Comprehensive Auditing and Ethics Report: Qantas Airways Limited

VerifiedAdded on 2022/09/16

|12

|2851

|16

Report

AI Summary

This report provides a comprehensive analysis of the auditing and ethical considerations for Qantas Airways Limited. It begins by examining the determination of materiality levels, crucial for identifying and assessing material misstatements in financial statements, and explains the three key steps involved: selecting a benchmark, determining a percentage, and providing justification. The report then delves into the review of draft notes, highlighting significant audit areas such as contingent liabilities and the adoption of new accounting standards. Preliminary analytical procedures are performed using financial ratios, including profitability, liquidity, and debt ratios, to identify potential audit risks. The report further reviews the cash flow statement, focusing on cash inflows and outflows from operating, investing, and financing activities, and assesses the company's going concern risk. Finally, it reviews the audit report, including the unqualified opinion issued by KPMG and the key audit matters addressed. The report integrates the concepts of materiality and risk, linking them to the audit procedures. The report is a valuable resource for understanding the complexities of auditing in the context of a major airline company.

Running head: AUDITING AND ETHIC

Auditing and Ethic

Name of the Student

Name of the University

Author’s Note

Auditing and Ethic

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ETHIC

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Materiality Level Determination............................................................................................2

Reviewing Draft Notes...........................................................................................................4

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................7

Cash Flow Statement Review................................................................................................7

Audit Report Review..............................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Section 1.....................................................................................................................................2

Materiality Level Determination............................................................................................2

Reviewing Draft Notes...........................................................................................................4

Section 2.....................................................................................................................................5

Section 3.....................................................................................................................................7

Cash Flow Statement Review................................................................................................7

Audit Report Review..............................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

2AUDITING AND ETHIC

Introduction

Auditing profession involves in the systematic as well as independent review of the

financial statements of the clients in order to make sure they are free from material

misstatements and appropriate audit standards have been used in order to prepare and present

them (William Jr, Glover & Prawitt, 2016). The auditors are responsible for taking into

account different factors in the auditing process. Determination of materiality level is a major

factors that is needed for the determination of material misstatements. Moreover, it is the

responsibility of the auditors to ensure the application of relevant analytical procedures in

order to test different component of financial statements so that the areas of higher audit risk

can be identified. The outcome of the whole audit program helps the auditors in expressing

the appropriate audit opinion. The main aim of this report is the analysis of different audit

related aspects of Qantas Airways Limited like the determination of materiality, audit risks

from financial ratios and others.

Section 1

Materiality Level Determination

Materiality is an important aspect in auditing which is considered as a fundamental

concept of auditing. The auditors apply the concept of materiality in the audit planning stage

and when they undertake the evaluation of the impact of assessed material mistsement on the

financial statements of the client. The same is applicable for the audit of Qantas Airways

Limited (Qantas). It needs to be mentioned that there are three steps that need to be followed

by the auditors while determining the level of materiality of Qantas for the financial year of

2018. These three steps are as follows:

1. Selection of the suitable and relevant benchmark;

Introduction

Auditing profession involves in the systematic as well as independent review of the

financial statements of the clients in order to make sure they are free from material

misstatements and appropriate audit standards have been used in order to prepare and present

them (William Jr, Glover & Prawitt, 2016). The auditors are responsible for taking into

account different factors in the auditing process. Determination of materiality level is a major

factors that is needed for the determination of material misstatements. Moreover, it is the

responsibility of the auditors to ensure the application of relevant analytical procedures in

order to test different component of financial statements so that the areas of higher audit risk

can be identified. The outcome of the whole audit program helps the auditors in expressing

the appropriate audit opinion. The main aim of this report is the analysis of different audit

related aspects of Qantas Airways Limited like the determination of materiality, audit risks

from financial ratios and others.

Section 1

Materiality Level Determination

Materiality is an important aspect in auditing which is considered as a fundamental

concept of auditing. The auditors apply the concept of materiality in the audit planning stage

and when they undertake the evaluation of the impact of assessed material mistsement on the

financial statements of the client. The same is applicable for the audit of Qantas Airways

Limited (Qantas). It needs to be mentioned that there are three steps that need to be followed

by the auditors while determining the level of materiality of Qantas for the financial year of

2018. These three steps are as follows:

1. Selection of the suitable and relevant benchmark;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ETHIC

2. Determination of a certain level which is the percentage of the above selected

benchmark; and,

3. Give necessary justification or rationale of the choice.

The following discussion shows the determination of the materiality level of Qantas for

2018 based on the above three steps.

1. In this step, the auditor of Qantas is needed to take into account certain factors for the

selection of benchmark; and these are the nature of the entity and the nature of the

industry in which the entity operates. The mostly used benchmarks are total income,

total expenses, profit before tax, net assets and gross profit. In case of Qantas, profit

before tax is choses as the benchmark because most of the companies in the airline

industry use this benchmark for materiality determination and this is helpful in

comparing the material level of Qantas with its competitors (Eilifsen & Messier Jr,

2014).

