Analysis of Qantas Airways: HI5020 Corporate Accounting Report

VerifiedAdded on 2024/05/31

|10

|2789

|497

Report

AI Summary

This report provides a detailed analysis of Qantas Airways' financial statements, focusing on the cash flow statement, other comprehensive income statement, and accounting for corporate income tax. The cash flow analysis categorizes activities into operating, investing, and financing, highlighting the positive cash balance from operations and negative flows from investing and financing. The report identifies items in the other comprehensive income statement, explaining why these are not included in the regular income statement due to their unrealized nature. Furthermore, the analysis delves into Qantas Airways' corporate income tax, comparing the tax expense with the company tax rate, commenting on deferred tax assets and liabilities, and discussing the differences between income tax expense and income tax paid. The report concludes by reflecting on the complexities and insights gained from examining Qantas Airways' tax treatment, noting the differences between tax expense and cash flow statements due to timing and accounting method variations. Desklib offers a wealth of similar solved assignments and past papers for students.

HI5020 Corporate Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

CASH FLOWS STATEMENT.......................................................................................................4

(i) Various items of cash flow statement.....................................................................................4

(ii) Comparative analysis of various categories in cash flow......................................................4

OTHER COMPREHENSIVE INCOME STATEMENT................................................................5

(iii) Items in another comprehensive income statement..............................................................5

(iv) Understanding of items identified.........................................................................................6

(v) Reasons for not including them in income statements...........................................................6

ACCOUNTING FOR CORPORATE INCOME TAX...................................................................6

(vi) Tax expense in latest financial statements............................................................................6

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm...................................................................7

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded..................................................7

(ix)Is there any current tax assets or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?.....................................................7

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?................................................8

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?...............................................................................................................8

2

CASH FLOWS STATEMENT.......................................................................................................4

(i) Various items of cash flow statement.....................................................................................4

(ii) Comparative analysis of various categories in cash flow......................................................4

OTHER COMPREHENSIVE INCOME STATEMENT................................................................5

(iii) Items in another comprehensive income statement..............................................................5

(iv) Understanding of items identified.........................................................................................6

(v) Reasons for not including them in income statements...........................................................6

ACCOUNTING FOR CORPORATE INCOME TAX...................................................................6

(vi) Tax expense in latest financial statements............................................................................6

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm...................................................................7

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded..................................................7

(ix)Is there any current tax assets or income tax payable recorded by your company? Why is

the income tax payable not the same as income tax expense?.....................................................7

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?................................................8

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s tax

expense in its accounts?...............................................................................................................8

2

References......................................................................................................................................10

3

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CASH FLOWS STATEMENT

(i) Various items of cash flow statements

In the cash flow statements, there are various items which are recorded and they include

following:

The amount of the cash which is received from customers and this fluctuates as it varies

in accordance with the operations undertaken such as it was 17239 in 2015 and then

17320 in 2016 but then in 2017 declined to 16947 (Qantas Airways, 2016).

Cash which is paid to all the suppliers is also included and it is 14747, 14197 and 13982

in 2015, 2016 and 2017 respectively (Qantas Airways, 2017).

Cash payments made for the income tax and the other expenses such as interest and the

receipt of the interest and dividends. They change due to the change in the income and

the loans which are taken. Such as interest paid was 281 in 2015 and then 227 and 164 in

the following two years.

Payments which are made in respect of any fixed asset or the investments that are made

are also included and with that the proceeds which are received on the disposal of the

assets are also taken (Qantas Airways, 2017). They change as an equal investment is not

made every year and also there are no assets which need to be disposed of in every year.

All the payments that are made for the share buyback, capital return, repayment of loan

and dividend paid. The entire amount received from borrowings is also considered.

The opening and closing balance of the cash will also be represented in this by which it

will be reconciled.

(ii) Comparative analysis of various categories in cash flow

The cash flow of the company is divided into three broad categories which are investment,

operations and financing activities. In them, the transactions which are related to them will be

specified. An explanation of same is as follows:

Operating activities: This is the category in which the items that are related to the normal

operations of the business are included. In this, all the payments and receipts which are related to

4

(i) Various items of cash flow statements

In the cash flow statements, there are various items which are recorded and they include

following:

The amount of the cash which is received from customers and this fluctuates as it varies

in accordance with the operations undertaken such as it was 17239 in 2015 and then

17320 in 2016 but then in 2017 declined to 16947 (Qantas Airways, 2016).

