Redistributive Effects of Income Tax Reform: Bulgaria vs. Spain

VerifiedAdded on 2023/04/11

|13

|2472

|179

Report

AI Summary

This report critically examines the redistributive effects of income tax reforms in Bulgaria and Spain. Bulgaria shifted from a progressive to a flat tax regime in 2008, aiming to simplify taxation and reduce inequality. The report analyzes the measures taken, including changes to income tax rates and minimum wages. Spain, in response to economic challenges, implemented a tax reform in 2015 to address income inequality, unemployment, and poverty. The report details the new tax schedules, withholding tax reductions, family taxation credits, and adjustments to retirement and social security contributions. The analysis includes the Atkinson and Gini indices to measure inequality. The conclusion summarizes the impact of these reforms, highlighting the effects on household liquidity, income redistribution, and overall economic development in both countries, emphasizing the importance of tax policy in reducing social inequalities and promoting balanced economic growth.

Running head: Public Finance and Taxation Policy

Public Finance and Taxation Policy

Name of Student

Name of the University

Author Note

Public Finance and Taxation Policy

Name of Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Public Finance and Taxation Policy

Executive Summary

The aim of this report is to make critical examination of the redistributive effect of the

income tax reform in the country like Bulgaria and Spain. The report focuses on the measure

taken by both the countries in making taxation amendment. As Bulgaria, in order to make

their taxation structure simpler and easy, they made a shift towards the flat taxation regime

from progressive structure. On the other hand the report further discusses the measure taken

by the Spanish government in their tax reform to tackle the challenges of the income

inequality, unemployment, poverty and many more. At the last the report provide conclusion

on the taxation policy analysis of both the country Spain and Bulgaria.

Public Finance and Taxation Policy

Executive Summary

The aim of this report is to make critical examination of the redistributive effect of the

income tax reform in the country like Bulgaria and Spain. The report focuses on the measure

taken by both the countries in making taxation amendment. As Bulgaria, in order to make

their taxation structure simpler and easy, they made a shift towards the flat taxation regime

from progressive structure. On the other hand the report further discusses the measure taken

by the Spanish government in their tax reform to tackle the challenges of the income

inequality, unemployment, poverty and many more. At the last the report provide conclusion

on the taxation policy analysis of both the country Spain and Bulgaria.

2

Public Finance and Taxation Policy

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

The aim of the recent tax reform in the Bulgaria and Spain......................................................3

Measures introduced in the Tax reform in Bulgaria in the year 2008.......................................4

Measures introduced in the Tax reform in Spain in the year 2015............................................6

Conclusion..................................................................................................................................9

Referencing..............................................................................................................................10

Public Finance and Taxation Policy

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

The aim of the recent tax reform in the Bulgaria and Spain......................................................3

Measures introduced in the Tax reform in Bulgaria in the year 2008.......................................4

Measures introduced in the Tax reform in Spain in the year 2015............................................6

Conclusion..................................................................................................................................9

Referencing..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Public Finance and Taxation Policy

Introduction

This report is about critical examination of redistributive effect of income tax reform

in the Bulgaria and Spain in the year 2008 and 2015 respectively. The purpose of this report

is to analyze and study the effect of income tax reform in the developed and less developed

economies. The report contains a brief introduction of Tax reform and detailed study has

been done to understand the measures taken by the government of the respective country for

the tax reform. Further the report discusses the role of income tax in the redistribution of

income, measures taken by the country in reducing the inequality and equity implication of

both the country. At last the report provide a conclusion on how can income tax can reduce

the social inequalities in the society and provide a way for the balance growth of the

economy.

Discussion

The aim of the recent tax reform in the Bulgaria and Spain.

Tax reform was introduced in the Bulgaria in the year 2008 (Vasilev 2015). The

country Bulgaria has shifted its tax structure from progressive to flat tax rate (Kleven and

Schultz 2014). The government has introduced the tax structure for a period of ten years in the

country. This step is taken by the government because of the following reasons like these flat

tax structure helps in reduction the income inequality, reduction in unemployment, and

minimization of Tax evasion. On the other hand progressive tax structure was not suitable for

the country with limited population. The progressive tax increases with the increase in the

income of the people which provides burdens on the people mind (Kleven and Schultz 2014).

Public Finance and Taxation Policy

Introduction

This report is about critical examination of redistributive effect of income tax reform

in the Bulgaria and Spain in the year 2008 and 2015 respectively. The purpose of this report

is to analyze and study the effect of income tax reform in the developed and less developed

economies. The report contains a brief introduction of Tax reform and detailed study has

been done to understand the measures taken by the government of the respective country for

the tax reform. Further the report discusses the role of income tax in the redistribution of

income, measures taken by the country in reducing the inequality and equity implication of

both the country. At last the report provide a conclusion on how can income tax can reduce

the social inequalities in the society and provide a way for the balance growth of the

economy.

Discussion

The aim of the recent tax reform in the Bulgaria and Spain.

