Corporate Accounting: In-depth Analysis of Qantas Airways Financials

VerifiedAdded on 2021/06/15

|19

|2772

|18

Report

AI Summary

This report provides a comprehensive analysis of Qantas Airways' financial statements, focusing on corporate accounting principles. It examines the statement of cash flow, detailing items in operating, investing, and financing activities, and analyzes changes over the years 2015-2017, highlighting decreases in cash flow from operations and changes in investing and financing activities. The report also delves into the other comprehensive income statement, identifying key items like net exchange variances and fair value adjustments. It explains why these items are reported in the comprehensive income statement and discusses income tax expenditure, including reconciliation between tax expense and payable, as well as deferred tax assets and liabilities. The analysis concludes by comparing income tax expense with income tax paid, and providing insights into the charge for current tax on earnings based on adjusted profits, as well as the reconciliation of income tax expenditure to the amount of tax payable. The report references several academic papers to support the analysis.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CORPORATE ACCOUNTING

Table of Contents

Requirement (i)..........................................................................................................................2

Requirement (ii).........................................................................................................................4

Requirement (iii)........................................................................................................................5

Requirement (iv)........................................................................................................................5

Requirement (v).........................................................................................................................5

Requirement (vi)........................................................................................................................6

Requirement (vii).......................................................................................................................7

Requirement (viii)......................................................................................................................7

Requirement (ix)........................................................................................................................7

Requirement (x).........................................................................................................................8

Requirement (xi)........................................................................................................................8

References................................................................................................................................10

CORPORATE ACCOUNTING

Table of Contents

Requirement (i)..........................................................................................................................2

Requirement (ii).........................................................................................................................4

Requirement (iii)........................................................................................................................5

Requirement (iv)........................................................................................................................5

Requirement (v).........................................................................................................................5

Requirement (vi)........................................................................................................................6

Requirement (vii).......................................................................................................................7

Requirement (viii)......................................................................................................................7

Requirement (ix)........................................................................................................................7

Requirement (x).........................................................................................................................8

Requirement (xi)........................................................................................................................8

References................................................................................................................................10

3

CORPORATE ACCOUNTING

Cash Flow Statement

Requirement (i)

List of each item reported in the statement of flow of cash

The statement of flow of cash of the selected corporation Qantas Airways comprises of usual

three sections namely flow of cash from operating, investing as well as financing activities.

Essentially, this reflects the net cash and equivalents of cash. Particularly, items that are

mentioned under the operating activities include depreciation, adjustments in income,

alterations in the accounts receivables, changes in inventory as well as transformations in

liability. Essentially, it can be hereby mentioned that the flow of cash of each one of the item

has declined. In essence, this is owing to higher generation of earnings that is specifically

inflow of cash (Tschopp & Nastanski, 2014).

Thereafter, investing actions handle capital expends, investments as well as cash

expenditures. In essence, flows of cash from particularly investing actions include payments

for specifically property, plant as well as equipment (PPE) and intangible assets, interest

disbursements and at the same time capitalised on qualifying assets (Sierra‐García et al.,

2015). The investing actions include disbursements for acquisitions of particularly controlled

entities as well as net of cash attained and disbursements for particularly investments under

equity methods. Again, net receipts are acquired for aircraft that is assigned to investment

mentioned under equity method. Again, inflow of cash can be observed from proceeds

acquired from disposal of particularly plant, property as well as equipment (Siew, 2015).

Further, inflow of cash can also be acquired from disposal of controlled entities, net loan

repayment from specifically investments under equity method and refinancing of operating

lease of aircraft. However, cash derived from operations include cash receipts from customers

and cash payments to different suppliers as well as employees (Schaltegger & Burritt, 2017).

CORPORATE ACCOUNTING

Cash Flow Statement

Requirement (i)

List of each item reported in the statement of flow of cash

The statement of flow of cash of the selected corporation Qantas Airways comprises of usual

three sections namely flow of cash from operating, investing as well as financing activities.

Essentially, this reflects the net cash and equivalents of cash. Particularly, items that are

mentioned under the operating activities include depreciation, adjustments in income,

alterations in the accounts receivables, changes in inventory as well as transformations in

liability. Essentially, it can be hereby mentioned that the flow of cash of each one of the item

has declined. In essence, this is owing to higher generation of earnings that is specifically

inflow of cash (Tschopp & Nastanski, 2014).

