Financial Statement Analysis, Valuation, & SWOT: Qantas Airways

VerifiedAdded on 2023/06/11

|11

|1930

|368

Report

AI Summary

This report presents a comprehensive financial statement analysis of Qantas Airways Limited, an ASX-listed firm. It employs various valuation models, including the method of comparables, dividend discount model, and discounted cash flow model, to assess the company's stock value. A SWOT analysis is conducted to evaluate the company's strengths, weaknesses, opportunities, and threats. The report compares Qantas Airways to competitors like Virgin Australia and Transurban, examining financial metrics such as sales revenue, earnings per share, and market value. The analysis concludes with an investment recommendation, suggesting that Qantas Airways' stock is undervalued and presents a potentially lucrative investment opportunity for investors. The appendices provide detailed calculations for the DCF model and cost of equity.

Running Head: Financial Statement Analysis For Business

1

Project Report: Running Head: Financial Statement Analysis For Business

1

Project Report: Running Head: Financial Statement Analysis For Business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis For Business 2

Contents

Introduction.......................................................................................................................3

Valuation model................................................................................................................3

Methods of comparables...............................................................................................3

Dividend discount model..............................................................................................4

Discounted cash flow model.........................................................................................5

SWOT analysis.................................................................................................................5

Recommendation and Conclusion....................................................................................6

References.........................................................................................................................8

Appendix...........................................................................................................................9

Contents

Introduction.......................................................................................................................3

Valuation model................................................................................................................3

Methods of comparables...............................................................................................3

Dividend discount model..............................................................................................4

Discounted cash flow model.........................................................................................5

SWOT analysis.................................................................................................................5

Recommendation and Conclusion....................................................................................6

References.........................................................................................................................8

Appendix...........................................................................................................................9

Financial Statement Analysis For Business 3

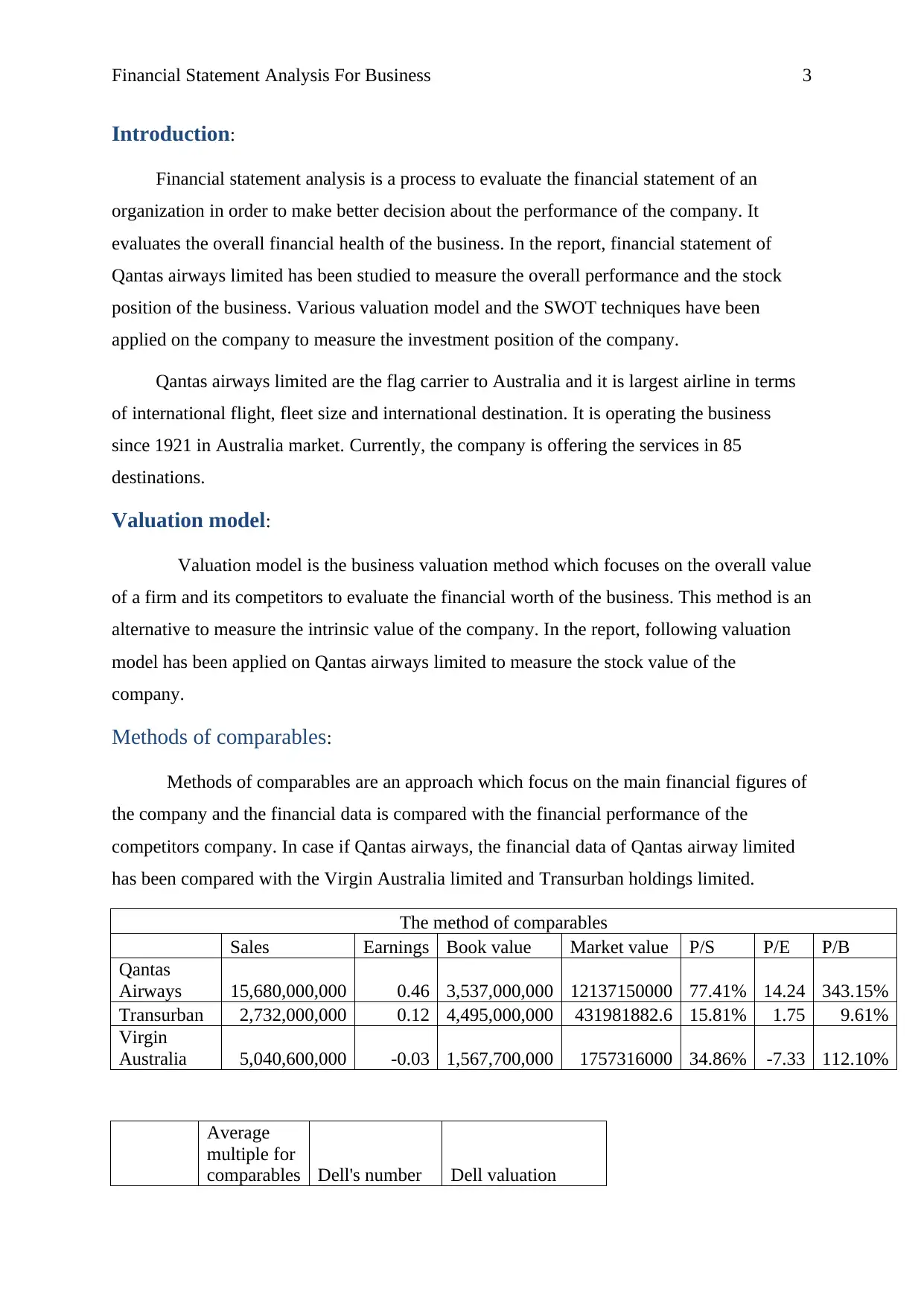

Introduction:

Financial statement analysis is a process to evaluate the financial statement of an

organization in order to make better decision about the performance of the company. It

evaluates the overall financial health of the business. In the report, financial statement of

Qantas airways limited has been studied to measure the overall performance and the stock

position of the business. Various valuation model and the SWOT techniques have been

applied on the company to measure the investment position of the company.

