Qantas Case Study: Balanced Scorecard and Strategic Analysis

VerifiedAdded on 2023/06/05

|9

|2030

|272

Case Study

AI Summary

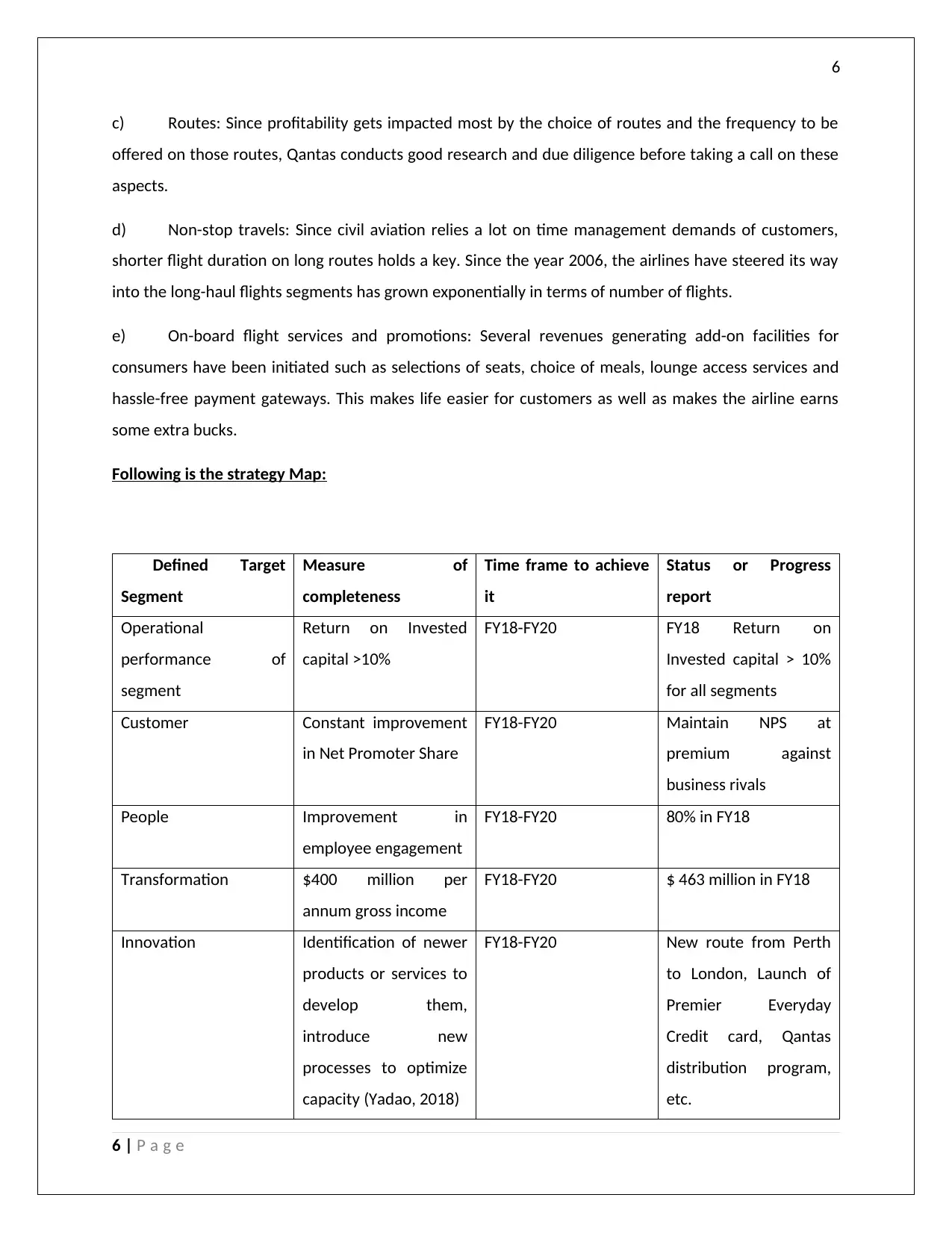

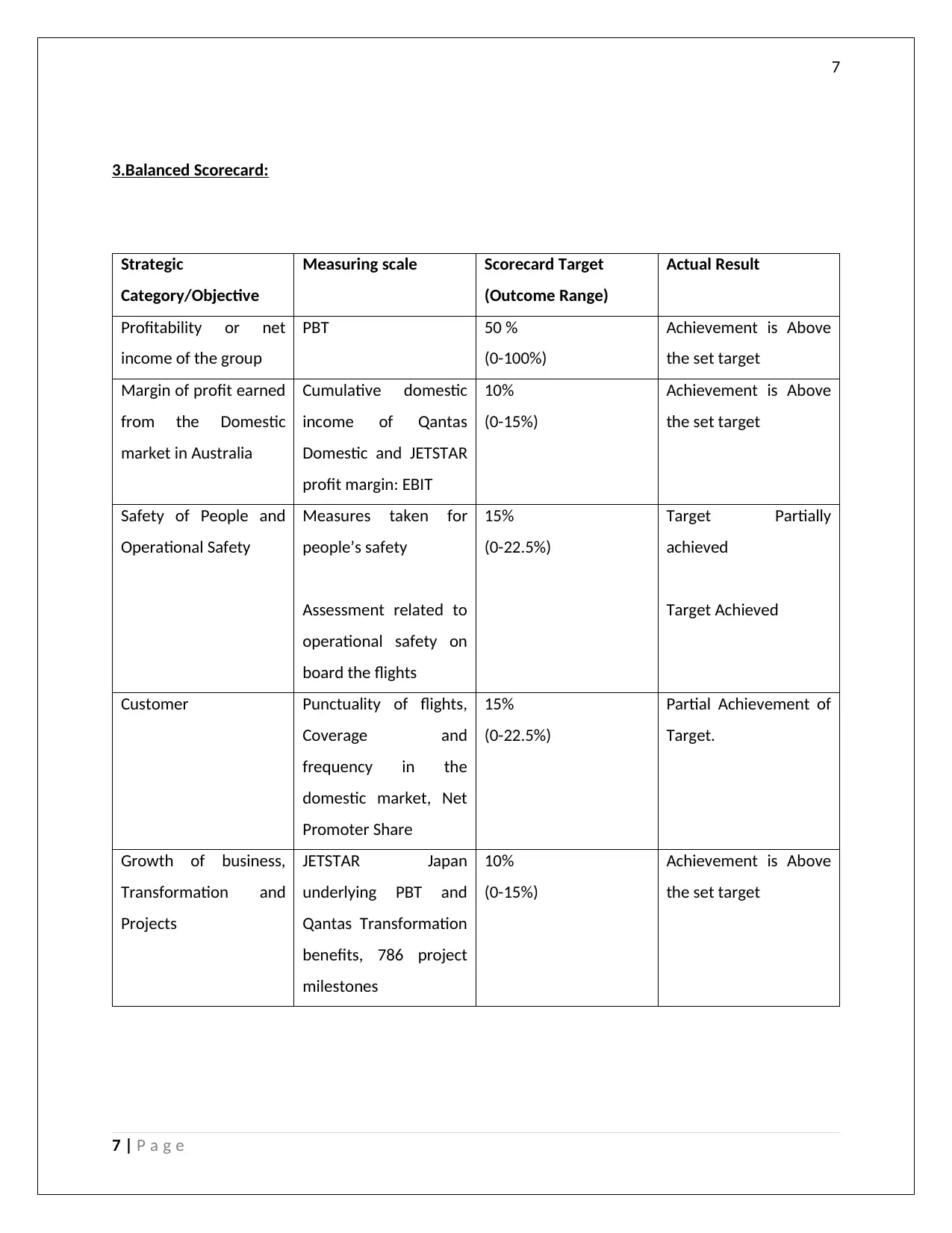

This assignment provides a comprehensive case study analysis of Qantas, focusing on its strategic performance through the lens of the Balanced Scorecard. Part A differentiates management accounting from financial accounting, highlighting the evolution of management accounting practices due to external and internal factors, including increased competition, globalization, technological advancements, and organizational restructuring. It further elaborates on the Balanced Scorecard approach, detailing its benefits such as aligning initiatives, enhancing performance reporting, improving information quality, enabling better strategic planning, and fostering organizational alignment and communication. Part B identifies critical success factors for Qantas, including management focus, workforce training, route selection, non-stop travel offerings, and on-board services. It presents a strategy map outlining targets, measures, and timeframes for operational performance, customer satisfaction, people development, transformation initiatives, and innovation. The assignment concludes with a balanced scorecard that assesses Qantas's performance across profitability, safety, customer satisfaction, and transformation projects, providing a detailed overview of the airline's strategic achievements and areas for improvement.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.