Thereafter, investing actions handle capital expends, investments as well as cash

expenditures. In essence, flows of cash from particularly investing actions include payments

for specifically property, plant as well as equipment (PPE) and intangible assets, interest

disbursements and at the same time capitalised on qualifying assets (Sierra‐García et al.,

2015). The investing actions include disbursements for acquisitions of particularly controlled

entities as well as net of cash attained and disbursements for particularly investments under

equity methods. Again, net receipts are acquired for aircraft that is assigned to investment

mentioned under equity method. Again, inflow of cash can be observed from proceeds

acquired from disposal of particularly plant, property as well as equipment (Siew, 2015).

Further, inflow of cash can also be acquired from disposal of controlled entities, net loan

repayment from specifically investments under equity method and refinancing of operating

lease of aircraft. However, cash derived from operations include cash receipts from customers

and cash payments to different suppliers as well as employees (Schaltegger & Burritt, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CORPORATE ACCOUNTING

Moreover, cash flows generated from financing activities include disbursements for

particularly capital return, share buy-back and treasury shares and receipts for proceeds from

particularly borrowing, proceeds from specifically sale, finance leaseback of different non-

current assets (Saeidi et al., 2015).

Discussion of changes in each of the items for the firm over the previous year

Essentially, net flow of cash from mainly operating actions has decreased to $2704 million in

2017 from $2819 million in 2016. This is mainly due to decrease in interest payment, further

increase in payments of cash and decrease in payment for cash for redundancies as well

associated costs. Again, the net cash that is used in investing activities include shows a

negative figure replicating cash outflow. The net cash outflow for investing actions has

increased from ($1923 million) to around ($2046 million). This is mainly due to increase in

interest paid as well as capitalised on different qualifying assets and specifically decrease in

proceeds from particularly disposal of particularly plant, property as well as equipment (Reid

& Myddelton, 2017). In case of financing activities, figure for net cash used is a negative

figure that is ($854 million), replicating a cash outflow. However, the cash outflow has

declined to ($854 million) from ($1825 million) due to decrease in payments for payments of

share buy backs and repayments for borrowings. However, at the end, the figure registered

for cash as well as cash equivalents stand at $1775 million in comparison to $1980 million.

This shows decrease in cash and cash equivalents at the ending of the year reflecting decrease

in cash inflow.

CORPORATE ACCOUNTING

Moreover, cash flows generated from financing activities include disbursements for

particularly capital return, share buy-back and treasury shares and receipts for proceeds from

particularly borrowing, proceeds from specifically sale, finance leaseback of different non-

current assets (Saeidi et al., 2015).

Discussion of changes in each of the items for the firm over the previous year

Essentially, net flow of cash from mainly operating actions has decreased to $2704 million in

2017 from $2819 million in 2016. This is mainly due to decrease in interest payment, further

increase in payments of cash and decrease in payment for cash for redundancies as well

associated costs. Again, the net cash that is used in investing activities include shows a

negative figure replicating cash outflow. The net cash outflow for investing actions has

increased from ($1923 million) to around ($2046 million). This is mainly due to increase in

interest paid as well as capitalised on different qualifying assets and specifically decrease in

proceeds from particularly disposal of particularly plant, property as well as equipment (Reid

& Myddelton, 2017). In case of financing activities, figure for net cash used is a negative

figure that is ($854 million), replicating a cash outflow. However, the cash outflow has

declined to ($854 million) from ($1825 million) due to decrease in payments for payments of

share buy backs and repayments for borrowings. However, at the end, the figure registered

for cash as well as cash equivalents stand at $1775 million in comparison to $1980 million.

This shows decrease in cash and cash equivalents at the ending of the year reflecting decrease

in cash inflow.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CORPORATE ACCOUNTING

