Financial Analysis of Qantas Airline: An Investment Consideration

VerifiedAdded on 2021/06/16

|15

|3343

|18

Report

AI Summary

This report provides a comprehensive financial analysis of Qantas Airline, focusing on its performance from 2015 to 2017. The analysis utilizes various financial ratios, including liquidity, efficiency, solvency, and profitability ratios, to assess the airline's financial health and investment potential. The report calculates and interprets ratios such as current ratio, quick ratio, accounts receivable turnover, debt-to-asset ratio, and profit margin. The findings offer insights into Qantas's ability to manage its short-term obligations, operational efficiency, leverage, and profitability. The analysis aims to determine whether Qantas is a good consideration for investment, offering recommendations based on the financial performance evaluation. The report provides a detailed overview of the company's financial statements, enabling a thorough understanding of its financial position and performance trends.

Running head: HOSPITALITY FINANCE AND REVENUE

Hospitality finance and revenue

Name of the student

Name of the university

Student ID

Author note

Hospitality finance and revenue

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1HOSPITALITY FINANCE AND REVENUE

Abstract

The main objective of the report is to analyse the financial performance of Qantas airline to

consider it from the investment aspect. The report will consider the financial statement of the

company for the year ended 2015, 2016 and 2017 and will calculate various ratios like

profitability ratio, solvency ratio, liquidity ratio and efficiency ratio. After analysing the

company’s performance through the ratios conclusions will be provide to measure whether

the company is a good consideration for investment or not and based on that some

recommendations will be provided.

Abstract

The main objective of the report is to analyse the financial performance of Qantas airline to

consider it from the investment aspect. The report will consider the financial statement of the

company for the year ended 2015, 2016 and 2017 and will calculate various ratios like

profitability ratio, solvency ratio, liquidity ratio and efficiency ratio. After analysing the

company’s performance through the ratios conclusions will be provide to measure whether

the company is a good consideration for investment or not and based on that some

recommendations will be provided.

2HOSPITALITY FINANCE AND REVENUE

Table of Contents

1.0 Introduction..........................................................................................................................3

2.0 Analysis of ratio...................................................................................................................3

2.1 Liquidity ratio...................................................................................................................5

2.2 Efficiency ratio.................................................................................................................6

2.3 Solvency ratio...................................................................................................................7

2.4 Profitability ratio..............................................................................................................9

3.0 Conclusion..........................................................................................................................10

4.0 Recommendation................................................................................................................10

Reference..................................................................................................................................12

Table of Contents

1.0 Introduction..........................................................................................................................3

2.0 Analysis of ratio...................................................................................................................3

2.1 Liquidity ratio...................................................................................................................5

2.2 Efficiency ratio.................................................................................................................6

2.3 Solvency ratio...................................................................................................................7

2.4 Profitability ratio..............................................................................................................9

3.0 Conclusion..........................................................................................................................10

4.0 Recommendation................................................................................................................10

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3HOSPITALITY FINANCE AND REVENUE

1.0 Introduction

The aim of the report is analysing Qantas Airline’s financial report with the

investment aspect. The report will interpret and analyse the performance taking into account

various financial ratio for the current year that is 2017 and comparing it with the previous

years that is 2016 and 2015. Ratios that will be considered are the efficiency ratio,

profitability ratio, liquidity ratio and solvency ratio. After analysing the performance of the

company through the ratios conclusions will be provide to measure whether the company is a

good consideration for investment or not and based on that some recommendations will be

provided.

Established in the year 1920, Qantas airline is counted among the largest domestic as

well as internal airlines in Australia. The company is engaged in mainly transportation

service through two of its complementary brand named as Qantas and Jetstar. Qantas is well

known for providing excellent services to its customers and for the engineering, maintenance,

customer’s safety, operational liability. Additional business carried out by the airline is the Q

catering under the specialist market. The company employs more than 30,000 employs out of

which more than 93% is Australian based. It provides regional, domestic and international

services and its main objective is to revolutionalise air transport all over the market segments.

The company achieves its objectives through providing smooth experience through all over

the domestic as well as the international market apart from retaining the excellence in service

level (Flights | Qantas AU, 2018).