2. This step involves in the determination of percentage and this is majorly dependent on

the judgments of the auditors of the companies. In this stage, it is needed for the

auditors to consider the materiality guidelines of AASB 1031. As per AASB 1031, the

auditor of Qantas have two options. First, he/she can select an amount that is equal to

or greater than 10% of the above-mentioned base that is presumed to be material.

Second, the auditor can chose an amount that is equal to or less than 5% of the above-

mentioned base that is considered as material (aasb.gov.au, 2019). From the above, it

depends on the judgment of the auditor to select among 5% to 10%. In case of Qantas,

the auditor needs to consider 5% of the benchmark (Mio, 2013).

Therefore, based on the above discussion, the materiality of Qantas can be determined in

the following manner:

2. Determination of a certain level which is the percentage of the above selected

benchmark; and,

3. Give necessary justification or rationale of the choice.

The following discussion shows the determination of the materiality level of Qantas for

2018 based on the above three steps.

1. In this step, the auditor of Qantas is needed to take into account certain factors for the

selection of benchmark; and these are the nature of the entity and the nature of the

industry in which the entity operates. The mostly used benchmarks are total income,

total expenses, profit before tax, net assets and gross profit. In case of Qantas, profit

before tax is choses as the benchmark because most of the companies in the airline

industry use this benchmark for materiality determination and this is helpful in

comparing the material level of Qantas with its competitors (Eilifsen & Messier Jr,

2014).

2. This step involves in the determination of percentage and this is majorly dependent on

the judgments of the auditors of the companies. In this stage, it is needed for the

auditors to consider the materiality guidelines of AASB 1031. As per AASB 1031, the

auditor of Qantas have two options. First, he/she can select an amount that is equal to

or greater than 10% of the above-mentioned base that is presumed to be material.

Second, the auditor can chose an amount that is equal to or less than 5% of the above-

mentioned base that is considered as material (aasb.gov.au, 2019). From the above, it

depends on the judgment of the auditor to select among 5% to 10%. In case of Qantas,

the auditor needs to consider 5% of the benchmark (Mio, 2013).

Therefore, based on the above discussion, the materiality of Qantas can be determined in

the following manner:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ETHIC

Overall Materiality = 5% of Profit before Income Tax

= 5% of $1573 million

= $78.65 million

Reviewing Draft Notes

The following discussion shows the draft notes that are crucial for the audit of Qantas:

Areas Significant to the Audit Audit Procedures

Qantas has mentioned about its contingent

liabilities under Note: 17 of the 2018 Annual

Report. As per this section, Qantas has

contingent liabilities due to guarantee in the

normal cause of business for securing a self-

insurance licence, financing agreements for

the acquisition of aircraft and due to its

claims and litigation from normal cause of

business (investor.qantas.com, 2019). In case

these contingent liabilities become due, they

can affect the whole audit planning process

of the company.

The required audit procedures are to read to

the written information to determine the

impact of these contingent liabilities. After

that, it is need to examine the related

documents of these contingent liabilities for

determining the facts about these incidents

(Byrnes et al., 2018).

Qantas has provided the details of the new

accounting standards and interpretations that

it has not yet adopted; and these include

AASB 9 (2014) Financial Instruments,

AASB 15 Revenue from Contract with

Customers and AASB 16 Leases

The required audit procedure is to calculate

the impact of these new accounting standards

on the financial statements of Qantas (Byrnes

et al., 2018).

Overall Materiality = 5% of Profit before Income Tax

= 5% of $1573 million

= $78.65 million

Reviewing Draft Notes

The following discussion shows the draft notes that are crucial for the audit of Qantas:

Areas Significant to the Audit Audit Procedures

Qantas has mentioned about its contingent

liabilities under Note: 17 of the 2018 Annual

Report. As per this section, Qantas has

contingent liabilities due to guarantee in the

normal cause of business for securing a self-

insurance licence, financing agreements for

the acquisition of aircraft and due to its

claims and litigation from normal cause of

business (investor.qantas.com, 2019). In case

these contingent liabilities become due, they

can affect the whole audit planning process

of the company.

The required audit procedures are to read to

the written information to determine the

impact of these contingent liabilities. After

that, it is need to examine the related

documents of these contingent liabilities for

determining the facts about these incidents

(Byrnes et al., 2018).

Qantas has provided the details of the new

accounting standards and interpretations that

it has not yet adopted; and these include

AASB 9 (2014) Financial Instruments,

AASB 15 Revenue from Contract with

Customers and AASB 16 Leases

The required audit procedure is to calculate

the impact of these new accounting standards

on the financial statements of Qantas (Byrnes

et al., 2018).

5AUDITING AND ETHIC

(investor.qantas.com, 2019). The outcome of

the financial statements of Qantas can be

affected due to the adoption of these new

standards which can have negative impact on

the audit process.