Tax reform was introduced in the Bulgaria in the year 2008 (Vasilev 2015). The

country Bulgaria has shifted its tax structure from progressive to flat tax rate (Kleven and

Schultz 2014). The government has introduced the tax structure for a period of ten years in the

country. This step is taken by the government because of the following reasons like these flat

tax structure helps in reduction the income inequality, reduction in unemployment, and

minimization of Tax evasion. On the other hand progressive tax structure was not suitable for

the country with limited population. The progressive tax increases with the increase in the

income of the people which provides burdens on the people mind (Kleven and Schultz 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Public Finance and Taxation Policy

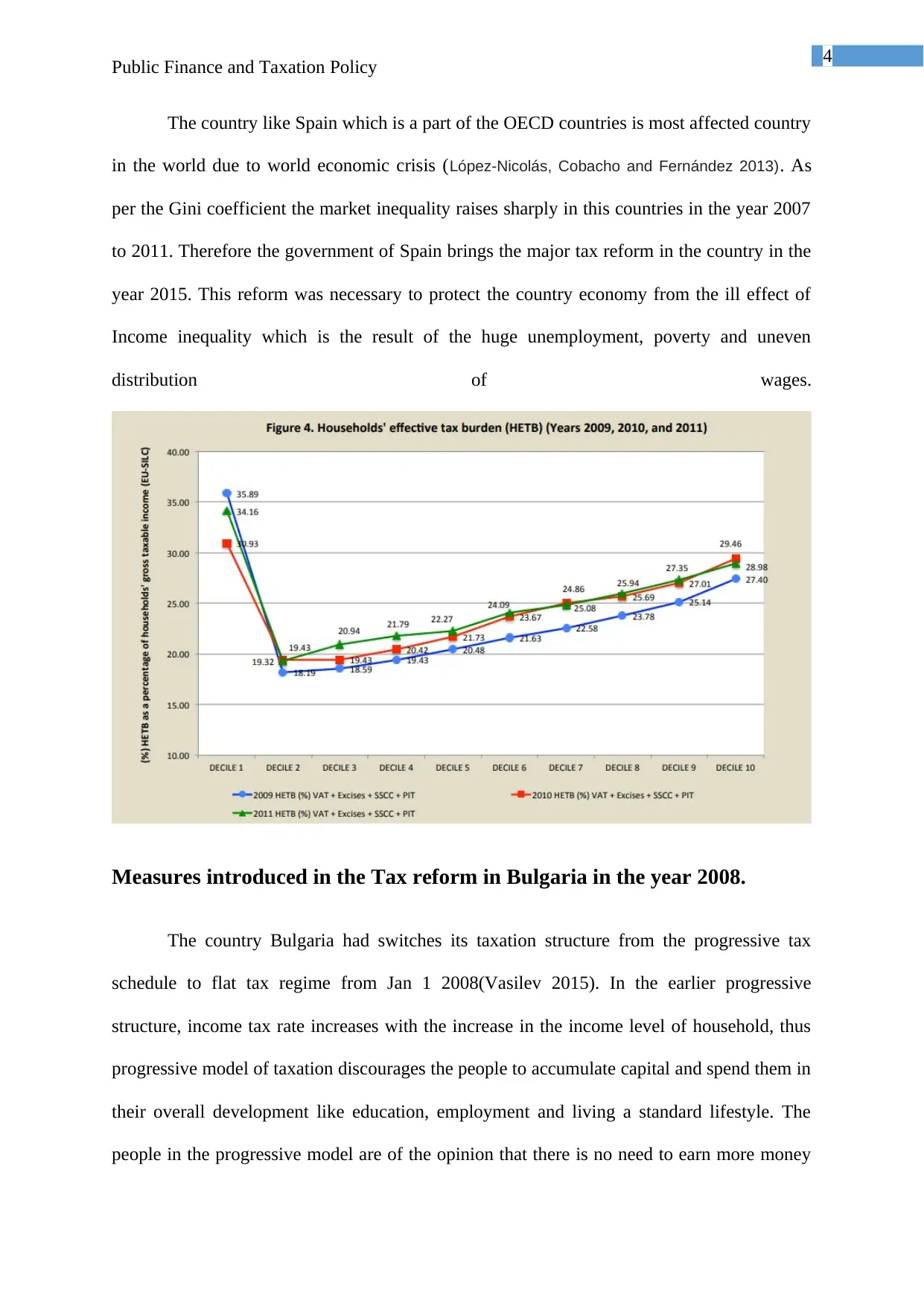

The country like Spain which is a part of the OECD countries is most affected country

in the world due to world economic crisis (López-Nicolás, Cobacho and Fernández 2013). As

per the Gini coefficient the market inequality raises sharply in this countries in the year 2007

to 2011. Therefore the government of Spain brings the major tax reform in the country in the

year 2015. This reform was necessary to protect the country economy from the ill effect of

Income inequality which is the result of the huge unemployment, poverty and uneven

distribution of wages.

Measures introduced in the Tax reform in Bulgaria in the year 2008.

The country Bulgaria had switches its taxation structure from the progressive tax

schedule to flat tax regime from Jan 1 2008(Vasilev 2015). In the earlier progressive

structure, income tax rate increases with the increase in the income level of household, thus

progressive model of taxation discourages the people to accumulate capital and spend them in

their overall development like education, employment and living a standard lifestyle. The

people in the progressive model are of the opinion that there is no need to earn more money

Public Finance and Taxation Policy

The country like Spain which is a part of the OECD countries is most affected country

in the world due to world economic crisis (López-Nicolás, Cobacho and Fernández 2013). As

per the Gini coefficient the market inequality raises sharply in this countries in the year 2007

to 2011. Therefore the government of Spain brings the major tax reform in the country in the

year 2015. This reform was necessary to protect the country economy from the ill effect of

Income inequality which is the result of the huge unemployment, poverty and uneven

distribution of wages.

Measures introduced in the Tax reform in Bulgaria in the year 2008.

The country Bulgaria had switches its taxation structure from the progressive tax

schedule to flat tax regime from Jan 1 2008(Vasilev 2015). In the earlier progressive

structure, income tax rate increases with the increase in the income level of household, thus

progressive model of taxation discourages the people to accumulate capital and spend them in

their overall development like education, employment and living a standard lifestyle. The

people in the progressive model are of the opinion that there is no need to earn more money

5

Public Finance and Taxation Policy

as they have to pay more taxes on their income as their earning rises. As a result of this, there

was a sharp increase in the unemployment, poverty, social inequality (Corak 2013).