2.0 Analysis of ratio

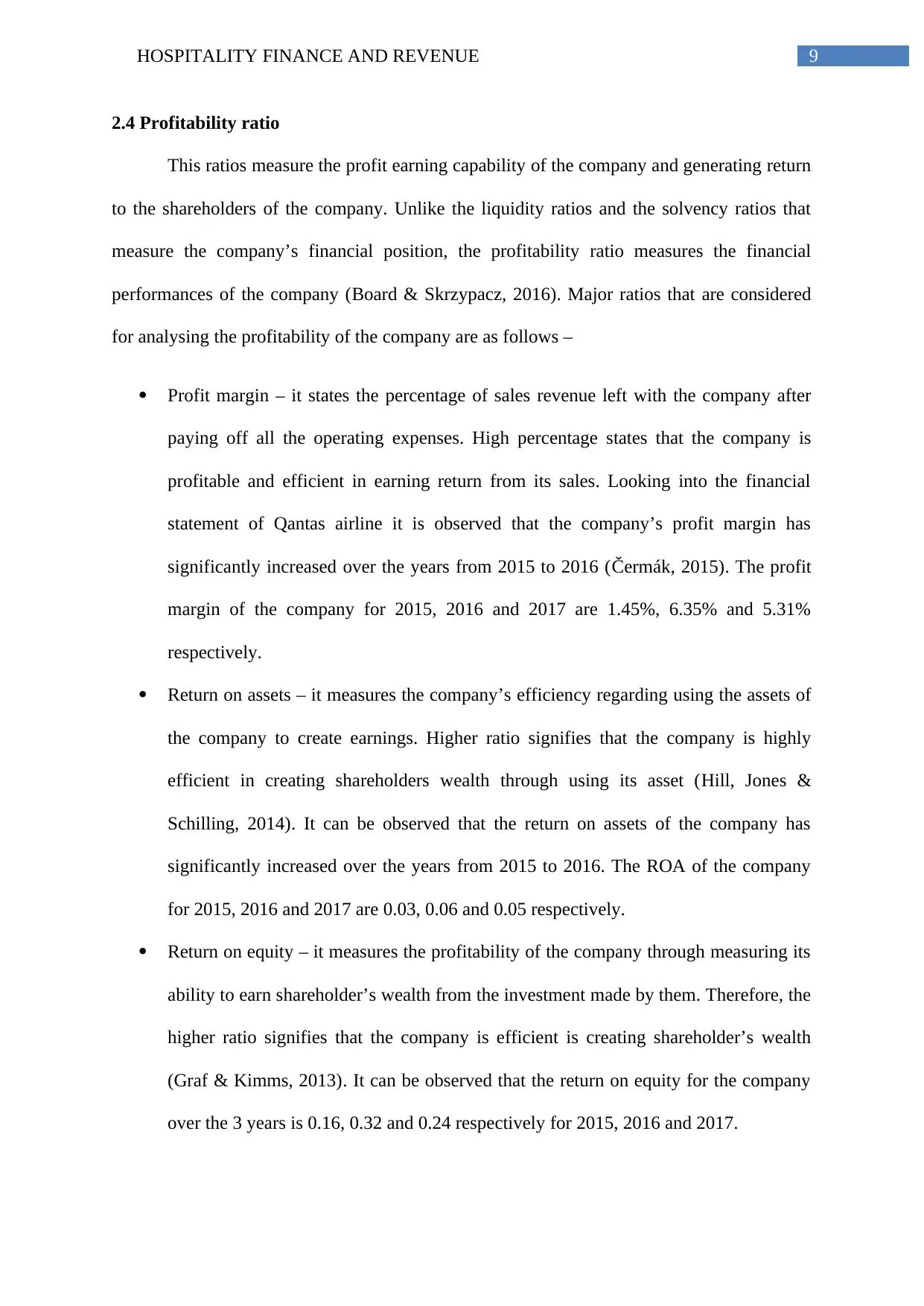

Ratio Formula Qantas Airline

2017 2016 2015

Current ratio Current assets/Current liabilities 0.44 0.49 0.68

1.0 Introduction

The aim of the report is analysing Qantas Airline’s financial report with the

investment aspect. The report will interpret and analyse the performance taking into account

various financial ratio for the current year that is 2017 and comparing it with the previous

years that is 2016 and 2015. Ratios that will be considered are the efficiency ratio,

profitability ratio, liquidity ratio and solvency ratio. After analysing the performance of the

company through the ratios conclusions will be provide to measure whether the company is a

good consideration for investment or not and based on that some recommendations will be

provided.

Established in the year 1920, Qantas airline is counted among the largest domestic as

well as internal airlines in Australia. The company is engaged in mainly transportation

service through two of its complementary brand named as Qantas and Jetstar. Qantas is well

known for providing excellent services to its customers and for the engineering, maintenance,

customer’s safety, operational liability. Additional business carried out by the airline is the Q

catering under the specialist market. The company employs more than 30,000 employs out of

which more than 93% is Australian based. It provides regional, domestic and international

services and its main objective is to revolutionalise air transport all over the market segments.

The company achieves its objectives through providing smooth experience through all over

the domestic as well as the international market apart from retaining the excellence in service

level (Flights | Qantas AU, 2018).

