Corporate Accounting: Financial Statement Analysis of Qantas Airways

VerifiedAdded on 2021/05/31

|16

|2218

|33

Report

AI Summary

This report offers a detailed financial analysis of Qantas Airways, examining key aspects of its financial statements. The report begins with an analysis of the cash flow statement, breaking down operating, investing, and financing activities, and highlighting significant trends in cash inflows and outflows over a three-year period. It then delves into the comprehensive income statement, identifying items that report comprehensive earnings and discussing the rationale behind their inclusion. The report further investigates income tax expenses, including present tax expenses, deferred tax assets and liabilities, and the reconciliation of income tax expense to tax payable. By examining these elements, the report provides a comprehensive overview of Qantas Airways' financial performance and position, offering valuable insights into its accounting practices and financial health. The analysis incorporates references to relevant accounting literature to support the findings.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

University Name

Student Name

Authors’ Note

Corporate Accounting

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

CORPORATE ACCOUNTING

Table of Contents

Answer to Question i)................................................................................................................3

Answer to Question ii)...............................................................................................................3

Answer to Question iii)..............................................................................................................5

Answer to Question iv)..............................................................................................................6

Answer to Question v)...............................................................................................................6

Answer to Question vi)..............................................................................................................6

Answer to Question vii).............................................................................................................7

Answer to Question viii)............................................................................................................7

Answer to Question ix)..............................................................................................................8

Answer to Question x)...............................................................................................................8

Answer to Question xi)..............................................................................................................9

References................................................................................................................................10

Appendix..................................................................................................................................11

CORPORATE ACCOUNTING

Table of Contents

Answer to Question i)................................................................................................................3

Answer to Question ii)...............................................................................................................3

Answer to Question iii)..............................................................................................................5

Answer to Question iv)..............................................................................................................6

Answer to Question v)...............................................................................................................6

Answer to Question vi)..............................................................................................................6

Answer to Question vii).............................................................................................................7

Answer to Question viii)............................................................................................................7

Answer to Question ix)..............................................................................................................8

Answer to Question x)...............................................................................................................8

Answer to Question xi)..............................................................................................................9

References................................................................................................................................10

Appendix..................................................................................................................................11

3

CORPORATE ACCOUNTING

The current study intends to carry out detailed analysis of yearly reports with special

reference to the operations of the firm Qantas Airways.

Answer to Question i)

List of each item reported in the assertion of cash stream

The assertion on the stream of cash of the selected firm Qantas Airways consists of

traditionally three different segments such as operating activities, investing activities along

with financing activities. The exhaustive list of items takes in changes in the company’s

earnings, varied liabilities, and various inventories together with alterations in diverse

operational acts. Different items that are included under cash utilized for investing activities

takes account of investment for corporation’s plant, property along with equipment (PPE)

along with intangibles, income earned from sales of PPE of the firm, income generated from

clearance as well as sales of business as well as associates, overall investment carried out in

mainly different associates and different joint deal of the business concern. In addition to this,

different items that are included under the caption of investing acts contain cash used for the

purpose of acquirement of various associates, redemption/investment in distinctively loan

notes (Watson 2015).

Answer to Question ii)