Section 2

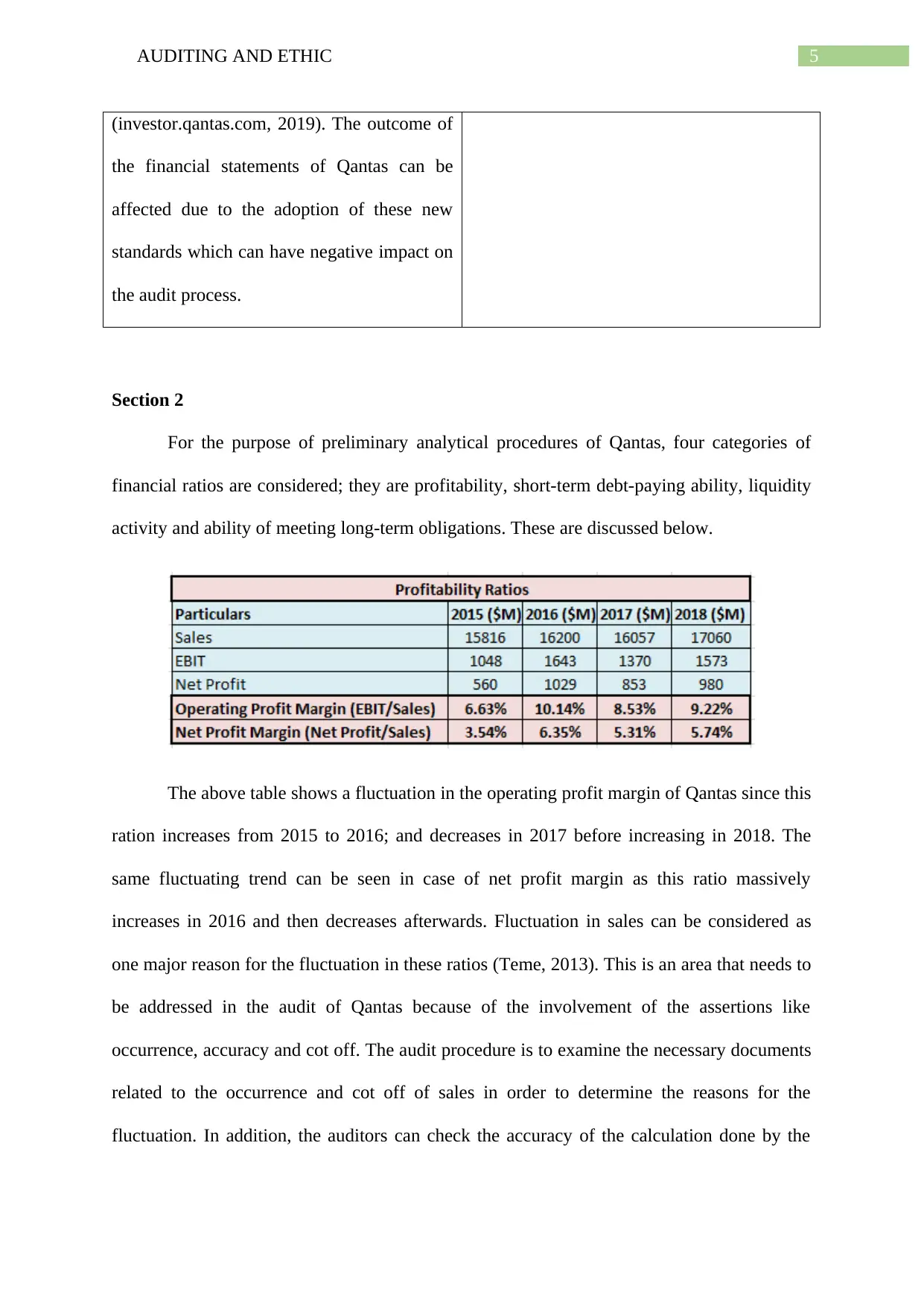

For the purpose of preliminary analytical procedures of Qantas, four categories of

financial ratios are considered; they are profitability, short-term debt-paying ability, liquidity

activity and ability of meeting long-term obligations. These are discussed below.

The above table shows a fluctuation in the operating profit margin of Qantas since this

ration increases from 2015 to 2016; and decreases in 2017 before increasing in 2018. The

same fluctuating trend can be seen in case of net profit margin as this ratio massively

increases in 2016 and then decreases afterwards. Fluctuation in sales can be considered as

one major reason for the fluctuation in these ratios (Teme, 2013). This is an area that needs to

be addressed in the audit of Qantas because of the involvement of the assertions like

occurrence, accuracy and cot off. The audit procedure is to examine the necessary documents

related to the occurrence and cot off of sales in order to determine the reasons for the

fluctuation. In addition, the auditors can check the accuracy of the calculation done by the

(investor.qantas.com, 2019). The outcome of

the financial statements of Qantas can be

affected due to the adoption of these new

standards which can have negative impact on

the audit process.

Section 2

For the purpose of preliminary analytical procedures of Qantas, four categories of

financial ratios are considered; they are profitability, short-term debt-paying ability, liquidity

activity and ability of meeting long-term obligations. These are discussed below.

