Property Investment and Risk Management Report: Investment Analysis

VerifiedAdded on 2022/10/12

|28

|3570

|106

Report

AI Summary

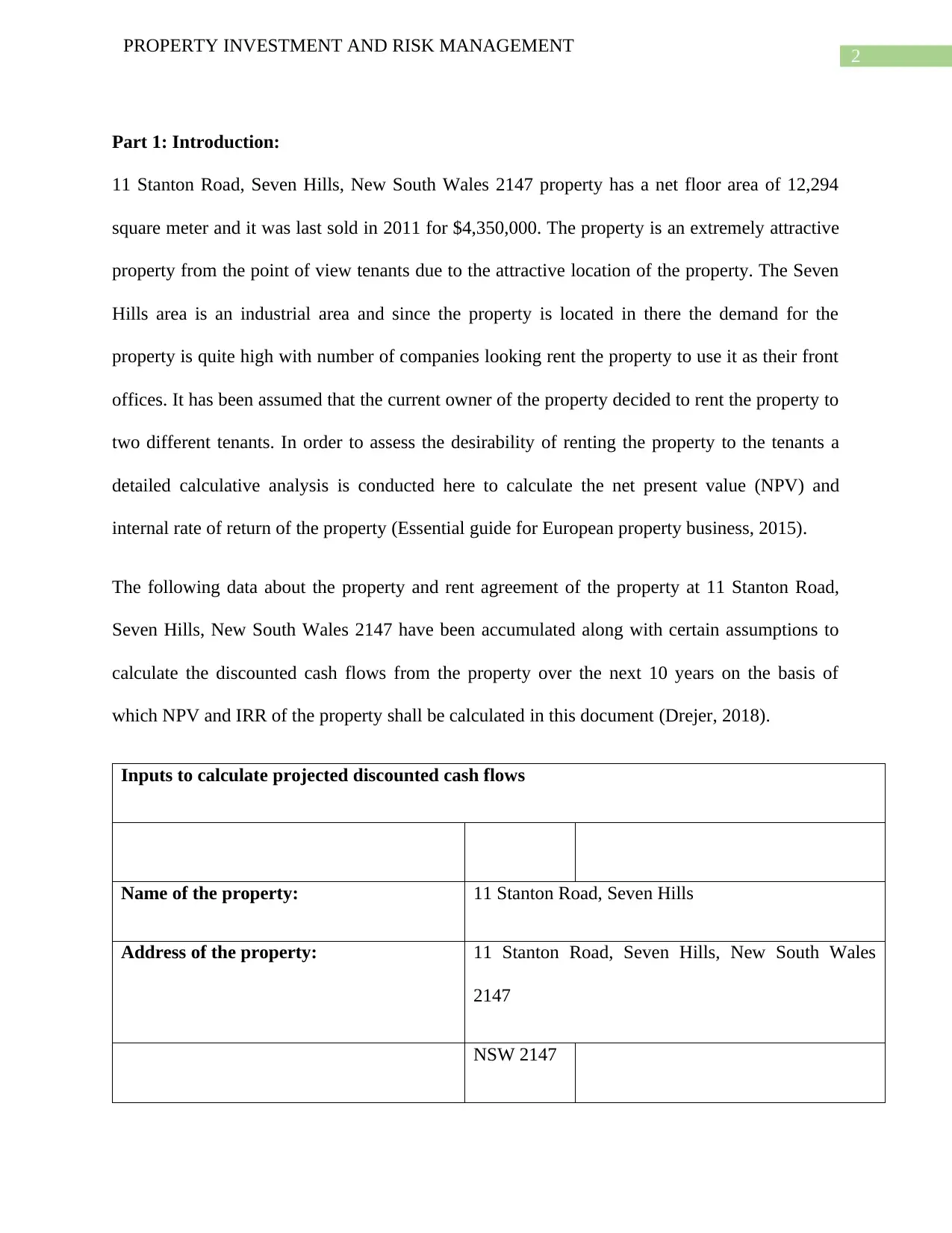

