Detailed Report: IFRS 16 Amendments on Property, Plant, and Equipment

VerifiedAdded on 2023/06/04

|22

|7178

|465

Report

AI Summary

This report provides an in-depth analysis of the Exposure Draft ED/2017/4, specifically focusing on the proposed amendments to IAS 16 regarding Property, Plant, and Equipment (PPE). The primary amendment discussed involves the prohibition of deducting proceeds from selling items produced while bringing an asset to its intended use from the cost of the asset. Instead, such proceeds, along with the associated production costs, are to be recognized in profit or loss. The report examines the background of these proposed changes, the invitation to comment on the Exposure Draft, and the specific amendments to IAS 16, including the addition of paragraph 20A and amendments to paragraph 17. It also includes draft amendments to other standards, such as IFRIC Interpretation 20. The report covers the Board's approval of the Exposure Draft, the basis for its conclusions, and includes an alternative view. The key focus is on understanding the implications of these amendments for financial reporting and the treatment of PPE costs and revenues during the asset's development phase. The document is a comprehensive review of the proposed changes to accounting standards related to PPE.

IFRS®Standards

Exposure Draft ED/2017/4

June 2017

Comments to be received by 19 October 2017

Property, Plant and Equipment—

Proceeds before Intended Use

Proposed amendments to IAS 16

Exposure Draft ED/2017/4

June 2017

Comments to be received by 19 October 2017

Property, Plant and Equipment—

Proceeds before Intended Use

Proposed amendments to IAS 16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Property,Plant and Equipment—

Proceeds before Intended Use

(Proposed amendments to IAS 16)

Comments to be received by 19 October 2017

Proceeds before Intended Use

(Proposed amendments to IAS 16)

Comments to be received by 19 October 2017

Exposure Draft ED/2017/4Property, Plant and Equipment—Proceeds before Intended Use(Proposed amendments

to IAS 16) is published by the International Accounting Standards Board (Board) for comment only.The

proposals may be modified in the light of the comments received before being issued in final form.

Comments need to be received by 19 October 2017 and should be submitted in writing to the address

below,by email to commentletters@ifrs.org or electronically using our ‘Open for comment’page at:

http://ifrs.org/projects/open-for-comment/.

All comments willbe on the public record and posted on our website atwww.ifrs.org unless the

respondent requests confidentiality.Such requests will not normally be granted unless supported by a

good reason, for example, commercial confidence.Please see our website for details on this and how we

use your Personal Data.

Disclaimer:To the extent permitted by applicable law,the Board and the IFRS Foundation (the

Foundation)expressly disclaim all liability howsoever arising from this publication or any translation

thereof whether in contract,tort or otherwise to any person in respect of any claims or losses of any

nature including direct, indirect, incidental or consequential loss, punitive damages, penalties or costs.

Information contained in this publication does not constitute advice and should not be substituted for

the services of an appropriately qualified professional.

ISBN: 978-1-911040-63-7

Copyright © 2017 IFRS Foundation

All rights reserved.Reproduction and use rights are strictly limited.Please contact the Foundation for

further details at licences@ifrs.org.

Copies of IASB® publications may be obtained from the Foundation’s Publications Department.Please

addresspublication and copyright matters to publications@ifrs.orgor visit our web shop at

https://shop.ifrs.org.

The Foundation has trade marks registered around the world (Marks) including ‘IAS®

’, ‘IASB®

’, the IASB®

logo,‘IFRIC®

’, ‘IFRS®

’, the IFRS®logo,‘IFRS for SMEs®

’, the IFRS for SMEs®logo,the ‘Hexagon Device’,

‘International Accounting Standards®

’, ‘International Financial Reporting Standards®

’, ‘NIIF®

’ and ‘SIC®

’.

Further details of the Foundation’s Marks are available from the Foundation on request.

The Foundation is a not-for-profitcorporation under the GeneralCorporation Law ofthe State of

Delaware,USA and operatesin England and Wales as an overseascompany (Company number:

FC023235) with its principal office at 30 Cannon Street, London, EC4M 6XH.

to IAS 16) is published by the International Accounting Standards Board (Board) for comment only.The

proposals may be modified in the light of the comments received before being issued in final form.

Comments need to be received by 19 October 2017 and should be submitted in writing to the address

below,by email to commentletters@ifrs.org or electronically using our ‘Open for comment’page at:

http://ifrs.org/projects/open-for-comment/.

All comments willbe on the public record and posted on our website atwww.ifrs.org unless the

respondent requests confidentiality.Such requests will not normally be granted unless supported by a

good reason, for example, commercial confidence.Please see our website for details on this and how we

use your Personal Data.

Disclaimer:To the extent permitted by applicable law,the Board and the IFRS Foundation (the

Foundation)expressly disclaim all liability howsoever arising from this publication or any translation

thereof whether in contract,tort or otherwise to any person in respect of any claims or losses of any

nature including direct, indirect, incidental or consequential loss, punitive damages, penalties or costs.

Information contained in this publication does not constitute advice and should not be substituted for

the services of an appropriately qualified professional.

ISBN: 978-1-911040-63-7

Copyright © 2017 IFRS Foundation

All rights reserved.Reproduction and use rights are strictly limited.Please contact the Foundation for

further details at licences@ifrs.org.

Copies of IASB® publications may be obtained from the Foundation’s Publications Department.Please

addresspublication and copyright matters to publications@ifrs.orgor visit our web shop at

https://shop.ifrs.org.