Qantas airways limited are the flag carrier to Australia and it is largest airline in terms

of international flight, fleet size and international destination. It is operating the business

since 1921 in Australia market. Currently, the company is offering the services in 85

destinations.

Valuation model:

Valuation model is the business valuation method which focuses on the overall value

of a firm and its competitors to evaluate the financial worth of the business. This method is an

alternative to measure the intrinsic value of the company. In the report, following valuation

model has been applied on Qantas airways limited to measure the stock value of the

company.

Methods of comparables:

Methods of comparables are an approach which focus on the main financial figures of

the company and the financial data is compared with the financial performance of the

competitors company. In case if Qantas airways, the financial data of Qantas airway limited

has been compared with the Virgin Australia limited and Transurban holdings limited.

The method of comparables

Sales Earnings Book value Market value P/S P/E P/B

Qantas

Airways 15,680,000,000 0.46 3,537,000,000 12137150000 77.41% 14.24 343.15%

Transurban 2,732,000,000 0.12 4,495,000,000 431981882.6 15.81% 1.75 9.61%

Virgin

Australia 5,040,600,000 -0.03 1,567,700,000 1757316000 34.86% -7.33 112.10%

Average

multiple for

comparables Dell's number Dell valuation

Introduction:

Financial statement analysis is a process to evaluate the financial statement of an

organization in order to make better decision about the performance of the company. It

evaluates the overall financial health of the business. In the report, financial statement of

Qantas airways limited has been studied to measure the overall performance and the stock

position of the business. Various valuation model and the SWOT techniques have been

applied on the company to measure the investment position of the company.

Qantas airways limited are the flag carrier to Australia and it is largest airline in terms

of international flight, fleet size and international destination. It is operating the business

since 1921 in Australia market. Currently, the company is offering the services in 85

destinations.

Valuation model:

Valuation model is the business valuation method which focuses on the overall value

of a firm and its competitors to evaluate the financial worth of the business. This method is an

alternative to measure the intrinsic value of the company. In the report, following valuation

model has been applied on Qantas airways limited to measure the stock value of the

company.

Methods of comparables:

Methods of comparables are an approach which focus on the main financial figures of

the company and the financial data is compared with the financial performance of the

competitors company. In case if Qantas airways, the financial data of Qantas airway limited

has been compared with the Virgin Australia limited and Transurban holdings limited.

The method of comparables

Sales Earnings Book value Market value P/S P/E P/B

Qantas

Airways 15,680,000,000 0.46 3,537,000,000 12137150000 77.41% 14.24 343.15%

Transurban 2,732,000,000 0.12 4,495,000,000 431981882.6 15.81% 1.75 9.61%

Virgin

Australia 5,040,600,000 -0.03 1,567,700,000 1757316000 34.86% -7.33 112.10%

Average

multiple for

comparables Dell's number Dell valuation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis For Business 4

Sales 0.25 15,680,000,000 3,972,932,459.49

Earnings 0.00 852380000

0.32

Book

value

0.61 3,537,000,000

2,152,360,825.70

Average valuation

2,041,764,428.51

Number of outstanding shares

1,853,000,000.0

Intrinsic value $

1.10

(Morningstar, 2018)

On the basis of the above table, it has been measured that the sales revenue, earnings

per share, market value etc of Qantas airways limited is higher than the Virgin Australia

limited and Transurban holdings limited. The price and sales ratio, price and earnings ratio,

price and book value ratio of the company has been discussed and it has been found that the

intrinsic value of the stock is $ 1.10 and the market price of the stock is $ 6.55 (Morningstar,

2018). On the basis of the study, it has been measured that the stock price of Qantas airways

limited is overvalued. .

The method is easier to calculate and communicate information to the market

participants. However, the comparison with the other companies is not useful to evaluate the

stock price of the company.

Dividend discount model:

Dividend discount model is among the business valuation methods which evaluates

the stock price of a business. It focuses on the theory that the stock price of a business is

worth the total of all the future dividend payment of the company. dividend discount model

study on Qantas airways limited is as follows:

Dividend growth rate

Year Dividend per share ($)

2013 0.050

2014 0.070

2015 0.100

2016 0.085

2017 0.070

Sales 0.25 15,680,000,000 3,972,932,459.49

Earnings 0.00 852380000

0.32

Book

value

0.61 3,537,000,000

2,152,360,825.70

Average valuation

2,041,764,428.51

Number of outstanding shares

1,853,000,000.0

Intrinsic value $

1.10

(Morningstar, 2018)

On the basis of the above table, it has been measured that the sales revenue, earnings

per share, market value etc of Qantas airways limited is higher than the Virgin Australia

limited and Transurban holdings limited. The price and sales ratio, price and earnings ratio,

price and book value ratio of the company has been discussed and it has been found that the

intrinsic value of the stock is $ 1.10 and the market price of the stock is $ 6.55 (Morningstar,

2018). On the basis of the study, it has been measured that the stock price of Qantas airways

limited is overvalued. .

The method is easier to calculate and communicate information to the market

participants. However, the comparison with the other companies is not useful to evaluate the

stock price of the company.

