Public Sector Auditing: Standards, Competencies, and Audit Types

VerifiedAdded on 2023/07/11

|14

|1089

|433

Presentation

AI Summary

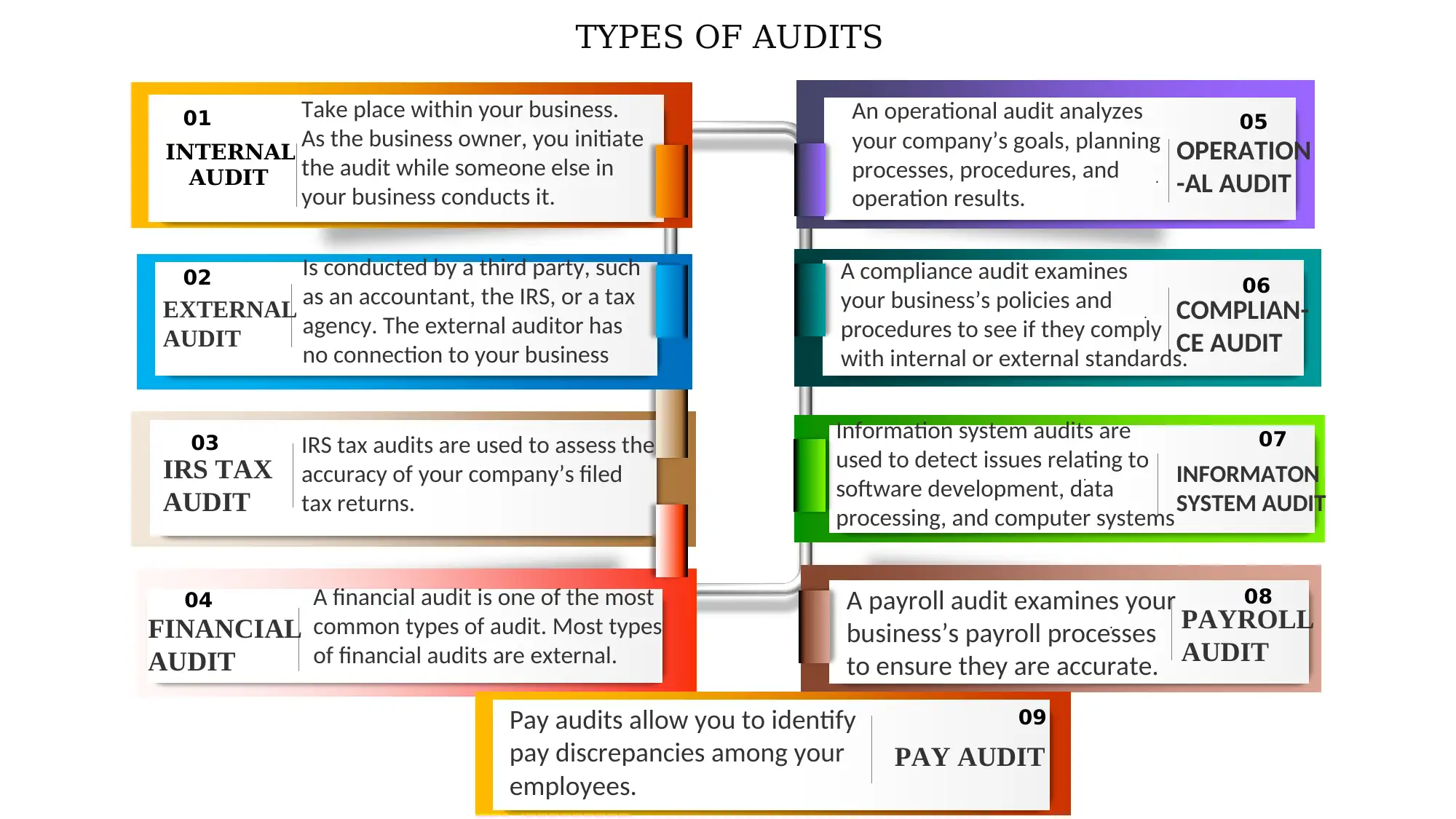

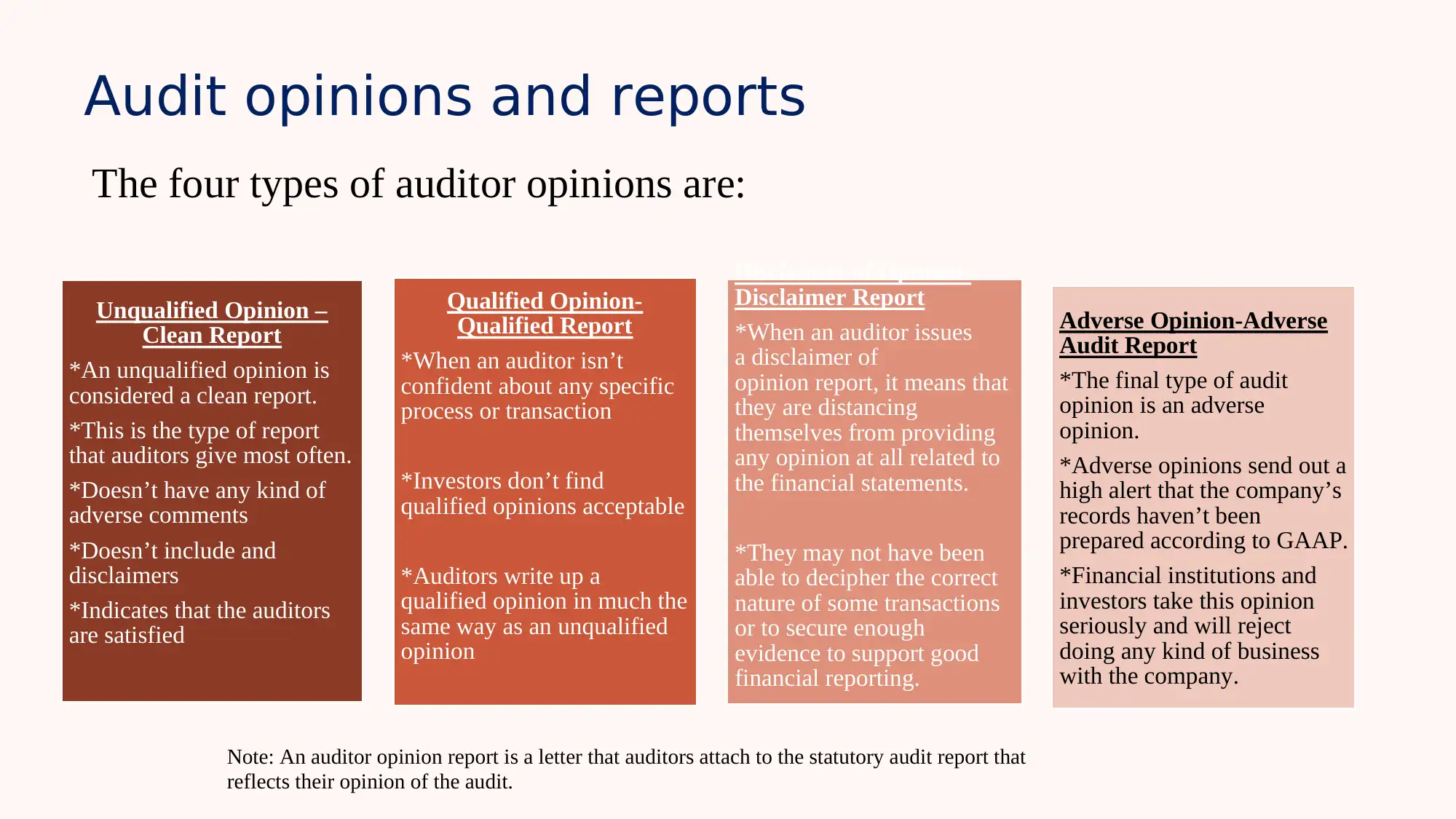

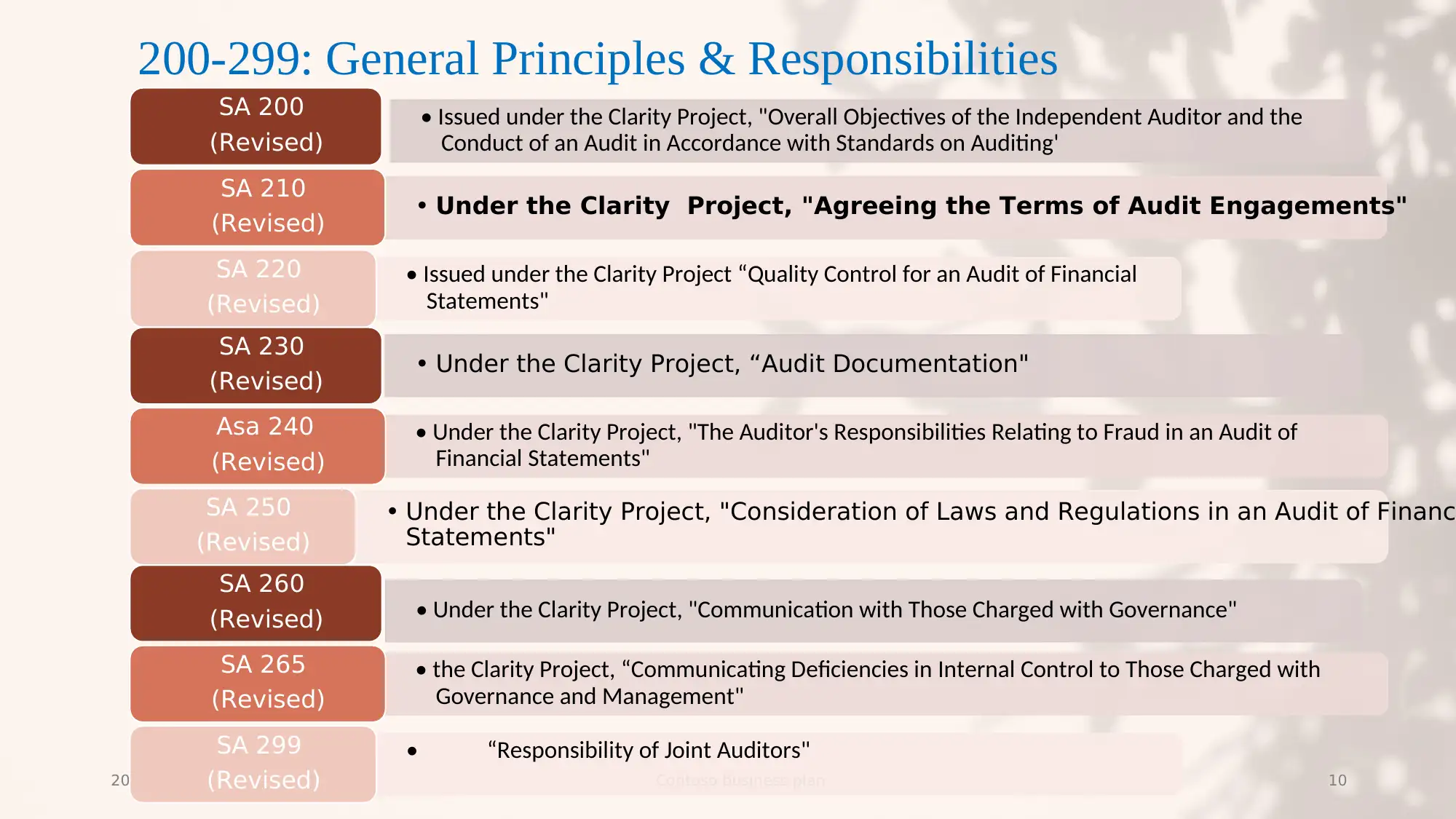

