Finance Report: Property Economics and Investment Analysis

VerifiedAdded on 2021/04/21

|12

|2537

|24

Report

AI Summary

This report delves into the core aspects of property economics and finance, commencing with an exploration of various funding sources available to developers, including personal savings, bank loans, and emerging alternatives like private funders and joint ventures. It then examines financing techniques, highlighting the significance of capital structure and its impact on firm leverage, investor returns, and cost of capital. Evaluation techniques, particularly Net Present Value (NPV) and capitalization rates, are analyzed to assess property value and profitability. The report also addresses critical risk management strategies, focusing on market risks, liquidity risks, and correlation analysis, providing insights into mitigating investment risks. Finally, the report considers the overall property economics, evaluating the impact of interest rate changes, government policies, unemployment, and supply dynamics on mixed-use development proposals and investment decisions within the real estate sector. The report provides a comprehensive overview of property finance and investment.

qwertyuiopasdfghjklzxcvbnmqw

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnm

PROPERTY ECONOMICS AND FINANCE

[Type the document subtitle]

[Pick the date]

#04074

ertyuiopasdfghjklzxcvbnmqwert

yuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiop

asdfghjklzxcvbnmqwertyuiopasd

fghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjkl

zxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnm

PROPERTY ECONOMICS AND FINANCE

[Type the document subtitle]

[Pick the date]

#04074

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Table of Contents

Sources and Types of Finance.................................................................................................2

Financing Techniques..............................................................................................................3

Evaluation Techniques.............................................................................................................3

Risk and Risk Management....................................................................................................4

Property economics overall view............................................................................................5

References.................................................................................................................................6

Table of Contents

Sources and Types of Finance.................................................................................................2

Financing Techniques..............................................................................................................3

Evaluation Techniques.............................................................................................................3

Risk and Risk Management....................................................................................................4

Property economics overall view............................................................................................5

References.................................................................................................................................6

2

Sources and Types of Finance

The developer within the property industry has to identify and evaluate the various

alternatives of financing before selecting the best one. Most of the developers first go for

personal savings as source of funds. In addition, they also rely on different banks and life

insurance companies for funding as its primary source. However, globalization has led other

sources like private funders and joint ventures to emerge as an alternative for many

developers. Moreover, they can also get advances from third parties as lease and

securitisation (SPVs). Further, they get the funds from mortgage brokers and mortgage

bankers for re-mortgaging as they have proficiency and understanding in property industry.

Other main sources include pension funds, auction finance and bridging finance, real estate

investment trusts, corporate finance and state finance programs (Berry et al., 2013).

The capital structure in property industry helps to know the quantum of equity and

debt in financing property and further expansion. Further, this also helps in to compute the

firm’s leverage (Migl, 2016). In this industry developer majorly uses debt for financing so the

company has a high leverage. However, it plays a crucial role in period of bankruptcy also. It

is important for a developer to focus on capital structure as helps to maximize the market

value of the firm which in turn increase the share price and dividends, minimizes the cost of

financing, recognize better investment opportunities for growth of the company and the

industry (Trisha, 2018).

The main capital structuring issue that are relevant to investor returns is considering

cost of capital which should be lower than expected returns. In addition to this, a tax

deduction in debt financing decreases the cost of debt and increases the possibility of returns

and dividends. Further, a high tax rate increases the proportion of debt in financing, but

increase the risk of bankruptcy. The concept of window of opportunity is also a major issue

Sources and Types of Finance

The developer within the property industry has to identify and evaluate the various

alternatives of financing before selecting the best one. Most of the developers first go for

personal savings as source of funds. In addition, they also rely on different banks and life

insurance companies for funding as its primary source. However, globalization has led other

sources like private funders and joint ventures to emerge as an alternative for many

developers. Moreover, they can also get advances from third parties as lease and

securitisation (SPVs). Further, they get the funds from mortgage brokers and mortgage

bankers for re-mortgaging as they have proficiency and understanding in property industry.

Other main sources include pension funds, auction finance and bridging finance, real estate

investment trusts, corporate finance and state finance programs (Berry et al., 2013).

The capital structure in property industry helps to know the quantum of equity and

debt in financing property and further expansion. Further, this also helps in to compute the

firm’s leverage (Migl, 2016). In this industry developer majorly uses debt for financing so the

company has a high leverage. However, it plays a crucial role in period of bankruptcy also. It

is important for a developer to focus on capital structure as helps to maximize the market

value of the firm which in turn increase the share price and dividends, minimizes the cost of

financing, recognize better investment opportunities for growth of the company and the

industry (Trisha, 2018).