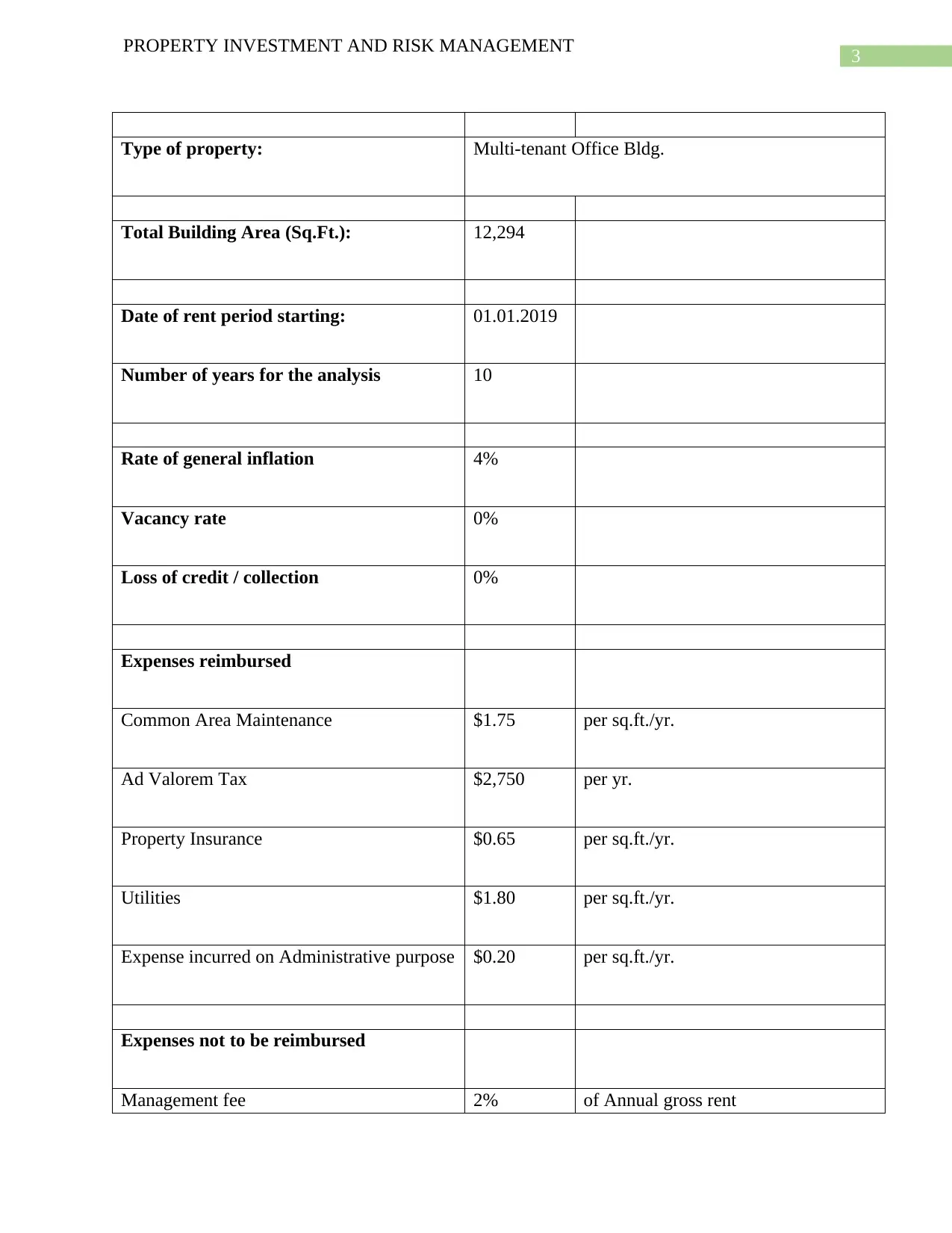

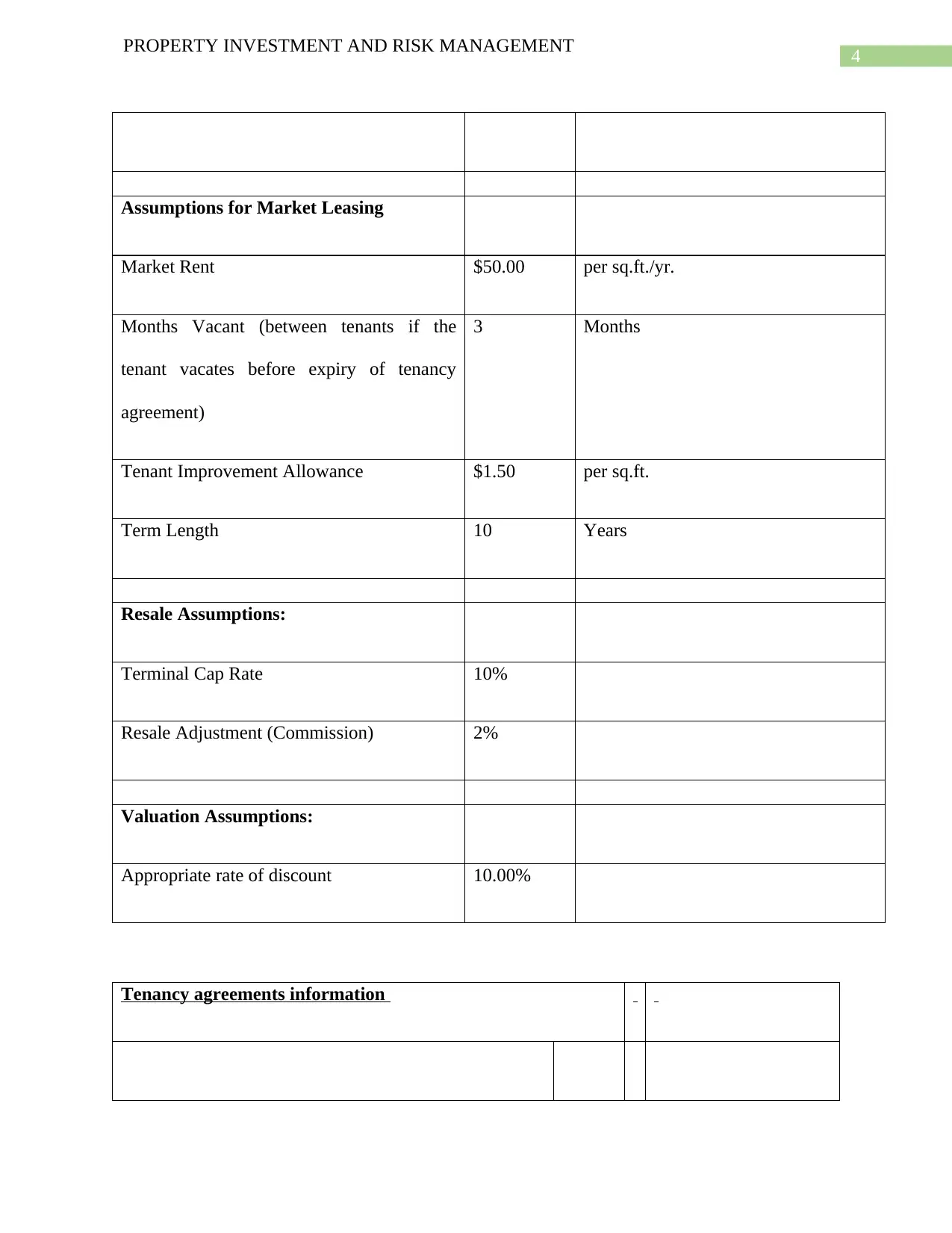

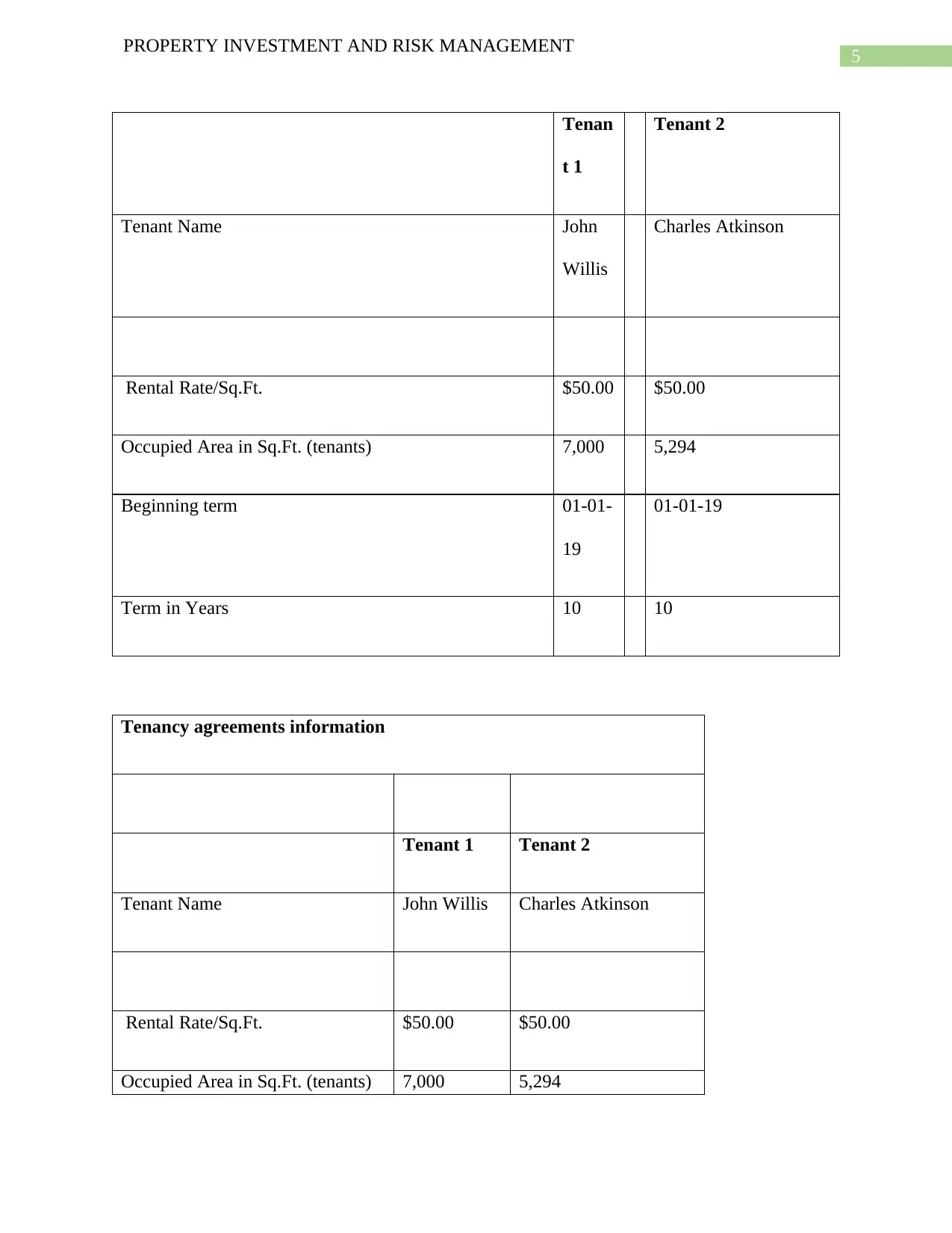

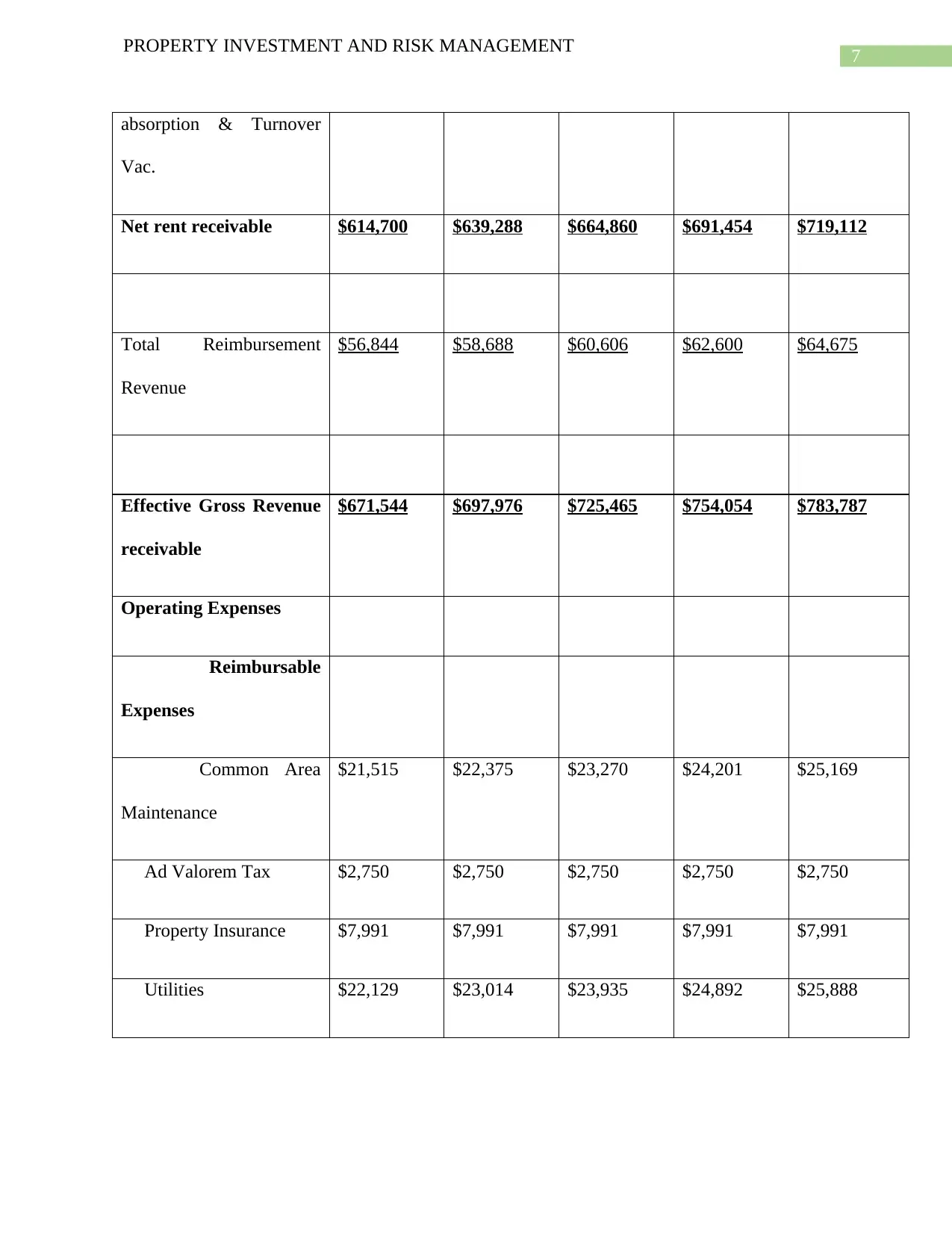

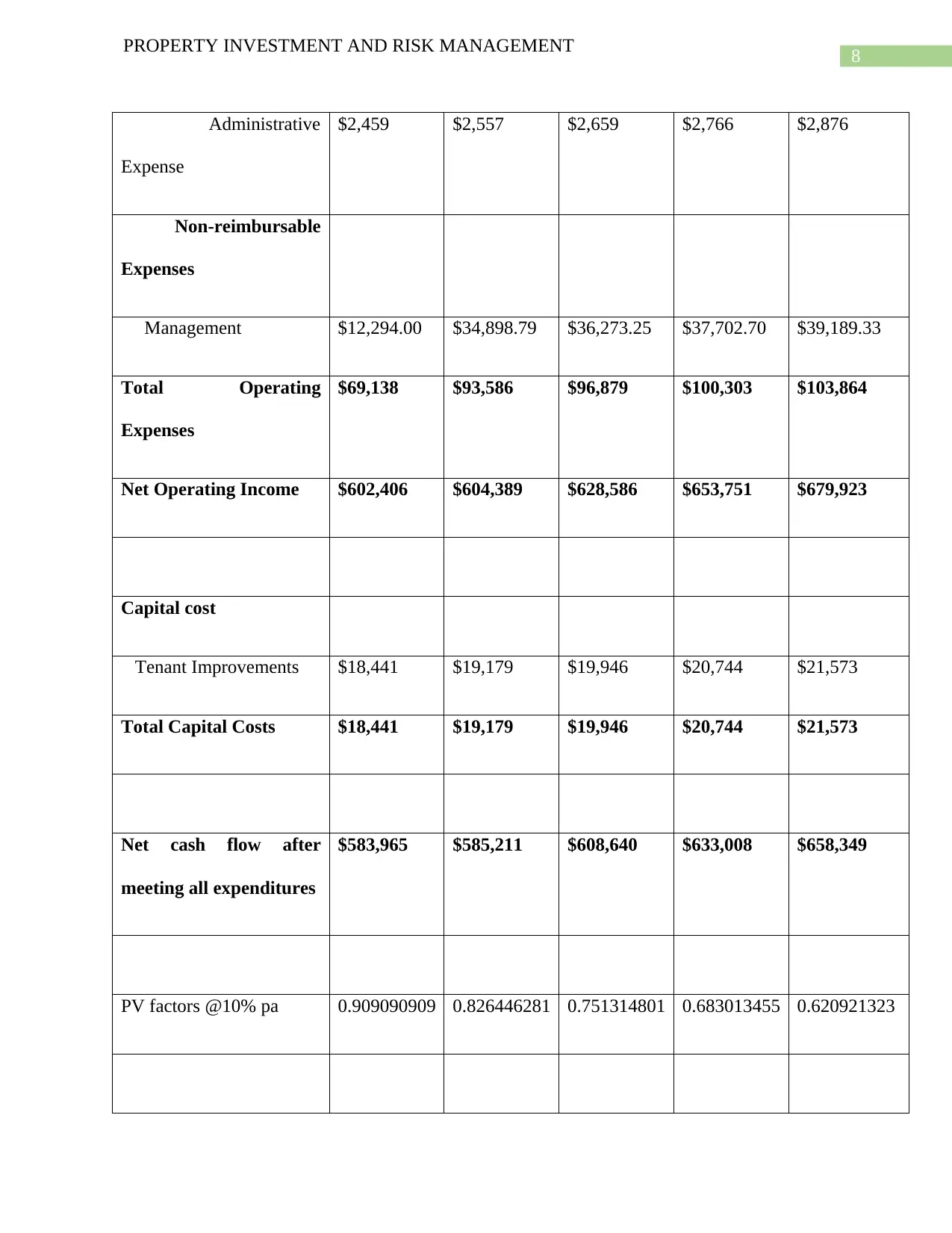

