Project Report: Principles of Accounting

VerifiedAdded on 2020/03/16

|16

|4152

|45

Report

AI Summary

This report investigates the financial performance of Violet Chan’s Consultancy Pty Ltd through various accounting principles. It includes an analysis of company transactions, performance metrics, and ratio analysis, concluding with recommendations for improving profitability and liquidity. The report highlights the need for better management of assets and equity to enhance the company's financial standing.

Running Head: Principles of accounting

1

Project report: Principles of accounting

1

Project report: Principles of accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principles of accounting

2

Contents

Introduction.......................................................................................................................3

Company performance......................................................................................................3

Transaction in the company..............................................................................................3

Ratio analysis....................................................................................................................4

Conclusion........................................................................................................................5

References.........................................................................................................................7

Appendix...........................................................................................................................8

2

Contents

Introduction.......................................................................................................................3

Company performance......................................................................................................3

Transaction in the company..............................................................................................3

Ratio analysis....................................................................................................................4

Conclusion........................................................................................................................5

References.........................................................................................................................7

Appendix...........................................................................................................................8

Principles of accounting

3

Introduction:

This report has been prepared to investigate the numbers of the Violet Chan’s

consultancy Pty ltd. Before preparing this report, the activities and transaction of the

company has been evaluated and for that preparation of journal entries, ledger account, trail

balance, profit and loss account, balance sheet and calculation of ratio analysis has been

done. This report depict that the performance of the company is not impressive and the

company is required to manage and maintain various expenses and required to make change

into the assets, equity and debt level to enhance the profitability, liquidity and debt position

of the company. In this report, the comparative study has also been done to found and analyze

the changes into financial performance of the company from last year.

Company performance:

According to the last year’s balance sheet of the company, it has been analyzed that

the performance of the company was bit better than current year as the company was able to

make at least the profit. But according to the current situation of the company, the company

has faced the situation of net loss. The current scenario of capital structure and the debt

equity, debt assets and equity ratio was almost similar as last year (Assessment, 2013). No

extra changes have been done by the company to manage and change the level of the

company, according to the performance of the company, it has been analyzed that the

company is required to make various changes into its activities and performance to manage

the profits. Owner is investing various capitals into the company but this amount is not used

by the company in a proper manner and that is why the excess problems are faced by the

company. Further, the level of the total assets, debt and equity has been analyzed and it has

been found that the level of total assets has been enhanced whereas the level of debt has been

reduced and the level of total equity of the company has also been enhanced from financial

year 2015 in financial year 2016. The average performance of the company expresses that the

company has not managed a good level of equity (Whittington, 2008). The company is

suggested to reduce the level of total assets to maintain the business in a good manner.

Transaction in the company:

Various transaction of the company has been studied in the month of June. The main

transaction was contributing more money into the account which was not required by the

company. The owner has contributed $ 17,000 more into the capital of the company. Further,

3

Introduction:

This report has been prepared to investigate the numbers of the Violet Chan’s

consultancy Pty ltd. Before preparing this report, the activities and transaction of the

company has been evaluated and for that preparation of journal entries, ledger account, trail

balance, profit and loss account, balance sheet and calculation of ratio analysis has been

done. This report depict that the performance of the company is not impressive and the

company is required to manage and maintain various expenses and required to make change

into the assets, equity and debt level to enhance the profitability, liquidity and debt position

of the company. In this report, the comparative study has also been done to found and analyze

the changes into financial performance of the company from last year.

Company performance:

According to the last year’s balance sheet of the company, it has been analyzed that

the performance of the company was bit better than current year as the company was able to

make at least the profit. But according to the current situation of the company, the company

has faced the situation of net loss. The current scenario of capital structure and the debt

equity, debt assets and equity ratio was almost similar as last year (Assessment, 2013). No

extra changes have been done by the company to manage and change the level of the

company, according to the performance of the company, it has been analyzed that the

company is required to make various changes into its activities and performance to manage

the profits. Owner is investing various capitals into the company but this amount is not used

by the company in a proper manner and that is why the excess problems are faced by the

company. Further, the level of the total assets, debt and equity has been analyzed and it has

been found that the level of total assets has been enhanced whereas the level of debt has been

reduced and the level of total equity of the company has also been enhanced from financial

year 2015 in financial year 2016. The average performance of the company expresses that the

company has not managed a good level of equity (Whittington, 2008). The company is

suggested to reduce the level of total assets to maintain the business in a good manner.

Transaction in the company:

Various transaction of the company has been studied in the month of June. The main

transaction was contributing more money into the account which was not required by the

company. The owner has contributed $ 17,000 more into the capital of the company. Further,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principles of accounting

4

a new computer has also been bought by the company on credit and the payment has not been

made by the company (Lee, 2006). Company has paid various monthly expenses in cash such

as salary, wages, rent, advertisement, telephone bill etc. Company has bought furniture on

credit basis and later on the entire amount has been paid by the company to its creditors.

