Corporate Accounting Project Report: Qantas Ltd Financial Analysis

VerifiedAdded on 2021/06/15

|11

|2787

|48

Project

AI Summary

This project report offers a comprehensive analysis of Qantas Limited's corporate accounting practices, focusing on the company's financial performance and position. The report examines the cash flow statement, comparing data from 2015 to 2017 to assess changes in operating, investing, and financing activities. It also analyzes the comprehensive income statement, highlighting the items included and the reasons for their treatment. Furthermore, the report delves into Qantas's tax expenses, comparing the reported tax amount with the accounting profit and exploring the deferred tax amount and current tax liabilities. The analysis provides insights into the differences between tax expenses and actual tax payments, detailing the factors influencing these discrepancies, such as deferred tax assets and liabilities. The report concludes by summarizing the key findings and implications of the financial analysis, offering a clear understanding of Qantas's financial health and accounting practices.

Running Head: Corporate Accounting

1

Project Report: Corporate Accounting

1

Project Report: Corporate Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

2

Contents

Introduction.......................................................................................................................3

Company overview...........................................................................................................3

1. Cash flow statement analysis........................................................................................3

2. Comparative analysis on cash flow statement..............................................................4

3. Comprehensive income statement analysis..................................................................5

4. Comprehensive income statement items......................................................................6

5. Reasons.........................................................................................................................6

6. Tax expenses of the company.......................................................................................6

7. Similarity in tax expenses.............................................................................................7

8. Deferred tax amount.....................................................................................................7

9. Current payable or receivable tax.................................................................................7

10. Differences in tax amount...........................................................................................8

11. Tax treatment..............................................................................................................8

Conclusion........................................................................................................................9

References.........................................................................................................................9

2

Contents

Introduction.......................................................................................................................3

Company overview...........................................................................................................3

1. Cash flow statement analysis........................................................................................3

2. Comparative analysis on cash flow statement..............................................................4

3. Comprehensive income statement analysis..................................................................5

4. Comprehensive income statement items......................................................................6

5. Reasons.........................................................................................................................6

6. Tax expenses of the company.......................................................................................6

7. Similarity in tax expenses.............................................................................................7

8. Deferred tax amount.....................................................................................................7

9. Current payable or receivable tax.................................................................................7

10. Differences in tax amount...........................................................................................8

11. Tax treatment..............................................................................................................8

Conclusion........................................................................................................................9

References.........................................................................................................................9

Corporate Accounting

3

Introduction:

Corporate accounting is an accounting branch which deals with the company’s

accounting process, preparation of final statement of the company and records all the

financial data of the company in proper way. In this report, accounting process of the Qantas

limited has been evaluated to measure the performance and the position of the company. The

main focus of the report is on the income statement, cash flow statement and the tax

treatment of the company. It identifies and measures the various values of the taxation in the

annual report of the comapny and identifies the tax recording process and the accounting

standards of the company.

Company overview:

Qantas limited is largest airline company in the Australian market. The company is

operating the activities through various subsidiaries companies such as Jetstar, Qantas

domestic airlines, Qantas international airlines etc. the company offers different deals and the

different services through its various subsidiary company. The company has diversified its

market at international level and currently, it is managing its business at around 65

destinations at international level (Our Company, 2018). The annual report (2017) of the

company explains that the company has followed AASB rules to record and perform the

accounting activities and process of the company.