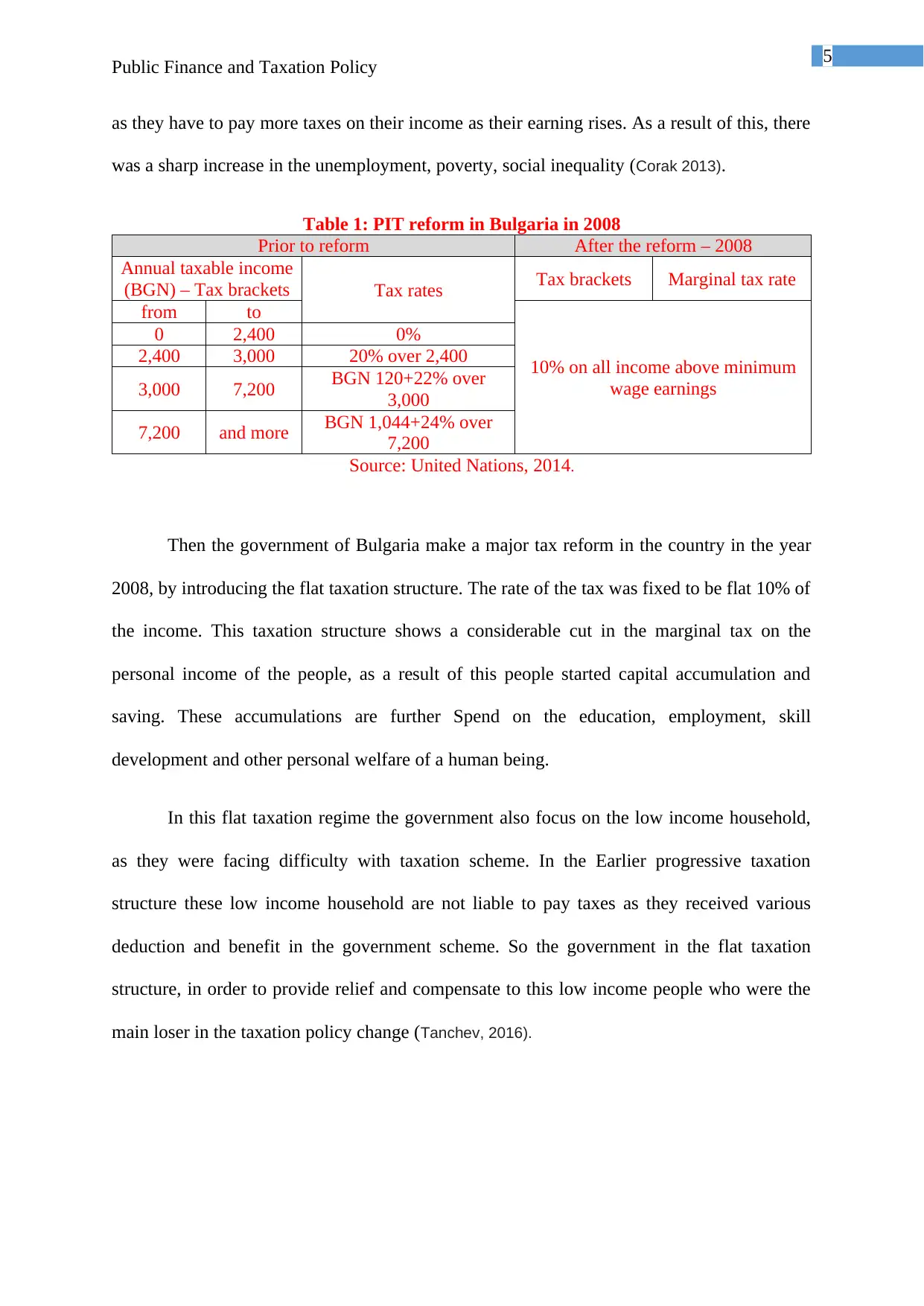

Table 1: PIT reform in Bulgaria in 2008

Prior to reform After the reform – 2008

Annual taxable income

(BGN) – Tax brackets Tax rates Tax brackets Marginal tax rate

from to

10% on all income above minimum

wage earnings

0 2,400 0%

2,400 3,000 20% over 2,400

3,000 7,200 BGN 120+22% over

3,000

7,200 and more BGN 1,044+24% over

7,200

Source: United Nations, 2014.

Then the government of Bulgaria make a major tax reform in the country in the year

2008, by introducing the flat taxation structure. The rate of the tax was fixed to be flat 10% of

the income. This taxation structure shows a considerable cut in the marginal tax on the

personal income of the people, as a result of this people started capital accumulation and

saving. These accumulations are further Spend on the education, employment, skill

development and other personal welfare of a human being.

In this flat taxation regime the government also focus on the low income household,

as they were facing difficulty with taxation scheme. In the Earlier progressive taxation

structure these low income household are not liable to pay taxes as they received various

deduction and benefit in the government scheme. So the government in the flat taxation

structure, in order to provide relief and compensate to this low income people who were the

main loser in the taxation policy change (Tanchev, 2016).

Public Finance and Taxation Policy

as they have to pay more taxes on their income as their earning rises. As a result of this, there

was a sharp increase in the unemployment, poverty, social inequality (Corak 2013).

Table 1: PIT reform in Bulgaria in 2008

Prior to reform After the reform – 2008

Annual taxable income

(BGN) – Tax brackets Tax rates Tax brackets Marginal tax rate

from to

10% on all income above minimum

wage earnings

0 2,400 0%

2,400 3,000 20% over 2,400

3,000 7,200 BGN 120+22% over

3,000

7,200 and more BGN 1,044+24% over

7,200

Source: United Nations, 2014.