Company has also depreciated the old and new furniture and the old and new computer

according to the SLM depreciation method (assumption). Thus through these analysis, it has

been found that the company has not made any special transaction to manage the level of

equity, assets, debt of the company. And company has also not made any extra effort to

enhance the revenue of the company, only $ 200 has been spent by the company on

advertisement. According to the evaluation of all of these, it has been found that the average

performance of the company expresses that the company has not managed a good level of

equity (Glasson, Therivel & Chadwick, 2013). The company is suggested to reduce the level

of total assets to maintain the business in a good manner.

Ratio analysis:

Ratio analysis study has been performed over the Violet Chan’s consultancy Pty ltd.

The study of ratio analysis of the company depict that the return on assets of the company is -

2.29% which depict that the performance of the company is not well and the company is

facing various losses in the market (Dye & Sunder, 2001). Through this analysis, it has been

found that the net profit of the company is $ -1146 and the total assets of the company is $

50,054. Further, it has been investigated that the current ratio of the company is 9.72:1 which

depict that the current assets of the company is 9.72 times more than the current liabilities of

the company.

The current ratio of the company depict that the liquidity position of the company has

been worst and it express that the company is required to reduce the level of current assets of

the company to manage the liquidity position of the company. The current assets of the

company are $ 40,854 and the current liabilities of the company are $ 4,200 which express

that the company must reduce the level of the current assets of the company (Laux & Leuz,

2009)..

Further, the assets turnover ratio of the company has been analyzed and it has been

found that the ratio of the company is 0.1208 which express that the total sales are 0.12 times

of the total assets of the company. The total sales of the company are $ 6,050 and the total

4

a new computer has also been bought by the company on credit and the payment has not been

made by the company (Lee, 2006). Company has paid various monthly expenses in cash such

as salary, wages, rent, advertisement, telephone bill etc. Company has bought furniture on

credit basis and later on the entire amount has been paid by the company to its creditors.

Company has also depreciated the old and new furniture and the old and new computer

according to the SLM depreciation method (assumption). Thus through these analysis, it has

been found that the company has not made any special transaction to manage the level of

equity, assets, debt of the company. And company has also not made any extra effort to

enhance the revenue of the company, only $ 200 has been spent by the company on

advertisement. According to the evaluation of all of these, it has been found that the average

performance of the company expresses that the company has not managed a good level of

equity (Glasson, Therivel & Chadwick, 2013). The company is suggested to reduce the level

of total assets to maintain the business in a good manner.

Ratio analysis:

Ratio analysis study has been performed over the Violet Chan’s consultancy Pty ltd.

The study of ratio analysis of the company depict that the return on assets of the company is -

2.29% which depict that the performance of the company is not well and the company is

facing various losses in the market (Dye & Sunder, 2001). Through this analysis, it has been

found that the net profit of the company is $ -1146 and the total assets of the company is $

50,054. Further, it has been investigated that the current ratio of the company is 9.72:1 which

depict that the current assets of the company is 9.72 times more than the current liabilities of

the company.

The current ratio of the company depict that the liquidity position of the company has

been worst and it express that the company is required to reduce the level of current assets of

the company to manage the liquidity position of the company. The current assets of the

company are $ 40,854 and the current liabilities of the company are $ 4,200 which express

that the company must reduce the level of the current assets of the company (Laux & Leuz,

2009)..

Further, the assets turnover ratio of the company has been analyzed and it has been

found that the ratio of the company is 0.1208 which express that the total sales are 0.12 times

of the total assets of the company. The total sales of the company are $ 6,050 and the total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principles of accounting

5

assets of the company are $ 50,054. According to this analysis, it is suggested top the

company to reduce the level of current assets. Company is not required to manage and

maintain this much of assets as the less level of total assets would also be sufficient for the

company and the current level would enhance the cost of the company only (Whittington,

2008).

More, the debt to equity ratio of the company has been analyzed. Through this ratio, it

has been found that the debt- equity relation of the company is 0.0915:1 which express that

the debt of the company is 0.09 times of the total equity of the company. The total debt of the

company is $4,200 whereas the total equity of the company is $ 45,854 which express that

the capital structure of the company is not at all good (Daly & Farley, 2011). Company is

required to reduce the level of equity which could be done through withdrawing the amount

from the capital account of the company to maintain an optimal capital structure on the

company .( Schroeder, Clark & Cathey, 2001)

More, the debt to assets ratio of the company has been analyzed. Through this ratio, it

has been found that the debt- asset relation of the company is 0.083:1 which express that the

debt of the company is 0.08 times of the total assets of the company. The total debt of the

company is $4,200 whereas the total assets of the company are $ 50,054 which express that

the company has not managed a good level of debt and equity (Arewa, 2006). The company

is suggested to reduce the level of total assets to maintain the business in a good manner.

More, the equity to assets ratio of the company has been analyzed. Through this ratio,

it has been found that the equity- asset relation of the company is 0.92:1 which express that

the equity of the company is 0.92 times of the total assets of the company. The total equity of

the company is $45,854 whereas the total assets of the company are $ 50,054 which express

that the company has not managed a good level of equity. The company is suggested to

reduce the level of total assets to maintain the business in a good manner.