Dividend discount model:

Dividend discount model is among the business valuation methods which evaluates

the stock price of a business. It focuses on the theory that the stock price of a business is

worth the total of all the future dividend payment of the company. dividend discount model

study on Qantas airways limited is as follows:

Dividend growth rate

Year Dividend per share ($)

2013 0.050

2014 0.070

2015 0.100

2016 0.085

2017 0.070

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis For Business 5

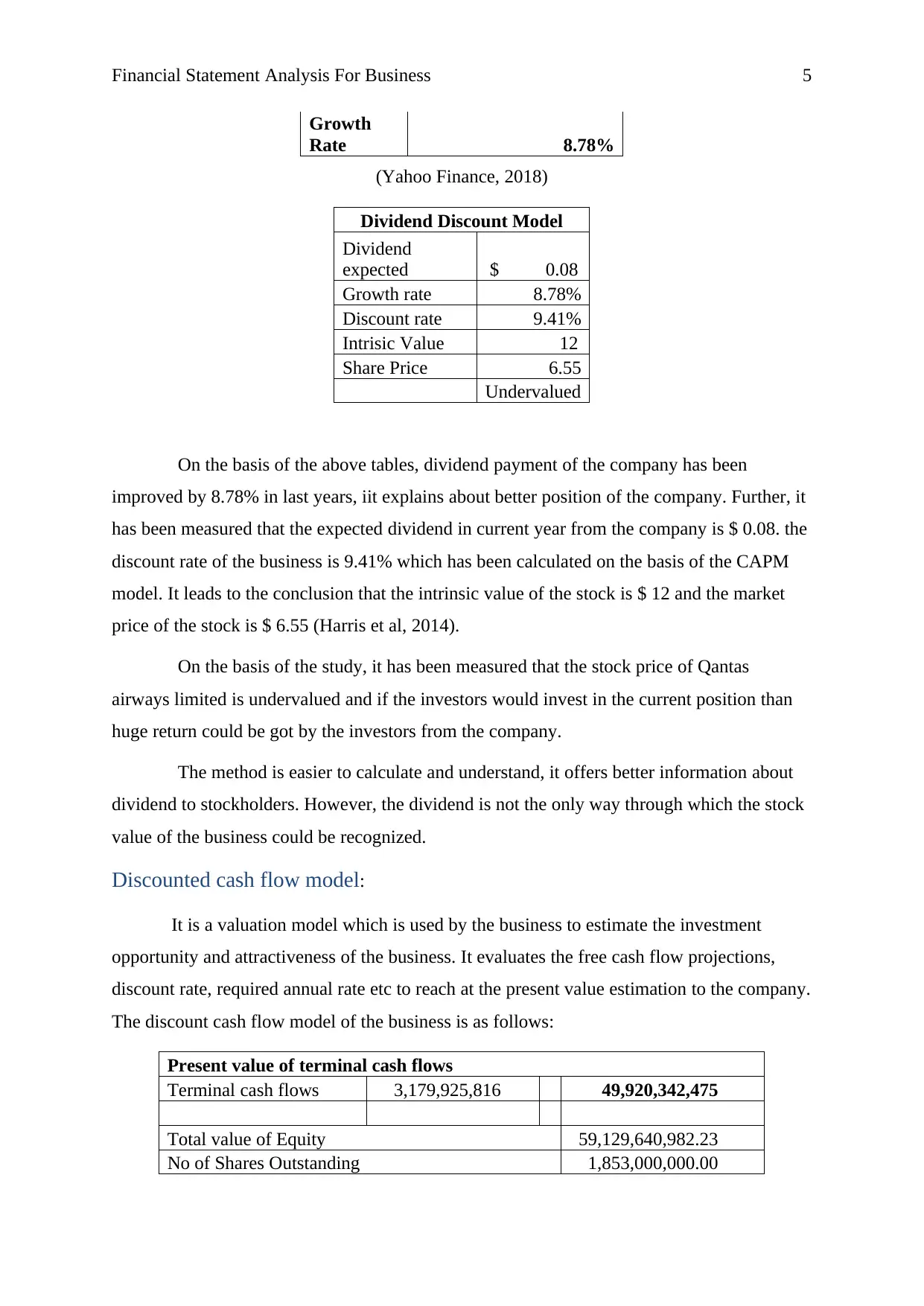

Growth

Rate 8.78%

(Yahoo Finance, 2018)

Dividend Discount Model

Dividend

expected $ 0.08

Growth rate 8.78%

Discount rate 9.41%

Intrisic Value 12

Share Price 6.55

Undervalued

On the basis of the above tables, dividend payment of the company has been

improved by 8.78% in last years, iit explains about better position of the company. Further, it

has been measured that the expected dividend in current year from the company is $ 0.08. the

discount rate of the business is 9.41% which has been calculated on the basis of the CAPM

model. It leads to the conclusion that the intrinsic value of the stock is $ 12 and the market

price of the stock is $ 6.55 (Harris et al, 2014).

On the basis of the study, it has been measured that the stock price of Qantas

airways limited is undervalued and if the investors would invest in the current position than

huge return could be got by the investors from the company.

The method is easier to calculate and understand, it offers better information about

dividend to stockholders. However, the dividend is not the only way through which the stock

value of the business could be recognized.

Discounted cash flow model:

It is a valuation model which is used by the business to estimate the investment

opportunity and attractiveness of the business. It evaluates the free cash flow projections,

discount rate, required annual rate etc to reach at the present value estimation to the company.