Cash which is paid to all the suppliers is also included and it is 14747, 14197 and 13982

in 2015, 2016 and 2017 respectively (Qantas Airways, 2017).

Cash payments made for the income tax and the other expenses such as interest and the

receipt of the interest and dividends. They change due to the change in the income and

the loans which are taken. Such as interest paid was 281 in 2015 and then 227 and 164 in

the following two years.

Payments which are made in respect of any fixed asset or the investments that are made

are also included and with that the proceeds which are received on the disposal of the

assets are also taken (Qantas Airways, 2017). They change as an equal investment is not

made every year and also there are no assets which need to be disposed of in every year.

All the payments that are made for the share buyback, capital return, repayment of loan

and dividend paid. The entire amount received from borrowings is also considered.

The opening and closing balance of the cash will also be represented in this by which it

will be reconciled.

(ii) Comparative analysis of various categories in cash flow

The cash flow of the company is divided into three broad categories which are investment,

operations and financing activities. In them, the transactions which are related to them will be

specified. An explanation of same is as follows:

Operating activities: This is the category in which the items that are related to the normal

operations of the business are included. In this, all the payments and receipts which are related to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the business activities will be undertaken. This includes the rent, interest and other expenses

which are met by the company.

Investing activities: Under this the transactions by which investment is made by the company

are covered (Bhandari & Adams, 2017). Such as purchase or sale of the assets or making of other

investment. Also, the repayment of the net loan will also be included in this.

Financing activities: The matters which are related to the financial aspects such as issue and

redemption of shares and the payment of a dividend in respect of them. If there is any payment

or receipt which is made in respect of the borrowing than that will be included in this.