The main capital structuring issue that are relevant to investor returns is considering

cost of capital which should be lower than expected returns. In addition to this, a tax

deduction in debt financing decreases the cost of debt and increases the possibility of returns

and dividends. Further, a high tax rate increases the proportion of debt in financing, but

increase the risk of bankruptcy. The concept of window of opportunity is also a major issue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

as it states the time when the funds are available at a lower cost considering the economy

conditions. Further, the restrictions on management and its style adopted as aggressive or

conservative is also a major issue affecting the investor’s return. The growth rate of the

company can finance its capital from debt easily increasing the business risk of the company

(Lumen, 2018).

Financing Techniques

The various risk faced by the financiers in the project finance are identified as

controllable or uncontrollable risks. Construction and completion risk is crucial to lenders as

they need to mitigate it by commodity derivatives if the completion costs increases.

Operating risk is faced when the cost of operations goes up and these can be mitigated

through future contracts, lump sum payments, turnkey contracts and warranty agreements.

Force majeure and change in law is a major risk for lenders so they need to regularly review

it. Further, political and regulatory risks are uncontrollable risk so lenders should be ready to

face this risk. This risk can be reduced through insurance. Repayment risk is the most

important risk to lenders and it is managed through Project Company itself by maintaining

reserve accounts and evaluating potential ratios. Currency exchange risk and interest rate risk

are some other risks that lenders have to deal with. To reduce it to the lowest level they use

the method of swapping with a different market financier (World Bank Group, 2018).

Further, the risk between parties is shared considering that which party can control the risk

efficiently and effectively. The party which can control the risk should tolerate it. However, if

none of the parties can control it than the party which can tolerate it easily should take efforts

to do so.

Evaluation Techniques

Computation of Net Present Values-

as it states the time when the funds are available at a lower cost considering the economy

conditions. Further, the restrictions on management and its style adopted as aggressive or

conservative is also a major issue affecting the investor’s return. The growth rate of the

company can finance its capital from debt easily increasing the business risk of the company

(Lumen, 2018).

Financing Techniques

The various risk faced by the financiers in the project finance are identified as

controllable or uncontrollable risks. Construction and completion risk is crucial to lenders as

they need to mitigate it by commodity derivatives if the completion costs increases.

Operating risk is faced when the cost of operations goes up and these can be mitigated

through future contracts, lump sum payments, turnkey contracts and warranty agreements.

Force majeure and change in law is a major risk for lenders so they need to regularly review

it. Further, political and regulatory risks are uncontrollable risk so lenders should be ready to

face this risk. This risk can be reduced through insurance. Repayment risk is the most

important risk to lenders and it is managed through Project Company itself by maintaining

reserve accounts and evaluating potential ratios. Currency exchange risk and interest rate risk

are some other risks that lenders have to deal with. To reduce it to the lowest level they use

the method of swapping with a different market financier (World Bank Group, 2018).

Further, the risk between parties is shared considering that which party can control the risk

efficiently and effectively. The party which can control the risk should tolerate it. However, if

none of the parties can control it than the party which can tolerate it easily should take efforts

to do so.

Evaluation Techniques

Computation of Net Present Values-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