Then the government of Bulgaria make a major tax reform in the country in the year

2008, by introducing the flat taxation structure. The rate of the tax was fixed to be flat 10% of

the income. This taxation structure shows a considerable cut in the marginal tax on the

personal income of the people, as a result of this people started capital accumulation and

saving. These accumulations are further Spend on the education, employment, skill

development and other personal welfare of a human being.

In this flat taxation regime the government also focus on the low income household,

as they were facing difficulty with taxation scheme. In the Earlier progressive taxation

structure these low income household are not liable to pay taxes as they received various

deduction and benefit in the government scheme. So the government in the flat taxation

structure, in order to provide relief and compensate to this low income people who were the

main loser in the taxation policy change (Tanchev, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Public Finance and Taxation Policy

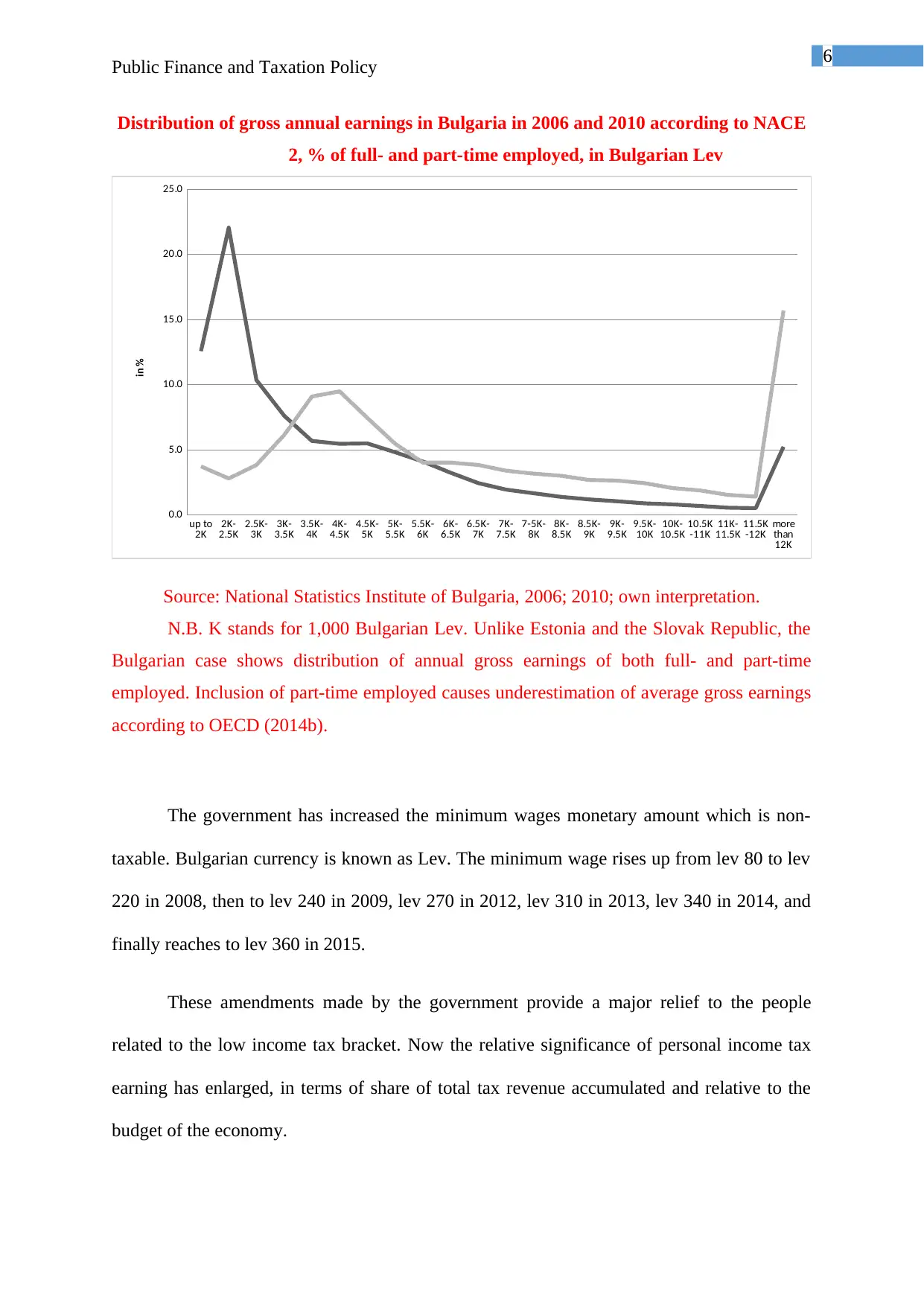

Distribution of gross annual earnings in Bulgaria in 2006 and 2010 according to NACE

2, % of full- and part-time employed, in Bulgarian Lev

up to

2K 2K-

2.5K 2.5K-

3K 3K-

3.5K 3.5K-

4K 4K-

4.5K 4.5K-

5K 5K-

5.5K 5.5K-

6K 6K-

6.5K 6.5K-

7K 7K-

7.5K 7-5K-

8K 8K-

8.5K 8.5K-

9K 9K-

9.5K 9.5K-

10K 10K-

10.5K 10.5K

-11K 11K-

11.5K 11.5K

-12K more

than

12K

0.0

5.0

10.0

15.0

20.0

25.0

in %

Source: National Statistics Institute of Bulgaria, 2006; 2010; own interpretation.

N.B. K stands for 1,000 Bulgarian Lev. Unlike Estonia and the Slovak Republic, the

Bulgarian case shows distribution of annual gross earnings of both full- and part-time

employed. Inclusion of part-time employed causes underestimation of average gross earnings

according to OECD (2014b).

The government has increased the minimum wages monetary amount which is non-

taxable. Bulgarian currency is known as Lev. The minimum wage rises up from lev 80 to lev

220 in 2008, then to lev 240 in 2009, lev 270 in 2012, lev 310 in 2013, lev 340 in 2014, and

finally reaches to lev 360 in 2015.