2.0 Analysis of ratio

Ratio Formula Qantas Airline

2017 2016 2015

Current ratio Current assets/Current liabilities 0.44 0.49 0.68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4HOSPITALITY FINANCE AND REVENUE

Quick ratio Current assets less

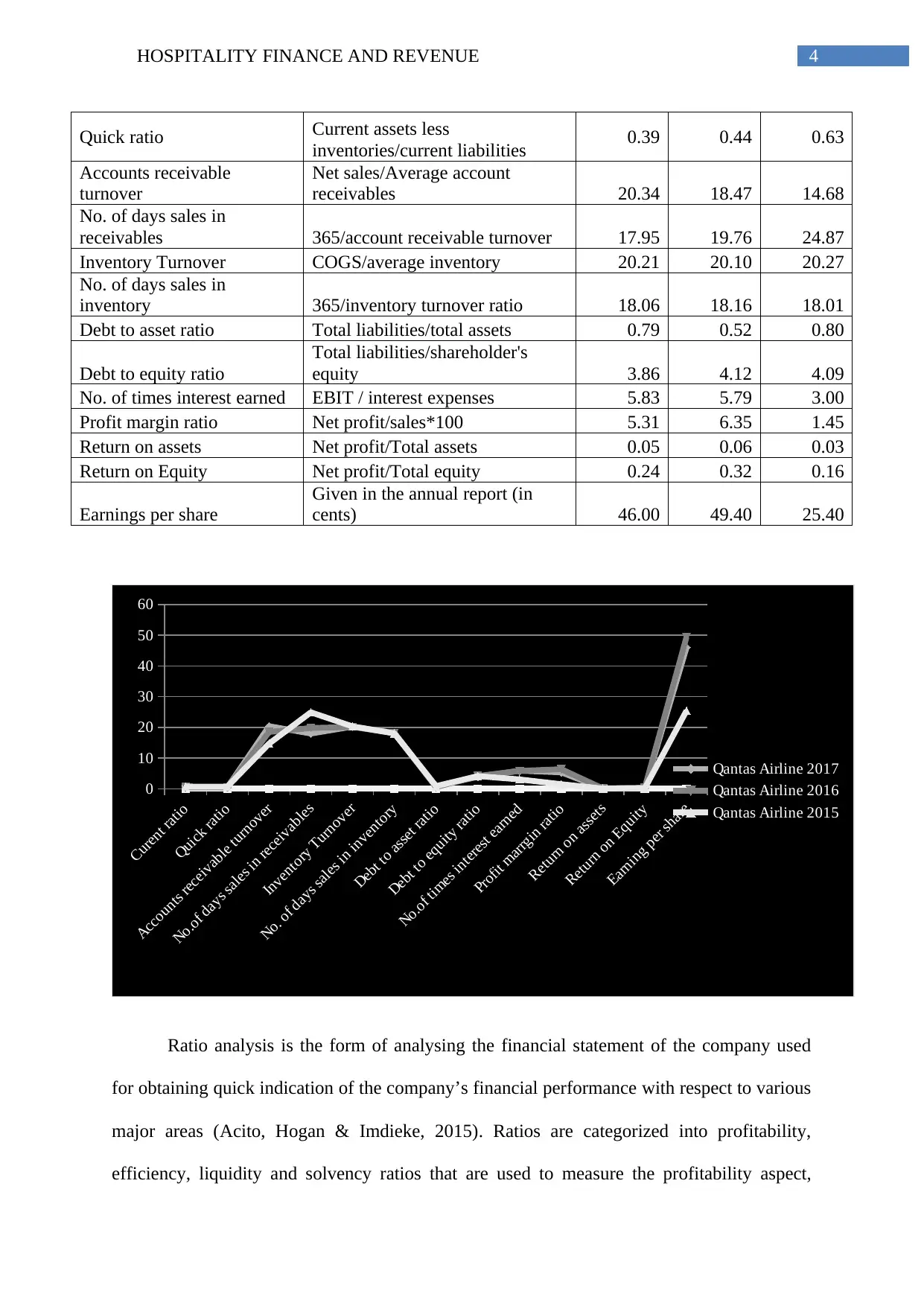

inventories/current liabilities 0.39 0.44 0.63

Accounts receivable

turnover

Net sales/Average account

receivables 20.34 18.47 14.68

No. of days sales in

receivables 365/account receivable turnover 17.95 19.76 24.87

Inventory Turnover COGS/average inventory 20.21 20.10 20.27

No. of days sales in

inventory 365/inventory turnover ratio 18.06 18.16 18.01

Debt to asset ratio Total liabilities/total assets 0.79 0.52 0.80

Debt to equity ratio

Total liabilities/shareholder's

equity 3.86 4.12 4.09

No. of times interest earned EBIT / interest expenses 5.83 5.79 3.00

Profit margin ratio Net profit/sales*100 5.31 6.35 1.45

Return on assets Net profit/Total assets 0.05 0.06 0.03

Return on Equity Net profit/Total equity 0.24 0.32 0.16

Earnings per share

Given in the annual report (in

cents) 46.00 49.40 25.40

Curent ratio

Quick ratio

Accounts receivable turnover

No.of days sales in receivables

Inventory Turnover

No. of days sales in inventory

Debt to asset ratio

Debt to equity ratio

No.of times interest earned

Profit marrgin ratio

Return on assets

Return on Equity

Earning per share

0

10

20

30

40

50

60

Qantas Airline 2017

Qantas Airline 2016

Qantas Airline 2015

Ratio analysis is the form of analysing the financial statement of the company used

for obtaining quick indication of the company’s financial performance with respect to various

major areas (Acito, Hogan & Imdieke, 2015). Ratios are categorized into profitability,

efficiency, liquidity and solvency ratios that are used to measure the profitability aspect,