Conclusion:

Through this report, calculation of ratio analysis, preparation of journal entries, ledger

account, trail balance, profit and loss account, balance sheet etc, it has been analyzed that the

company is required to manage the level of the assets and equity to maintain the business in a

good manner. The company is suggested to look over the activities and transaction of

competitive business and make a good decision accordingly. Through this case study, it has

5

assets of the company are $ 50,054. According to this analysis, it is suggested top the

company to reduce the level of current assets. Company is not required to manage and

maintain this much of assets as the less level of total assets would also be sufficient for the

company and the current level would enhance the cost of the company only (Whittington,

2008).

More, the debt to equity ratio of the company has been analyzed. Through this ratio, it

has been found that the debt- equity relation of the company is 0.0915:1 which express that

the debt of the company is 0.09 times of the total equity of the company. The total debt of the

company is $4,200 whereas the total equity of the company is $ 45,854 which express that

the capital structure of the company is not at all good (Daly & Farley, 2011). Company is

required to reduce the level of equity which could be done through withdrawing the amount

from the capital account of the company to maintain an optimal capital structure on the

company .( Schroeder, Clark & Cathey, 2001)

More, the debt to assets ratio of the company has been analyzed. Through this ratio, it

has been found that the debt- asset relation of the company is 0.083:1 which express that the

debt of the company is 0.08 times of the total assets of the company. The total debt of the

company is $4,200 whereas the total assets of the company are $ 50,054 which express that

the company has not managed a good level of debt and equity (Arewa, 2006). The company

is suggested to reduce the level of total assets to maintain the business in a good manner.

More, the equity to assets ratio of the company has been analyzed. Through this ratio,

it has been found that the equity- asset relation of the company is 0.92:1 which express that

the equity of the company is 0.92 times of the total assets of the company. The total equity of

the company is $45,854 whereas the total assets of the company are $ 50,054 which express

that the company has not managed a good level of equity. The company is suggested to

reduce the level of total assets to maintain the business in a good manner.

Conclusion:

Through this report, calculation of ratio analysis, preparation of journal entries, ledger

account, trail balance, profit and loss account, balance sheet etc, it has been analyzed that the

company is required to manage the level of the assets and equity to maintain the business in a

good manner. The company is suggested to look over the activities and transaction of

competitive business and make a good decision accordingly. Through this case study, it has

Principles of accounting

6

been found that this company is not able to manage the capital structure in a good manner

and the turnover of the company is also not good. The comparative study of financial year

2015 and financial year 2016 depict that any extra efforts have not been made by the

company to manage the performance and profitability position of the company. So the

company is suggested to enhance the expenditure on advertisement and promotion and reduce

the level of total assets and total equity.

6

been found that this company is not able to manage the capital structure in a good manner

and the turnover of the company is also not good. The comparative study of financial year

2015 and financial year 2016 depict that any extra efforts have not been made by the

company to manage the performance and profitability position of the company. So the

company is suggested to enhance the expenditure on advertisement and promotion and reduce

the level of total assets and total equity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principles of accounting

7

References:

Arewa, O.B., (2006). Measuring &representing the knowledge economy: accounting for

economic reality under the intangibles paradigm. Buff. L. Rev., 54, p.1.

Assessment, W.S.B.P., (2013). Conceptual Framework.

Daly, H. E., &Farley, J., (2011). Ecological economics: principles &applications. Isl&press.

Dye, R.A. &Sunder, S.,(2001). Why not allow FASB &IASB standards to compete in the

US?. Accounting horizons, 15(3), pp.257-271.

Glasson, J., Therivel, R., &Chadwick, A., (2013). Introduction to environmental impact

assessment. Routledge.

Laux, C. &Leuz, C., (2009). The crisis of fair-value accounting: Making sense of the recent

debate. Accounting, organizations &society, 34(6), pp.826-834.

Lee, T.A., (2006). The FASB &accounting for economic reality. Accounting &the Public

Interest, 6(1), pp.1-21.

Schroeder, R.G., Clark, M.W. &Cathey, J.M., (2001). Accounting theory &analysis. Chapel

Hill: University of North Carolina.

Whittington, G., (2008) (B). Fair value &the IASB/FASB conceptual framework project: an

alternative view. Abacus, 44(2), pp.139-168.

Whittington, G., (2008). Fair value &the IASB/FASB conceptual framework project: an

alternative view. Abacus, 44(2), pp.139-168.

7

References:

Arewa, O.B., (2006). Measuring &representing the knowledge economy: accounting for

economic reality under the intangibles paradigm. Buff. L. Rev., 54, p.1.

Assessment, W.S.B.P., (2013). Conceptual Framework.

Daly, H. E., &Farley, J., (2011). Ecological economics: principles &applications. Isl&press.

Dye, R.A. &Sunder, S.,(2001). Why not allow FASB &IASB standards to compete in the

US?. Accounting horizons, 15(3), pp.257-271.