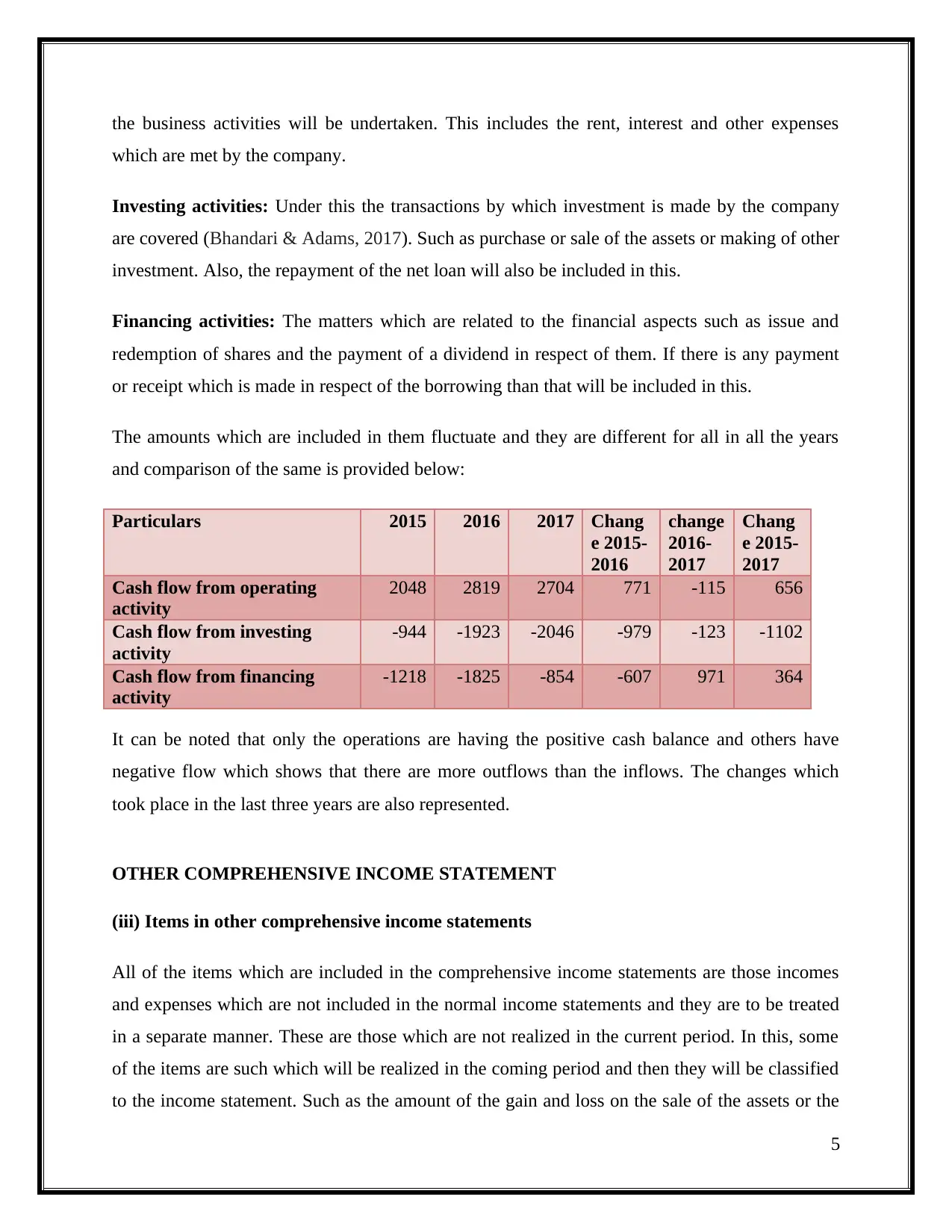

The amounts which are included in them fluctuate and they are different for all in all the years

and comparison of the same is provided below:

Particulars 2015 2016 2017 Chang

e 2015-

2016

change

2016-

2017

Chang

e 2015-

2017

Cash flow from operating

activity

2048 2819 2704 771 -115 656

Cash flow from investing

activity

-944 -1923 -2046 -979 -123 -1102

Cash flow from financing

activity

-1218 -1825 -854 -607 971 364

It can be noted that only the operations are having the positive cash balance and others have

negative flow which shows that there are more outflows than the inflows. The changes which

took place in the last three years are also represented.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) Items in other comprehensive income statements

All of the items which are included in the comprehensive income statements are those incomes

and expenses which are not included in the normal income statements and they are to be treated

in a separate manner. These are those which are not realized in the current period. In this, some

of the items are such which will be realized in the coming period and then they will be classified

to the income statement. Such as the amount of the gain and loss on the sale of the assets or the

5

which are met by the company.

Investing activities: Under this the transactions by which investment is made by the company

are covered (Bhandari & Adams, 2017). Such as purchase or sale of the assets or making of other

investment. Also, the repayment of the net loan will also be included in this.

Financing activities: The matters which are related to the financial aspects such as issue and

redemption of shares and the payment of a dividend in respect of them. If there is any payment

or receipt which is made in respect of the borrowing than that will be included in this.

The amounts which are included in them fluctuate and they are different for all in all the years

and comparison of the same is provided below:

Particulars 2015 2016 2017 Chang

e 2015-

2016

change

2016-

2017

Chang

e 2015-

2017

Cash flow from operating

activity

2048 2819 2704 771 -115 656

Cash flow from investing

activity

-944 -1923 -2046 -979 -123 -1102

Cash flow from financing

activity

-1218 -1825 -854 -607 971 364

It can be noted that only the operations are having the positive cash balance and others have

negative flow which shows that there are more outflows than the inflows. The changes which

took place in the last three years are also represented.

OTHER COMPREHENSIVE INCOME STATEMENT

(iii) Items in other comprehensive income statements

All of the items which are included in the comprehensive income statements are those incomes

and expenses which are not included in the normal income statements and they are to be treated

in a separate manner. These are those which are not realized in the current period. In this, some

of the items are such which will be realized in the coming period and then they will be classified

to the income statement. Such as the amount of the gain and loss on the sale of the assets or the

5

foreign currency transactions. By the help of this, a better understanding of the financial position

of the company will be obtained.

(iv) Understanding of items identified

In the comprehensive income statements, those items are included which are not included in the

income statement of the company. This includes various transactions such as the changes which

take place in the cash flow hedges and they are taken a net of the tax. The time value of the

option is considered and the net change in that is also recognized in this (Gobetti & Orair, 2017).