The Foundation has trade marks registered around the world (Marks) including ‘IAS®

’, ‘IASB®

’, the IASB®

logo,‘IFRIC®

’, ‘IFRS®

’, the IFRS®logo,‘IFRS for SMEs®

’, the IFRS for SMEs®logo,the ‘Hexagon Device’,

‘International Accounting Standards®

’, ‘International Financial Reporting Standards®

’, ‘NIIF®

’ and ‘SIC®

’.

Further details of the Foundation’s Marks are available from the Foundation on request.

The Foundation is a not-for-profitcorporation under the GeneralCorporation Law ofthe State of

Delaware,USA and operatesin England and Wales as an overseascompany (Company number:

FC023235) with its principal office at 30 Cannon Street, London, EC4M 6XH.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONTENTS

from page

INTRODUCTION 4

INVITATION TO COMMENT 4

[DRAFT] AMENDMENTS TO IAS 16 PROPERTY, PLANT AND EQUIPMENT 6

[DRAFT] AMENDMENTS TO OTHER STANDARDS 8

APPROVAL BY THE BOARD OF EXPOSURE DRAFT PROPERTY, PLANT AND

EQUIPMENT—PROCEEDS BEFORE INTENDED USE PUBLISHED IN

JUNE 2017 9

BASIS FOR CONCLUSIONS ON THE EXPOSURE DRAFT PROPERTY, PLANT

AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE 10

ALTERNATIVE VIEW 17

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation3

from page

INTRODUCTION 4

INVITATION TO COMMENT 4

[DRAFT] AMENDMENTS TO IAS 16 PROPERTY, PLANT AND EQUIPMENT 6

[DRAFT] AMENDMENTS TO OTHER STANDARDS 8

APPROVAL BY THE BOARD OF EXPOSURE DRAFT PROPERTY, PLANT AND

EQUIPMENT—PROCEEDS BEFORE INTENDED USE PUBLISHED IN

JUNE 2017 9

BASIS FOR CONCLUSIONS ON THE EXPOSURE DRAFT PROPERTY, PLANT

AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE 10

ALTERNATIVE VIEW 17

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction

In this Exposure Draft,the International Accounting Standards Board (Board)proposes to

amend IAS 16Property,Plantand Equipment. The amendments would prohibit deducting

from the cost of an item of property, plant and equipment any proceeds from selling items

produced while bringing that asset to the location and condition necessary for it to be

capable of operating in the manner intended by management.Instead,an entity would

recognise those sales proceeds in profit or loss.

Background

Paragraph 17 of IAS 16 specifies examples of costs directly attributable to bringing an item

of property,plant and equipmentto the location and condition necessary for itto be

capable of operating in the manner intended by management.One such example is the

costs of testing.Paragraph 17(e) of IAS 16 states that the cost of an item of property, plant

and equipment includes the costs of testing whether the asset is functioning properly, after

deducting the net proceeds from selling any items produced while bringing the asset to that

location and condition.

The IFRS Interpretations Committee (Committee)received a request asking two questions

about paragraph 17(e) of IAS 16:

(a) whether the proceeds referred to in that paragraph relate only to items produced

from testing; and

(b) whether an entity deducts from the cost of an item of property, plant and

equipment any proceeds that exceed the costs of testing.

When discussing the issue, the Committee identified a number of related questions about

the cost of property,plant and equipment. After exploring differentapproaches,the

Committee recommended that the Board propose an amendment to IAS 16 to prohibit

deducting sales proceeds from the cost of an item of property, plant and equipment.The

Board agreed with the Committee’s recommendations.

Invitation to comment

The Board invites comments on the proposals in this Exposure Draft,particularly on the

questions set out below.Comments are most helpful if they:

(a) comment on the question as stated;

(b) indicate the specific paragraph(s) to which they relate;

(c) contain a clear rationale;

(d) identify any wording in the proposals that is difficult to translate; and

(e) include any alternative the Board should consider.

The Board is not requesting comments on matters that are not considered in this Exposure

Draft.

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 4

In this Exposure Draft,the International Accounting Standards Board (Board)proposes to

amend IAS 16Property,Plantand Equipment. The amendments would prohibit deducting

from the cost of an item of property, plant and equipment any proceeds from selling items

produced while bringing that asset to the location and condition necessary for it to be

capable of operating in the manner intended by management.Instead,an entity would

recognise those sales proceeds in profit or loss.

Background

Paragraph 17 of IAS 16 specifies examples of costs directly attributable to bringing an item

of property,plant and equipmentto the location and condition necessary for itto be

capable of operating in the manner intended by management.One such example is the

costs of testing.Paragraph 17(e) of IAS 16 states that the cost of an item of property, plant

and equipment includes the costs of testing whether the asset is functioning properly, after

deducting the net proceeds from selling any items produced while bringing the asset to that

location and condition.

The IFRS Interpretations Committee (Committee)received a request asking two questions

about paragraph 17(e) of IAS 16:

(a) whether the proceeds referred to in that paragraph relate only to items produced

from testing; and

(b) whether an entity deducts from the cost of an item of property, plant and

equipment any proceeds that exceed the costs of testing.

When discussing the issue, the Committee identified a number of related questions about

the cost of property,plant and equipment. After exploring differentapproaches,the

Committee recommended that the Board propose an amendment to IAS 16 to prohibit

deducting sales proceeds from the cost of an item of property, plant and equipment.The

Board agreed with the Committee’s recommendations.