Glasson, J., Therivel, R., &Chadwick, A., (2013). Introduction to environmental impact

assessment. Routledge.

Laux, C. &Leuz, C., (2009). The crisis of fair-value accounting: Making sense of the recent

debate. Accounting, organizations &society, 34(6), pp.826-834.

Lee, T.A., (2006). The FASB &accounting for economic reality. Accounting &the Public

Interest, 6(1), pp.1-21.

Schroeder, R.G., Clark, M.W. &Cathey, J.M., (2001). Accounting theory &analysis. Chapel

Hill: University of North Carolina.

Whittington, G., (2008) (B). Fair value &the IASB/FASB conceptual framework project: an

alternative view. Abacus, 44(2), pp.139-168.

Whittington, G., (2008). Fair value &the IASB/FASB conceptual framework project: an

alternative view. Abacus, 44(2), pp.139-168.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principles of accounting

8

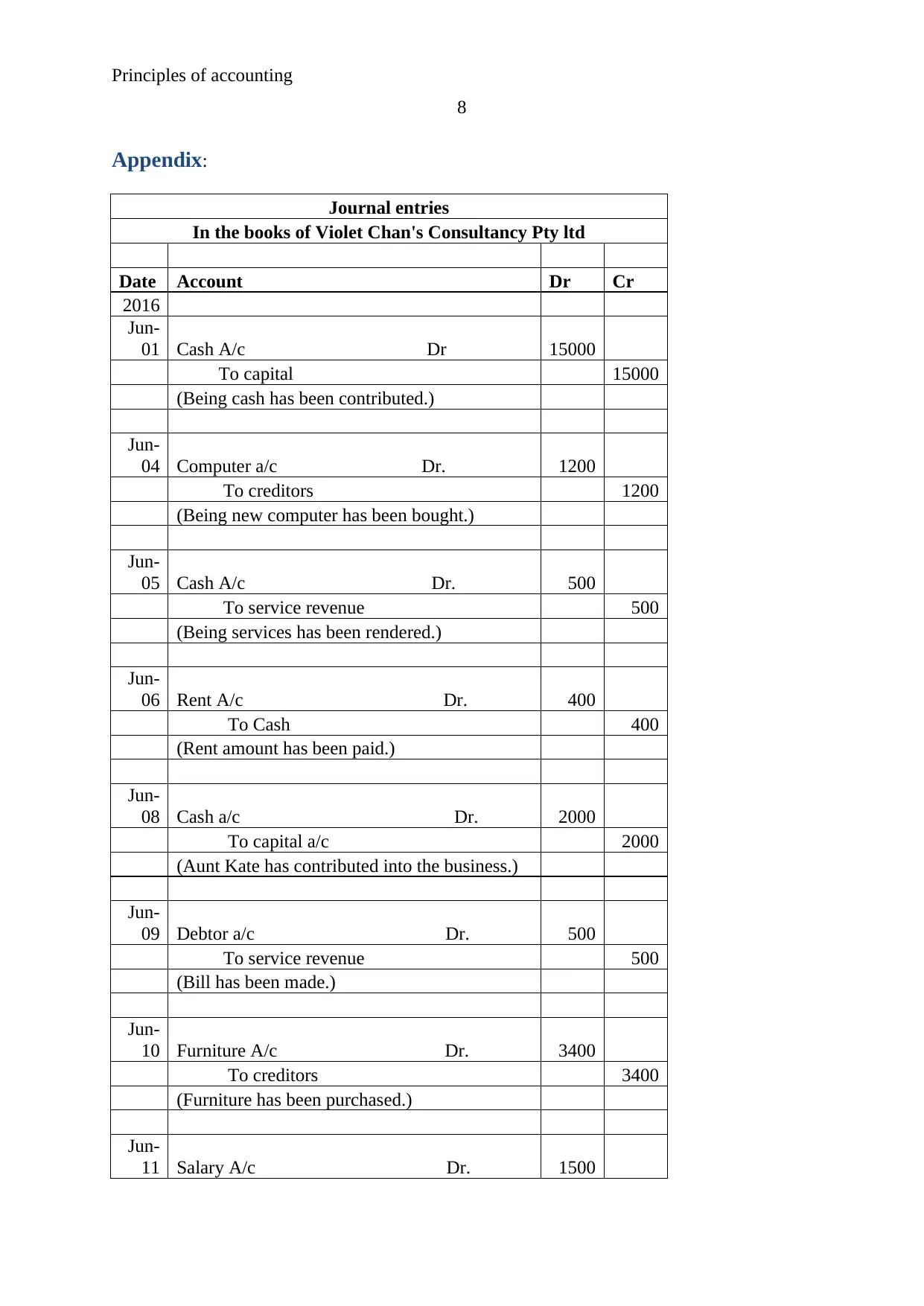

Appendix:

Journal entries

In the books of Violet Chan's Consultancy Pty ltd

Date Account Dr Cr

2016

Jun-

01 Cash A/c Dr 15000

To capital 15000

(Being cash has been contributed.)