The above table shows a fluctuation in the operating profit margin of Qantas since this

ration increases from 2015 to 2016; and decreases in 2017 before increasing in 2018. The

same fluctuating trend can be seen in case of net profit margin as this ratio massively

increases in 2016 and then decreases afterwards. Fluctuation in sales can be considered as

one major reason for the fluctuation in these ratios (Teme, 2013). This is an area that needs to

be addressed in the audit of Qantas because of the involvement of the assertions like

occurrence, accuracy and cot off. The audit procedure is to examine the necessary documents

related to the occurrence and cot off of sales in order to determine the reasons for the

fluctuation. In addition, the auditors can check the accuracy of the calculation done by the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ETHIC

management for determining the calculation of net profit and operating profit of Qantas (Jans,

Alles & Vasarhelyi, 2014).

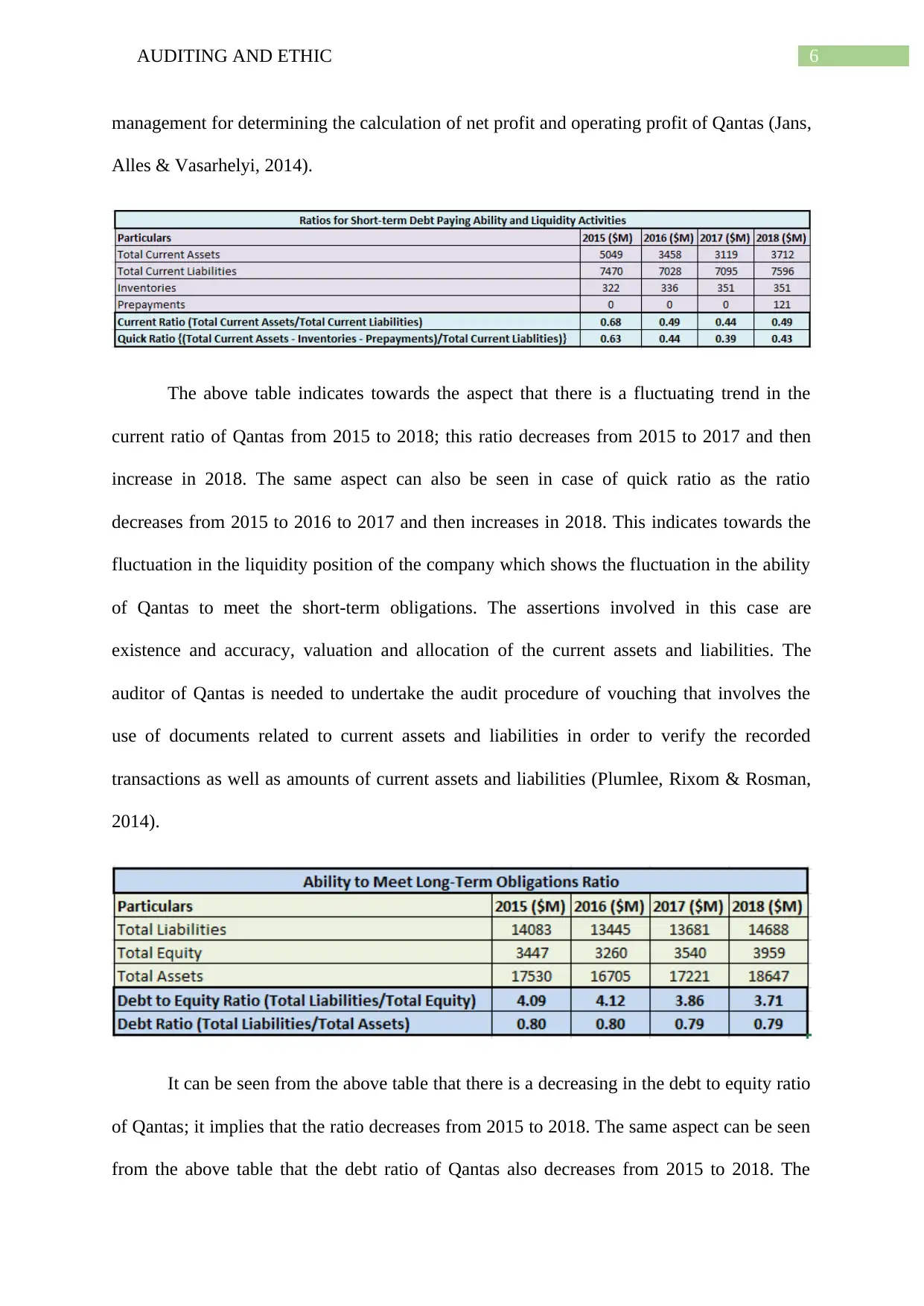

The above table indicates towards the aspect that there is a fluctuating trend in the

current ratio of Qantas from 2015 to 2018; this ratio decreases from 2015 to 2017 and then

increase in 2018. The same aspect can also be seen in case of quick ratio as the ratio

decreases from 2015 to 2016 to 2017 and then increases in 2018. This indicates towards the

fluctuation in the liquidity position of the company which shows the fluctuation in the ability

of Qantas to meet the short-term obligations. The assertions involved in this case are

existence and accuracy, valuation and allocation of the current assets and liabilities. The

auditor of Qantas is needed to undertake the audit procedure of vouching that involves the

use of documents related to current assets and liabilities in order to verify the recorded

transactions as well as amounts of current assets and liabilities (Plumlee, Rixom & Rosman,

2014).