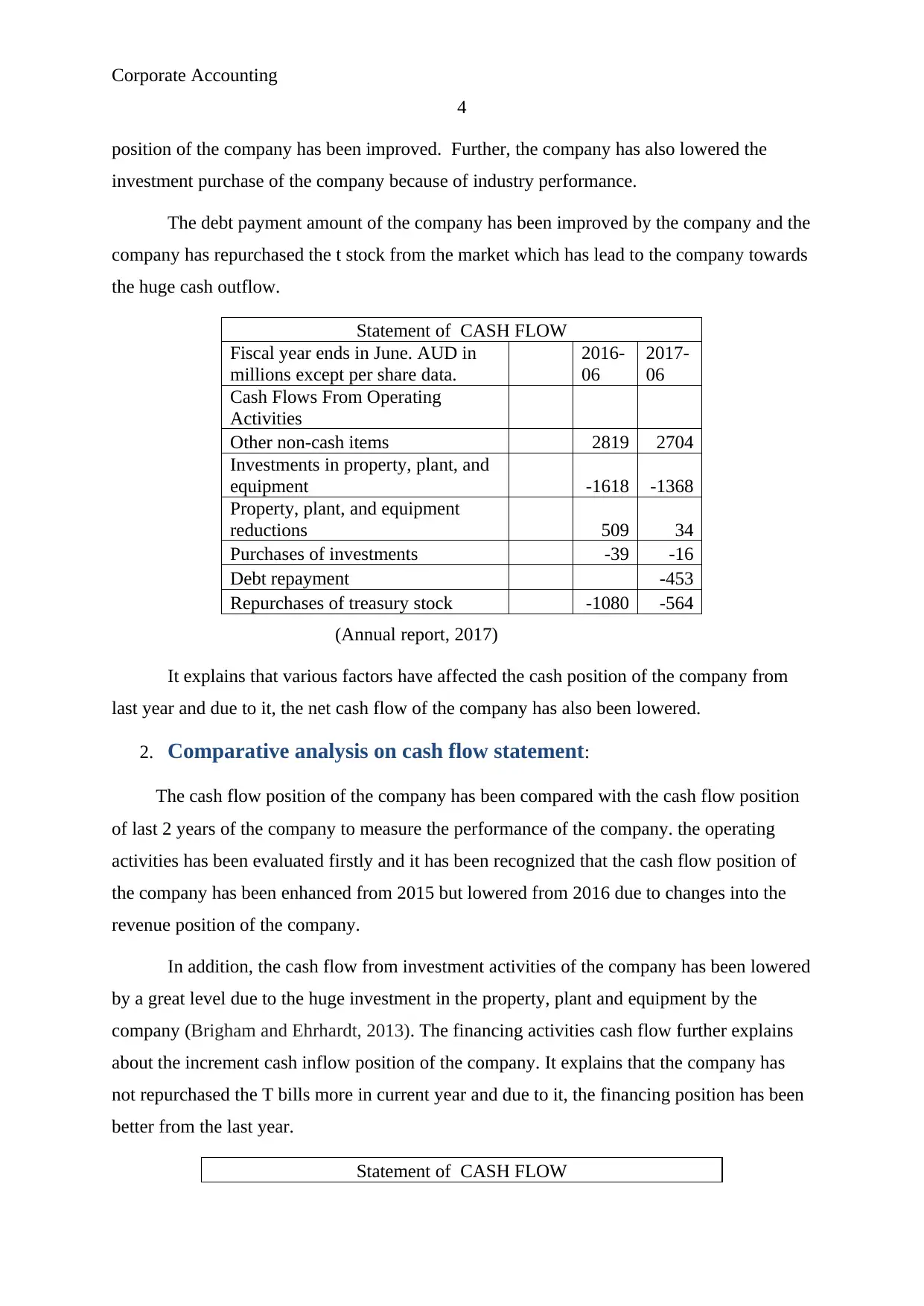

1. Cash flow statement analysis:

Cash flow statement is a financial statement which explains about the changes into the

cash flow of the company in a specific time period. It evaluates the changes in the cash

position of the comapny and explains about the liquidity position of the company to the

stakeholders of the company.

Annual report (2017) of the company explains that the cash flow position of the

company has been changed from 2016 to 2017. Firstly, it has been found that the revenues

and the non cash items of the company have affected the operating activities cash position of

the company. It explains that the cash position has been lowered due to higher cost of

revenue of the company (Tran, 2015).

In addition, the changes have been identified in the property, plant and equipment of

the company. The investment has been lowered by the company and due to it; the investment

3

Introduction:

Corporate accounting is an accounting branch which deals with the company’s

accounting process, preparation of final statement of the company and records all the

financial data of the company in proper way. In this report, accounting process of the Qantas

limited has been evaluated to measure the performance and the position of the company. The

main focus of the report is on the income statement, cash flow statement and the tax

treatment of the company. It identifies and measures the various values of the taxation in the

annual report of the comapny and identifies the tax recording process and the accounting

standards of the company.

Company overview:

Qantas limited is largest airline company in the Australian market. The company is

operating the activities through various subsidiaries companies such as Jetstar, Qantas

domestic airlines, Qantas international airlines etc. the company offers different deals and the

different services through its various subsidiary company. The company has diversified its

market at international level and currently, it is managing its business at around 65

destinations at international level (Our Company, 2018). The annual report (2017) of the

company explains that the company has followed AASB rules to record and perform the

accounting activities and process of the company.

1. Cash flow statement analysis:

Cash flow statement is a financial statement which explains about the changes into the

cash flow of the company in a specific time period. It evaluates the changes in the cash

position of the comapny and explains about the liquidity position of the company to the

stakeholders of the company.

Annual report (2017) of the company explains that the cash flow position of the

company has been changed from 2016 to 2017. Firstly, it has been found that the revenues

and the non cash items of the company have affected the operating activities cash position of

the company. It explains that the cash position has been lowered due to higher cost of

revenue of the company (Tran, 2015).

In addition, the changes have been identified in the property, plant and equipment of

the company. The investment has been lowered by the company and due to it; the investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

4

position of the company has been improved. Further, the company has also lowered the

investment purchase of the company because of industry performance.

The debt payment amount of the company has been improved by the company and the

company has repurchased the t stock from the market which has lead to the company towards

the huge cash outflow.

Statement of CASH FLOW

Fiscal year ends in June. AUD in

millions except per share data.

2016-

06

2017-

06

Cash Flows From Operating

Activities

Other non-cash items 2819 2704

Investments in property, plant, and

equipment -1618 -1368

Property, plant, and equipment

reductions 509 34

Purchases of investments -39 -16

Debt repayment -453

Repurchases of treasury stock -1080 -564

(Annual report, 2017)

It explains that various factors have affected the cash position of the company from

last year and due to it, the net cash flow of the company has also been lowered.