Jun-

04 Computer a/c Dr. 1200

To creditors 1200

(Being new computer has been bought.)

Jun-

05 Cash A/c Dr. 500

To service revenue 500

(Being services has been rendered.)

Jun-

06 Rent A/c Dr. 400

To Cash 400

(Rent amount has been paid.)

Jun-

08 Cash a/c Dr. 2000

To capital a/c 2000

(Aunt Kate has contributed into the business.)

Jun-

09 Debtor a/c Dr. 500

To service revenue 500

(Bill has been made.)

Jun-

10 Furniture A/c Dr. 3400

To creditors 3400

(Furniture has been purchased.)

Jun-

11 Salary A/c Dr. 1500

8

Appendix:

Journal entries

In the books of Violet Chan's Consultancy Pty ltd

Date Account Dr Cr

2016

Jun-

01 Cash A/c Dr 15000

To capital 15000

(Being cash has been contributed.)

Jun-

04 Computer a/c Dr. 1200

To creditors 1200

(Being new computer has been bought.)

Jun-

05 Cash A/c Dr. 500

To service revenue 500

(Being services has been rendered.)

Jun-

06 Rent A/c Dr. 400

To Cash 400

(Rent amount has been paid.)

Jun-

08 Cash a/c Dr. 2000

To capital a/c 2000

(Aunt Kate has contributed into the business.)

Jun-

09 Debtor a/c Dr. 500

To service revenue 500

(Bill has been made.)

Jun-

10 Furniture A/c Dr. 3400

To creditors 3400

(Furniture has been purchased.)

Jun-

11 Salary A/c Dr. 1500

Principles of accounting

9

To cash 1500

(Salary amount has been paid.)

Jun-

15 Telephone expenses a/c Dr. 65

To Cash 65

(Telephone expenses have been paid.)

Jun-

16 Cleaning bill a/c Dr. 231

To Cash 231

(Cleaning expenses have been paid.)

Jun-

20 Rent a/c Dr. 400

To cash 400

(Rent amount has been paid.)

Jun-

23 Cash A/c Dr. 250

To consultancy revenue 250

(Consultancy amount has been received.)

Jun-

24 Debtors A/c Dr. 4800

To service revenue 4800

(Services have been rendered on credit.)

Jun-

26 Salary a/c Dr. 1500

To cash 1500

(Salary amount has been paid.)

Jun-

28 Creditors a/c Dr. 3400

To cash 3400

(Furniture amount has been paid.)

Jun-

30 Advertisement a/c Dr. 200

To cash 200

(Advertisement amount has been paid.)

