QANTA Finance: Capital Budgeting and Debt Valuation Analysis

VerifiedAdded on 2023/06/05

|7

|1617

|81

Report

AI Summary

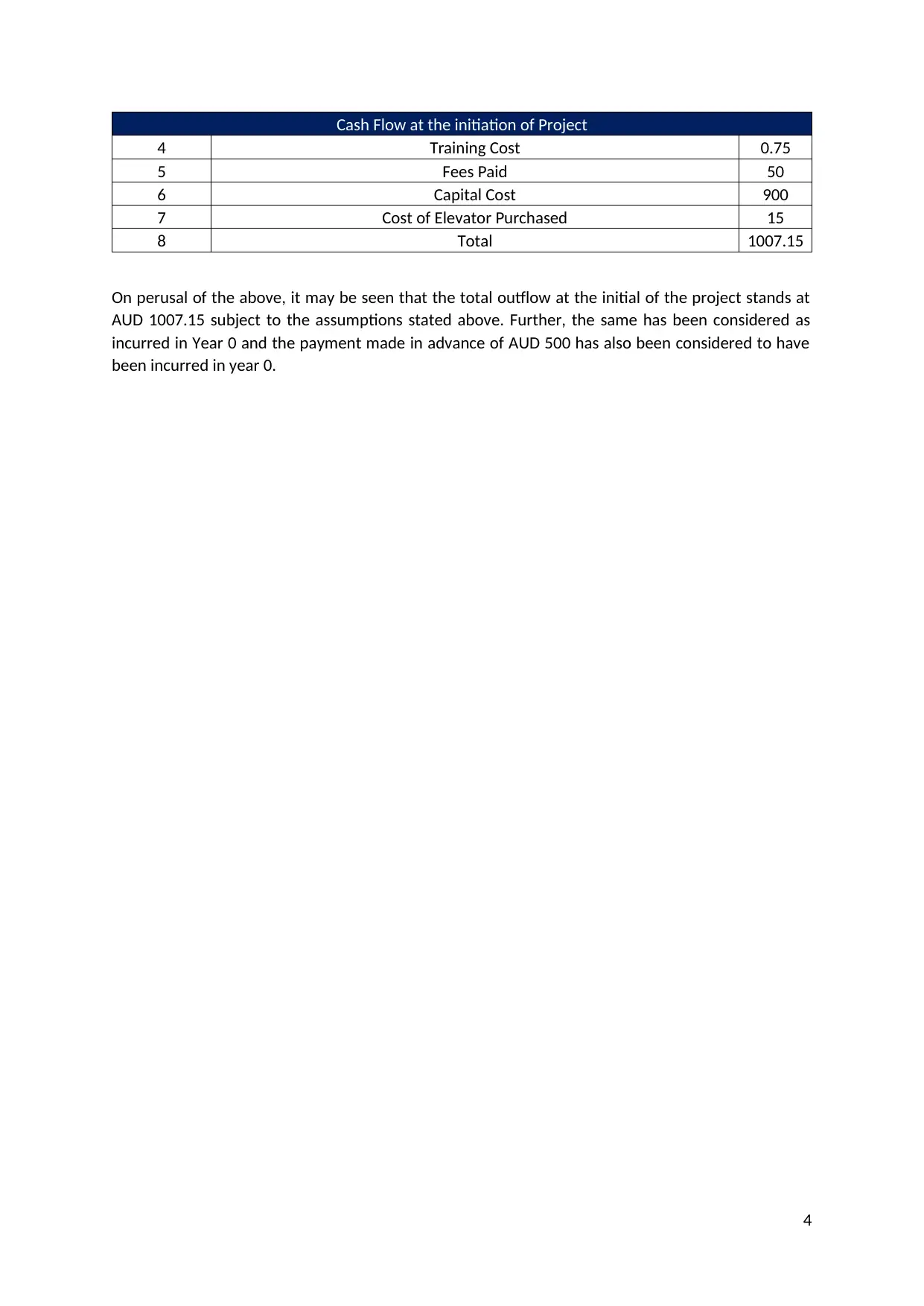

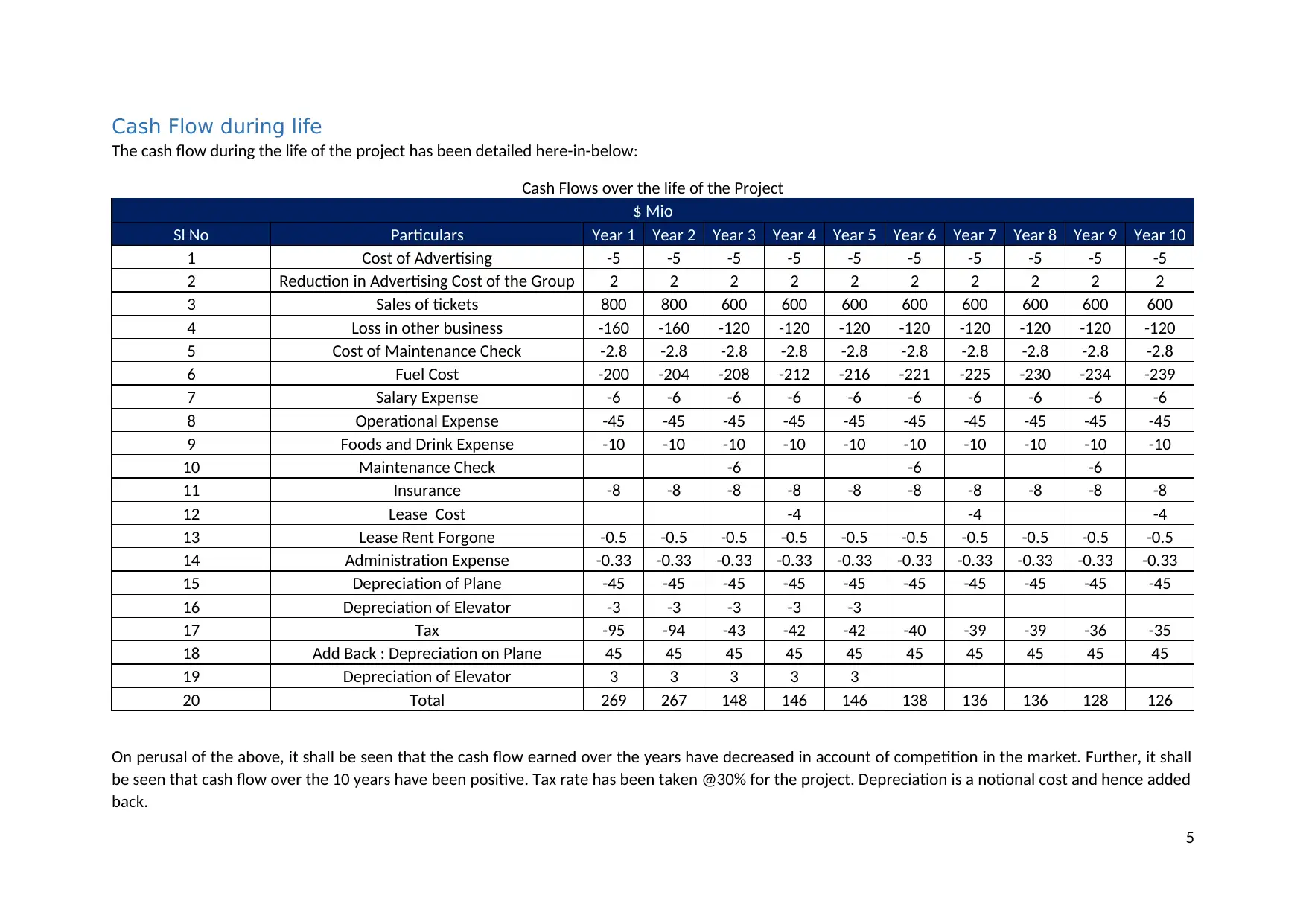

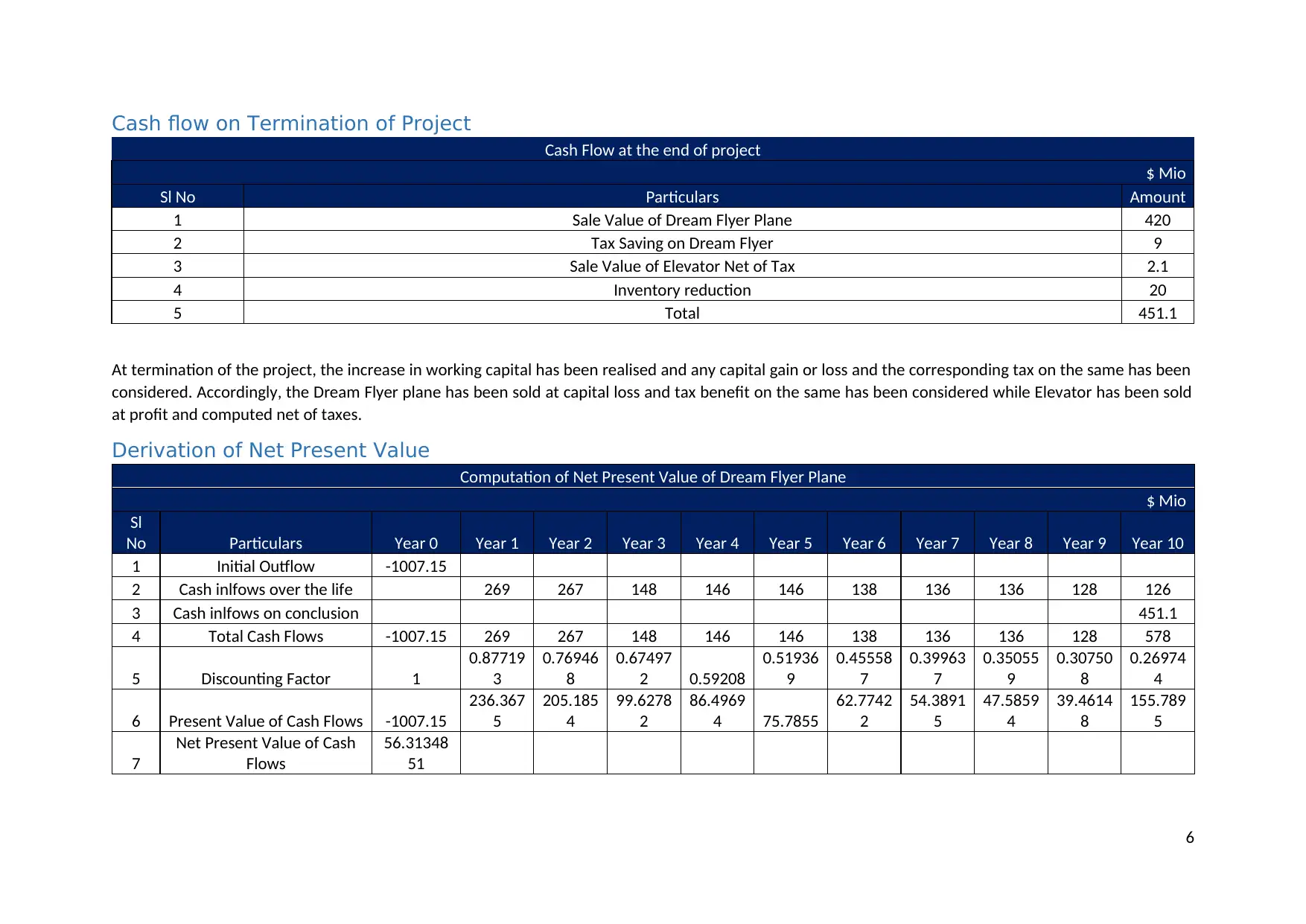

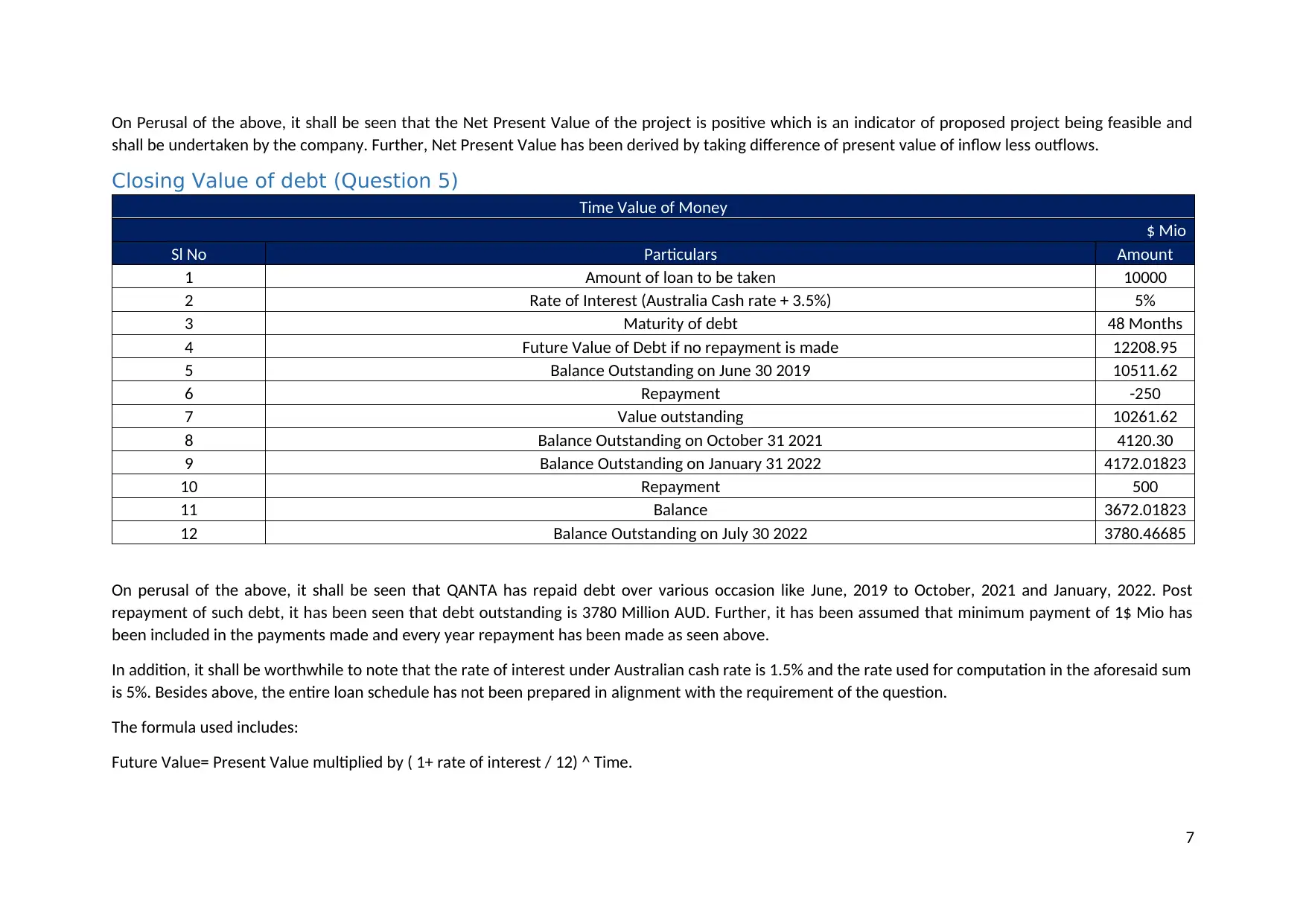

This report analyzes the financial feasibility of QANTA's proposed project involving non-stop flights from Sydney to London, utilizing capital budgeting techniques. It details the cash flows at initiation, during the project's life, and at termination, ultimately deriving the net present value (NPV) to determine project viability. The analysis considers various factors like advertising costs, sales of tickets, operational expenses, depreciation, and tax implications. Additionally, the report calculates the closing value of debt undertaken by QANTA to provide insurance cover, considering interest rates and repayment schedules. The findings indicate a positive NPV, suggesting the project's feasibility, and a remaining debt of $3780 million AUD.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.