Invitation to comment

The Board invites comments on the proposals in this Exposure Draft,particularly on the

questions set out below.Comments are most helpful if they:

(a) comment on the question as stated;

(b) indicate the specific paragraph(s) to which they relate;

(c) contain a clear rationale;

(d) identify any wording in the proposals that is difficult to translate; and

(e) include any alternative the Board should consider.

The Board is not requesting comments on matters that are not considered in this Exposure

Draft.

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 4

Comments should be submitted in writing so as to be received no later than 19 October

2017.

Question for respondents

The Board is proposing to amend IAS 16 to prohibit deducting from the cost of an item

of property, plant and equipment any proceeds from selling items produced while

bringing that asset to the location and condition necessary for it to be capable of

operating in the manner intended by management.Instead, an entity would recognise

the proceeds from selling such items, and the costs of producing those items, in profit

or loss.

Do you agree with the Board’s proposal? Why or why not? If not, what alternative would

you propose, and why?

How to comment

Comments should be submitted using one of the following methods.

Electronically

(our preferred method)

Visit the ‘Open for comment’ page, which can be found at:

http://ifrs.org/projects/open-for-comment/

Email Email comments can be sent to: commentletters@ifrs.org

Postal IFRS Foundation

30 Cannon Street

London EC4M 6XH

United Kingdom

All comments will be on the public record and posted on our website at www.ifrs.org unless

the respondent requests confidentiality.Such requests will not normally be granted unless

supported by a good reason, for example, commercial confidence.Please see our website for

details on this and how we use your personal data.

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation5

2017.

Question for respondents

The Board is proposing to amend IAS 16 to prohibit deducting from the cost of an item

of property, plant and equipment any proceeds from selling items produced while

bringing that asset to the location and condition necessary for it to be capable of

operating in the manner intended by management.Instead, an entity would recognise

the proceeds from selling such items, and the costs of producing those items, in profit

or loss.

Do you agree with the Board’s proposal? Why or why not? If not, what alternative would

you propose, and why?

How to comment

Comments should be submitted using one of the following methods.

Electronically

(our preferred method)

Visit the ‘Open for comment’ page, which can be found at:

http://ifrs.org/projects/open-for-comment/

Email Email comments can be sent to: commentletters@ifrs.org

Postal IFRS Foundation

30 Cannon Street

London EC4M 6XH

United Kingdom

All comments will be on the public record and posted on our website at www.ifrs.org unless

the respondent requests confidentiality.Such requests will not normally be granted unless

supported by a good reason, for example, commercial confidence.Please see our website for

details on this and how we use your personal data.