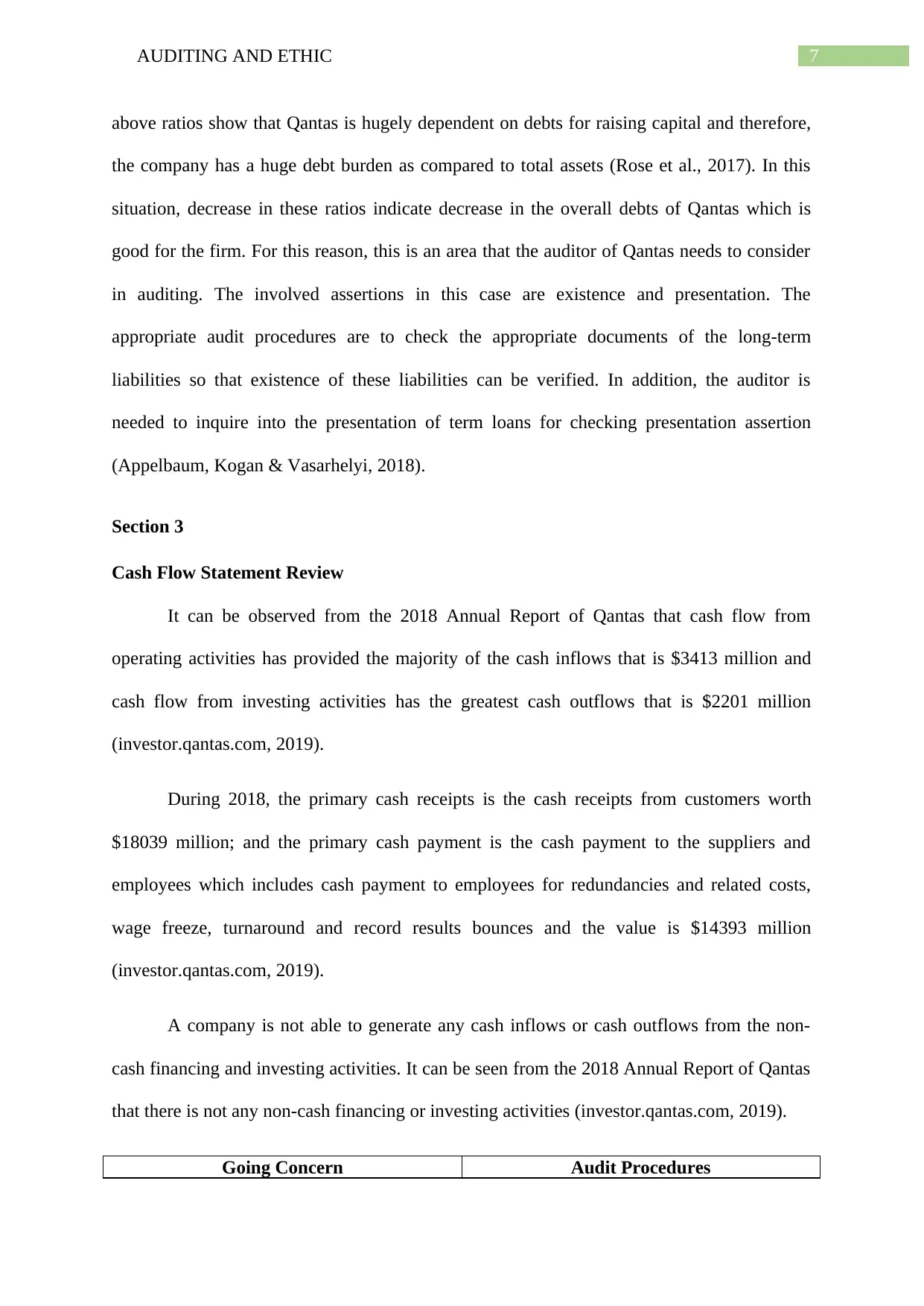

It can be seen from the above table that there is a decreasing in the debt to equity ratio

of Qantas; it implies that the ratio decreases from 2015 to 2018. The same aspect can be seen

from the above table that the debt ratio of Qantas also decreases from 2015 to 2018. The

management for determining the calculation of net profit and operating profit of Qantas (Jans,

Alles & Vasarhelyi, 2014).