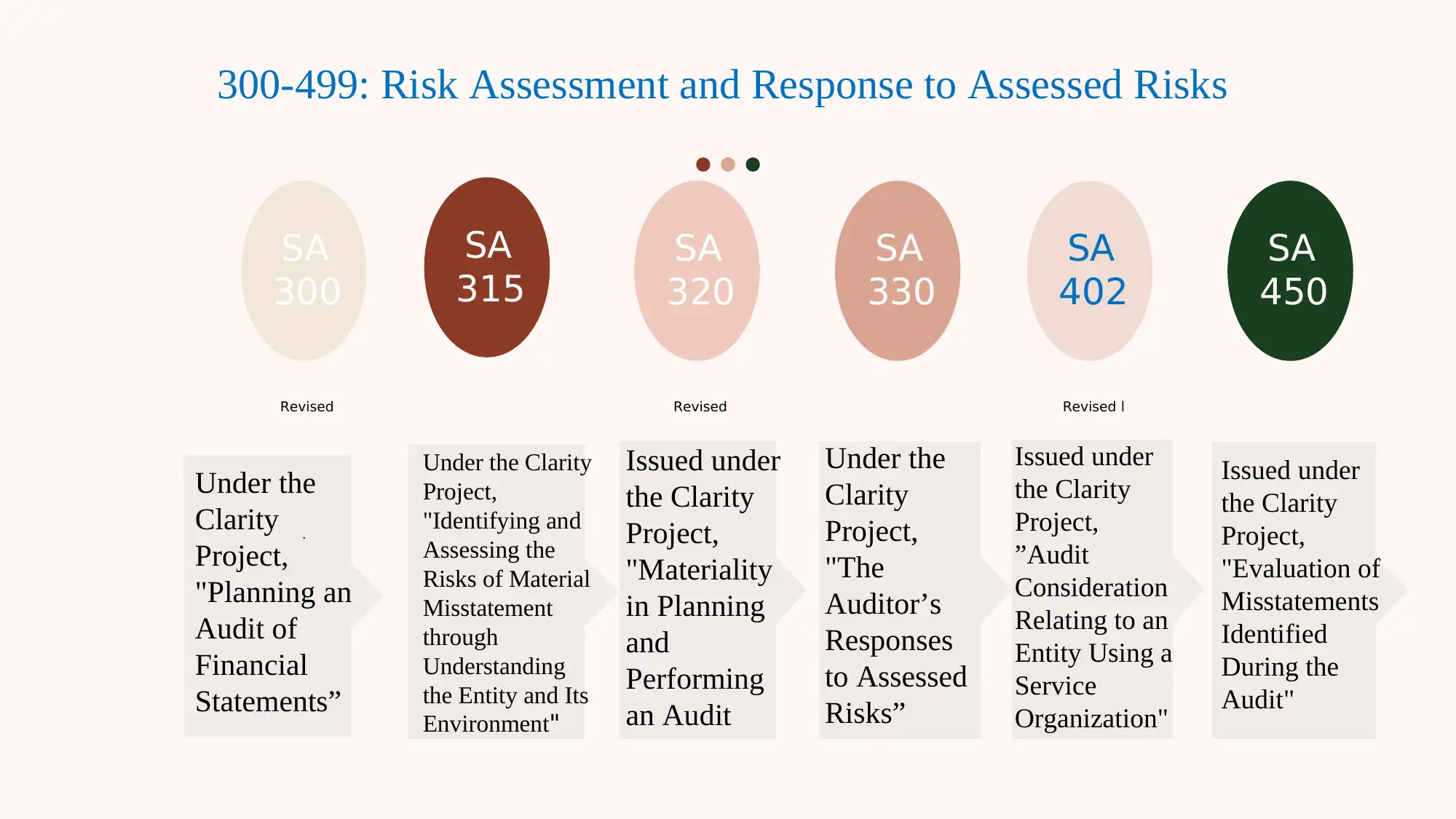

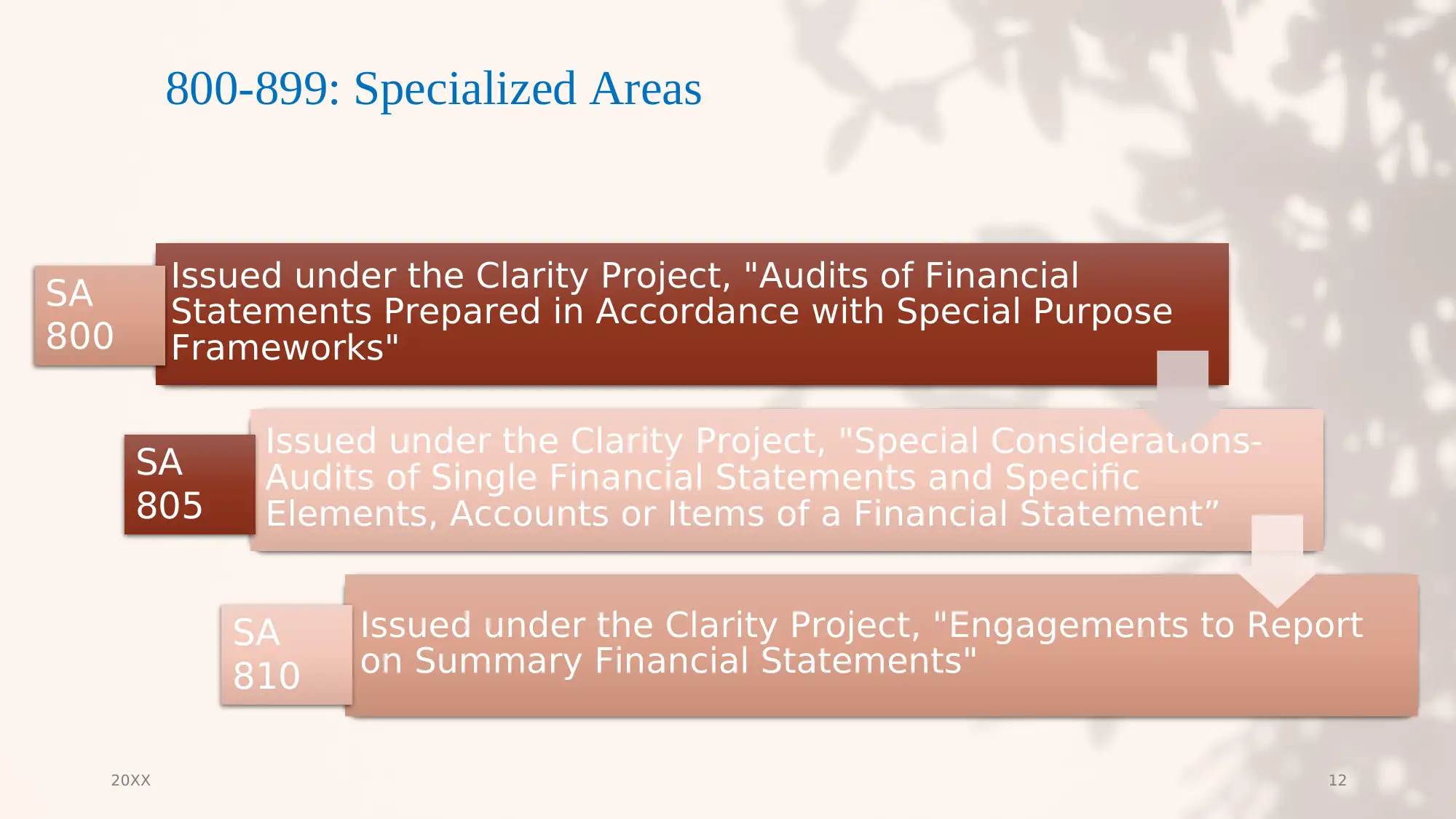

This presentation provides a comprehensive overview of public sector auditing, starting with an introduction to auditing principles, objectives, advantages, and limitations. It covers the different types of audits, including internal, operational, external, compliance, IRS tax, financial, information system, payroll, and pay audits. The presentation details the four types of auditor opinions: unqualified, qualified, disclaimer of opinion, and adverse opinion. It further discusses the Standards on Auditing (SA) under the Clarity Project, focusing on risk assessment, responses to assessed risks, and specialized areas. The presentation also touches upon the INTOSAI competency framework for SAI audit professionals, highlighting cross-cutting competencies relevant to compliance, financial, and performance audits. The document is intended to provide a foundational understanding of public sector auditing practices and standards.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.