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

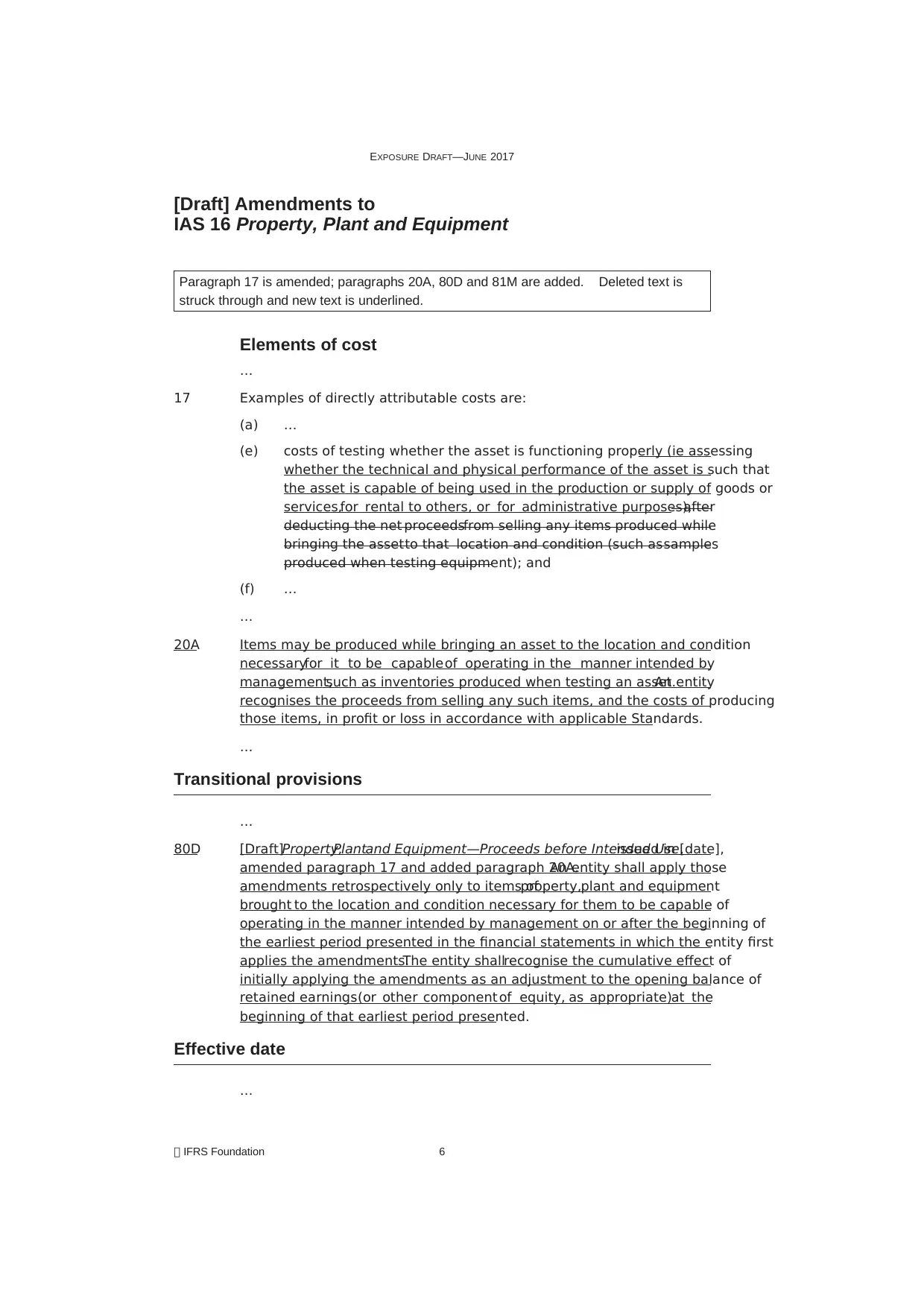

[Draft] Amendments to

IAS 16 Property, Plant and Equipment

Paragraph 17 is amended; paragraphs 20A, 80D and 81M are added. Deleted text is

struck through and new text is underlined.

Elements of cost

…

17 Examples of directly attributable costs are:

(a) …

(e) costs of testing whether the asset is functioning properly (ie assessing

whether the technical and physical performance of the asset is such that

the asset is capable of being used in the production or supply of goods or

services,for rental to others, or for administrative purposes),after

deducting the net proceedsfrom selling any items produced while

bringing the assetto that location and condition (such assamples

produced when testing equipment); and

(f) …

…

20A Items may be produced while bringing an asset to the location and condition

necessaryfor it to be capableof operating in the manner intended by

management,such as inventories produced when testing an asset.An entity

recognises the proceeds from selling any such items, and the costs of producing

those items, in profit or loss in accordance with applicable Standards.

…

Transitional provisions

…

80D [Draft]Property,Plantand Equipment—Proceeds before Intended Use,issued in [date],

amended paragraph 17 and added paragraph 20A.An entity shall apply those

amendments retrospectively only to items ofproperty,plant and equipment

brought to the location and condition necessary for them to be capable of

operating in the manner intended by management on or after the beginning of

the earliest period presented in the financial statements in which the entity first

applies the amendments.The entity shallrecognise the cumulative effect of

initially applying the amendments as an adjustment to the opening balance of

retained earnings(or other component of equity, as appropriate)at the

beginning of that earliest period presented.

Effective date

…

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 6

IAS 16 Property, Plant and Equipment

Paragraph 17 is amended; paragraphs 20A, 80D and 81M are added. Deleted text is

struck through and new text is underlined.

Elements of cost

…

17 Examples of directly attributable costs are:

(a) …

(e) costs of testing whether the asset is functioning properly (ie assessing

whether the technical and physical performance of the asset is such that

the asset is capable of being used in the production or supply of goods or

services,for rental to others, or for administrative purposes),after

deducting the net proceedsfrom selling any items produced while

bringing the assetto that location and condition (such assamples

produced when testing equipment); and

(f) …

…

20A Items may be produced while bringing an asset to the location and condition

necessaryfor it to be capableof operating in the manner intended by

management,such as inventories produced when testing an asset.An entity

recognises the proceeds from selling any such items, and the costs of producing

those items, in profit or loss in accordance with applicable Standards.

…

Transitional provisions

…

80D [Draft]Property,Plantand Equipment—Proceeds before Intended Use,issued in [date],

amended paragraph 17 and added paragraph 20A.An entity shall apply those

amendments retrospectively only to items ofproperty,plant and equipment

brought to the location and condition necessary for them to be capable of

operating in the manner intended by management on or after the beginning of

the earliest period presented in the financial statements in which the entity first

applies the amendments.The entity shallrecognise the cumulative effect of

initially applying the amendments as an adjustment to the opening balance of

retained earnings(or other component of equity, as appropriate)at the

beginning of that earliest period presented.