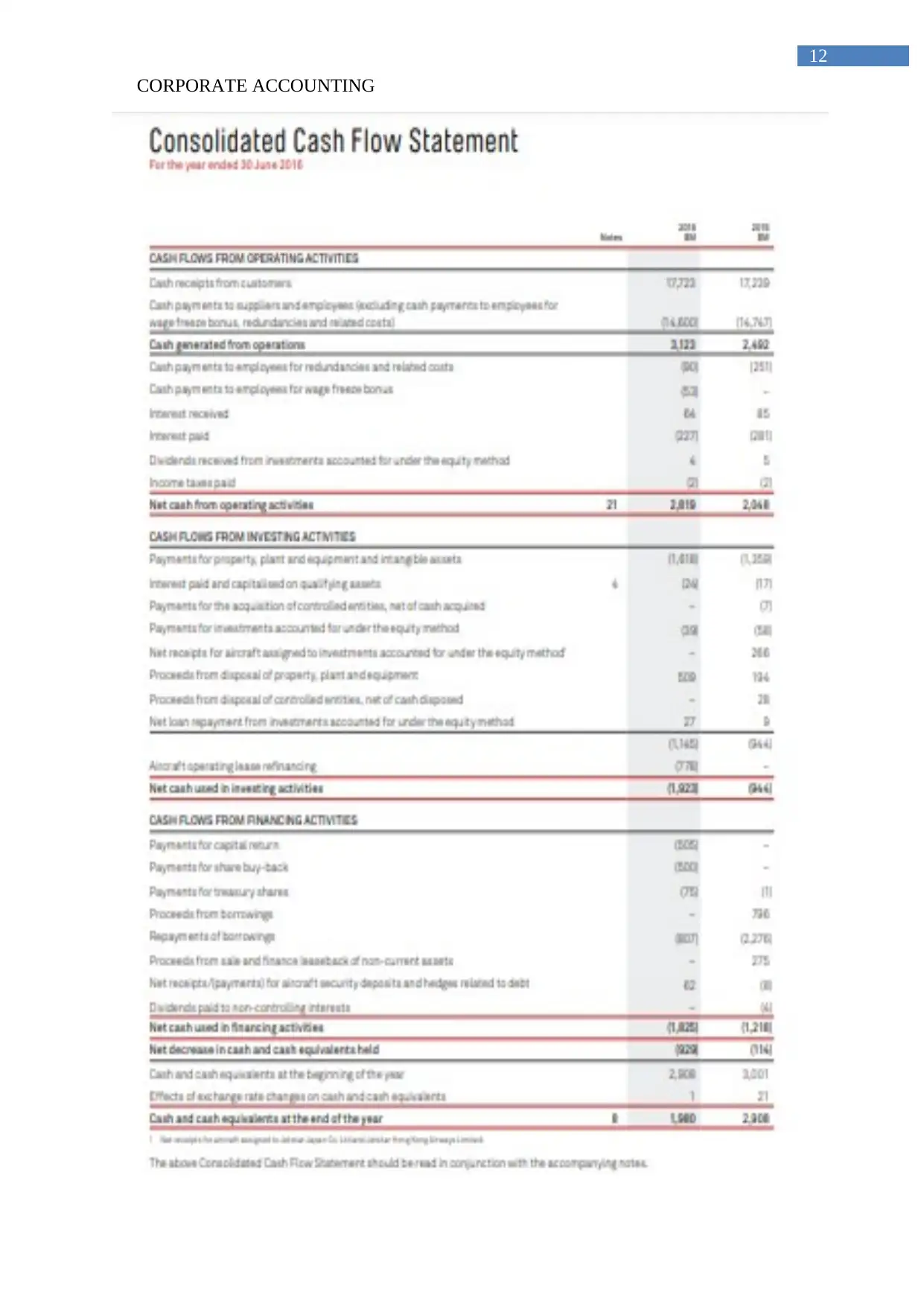

Analysis of stream of cash of the firm Qantas Airways divulges the fact that the cash

generated out of the operational acts of the corporation takes account of AUD 2704 m in the

financial year (2017). On the other hand, the same was registered to be AUD 2819 m in the

financial year (2016). As a result, it can necessarily be stated that inflow of cash stream from

operational activities increased to approximately AUD 2819 m in the financial year 2016

CORPORATE ACCOUNTING

The current study intends to carry out detailed analysis of yearly reports with special

reference to the operations of the firm Qantas Airways.

Answer to Question i)

List of each item reported in the assertion of cash stream

The assertion on the stream of cash of the selected firm Qantas Airways consists of

traditionally three different segments such as operating activities, investing activities along

with financing activities. The exhaustive list of items takes in changes in the company’s

earnings, varied liabilities, and various inventories together with alterations in diverse

operational acts. Different items that are included under cash utilized for investing activities

takes account of investment for corporation’s plant, property along with equipment (PPE)

along with intangibles, income earned from sales of PPE of the firm, income generated from

clearance as well as sales of business as well as associates, overall investment carried out in

mainly different associates and different joint deal of the business concern. In addition to this,

different items that are included under the caption of investing acts contain cash used for the

purpose of acquirement of various associates, redemption/investment in distinctively loan

notes (Watson 2015).