The discount cash flow model of the business is as follows:

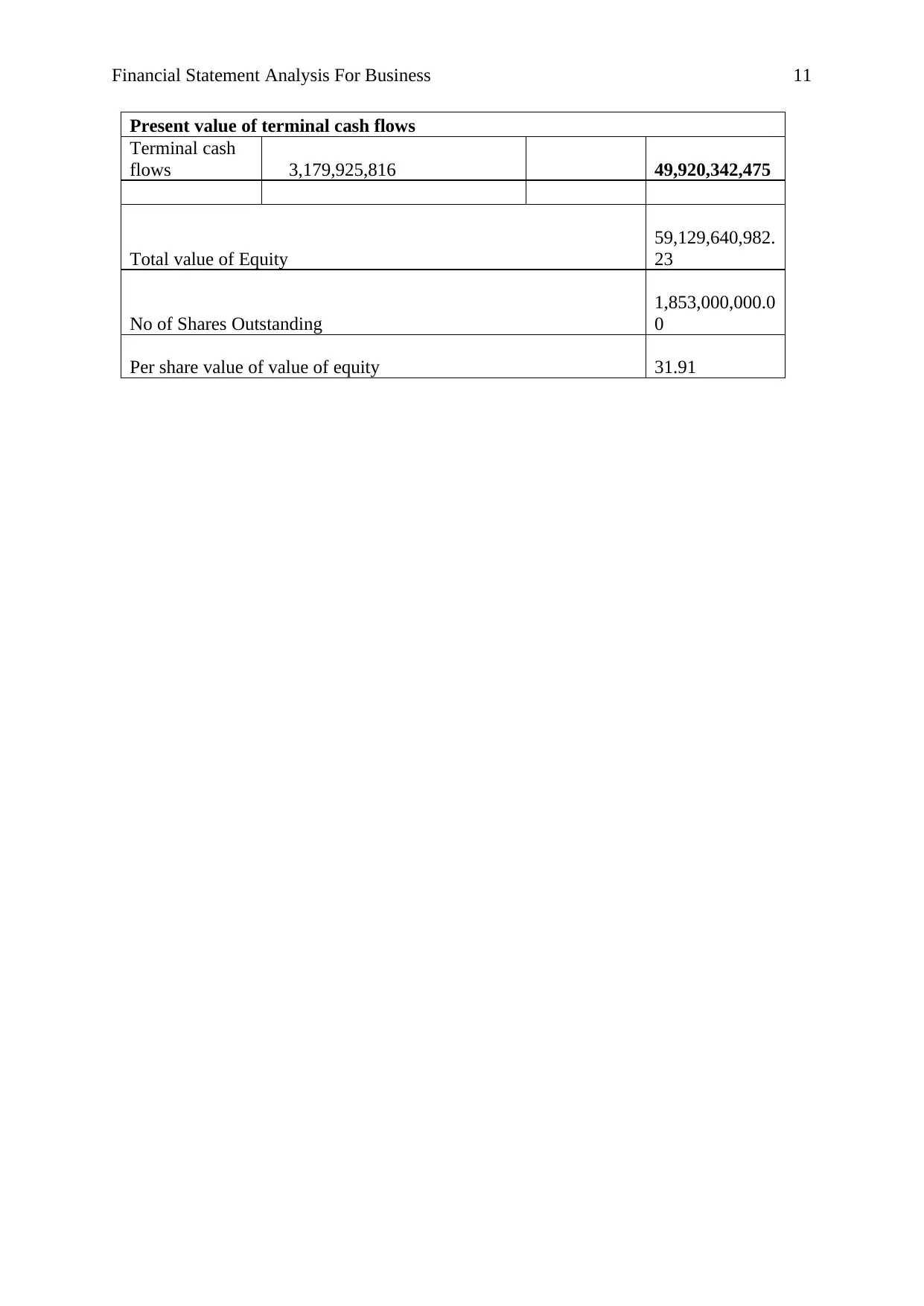

Present value of terminal cash flows

Terminal cash flows 3,179,925,816 49,920,342,475

Total value of Equity 59,129,640,982.23

No of Shares Outstanding 1,853,000,000.00

Growth

Rate 8.78%

(Yahoo Finance, 2018)

Dividend Discount Model

Dividend

expected $ 0.08

Growth rate 8.78%

Discount rate 9.41%

Intrisic Value 12

Share Price 6.55

Undervalued

On the basis of the above tables, dividend payment of the company has been

improved by 8.78% in last years, iit explains about better position of the company. Further, it

has been measured that the expected dividend in current year from the company is $ 0.08. the

discount rate of the business is 9.41% which has been calculated on the basis of the CAPM

model. It leads to the conclusion that the intrinsic value of the stock is $ 12 and the market

price of the stock is $ 6.55 (Harris et al, 2014).

On the basis of the study, it has been measured that the stock price of Qantas

airways limited is undervalued and if the investors would invest in the current position than

huge return could be got by the investors from the company.

The method is easier to calculate and understand, it offers better information about

dividend to stockholders. However, the dividend is not the only way through which the stock

value of the business could be recognized.