Jun-

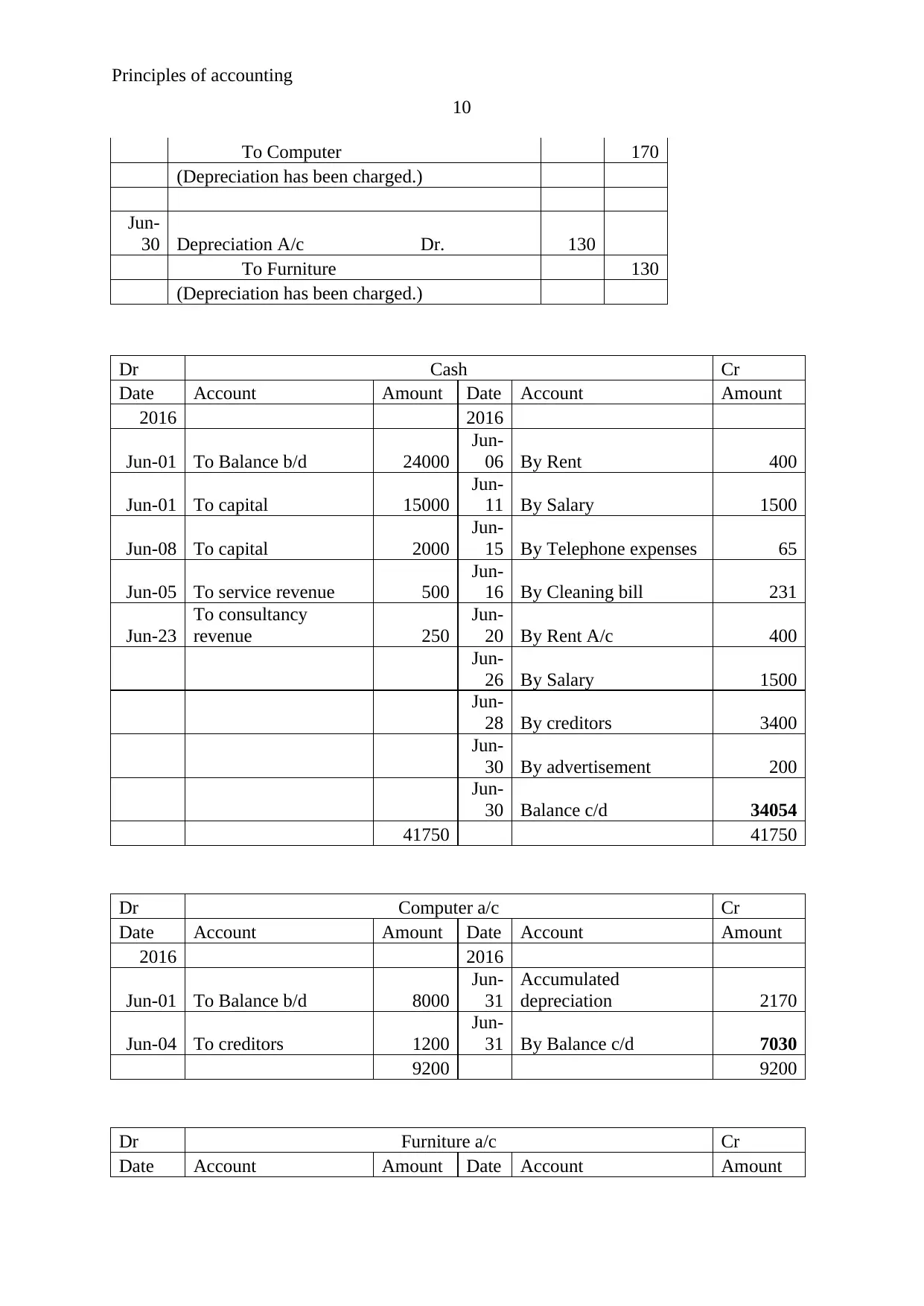

30 Depreciation A/c Dr. 170

9

To cash 1500

(Salary amount has been paid.)

Jun-

15 Telephone expenses a/c Dr. 65

To Cash 65

(Telephone expenses have been paid.)

Jun-

16 Cleaning bill a/c Dr. 231

To Cash 231

(Cleaning expenses have been paid.)

Jun-

20 Rent a/c Dr. 400

To cash 400

(Rent amount has been paid.)

Jun-

23 Cash A/c Dr. 250

To consultancy revenue 250

(Consultancy amount has been received.)

Jun-

24 Debtors A/c Dr. 4800

To service revenue 4800

(Services have been rendered on credit.)

Jun-

26 Salary a/c Dr. 1500

To cash 1500

(Salary amount has been paid.)

Jun-

28 Creditors a/c Dr. 3400

To cash 3400

(Furniture amount has been paid.)

Jun-

30 Advertisement a/c Dr. 200

To cash 200

(Advertisement amount has been paid.)

Jun-

30 Depreciation A/c Dr. 170

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Principles of accounting

10

To Computer 170

(Depreciation has been charged.)

Jun-

30 Depreciation A/c Dr. 130

To Furniture 130

(Depreciation has been charged.)

Dr Cash Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 24000

Jun-

06 By Rent 400

Jun-01 To capital 15000

Jun-

11 By Salary 1500

Jun-08 To capital 2000

Jun-

15 By Telephone expenses 65

Jun-05 To service revenue 500

Jun-

16 By Cleaning bill 231

Jun-23

To consultancy

revenue 250

Jun-

20 By Rent A/c 400

Jun-

26 By Salary 1500

Jun-

28 By creditors 3400

Jun-

30 By advertisement 200

Jun-

30 Balance c/d 34054

41750 41750

Dr Computer a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 8000

Jun-

31

Accumulated

depreciation 2170

Jun-04 To creditors 1200

Jun-

31 By Balance c/d 7030

9200 9200

Dr Furniture a/c Cr

Date Account Amount Date Account Amount

10

To Computer 170

(Depreciation has been charged.)

Jun-

30 Depreciation A/c Dr. 130

To Furniture 130

(Depreciation has been charged.)