Answer to Question ii)

Analysis of stream of cash of the firm Qantas Airways divulges the fact that the cash

generated out of the operational acts of the corporation takes account of AUD 2704 m in the

financial year (2017). On the other hand, the same was registered to be AUD 2819 m in the

financial year (2016). As a result, it can necessarily be stated that inflow of cash stream from

operational activities increased to approximately AUD 2819 m in the financial year 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

CORPORATE ACCOUNTING

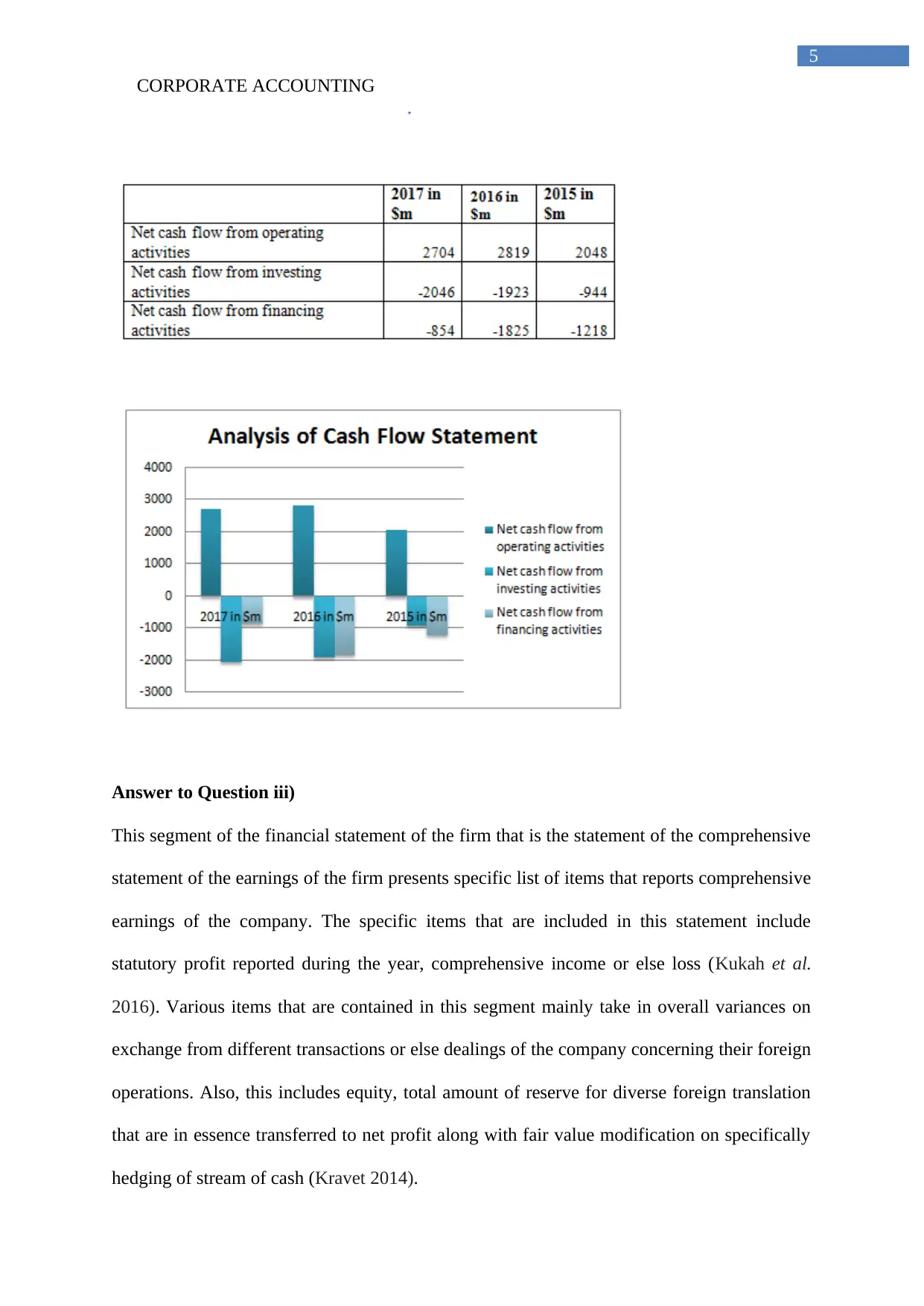

from the point of AUD 2014 m documented in the year 2015. A downward movement

therefore can be observed in the inflow of cash from operational acts in the year 2017. This is

on account of augmented receipts of the business concern from their customers, enhancement

in interests that are accepted by the corporation and decrease in overall costs borne for the

purpose of borrowing and steady reduction in overall disbursements for income tax.