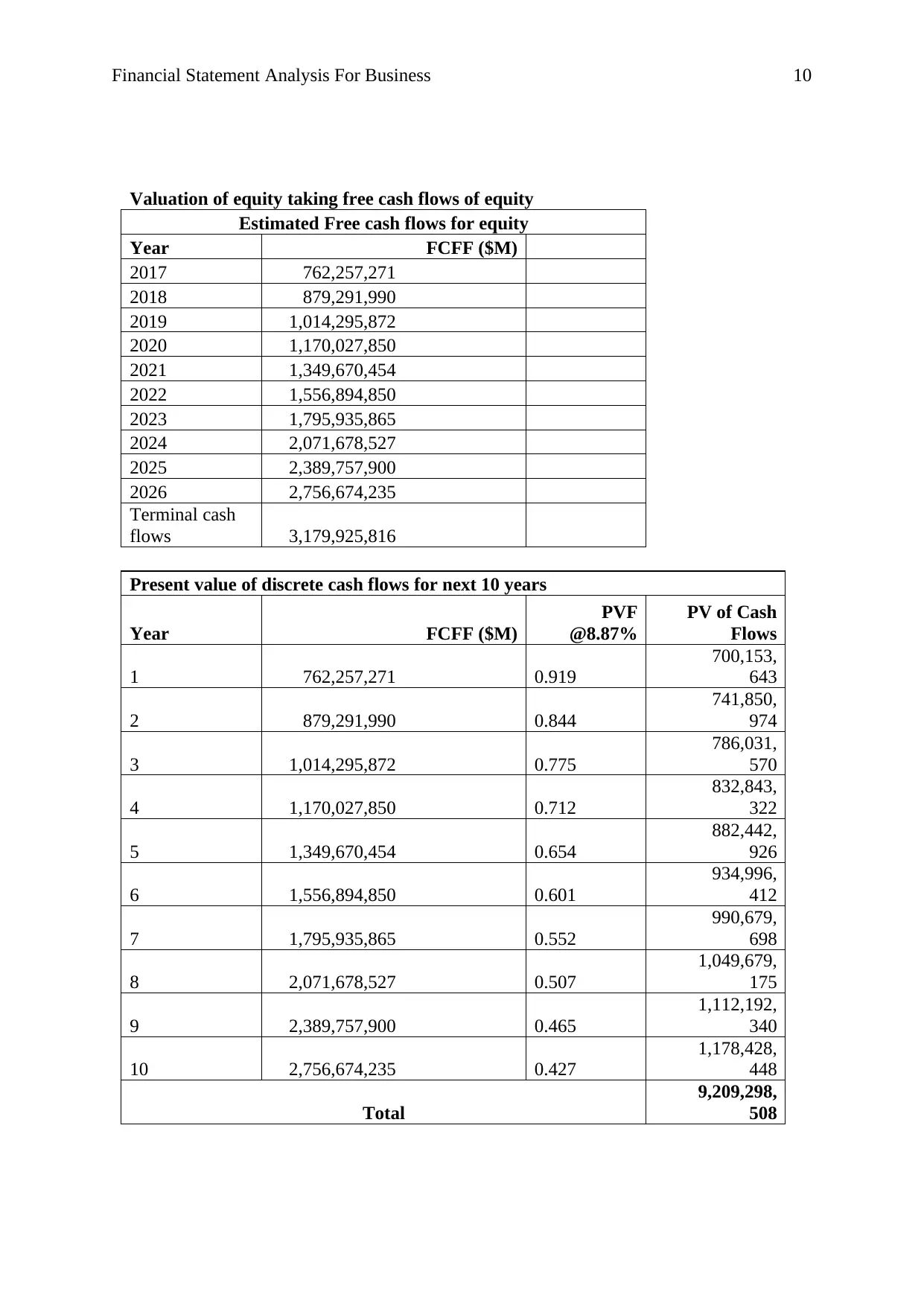

Discounted cash flow model:

It is a valuation model which is used by the business to estimate the investment

opportunity and attractiveness of the business. It evaluates the free cash flow projections,

discount rate, required annual rate etc to reach at the present value estimation to the company.

The discount cash flow model of the business is as follows:

Present value of terminal cash flows

Terminal cash flows 3,179,925,816 49,920,342,475

Total value of Equity 59,129,640,982.23

No of Shares Outstanding 1,853,000,000.00

Financial Statement Analysis For Business 6

Per share value of value of equity 31.91

(Morningstar, 2018)

The calculations of DCF model has been given in the appendix. According to the

above table, it has been found that the intrinsic value of the stock is $ 31.91 and the market

price of the stock is $ 6.55 (Gompers, Ishii and Metrick, 2003). On the basis of the study, it

has been measured that the stock price of Qantas airways limited is undervalued and if the

investors would invest in the current position than huge return could be got by the investors

from the company.

The method focuses on the various relevant factors which make the outcome more

relevant. However, it ignores few important factors of the business valuation such as changes

into the stock price etc.

SWOT analysis:

Further, SWOT analysis study has been done on Qantas airways limited which are as

follows:

Strength:

Strong brand image

Steady and consistent growth

Qantas transformation program

Superior services

Successful cost cutting

Weakness:

Low profits in international flights

Labour and union issues

Directorates

Opportunity:

Business travel

Low fuel prices

International destination to be grabbed

Strong demand in the market

Threat:

Competition

Management of cost

(Gompers, Kaplan and Mukharlyamov, 2016)

((Gompers, Kaplan and Mukharlyamov, 2016))

Per share value of value of equity 31.91

(Morningstar, 2018)

The calculations of DCF model has been given in the appendix. According to the

above table, it has been found that the intrinsic value of the stock is $ 31.91 and the market

price of the stock is $ 6.55 (Gompers, Ishii and Metrick, 2003). On the basis of the study, it

has been measured that the stock price of Qantas airways limited is undervalued and if the

investors would invest in the current position than huge return could be got by the investors

from the company.

The method focuses on the various relevant factors which make the outcome more

relevant. However, it ignores few important factors of the business valuation such as changes

into the stock price etc.