2. Comparative analysis on cash flow statement:

The cash flow position of the company has been compared with the cash flow position

of last 2 years of the company to measure the performance of the company. the operating

activities has been evaluated firstly and it has been recognized that the cash flow position of

the company has been enhanced from 2015 but lowered from 2016 due to changes into the

revenue position of the company.

In addition, the cash flow from investment activities of the company has been lowered

by a great level due to the huge investment in the property, plant and equipment by the

company (Brigham and Ehrhardt, 2013). The financing activities cash flow further explains

about the increment cash inflow position of the company. It explains that the company has

not repurchased the T bills more in current year and due to it, the financing position has been

better from the last year.

Statement of CASH FLOW

4

position of the company has been improved. Further, the company has also lowered the

investment purchase of the company because of industry performance.

The debt payment amount of the company has been improved by the company and the

company has repurchased the t stock from the market which has lead to the company towards

the huge cash outflow.

Statement of CASH FLOW

Fiscal year ends in June. AUD in

millions except per share data.

2016-

06

2017-

06

Cash Flows From Operating

Activities

Other non-cash items 2819 2704

Investments in property, plant, and

equipment -1618 -1368

Property, plant, and equipment

reductions 509 34

Purchases of investments -39 -16

Debt repayment -453

Repurchases of treasury stock -1080 -564

(Annual report, 2017)

It explains that various factors have affected the cash position of the company from

last year and due to it, the net cash flow of the company has also been lowered.

2. Comparative analysis on cash flow statement:

The cash flow position of the company has been compared with the cash flow position

of last 2 years of the company to measure the performance of the company. the operating

activities has been evaluated firstly and it has been recognized that the cash flow position of

the company has been enhanced from 2015 but lowered from 2016 due to changes into the

revenue position of the company.

In addition, the cash flow from investment activities of the company has been lowered

by a great level due to the huge investment in the property, plant and equipment by the

company (Brigham and Ehrhardt, 2013). The financing activities cash flow further explains

about the increment cash inflow position of the company. It explains that the company has

not repurchased the T bills more in current year and due to it, the financing position has been

better from the last year.

Statement of CASH FLOW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

5

Fiscal year ends in June. (Amt in AUD

million)

2015-

06

2016-

06

2017-

06

Net cash provided by operating activities 2048 2819 2704

Net cash used for investing activities -944 -1923 -2046

Net cash provided by (used for)

financing activities -1218 -1825 -854

Net change in cash -93 -928 -205

It further explains that due to total changes in all the activities of the cash flow

statement of the company, net changes in the cash flow have been improved.

