Comprehensive Review of Qantas Airlines' 2016 Annual Report

VerifiedAdded on 2020/03/07

|7

|1625

|37

Report

AI Summary

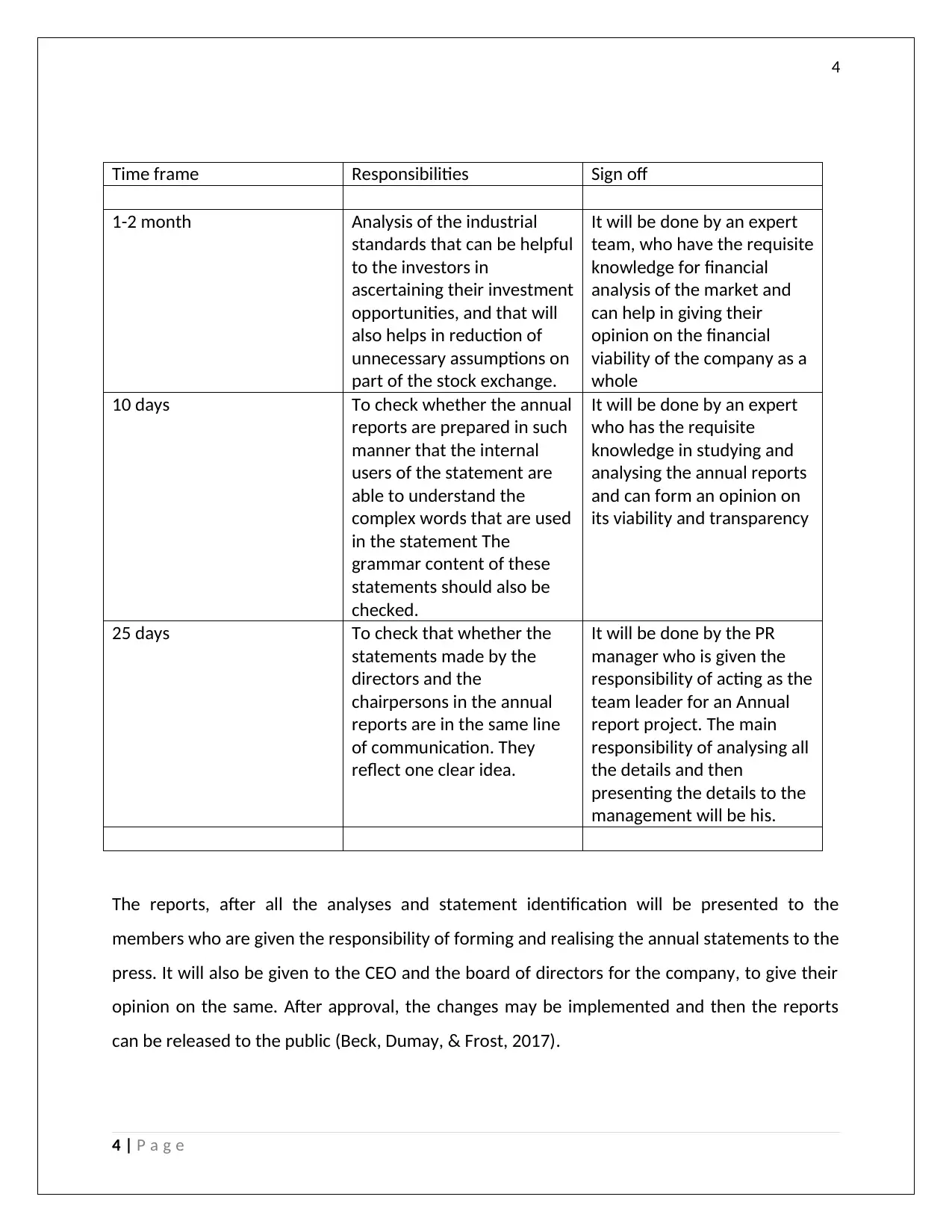

This report offers a comprehensive review of the Qantas Airlines 2016 annual report, adhering to Australian Accounting Standards and Corporations Regulation, 2001. It analyzes the company's financial statements, highlighting the importance of proper disclosure of management assumptions. The report identifies shortcomings in the presentation of the annual report, such as accounting delays and the need for clear communication, especially for non-accountants. It discusses the roles of various team members, including investors, stakeholders, and finance department employees, in reviewing the annual report. The report outlines internal and external briefs, emphasizing the needs of employees and stakeholders. It also includes a timeline with responsibilities for analyzing industry standards, ensuring clarity in the reports, and aligning communications from directors and chairpersons. The report addresses scenarios involving non-compliance with word limits and the inclusion of potentially negative information, emphasizing the importance of presenting a correct view of the company's accounts. It also touches on the importance of avoiding last-minute changes and using an affirmative tone in comparison reports.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.