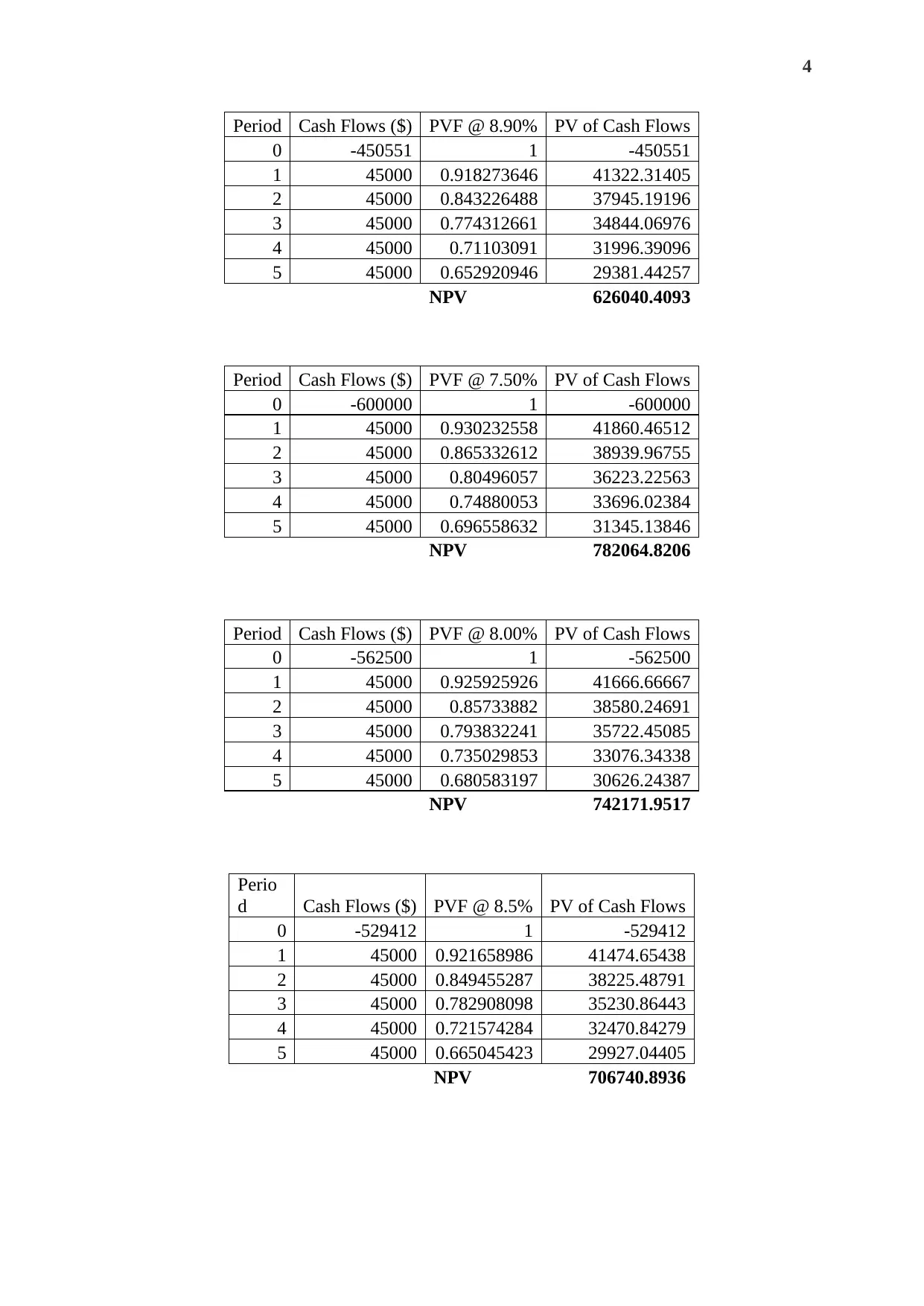

Period Cash Flows ($) PVF @ 8.90% PV of Cash Flows

0 -450551 1 -450551

1 45000 0.918273646 41322.31405

2 45000 0.843226488 37945.19196

3 45000 0.774312661 34844.06976

4 45000 0.71103091 31996.39096

5 45000 0.652920946 29381.44257

NPV 626040.4093

Period Cash Flows ($) PVF @ 7.50% PV of Cash Flows

0 -600000 1 -600000

1 45000 0.930232558 41860.46512

2 45000 0.865332612 38939.96755

3 45000 0.80496057 36223.22563

4 45000 0.74880053 33696.02384

5 45000 0.696558632 31345.13846

NPV 782064.8206

Period Cash Flows ($) PVF @ 8.00% PV of Cash Flows

0 -562500 1 -562500

1 45000 0.925925926 41666.66667

2 45000 0.85733882 38580.24691

3 45000 0.793832241 35722.45085

4 45000 0.735029853 33076.34338

5 45000 0.680583197 30626.24387

NPV 742171.9517

Perio

d Cash Flows ($) PVF @ 8.5% PV of Cash Flows

0 -529412 1 -529412

1 45000 0.921658986 41474.65438

2 45000 0.849455287 38225.48791

3 45000 0.782908098 35230.86443

4 45000 0.721574284 32470.84279

5 45000 0.665045423 29927.04405

NPV 706740.8936

Period Cash Flows ($) PVF @ 8.90% PV of Cash Flows

0 -450551 1 -450551

1 45000 0.918273646 41322.31405

2 45000 0.843226488 37945.19196

3 45000 0.774312661 34844.06976

4 45000 0.71103091 31996.39096

5 45000 0.652920946 29381.44257

NPV 626040.4093

Period Cash Flows ($) PVF @ 7.50% PV of Cash Flows

0 -600000 1 -600000

1 45000 0.930232558 41860.46512

2 45000 0.865332612 38939.96755

3 45000 0.80496057 36223.22563

4 45000 0.74880053 33696.02384

5 45000 0.696558632 31345.13846

NPV 782064.8206

Period Cash Flows ($) PVF @ 8.00% PV of Cash Flows

0 -562500 1 -562500

1 45000 0.925925926 41666.66667

2 45000 0.85733882 38580.24691

3 45000 0.793832241 35722.45085

4 45000 0.735029853 33076.34338

5 45000 0.680583197 30626.24387