These amendments made by the government provide a major relief to the people

related to the low income tax bracket. Now the relative significance of personal income tax

earning has enlarged, in terms of share of total tax revenue accumulated and relative to the

budget of the economy.

Public Finance and Taxation Policy

Distribution of gross annual earnings in Bulgaria in 2006 and 2010 according to NACE

2, % of full- and part-time employed, in Bulgarian Lev

up to

2K 2K-

2.5K 2.5K-

3K 3K-

3.5K 3.5K-

4K 4K-

4.5K 4.5K-

5K 5K-

5.5K 5.5K-

6K 6K-

6.5K 6.5K-

7K 7K-

7.5K 7-5K-

8K 8K-

8.5K 8.5K-

9K 9K-

9.5K 9.5K-

10K 10K-

10.5K 10.5K

-11K 11K-

11.5K 11.5K

-12K more

than

12K

0.0

5.0

10.0

15.0

20.0

25.0

in %

Source: National Statistics Institute of Bulgaria, 2006; 2010; own interpretation.

N.B. K stands for 1,000 Bulgarian Lev. Unlike Estonia and the Slovak Republic, the

Bulgarian case shows distribution of annual gross earnings of both full- and part-time

employed. Inclusion of part-time employed causes underestimation of average gross earnings

according to OECD (2014b).

The government has increased the minimum wages monetary amount which is non-

taxable. Bulgarian currency is known as Lev. The minimum wage rises up from lev 80 to lev

220 in 2008, then to lev 240 in 2009, lev 270 in 2012, lev 310 in 2013, lev 340 in 2014, and

finally reaches to lev 360 in 2015.

These amendments made by the government provide a major relief to the people

related to the low income tax bracket. Now the relative significance of personal income tax

earning has enlarged, in terms of share of total tax revenue accumulated and relative to the

budget of the economy.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Public Finance and Taxation Policy

Apart from this, the relative share of the revenues from individual income as a share

in output had become comparatively stable.Thus it can be said that Bulgaria started making

balance growth in the flat tax regime as compare to the progressive taxation structure (Tullock

2013).

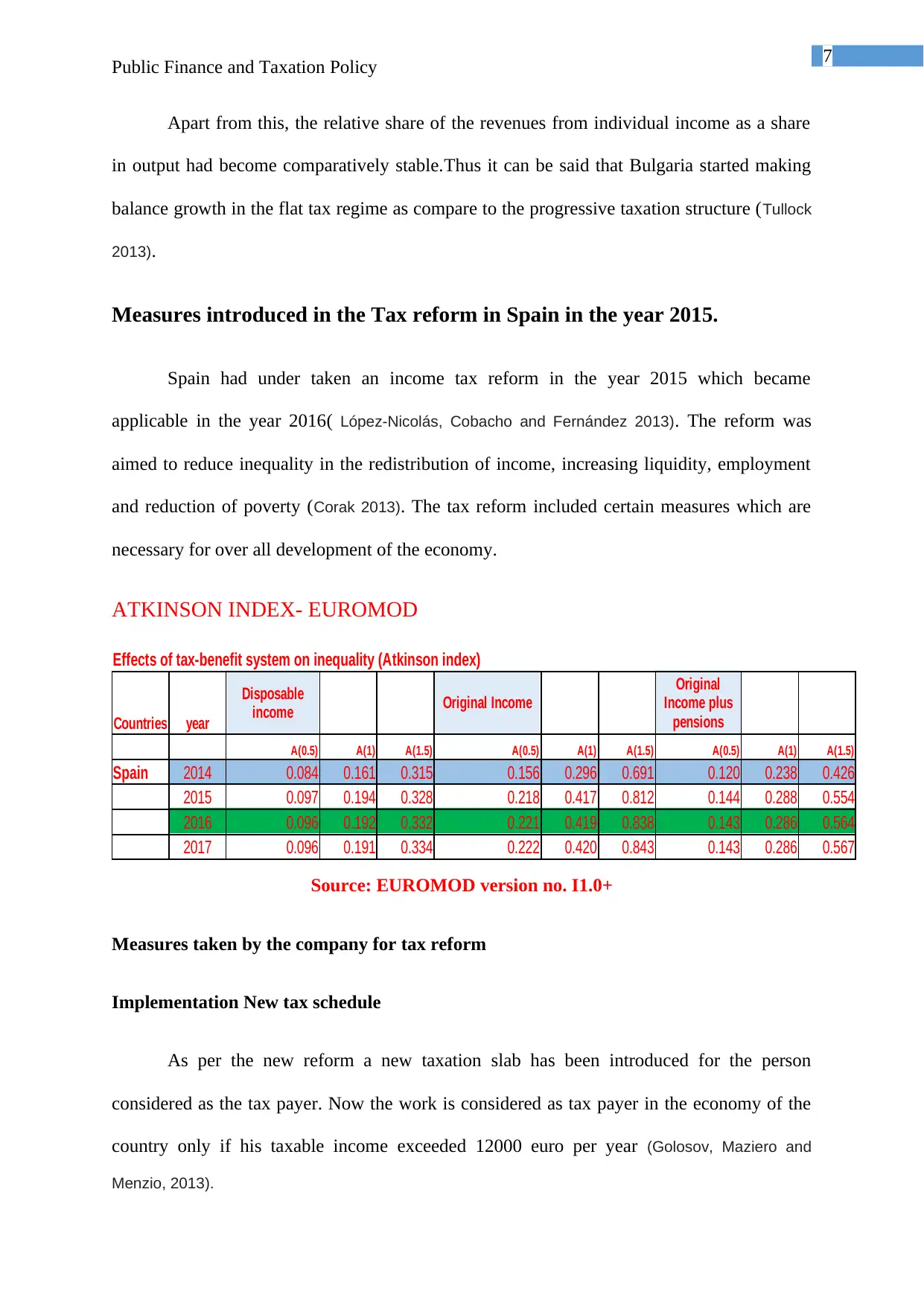

Measures introduced in the Tax reform in Spain in the year 2015.