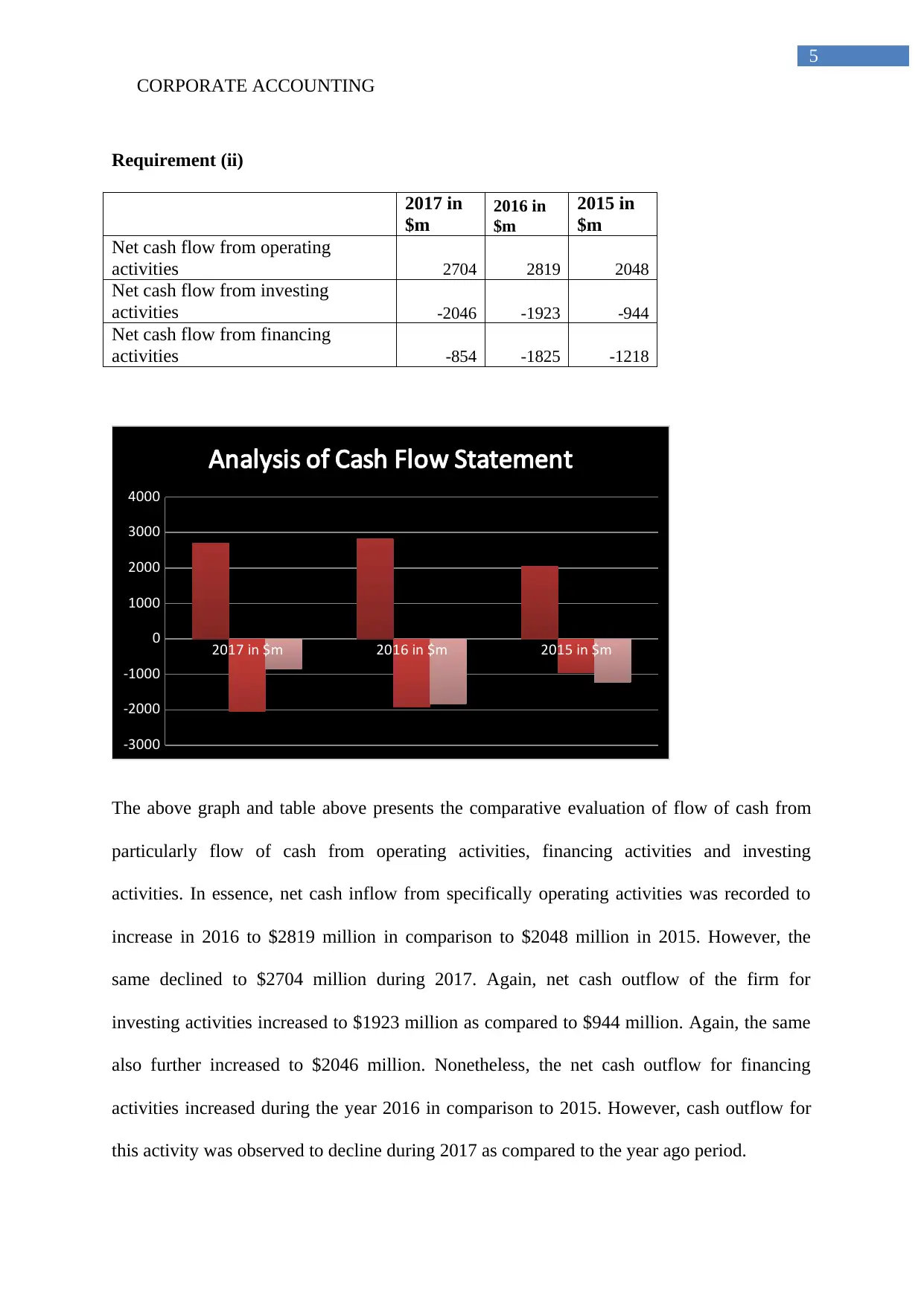

Requirement (ii)

2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating

activities 2704 2819 2048

Net cash flow from investing

activities -2046 -1923 -944

Net cash flow from financing

activities -854 -1825 -1218

2017 in $m 2016 in $m 2015 in $m

-3000

-2000

-1000

0

1000

2000

3000

4000

Analysis of Cash Flow Statement

The above graph and table above presents the comparative evaluation of flow of cash from

particularly flow of cash from operating activities, financing activities and investing

activities. In essence, net cash inflow from specifically operating activities was recorded to

increase in 2016 to $2819 million in comparison to $2048 million in 2015. However, the

same declined to $2704 million during 2017. Again, net cash outflow of the firm for

investing activities increased to $1923 million as compared to $944 million. Again, the same

also further increased to $2046 million. Nonetheless, the net cash outflow for financing

activities increased during the year 2016 in comparison to 2015. However, cash outflow for

this activity was observed to decline during 2017 as compared to the year ago period.