NPV 742171.9517

Perio

d Cash Flows ($) PVF @ 8.5% PV of Cash Flows

0 -529412 1 -529412

1 45000 0.921658986 41474.65438

2 45000 0.849455287 38225.48791

3 45000 0.782908098 35230.86443

4 45000 0.721574284 32470.84279

5 45000 0.665045423 29927.04405

NPV 706740.8936

5

Period Cash Flows ($) PVF @ 9% PV of Cash Flows

0 -500000 1 -500000

1 45000

0.91743119

3 41284.40367

2 45000

0.84167999

3 37875.5997

3 45000 0.77218348 34748.2566

4 45000

0.70842521

1 31879.1345

5 45000

0.64993138

6 29246.91238

NPV 675034.3069

Perio

d Cash Flows ($) PVF @ 9.5% PV of Cash Flows

0 -473684 1 -473684

1 45000 0.913242009 41095.89041

2 45000 0.834010967 37530.49353

3 45000 0.761653851 34274.42331

4 45000 0.695574293 31300.84321

5 45000 0.635227665 28585.24494

NPV 646470.8954

Perio

d Cash Flows ($) PVF @ 10.00% PV of Cash Flows

0 -450000 1 -450000

1 45000 0.909090909 40909.09091

2 45000 0.826446281 37190.08264

3 45000 0.751314801 33809.16604

4 45000 0.683013455 30735.60549

5 45000 0.620921323 27941.45954

NPV 620585.4046

Perio

d Cash Flows ($) PVF @ 10.50% PV of Cash Flows

0 -428571 1 -428571

1 45000 0.904977376 40723.9819

2 45000 0.81898405 36854.28226

3 45000 0.741162036 33352.29164

4 45000 0.670734875 30183.06936

5 45000 0.606999887 27314.99489

Period Cash Flows ($) PVF @ 9% PV of Cash Flows

0 -500000 1 -500000

1 45000

0.91743119

3 41284.40367

2 45000

0.84167999

3 37875.5997

3 45000 0.77218348 34748.2566

4 45000

0.70842521

1 31879.1345

5 45000

0.64993138

6 29246.91238

NPV 675034.3069

Perio

d Cash Flows ($) PVF @ 9.5% PV of Cash Flows

0 -473684 1 -473684

1 45000 0.913242009 41095.89041

2 45000 0.834010967 37530.49353

3 45000 0.761653851 34274.42331

4 45000 0.695574293 31300.84321

5 45000 0.635227665 28585.24494