Analysis of cash flow from investing activities of the firm Qantas Airways reveals the fact

that the there is outward stream of cash throughout the specified three year period. However,

the outward stream of cash is observed to have increased during the three year period from -

$944 m in 2015 to -$1923 m in 2016 to -2046 m in 2017. This movement in the stream of

cash reveals enhanced outlay of the firm towards plant, property along with equipment,

shrinkage in outward movement or else stream of cash for firm’s requirement to acquire

subsidiaries. Also, there is also higher inward stream of cash that is generated out of the

earnings stemming from sale of business units’ PPE and increased income from sale of

majority of businesses together with business associates (Watson 2015).

Critical analysis of the flow of cash from financial acts is said to have enhanced during the

year 2016 in comparison to figure that is primarily recognized in the year 2015. Cash flow

from financing acts increased from -$1218 m in 2015 to -$1825 m in 2016. However, the

same is said to have thereafter further declined in the year 2017 to approximately -$854 m in

2017. Fundamentally, this is chiefly because of enhancement in payments of interests and at

the same time capitalised especially on diverse assets and particularly due to shrink in overall

proceeds acquired by the firm from sales of the firm (Kravet 2014). Nevertheless, finally,

numeral documented in the financial statement of firm represents decline in cash and cash

equivalents inflow during the closing of the financial year. Fundamentally, shrink in the

figure for cash and cash equivalents presents decrease in inward flow of cash for the

company.

CORPORATE ACCOUNTING

from the point of AUD 2014 m documented in the year 2015. A downward movement

therefore can be observed in the inflow of cash from operational acts in the year 2017. This is

on account of augmented receipts of the business concern from their customers, enhancement

in interests that are accepted by the corporation and decrease in overall costs borne for the

purpose of borrowing and steady reduction in overall disbursements for income tax.

Analysis of cash flow from investing activities of the firm Qantas Airways reveals the fact

that the there is outward stream of cash throughout the specified three year period. However,

the outward stream of cash is observed to have increased during the three year period from -

$944 m in 2015 to -$1923 m in 2016 to -2046 m in 2017. This movement in the stream of

cash reveals enhanced outlay of the firm towards plant, property along with equipment,

shrinkage in outward movement or else stream of cash for firm’s requirement to acquire

subsidiaries. Also, there is also higher inward stream of cash that is generated out of the

earnings stemming from sale of business units’ PPE and increased income from sale of

majority of businesses together with business associates (Watson 2015).

Critical analysis of the flow of cash from financial acts is said to have enhanced during the

year 2016 in comparison to figure that is primarily recognized in the year 2015. Cash flow

from financing acts increased from -$1218 m in 2015 to -$1825 m in 2016. However, the

same is said to have thereafter further declined in the year 2017 to approximately -$854 m in

2017. Fundamentally, this is chiefly because of enhancement in payments of interests and at

the same time capitalised especially on diverse assets and particularly due to shrink in overall

proceeds acquired by the firm from sales of the firm (Kravet 2014). Nevertheless, finally,

numeral documented in the financial statement of firm represents decline in cash and cash

equivalents inflow during the closing of the financial year. Fundamentally, shrink in the

figure for cash and cash equivalents presents decrease in inward flow of cash for the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

CORPORATE ACCOUNTING

Answer to Question iii)

This segment of the financial statement of the firm that is the statement of the comprehensive

statement of the earnings of the firm presents specific list of items that reports comprehensive

earnings of the company. The specific items that are included in this statement include

statutory profit reported during the year, comprehensive income or else loss (Kukah et al.

2016). Various items that are contained in this segment mainly take in overall variances on

exchange from different transactions or else dealings of the company concerning their foreign

operations. Also, this includes equity, total amount of reserve for diverse foreign translation

that are in essence transferred to net profit along with fair value modification on specifically

hedging of stream of cash (Kravet 2014).