CORPORATE ACCOUNTING

Requirement (ii)

2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating

activities 2704 2819 2048

Net cash flow from investing

activities -2046 -1923 -944

Net cash flow from financing

activities -854 -1825 -1218

2017 in $m 2016 in $m 2015 in $m

-3000

-2000

-1000

0

1000

2000

3000

4000

Analysis of Cash Flow Statement

The above graph and table above presents the comparative evaluation of flow of cash from

particularly flow of cash from operating activities, financing activities and investing

activities. In essence, net cash inflow from specifically operating activities was recorded to

increase in 2016 to $2819 million in comparison to $2048 million in 2015. However, the

same declined to $2704 million during 2017. Again, net cash outflow of the firm for

investing activities increased to $1923 million as compared to $944 million. Again, the same

also further increased to $2046 million. Nonetheless, the net cash outflow for financing

activities increased during the year 2016 in comparison to 2015. However, cash outflow for

this activity was observed to decline during 2017 as compared to the year ago period.

6

CORPORATE ACCOUNTING

Requirement (iii)

Other comprehensive statement of income: Items reported in other comprehensive

statement of income

The comprehensive statement of earning of the firm Qantas Airways highlights other

comprehensive earning/loss for the particular year. This statement presents the statutory

profit for the financial year 2017 and 2016. Other comprehensive earning or else loss states

that Qantas Airways registered comprehensive income of $180 million, while company

registered other comprehensive loss of -$179 million. This statement also replicates total

comprehensive income of $1033 million in the year 2017 while the same was recorded to be

$850 million. The items that are essentially included in this section are the net exchange

variances from transactions of necessarily foreign operations that are taken under equity,

overall amount of reserve for foreign translations that are essentially transferred to net profit

as well as fair value adjustment on particularly hedging of cash flow (Miglani et al., 2015).

Requirement (iv)

The net exchange variances can be witnessed in effectual alterations in fair value of hedging

of cash flow that reflects drastic increase during the year 2017. Again, there is drastic decline

in the transfer of particularly hedge reserve to essentially consolidated income statement to -

$6 million from $198 million.

Requirement (v)

Reason why these items are reported in P/L statement

In essence, comprehensive income statement is necessarily utilized for the purpose of

enumeration of any kind of alteration in primarily interests of varied owners. In essence, this

takes into consideration the income along with expends that are not realised and is utilized for

CORPORATE ACCOUNTING

Requirement (iii)

Other comprehensive statement of income: Items reported in other comprehensive

statement of income

The comprehensive statement of earning of the firm Qantas Airways highlights other

comprehensive earning/loss for the particular year. This statement presents the statutory

profit for the financial year 2017 and 2016. Other comprehensive earning or else loss states

that Qantas Airways registered comprehensive income of $180 million, while company

registered other comprehensive loss of -$179 million. This statement also replicates total

comprehensive income of $1033 million in the year 2017 while the same was recorded to be

$850 million. The items that are essentially included in this section are the net exchange

variances from transactions of necessarily foreign operations that are taken under equity,

overall amount of reserve for foreign translations that are essentially transferred to net profit

as well as fair value adjustment on particularly hedging of cash flow (Miglani et al., 2015).

Requirement (iv)

The net exchange variances can be witnessed in effectual alterations in fair value of hedging

of cash flow that reflects drastic increase during the year 2017. Again, there is drastic decline

in the transfer of particularly hedge reserve to essentially consolidated income statement to -

$6 million from $198 million.

Requirement (v)

Reason why these items are reported in P/L statement

In essence, comprehensive income statement is necessarily utilized for the purpose of

enumeration of any kind of alteration in primarily interests of varied owners. In essence, this

takes into consideration the income along with expends that are not realised and is utilized for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

CORPORATE ACCOUNTING

the purpose of sidestepping the earnings statement (Miao et al., 2016). In particular, other

comprehensive statement of earning considers certain items namely gain/loss from different

derivative instruments, effectual portion of alterations in specifically fair value of hedging of

flow of cash (that is net of taxes), transfer of reserve of hedge to mainly consolidated income

statement (that is net of taxes), identification of effectual hedge of cash flow on particularly

capitalised assets (that is net of taxes) (Kushnirenko, 2017). Also, this statement replicates net

alterations in reserve of hedge for particularly time value of specific options (that is net of

taxes). Furthermore, this statement includes foreign currency translation of varied controlled

entities, translation of foreign currency of necessarily investments that is accounted for

mainly under the equity mechanism and shares of diverse other comprehensive earning or

else loss of investments accounted under the equity method.