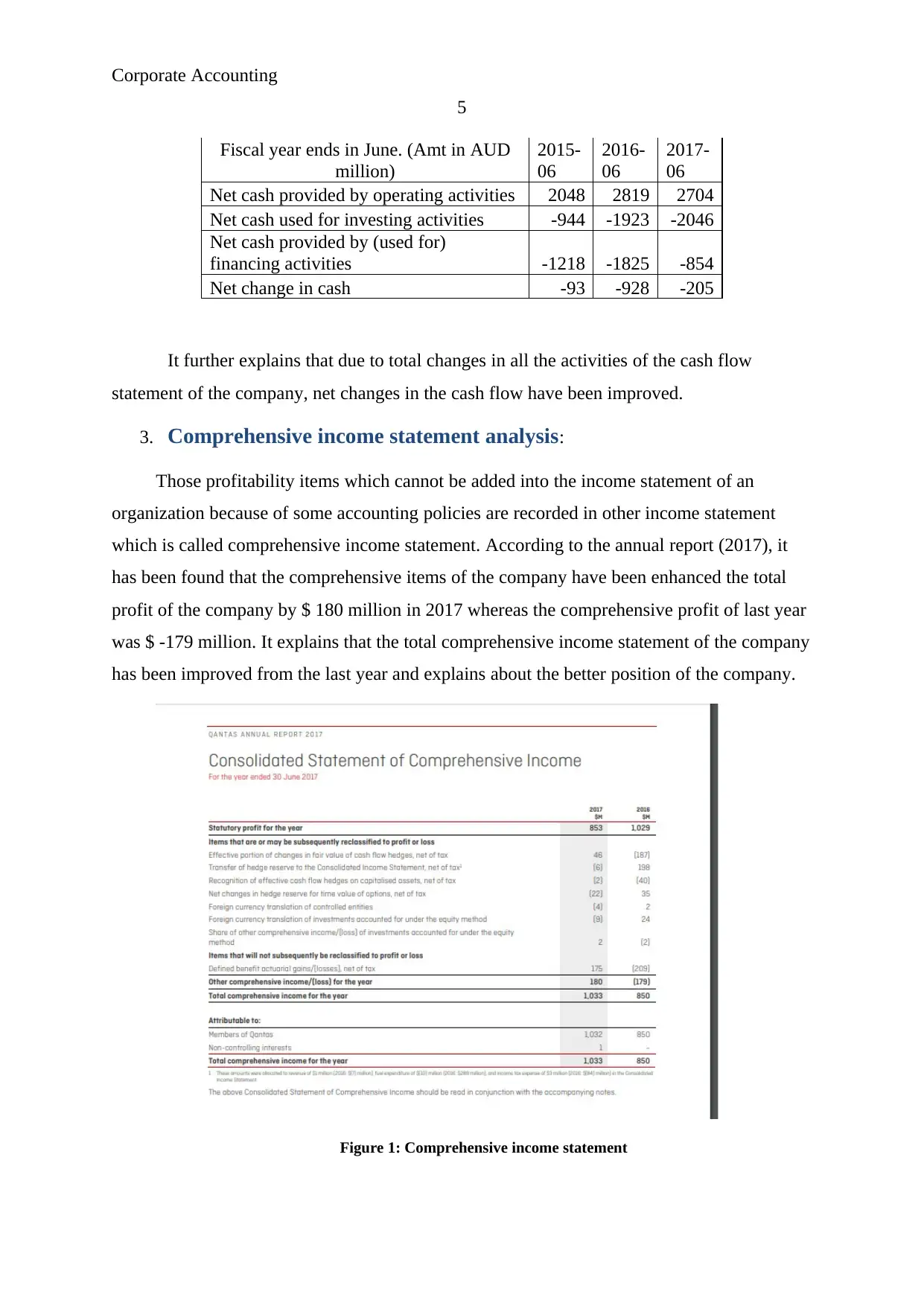

3. Comprehensive income statement analysis:

Those profitability items which cannot be added into the income statement of an

organization because of some accounting policies are recorded in other income statement

which is called comprehensive income statement. According to the annual report (2017), it

has been found that the comprehensive items of the company have been enhanced the total

profit of the company by $ 180 million in 2017 whereas the comprehensive profit of last year

was $ -179 million. It explains that the total comprehensive income statement of the company

has been improved from the last year and explains about the better position of the company.

Figure 1: Comprehensive income statement

5

Fiscal year ends in June. (Amt in AUD

million)

2015-

06

2016-

06

2017-

06

Net cash provided by operating activities 2048 2819 2704

Net cash used for investing activities -944 -1923 -2046

Net cash provided by (used for)

financing activities -1218 -1825 -854

Net change in cash -93 -928 -205

It further explains that due to total changes in all the activities of the cash flow

statement of the company, net changes in the cash flow have been improved.

3. Comprehensive income statement analysis:

Those profitability items which cannot be added into the income statement of an

organization because of some accounting policies are recorded in other income statement

which is called comprehensive income statement. According to the annual report (2017), it

has been found that the comprehensive items of the company have been enhanced the total

profit of the company by $ 180 million in 2017 whereas the comprehensive profit of last year

was $ -179 million. It explains that the total comprehensive income statement of the company

has been improved from the last year and explains about the better position of the company.

Figure 1: Comprehensive income statement

Corporate Accounting

6

(Annual report, 2017)

4. Comprehensive income statement items:

The main items of comprehensive income statement of the company is changes in the

fair value, net changes in the cash flow hedges, exchange rates, foreign currency investment,

loss of investment, taxation value etc. all of these factors are not related with the daily

activities and the operations of the company (Watson, 2017). These all factors are fluctuated

and cannot be recorded by the company in its annual reports because of some accounting

policies and the income statement preparation method.

5. Reasons:

On the basis of the study on comprehensive income statement and the items of

comprehensive income statement, it has been found that those profitability items which

cannot be added into the income statement of an organization because of materiality policies

and fair accounting policies are recorded in other income statement which is called

comprehensive income statement (Morris, 2017). The main reason behind not adding the

items in the income statement of the company is that these factors are not related to the

operating and non operating activities of the company and have been generated due to market

factors. Thus, it could affect the profitability level and manipulate the stakeholders of the

company.

6. Tax expenses of the company:

Tax expenses of the company have been evaluated further. Annual report (2017)

explains that the total tax expense of the company have been lowered from last year in 2017.

Tax expense explains about the total amount which has to pay from the accounting profit of

the company to the Australian government (Larson et al, 2017).

Particular( $ in millions) 2016 2017

Income tax expenses 395 328

6

(Annual report, 2017)

4. Comprehensive income statement items:

The main items of comprehensive income statement of the company is changes in the

fair value, net changes in the cash flow hedges, exchange rates, foreign currency investment,

loss of investment, taxation value etc. all of these factors are not related with the daily

activities and the operations of the company (Watson, 2017). These all factors are fluctuated

and cannot be recorded by the company in its annual reports because of some accounting

policies and the income statement preparation method.

5. Reasons:

On the basis of the study on comprehensive income statement and the items of

comprehensive income statement, it has been found that those profitability items which

cannot be added into the income statement of an organization because of materiality policies

and fair accounting policies are recorded in other income statement which is called

comprehensive income statement (Morris, 2017). The main reason behind not adding the

items in the income statement of the company is that these factors are not related to the

operating and non operating activities of the company and have been generated due to market

factors. Thus, it could affect the profitability level and manipulate the stakeholders of the

company.