Effective date

…

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

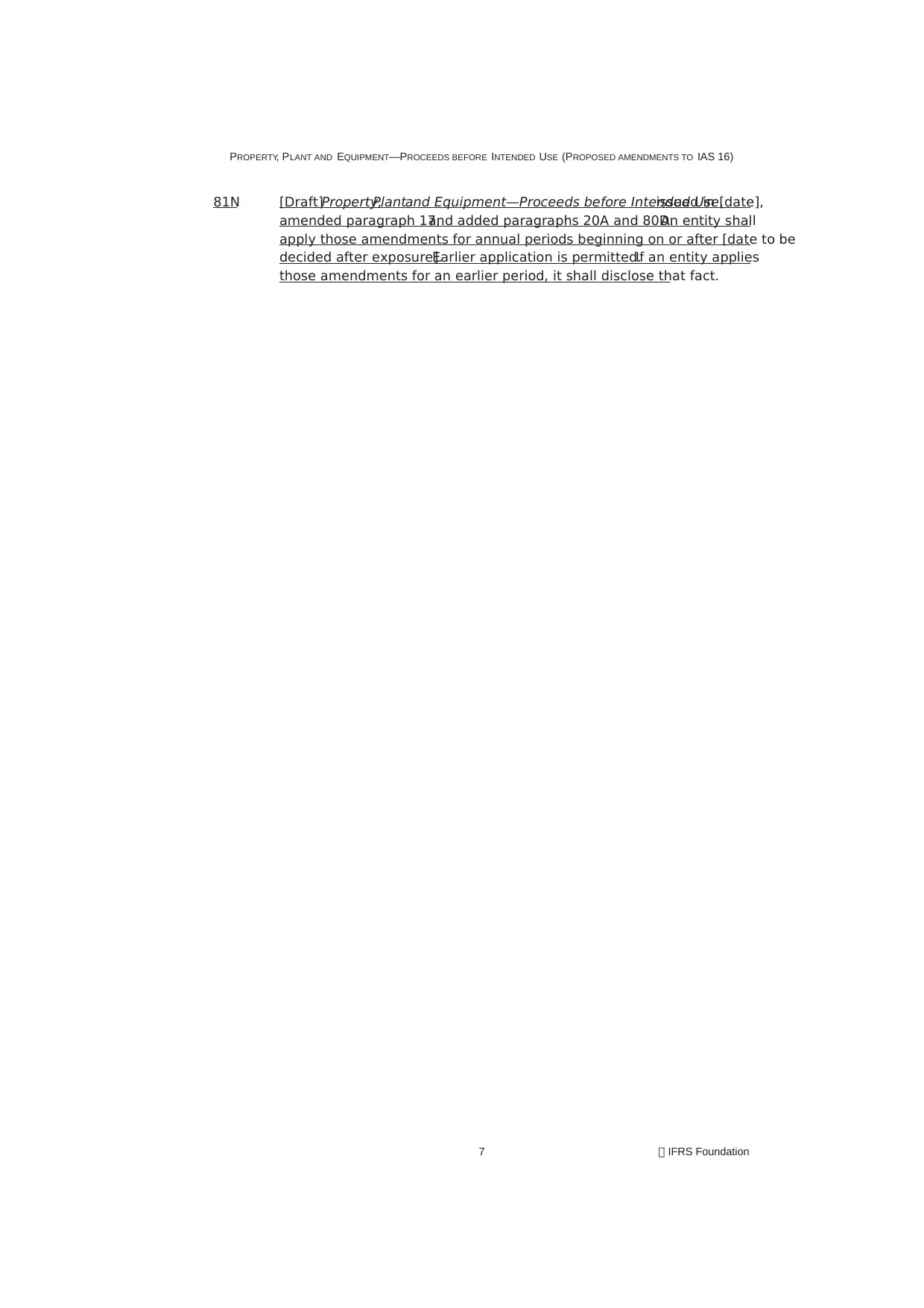

81N [Draft]Property,Plantand Equipment—Proceeds before Intended Use,issued in [date],

amended paragraph 17,and added paragraphs 20A and 80D.An entity shall

apply those amendments for annual periods beginning on or after [date to be

decided after exposure].Earlier application is permitted.If an entity applies

those amendments for an earlier period, it shall disclose that fact.

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation7

amended paragraph 17,and added paragraphs 20A and 80D.An entity shall

apply those amendments for annual periods beginning on or after [date to be

decided after exposure].Earlier application is permitted.If an entity applies

those amendments for an earlier period, it shall disclose that fact.