NPV 646470.8954

Perio

d Cash Flows ($) PVF @ 10.00% PV of Cash Flows

0 -450000 1 -450000

1 45000 0.909090909 40909.09091

2 45000 0.826446281 37190.08264

3 45000 0.751314801 33809.16604

4 45000 0.683013455 30735.60549

5 45000 0.620921323 27941.45954

NPV 620585.4046

Perio

d Cash Flows ($) PVF @ 10.50% PV of Cash Flows

0 -428571 1 -428571

1 45000 0.904977376 40723.9819

2 45000 0.81898405 36854.28226

3 45000 0.741162036 33352.29164

4 45000 0.670734875 30183.06936

5 45000 0.606999887 27314.99489

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

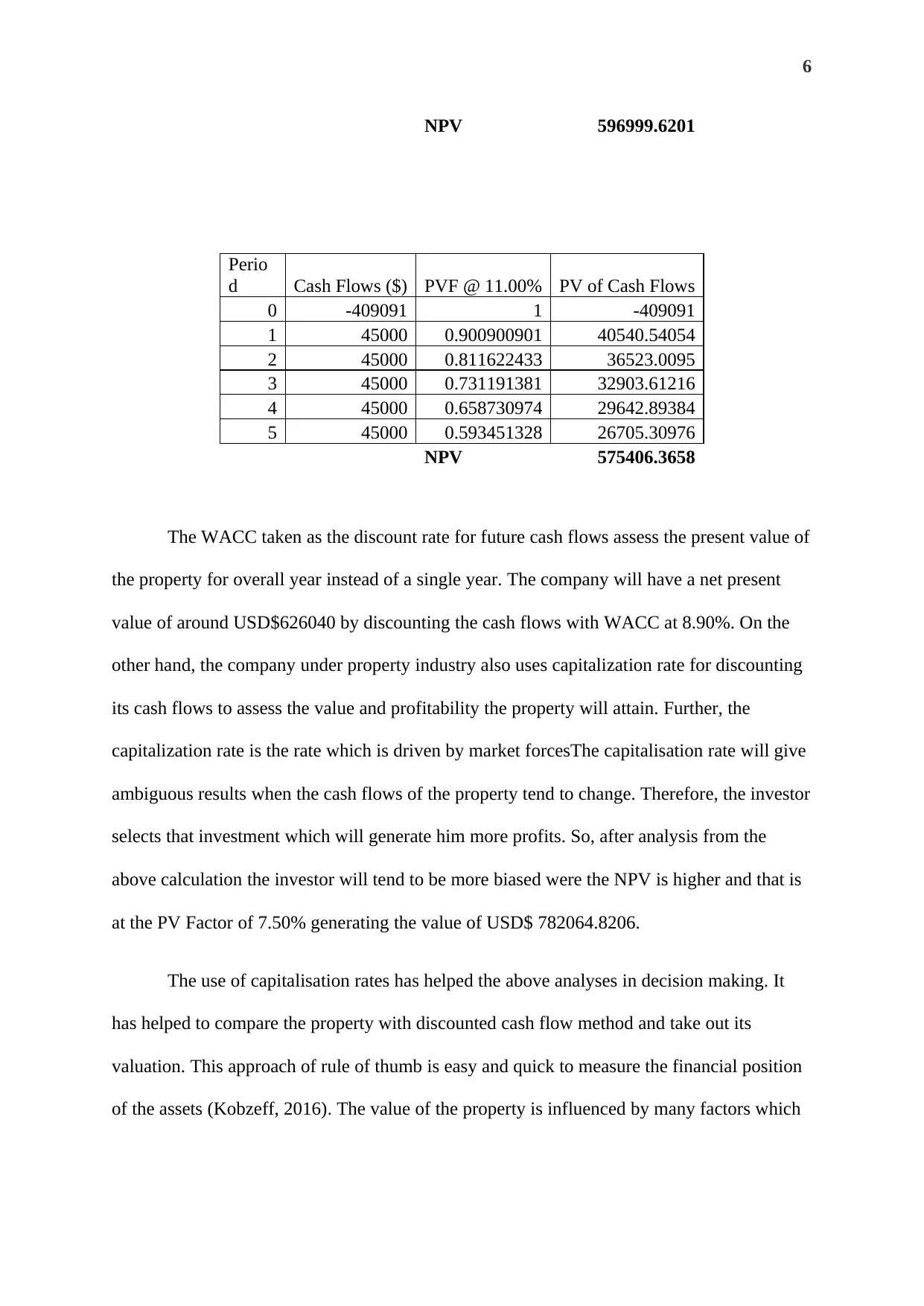

NPV 596999.6201

Perio

d Cash Flows ($) PVF @ 11.00% PV of Cash Flows

0 -409091 1 -409091

1 45000 0.900900901 40540.54054

2 45000 0.811622433 36523.0095

3 45000 0.731191381 32903.61216

4 45000 0.658730974 29642.89384

5 45000 0.593451328 26705.30976

NPV 575406.3658

The WACC taken as the discount rate for future cash flows assess the present value of

the property for overall year instead of a single year. The company will have a net present

value of around USD$626040 by discounting the cash flows with WACC at 8.90%. On the

other hand, the company under property industry also uses capitalization rate for discounting

its cash flows to assess the value and profitability the property will attain. Further, the

capitalization rate is the rate which is driven by market forcesThe capitalisation rate will give

ambiguous results when the cash flows of the property tend to change. Therefore, the investor

selects that investment which will generate him more profits. So, after analysis from the

above calculation the investor will tend to be more biased were the NPV is higher and that is

at the PV Factor of 7.50% generating the value of USD$ 782064.8206.