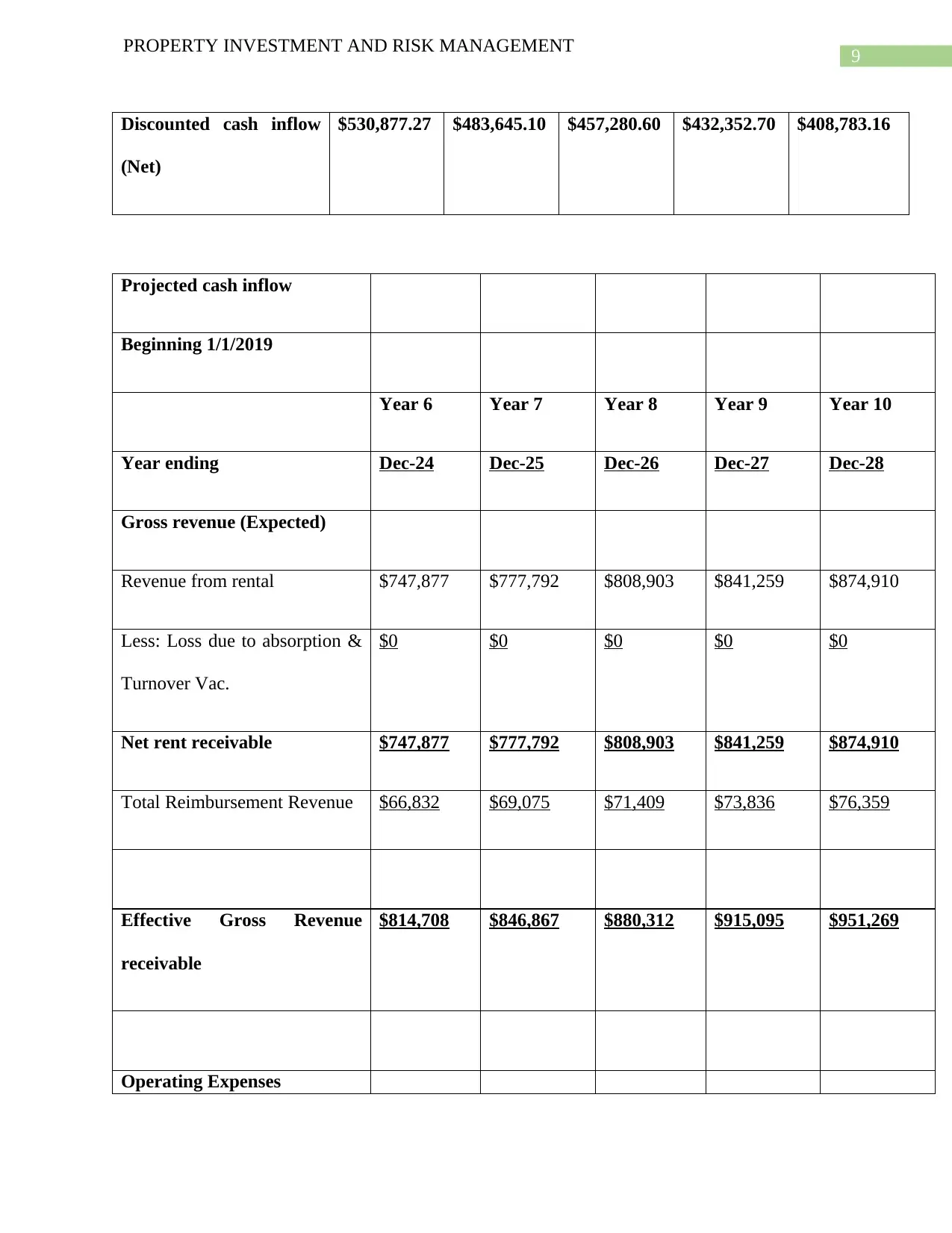

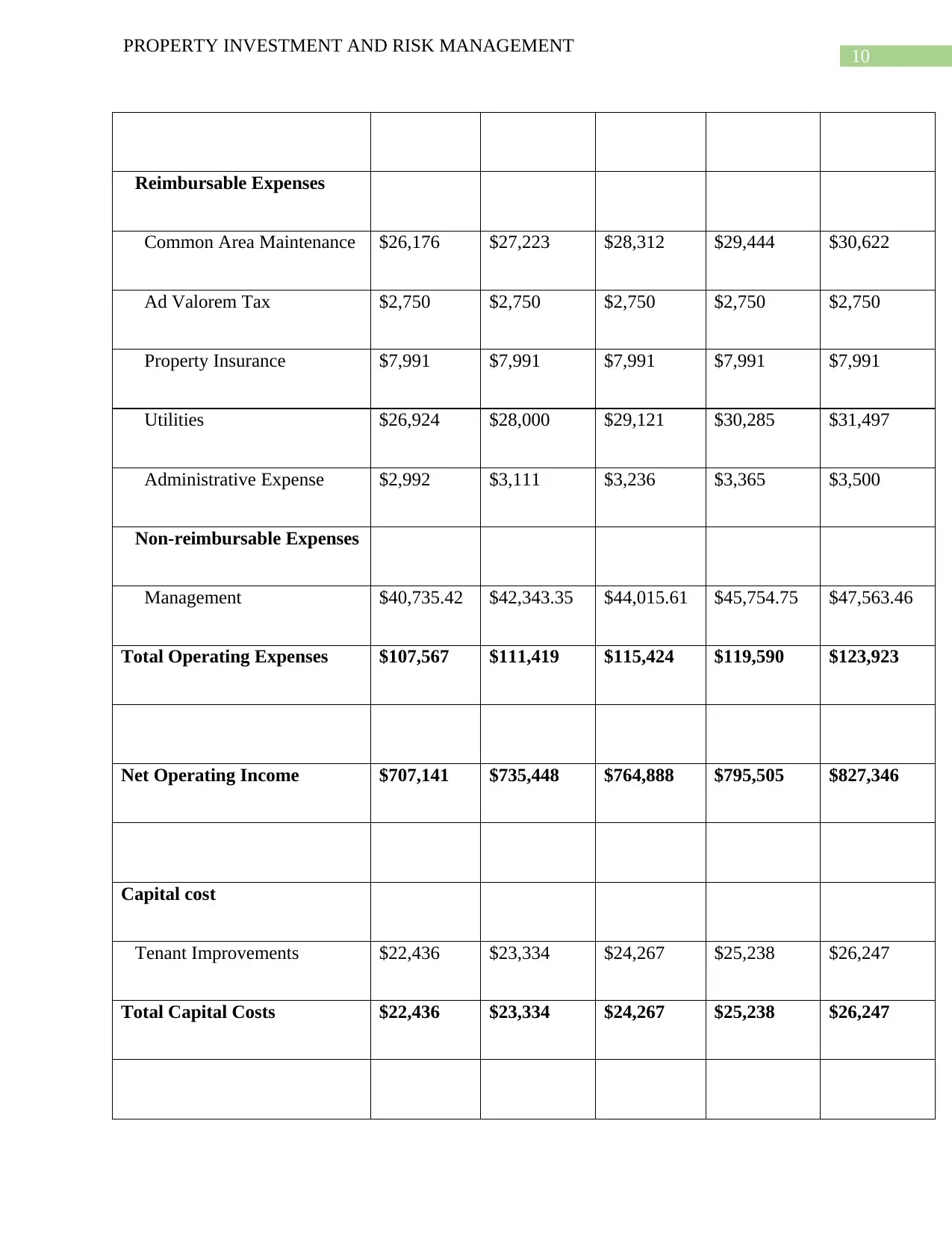

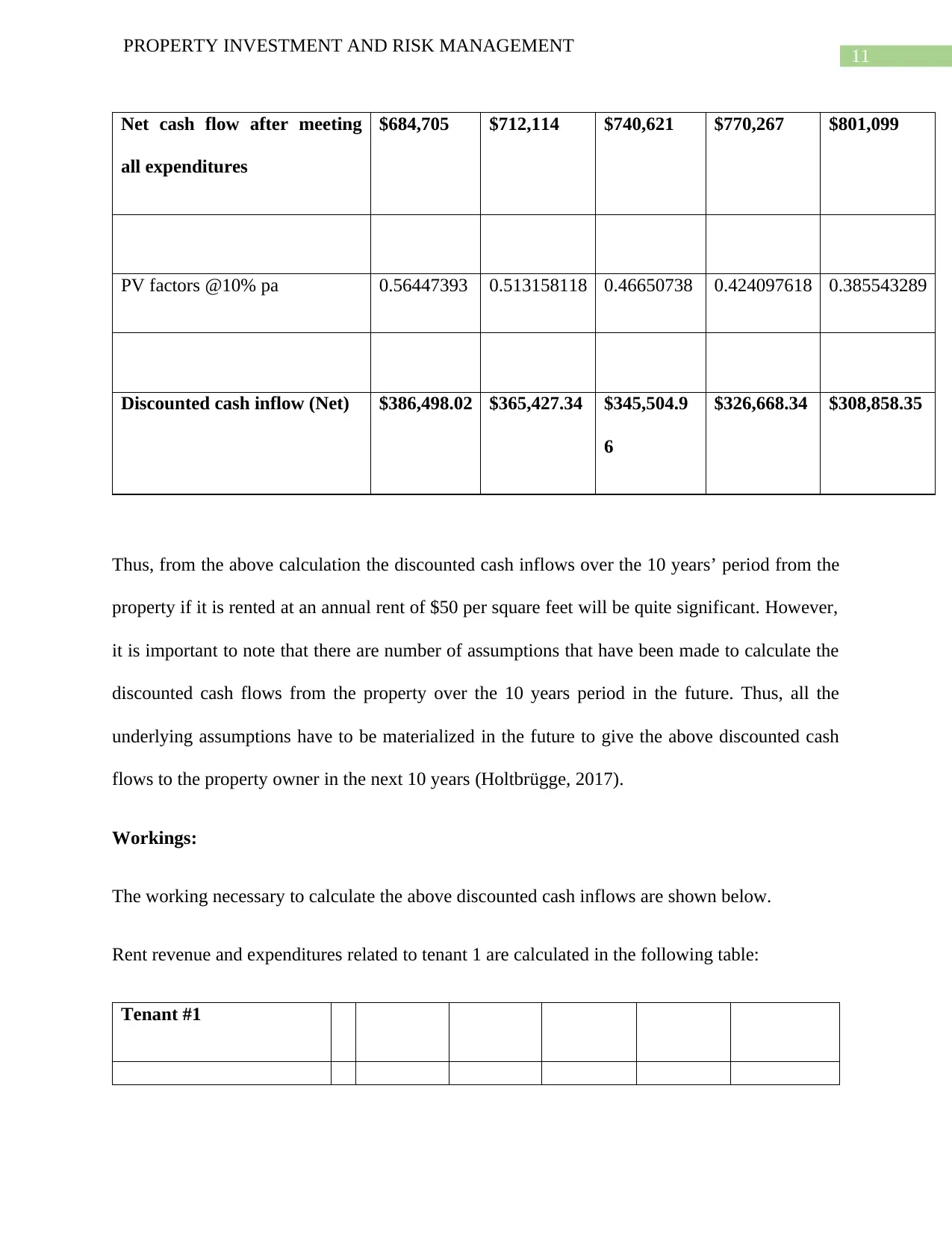

This report presents a detailed investment analysis of a multi-tenant office building located at 11 Stanton Road, Seven Hills, New South Wales. The analysis utilizes a discounted cash flow (DCF) model to project cash flows over a ten-year period, incorporating various inputs such as rental rates, expenses, and vacancy rates. The report calculates the Net Present Value (NPV) and Internal Rate of Return (IRR) to assess the financial viability of renting the property to two tenants. The analysis includes detailed workings for revenue and expenditure calculations for each tenant, along with a sensitivity analysis based on different assumptions. Furthermore, the report discusses the impact of leverage, risk, and taxation on the investment analysis, providing a comprehensive evaluation of the property's investment potential. The report concludes with recommendations for the property owner based on the financial analysis.

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.