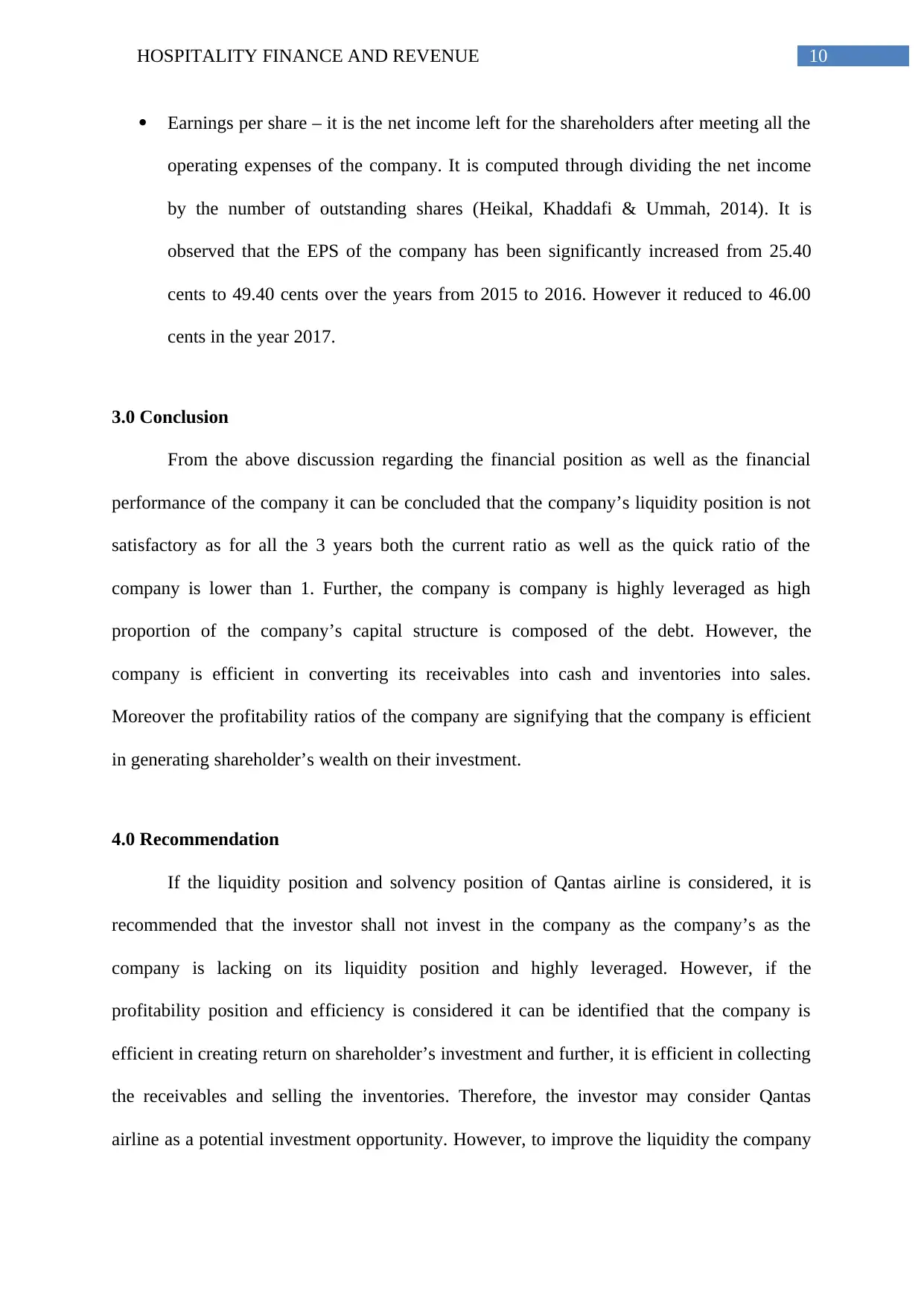

Quick ratio Current assets less

inventories/current liabilities 0.39 0.44 0.63

Accounts receivable

turnover

Net sales/Average account

receivables 20.34 18.47 14.68

No. of days sales in

receivables 365/account receivable turnover 17.95 19.76 24.87

Inventory Turnover COGS/average inventory 20.21 20.10 20.27

No. of days sales in

inventory 365/inventory turnover ratio 18.06 18.16 18.01

Debt to asset ratio Total liabilities/total assets 0.79 0.52 0.80

Debt to equity ratio

Total liabilities/shareholder's

equity 3.86 4.12 4.09

No. of times interest earned EBIT / interest expenses 5.83 5.79 3.00

Profit margin ratio Net profit/sales*100 5.31 6.35 1.45

Return on assets Net profit/Total assets 0.05 0.06 0.03

Return on Equity Net profit/Total equity 0.24 0.32 0.16

Earnings per share

Given in the annual report (in

cents) 46.00 49.40 25.40

Curent ratio

Quick ratio

Accounts receivable turnover

No.of days sales in receivables

Inventory Turnover

No. of days sales in inventory

Debt to asset ratio

Debt to equity ratio

No.of times interest earned

Profit marrgin ratio

Return on assets

Return on Equity

Earning per share

0

10

20

30

40

50

60

Qantas Airline 2017

Qantas Airline 2016

Qantas Airline 2015

Ratio analysis is the form of analysing the financial statement of the company used