The use of capitalisation rates has helped the above analyses in decision making. It

has helped to compare the property with discounted cash flow method and take out its

valuation. This approach of rule of thumb is easy and quick to measure the financial position

of the assets (Kobzeff, 2016). The value of the property is influenced by many factors which

NPV 596999.6201

Perio

d Cash Flows ($) PVF @ 11.00% PV of Cash Flows

0 -409091 1 -409091

1 45000 0.900900901 40540.54054

2 45000 0.811622433 36523.0095

3 45000 0.731191381 32903.61216

4 45000 0.658730974 29642.89384

5 45000 0.593451328 26705.30976

NPV 575406.3658

The WACC taken as the discount rate for future cash flows assess the present value of

the property for overall year instead of a single year. The company will have a net present

value of around USD$626040 by discounting the cash flows with WACC at 8.90%. On the

other hand, the company under property industry also uses capitalization rate for discounting

its cash flows to assess the value and profitability the property will attain. Further, the

capitalization rate is the rate which is driven by market forcesThe capitalisation rate will give

ambiguous results when the cash flows of the property tend to change. Therefore, the investor

selects that investment which will generate him more profits. So, after analysis from the

above calculation the investor will tend to be more biased were the NPV is higher and that is

at the PV Factor of 7.50% generating the value of USD$ 782064.8206.

The use of capitalisation rates has helped the above analyses in decision making. It

has helped to compare the property with discounted cash flow method and take out its

valuation. This approach of rule of thumb is easy and quick to measure the financial position

of the assets (Kobzeff, 2016). The value of the property is influenced by many factors which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

should be considered by the investors. These include location of the property, valuation of the

property, purpose of the investments and profit expectations.

Risk and Risk Management

From the investor’s side, the key risk connected with the property investment is

market risks which include equity, interest and currency risks. Liquidity risk is challenge to

sell the investment at a reasonable price. There is concentration risk also i.e. not diversifying

in different portfolios. Investors who do not get their principal amount and interest on

maturity from Companies facing financial difficulties faces credit risk. Some other major

risks faced by the investors are foreign investment risks, horizon risk, inflation risk, capital

risk, on-going return risk, degradation in the value of the property. These risks when

identified can be majorly managed through guidance from experts and diversification of the

property portfolio. Investors should avoid leverage margin trading. Risk can also be reduced

by investing in companies which have a stable and consistent record of stock in the past.

Further, in the recession period, investors should avoid investing in levered companies.

However, a positive cash flow should be managed by the investors for high returns (Duggan

& Benzinga, 2014).

Correlation indicates the degree of relationship between the two variables or sectors.

It helps the investors to diversify their risk in investments by decreasing the correlation

between them. Commercial and residential sectors as two variables have a strong correlation

between them. This means that the value for both will fluctuate in same directions. According

to some economist, there are same factors that affect the demand for both the sectors.

However, demand plays an important factor for measuring the relationship between these two

markets. For example, increase in the household market cause the commercial market to also

increase indicating a strong positive correlation. Similarly, a negative correlation is seen

should be considered by the investors. These include location of the property, valuation of the

property, purpose of the investments and profit expectations.

Risk and Risk Management

From the investor’s side, the key risk connected with the property investment is

market risks which include equity, interest and currency risks. Liquidity risk is challenge to

sell the investment at a reasonable price. There is concentration risk also i.e. not diversifying

in different portfolios. Investors who do not get their principal amount and interest on

maturity from Companies facing financial difficulties faces credit risk. Some other major

risks faced by the investors are foreign investment risks, horizon risk, inflation risk, capital

risk, on-going return risk, degradation in the value of the property. These risks when

identified can be majorly managed through guidance from experts and diversification of the

property portfolio. Investors should avoid leverage margin trading. Risk can also be reduced

by investing in companies which have a stable and consistent record of stock in the past.

Further, in the recession period, investors should avoid investing in levered companies.

However, a positive cash flow should be managed by the investors for high returns (Duggan

& Benzinga, 2014).

Correlation indicates the degree of relationship between the two variables or sectors.

It helps the investors to diversify their risk in investments by decreasing the correlation

between them. Commercial and residential sectors as two variables have a strong correlation

between them. This means that the value for both will fluctuate in same directions. According

to some economist, there are same factors that affect the demand for both the sectors.

However, demand plays an important factor for measuring the relationship between these two

markets. For example, increase in the household market cause the commercial market to also

increase indicating a strong positive correlation. Similarly, a negative correlation is seen

8

when there is unemployment caused in the commercial market affecting the household

market (Konigsberg, 2018). However, this indicates that these sectors are more risky as they

have a positive correlation. This portfolio risk can be diluted by using the assets that have a

lesser amount of correlation, thus contributing to an efficient portfolio (Reisman, 2014).

