Corporate Accounting Analysis of Qantas and Sydney Airport (HI5020)

VerifiedAdded on 2022/11/14

|48

|4077

|465

Report

AI Summary

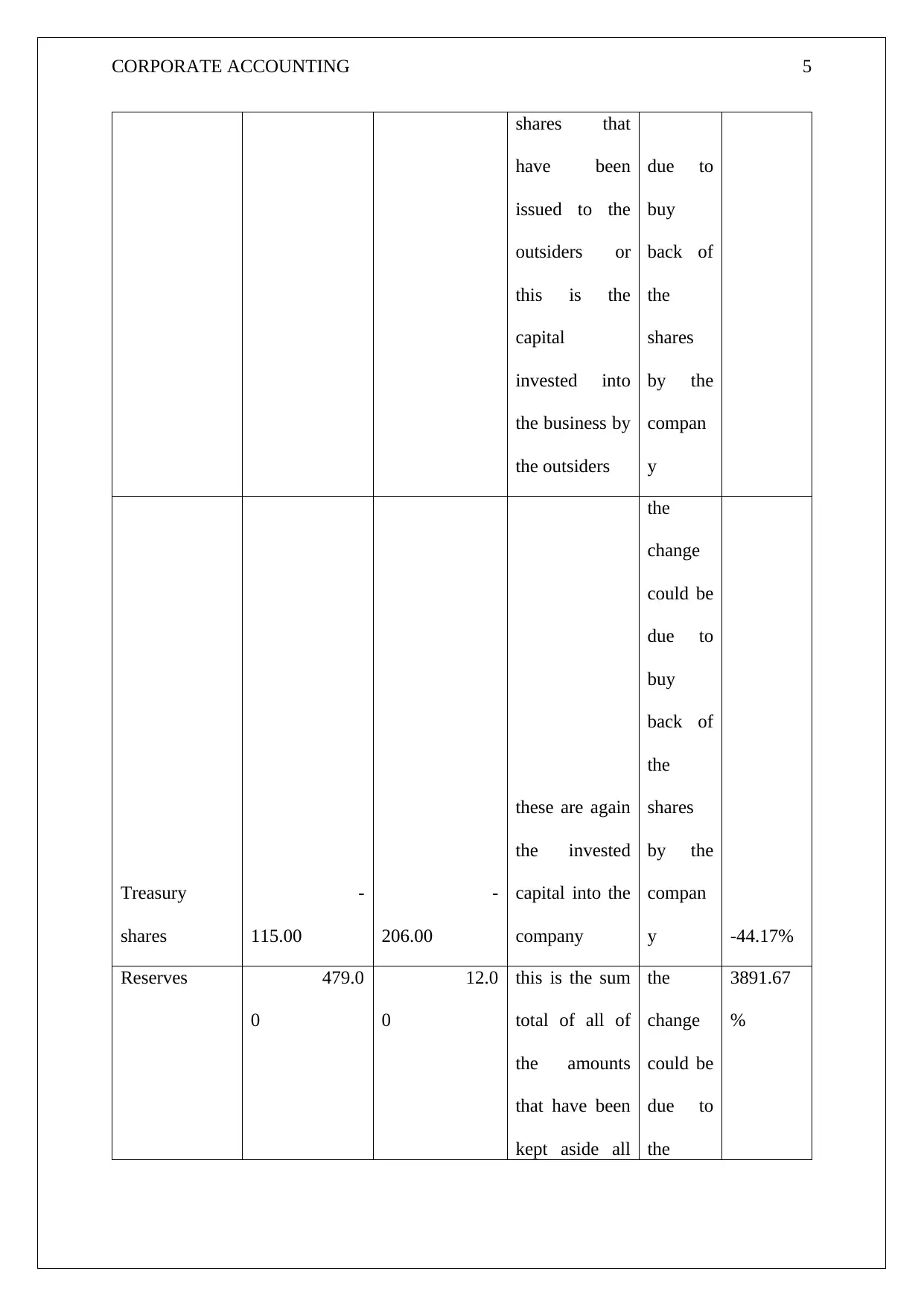

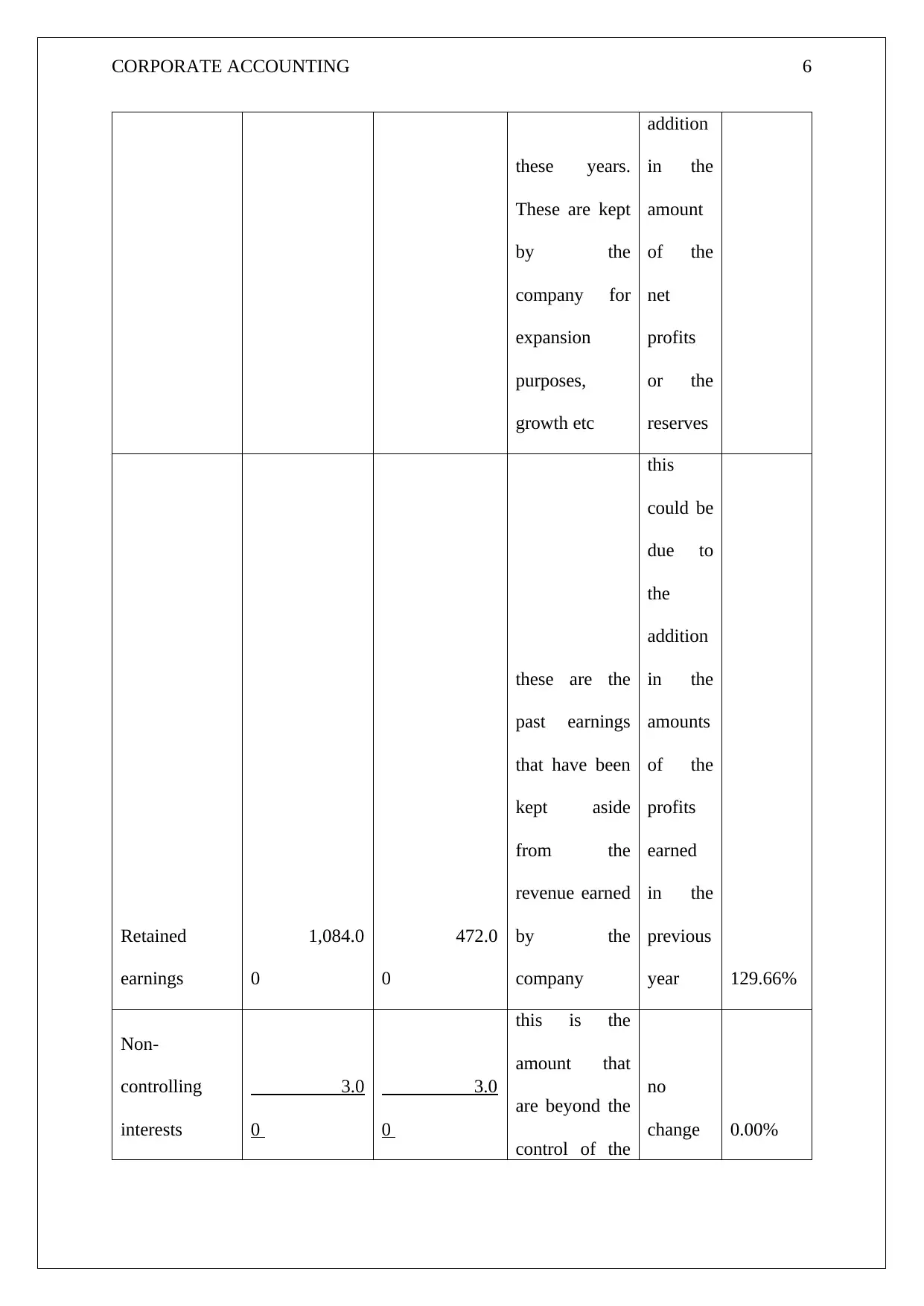

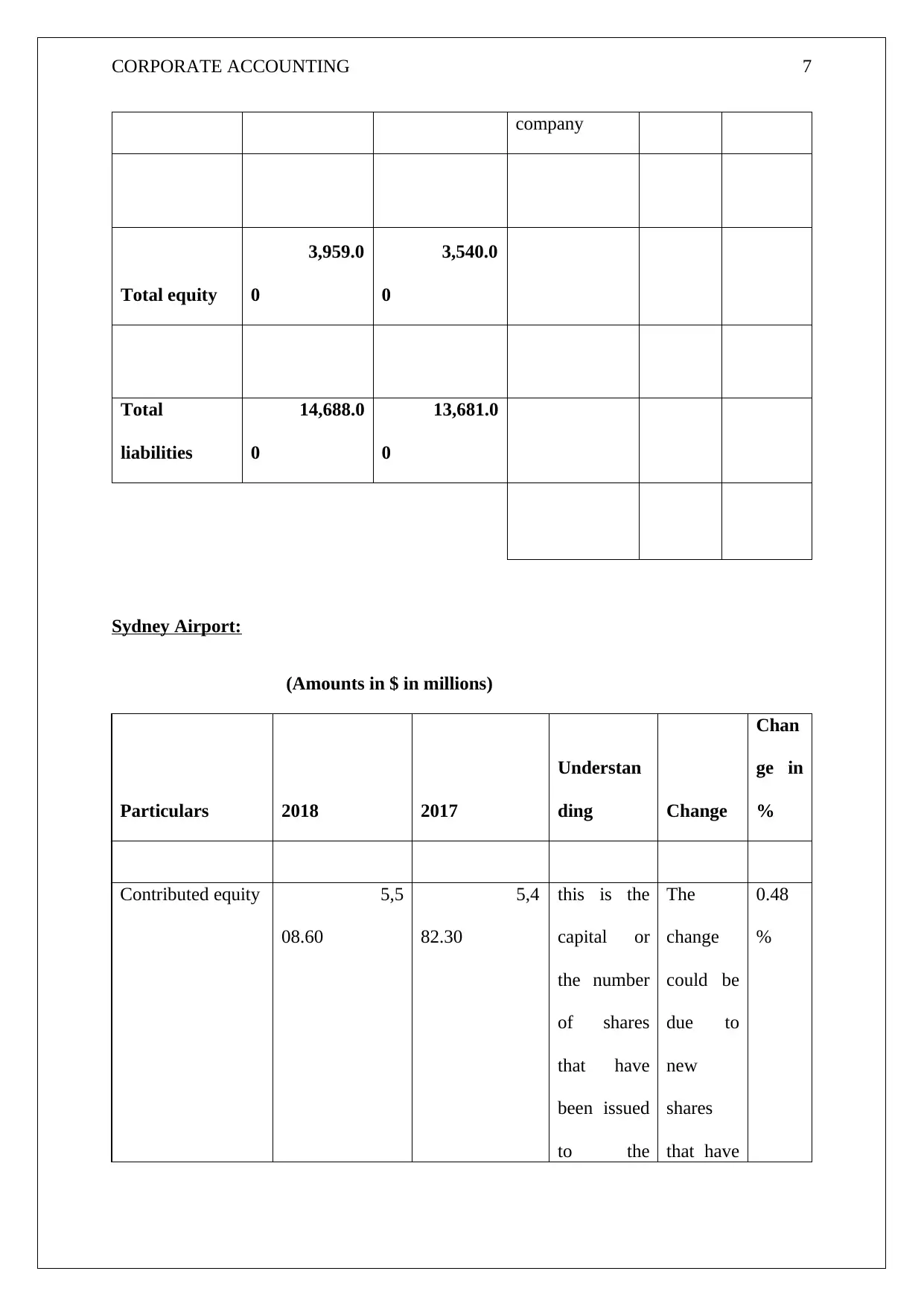