CORPORATE ACCOUNTING

Answer to Question iii)

This segment of the financial statement of the firm that is the statement of the comprehensive

statement of the earnings of the firm presents specific list of items that reports comprehensive

earnings of the company. The specific items that are included in this statement include

statutory profit reported during the year, comprehensive income or else loss (Kukah et al.

2016). Various items that are contained in this segment mainly take in overall variances on

exchange from different transactions or else dealings of the company concerning their foreign

operations. Also, this includes equity, total amount of reserve for diverse foreign translation

that are in essence transferred to net profit along with fair value modification on specifically

hedging of stream of cash (Kravet 2014).

6

CORPORATE ACCOUNTING

Answer to Question iv)

Overall exchange variation can be observed in effective transformation in fair value hedging

of stream of cash that replicates sharp increase in the financial year 2017. Additionally, there

is drastic decrease in transfer of specifically reserve of hedge to necessarily consolidated

earnings pronouncements. This is recorded to be mere $6 m from the level of $198m in 2016.

Answer to Question v)

Rationale behind why these specific items are pronounced in the P/L assertion

Essentially, pronouncement on other comprehensive income also indicated as OCI takes in

varied items. This takes in both income as well as expenditure including adjustments that are

undertaken for largely reclassification. This is routinely identified in the assertion for profit or

else loss mentioned in the P/L account. In essence, accountability of OCI is for the most

supports profit otherwise loss (Watson 2015). Again, of its own accord, any kind of gains

otherwise loss can be accepted in the assertion of other comprehensive income when this

completed other types of comprehensive part of earnings.

Answer to Question vi)

The present tax expends of the firm Qantas Airways during the financial year 2017 was noted

to be -$328 m in the financial year 2017 as well as -$395 m in 2016. In particular, the income

tax expend uses domestic corporate tax rate of roughly 30% and statutory profit before

income tax expenditure are modified for non-assessable dividends from specifically

controlled entities, diverse non-deductible share of specifically net loss for particularly

investments that are taken into account for the system of equity, diverse non-assessable gain

on predominantly disposal of plant, property as well as equipment (also indicated as PPE),

CORPORATE ACCOUNTING

Answer to Question iv)

Overall exchange variation can be observed in effective transformation in fair value hedging

of stream of cash that replicates sharp increase in the financial year 2017. Additionally, there

is drastic decrease in transfer of specifically reserve of hedge to necessarily consolidated

earnings pronouncements. This is recorded to be mere $6 m from the level of $198m in 2016.

Answer to Question v)

Rationale behind why these specific items are pronounced in the P/L assertion

Essentially, pronouncement on other comprehensive income also indicated as OCI takes in

varied items. This takes in both income as well as expenditure including adjustments that are

undertaken for largely reclassification. This is routinely identified in the assertion for profit or

else loss mentioned in the P/L account. In essence, accountability of OCI is for the most

supports profit otherwise loss (Watson 2015). Again, of its own accord, any kind of gains

otherwise loss can be accepted in the assertion of other comprehensive income when this

completed other types of comprehensive part of earnings.

Answer to Question vi)

The present tax expends of the firm Qantas Airways during the financial year 2017 was noted

to be -$328 m in the financial year 2017 as well as -$395 m in 2016. In particular, the income

tax expend uses domestic corporate tax rate of roughly 30% and statutory profit before

income tax expenditure are modified for non-assessable dividends from specifically

controlled entities, diverse non-deductible share of specifically net loss for particularly

investments that are taken into account for the system of equity, diverse non-assessable gain

on predominantly disposal of plant, property as well as equipment (also indicated as PPE),

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

CORPORATE ACCOUNTING

different non-quantifiable items along with provisions from various period of time (Shapiro

2015).

Answer to Question vii)

Total amount of income tax is calculated by using specific tax rates that are necessarily

forced noticeably by the financial position announcement. Again, the present expends on tax

in the financial year 2017 was registered to be -$328 m in the financial year 2017. On the

other hand, the same was recorded to be -$395 million in the financial year 2016 as presented

in the pecuniary declaration. Particularly, this reflects that expenditure of the firm on tax has

increased by approximately $67 m. Hence, it cannot be hereby evaluated whether numerals

are identical as that of the rate of tax times overall accounting income.