The balance of the hedge account is then transferred to the income statements. All the foreign

currency translations which are related to the investments are also included in which are taken by

the use of the equity method (Qantas Airways, 2017). All of these accounts will be subsequently

reclassified to the profits and loss account of the business. The actuarial gains which are there

and will not be reclassified are also included in this statement.

(v) Reasons for not including them in income statements

In the income statement only those amount are included which are related to the current period

and are realized in the same period and due to this, it can be used to determine the profit of the

current period. But the items which are included in the comprehensive statement are not realized

and will be transferred to the income statements once they are realized by the company. If they

are incorporated in the profit and loss account then the true picture of the business will not be

identified and the profits will be misstated which will lead to the calculation of the wrong

amount of the tax also.

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) Tax expense in latest financial statements.

In all the businesses there is the need to identify the tax which is to be paid by the company and

for a tart, all the laws which are made in this respect shall be followed by the company so that

the correct amount of the tax is identified. In the financial statements, it is required that expenses

in respect of the tax shall be recognized. In the income statement, a fixed rate of the tax will be

taken on the earnings which are made (Graham, et. al., 2012). In the current year, the financial

6

of the company will be obtained.

(iv) Understanding of items identified

In the comprehensive income statements, those items are included which are not included in the

income statement of the company. This includes various transactions such as the changes which

take place in the cash flow hedges and they are taken a net of the tax. The time value of the

option is considered and the net change in that is also recognized in this (Gobetti & Orair, 2017).

The balance of the hedge account is then transferred to the income statements. All the foreign

currency translations which are related to the investments are also included in which are taken by

the use of the equity method (Qantas Airways, 2017). All of these accounts will be subsequently

reclassified to the profits and loss account of the business. The actuarial gains which are there

and will not be reclassified are also included in this statement.

(v) Reasons for not including them in income statements

In the income statement only those amount are included which are related to the current period

and are realized in the same period and due to this, it can be used to determine the profit of the

current period. But the items which are included in the comprehensive statement are not realized

and will be transferred to the income statements once they are realized by the company. If they

are incorporated in the profit and loss account then the true picture of the business will not be

identified and the profits will be misstated which will lead to the calculation of the wrong

amount of the tax also.

ACCOUNTING FOR CORPORATE INCOME TAX

(vi) Tax expense in latest financial statements.

In all the businesses there is the need to identify the tax which is to be paid by the company and

for a tart, all the laws which are made in this respect shall be followed by the company so that

the correct amount of the tax is identified. In the financial statements, it is required that expenses

in respect of the tax shall be recognized. In the income statement, a fixed rate of the tax will be

taken on the earnings which are made (Graham, et. al., 2012). In the current year, the financial

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

statements of the Qantas airways show the tax expense of 328. This is identified on the profits

which are made by the company (Qantas Airways, 2017).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

The amount which is identified as the tax expense in the income statement is not similar to the

amount which is recognised as per the tax laws and this is due to the difference in the treatment

of the various items which leads to the deviation in the amounts which is recognised as the

profits and also the tax rate which is applicable in both the cases is different. The amount of tax

as per the corporate tax rate of 30% is 354 and then in this adjustments are made in respect of the

non- assessable dividends, loss from the investments and the foreign branches (Qantas Airways,

2017). All other items which are non-deductible according to the law are taken into accounts and

by including all of them the final amount of the tax expenses which is 328 in the given case is

determined.

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded.

Deferred tax asset and liabilities are identified in the accounts of the company due to the

difference in the accounting and the taxable profits and losses which are determined. There is

certainly an amount which is considered in the one law but is not included in the other and so to

make the balance among them deferred tax is determined (Jaya, 2016). In the Qantas airways, it

can be noted from the financial statements that the company was having deferred tax assets in the

2015 and 2016 which amounted to 333 and 39 respectively. Then in the current 2017, the amount

is recognized as 353 and that is deferred tax liabilities. So the timing difference which exists is

eliminated by the company with the help of this (Qantas Airways, 2017).