Spain had under taken an income tax reform in the year 2015 which became

applicable in the year 2016( López-Nicolás, Cobacho and Fernández 2013). The reform was

aimed to reduce inequality in the redistribution of income, increasing liquidity, employment

and reduction of poverty (Corak 2013). The tax reform included certain measures which are

necessary for over all development of the economy.

ATKINSON INDEX- EUROMOD

Effects of tax-benefit system on inequality (Atkinson index)

Countries year

Original Income

A(0.5) A(1) A(1.5) A(0.5) A(1) A(1.5) A(0.5) A(1) A(1.5)

Spain 2014 0.084 0.161 0.315 0.156 0.296 0.691 0.120 0.238 0.426

2015 0.097 0.194 0.328 0.218 0.417 0.812 0.144 0.288 0.554

2016 0.096 0.192 0.332 0.221 0.419 0.838 0.143 0.286 0.564

2017 0.096 0.191 0.334 0.222 0.420 0.843 0.143 0.286 0.567

Disposable

income

Original

Income plus

pensions

Source: EUROMOD version no. I1.0+

Measures taken by the company for tax reform

Implementation New tax schedule

As per the new reform a new taxation slab has been introduced for the person

considered as the tax payer. Now the work is considered as tax payer in the economy of the

country only if his taxable income exceeded 12000 euro per year (Golosov, Maziero and

Menzio, 2013).

Public Finance and Taxation Policy

Apart from this, the relative share of the revenues from individual income as a share

in output had become comparatively stable.Thus it can be said that Bulgaria started making

balance growth in the flat tax regime as compare to the progressive taxation structure (Tullock

2013).

Measures introduced in the Tax reform in Spain in the year 2015.

Spain had under taken an income tax reform in the year 2015 which became

applicable in the year 2016( López-Nicolás, Cobacho and Fernández 2013). The reform was

aimed to reduce inequality in the redistribution of income, increasing liquidity, employment

and reduction of poverty (Corak 2013). The tax reform included certain measures which are

necessary for over all development of the economy.

ATKINSON INDEX- EUROMOD

Effects of tax-benefit system on inequality (Atkinson index)

Countries year

Original Income

A(0.5) A(1) A(1.5) A(0.5) A(1) A(1.5) A(0.5) A(1) A(1.5)

Spain 2014 0.084 0.161 0.315 0.156 0.296 0.691 0.120 0.238 0.426

2015 0.097 0.194 0.328 0.218 0.417 0.812 0.144 0.288 0.554

2016 0.096 0.192 0.332 0.221 0.419 0.838 0.143 0.286 0.564

2017 0.096 0.191 0.334 0.222 0.420 0.843 0.143 0.286 0.567

Disposable

income

Original

Income plus

pensions

Source: EUROMOD version no. I1.0+

Measures taken by the company for tax reform

Implementation New tax schedule

As per the new reform a new taxation slab has been introduced for the person

considered as the tax payer. Now the work is considered as tax payer in the economy of the

country only if his taxable income exceeded 12000 euro per year (Golosov, Maziero and

Menzio, 2013).

8

Public Finance and Taxation Policy

A significant reduction in the withholding tax

A significant reduction of 19% in the tax rate for the manager whose remuneration

comes from an organization whose turnover is less than 100000 euro.

Also there is a sharp reduction being made in the retention income of the professional of

about 18% in general and 15% or 9% in the specific circumstances.

Family taxation

This reform is made keeping in mind the person with disability or minor living with

their parents. This new tax credit scheme is mostly for the person with high family burden,

large family or the person with disabilities. Now under the new scheme they can deduct 1200

euro per annum as an expense in taking care of their family (Golosov, Maziero and Menzio,

2013).

Contribution to retirement pension plan and social security.

As per the new taxation scheme the individual limit of the contribution in the

retirement pension plan have been reduced from 10000 euro to 8000 euro. The reform also

made an amendment in the amount of contribution in the social security. Such contribution

has increased from about 2000 euro to 2500 euro per year. This amendment is only applicable

Public Finance and Taxation Policy

A significant reduction in the withholding tax

A significant reduction of 19% in the tax rate for the manager whose remuneration

comes from an organization whose turnover is less than 100000 euro.

Also there is a sharp reduction being made in the retention income of the professional of

about 18% in general and 15% or 9% in the specific circumstances.

Family taxation

This reform is made keeping in mind the person with disability or minor living with

their parents. This new tax credit scheme is mostly for the person with high family burden,

large family or the person with disabilities. Now under the new scheme they can deduct 1200

euro per annum as an expense in taking care of their family (Golosov, Maziero and Menzio,

2013).

Contribution to retirement pension plan and social security.

As per the new taxation scheme the individual limit of the contribution in the

retirement pension plan have been reduced from 10000 euro to 8000 euro. The reform also

made an amendment in the amount of contribution in the social security. Such contribution

has increased from about 2000 euro to 2500 euro per year. This amendment is only applicable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

Public Finance and Taxation Policy

to the tax payer spouse who does not obtain income from work or business for an amount of

8000 Euro.

Patronage deduction

The Spanish tax reform has introduced fiscal measures for the increment in the

patronage activities (Del Pino 2013). The general deduction has been increased from 25% to

30% in the personal income taxation of an individual. For stable donation an increase rate has

been provided for the deduction at rate of 35%. For the increment in the micro patronage, a

maximum deduction of 75% has been introduced for a donation of 15 euro.