6. Tax expenses of the company:

Tax expenses of the company have been evaluated further. Annual report (2017)

explains that the total tax expense of the company have been lowered from last year in 2017.

Tax expense explains about the total amount which has to pay from the accounting profit of

the company to the Australian government (Larson et al, 2017).

Particular( $ in millions) 2016 2017

Income tax expenses 395 328

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

7

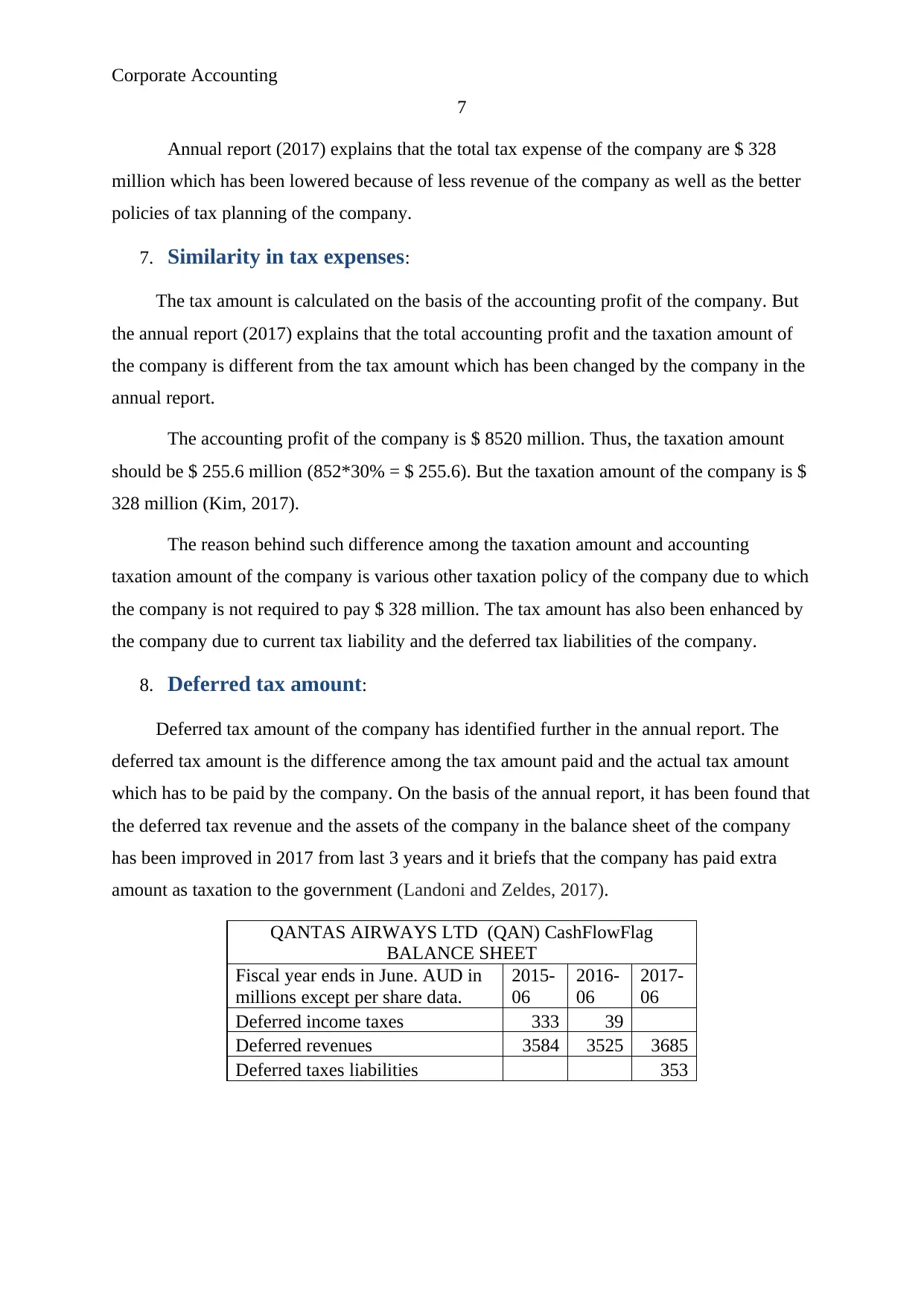

Annual report (2017) explains that the total tax expense of the company are $ 328

million which has been lowered because of less revenue of the company as well as the better

policies of tax planning of the company.

7. Similarity in tax expenses:

The tax amount is calculated on the basis of the accounting profit of the company. But

the annual report (2017) explains that the total accounting profit and the taxation amount of

the company is different from the tax amount which has been changed by the company in the

annual report.

The accounting profit of the company is $ 8520 million. Thus, the taxation amount

should be $ 255.6 million (852*30% = $ 255.6). But the taxation amount of the company is $

328 million (Kim, 2017).