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation7

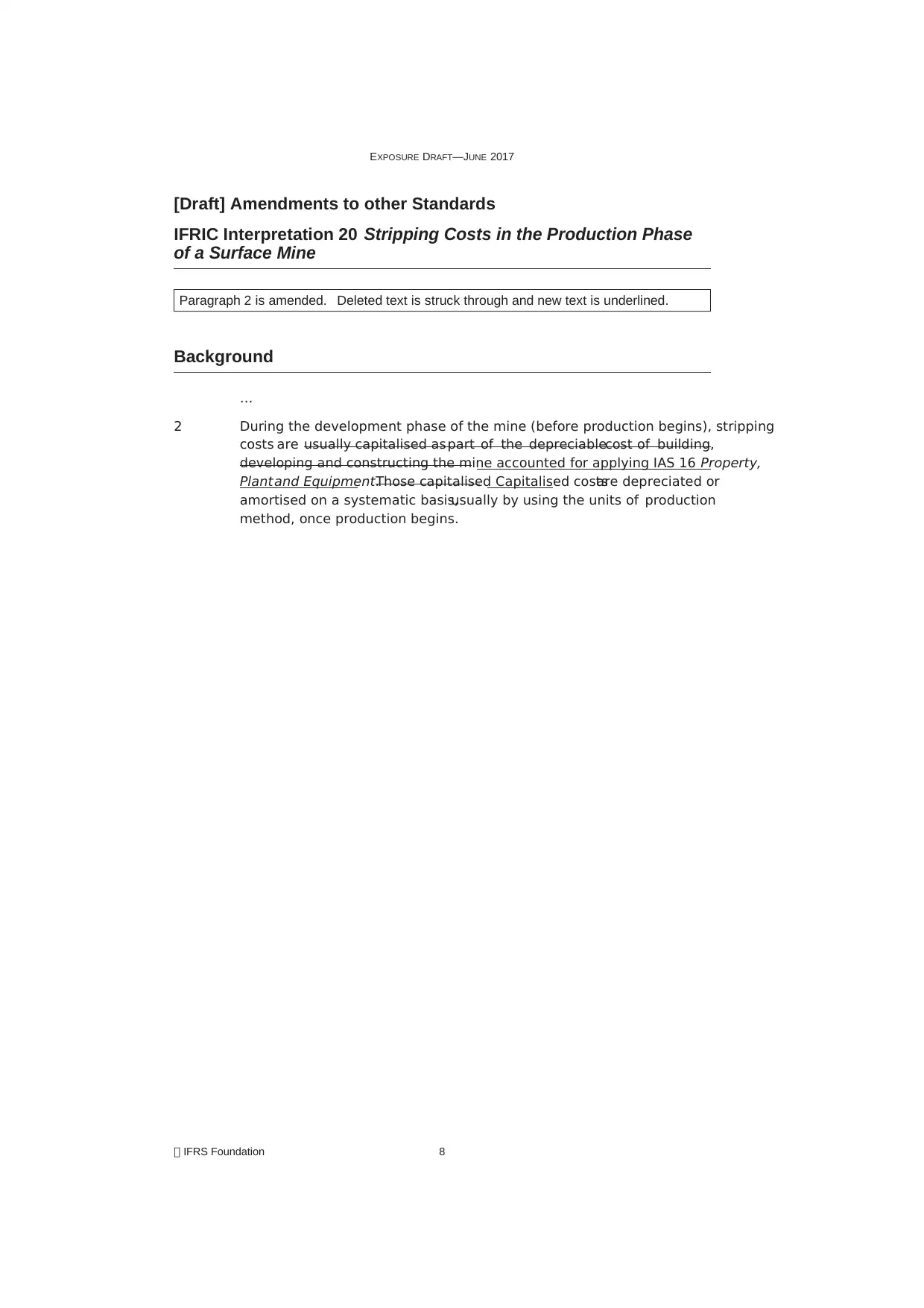

[Draft] Amendments to other Standards

IFRIC Interpretation 20 Stripping Costs in the Production Phase

of a Surface Mine

Paragraph 2 is amended. Deleted text is struck through and new text is underlined.

Background

…

2 During the development phase of the mine (before production begins), stripping

costs are usually capitalised aspart of the depreciablecost of building,

developing and constructing the mine accounted for applying IAS 16 Property,

Plantand Equipment.Those capitalised Capitalised costsare depreciated or

amortised on a systematic basis,usually by using the units of production

method, once production begins.

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 8

IFRIC Interpretation 20 Stripping Costs in the Production Phase

of a Surface Mine

Paragraph 2 is amended. Deleted text is struck through and new text is underlined.

Background

…

2 During the development phase of the mine (before production begins), stripping

costs are usually capitalised aspart of the depreciablecost of building,

developing and constructing the mine accounted for applying IAS 16 Property,

Plantand Equipment.Those capitalised Capitalised costsare depreciated or

amortised on a systematic basis,usually by using the units of production

method, once production begins.

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

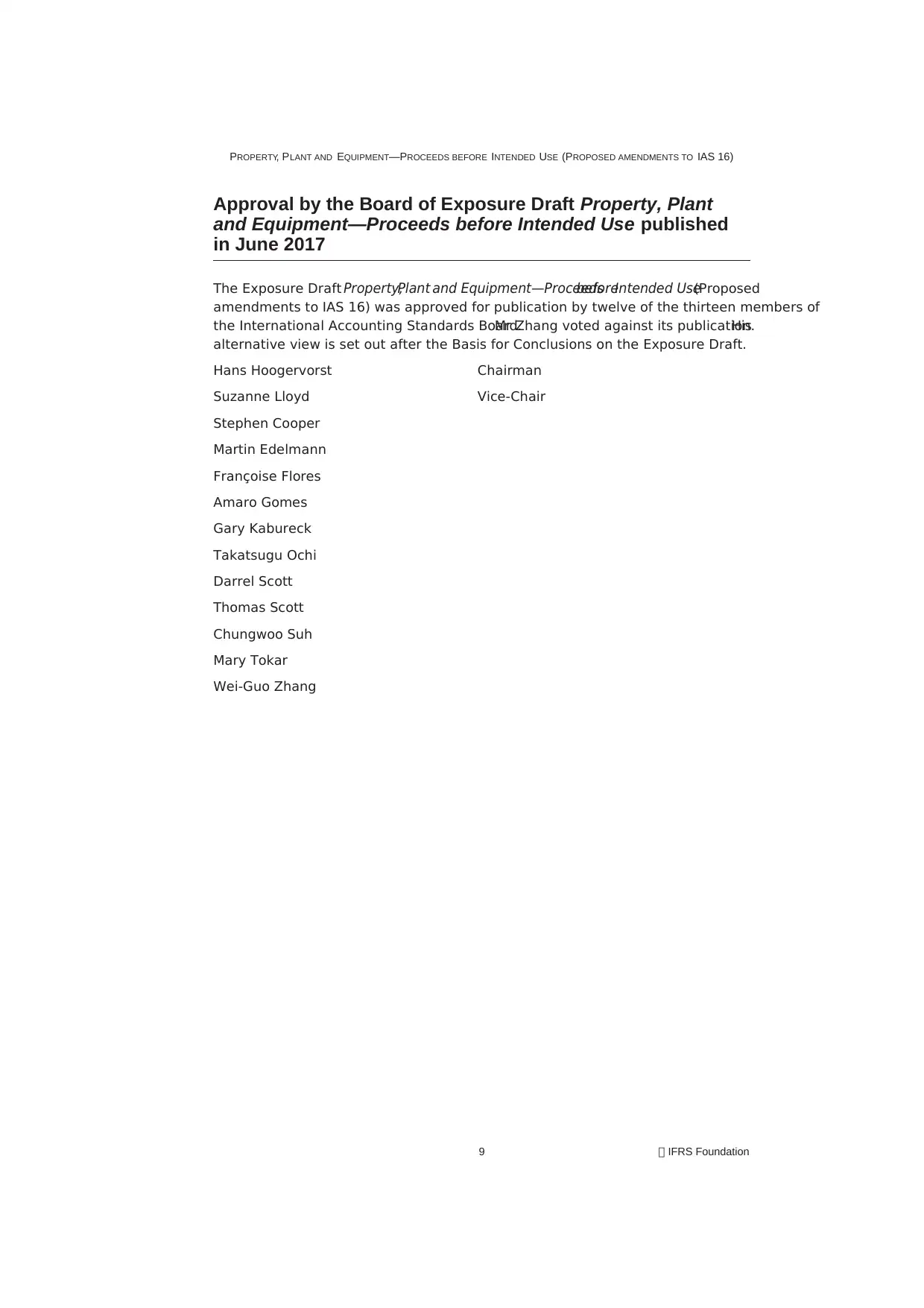

Approval by the Board of Exposure Draft Property, Plant

and Equipment—Proceeds before Intended Use published

in June 2017

The Exposure Draft Property,Plant and Equipment—ProceedsbeforeIntended Use(Proposed