The above table indicates towards the aspect that there is a fluctuating trend in the

current ratio of Qantas from 2015 to 2018; this ratio decreases from 2015 to 2017 and then

increase in 2018. The same aspect can also be seen in case of quick ratio as the ratio

decreases from 2015 to 2016 to 2017 and then increases in 2018. This indicates towards the

fluctuation in the liquidity position of the company which shows the fluctuation in the ability

of Qantas to meet the short-term obligations. The assertions involved in this case are

existence and accuracy, valuation and allocation of the current assets and liabilities. The

auditor of Qantas is needed to undertake the audit procedure of vouching that involves the

use of documents related to current assets and liabilities in order to verify the recorded

transactions as well as amounts of current assets and liabilities (Plumlee, Rixom & Rosman,

2014).

It can be seen from the above table that there is a decreasing in the debt to equity ratio

of Qantas; it implies that the ratio decreases from 2015 to 2018. The same aspect can be seen

from the above table that the debt ratio of Qantas also decreases from 2015 to 2018. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ETHIC

above ratios show that Qantas is hugely dependent on debts for raising capital and therefore,

the company has a huge debt burden as compared to total assets (Rose et al., 2017). In this

situation, decrease in these ratios indicate decrease in the overall debts of Qantas which is

good for the firm. For this reason, this is an area that the auditor of Qantas needs to consider

in auditing. The involved assertions in this case are existence and presentation. The

appropriate audit procedures are to check the appropriate documents of the long-term

liabilities so that existence of these liabilities can be verified. In addition, the auditor is

needed to inquire into the presentation of term loans for checking presentation assertion

(Appelbaum, Kogan & Vasarhelyi, 2018).

Section 3

Cash Flow Statement Review

It can be observed from the 2018 Annual Report of Qantas that cash flow from

operating activities has provided the majority of the cash inflows that is $3413 million and

cash flow from investing activities has the greatest cash outflows that is $2201 million

(investor.qantas.com, 2019).

During 2018, the primary cash receipts is the cash receipts from customers worth

$18039 million; and the primary cash payment is the cash payment to the suppliers and

employees which includes cash payment to employees for redundancies and related costs,

wage freeze, turnaround and record results bounces and the value is $14393 million

(investor.qantas.com, 2019).

A company is not able to generate any cash inflows or cash outflows from the non-

cash financing and investing activities. It can be seen from the 2018 Annual Report of Qantas

that there is not any non-cash financing or investing activities (investor.qantas.com, 2019).

Going Concern Audit Procedures

above ratios show that Qantas is hugely dependent on debts for raising capital and therefore,

the company has a huge debt burden as compared to total assets (Rose et al., 2017). In this

situation, decrease in these ratios indicate decrease in the overall debts of Qantas which is

good for the firm. For this reason, this is an area that the auditor of Qantas needs to consider

in auditing. The involved assertions in this case are existence and presentation. The

appropriate audit procedures are to check the appropriate documents of the long-term

liabilities so that existence of these liabilities can be verified. In addition, the auditor is

needed to inquire into the presentation of term loans for checking presentation assertion

(Appelbaum, Kogan & Vasarhelyi, 2018).

Section 3

Cash Flow Statement Review

It can be observed from the 2018 Annual Report of Qantas that cash flow from

operating activities has provided the majority of the cash inflows that is $3413 million and

cash flow from investing activities has the greatest cash outflows that is $2201 million

(investor.qantas.com, 2019).

During 2018, the primary cash receipts is the cash receipts from customers worth

$18039 million; and the primary cash payment is the cash payment to the suppliers and

employees which includes cash payment to employees for redundancies and related costs,

wage freeze, turnaround and record results bounces and the value is $14393 million

(investor.qantas.com, 2019).

A company is not able to generate any cash inflows or cash outflows from the non-

cash financing and investing activities. It can be seen from the 2018 Annual Report of Qantas

that there is not any non-cash financing or investing activities (investor.qantas.com, 2019).

Going Concern Audit Procedures

8AUDITING AND ETHIC

It can be observed from the above that Qantas has

been able in generating healthy cash inflows from

operating activities which indicates towards the

strengths of the core business operations of

Qantas. Negative cash flow from investing

activities indicates that Qantas is investing in

future operation through purchase of property,

plant and equipment and others (Amin, Krishnan

& Yang, 2014). Lastly, negative cash flows from

investing activities indicate that Qantas is serving

borrowings and making dividend payments. All

thee indicates that the going concern risk of

Qantas is low.

In order to address going concern risk, the auditor

of Qantas is needed to obtain sufficient evidence

regarding the appropriateness of management’s

use of going concern basis. After that, on the

basis of the audit evidence, the auditor is needed

to assess whether there is existence of any

material uncertainty that cast significant doubt

about the entity’s ability to continue as a going

concern (Geiger, Raghunandan & Riccardi,

2013).

Audit Report Review

It can be seen from the 2018 Annual Report of Qantas that the audit partner of the

company, KPMG, has expressed unqualified audit opinion by mentioning the fact that Qantas

has complied with Corporations Act 2001 and Australian Accounting Standards that gives the

true and fair view of the company’s financial performance and position (investor.qantas.com,

2019).