Dr Cash Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 24000

Jun-

06 By Rent 400

Jun-01 To capital 15000

Jun-

11 By Salary 1500

Jun-08 To capital 2000

Jun-

15 By Telephone expenses 65

Jun-05 To service revenue 500

Jun-

16 By Cleaning bill 231

Jun-23

To consultancy

revenue 250

Jun-

20 By Rent A/c 400

Jun-

26 By Salary 1500

Jun-

28 By creditors 3400

Jun-

30 By advertisement 200

Jun-

30 Balance c/d 34054

41750 41750

Dr Computer a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 8000

Jun-

31

Accumulated

depreciation 2170

Jun-04 To creditors 1200

Jun-

31 By Balance c/d 7030

9200 9200

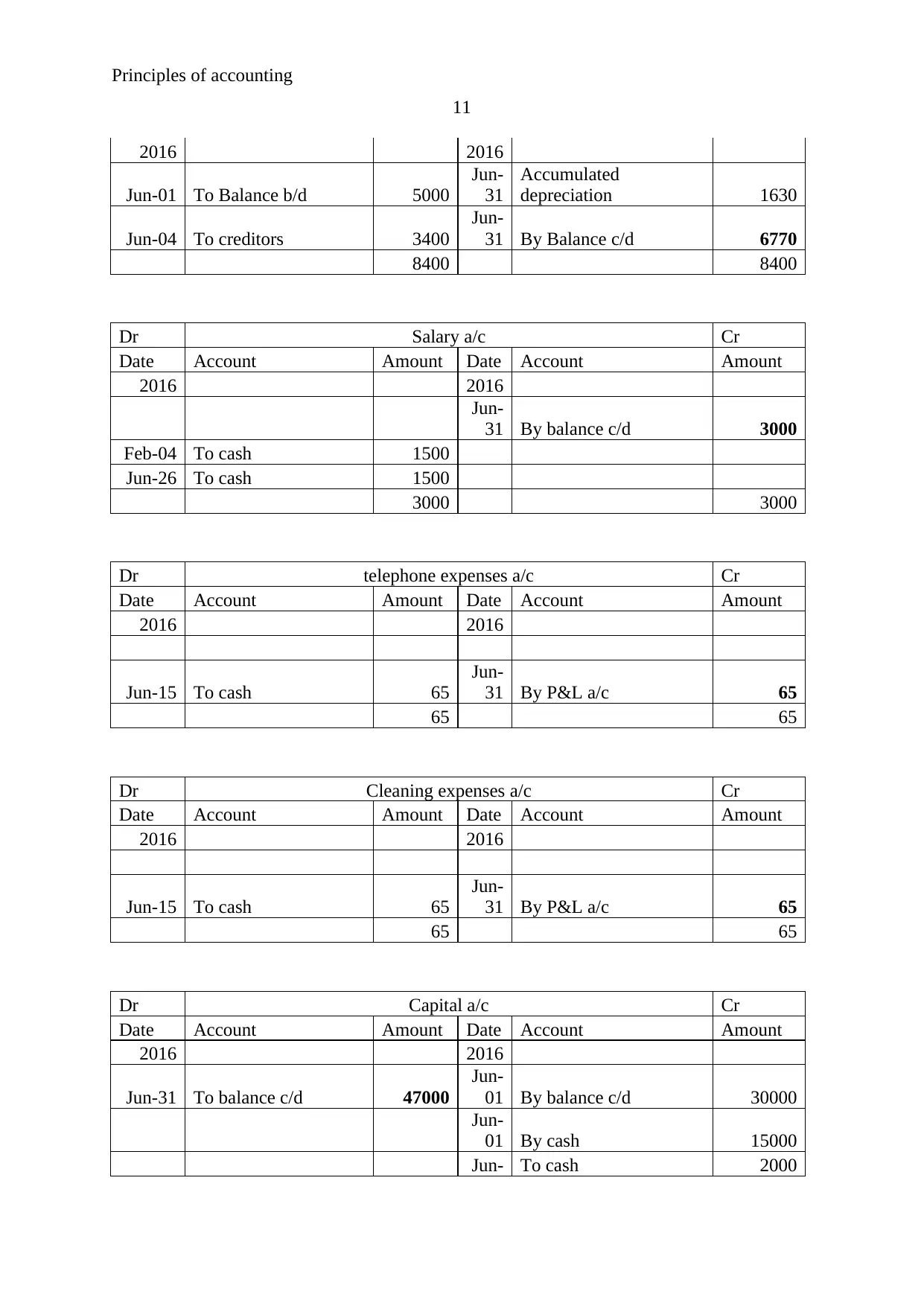

Dr Furniture a/c Cr

Date Account Amount Date Account Amount

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Principles of accounting

11

2016 2016

Jun-01 To Balance b/d 5000

Jun-

31

Accumulated

depreciation 1630

Jun-04 To creditors 3400

Jun-

31 By Balance c/d 6770

8400 8400

Dr Salary a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-

31 By balance c/d 3000

Feb-04 To cash 1500

Jun-26 To cash 1500

3000 3000

Dr telephone expenses a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-15 To cash 65

Jun-

31 By P&L a/c 65

65 65

Dr Cleaning expenses a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-15 To cash 65

Jun-

31 By P&L a/c 65

65 65

Dr Capital a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-31 To balance c/d 47000

Jun-

01 By balance c/d 30000

Jun-

01 By cash 15000

Jun- To cash 2000

11

2016 2016

Jun-01 To Balance b/d 5000

Jun-

31

Accumulated

depreciation 1630

Jun-04 To creditors 3400

Jun-

31 By Balance c/d 6770

8400 8400

Dr Salary a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-

31 By balance c/d 3000

Feb-04 To cash 1500

Jun-26 To cash 1500

3000 3000

Dr telephone expenses a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-15 To cash 65

Jun-

31 By P&L a/c 65

65 65

Dr Cleaning expenses a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-15 To cash 65

Jun-

31 By P&L a/c 65

65 65

Dr Capital a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-31 To balance c/d 47000