Requirement (vi)

The amount of income tax expenditure was registered to be -$328 million in 2017 and -$395

million. In essence, the income tax expenditure utilizes the domestic corporate rate tax of

approximately 30% and statutory profit before income tax expends are adjusted for non-

assessable dividends from particularly controlled entities, different non-deductible share of

particularly net loss for specifically investments accounted under equity system, varied non-

deductible losses essentially for foreign branches as well as controlled entity losses (Warren

& Jones, 2018). Adjustments also include usage of previously unrecognized losses of capital,

non-assessable gain on particularly disposal of PPE, other non-assessable items as well as

provisions from previous periods (Ijiri, 2018).

CORPORATE ACCOUNTING

the purpose of sidestepping the earnings statement (Miao et al., 2016). In particular, other

comprehensive statement of earning considers certain items namely gain/loss from different

derivative instruments, effectual portion of alterations in specifically fair value of hedging of

flow of cash (that is net of taxes), transfer of reserve of hedge to mainly consolidated income

statement (that is net of taxes), identification of effectual hedge of cash flow on particularly

capitalised assets (that is net of taxes) (Kushnirenko, 2017). Also, this statement replicates net

alterations in reserve of hedge for particularly time value of specific options (that is net of

taxes). Furthermore, this statement includes foreign currency translation of varied controlled

entities, translation of foreign currency of necessarily investments that is accounted for

mainly under the equity mechanism and shares of diverse other comprehensive earning or

else loss of investments accounted under the equity method.

Requirement (vi)

The amount of income tax expenditure was registered to be -$328 million in 2017 and -$395

million. In essence, the income tax expenditure utilizes the domestic corporate rate tax of

approximately 30% and statutory profit before income tax expends are adjusted for non-

assessable dividends from particularly controlled entities, different non-deductible share of

particularly net loss for specifically investments accounted under equity system, varied non-

deductible losses essentially for foreign branches as well as controlled entity losses (Warren

& Jones, 2018). Adjustments also include usage of previously unrecognized losses of capital,

non-assessable gain on particularly disposal of PPE, other non-assessable items as well as

provisions from previous periods (Ijiri, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE ACCOUNTING

Requirement (vii)

Amount of income tax is enumerated utilizing rates of tax that are imposed significantly by

the financial position assertion. The current expenditure on tax during the year 2017 was

recorded to be ($328 million) during the financial year 2017 while the same was registered to

be ($395 million) in 2016 as mentioned in the financial pronouncement. In essence, this

shows that the tax expenditure has escalated by around $67 million. Thus, it cannot be hereby

analysed whether figures for income tax expenditure are identical as that of the tax rate times

the total accounting earnings (Heese et al., 2015).

Requirement (viii)

The deferred tax (liabilities) or assets of the firm Qantas Airways stands at ($353 million

during the year 2017 whereas the same stands at $39 million. Essentially, deferred tax is

necessarily identified with regard to temporary variances between particularly carrying

amounts of specifically the carrying amounts of assets/liabilities for mainly pecuniary

reporting reasons and the total amounts utilized for taxation. Particularly, deferred tax assets

are necessarily identified for specifically unused losses for tax, unused credits for tax along

with deductible temporary variances to the particular extent that it is likely that taxable profits

in the upcoming period against which they can be utilized (Chaibi et al., 2014).

Requirement (ix)

The income tax expends for the financial year 2017 is recorded to be ($328 million) while the

same was recorded to be ($395 million). However, the income tax payable stands at ($4

million). A reconciliation of income tax expense of the firm Qantas Airways to particularly

income tax payable involves adjustments for mainly temporary variances. Adjustment for

temporary variances include adjustments for inventories, plant, property as well as

CORPORATE ACCOUNTING

Requirement (vii)

Amount of income tax is enumerated utilizing rates of tax that are imposed significantly by

the financial position assertion. The current expenditure on tax during the year 2017 was

recorded to be ($328 million) during the financial year 2017 while the same was registered to

be ($395 million) in 2016 as mentioned in the financial pronouncement. In essence, this

shows that the tax expenditure has escalated by around $67 million. Thus, it cannot be hereby

analysed whether figures for income tax expenditure are identical as that of the tax rate times

the total accounting earnings (Heese et al., 2015).