The reason behind such difference among the taxation amount and accounting

taxation amount of the company is various other taxation policy of the company due to which

the company is not required to pay $ 328 million. The tax amount has also been enhanced by

the company due to current tax liability and the deferred tax liabilities of the company.

8. Deferred tax amount:

Deferred tax amount of the company has identified further in the annual report. The

deferred tax amount is the difference among the tax amount paid and the actual tax amount

which has to be paid by the company. On the basis of the annual report, it has been found that

the deferred tax revenue and the assets of the company in the balance sheet of the company

has been improved in 2017 from last 3 years and it briefs that the company has paid extra

amount as taxation to the government (Landoni and Zeldes, 2017).

QANTAS AIRWAYS LTD (QAN) CashFlowFlag

BALANCE SHEET

Fiscal year ends in June. AUD in

millions except per share data.

2015-

06

2016-

06

2017-

06

Deferred income taxes 333 39

Deferred revenues 3584 3525 3685

Deferred taxes liabilities 353

7

Annual report (2017) explains that the total tax expense of the company are $ 328

million which has been lowered because of less revenue of the company as well as the better

policies of tax planning of the company.

7. Similarity in tax expenses:

The tax amount is calculated on the basis of the accounting profit of the company. But

the annual report (2017) explains that the total accounting profit and the taxation amount of

the company is different from the tax amount which has been changed by the company in the

annual report.

The accounting profit of the company is $ 8520 million. Thus, the taxation amount

should be $ 255.6 million (852*30% = $ 255.6). But the taxation amount of the company is $

328 million (Kim, 2017).

The reason behind such difference among the taxation amount and accounting

taxation amount of the company is various other taxation policy of the company due to which

the company is not required to pay $ 328 million. The tax amount has also been enhanced by

the company due to current tax liability and the deferred tax liabilities of the company.

8. Deferred tax amount:

Deferred tax amount of the company has identified further in the annual report. The

deferred tax amount is the difference among the tax amount paid and the actual tax amount

which has to be paid by the company. On the basis of the annual report, it has been found that

the deferred tax revenue and the assets of the company in the balance sheet of the company

has been improved in 2017 from last 3 years and it briefs that the company has paid extra

amount as taxation to the government (Landoni and Zeldes, 2017).

QANTAS AIRWAYS LTD (QAN) CashFlowFlag

BALANCE SHEET

Fiscal year ends in June. AUD in

millions except per share data.

