Corporate Finance Assignment: PUMA's Financial Performance Analysis

VerifiedAdded on 2022/09/05

|29

|4639

|30

Report

AI Summary

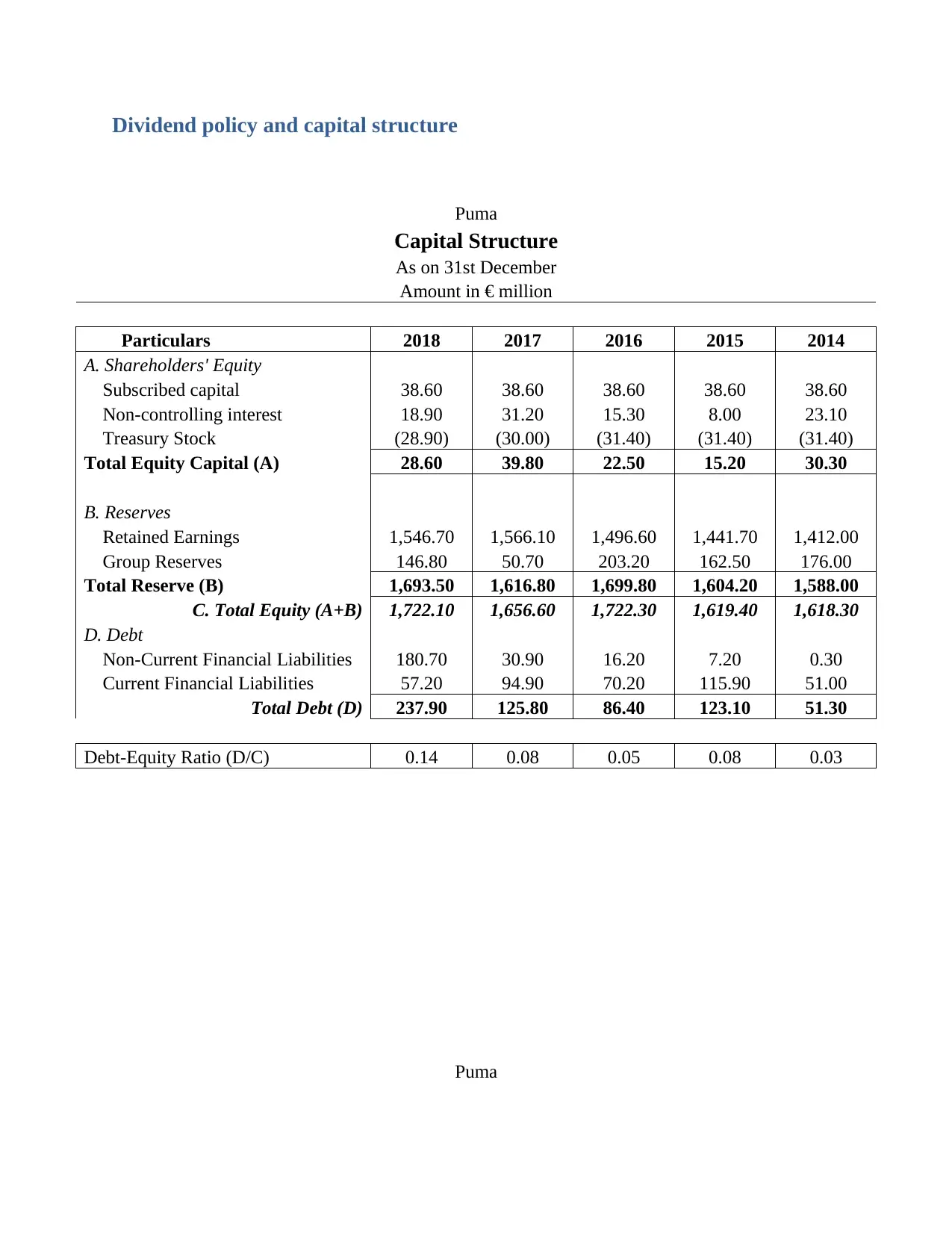

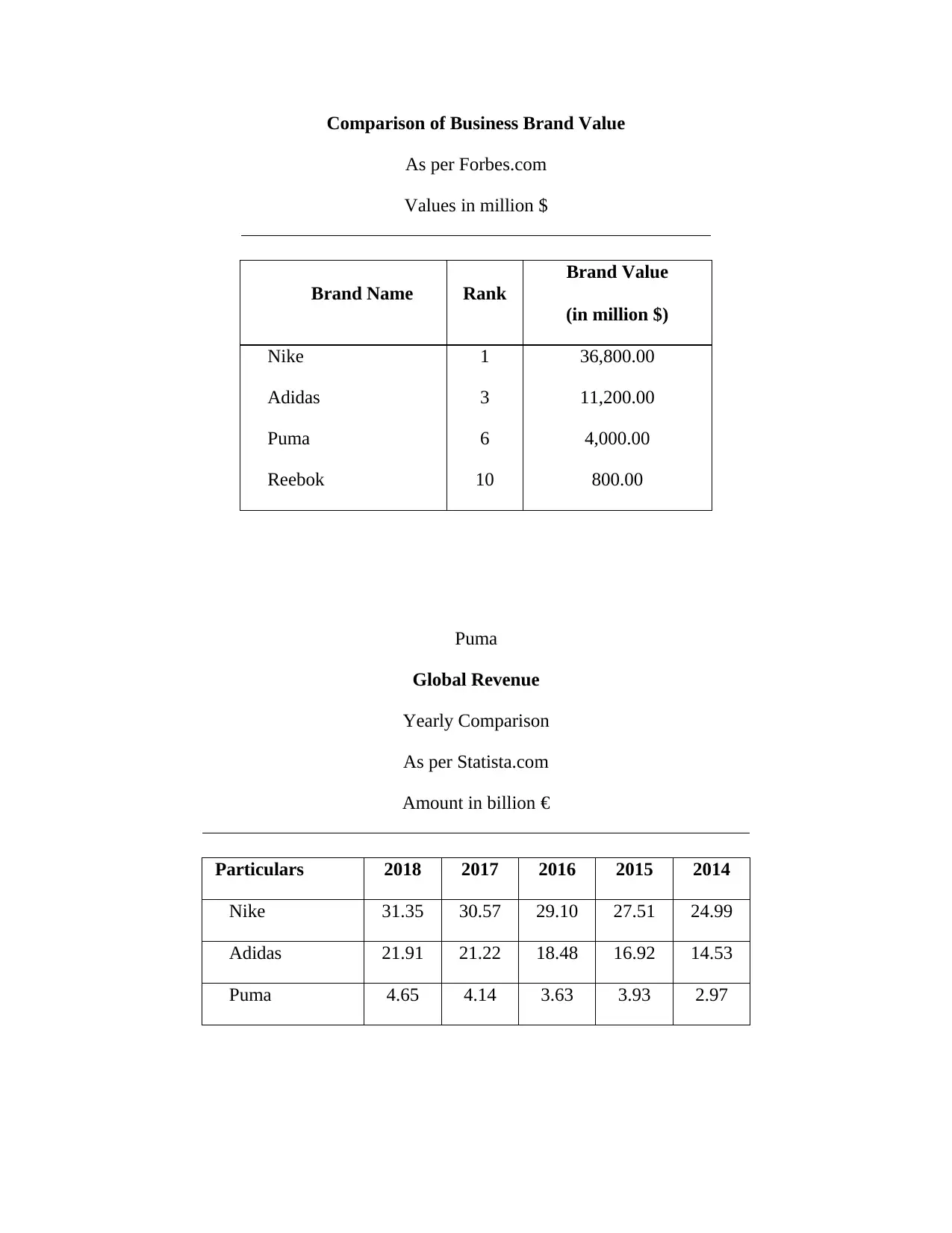