Requirement (viii)

The deferred tax (liabilities) or assets of the firm Qantas Airways stands at ($353 million

during the year 2017 whereas the same stands at $39 million. Essentially, deferred tax is

necessarily identified with regard to temporary variances between particularly carrying

amounts of specifically the carrying amounts of assets/liabilities for mainly pecuniary

reporting reasons and the total amounts utilized for taxation. Particularly, deferred tax assets

are necessarily identified for specifically unused losses for tax, unused credits for tax along

with deductible temporary variances to the particular extent that it is likely that taxable profits

in the upcoming period against which they can be utilized (Chaibi et al., 2014).

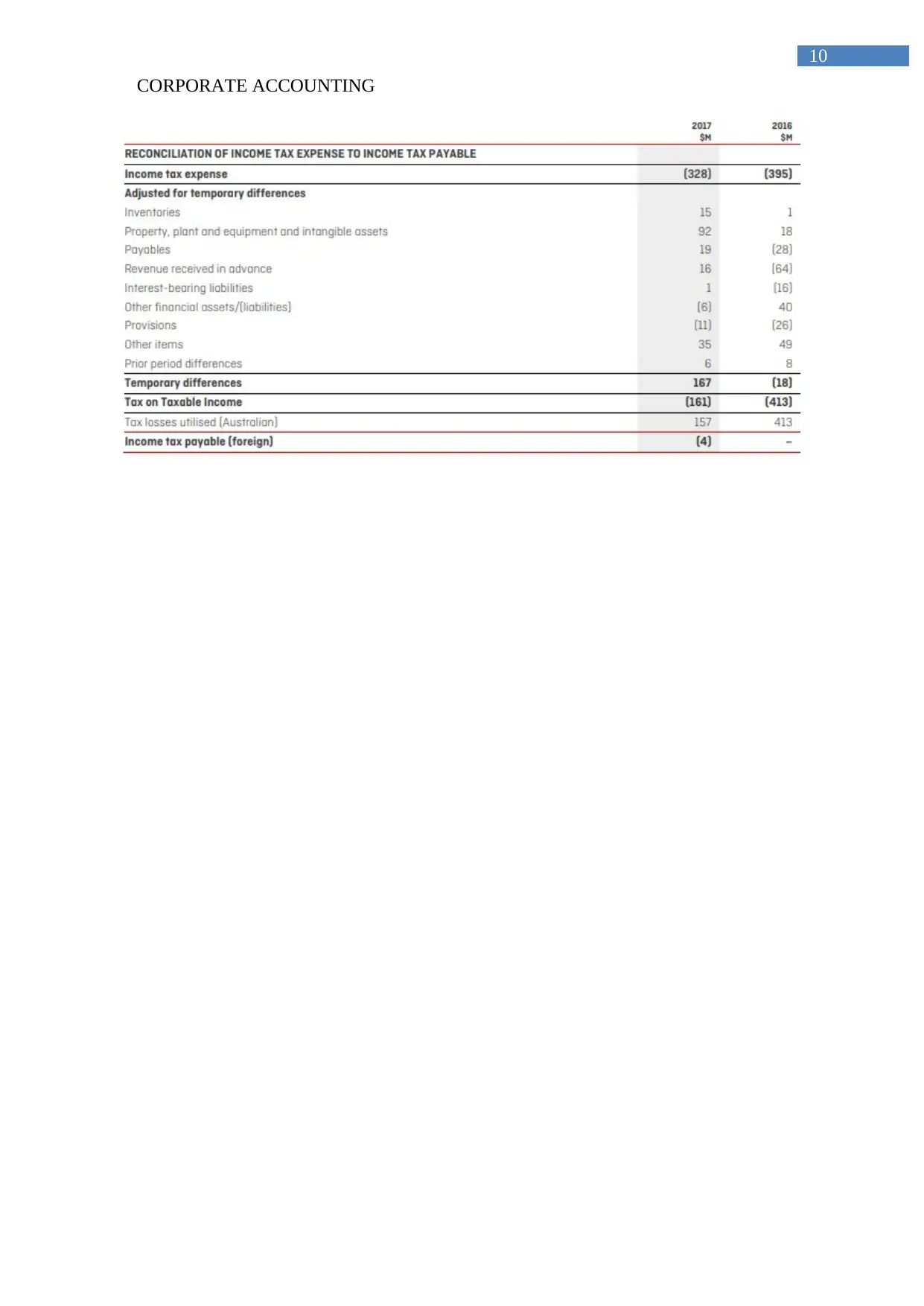

Requirement (ix)