(ix)Is there any current tax assets or income tax payable recorded by your company? Why

is the income tax payable not the same as income tax expense?

In the business, there are certain situations in which the company will be required to identify the

asset or the liability in respect of the tax. This happens when the company is not paying all of the

tax expense in the current year and due to that the amount which remains unpaid is shown in the

7

which are made by the company (Qantas Airways, 2017).

(vii) Is this figure the same as the company tax rate times your firm’s accounting income?

Explain why this is, or is not, the case for your firm.

The amount which is identified as the tax expense in the income statement is not similar to the

amount which is recognised as per the tax laws and this is due to the difference in the treatment

of the various items which leads to the deviation in the amounts which is recognised as the

profits and also the tax rate which is applicable in both the cases is different. The amount of tax

as per the corporate tax rate of 30% is 354 and then in this adjustments are made in respect of the

non- assessable dividends, loss from the investments and the foreign branches (Qantas Airways,

2017). All other items which are non-deductible according to the law are taken into accounts and

by including all of them the final amount of the tax expenses which is 328 in the given case is

determined.

(viii) Comment on deferred tax assets/liabilities that are reported on the balance sheet

articulating the possible reasons why they have been recorded.

Deferred tax asset and liabilities are identified in the accounts of the company due to the

difference in the accounting and the taxable profits and losses which are determined. There is

certainly an amount which is considered in the one law but is not included in the other and so to

make the balance among them deferred tax is determined (Jaya, 2016). In the Qantas airways, it

can be noted from the financial statements that the company was having deferred tax assets in the

2015 and 2016 which amounted to 333 and 39 respectively. Then in the current 2017, the amount

is recognized as 353 and that is deferred tax liabilities. So the timing difference which exists is

eliminated by the company with the help of this (Qantas Airways, 2017).

(ix)Is there any current tax assets or income tax payable recorded by your company? Why

is the income tax payable not the same as income tax expense?

In the business, there are certain situations in which the company will be required to identify the

asset or the liability in respect of the tax. This happens when the company is not paying all of the

tax expense in the current year and due to that the amount which remains unpaid is shown in the

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

statement of the financial position. In the current case of Qantas Airways, there is no such

amount which has been recognized by the company and so the situation of the difference in the

amount payable and expense does not exist.

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

The amount which is shown as income tax expense in the income statement is not similar to the

one which is identified in the cash flow statement. This is because the cash flow includes only

that amount which is paid in the cash and it is not necessary that the whole amount will be paid

in cash (Samuel & De Dieu, 2014). In the given company the amount of the expense which is

identified is 328 but in the cash flow, only the amount which is related to foreign tax has been

presented which is 4. In the income statement, the total amount is taken into consideration but is

not possible for the company to have the funds by which all of the payment can be made in the

current period only. Due to this the difference which is identified exists.

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s

tax expense in its accounts?

In the Qantas Airways, it has been determined that the company is having the very less amount

of the tax which has been paid and this I due to the adjustment which is made by using the losses

which are carried forward. There is the temporary difference which exists and that has been

identified due to which there is the difference in the taxable profit and the statutory profit.

In order to fulfill the corporate governance requirement, the company is undertaking the risk

management practiced and by that all the objectives which are set in this respect are achieved by

the company. For this, the tax management policy is also taken into consideration. In the

company, it is identified that all of the payments are made and all the laws which are specified in

this respect have also been met and this is good for the company which establishes the positive

image of it in eyes of all (Qantas Airways, 2017). In the company income tax and goods and

service tax both reincluded and all the aspects which require the adjustment in respect of this

8

amount which has been recognized by the company and so the situation of the difference in the

amount payable and expense does not exist.

(x) Is the income tax expense shown in the income statement same as the income tax paid

shown in the cash flow statement? If not why is the difference?

The amount which is shown as income tax expense in the income statement is not similar to the

one which is identified in the cash flow statement. This is because the cash flow includes only

that amount which is paid in the cash and it is not necessary that the whole amount will be paid

in cash (Samuel & De Dieu, 2014). In the given company the amount of the expense which is

identified is 328 but in the cash flow, only the amount which is related to foreign tax has been

presented which is 4. In the income statement, the total amount is taken into consideration but is

not possible for the company to have the funds by which all of the payment can be made in the

current period only. Due to this the difference which is identified exists.