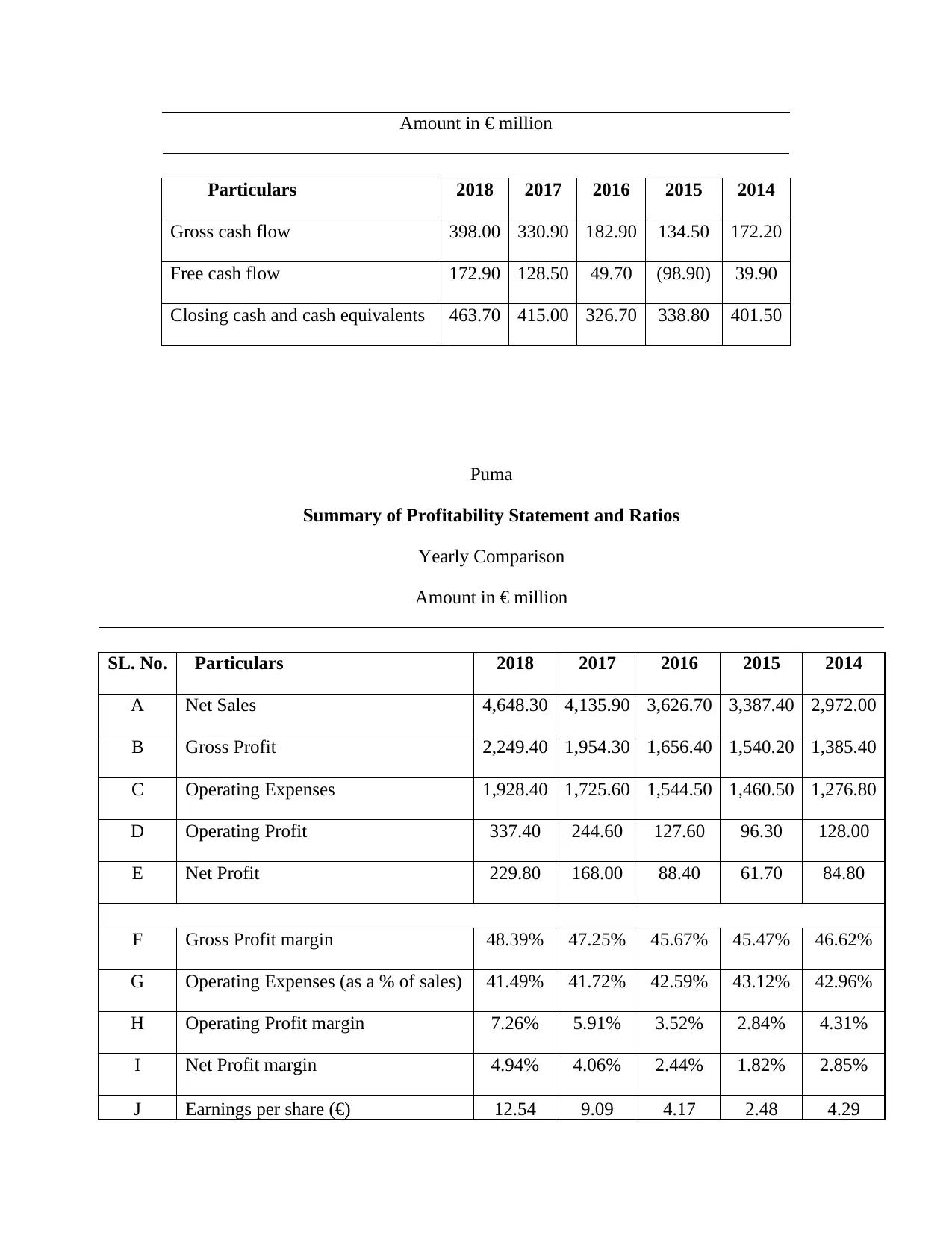

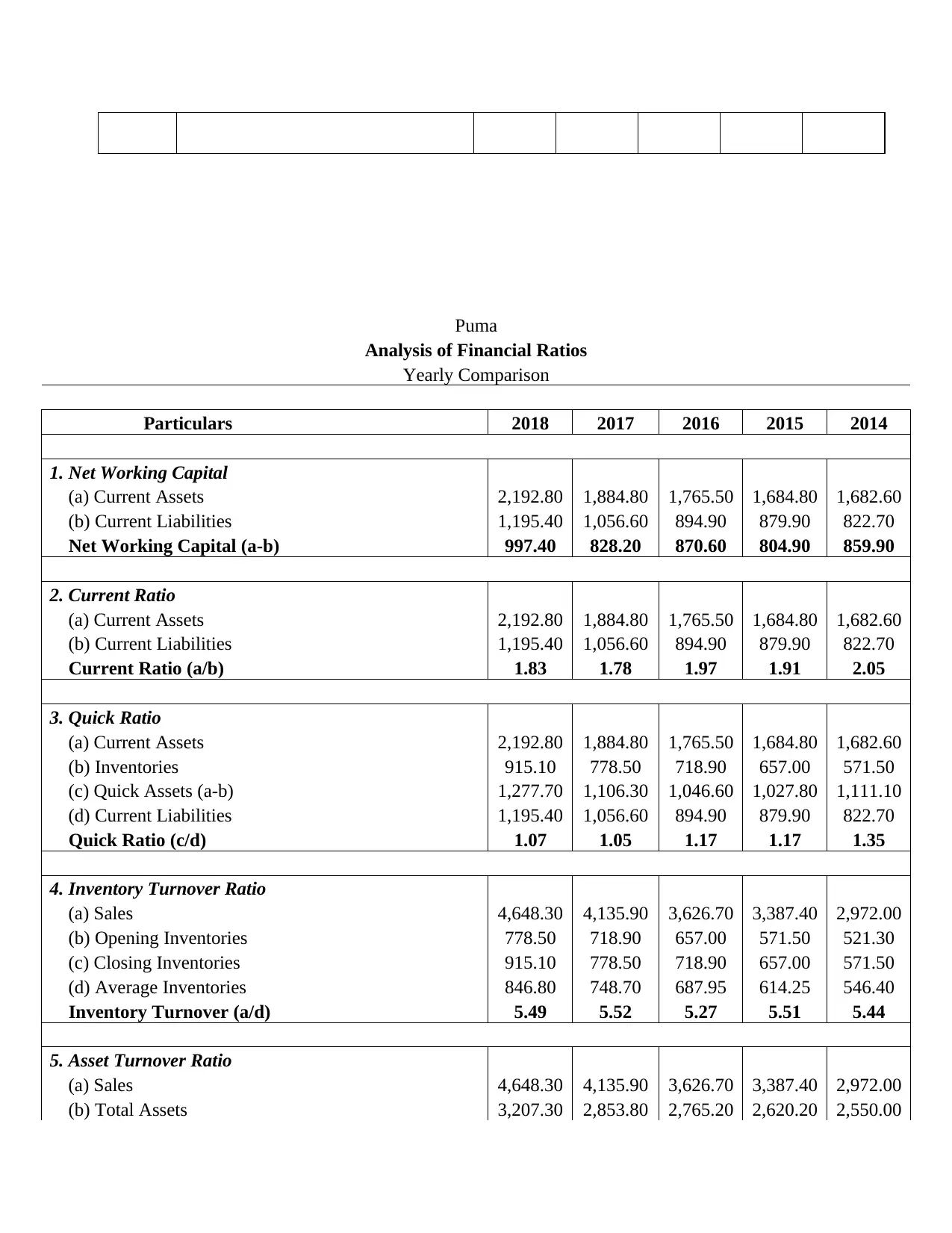

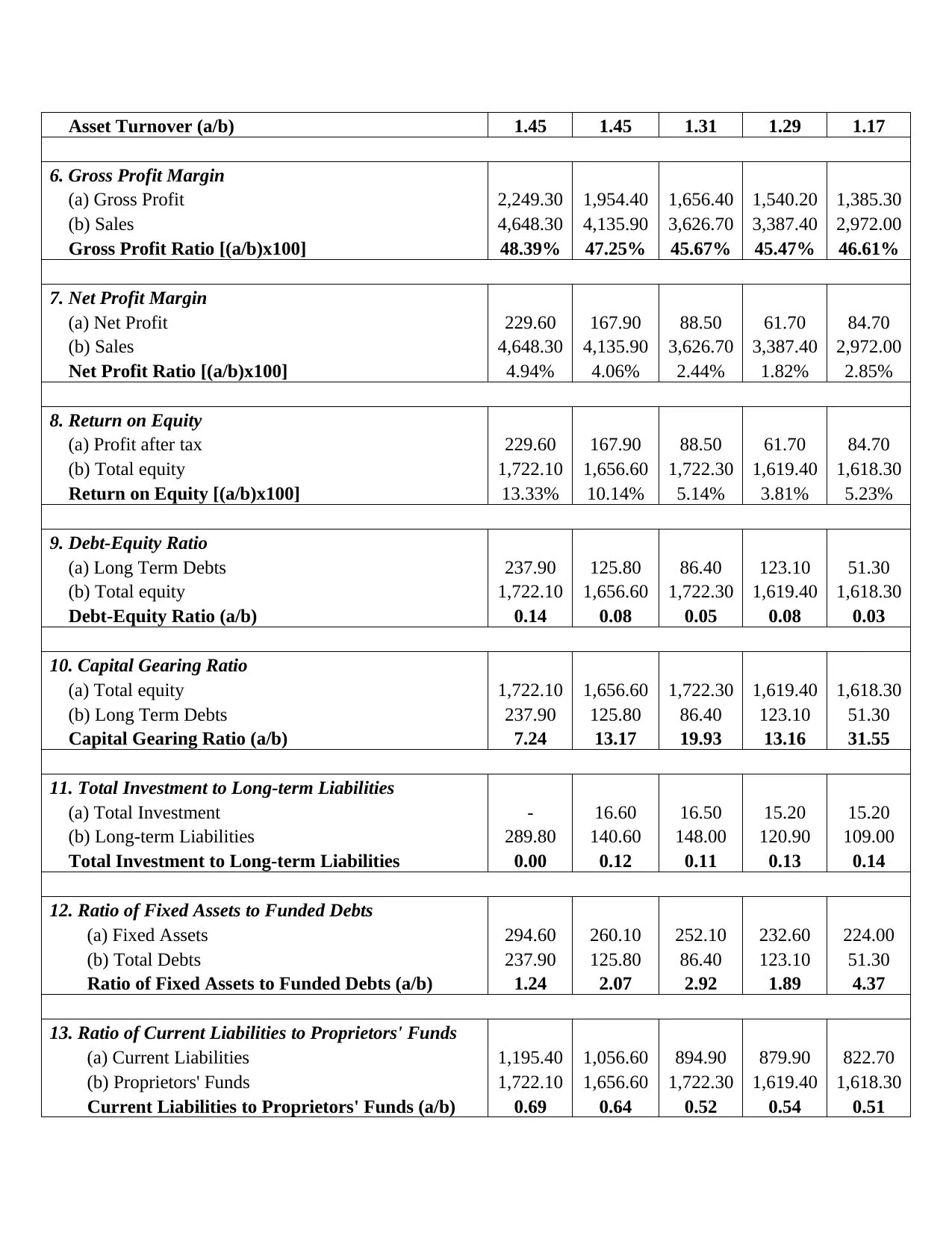

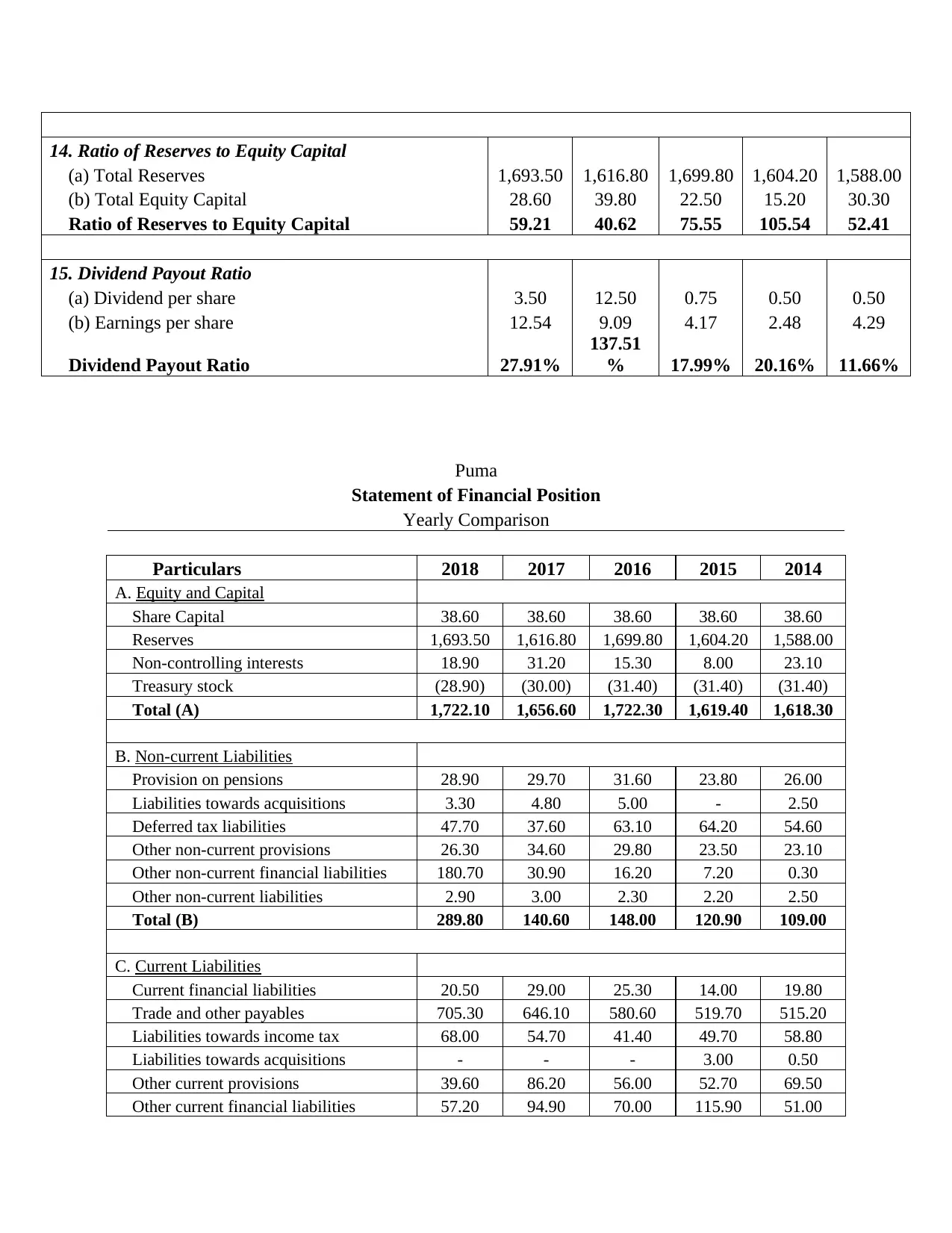

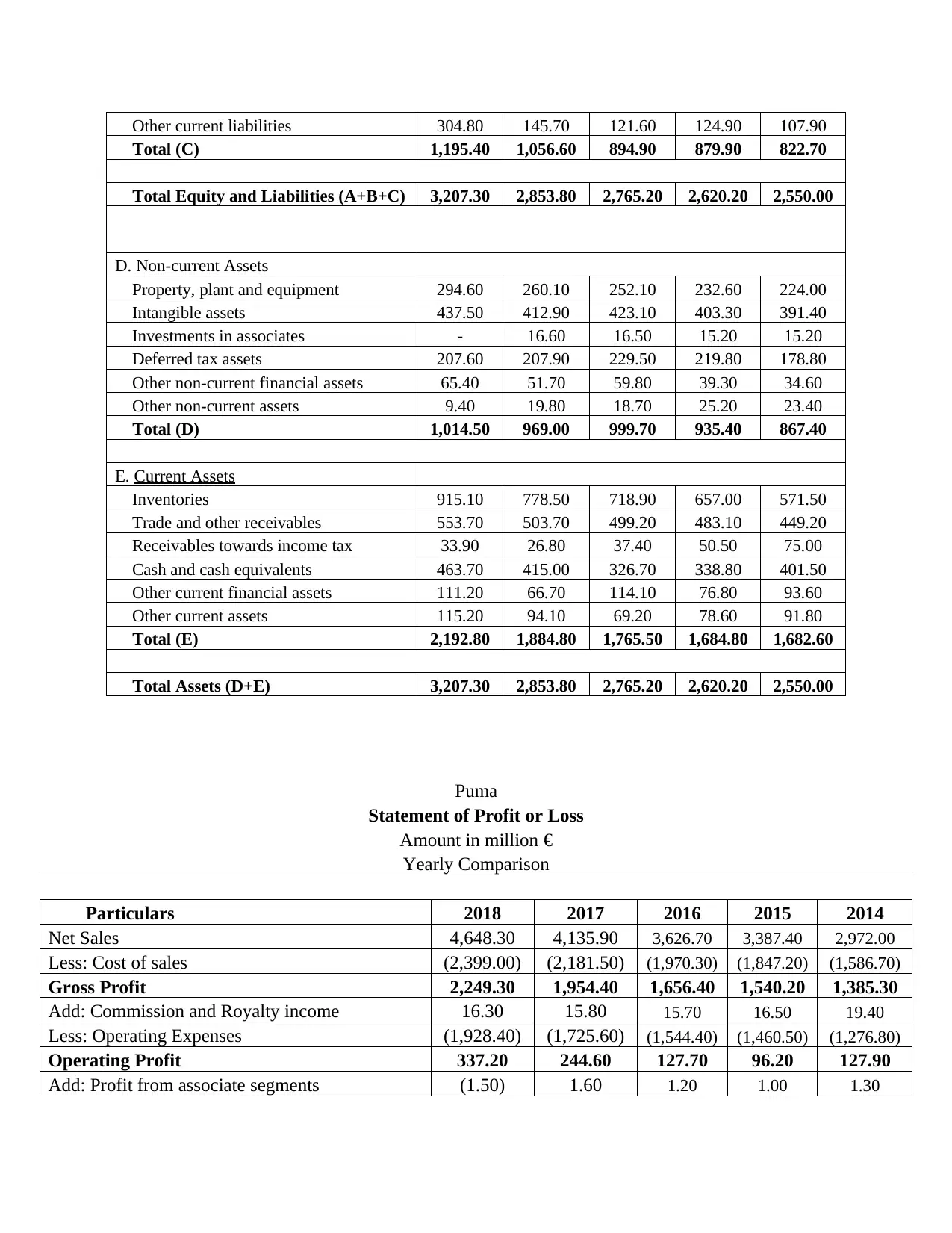

This report provides a comprehensive financial analysis of PUMA, examining its capital structure, dividend policy, and their impact on the company's performance over a three-year period. The analysis includes an overview of PUMA's background, key corporate objectives, and a comparison with competitors like Nike and Adidas. The report delves into PUMA's capital structure, presenting financial data and ratios such as the debt-equity ratio and dividend payout ratio. It also explores various sources of finance, discussing the potential impact of equity shares and debentures. Furthermore, the report identifies and evaluates financial management appraisal techniques, including payback period, internal rate of return, profitability index, and net present value, to aid in effective decision-making. Finally, the report concludes with a discussion of the strengths and weaknesses of the analysis, offering recommendations for future financial strategies. The report uses financial statements, ratios and comparisons to explain the performance of the company and its standing in the market.

1 out of 29

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.