Answer to Question viii)

Deferred tax (for both assets/liabilities) of the corporation Qantas Airways is documented to

be -$353 m in the financial year 2017. Conversely, the same is registered to be $39 m in

2026. In essence, this deferred tax is essentially recognized with respect to temporary

variances. Essentially, deferred tax is primarily recognized with respect to temporary

variance between principally carrying amounts of mainly carrying amounts of assets else

wise liabilities for the most part financial assertion reasons and overall amounts used for the

purpose of taxation (Balakrishnan et al. 2016). In essence, deferred tax (indicated as tax

assets) are essentially recognized for particularly unutilized loss due to tax, unutilized credits

for mainly credit for particularly tax in conjunction with deductible temporary variation to

certain extent. This is expected that taxable gains in the forthcoming period against which

they can be used.

CORPORATE ACCOUNTING

different non-quantifiable items along with provisions from various period of time (Shapiro

2015).

Answer to Question vii)

Total amount of income tax is calculated by using specific tax rates that are necessarily

forced noticeably by the financial position announcement. Again, the present expends on tax

in the financial year 2017 was registered to be -$328 m in the financial year 2017. On the

other hand, the same was recorded to be -$395 million in the financial year 2016 as presented

in the pecuniary declaration. Particularly, this reflects that expenditure of the firm on tax has

increased by approximately $67 m. Hence, it cannot be hereby evaluated whether numerals

are identical as that of the rate of tax times overall accounting income.

Answer to Question viii)

Deferred tax (for both assets/liabilities) of the corporation Qantas Airways is documented to

be -$353 m in the financial year 2017. Conversely, the same is registered to be $39 m in

2026. In essence, this deferred tax is essentially recognized with respect to temporary

variances. Essentially, deferred tax is primarily recognized with respect to temporary

variance between principally carrying amounts of mainly carrying amounts of assets else

wise liabilities for the most part financial assertion reasons and overall amounts used for the

purpose of taxation (Balakrishnan et al. 2016). In essence, deferred tax (indicated as tax

assets) are essentially recognized for particularly unutilized loss due to tax, unutilized credits

for mainly credit for particularly tax in conjunction with deductible temporary variation to

certain extent. This is expected that taxable gains in the forthcoming period against which

they can be used.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

CORPORATE ACCOUNTING

Answer to Question ix)

As rightly indicated by (), the income tax outgoings for the financial year 2017 is slated to be

-$328 m in 2017 whereas the same is sketched to be -395 m in 2016. Nevertheless, the

income tax payable is registered to be -4 m. Therefore, a reconciliation of expenditure of

income tax of the business concern Qantas Airways to essentially income tax payable

engages adjustment for particularly temporary variances. Modification for temporary

variances includes important adjustment for particularly temporary variations (Uyar 2016).

As such, the temporary variation contains adjustments made for firm’s inventories, PPE,

different obligation of payables, firm’s revenues that firm accepts in advance, varied

liabilities that are essentially interest bearing, diverse financial assets as well as variation of

prior period. In itself, temporary variations for the firm are observed to be $167 m in 2017 as

compared to -$18 m in the year 2016. Hence, tax payable necessarily is documented to be -

$4m.

Answer to Question x)

Detailed analysis of financial report of the business concern Qantas Airways divulges that

expend of the firm on tax gets represented in the earnings pronouncement. This is not

indistinguishable to that of income tax paid represented in the assertion on stream of cash. In

essence, disbursements for particularly tax on earnings consists of influence of income tax

linked to different financing acts so that stream of cash after imposition of tax is represented

in the sub totals of net stream of cash (Warren and Jones 2018). On the contrary, expend of

the business concern on the tax is necessarily the total amount that represents costs borne for

income tax.

CORPORATE ACCOUNTING

Answer to Question ix)

As rightly indicated by (), the income tax outgoings for the financial year 2017 is slated to be

-$328 m in 2017 whereas the same is sketched to be -395 m in 2016. Nevertheless, the

income tax payable is registered to be -4 m. Therefore, a reconciliation of expenditure of

income tax of the business concern Qantas Airways to essentially income tax payable

engages adjustment for particularly temporary variances. Modification for temporary

variances includes important adjustment for particularly temporary variations (Uyar 2016).