for obtaining quick indication of the company’s financial performance with respect to various

major areas (Acito, Hogan & Imdieke, 2015). Ratios are categorized into profitability,

efficiency, liquidity and solvency ratios that are used to measure the profitability aspect,

5HOSPITALITY FINANCE AND REVENUE

liquidity aspect, sustainability aspect and efficiency of the company. Based upon various

categories the ratios will be analysed as follows –

2.1 Liquidity ratio

The liquidity ratios are used to measure the liquidity position of the company through

analysing its ability to meet the short-term obligations through the available short-term assets

of the company when the obligations become due (Drehmann & Nikolaou, 2013). For

measuring the liquidity of the company the below mentioned ratios are taken into

consideration -

Current ratio – One of the most commonly used liquidity ratio of any company is the

current ratio. It analyses the liquidity position of the company through comparing its

current assets with the current liabilities. It also helps the investors to assess the

company’s financial health. High current ratio like more than 1 signifies that company

is efficient and able to pay-off its short term obligations (Nobes, 2014). On the

contrary, low current ratio signifies that the company has issues regarding payment of

its short-term obligations. From the calculation table it is observed that the current

ratio of the company is in decreasing trend and for all the 3 years the current ratio of

the company is significantly lower than 1. It is identified that the current ratio of the

company is 0.68, 0.49 and 0.44 respectively for the years 2015, 2016 and 2017.

Quick ratio – this ratio also measures the liquidity status of the company. The main

difference among the current ratio and quick ratio is that the quick ratio only takes

into account the quick assets and does not consider the assets that take some time to

get converted into cash like inventories (Prasetyorini, 2013). High quick ratio like

more than 1 signifies that company is efficient and able to pay-off its short term

obligations. From the calculation table it is observed that the quick ratio of the

company is in decreasing trend and for all the 3 years the quick ratio of the company

liquidity aspect, sustainability aspect and efficiency of the company. Based upon various

categories the ratios will be analysed as follows –

2.1 Liquidity ratio

The liquidity ratios are used to measure the liquidity position of the company through

analysing its ability to meet the short-term obligations through the available short-term assets

of the company when the obligations become due (Drehmann & Nikolaou, 2013). For

measuring the liquidity of the company the below mentioned ratios are taken into

consideration -

Current ratio – One of the most commonly used liquidity ratio of any company is the

current ratio. It analyses the liquidity position of the company through comparing its

current assets with the current liabilities. It also helps the investors to assess the

company’s financial health. High current ratio like more than 1 signifies that company

is efficient and able to pay-off its short term obligations (Nobes, 2014). On the

contrary, low current ratio signifies that the company has issues regarding payment of

its short-term obligations. From the calculation table it is observed that the current

ratio of the company is in decreasing trend and for all the 3 years the current ratio of

the company is significantly lower than 1. It is identified that the current ratio of the

company is 0.68, 0.49 and 0.44 respectively for the years 2015, 2016 and 2017.

Quick ratio – this ratio also measures the liquidity status of the company. The main

difference among the current ratio and quick ratio is that the quick ratio only takes

into account the quick assets and does not consider the assets that take some time to

get converted into cash like inventories (Prasetyorini, 2013). High quick ratio like

more than 1 signifies that company is efficient and able to pay-off its short term

obligations. From the calculation table it is observed that the quick ratio of the

company is in decreasing trend and for all the 3 years the quick ratio of the company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6HOSPITALITY FINANCE AND REVENUE

is significantly lower than 1. It is identified that the quick ratio of the company is

0.63, 0.44 and 0.39 respectively for the years 2015, 2016 and 2017.

2.2 Efficiency ratio

The efficiency ratios are computed to assess the company’s operational efficiency. It

is used to measure the efficiency of the company regarding the time taken by the company to

convert its account receivables into cash and converting the inventories into sales (Scott,

2015). To be more specific, it measures the company’s efficiency with respect to usage of its

assets as well as the working capital. Major activity ratios considered for measuring the

efficiency of Qantas Airlines are as follows –

Receivable turnover ratio and number of the days sales in receivables – receivable

turnover ratio is used to measure the efficiency of the company in collecting its credit

sales and converting it into cash. High ratio signifies that the company is highly

efficient in collecting its receivables and take short time in collecting it. On the

contrary, lower ratio signifies the inefficiency of the company (Sunder, 2016).