Jun-

01 By balance c/d 30000

Jun-

01 By cash 15000

Jun- To cash 2000

Principles of accounting

12

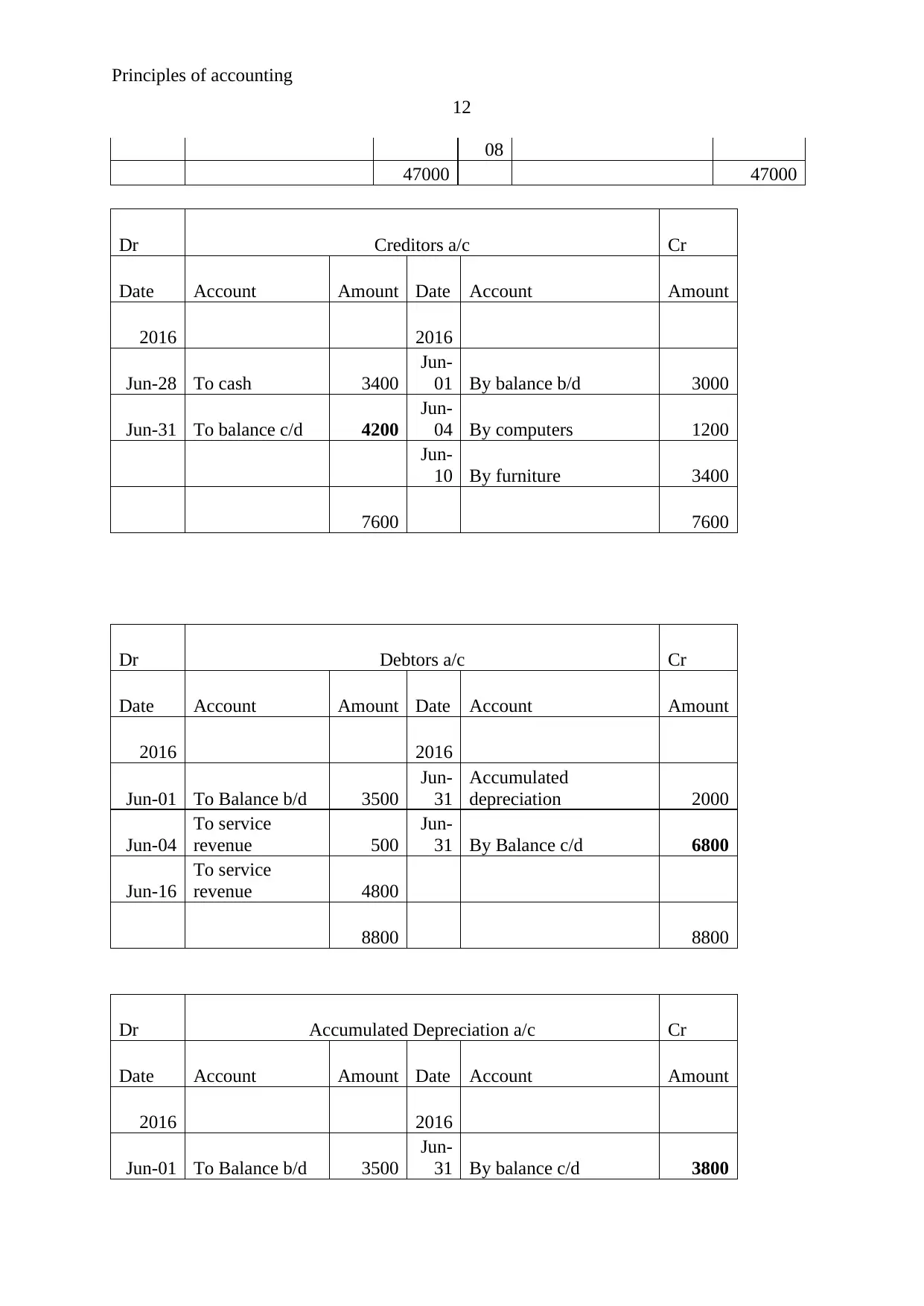

08

47000 47000

Dr Creditors a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-28 To cash 3400

Jun-

01 By balance b/d 3000

Jun-31 To balance c/d 4200

Jun-

04 By computers 1200

Jun-

10 By furniture 3400

7600 7600

Dr Debtors a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 3500

Jun-

31

Accumulated

depreciation 2000

Jun-04

To service

revenue 500

Jun-

31 By Balance c/d 6800

Jun-16

To service

revenue 4800

8800 8800

Dr Accumulated Depreciation a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 3500

Jun-

31 By balance c/d 3800

12

08

47000 47000

Dr Creditors a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-28 To cash 3400

Jun-

01 By balance b/d 3000

Jun-31 To balance c/d 4200

Jun-

04 By computers 1200

Jun-

10 By furniture 3400

7600 7600

Dr Debtors a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 3500

Jun-

31

Accumulated

depreciation 2000

Jun-04

To service

revenue 500

Jun-

31 By Balance c/d 6800

Jun-16

To service

revenue 4800

8800 8800

Dr Accumulated Depreciation a/c Cr

Date Account Amount Date Account Amount

2016 2016

Jun-01 To Balance b/d 3500

Jun-

31 By balance c/d 3800

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.