2015-

06

2016-

06

2017-

06

Deferred income taxes 333 39

Deferred revenues 3584 3525 3685

Deferred taxes liabilities 353

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

8

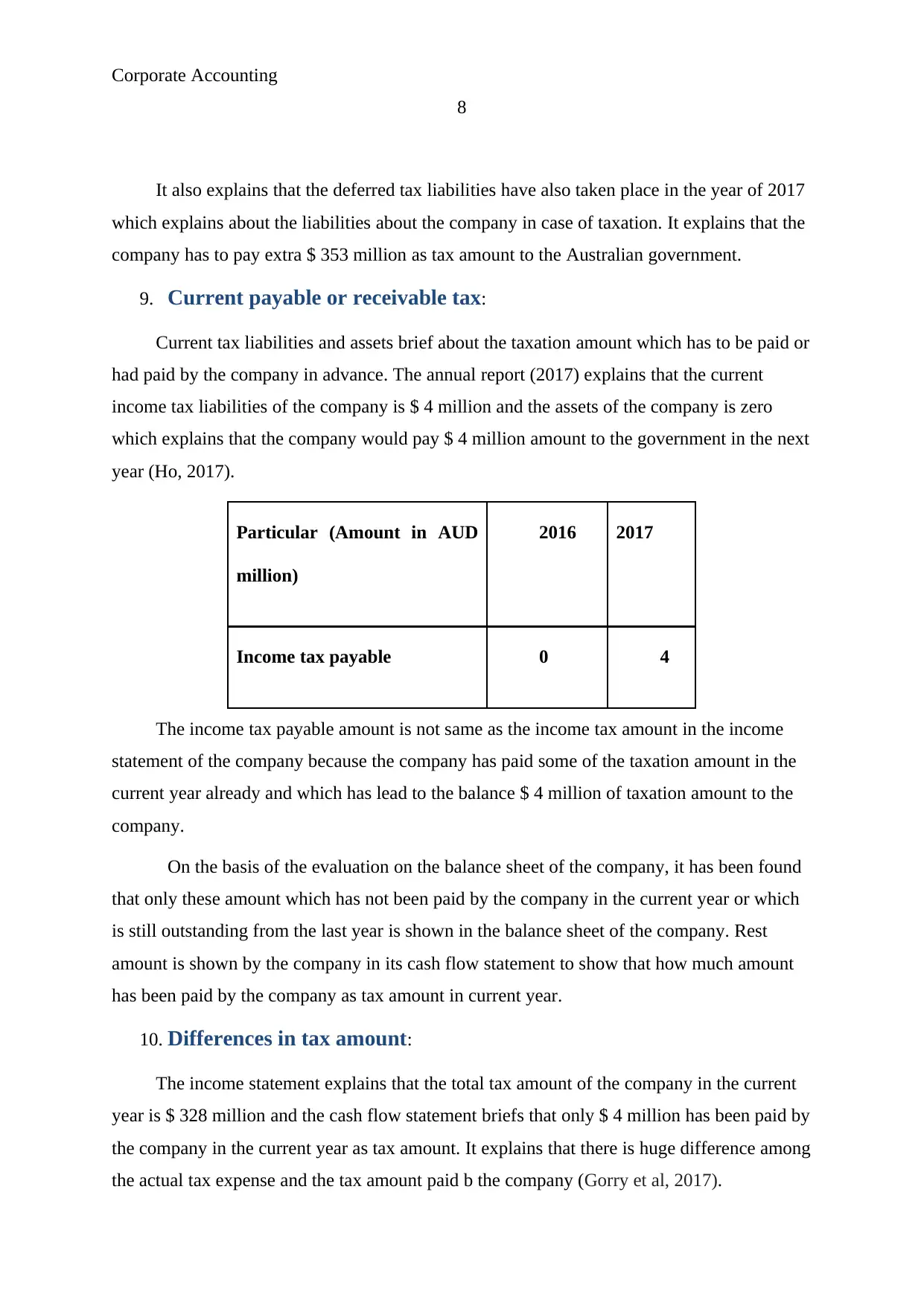

It also explains that the deferred tax liabilities have also taken place in the year of 2017

which explains about the liabilities about the company in case of taxation. It explains that the

company has to pay extra $ 353 million as tax amount to the Australian government.

9. Current payable or receivable tax:

Current tax liabilities and assets brief about the taxation amount which has to be paid or

had paid by the company in advance. The annual report (2017) explains that the current

income tax liabilities of the company is $ 4 million and the assets of the company is zero

which explains that the company would pay $ 4 million amount to the government in the next

year (Ho, 2017).

Particular (Amount in AUD

million)

2016 2017

Income tax payable 0 4

The income tax payable amount is not same as the income tax amount in the income

statement of the company because the company has paid some of the taxation amount in the

current year already and which has lead to the balance $ 4 million of taxation amount to the

company.

On the basis of the evaluation on the balance sheet of the company, it has been found

that only these amount which has not been paid by the company in the current year or which

is still outstanding from the last year is shown in the balance sheet of the company. Rest

amount is shown by the company in its cash flow statement to show that how much amount

has been paid by the company as tax amount in current year.

10. Differences in tax amount:

The income statement explains that the total tax amount of the company in the current

year is $ 328 million and the cash flow statement briefs that only $ 4 million has been paid by

the company in the current year as tax amount. It explains that there is huge difference among

the actual tax expense and the tax amount paid b the company (Gorry et al, 2017).

8

It also explains that the deferred tax liabilities have also taken place in the year of 2017

which explains about the liabilities about the company in case of taxation. It explains that the

company has to pay extra $ 353 million as tax amount to the Australian government.

9. Current payable or receivable tax:

Current tax liabilities and assets brief about the taxation amount which has to be paid or

had paid by the company in advance. The annual report (2017) explains that the current

income tax liabilities of the company is $ 4 million and the assets of the company is zero

which explains that the company would pay $ 4 million amount to the government in the next

year (Ho, 2017).

Particular (Amount in AUD

million)

2016 2017

Income tax payable 0 4

The income tax payable amount is not same as the income tax amount in the income

statement of the company because the company has paid some of the taxation amount in the

current year already and which has lead to the balance $ 4 million of taxation amount to the

company.

On the basis of the evaluation on the balance sheet of the company, it has been found

that only these amount which has not been paid by the company in the current year or which

is still outstanding from the last year is shown in the balance sheet of the company. Rest

amount is shown by the company in its cash flow statement to show that how much amount

has been paid by the company as tax amount in current year.

10. Differences in tax amount:

The income statement explains that the total tax amount of the company in the current

year is $ 328 million and the cash flow statement briefs that only $ 4 million has been paid by

the company in the current year as tax amount. It explains that there is huge difference among

the actual tax expense and the tax amount paid b the company (Gorry et al, 2017).

Corporate Accounting

9

These changes have taken place due to various internal reasons of the company such

as company has already paid extra amount to the government of the country and it is recoded

as deferred tax assets in the annual report of the company (Bardley, 2017). So, the company

has paid only $ 4 million in the current year.

11. Tax treatment:

The annual report explains that the treatment of the tax has been done in a better way

by the company. The tax treatment of the company explains that the company has followed

the ASSB 112 rules to record the taxation amount in the annual report of the company.

The above study was quite interesting due to the various taxation figures and their

different recording system. Every taxation figures have a note attached to it about it’s derive

and the reasons behind the figures,

The story was quite interesting because of various surprising elements. Various new

things have been learnt in the report and it has been found that how the different amount of

the taxation could is recorded in the annual report of the company.

Further, the main confusing point in the report was the deferred tax liabilities and the

current tax payable figures and the main difference among both the factors.