Number of days the sales in receivable signifies the average days in number the

company takes to collect its receivables after making the sales. Therefore, lower ratio

is considered better as it signifies that the company less time in collecting its

receivables. Looking into the computation table for ratios it is observed that both the

receivable turnover and days sales in inventories for Qantas airline for the years 2015,

2016 and 2017 are in improving trend. Account receivable turnover for the company

is 14.68, 18.47 and 20.34 respectively for 2015, 2016 and 2017. On the other hand,

number of day’s sales in receivables for the company is 24.87 days, 19.76 days and

17.95 days respectively for 2015, 2016 and 2017.

Inventory turnover ratio and number of day’s sales in inventory – inventory turnover

is the efficiency ratio that measures the no. of times the company is able to sell and

is significantly lower than 1. It is identified that the quick ratio of the company is

0.63, 0.44 and 0.39 respectively for the years 2015, 2016 and 2017.

2.2 Efficiency ratio

The efficiency ratios are computed to assess the company’s operational efficiency. It

is used to measure the efficiency of the company regarding the time taken by the company to

convert its account receivables into cash and converting the inventories into sales (Scott,

2015). To be more specific, it measures the company’s efficiency with respect to usage of its

assets as well as the working capital. Major activity ratios considered for measuring the

efficiency of Qantas Airlines are as follows –

Receivable turnover ratio and number of the days sales in receivables – receivable

turnover ratio is used to measure the efficiency of the company in collecting its credit

sales and converting it into cash. High ratio signifies that the company is highly

efficient in collecting its receivables and take short time in collecting it. On the

contrary, lower ratio signifies the inefficiency of the company (Sunder, 2016).

Number of days the sales in receivable signifies the average days in number the

company takes to collect its receivables after making the sales. Therefore, lower ratio

is considered better as it signifies that the company less time in collecting its

receivables. Looking into the computation table for ratios it is observed that both the

receivable turnover and days sales in inventories for Qantas airline for the years 2015,

2016 and 2017 are in improving trend. Account receivable turnover for the company

is 14.68, 18.47 and 20.34 respectively for 2015, 2016 and 2017. On the other hand,

number of day’s sales in receivables for the company is 24.87 days, 19.76 days and

17.95 days respectively for 2015, 2016 and 2017.

Inventory turnover ratio and number of day’s sales in inventory – inventory turnover

is the efficiency ratio that measures the no. of times the company is able to sell and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7HOSPITALITY FINANCE AND REVENUE

replace its inventories. It is measured through dividing the COGS of the company by

the average inventories. High ratio signifies that the company is highly efficient in

replacing or selling its inventories. On the contrary, lower ratio signifies the

inefficiency of the company. Looking into the calculation table it can be stated that

for the last 3 years the company is stable in selling its inventories and there is not

much changes in the ratio. The inventory turnover ratio for the company is 20.27,

20.10 and 20.21 respectively for 2015, 2016 and 2017. On the other hand, it can be

observed that the number of day’s sales in inventory for the company over the last 3

years is and there is not much changes in the ratio. Number of day’s sales in inventory

for the company is 18.01, 18.16 and 18.06 respectively for 2015, 2016 and 2017.

2.3 Solvency ratio

This ratio is analysed to measure the leverage level of the company. It measures the

solvency of the company through calculating the capital structure and financial risk of the

company. Further, the long-term sustainability of the company is measured through

measuring the long-term borrowings of the company and its ability to pay-off the interest

obligation related to the borrowing (Ch, Patel & White, 2015). Solvency of Qantas airline is

analysed through the following ratios –

Debt to assets ratio – it is the leverage ratio that is measured through comparing the

total liabilities of the company to its total assets. It shows how much proportion of the

assets is financed through borrowing as compared to that of financed by investors.

The ratio of 1 signifies that the assets of the company are equally financed by the

investors as well as borrowings. However the ratio of more than 1 signifies that the

company is highly leveraged (Luez & Wysocki, 2016). From the calculation table it

can be observed that the for all the 3 years the debt to assets ratio of the company is

less than 1 and the ratios are 0.80, 0.52 and 0.79 for 2015, 2016 and 2017

replace its inventories. It is measured through dividing the COGS of the company by

the average inventories. High ratio signifies that the company is highly efficient in

replacing or selling its inventories. On the contrary, lower ratio signifies the

inefficiency of the company. Looking into the calculation table it can be stated that

for the last 3 years the company is stable in selling its inventories and there is not

much changes in the ratio. The inventory turnover ratio for the company is 20.27,

20.10 and 20.21 respectively for 2015, 2016 and 2017. On the other hand, it can be

observed that the number of day’s sales in inventory for the company over the last 3

years is and there is not much changes in the ratio. Number of day’s sales in inventory

for the company is 18.01, 18.16 and 18.06 respectively for 2015, 2016 and 2017.