From the above discussion, it can be summarised that Spanish personal tax reform has

initiated many goods to the society and in the development of the country economy. The tax

reform has improved the household liquidity of the individual, help in the redistribution of

income, progressivity and poverty reduction.

Why Reducing Inequality matters

As per the data released by the world inequality report 2018, there is a sharp increase

in the inequality in the world. Rich person is becoming wealthier and poor people is

becoming poorer. The consequences of this growing trend in inequality is very hazardous.

Poverty, Unemployment and the social conflicts are the by-product of the increase in

Inequality in the society. Therefore government should eradicate the inequality from the

society by bringing the major tax reform in the country and taking some constructive fiscal

measures.

Public Finance and Taxation Policy

to the tax payer spouse who does not obtain income from work or business for an amount of

8000 Euro.

Patronage deduction

The Spanish tax reform has introduced fiscal measures for the increment in the

patronage activities (Del Pino 2013). The general deduction has been increased from 25% to

30% in the personal income taxation of an individual. For stable donation an increase rate has

been provided for the deduction at rate of 35%. For the increment in the micro patronage, a

maximum deduction of 75% has been introduced for a donation of 15 euro.

From the above discussion, it can be summarised that Spanish personal tax reform has

initiated many goods to the society and in the development of the country economy. The tax

reform has improved the household liquidity of the individual, help in the redistribution of

income, progressivity and poverty reduction.

Why Reducing Inequality matters

As per the data released by the world inequality report 2018, there is a sharp increase

in the inequality in the world. Rich person is becoming wealthier and poor people is

becoming poorer. The consequences of this growing trend in inequality is very hazardous.

Poverty, Unemployment and the social conflicts are the by-product of the increase in

Inequality in the society. Therefore government should eradicate the inequality from the

society by bringing the major tax reform in the country and taking some constructive fiscal

measures.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

Public Finance and Taxation Policy

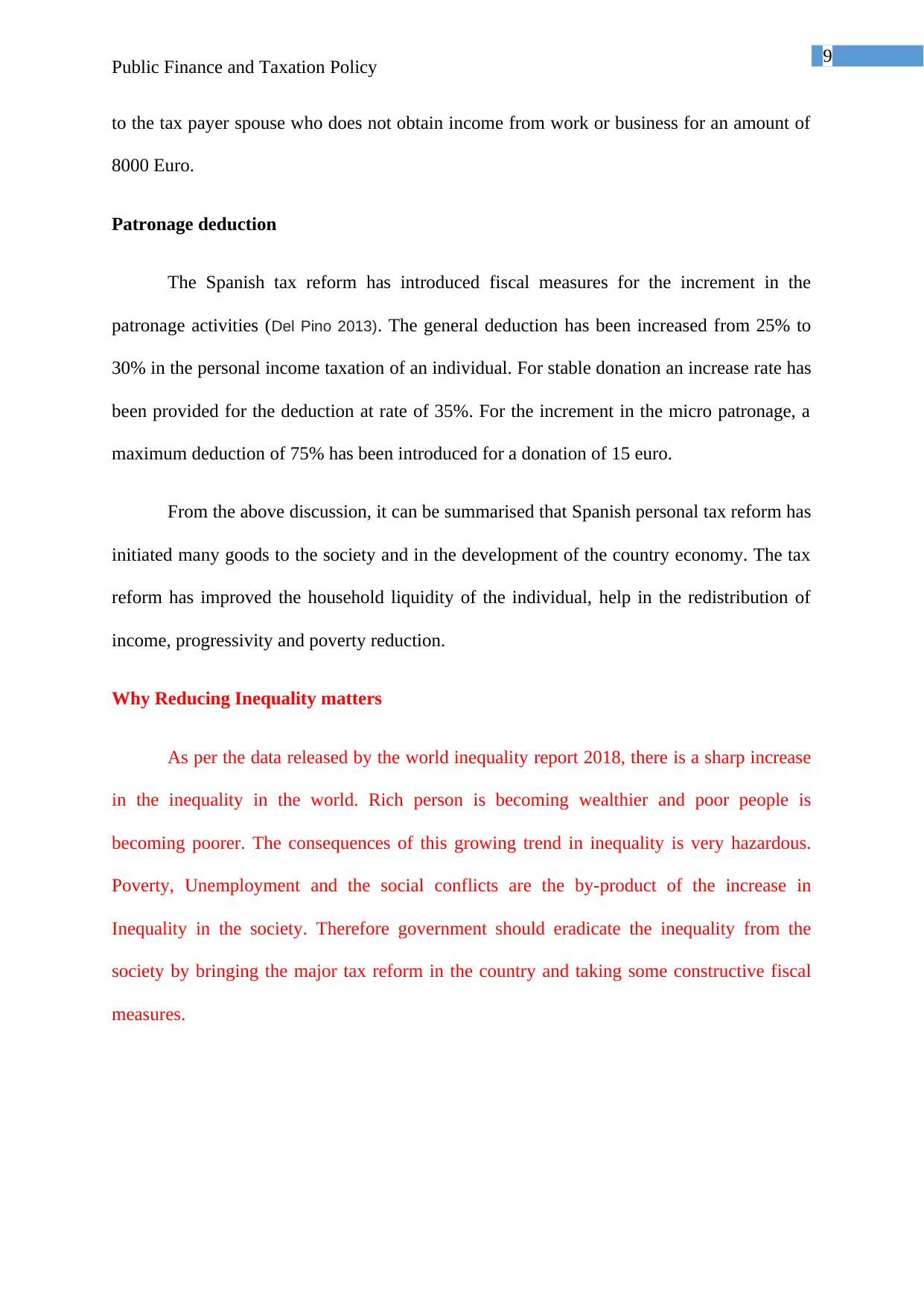

Effects of tax-benefit components on inequality

Gini index

Country Year

Spain 2017 0.338 0.373 0.349 0.381 0.335 0.530 0.419

2016 0.339 0.373 0.350 0.382 0.336 0.530 0.419

2015 0.340 0.374 0.351 0.383 0.337 0.528 0.420

Disposable

income (DPI)

DPI less

means-

tested

benefits

DPI less

non means-

tested

benefits

DPI plus direct

taxes

DPI plus

Social

Insurance

Contrib.