(xi)What do you find interesting, confusing, surprising or difficult to understand about the

treatment of tax in your firm’s financial statements? What new insights, if any, have you

gained about how companies account for income tax as a result of examining your firm’s

tax expense in its accounts?

In the Qantas Airways, it has been determined that the company is having the very less amount

of the tax which has been paid and this I due to the adjustment which is made by using the losses

which are carried forward. There is the temporary difference which exists and that has been

identified due to which there is the difference in the taxable profit and the statutory profit.

In order to fulfill the corporate governance requirement, the company is undertaking the risk

management practiced and by that all the objectives which are set in this respect are achieved by

the company. For this, the tax management policy is also taken into consideration. In the

company, it is identified that all of the payments are made and all the laws which are specified in

this respect have also been met and this is good for the company which establishes the positive

image of it in eyes of all (Qantas Airways, 2017). In the company income tax and goods and

service tax both reincluded and all the aspects which require the adjustment in respect of this

8

have been made. All of the payments which are to be made by the company for the GST have

also been recognized in the financial statements of the company. As there are specific rules in

relation to the airlines business there is the treatment which is provided by the company in

Australia only for the tax and the company considered most of its income in Australia so that

proper liability is identified.

9

also been recognized in the financial statements of the company. As there are specific rules in

relation to the airlines business there is the treatment which is provided by the company in

Australia only for the tax and the company considered most of its income in Australia so that

proper liability is identified.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Bhandari, S. B., & Adams, M. T. (2017). On the Definition, Measurement, and Use of the

Free Cash Flow Concept in Financial Reporting and Analysis: A Review and

Recommendations. Journal of Accounting and Finance, 17(1), 11-19.

Gobetti, S. W., & Orair, R. O. (2017). Taxation and distribution of income in Brazil: new

evidence from personal income tax data. Revista de Economia Política, 37(2), 267-286.

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for

income taxes. Journal of Accounting and Economics, 53(1), 412-434.

Jaya, T. E. (2016). Earnings, Leverage, and Deferred Tax on Tax Penalties and Fines

(Case study in Indonesia).

Qantas Airways. (2016). Annual report. [Online]. Qantas Airways. Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgy

w/file/annual-reports/2016AnnualReport.pdf. [Accessed: 15 May 2018]

Qantas Airways. (2017). Annual report. [Online]. Qantas Airways. Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/AH_NGR9NxUaXc0W8Qv

3Kfg/docs/QantasAnnualReport2017.pdf. [Accessed: 15 May 2018]

Samuel, M., & De Dieu, R. J. (2014). The impact of taxpayers' financial statements audit

on tax revenue growth. International Journal of Business and Economic Development

(IJBED), 2(2).

10

Bhandari, S. B., & Adams, M. T. (2017). On the Definition, Measurement, and Use of the

Free Cash Flow Concept in Financial Reporting and Analysis: A Review and

Recommendations. Journal of Accounting and Finance, 17(1), 11-19.

Gobetti, S. W., & Orair, R. O. (2017). Taxation and distribution of income in Brazil: new

evidence from personal income tax data. Revista de Economia Política, 37(2), 267-286.

Graham, J. R., Raedy, J. S., & Shackelford, D. A. (2012). Research in accounting for

income taxes. Journal of Accounting and Economics, 53(1), 412-434.

Jaya, T. E. (2016). Earnings, Leverage, and Deferred Tax on Tax Penalties and Fines

(Case study in Indonesia).

Qantas Airways. (2016). Annual report. [Online]. Qantas Airways. Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgy

w/file/annual-reports/2016AnnualReport.pdf. [Accessed: 15 May 2018]

Qantas Airways. (2017). Annual report. [Online]. Qantas Airways. Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/AH_NGR9NxUaXc0W8Qv

3Kfg/docs/QantasAnnualReport2017.pdf. [Accessed: 15 May 2018]

Samuel, M., & De Dieu, R. J. (2014). The impact of taxpayers' financial statements audit

on tax revenue growth. International Journal of Business and Economic Development

(IJBED), 2(2).

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.