2.3 Solvency ratio

This ratio is analysed to measure the leverage level of the company. It measures the

solvency of the company through calculating the capital structure and financial risk of the

company. Further, the long-term sustainability of the company is measured through

measuring the long-term borrowings of the company and its ability to pay-off the interest

obligation related to the borrowing (Ch, Patel & White, 2015). Solvency of Qantas airline is

analysed through the following ratios –

Debt to assets ratio – it is the leverage ratio that is measured through comparing the

total liabilities of the company to its total assets. It shows how much proportion of the

assets is financed through borrowing as compared to that of financed by investors.

The ratio of 1 signifies that the assets of the company are equally financed by the

investors as well as borrowings. However the ratio of more than 1 signifies that the

company is highly leveraged (Luez & Wysocki, 2016). From the calculation table it

can be observed that the for all the 3 years the debt to assets ratio of the company is

less than 1 and the ratios are 0.80, 0.52 and 0.79 for 2015, 2016 and 2017

8HOSPITALITY FINANCE AND REVENUE

respectively. Therefore, the company is lower leveraged and less exposed to financial

risk. .

Debt to equity ratio – it measures the capital structure of the company that is the

percentage of debt component and equity component in the capital structure of the

company. It further states the percentage of assets financed through borrowing and

financed tough the investor’s capital (Grant, 2016). If company obtained outside

finance in its capital structure it will be able to increase its profit as compared to the

situation where the capital structure only includes only equity as the debt are

deductible expenses under tax whereas equity is not deductible. However, very high

ratio signifies that the company’s debt component is very high and it will put

additional burden on the company that may lead to the level of un-sustainability.

Looking into the financial statement of the company for the years 2015, 2016 and

2017 it is identified that for all the years the debt to equity ratio of the company is

significantly high and the ratio is 4.09, 4.12 and 3.86 respectively. It states that the

company’s capital structure includes high proportion of debt that signifies that the

company is highly leveraged (Kettunen, 2017).

Number of times interest earned – it measures the efficiency of the company with

regard to its ability of paying the interest on its financial obligation. very low ratio

like less than 2 signifies the company’s inefficiencies regarding the payment of

interest expenses (Jones & Kulish, 2013). Looking into the ratio calculation table it

can be observed that company has improved its efficiency over the years from 2015 to

2016. Further, the number of times interest earned by the company is 3.00 times, 5.79

times and 5.83 times respectively for the years 2015, 2016 and 2017.

respectively. Therefore, the company is lower leveraged and less exposed to financial

risk. .

Debt to equity ratio – it measures the capital structure of the company that is the

percentage of debt component and equity component in the capital structure of the

company. It further states the percentage of assets financed through borrowing and

financed tough the investor’s capital (Grant, 2016). If company obtained outside

finance in its capital structure it will be able to increase its profit as compared to the

situation where the capital structure only includes only equity as the debt are

deductible expenses under tax whereas equity is not deductible. However, very high

ratio signifies that the company’s debt component is very high and it will put

additional burden on the company that may lead to the level of un-sustainability.

Looking into the financial statement of the company for the years 2015, 2016 and

2017 it is identified that for all the years the debt to equity ratio of the company is

significantly high and the ratio is 4.09, 4.12 and 3.86 respectively. It states that the

company’s capital structure includes high proportion of debt that signifies that the

company is highly leveraged (Kettunen, 2017).

Number of times interest earned – it measures the efficiency of the company with

regard to its ability of paying the interest on its financial obligation. very low ratio

like less than 2 signifies the company’s inefficiencies regarding the payment of

interest expenses (Jones & Kulish, 2013). Looking into the ratio calculation table it

can be observed that company has improved its efficiency over the years from 2015 to

2016. Further, the number of times interest earned by the company is 3.00 times, 5.79

times and 5.83 times respectively for the years 2015, 2016 and 2017.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9HOSPITALITY FINANCE AND REVENUE

2.4 Profitability ratio

This ratios measure the profit earning capability of the company and generating return

to the shareholders of the company. Unlike the liquidity ratios and the solvency ratios that

measure the company’s financial position, the profitability ratio measures the financial

performances of the company (Board & Skrzypacz, 2016). Major ratios that are considered

for analysing the profitability of the company are as follows –

Profit margin – it states the percentage of sales revenue left with the company after

paying off all the operating expenses. High percentage states that the company is

profitable and efficient in earning return from its sales. Looking into the financial

statement of Qantas airline it is observed that the company’s profit margin has

significantly increased over the years from 2015 to 2016 (Čermák, 2015). The profit

margin of the company for 2015, 2016 and 2017 are 1.45%, 6.35% and 5.31%

respectively.

Return on assets – it measures the company’s efficiency regarding using the assets of

the company to create earnings. Higher ratio signifies that the company is highly

efficient in creating shareholders wealth through using its asset (Hill, Jones &

Schilling, 2014). It can be observed that the return on assets of the company has

significantly increased over the years from 2015 to 2016. The ROA of the company

for 2015, 2016 and 2017 are 0.03, 0.06 and 0.05 respectively.