The income tax expends for the financial year 2017 is recorded to be ($328 million) while the

same was recorded to be ($395 million). However, the income tax payable stands at ($4

million). A reconciliation of income tax expense of the firm Qantas Airways to particularly

income tax payable involves adjustments for mainly temporary variances. Adjustment for

temporary variances include adjustments for inventories, plant, property as well as

9

CORPORATE ACCOUNTING

equipment, payables, revenue that is received/accepted in advance, diverse interest bearing

liabilities, different financial assets, provisions, diverse other items and previous period

variances (Carnegie, 2014). Essentially, the temporary variances stand at $167 million in

2017 as against ($ 18 million). Therefore, the tax payable stands at ($4 million).

Requirement (x)

Analysis of the yearly financial pronouncements of the firm Qantas Airways reveals the fact

that the income tax expenditure reflected in the income assertion is not identical to that of the

income tax paid replicated in the statement on flow of cash. Essentially, payments for income

tax comprises of the influence of income tax of specific losses or else gains associated to

financing activities so that the after tax flow of cash is replicated in the subtotals of net flow

of cash. However, contrarily, expenditure of the company on the income tax is essentially the

amount that replicates recording of costs of income tax (Beekes et al., 2015).

Requirement (xi)

Based on the yearly report analysis of the firm Qantas Airways, it can be recognized that

charge for particularly current tax on earnings is made founded on adjusted profits that are

necessarily attributable for any disallowed else wise non-assessable item. Further, the notes to

the financial assertions deliver the numerical reconciliation of necessarily income tax

expenditure to amount of tax payable. This kind of reconciliation delivers information to

different users regarding the computation of this kind of income tax expenditure

(Balakrishnan et al., 2016). Thus, the striking part in association to realization of income tax

expenditures is necessarily reconciliation of temporary variance and any kind of amount of

net loss incurred after tax on earnings.

CORPORATE ACCOUNTING

equipment, payables, revenue that is received/accepted in advance, diverse interest bearing

liabilities, different financial assets, provisions, diverse other items and previous period

variances (Carnegie, 2014). Essentially, the temporary variances stand at $167 million in

2017 as against ($ 18 million). Therefore, the tax payable stands at ($4 million).

Requirement (x)

Analysis of the yearly financial pronouncements of the firm Qantas Airways reveals the fact

that the income tax expenditure reflected in the income assertion is not identical to that of the

income tax paid replicated in the statement on flow of cash. Essentially, payments for income

tax comprises of the influence of income tax of specific losses or else gains associated to

financing activities so that the after tax flow of cash is replicated in the subtotals of net flow

of cash. However, contrarily, expenditure of the company on the income tax is essentially the

amount that replicates recording of costs of income tax (Beekes et al., 2015).

Requirement (xi)

Based on the yearly report analysis of the firm Qantas Airways, it can be recognized that

charge for particularly current tax on earnings is made founded on adjusted profits that are

necessarily attributable for any disallowed else wise non-assessable item. Further, the notes to

the financial assertions deliver the numerical reconciliation of necessarily income tax

expenditure to amount of tax payable. This kind of reconciliation delivers information to

different users regarding the computation of this kind of income tax expenditure

(Balakrishnan et al., 2016). Thus, the striking part in association to realization of income tax

expenditures is necessarily reconciliation of temporary variance and any kind of amount of

net loss incurred after tax on earnings.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CORPORATE ACCOUNTING

CORPORATE ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CORPORATE ACCOUNTING

References

Balakrishnan, K., Watts, R., & Zuo, L. (2016). The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), 513-542.

Beekes, W., Brown, P., & Zhang, Q. (2015). Corporate governance and the informativeness

of disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), 931-963.

Carnegie, G. (2014). Pastoral accounting in colonial Australia: a case study of unregulated

accounting. Routledge.

Chaibi, H., Trabelsi, S., & Omri, A. (2014). Investment opportunity set, corporate accounting

policy and discretionary accruals. Journal of Economic and Financial Modelling, 1(1), 1-12.