The section called “Key Audit Matters” in the auditor’s report discusses about three

issues that were most significant in the audit of the financial statements of Qantas. These

issues are mentioned below.

It can be observed from the above that Qantas has

been able in generating healthy cash inflows from

operating activities which indicates towards the

strengths of the core business operations of

Qantas. Negative cash flow from investing

activities indicates that Qantas is investing in

future operation through purchase of property,

plant and equipment and others (Amin, Krishnan

& Yang, 2014). Lastly, negative cash flows from

investing activities indicate that Qantas is serving

borrowings and making dividend payments. All

thee indicates that the going concern risk of

Qantas is low.

In order to address going concern risk, the auditor

of Qantas is needed to obtain sufficient evidence

regarding the appropriateness of management’s

use of going concern basis. After that, on the

basis of the audit evidence, the auditor is needed

to assess whether there is existence of any

material uncertainty that cast significant doubt

about the entity’s ability to continue as a going

concern (Geiger, Raghunandan & Riccardi,

2013).

Audit Report Review

It can be seen from the 2018 Annual Report of Qantas that the audit partner of the

company, KPMG, has expressed unqualified audit opinion by mentioning the fact that Qantas

has complied with Corporations Act 2001 and Australian Accounting Standards that gives the

true and fair view of the company’s financial performance and position (investor.qantas.com,

2019).

The section called “Key Audit Matters” in the auditor’s report discusses about three

issues that were most significant in the audit of the financial statements of Qantas. These

issues are mentioned below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ETHIC

Recognition of Passenger Revenue – KPMG has considered passenger revenue recognition

as a key audit matter because of its financial importance, high volume of low passenger ticket

and complexities in accounting processes. Adequate steps have been taken for addressing this

issue (investor.qantas.com, 2019).

Recognition of Frequent Flyer Revenue – KPMG has considered the recognition of

revenue from Frequent Flyer as a key audit matter due to the involvement of significant

judgments to estimate the deferred amount as Unredeemed Frequent Flyer revenue. The

auditors have taken adequate steps to address this issue (investor.qantas.com, 2019).

Accounting for Derivative Financial Instruments – The financial accounting related

accounting and valuation is a key audit matter to KPMG because of the presence of complex

inherent estimation of fair value, impact of accounting changes and others. The auditors have

taken adequate steps to address this issue (investor.qantas.com, 2019).

Conclusion

It can be seen from the above discussion that the auditors are required to earlier-

discussed three steps for the determination of materiality level of Qantas like benchmark

selection, appropriate percentage determination and materiality determination. The above

discussion also shows that the analysis of appropriate ratios is a crucial analytical process that

helps the auditors in the identification of the areas of risks in the financial statements that

need to consider in the audit process and this assists the auditors in taking appropriate audit

procedures to address the risk areas. The above discussion also shows the importance of cash

flows analysis for the determination of issues related to going concern of the companies. It is

needed for the auditors to express the audit opinion based on the outcome of the whole audit

operation.

Recognition of Passenger Revenue – KPMG has considered passenger revenue recognition

as a key audit matter because of its financial importance, high volume of low passenger ticket

and complexities in accounting processes. Adequate steps have been taken for addressing this

issue (investor.qantas.com, 2019).

Recognition of Frequent Flyer Revenue – KPMG has considered the recognition of

revenue from Frequent Flyer as a key audit matter due to the involvement of significant

judgments to estimate the deferred amount as Unredeemed Frequent Flyer revenue. The

auditors have taken adequate steps to address this issue (investor.qantas.com, 2019).

Accounting for Derivative Financial Instruments – The financial accounting related

accounting and valuation is a key audit matter to KPMG because of the presence of complex

inherent estimation of fair value, impact of accounting changes and others. The auditors have

taken adequate steps to address this issue (investor.qantas.com, 2019).

Conclusion

It can be seen from the above discussion that the auditors are required to earlier-

discussed three steps for the determination of materiality level of Qantas like benchmark

selection, appropriate percentage determination and materiality determination. The above

discussion also shows that the analysis of appropriate ratios is a crucial analytical process that

helps the auditors in the identification of the areas of risks in the financial statements that

need to consider in the audit process and this assists the auditors in taking appropriate audit

procedures to address the risk areas. The above discussion also shows the importance of cash

flows analysis for the determination of issues related to going concern of the companies. It is

needed for the auditors to express the audit opinion based on the outcome of the whole audit

operation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AUDITING AND ETHIC

References

Aasb.gov.au. (2019). Materiality. Retrieved 24 August 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_07-

04_COMPdec09_01-11.pdf

Amin, K., Krishnan, J., & Yang, J. S. (2014). Going concern opinion and cost of

equity. Auditing: A Journal of Practice & Theory, 33(4), 1-39.