Property economics overall view

1. Changes to interest rates

When any change is seen in the interest rates, it has a significant impact on mixed

development. A high interest rate will make it difficult for the developer to gather

funds for financing from different sources. Further, this leads to increase in costs of

loans and other funding’s. The new mixed development proposal will have to face a

challenge by this factor as for commercial and residential development, huge amount

of funds are required.

2. Federal government changes (increase) to withholding tax applicable to offshore REIT

investors

Retail Estate Investment Trust (REIT) investors are tax efficient investors in the

property industry. They will tend to invest less in the property due to increased

changes in the federal government to withhold tax applicable to them. This will reduce

their profits as they have to pay more tax. From the profits they earn, they are required

to benefit their investors and shareholders by paying out 90% out of it. So, they will be

left with lesser profits after tax disappointing the shareholders.

3. Rising unemployment

Rising unemployment will have a major impact on the new mixed development

proposal. This will make the proposal less attractive. The problem of unemployment

leads to less capital in the hands of developer and as well as investors. There will be

fewer saving from the household sectors leading to decrease channelizing and

when there is unemployment caused in the commercial market affecting the household

market (Konigsberg, 2018). However, this indicates that these sectors are more risky as they

have a positive correlation. This portfolio risk can be diluted by using the assets that have a

lesser amount of correlation, thus contributing to an efficient portfolio (Reisman, 2014).

Property economics overall view

1. Changes to interest rates

When any change is seen in the interest rates, it has a significant impact on mixed

development. A high interest rate will make it difficult for the developer to gather

funds for financing from different sources. Further, this leads to increase in costs of

loans and other funding’s. The new mixed development proposal will have to face a

challenge by this factor as for commercial and residential development, huge amount

of funds are required.

2. Federal government changes (increase) to withholding tax applicable to offshore REIT

investors

Retail Estate Investment Trust (REIT) investors are tax efficient investors in the

property industry. They will tend to invest less in the property due to increased

changes in the federal government to withhold tax applicable to them. This will reduce

their profits as they have to pay more tax. From the profits they earn, they are required

to benefit their investors and shareholders by paying out 90% out of it. So, they will be

left with lesser profits after tax disappointing the shareholders.

3. Rising unemployment

Rising unemployment will have a major impact on the new mixed development

proposal. This will make the proposal less attractive. The problem of unemployment

leads to less capital in the hands of developer and as well as investors. There will be

fewer saving from the household sectors leading to decrease channelizing and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

mobilizing of funds. Therefore, it will have a direct impact on the developer as they

will be less investor in the market.

4. Rapid growth in supply of residential property - to be delivered / settled within 3 years

This rapid growth will affect the commercial property proposal by the developer to the

investors. The corporate investors will not find this proposal attractive as they want the

commercial development also fast along with residential property supply. On the contrary, this

will benefit the household investors in many ways like working from home in case of

emergencies.

5. Continued strength / investment in the resources sector

Investment in the resources sector will affect the investments in the new mixed development

proposal; thereby, putting the developer in great loss. Resources sector needs a great

development for the uplift of the economy and the country thereby, letting the property

industry to struggle in the market for its development. The government and the legislation

will majorly emphasize on this sector instead of property development.

6. Rising interest rates

A rise in the interest rate will make the investors more prone to invest in property. This will

generate huge loss to the developers. Therefore, it will have a direct impact on the mixed used

development proposal. The investors will not find this situation attractive to buy or purchase

the property and will wait for the market conditions to improve and fall in the interest rates.

References

Berry, J.N., Deddis, N.G., McGreal, W.S. (2013). Urban Regeneration: Property Investment

and Development: Taylor & Francis.

Yardney, B. (2018, April 6). Property Development Guide Part 5 – Financing your Project.

Retrieved from https://propertyupdate.com.au/property-development-finance/.

Migl, A. (2016). Capital Structure in the Modern World: Springer.

mobilizing of funds. Therefore, it will have a direct impact on the developer as they

will be less investor in the market.

4. Rapid growth in supply of residential property - to be delivered / settled within 3 years

This rapid growth will affect the commercial property proposal by the developer to the

investors. The corporate investors will not find this proposal attractive as they want the

commercial development also fast along with residential property supply. On the contrary, this

will benefit the household investors in many ways like working from home in case of

emergencies.