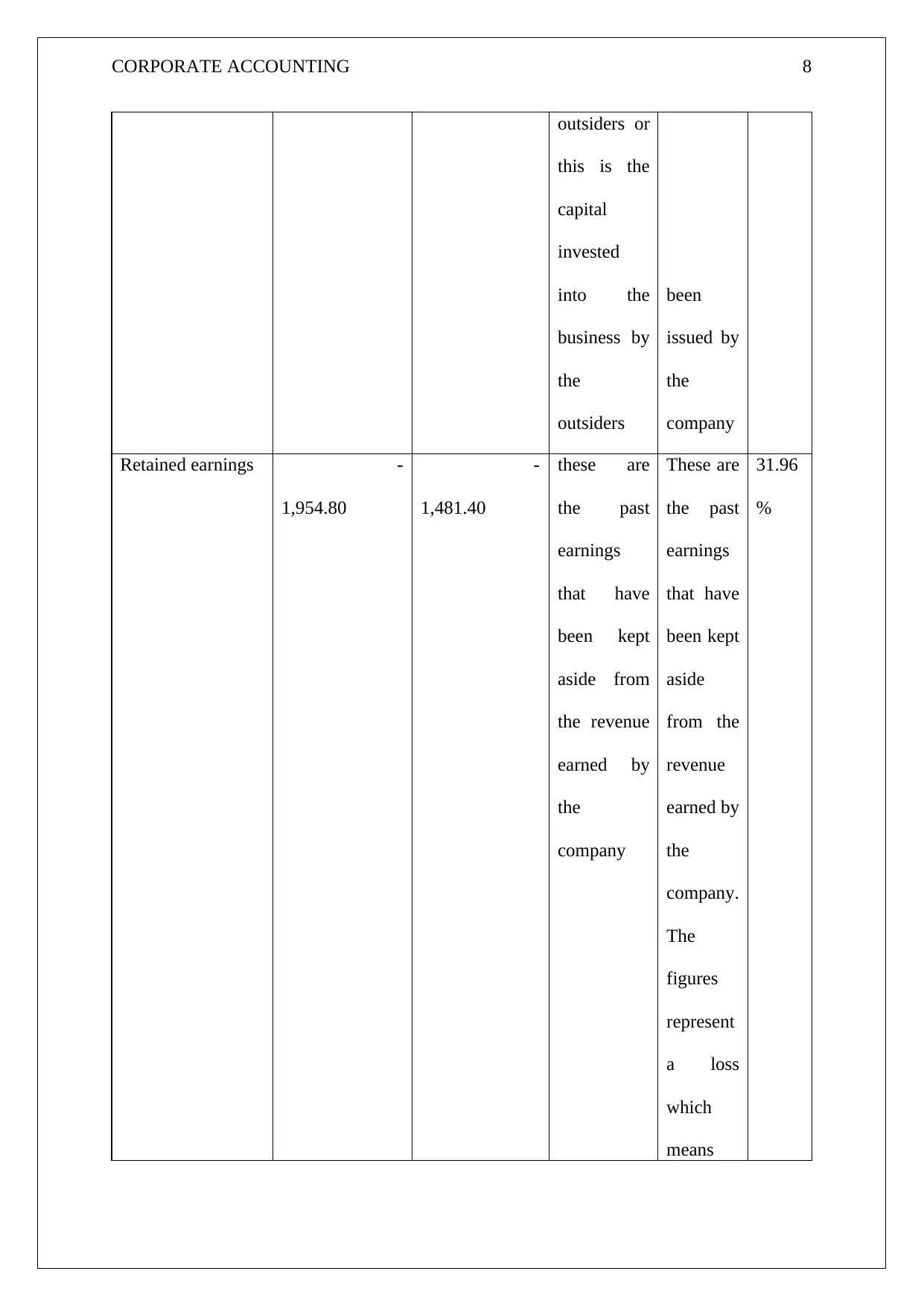

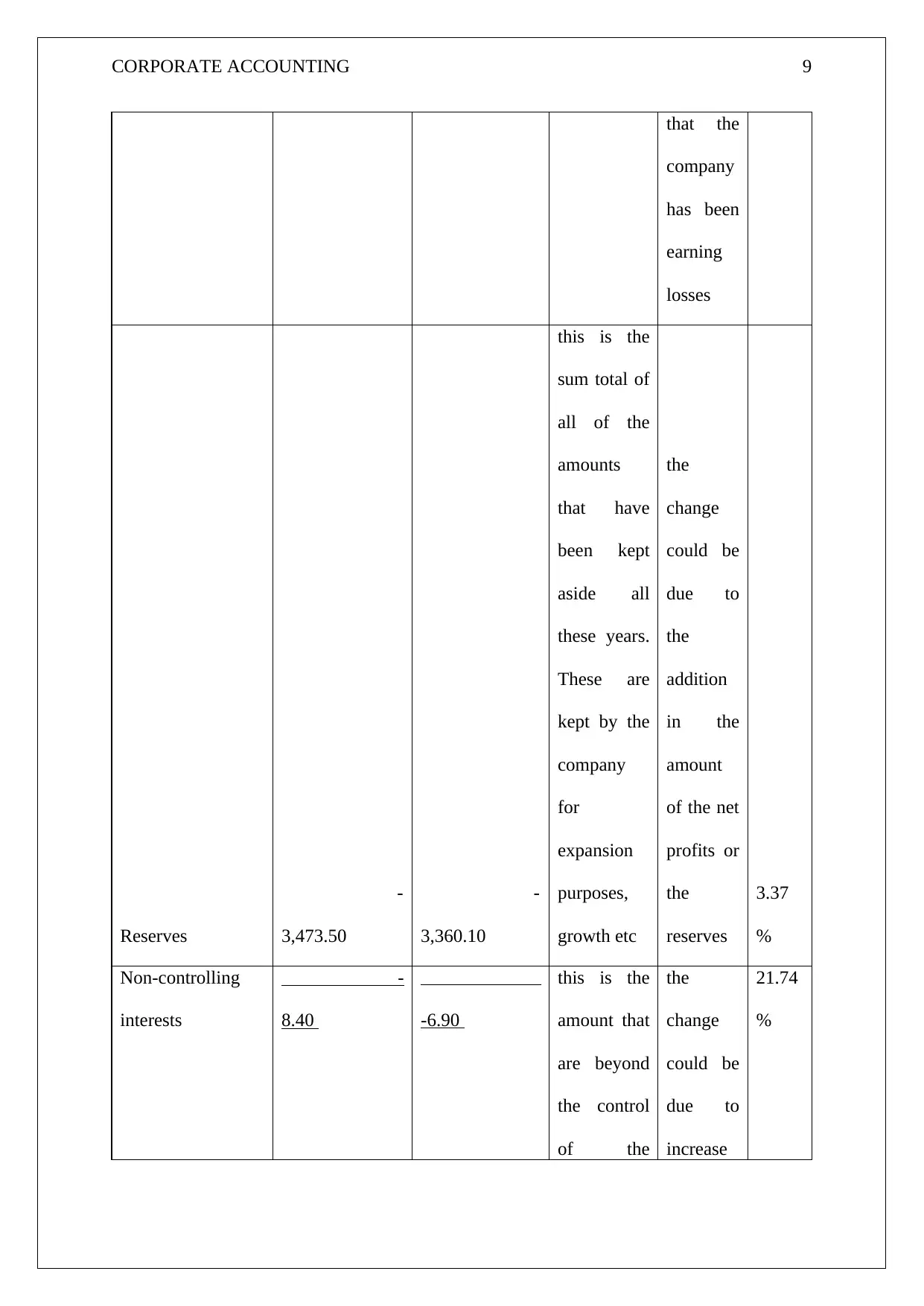

This report presents a comprehensive analysis of the financial performance of two Australian Securities Exchange (ASX) listed companies: Qantas and Sydney Airport, both operating within the airline industry. The report delves into the companies' financial positions by examining their cash flow statements, owners' equity, and statements of comprehensive income. It includes detailed breakdowns of key financial metrics such as issued capital, retained earnings, cash receipts, and payments. The analysis compares the financial data of both companies for the years 2017 and 2018, providing insights into changes and trends. The report aims to offer a clear understanding of the financial health and operational performance of Qantas and Sydney Airport. This document is available on Desklib, a platform providing students with study resources, including past papers and solved assignments.

1 out of 48

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.