As such, the temporary variation contains adjustments made for firm’s inventories, PPE,

different obligation of payables, firm’s revenues that firm accepts in advance, varied

liabilities that are essentially interest bearing, diverse financial assets as well as variation of

prior period. In itself, temporary variations for the firm are observed to be $167 m in 2017 as

compared to -$18 m in the year 2016. Hence, tax payable necessarily is documented to be -

$4m.

Answer to Question x)

Detailed analysis of financial report of the business concern Qantas Airways divulges that

expend of the firm on tax gets represented in the earnings pronouncement. This is not

indistinguishable to that of income tax paid represented in the assertion on stream of cash. In

essence, disbursements for particularly tax on earnings consists of influence of income tax

linked to different financing acts so that stream of cash after imposition of tax is represented

in the sub totals of net stream of cash (Warren and Jones 2018). On the contrary, expend of

the business concern on the tax is necessarily the total amount that represents costs borne for

income tax.

9

CORPORATE ACCOUNTING

Answer to Question xi)

Founded on annual financial statement of the firm Qantas Airways, it can be identified that

charge for mainly current tax on income is based on adjusted profits. This is necessarily

attributable for any type of disqualified or else non-assessable item. Moreover, notes

provided after pecuniary statements presents the reconciliation of particularly earning tax

expend to entire quantity of tax payable. In essence, this sort of reconciliation presents

information to particular users concerning computation of this type of income tax (Jefrey

2018). As a consequence, the important part in relation to realization of tax expenses is

principally reconciliation of the temporary variation and net loss borne after imposition of tax

on income.

CORPORATE ACCOUNTING

Answer to Question xi)

Founded on annual financial statement of the firm Qantas Airways, it can be identified that

charge for mainly current tax on income is based on adjusted profits. This is necessarily

attributable for any type of disqualified or else non-assessable item. Moreover, notes

provided after pecuniary statements presents the reconciliation of particularly earning tax

expend to entire quantity of tax payable. In essence, this sort of reconciliation presents

information to particular users concerning computation of this type of income tax (Jefrey

2018). As a consequence, the important part in relation to realization of tax expenses is

principally reconciliation of the temporary variation and net loss borne after imposition of tax

on income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

CORPORATE ACCOUNTING

References

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Kravet, T.D., 2014. Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2), pp.218-240.

Kukah, M.A., Amidu, M. and Abor, J.Y., 2016. Corporate governance mechanisms and

accounting information quality of listed firms in Ghana. African Journal of Accounting,

Auditing and Finance, 5(1), pp.38-58.

Shapiro, D.M., 2015. Assessing Corporate Governance in M&As. Journal of Corporate

Accounting & Finance, 26(2), pp.35-39.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of Corporate

Accounting & Finance, 27(4), pp.27-30.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

CORPORATE ACCOUNTING

References

Balakrishnan, K., Watts, R. and Zuo, L., 2016. The effect of accounting conservatism on

corporate investment during the global financial crisis. Journal of Business Finance &

Accounting, 43(5-6), pp.513-542.

Jefrey, C. ed., 2018. Research on professional responsibility and ethics in accounting.

Emerald Publishing Limited.

Kravet, T.D., 2014. Accounting conservatism and managerial risk-taking: Corporate

acquisitions. Journal of Accounting and Economics, 57(2), pp.218-240.

Kukah, M.A., Amidu, M. and Abor, J.Y., 2016. Corporate governance mechanisms and

accounting information quality of listed firms in Ghana. African Journal of Accounting,

Auditing and Finance, 5(1), pp.38-58.

Shapiro, D.M., 2015. Assessing Corporate Governance in M&As. Journal of Corporate

Accounting & Finance, 26(2), pp.35-39.

Uyar, A., 2016. Evolution of corporate reporting and emerging trends. Journal of Corporate

Accounting & Finance, 27(4), pp.27-30.

Warren, C.S. and Jones, J., 2018. Corporate financial accounting. Cengage Learning.

Watson, L., 2015. Corporate social responsibility research in accounting. Journal of

Accounting Literature, 34, pp.1-16.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

CORPORATE ACCOUNTING

Appendix

CORPORATE ACCOUNTING

Appendix

12

CORPORATE ACCOUNTING

CORPORATE ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.