SWOT analysis:

Further, SWOT analysis study has been done on Qantas airways limited which are as

follows:

Strength:

Strong brand image

Steady and consistent growth

Qantas transformation program

Superior services

Successful cost cutting

Weakness:

Low profits in international flights

Labour and union issues

Directorates

Opportunity:

Business travel

Low fuel prices

International destination to be grabbed

Strong demand in the market

Threat:

Competition

Management of cost

(Gompers, Kaplan and Mukharlyamov, 2016)

((Gompers, Kaplan and Mukharlyamov, 2016))

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis For Business 7

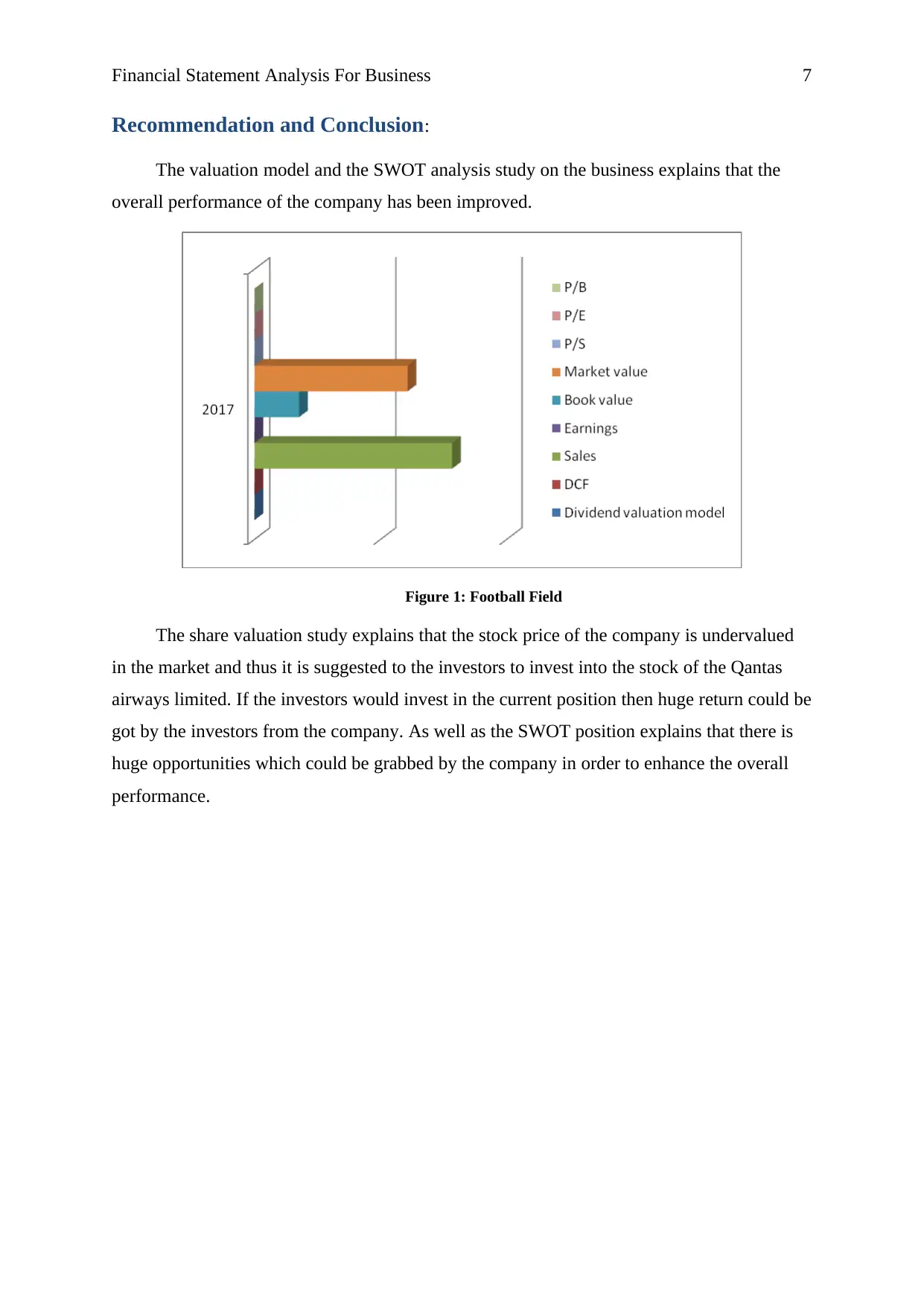

Recommendation and Conclusion:

The valuation model and the SWOT analysis study on the business explains that the

overall performance of the company has been improved.

Figure 1: Football Field

The share valuation study explains that the stock price of the company is undervalued

in the market and thus it is suggested to the investors to invest into the stock of the Qantas

airways limited. If the investors would invest in the current position then huge return could be

got by the investors from the company. As well as the SWOT position explains that there is

huge opportunities which could be grabbed by the company in order to enhance the overall

performance.

Recommendation and Conclusion:

The valuation model and the SWOT analysis study on the business explains that the

overall performance of the company has been improved.

Figure 1: Football Field

The share valuation study explains that the stock price of the company is undervalued

in the market and thus it is suggested to the investors to invest into the stock of the Qantas

airways limited. If the investors would invest in the current position then huge return could be

got by the investors from the company. As well as the SWOT position explains that there is

huge opportunities which could be grabbed by the company in order to enhance the overall

performance.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis For Business 8

References:

Gompers, P., Ishii, J. and Metrick, A., 2003. Corporate governance and equity prices. The

quarterly journal of economics, 118(1), pp.107-156.

Gompers, P., Kaplan, S.N. and Mukharlyamov, V., 2016. What do private equity firms say

they do?. Journal of Financial Economics, 121(3), pp.449-476.

Harris, R.S., Jenkinson, T. and Kaplan, S.N., 2014. Private equity performance: What do we

know?. The Journal of Finance, 69(5), pp.1851-1882.

Morningstar. 2018. Qantas airways limited. [online]. Accessed from:

http://financials.morningstar.com/income-statement/is.html?

t=QAN®ion=aus&culture=en-US&platform=sal (available 23/6/18).