Appelbaum, D. A., Kogan, A., & Vasarhelyi, M. A. (2018). Analytical procedures in external

auditing: A comprehensive literature survey and framework for external audit

analytics. Journal of Accounting Literature, 40, 83-101.

Byrnes, P. E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J. D., &

Vasarhelyi, M. (2018). Evolution of Auditing: From the Traditional Approach to the

Future Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297).

Emerald Publishing Limited.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Geiger, M. A., Raghunandan, K., & Riccardi, W. (2013). The global financial crisis: US

bankruptcies and going-concern audit opinions. Accounting Horizons, 28(1), 59-75.

Investor.qantas.com. (2019). QANTAS ANNUAL REPORT 2017. Retrieved 24 August 2019,

from

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1t

pgyw/file/annual-reports/2016AnnualReport.pdf

Investor.qantas.com. (2019). QANTAS ANNUAL REPORT 2017. Retrieved 24 August 2019,

from

References

Aasb.gov.au. (2019). Materiality. Retrieved 24 August 2019, from

https://www.aasb.gov.au/admin/file/content105/c9/AASB1031_07-

04_COMPdec09_01-11.pdf

Amin, K., Krishnan, J., & Yang, J. S. (2014). Going concern opinion and cost of

equity. Auditing: A Journal of Practice & Theory, 33(4), 1-39.

Appelbaum, D. A., Kogan, A., & Vasarhelyi, M. A. (2018). Analytical procedures in external

auditing: A comprehensive literature survey and framework for external audit

analytics. Journal of Accounting Literature, 40, 83-101.

Byrnes, P. E., Al-Awadhi, A., Gullvist, B., Brown-Liburd, H., Teeter, R., Warren Jr, J. D., &

Vasarhelyi, M. (2018). Evolution of Auditing: From the Traditional Approach to the

Future Audit 1. In Continuous Auditing: Theory and Application (pp. 285-297).

Emerald Publishing Limited.

Eilifsen, A., & Messier Jr, W. F. (2014). Materiality guidance of the major public accounting

firms. Auditing: A Journal of Practice & Theory, 34(2), 3-26.

Geiger, M. A., Raghunandan, K., & Riccardi, W. (2013). The global financial crisis: US

bankruptcies and going-concern audit opinions. Accounting Horizons, 28(1), 59-75.

Investor.qantas.com. (2019). QANTAS ANNUAL REPORT 2017. Retrieved 24 August 2019,

from

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1t

pgyw/file/annual-reports/2016AnnualReport.pdf

Investor.qantas.com. (2019). QANTAS ANNUAL REPORT 2017. Retrieved 24 August 2019,

from

11AUDITING AND ETHIC

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1t

pgyw/file/annual-reports/2017AnnualReport.pdf

Investor.qantas.com. (2019). Qantas Annual Report 2018. Retrieved 24 August 2019, from

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1t

pgyw/file/annual-reports/2018-Annual-Report-ASX.pdf

Jans, M., Alles, M. G., & Vasarhelyi, M. A. (2014). A field study on the use of process

mining of event logs as an analytical procedure in auditing. The Accounting

Review, 89(5), 1751-1773.

Mio, C. (2013). Materiality and assurance: building the link. In Integrated Reporting (pp. 79-

94). Springer, Cham.

Plumlee, R. D., Rixom, B. A., & Rosman, A. J. (2014). Training auditors to perform

analytical procedures using metacognitive skills. The Accounting Review, 90(1), 351-

369.

Rose, A. M., Rose, J. M., Sanderson, K. A., & Thibodeau, J. C. (2017). When should audit

firms introduce analyses of Big Data into the audit process?. Journal of Information

Systems, 31(3), 81-99.

TEME, E. (2013). Audit procedures for disclosure of errors and fraud in financial

statements. EKONOMSKE TE EKONOMSKE TEME, 51(2), 355-375.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1t

pgyw/file/annual-reports/2017AnnualReport.pdf

Investor.qantas.com. (2019). Qantas Annual Report 2018. Retrieved 24 August 2019, from

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1t

pgyw/file/annual-reports/2018-Annual-Report-ASX.pdf

Jans, M., Alles, M. G., & Vasarhelyi, M. A. (2014). A field study on the use of process

mining of event logs as an analytical procedure in auditing. The Accounting

Review, 89(5), 1751-1773.

Mio, C. (2013). Materiality and assurance: building the link. In Integrated Reporting (pp. 79-

94). Springer, Cham.

Plumlee, R. D., Rixom, B. A., & Rosman, A. J. (2014). Training auditors to perform

analytical procedures using metacognitive skills. The Accounting Review, 90(1), 351-

369.

Rose, A. M., Rose, J. M., Sanderson, K. A., & Thibodeau, J. C. (2017). When should audit

firms introduce analyses of Big Data into the audit process?. Journal of Information

Systems, 31(3), 81-99.

TEME, E. (2013). Audit procedures for disclosure of errors and fraud in financial

statements. EKONOMSKE TE EKONOMSKE TEME, 51(2), 355-375.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.