5. Continued strength / investment in the resources sector

Investment in the resources sector will affect the investments in the new mixed development

proposal; thereby, putting the developer in great loss. Resources sector needs a great

development for the uplift of the economy and the country thereby, letting the property

industry to struggle in the market for its development. The government and the legislation

will majorly emphasize on this sector instead of property development.

6. Rising interest rates

A rise in the interest rate will make the investors more prone to invest in property. This will

generate huge loss to the developers. Therefore, it will have a direct impact on the mixed used

development proposal. The investors will not find this situation attractive to buy or purchase

the property and will wait for the market conditions to improve and fall in the interest rates.

References

Berry, J.N., Deddis, N.G., McGreal, W.S. (2013). Urban Regeneration: Property Investment

and Development: Taylor & Francis.

Yardney, B. (2018, April 6). Property Development Guide Part 5 – Financing your Project.

Retrieved from https://propertyupdate.com.au/property-development-finance/.

Migl, A. (2016). Capital Structure in the Modern World: Springer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Trisha, (2018, February 28). Capital Structure: Concept, Definition and Importance.

Retrieved from http://www.yourarticlelibrary.com/financial-management/capital-structure/

capital-structure-concept-definition-and-importance/44063.

Lumen, (2018, February 28). Capital Structure Considerations. Retrieved from

https://courses.lumenlearning.com/boundless-finance/chapter/capital-structure-

considerations/.

Fletcher, P. & Pendleton, A. (2018, February 28). Identifying and Managing Project Finance

Risks: Overview (UK). Retrieved from

https://www.milbank.com/images/content/1/6/16376/5-564-5045-pl-milbank-updated.pdf.

World Bank Group (2018, February 28). Risk Allocation, Bankability and Mitigation in

Project Financed Transactions. Retrieved from http://ppp.worldbank.org/public-private-

partnership/financing/risk-allocation-mitigation.

Duggan, W. & Benzinga (2014, November 18). 4 Ways to Manage Risk in your Portfolio.

Retrieved from https://www.benzinga.com/general/education/14/11/5012949/4-ways-to-

manage-risk-in-your-portfolio.

Koenigsberg, R. (2018, February 28). A Link between Commercial and Residential Real

Estate. Retrieved from http://aiprops.com/newsletter/april/Koenigsberg-

Bulletin_commercial-and-residential.pdf.

Reisman, E. (2014, May 19). What is Correlation and Why Does it Matter for your Portfolio?

[Blog post]. Retrieved from: https://www.stockrover.com/blog/what-is-correlation-and-why-

does-it-matter-for-your-portfolio/.

Trisha, (2018, February 28). Capital Structure: Concept, Definition and Importance.

Retrieved from http://www.yourarticlelibrary.com/financial-management/capital-structure/

capital-structure-concept-definition-and-importance/44063.

Lumen, (2018, February 28). Capital Structure Considerations. Retrieved from

https://courses.lumenlearning.com/boundless-finance/chapter/capital-structure-

considerations/.

Fletcher, P. & Pendleton, A. (2018, February 28). Identifying and Managing Project Finance

Risks: Overview (UK). Retrieved from

https://www.milbank.com/images/content/1/6/16376/5-564-5045-pl-milbank-updated.pdf.

World Bank Group (2018, February 28). Risk Allocation, Bankability and Mitigation in

Project Financed Transactions. Retrieved from http://ppp.worldbank.org/public-private-

partnership/financing/risk-allocation-mitigation.

Duggan, W. & Benzinga (2014, November 18). 4 Ways to Manage Risk in your Portfolio.

Retrieved from https://www.benzinga.com/general/education/14/11/5012949/4-ways-to-

manage-risk-in-your-portfolio.

Koenigsberg, R. (2018, February 28). A Link between Commercial and Residential Real

Estate. Retrieved from http://aiprops.com/newsletter/april/Koenigsberg-

Bulletin_commercial-and-residential.pdf.

Reisman, E. (2014, May 19). What is Correlation and Why Does it Matter for your Portfolio?

[Blog post]. Retrieved from: https://www.stockrover.com/blog/what-is-correlation-and-why-

does-it-matter-for-your-portfolio/.

11

Kobzeff, J. (2016, July 19). Capitalization Rate: How to Compute and Use. Retrieved from:

http://www.proapod.com/Articles/capitalization_rate.htm.

Kobzeff, J. (2016, July 19). Capitalization Rate: How to Compute and Use. Retrieved from:

http://www.proapod.com/Articles/capitalization_rate.htm.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.