Conclusion:

To conclude, the Qantas limited has followed the international accounting rules and

AASB rules to measure the performance and the position of the company. It explains that the

company has performed a better process in recording and presenting the accounting and

financial transactions of the company in the annual report.

9

These changes have taken place due to various internal reasons of the company such

as company has already paid extra amount to the government of the country and it is recoded

as deferred tax assets in the annual report of the company (Bardley, 2017). So, the company

has paid only $ 4 million in the current year.

11. Tax treatment:

The annual report explains that the treatment of the tax has been done in a better way

by the company. The tax treatment of the company explains that the company has followed

the ASSB 112 rules to record the taxation amount in the annual report of the company.

The above study was quite interesting due to the various taxation figures and their

different recording system. Every taxation figures have a note attached to it about it’s derive

and the reasons behind the figures,

The story was quite interesting because of various surprising elements. Various new

things have been learnt in the report and it has been found that how the different amount of

the taxation could is recorded in the annual report of the company.

Further, the main confusing point in the report was the deferred tax liabilities and the

current tax payable figures and the main difference among both the factors.

Conclusion:

To conclude, the Qantas limited has followed the international accounting rules and

AASB rules to measure the performance and the position of the company. It explains that the

company has performed a better process in recording and presenting the accounting and

financial transactions of the company in the annual report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Corporate Accounting

10

References:

Annual report. 2017. Qantas Airways limited. (Online). Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/AH_NGR9NxUaXc0W8Qv3Kf

g/docs/QantasAnnualReport2017.pdf (accessed 24/5/18).

Bradley, S., 2017. Inattention to Deferred Increases in Tax Bases: How Michigan Home

Buyers Are Paying for Assessment Limits. Review of Economics and Statistics, 99(1), pp.53-

66.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Gorry, A., Hassett, K.A., Hubbard, R.G. and Mathur, A., 2017. The response of deferred

executive compensation to changes in tax rates. Journal of Public Economics, 151, pp.28-40.

Ho, A.T., 2017. Tax-deferred saving accounts: Heterogeneity and policy reforms. European

Economic Review, 97, pp.26-41.

Kim, J.H., 2017. What Really Determines the Information Content of Tax Expense and

Deferred Tax?. 회회회회회, 42(2), pp.1-44.

Landoni, M. and Zeldes, S.P., 2017. Should the government be paying investment fees on $3

trillion of tax-deferred retirement assets?

Larson, M.P., Lewis, T.K. and Spilker, B.C., 2017. A Case Integrating Financial and Tax

Accounting Using the Balance Sheet Approach to Account for Income Taxes. Issues in

Accounting Education, 32(4), pp.41-49.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplication. Journal of Accounting and

Finance, 17(8), pp.198-208.

Our company. 2017. Qantas Airways limited. (online). Available at:

https://www.qantas.com/travel/airlines/company/global/en (accessed 24/5/18).

10

References:

Annual report. 2017. Qantas Airways limited. (Online). Available at:

http://investor.qantas.com/FormBuilder/_Resource/_module/AH_NGR9NxUaXc0W8Qv3Kf

g/docs/QantasAnnualReport2017.pdf (accessed 24/5/18).

Bradley, S., 2017. Inattention to Deferred Increases in Tax Bases: How Michigan Home

Buyers Are Paying for Assessment Limits. Review of Economics and Statistics, 99(1), pp.53-

66.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice.

Cengage Learning.

Gorry, A., Hassett, K.A., Hubbard, R.G. and Mathur, A., 2017. The response of deferred

executive compensation to changes in tax rates. Journal of Public Economics, 151, pp.28-40.

Ho, A.T., 2017. Tax-deferred saving accounts: Heterogeneity and policy reforms. European

Economic Review, 97, pp.26-41.

Kim, J.H., 2017. What Really Determines the Information Content of Tax Expense and

Deferred Tax?. 회회회회회, 42(2), pp.1-44.

Landoni, M. and Zeldes, S.P., 2017. Should the government be paying investment fees on $3

trillion of tax-deferred retirement assets?

Larson, M.P., Lewis, T.K. and Spilker, B.C., 2017. A Case Integrating Financial and Tax

Accounting Using the Balance Sheet Approach to Account for Income Taxes. Issues in

Accounting Education, 32(4), pp.41-49.

Morris, J.L., 2017. Classification of Deferred Tax Assets and Deferred Tax Liabilities: An

Evaluation of FASB's Attempt at Standards Simplication. Journal of Accounting and

Finance, 17(8), pp.198-208.

Our company. 2017. Qantas Airways limited. (online). Available at:

https://www.qantas.com/travel/airlines/company/global/en (accessed 24/5/18).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Corporate Accounting

11

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia?. Browser Download This Paper.

Watson, L. 2017. Discussion of'Does the Deferred Tax Asset Valuation Allowance Signal

Firm Creditworthiness?'.

11

Tran, A., 2015. Can taxable income be estimated from financial reports of listed companies in

Australia?. Browser Download This Paper.

Watson, L. 2017. Discussion of'Does the Deferred Tax Asset Valuation Allowance Signal

Firm Creditworthiness?'.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.