Morningstar. 2018. Transurban. [online]. Accessed from:

http://financials.morningstar.com/income-statement/is.html?t=TCL®ion=aus&culture=en-

US (available 23/6/18).

Morningstar. 2018. Virgin Australia holdings limited. [online]. Accessed from:

http://financials.morningstar.com/income-statement/is.html?

t=VAH®ion=aus&culture=en-US&platform=sal (available 23/6/18).

Yahoo finance. 2018. Qantas airways limited. [online]. Accessed from:

https://in.finance.yahoo.com/quote/QAN.AX/history?

period1=1339957800&period2=1529692200&interval=div

%7Csplit&filter=div&frequency=1d (available 23/6/18).

References:

Gompers, P., Ishii, J. and Metrick, A., 2003. Corporate governance and equity prices. The

quarterly journal of economics, 118(1), pp.107-156.

Gompers, P., Kaplan, S.N. and Mukharlyamov, V., 2016. What do private equity firms say

they do?. Journal of Financial Economics, 121(3), pp.449-476.

Harris, R.S., Jenkinson, T. and Kaplan, S.N., 2014. Private equity performance: What do we

know?. The Journal of Finance, 69(5), pp.1851-1882.

Morningstar. 2018. Qantas airways limited. [online]. Accessed from:

http://financials.morningstar.com/income-statement/is.html?

t=QAN®ion=aus&culture=en-US&platform=sal (available 23/6/18).

Morningstar. 2018. Transurban. [online]. Accessed from:

http://financials.morningstar.com/income-statement/is.html?t=TCL®ion=aus&culture=en-

US (available 23/6/18).

Morningstar. 2018. Virgin Australia holdings limited. [online]. Accessed from:

http://financials.morningstar.com/income-statement/is.html?

t=VAH®ion=aus&culture=en-US&platform=sal (available 23/6/18).

Yahoo finance. 2018. Qantas airways limited. [online]. Accessed from:

https://in.finance.yahoo.com/quote/QAN.AX/history?

period1=1339957800&period2=1529692200&interval=div

%7Csplit&filter=div&frequency=1d (available 23/6/18).

Financial Statement Analysis For Business 9

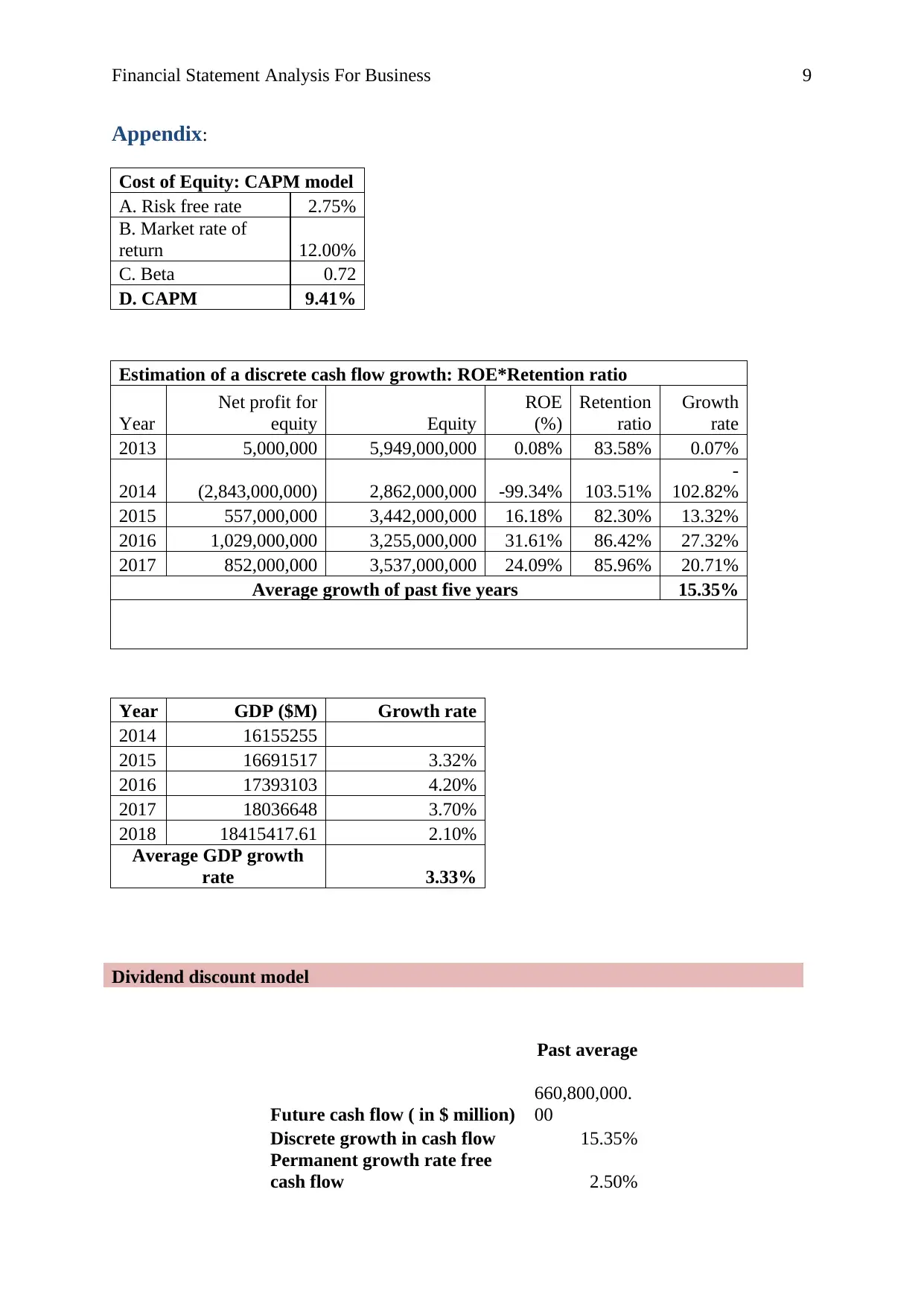

Appendix:

Cost of Equity: CAPM model

A. Risk free rate 2.75%

B. Market rate of

return 12.00%

C. Beta 0.72

D. CAPM 9.41%

Estimation of a discrete cash flow growth: ROE*Retention ratio

Year

Net profit for

equity Equity

ROE

(%)

Retention

ratio

Growth

rate

2013 5,000,000 5,949,000,000 0.08% 83.58% 0.07%

2014 (2,843,000,000) 2,862,000,000 -99.34% 103.51%

-

102.82%

2015 557,000,000 3,442,000,000 16.18% 82.30% 13.32%

2016 1,029,000,000 3,255,000,000 31.61% 86.42% 27.32%

2017 852,000,000 3,537,000,000 24.09% 85.96% 20.71%

Average growth of past five years 15.35%

Year GDP ($M) Growth rate

2014 16155255

2015 16691517 3.32%

2016 17393103 4.20%

2017 18036648 3.70%

2018 18415417.61 2.10%

Average GDP growth

rate 3.33%

Dividend discount model

Past average

Future cash flow ( in $ million)

660,800,000.

00

Discrete growth in cash flow 15.35%

Permanent growth rate free

cash flow 2.50%

Appendix:

Cost of Equity: CAPM model

A. Risk free rate 2.75%

B. Market rate of

return 12.00%

C. Beta 0.72

D. CAPM 9.41%

Estimation of a discrete cash flow growth: ROE*Retention ratio

Year

Net profit for

equity Equity

ROE

(%)

Retention

ratio

Growth

rate

2013 5,000,000 5,949,000,000 0.08% 83.58% 0.07%

2014 (2,843,000,000) 2,862,000,000 -99.34% 103.51%

-

102.82%

2015 557,000,000 3,442,000,000 16.18% 82.30% 13.32%

2016 1,029,000,000 3,255,000,000 31.61% 86.42% 27.32%

2017 852,000,000 3,537,000,000 24.09% 85.96% 20.71%

Average growth of past five years 15.35%

Year GDP ($M) Growth rate

2014 16155255

2015 16691517 3.32%

2016 17393103 4.20%

2017 18036648 3.70%

2018 18415417.61 2.10%

Average GDP growth

rate 3.33%

Dividend discount model

Past average

Future cash flow ( in $ million)

660,800,000.

00

Discrete growth in cash flow 15.35%

Permanent growth rate free

cash flow 2.50%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Statement Analysis For Business 10

Valuation of equity taking free cash flows of equity

Estimated Free cash flows for equity

Year FCFF ($M)

2017 762,257,271

2018 879,291,990

2019 1,014,295,872

2020 1,170,027,850

2021 1,349,670,454

2022 1,556,894,850

2023 1,795,935,865

2024 2,071,678,527

2025 2,389,757,900

2026 2,756,674,235

Terminal cash

flows 3,179,925,816

Present value of discrete cash flows for next 10 years

Year FCFF ($M)

PVF

@8.87%

PV of Cash

Flows

1 762,257,271 0.919

700,153,

643

2 879,291,990 0.844

741,850,

974

3 1,014,295,872 0.775

786,031,

570

4 1,170,027,850 0.712

832,843,

322

5 1,349,670,454 0.654

882,442,

926

6 1,556,894,850 0.601

934,996,

412

7 1,795,935,865 0.552

990,679,

698

8 2,071,678,527 0.507

1,049,679,

175

9 2,389,757,900 0.465

1,112,192,

340

10 2,756,674,235 0.427

1,178,428,

448

Total

9,209,298,

508

Valuation of equity taking free cash flows of equity

Estimated Free cash flows for equity

Year FCFF ($M)

2017 762,257,271

2018 879,291,990

2019 1,014,295,872

2020 1,170,027,850

2021 1,349,670,454

2022 1,556,894,850

2023 1,795,935,865

2024 2,071,678,527

2025 2,389,757,900

2026 2,756,674,235

Terminal cash

flows 3,179,925,816

Present value of discrete cash flows for next 10 years

Year FCFF ($M)

PVF

@8.87%

PV of Cash

Flows

1 762,257,271 0.919

700,153,

643

2 879,291,990 0.844

741,850,

974

3 1,014,295,872 0.775

786,031,

570

4 1,170,027,850 0.712

832,843,

322

5 1,349,670,454 0.654

882,442,

926

6 1,556,894,850 0.601

934,996,

412

7 1,795,935,865 0.552

990,679,

698

8 2,071,678,527 0.507

1,049,679,

175

9 2,389,757,900 0.465

1,112,192,

340

10 2,756,674,235 0.427

1,178,428,

448

Total

9,209,298,

508

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Statement Analysis For Business 11

Present value of terminal cash flows

Terminal cash

flows 3,179,925,816 49,920,342,475

Total value of Equity

59,129,640,982.

23

No of Shares Outstanding

1,853,000,000.0

0

Per share value of value of equity 31.91

Present value of terminal cash flows

Terminal cash

flows 3,179,925,816 49,920,342,475

Total value of Equity

59,129,640,982.

23

No of Shares Outstanding

1,853,000,000.0

0

Per share value of value of equity 31.91

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.