Return on equity – it measures the profitability of the company through measuring its

ability to earn shareholder’s wealth from the investment made by them. Therefore, the

higher ratio signifies that the company is efficient is creating shareholder’s wealth

(Graf & Kimms, 2013). It can be observed that the return on equity for the company

over the 3 years is 0.16, 0.32 and 0.24 respectively for 2015, 2016 and 2017.

2.4 Profitability ratio

This ratios measure the profit earning capability of the company and generating return

to the shareholders of the company. Unlike the liquidity ratios and the solvency ratios that

measure the company’s financial position, the profitability ratio measures the financial

performances of the company (Board & Skrzypacz, 2016). Major ratios that are considered

for analysing the profitability of the company are as follows –

Profit margin – it states the percentage of sales revenue left with the company after

paying off all the operating expenses. High percentage states that the company is

profitable and efficient in earning return from its sales. Looking into the financial

statement of Qantas airline it is observed that the company’s profit margin has

significantly increased over the years from 2015 to 2016 (Čermák, 2015). The profit

margin of the company for 2015, 2016 and 2017 are 1.45%, 6.35% and 5.31%

respectively.

Return on assets – it measures the company’s efficiency regarding using the assets of

the company to create earnings. Higher ratio signifies that the company is highly

efficient in creating shareholders wealth through using its asset (Hill, Jones &

Schilling, 2014). It can be observed that the return on assets of the company has

significantly increased over the years from 2015 to 2016. The ROA of the company

for 2015, 2016 and 2017 are 0.03, 0.06 and 0.05 respectively.

Return on equity – it measures the profitability of the company through measuring its

ability to earn shareholder’s wealth from the investment made by them. Therefore, the

higher ratio signifies that the company is efficient is creating shareholder’s wealth

(Graf & Kimms, 2013). It can be observed that the return on equity for the company

over the 3 years is 0.16, 0.32 and 0.24 respectively for 2015, 2016 and 2017.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10HOSPITALITY FINANCE AND REVENUE

Earnings per share – it is the net income left for the shareholders after meeting all the

operating expenses of the company. It is computed through dividing the net income

by the number of outstanding shares (Heikal, Khaddafi & Ummah, 2014). It is

observed that the EPS of the company has been significantly increased from 25.40

cents to 49.40 cents over the years from 2015 to 2016. However it reduced to 46.00

cents in the year 2017.

3.0 Conclusion

From the above discussion regarding the financial position as well as the financial

performance of the company it can be concluded that the company’s liquidity position is not

satisfactory as for all the 3 years both the current ratio as well as the quick ratio of the

company is lower than 1. Further, the company is company is highly leveraged as high

proportion of the company’s capital structure is composed of the debt. However, the

company is efficient in converting its receivables into cash and inventories into sales.

Moreover the profitability ratios of the company are signifying that the company is efficient

in generating shareholder’s wealth on their investment.

4.0 Recommendation

If the liquidity position and solvency position of Qantas airline is considered, it is

recommended that the investor shall not invest in the company as the company’s as the

company is lacking on its liquidity position and highly leveraged. However, if the

profitability position and efficiency is considered it can be identified that the company is

efficient in creating return on shareholder’s investment and further, it is efficient in collecting

the receivables and selling the inventories. Therefore, the investor may consider Qantas

airline as a potential investment opportunity. However, to improve the liquidity the company

Earnings per share – it is the net income left for the shareholders after meeting all the

operating expenses of the company. It is computed through dividing the net income

by the number of outstanding shares (Heikal, Khaddafi & Ummah, 2014). It is

observed that the EPS of the company has been significantly increased from 25.40

cents to 49.40 cents over the years from 2015 to 2016. However it reduced to 46.00

cents in the year 2017.

3.0 Conclusion

From the above discussion regarding the financial position as well as the financial

performance of the company it can be concluded that the company’s liquidity position is not

satisfactory as for all the 3 years both the current ratio as well as the quick ratio of the

company is lower than 1. Further, the company is company is highly leveraged as high

proportion of the company’s capital structure is composed of the debt. However, the

company is efficient in converting its receivables into cash and inventories into sales.

Moreover the profitability ratios of the company are signifying that the company is efficient

in generating shareholder’s wealth on their investment.

4.0 Recommendation

If the liquidity position and solvency position of Qantas airline is considered, it is

recommended that the investor shall not invest in the company as the company’s as the

company is lacking on its liquidity position and highly leveraged. However, if the

profitability position and efficiency is considered it can be identified that the company is

efficient in creating return on shareholder’s investment and further, it is efficient in collecting

the receivables and selling the inventories. Therefore, the investor may consider Qantas

airline as a potential investment opportunity. However, to improve the liquidity the company

11HOSPITALITY FINANCE AND REVENUE

shall pay off its current obligation and to improve the solvency it shall raise further fund

through equity instead of debt.

shall pay off its current obligation and to improve the solvency it shall raise further fund

through equity instead of debt.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.