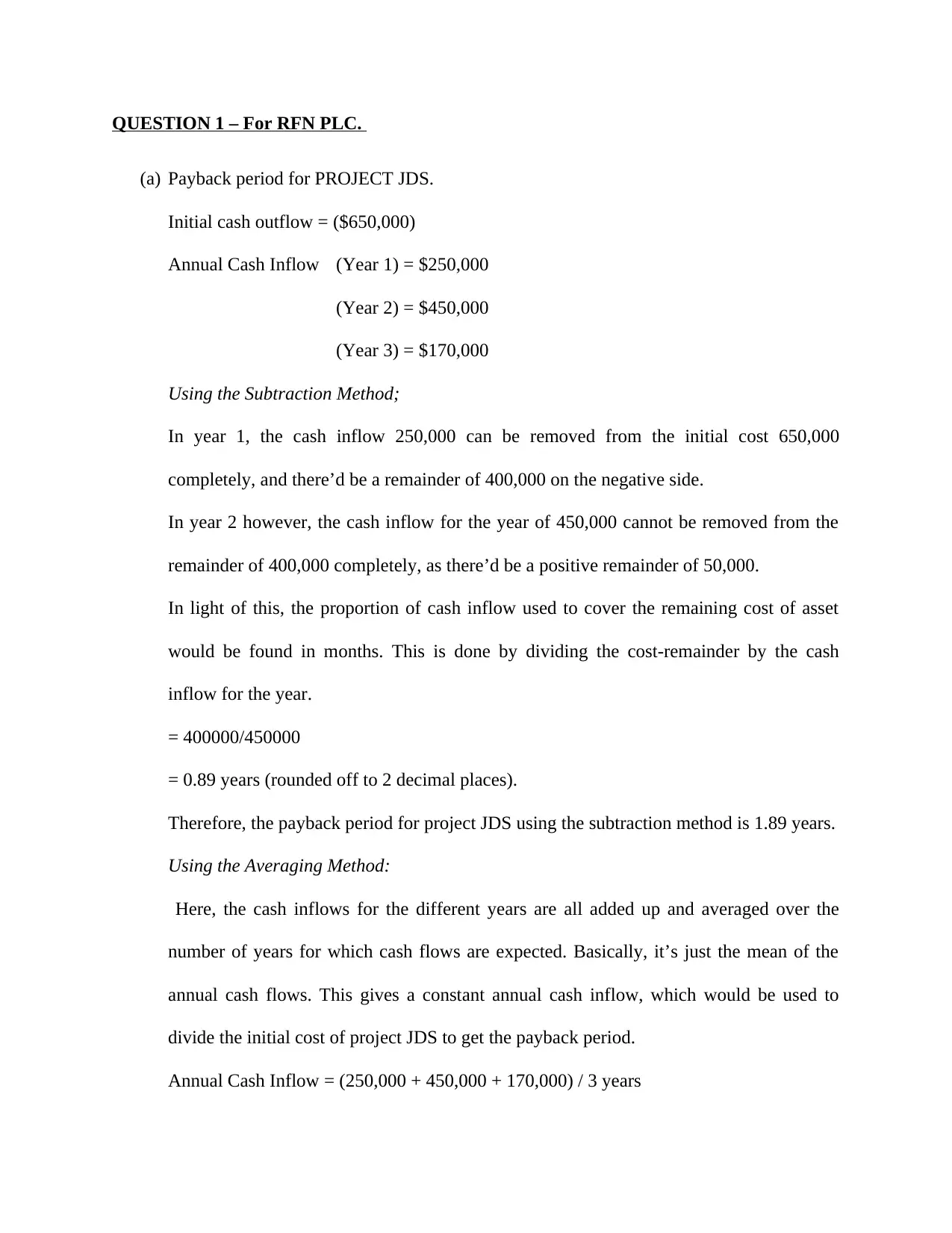

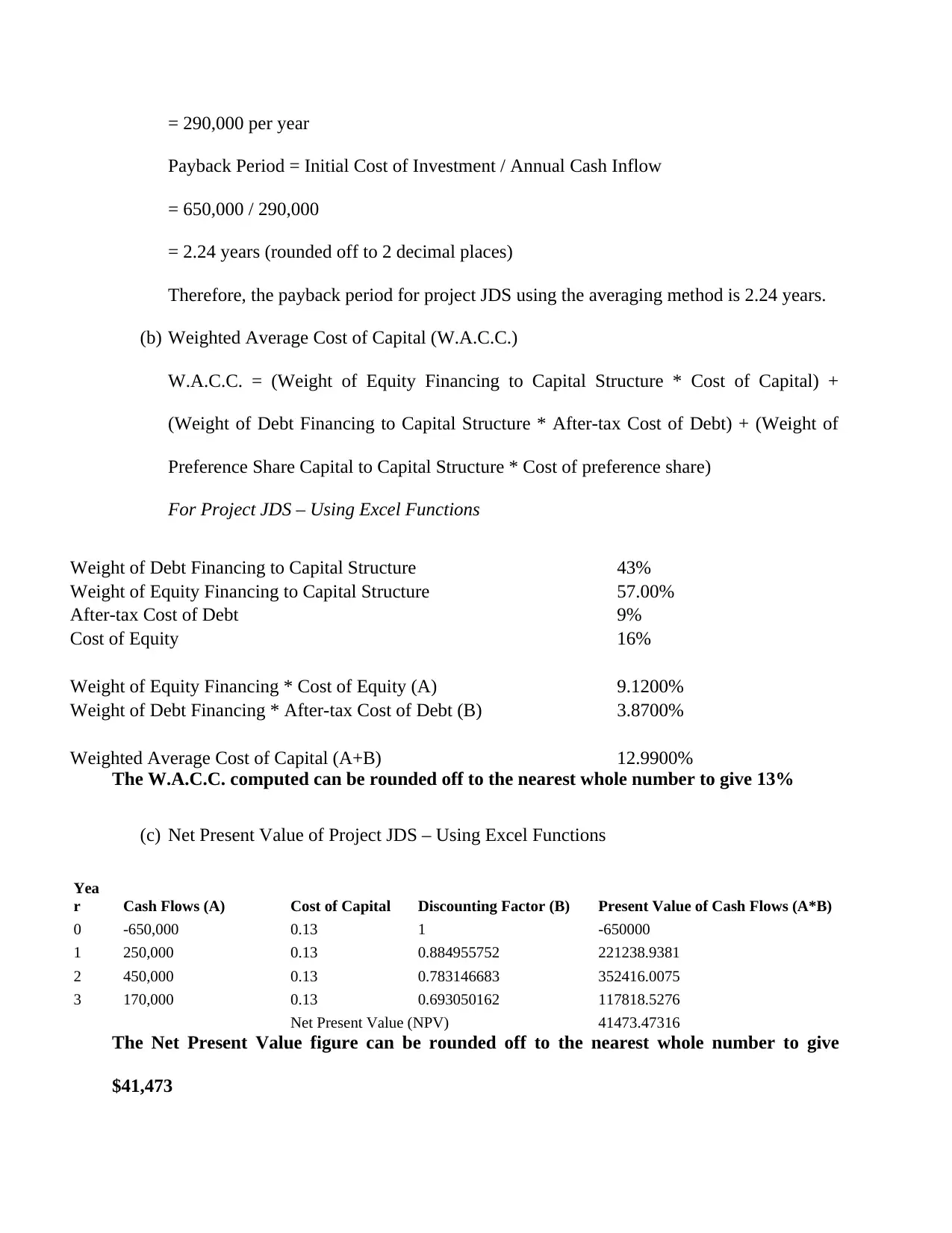

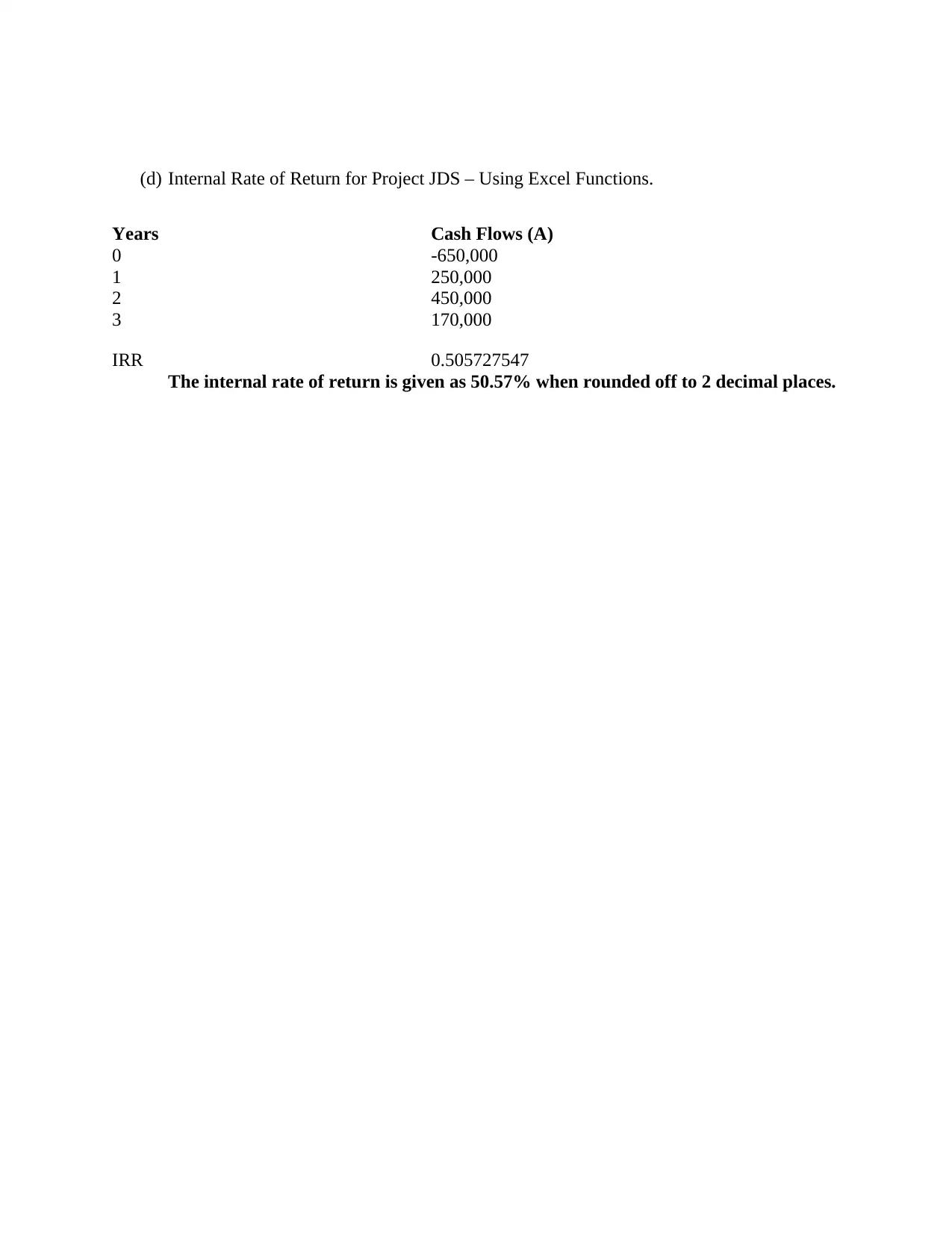

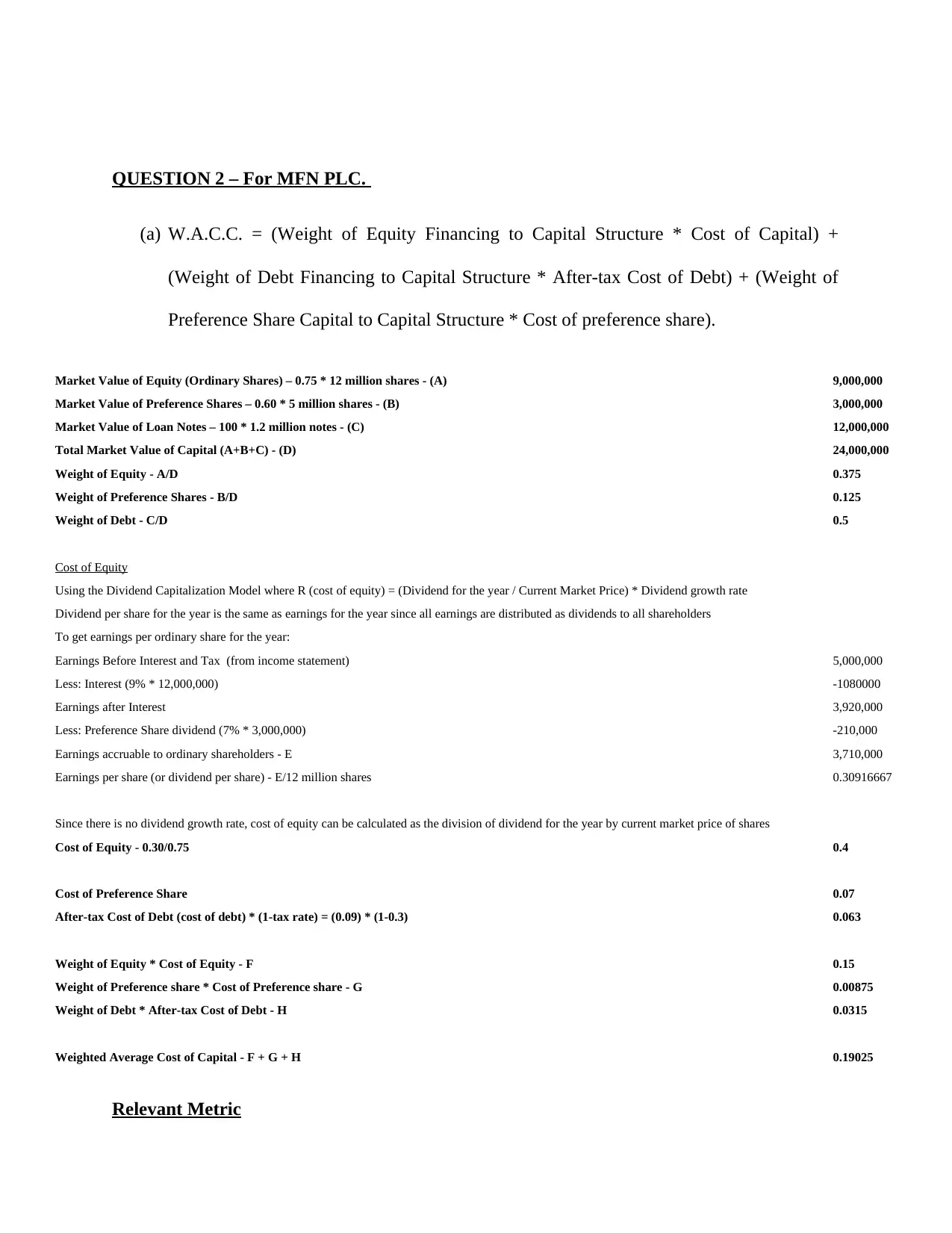

This assignment delves into various financial analysis techniques applied to project valuation. It begins with calculating the payback period for Project JDS using both subtraction and averaging methods. The assignment then determines the Weighted Average Cost of Capital (WACC) for both RFN PLC and MFN PLC, utilizing Excel functions for calculations. Furthermore, it computes the Net Present Value (NPV) and Internal Rate of Return (IRR) for Project JDS. The assignment also explores time value of money concepts, calculating present and future values, and analyzing investment options, including lump-sum deposits and annuity payments. The final part of the assignment involves calculating the interest rates and semi-annual installments needed to achieve specific financial goals. The assignment uses Excel functions for various calculations and provides detailed explanations of the financial concepts involved.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.