amendments to IAS 16) was approved for publication by twelve of the thirteen members of

the International Accounting Standards Board.Mr Zhang voted against its publication.His

alternative view is set out after the Basis for Conclusions on the Exposure Draft.

Hans Hoogervorst Chairman

Suzanne Lloyd Vice-Chair

Stephen Cooper

Martin Edelmann

Françoise Flores

Amaro Gomes

Gary Kabureck

Takatsugu Ochi

Darrel Scott

Thomas Scott

Chungwoo Suh

Mary Tokar

Wei-Guo Zhang

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation9

and Equipment—Proceeds before Intended Use published

in June 2017

The Exposure Draft Property,Plant and Equipment—ProceedsbeforeIntended Use(Proposed

amendments to IAS 16) was approved for publication by twelve of the thirteen members of

the International Accounting Standards Board.Mr Zhang voted against its publication.His

alternative view is set out after the Basis for Conclusions on the Exposure Draft.

Hans Hoogervorst Chairman

Suzanne Lloyd Vice-Chair

Stephen Cooper

Martin Edelmann

Françoise Flores

Amaro Gomes

Gary Kabureck

Takatsugu Ochi

Darrel Scott

Thomas Scott

Chungwoo Suh

Mary Tokar

Wei-Guo Zhang

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Basis for Conclusions on the

Exposure Draft Property, Plant and Equipment—

Proceeds before Intended Use

ThisBasisfor Conclusionsaccompanies,but is not part of, the proposed amendments.It

summarisesthe considerationsof the InternationalAccounting StandardsBoard (Board)when

developing the proposed amendments.IndividualBoard members gave greater weight to some

factors than to others.

Background

BC1 Paragraph 16(b) of IAS 16Property, Plant and Equipmentexplains that the cost of an

item of property,plant and equipment includes costs directly attributable to

bringing that asset to the location and condition necessary for it to be capable of

operating in the manner intended by management.Paragraph 17 ofIAS 16

specifies examples of directly attributable costs.One example specified is the

costs of testing whether the asset is functioning properly,after deducting the

net proceeds from selling any items produced while bringing the asset to that

location and condition.

BC2 The IFRS InterpretationsCommittee (Committee)received a requestasking

whether:

(a) the proceeds specified in paragraph 17(e)of IAS 16 relate only to items

produced from testing; and

(b) an entity deductsfrom the cost of an item of property,plant and

equipment any proceeds that exceed the costs of testing.

BC3 The Committee noted that feedback from its outreach on the request indicated

that:

(a) the issue mainly affects a few industries,such as the extractive and

petrochemical industries.

(b) diverse reporting methodsare applied. Some entitiesdeduct only

proceeds from selling items produced from testing;others deduct all

sales proceeds until the asset is in the location and condition necessary

for it to be capable of operating in the manner intended by management

(ie available for use).For some entities, the proceeds deducted from the

cost of an item of property, plant and equipment can be significant and

can exceed the costs of testing.

BC4 In addition, feedback from outreach indicated thatentities use different

methods to assess when an item of property,plant and equipment is available

for use.

Prohibit deducting sales proceeds from the cost of an

item of property, plant and equipment

BC5 Having considered the Committee’s recommendations,the Board proposes to

amend paragraph 17 of IAS 16 to prohibit deducting from the cost of an item of

property, plant and equipment any proceeds from selling items produced before

that asset is available for use.As a consequence, an entity would recognise such

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 10

Exposure Draft Property, Plant and Equipment—

Proceeds before Intended Use

ThisBasisfor Conclusionsaccompanies,but is not part of, the proposed amendments.It

summarisesthe considerationsof the InternationalAccounting StandardsBoard (Board)when

developing the proposed amendments.IndividualBoard members gave greater weight to some

factors than to others.

Background

BC1 Paragraph 16(b) of IAS 16Property, Plant and Equipmentexplains that the cost of an

item of property,plant and equipment includes costs directly attributable to

bringing that asset to the location and condition necessary for it to be capable of

operating in the manner intended by management.Paragraph 17 ofIAS 16

specifies examples of directly attributable costs.One example specified is the

costs of testing whether the asset is functioning properly,after deducting the

net proceeds from selling any items produced while bringing the asset to that

location and condition.

BC2 The IFRS InterpretationsCommittee (Committee)received a requestasking

whether:

(a) the proceeds specified in paragraph 17(e)of IAS 16 relate only to items

produced from testing; and

(b) an entity deductsfrom the cost of an item of property,plant and

equipment any proceeds that exceed the costs of testing.

BC3 The Committee noted that feedback from its outreach on the request indicated

that:

(a) the issue mainly affects a few industries,such as the extractive and

petrochemical industries.

