ACCG224: Financial Accounting and Reporting on Qantas Impairment

VerifiedAdded on 2022/12/14

|11

|1802

|180

Report

AI Summary

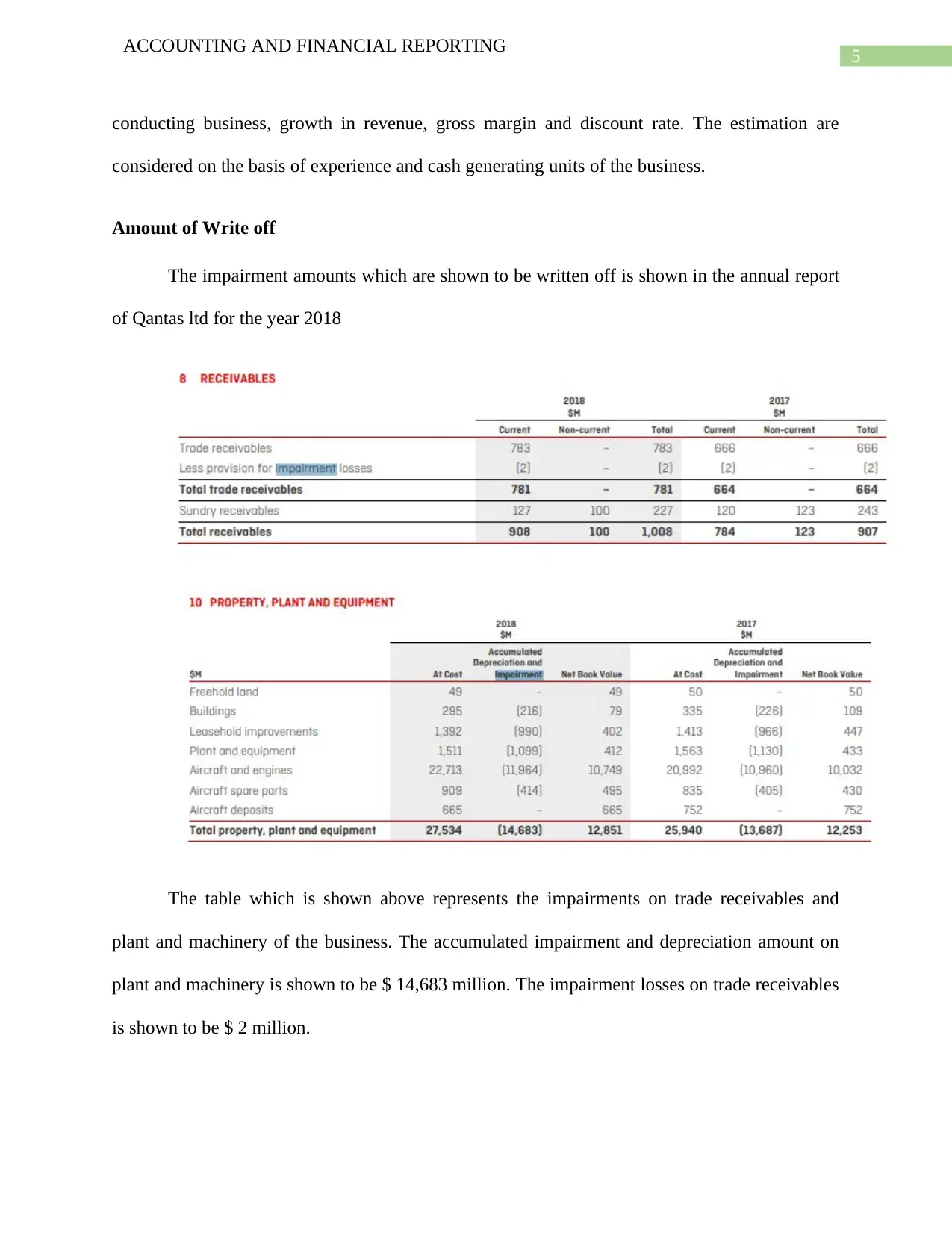

This report analyzes the financial reporting practices of Qantas Ltd, focusing on the application of professional judgment in impairment testing. It examines the impaired assets of the company, including trade receivables, land, buildings, and intangible assets, and the estimation processes used for write-downs. The report evaluates the disclosures made by Qantas Ltd regarding impairment testing, considering the guidelines provided by ASIC. The assessment highlights the importance of professional judgment in ensuring the quality and accuracy of financial reports and identifies areas where Qantas Ltd could improve its disclosures and assumptions, particularly in relation to cash flow estimations and the allocation of corporate assets to cash-generating units. The conclusion emphasizes the significance of detailed disclosures and adherence to accounting standards, particularly in the context of impairment testing, to provide a transparent and reliable view of a company's financial position.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.