Original

Income

Original Income

plus pensions

Sour

ce: EUROMOD version no. I1.0+

Conclusion

From the above detailed study of the Bulgarian and Spanish taxation structure it can

concluded that both the country have made a reform in their economy by introducing new

taxation scheme. Bulgarian economy has shifted its taxation policy from the progressive to

flat taxation regime. This change was introduced to cope up with the challenges in the

unequal redistribution of income, poverty, unemployment.

On the other hand Spanish government has made a reform in the taxation structure

which is applicable in year 2016. The new taxation structure has made a positive impact on

the redistribution of the income, increases the liquidity position of assets class, reduction in

the poverty. The tax reform rises the redistributive consequence to 6.3% that is considered as

extra redistributive as compare to the year 2011. Some of the important Spanish tax reform

like implementation of the new tax schedule, reduction in the withholding tax, family

taxation and patronage deduction helps the country in attaining the economic growth and a

balance taxation structure.

Public Finance and Taxation Policy

Effects of tax-benefit components on inequality

Gini index

Country Year

Spain 2017 0.338 0.373 0.349 0.381 0.335 0.530 0.419

2016 0.339 0.373 0.350 0.382 0.336 0.530 0.419

2015 0.340 0.374 0.351 0.383 0.337 0.528 0.420

Disposable

income (DPI)

DPI less

means-

tested

benefits

DPI less

non means-

tested

benefits

DPI plus direct

taxes

DPI plus

Social

Insurance

Contrib.

Original

Income

Original Income

plus pensions

Sour

ce: EUROMOD version no. I1.0+

Conclusion

From the above detailed study of the Bulgarian and Spanish taxation structure it can

concluded that both the country have made a reform in their economy by introducing new

taxation scheme. Bulgarian economy has shifted its taxation policy from the progressive to

flat taxation regime. This change was introduced to cope up with the challenges in the

unequal redistribution of income, poverty, unemployment.

On the other hand Spanish government has made a reform in the taxation structure

which is applicable in year 2016. The new taxation structure has made a positive impact on

the redistribution of the income, increases the liquidity position of assets class, reduction in

the poverty. The tax reform rises the redistributive consequence to 6.3% that is considered as

extra redistributive as compare to the year 2011. Some of the important Spanish tax reform

like implementation of the new tax schedule, reduction in the withholding tax, family

taxation and patronage deduction helps the country in attaining the economic growth and a

balance taxation structure.

11

Public Finance and Taxation Policy

Referencing

Bozio, A., Emmerson, C., Peichl, A. and Tetlow, G., 2015. European public finances and the

great recession: France, Germany, Ireland, Italy, Spain and the United Kingdom

compared. Fiscal Studies, 36(4), pp.405-430.

Corak, M., 2013. Income inequality, equality of opportunity, and intergenerational

mobility. Journal of Economic Perspectives, 27(3), pp.79-102.

Corbacho, A., Cibils, V.F. and Lora, E., 2013. More than Revenue: Taxation as a

development tool. Springer.

Del Pino, E., 2013. The Spanish welfare state from Zapatero to Rajoy: Recalibration to

retrenchment. In Politics and Society in Contemporary Spain (pp. 197-216). Palgrave

Macmillan, New York.

Di Mascio, F. and Natalini, A., 2015. Fiscal retrenchment in southern Europe: Changing

patterns of public management in Greece, Italy, Portugal and Spain. Public Management

Review, 17(1), pp.129-148.

Golosov, M., Maziero, P. and Menzio, G., 2013. Taxation and redistribution of residual

income inequality. Journal of Political Economy, 121(6), pp.1160-1204.

Kalchev, E., 2014. The Bulgarian Flat Tax. Economic Alternatives, (1), pp.33-41.

Kleven, H.J. and Schultz, E.A., 2014. Estimating taxable income responses using Danish tax

reforms. American Economic Journal: Economic Policy, 6(4), pp.271-301.

Public Finance and Taxation Policy

Referencing

Bozio, A., Emmerson, C., Peichl, A. and Tetlow, G., 2015. European public finances and the

great recession: France, Germany, Ireland, Italy, Spain and the United Kingdom

compared. Fiscal Studies, 36(4), pp.405-430.

Corak, M., 2013. Income inequality, equality of opportunity, and intergenerational

mobility. Journal of Economic Perspectives, 27(3), pp.79-102.

Corbacho, A., Cibils, V.F. and Lora, E., 2013. More than Revenue: Taxation as a

development tool. Springer.

Del Pino, E., 2013. The Spanish welfare state from Zapatero to Rajoy: Recalibration to

retrenchment. In Politics and Society in Contemporary Spain (pp. 197-216). Palgrave

Macmillan, New York.

Di Mascio, F. and Natalini, A., 2015. Fiscal retrenchment in southern Europe: Changing

patterns of public management in Greece, Italy, Portugal and Spain. Public Management

Review, 17(1), pp.129-148.

Golosov, M., Maziero, P. and Menzio, G., 2013. Taxation and redistribution of residual

income inequality. Journal of Political Economy, 121(6), pp.1160-1204.

Kalchev, E., 2014. The Bulgarian Flat Tax. Economic Alternatives, (1), pp.33-41.

Kleven, H.J. and Schultz, E.A., 2014. Estimating taxable income responses using Danish tax

reforms. American Economic Journal: Economic Policy, 6(4), pp.271-301.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.