Heese, J., Khan, M., & Ramanna, K. (2015). Political Standards: Corporate Interest,

Ideology, and Leadership in the Shaping of Accounting Rules for the Market

Economy. Journal of Accounting & Economics, 64(20), 2-3.

Ijiri, Y. (2018). An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

Kushnirenko, O. (2017). Tax-Based Calculations Applied by Agricultural Enterprises as

Object of Accounting and Control. Accounting and Finance, (2), 27-35.

Miao, B., Teoh, S.H. & Zhu, Z., (2016). Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-515.

CORPORATE ACCOUNTING

References

Balakrishnan, K., Watts, R., & Zuo, L. (2016). The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), 513-542.

Beekes, W., Brown, P., & Zhang, Q. (2015). Corporate governance and the informativeness

of disclosures in Australia: A re‐examination. Accounting & Finance, 55(4), 931-963.

Carnegie, G. (2014). Pastoral accounting in colonial Australia: a case study of unregulated

accounting. Routledge.

Chaibi, H., Trabelsi, S., & Omri, A. (2014). Investment opportunity set, corporate accounting

policy and discretionary accruals. Journal of Economic and Financial Modelling, 1(1), 1-12.

Heese, J., Khan, M., & Ramanna, K. (2015). Political Standards: Corporate Interest,

Ideology, and Leadership in the Shaping of Accounting Rules for the Market

Economy. Journal of Accounting & Economics, 64(20), 2-3.

Ijiri, Y. (2018). An Introduction to Corporate Accounting Standards: A Review. Accounting,

Economics, and Law: A Convivium, 8(1).

Kushnirenko, O. (2017). Tax-Based Calculations Applied by Agricultural Enterprises as

Object of Accounting and Control. Accounting and Finance, (2), 27-35.

Miao, B., Teoh, S.H. & Zhu, Z., (2016). Limited attention, statement of cash flow disclosure,

and the valuation of accruals. Review of Accounting Studies, 21(2), pp.473-515.

12

CORPORATE ACCOUNTING

Miglani, S., Ahmed, K., & Henry, D. (2015). Voluntary corporate governance structure and

financial distress: evidence from Australia. Journal of Contemporary Accounting &

Economics, 11(1), 18-30.

Reid, W. & Myddelton, D.R., (2017). Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate

social responsibility contribute to firm financial performance? The mediating role of

competitive advantage, reputation, and customer satisfaction. Journal of Business

Research, 68(2), 341-350.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Sierra‐García, L., Zorio‐Grima, A. & García‐Benau, M.A., (2015). Stakeholder engagement,

corporate social responsibility and integrated reporting: an exploratory study. Corporate

Social Responsibility and Environmental Management, 22(5), pp.286-304.

Siew, R.Y., (2015). A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Tschopp, D. & Nastanski, M., (2014). The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

CORPORATE ACCOUNTING

Miglani, S., Ahmed, K., & Henry, D. (2015). Voluntary corporate governance structure and

financial distress: evidence from Australia. Journal of Contemporary Accounting &

Economics, 11(1), 18-30.

Reid, W. & Myddelton, D.R., (2017). Cash flow statement. In The Meaning of Company

Accounts (pp. 16-16). Routledge.

Saeidi, S. P., Sofian, S., Saeidi, P., Saeidi, S. P., & Saaeidi, S. A. (2015). How does corporate

social responsibility contribute to firm financial performance? The mediating role of

competitive advantage, reputation, and customer satisfaction. Journal of Business

Research, 68(2), 341-350.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Schaltegger, S., & Burritt, R. (2017). Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Sierra‐García, L., Zorio‐Grima, A. & García‐Benau, M.A., (2015). Stakeholder engagement,

corporate social responsibility and integrated reporting: an exploratory study. Corporate

Social Responsibility and Environmental Management, 22(5), pp.286-304.

Siew, R.Y., (2015). A review of corporate sustainability reporting tools (SRTs). Journal of

environmental management, 164, pp.180-195.

Tschopp, D. & Nastanski, M., (2014). The harmonization and convergence of corporate

social responsibility reporting standards. Journal of Business Ethics, 125(1), pp.147-162.

Warren, C. S., & Jones, J. (2018). Corporate financial accounting. Cengage Learning.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.