(b) diverse reporting methodsare applied. Some entitiesdeduct only

proceeds from selling items produced from testing;others deduct all

sales proceeds until the asset is in the location and condition necessary

for it to be capable of operating in the manner intended by management

(ie available for use).For some entities, the proceeds deducted from the

cost of an item of property, plant and equipment can be significant and

can exceed the costs of testing.

BC4 In addition, feedback from outreach indicated thatentities use different

methods to assess when an item of property,plant and equipment is available

for use.

Prohibit deducting sales proceeds from the cost of an

item of property, plant and equipment

BC5 Having considered the Committee’s recommendations,the Board proposes to

amend paragraph 17 of IAS 16 to prohibit deducting from the cost of an item of

property, plant and equipment any proceeds from selling items produced before

that asset is available for use.As a consequence, an entity would recognise such

EXPOSURE DRAFT—JUNE 2017

姝 IFRS Foundation 10

sales proceeds in profit or loss.The Board views its proposals as a simple and

effective way of removing the identified diversity in practice in a manner that

would improve financial reporting.

BC6 The Board concluded that the proposed amendments would provide relevant

information to users of financial statements by requiring entities to recognise all

sales as income (including revenue) when they occur.The existing requirements

in IAS 16 make it difficult for a user to have a clear picture of an entity’s total

revenue in the period because some sales proceeds might be offset against the

cost of property,plant and equipment. Those requirementsalso make it

difficult to have a clear picture of the actualcost of some items of property,

plant and equipment.The cost of those assets can be distorted by deducting

sales proceeds before the assets are available for use.

BC7 During the development of the proposed amendments,the Board observed the

following:

(a) an entity would be required to identify the costs that relate to items

produced and sold before an item of property,plant and equipment is

available for use, and to distinguish those costs from other costs incurred

before that date.This is discussed further in paragraphs BC8–BC10.

(b) before an item of property, plant and equipment is available for use, the

costs of producing any inventories excludes depreciation of that asset.

This is because an entity depreciates an item ofproperty,plant and

equipment only from the date it is available for use.This is discussed

further in paragraph BC11.

BC8 The Board observed that an entity would have to apply judgement in identifying

the costs that relate to items produced and sold before an item of property, plant

and equipment is available for use,and to distinguish those costs from other

costs incurred before that date.However,the proposed amendments would

require little more judgementbeyond that already required to apply IFRS

Standards.For example, an entity is already required to identify and distinguish

the following:

(a) costs directly attributable to making an item ofproperty,plant and

equipment available for use, which the entity includes in the cost of the

asset;

(b) costs of bringing inventories to their presentlocation and condition

included as part of the cost of inventories(paragraph 10 ofIAS 2

Inventories), which it then recognises in profit or loss at the time that the

inventories are sold;

(c) costs excluded from the cost of inventories and recognised as expenses in

the period in which they are incurred,such as abnormalamounts of

wasted materials,labour or other production costs (paragraph 16 of

IAS 2);

(d) costs of stripping activity assets and cost of inventories produced during

the production phase ofa surface mine (IFRIC 20Stripping Costsin the

Production Phase of a Surface Mine); and

(e) costs that it recognises directly in profit or loss, for example:

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation11

effective way of removing the identified diversity in practice in a manner that

would improve financial reporting.

BC6 The Board concluded that the proposed amendments would provide relevant

information to users of financial statements by requiring entities to recognise all

sales as income (including revenue) when they occur.The existing requirements

in IAS 16 make it difficult for a user to have a clear picture of an entity’s total

revenue in the period because some sales proceeds might be offset against the

cost of property,plant and equipment. Those requirementsalso make it

difficult to have a clear picture of the actualcost of some items of property,

plant and equipment.The cost of those assets can be distorted by deducting

sales proceeds before the assets are available for use.

BC7 During the development of the proposed amendments,the Board observed the

following:

(a) an entity would be required to identify the costs that relate to items

produced and sold before an item of property,plant and equipment is

available for use, and to distinguish those costs from other costs incurred

before that date.This is discussed further in paragraphs BC8–BC10.

(b) before an item of property, plant and equipment is available for use, the

costs of producing any inventories excludes depreciation of that asset.

This is because an entity depreciates an item ofproperty,plant and

equipment only from the date it is available for use.This is discussed

further in paragraph BC11.

BC8 The Board observed that an entity would have to apply judgement in identifying

the costs that relate to items produced and sold before an item of property, plant

and equipment is available for use,and to distinguish those costs from other

costs incurred before that date.However,the proposed amendments would

require little more judgementbeyond that already required to apply IFRS

Standards.For example, an entity is already required to identify and distinguish

the following:

(a) costs directly attributable to making an item ofproperty,plant and

equipment available for use, which the entity includes in the cost of the

asset;

(b) costs of bringing inventories to their presentlocation and condition

included as part of the cost of inventories(paragraph 10 ofIAS 2

Inventories), which it then recognises in profit or loss at the time that the

inventories are sold;

(c) costs excluded from the cost of inventories and recognised as expenses in

the period in which they are incurred,such as abnormalamounts of

wasted materials,labour or other production costs (paragraph 16 of

IAS 2);

(d) costs of stripping activity assets and cost of inventories produced during

the production phase ofa surface mine (IFRIC 20Stripping Costsin the

Production Phase of a Surface Mine); and

(e) costs that it recognises directly in profit or loss, for example:

PROPERTY, PLANT AND EQUIPMENT—PROCEEDS BEFORE INTENDED USE (PROPOSED AMENDMENTS TO IAS 16)

姝 IFRS Foundation11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.