Financial Management: Qantas Airways Turnaround Story Analysis Report

VerifiedAdded on 2020/03/01

|10

|3335

|60

Report

AI Summary

This report provides a comprehensive financial analysis of Qantas Airways, focusing on its turnaround story over the last five years. It begins with an executive summary and an introduction to Qantas' operations, including its domestic and international routes and its subsidiary brands like Jetstar. The analysis delves into the company's income statement, balance sheet, and cash flow statement, highlighting key trends such as muted revenue growth, improved EBITDA margins, and decreasing debt. Ratio analysis, including return on equity, return on sales, and gearing ratio, is used to assess financial performance. The report also examines the future of the business, emphasizing the impact of cost-cutting measures, fuel prices, and competition. Ethical considerations of insolvency and the influence of the political environment, including environmental taxes and currency rates, are discussed. The report concludes with recommendations for investing in Qantas stock, based on the financial analysis and future outlook.

FINANCIAL MANAGEMENT

QANTAS – A Turnaround Story

STUDENT ID:

[Pick the date]

QANTAS – A Turnaround Story

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

Executive Summary

Qantas is the national carrier of Australia and along with Jetstar operates domestic and

international flights. The objective of the given report is to critically analyse the financial

statements using ratio analysis and trend analysis in order to understand the financial

performance of the company in the last five years. Further, the report aims to picture the

likely future performance of the company based on current turnaround in the company. Also,

the report highlights the ethical implications of bankruptcy along with potential external

factors for mergers and acquisitions in the context of Qantas. Lastly, the role of the political

environment in the context of airline industry and more specific Qantas has also been

highlighted. Based on the above discussion, recommendation has been provided with regards

to investing in the Qantas stock.

Introduction

Qantas Airways Limited (QAN) is a well-known Australian air transportation company.

Qantas is a listed company on ASX which operates on both international as well as domestic

routes with revenue almost equally divided between the two. The strength of the workforce is

nearly 28,000 who are predominantly working in Australia. The Chairman of Qantas Airways

Limited is Mr. Leigh Clifford and Chief Executive of the company is Mr. Alan Joyce. The

main headquarters of Qantas is located in New South Wale Australia. In the year 2016, the

total revenue of Qantas Airways Limited was $16,490 million (including other and sales

revenues). Till now, the company has owned fleet of 299 aircrafts which includes 11 fulltime

freighters aircrafts. The main airlines brands of Qantas are Jetstar and Qantas. However,

company also operates other businesses and airlines such as Q-Catering, Qantas freight,

Qantas frequent flyer (Qantas, 2016).

Jetstar – Domestic and internationals routes mainly in Australia, Japan and New Zealand.

Approximately, 4000 flights in single week to more than 60 destinations across 17 countries

(IBIS, 2017b).

Qantas – Huge network of domestic and international flights with four travel classes. Full

domestic network makes it more of a regional airline in Australia. Nearly, 2000 flights in a

single week (IBIS, 2017b).

Q- Catering – Snap fresh and Q- catering which run nearly five catering and food

service/production centres in Australia. (IBIS, 2017b).

Executive Summary

Qantas is the national carrier of Australia and along with Jetstar operates domestic and

international flights. The objective of the given report is to critically analyse the financial

statements using ratio analysis and trend analysis in order to understand the financial

performance of the company in the last five years. Further, the report aims to picture the

likely future performance of the company based on current turnaround in the company. Also,

the report highlights the ethical implications of bankruptcy along with potential external

factors for mergers and acquisitions in the context of Qantas. Lastly, the role of the political

environment in the context of airline industry and more specific Qantas has also been

highlighted. Based on the above discussion, recommendation has been provided with regards

to investing in the Qantas stock.

Introduction

Qantas Airways Limited (QAN) is a well-known Australian air transportation company.

Qantas is a listed company on ASX which operates on both international as well as domestic

routes with revenue almost equally divided between the two. The strength of the workforce is

nearly 28,000 who are predominantly working in Australia. The Chairman of Qantas Airways

Limited is Mr. Leigh Clifford and Chief Executive of the company is Mr. Alan Joyce. The

main headquarters of Qantas is located in New South Wale Australia. In the year 2016, the

total revenue of Qantas Airways Limited was $16,490 million (including other and sales

revenues). Till now, the company has owned fleet of 299 aircrafts which includes 11 fulltime

freighters aircrafts. The main airlines brands of Qantas are Jetstar and Qantas. However,

company also operates other businesses and airlines such as Q-Catering, Qantas freight,

Qantas frequent flyer (Qantas, 2016).

Jetstar – Domestic and internationals routes mainly in Australia, Japan and New Zealand.

Approximately, 4000 flights in single week to more than 60 destinations across 17 countries

(IBIS, 2017b).

Qantas – Huge network of domestic and international flights with four travel classes. Full

domestic network makes it more of a regional airline in Australia. Nearly, 2000 flights in a

single week (IBIS, 2017b).

Q- Catering – Snap fresh and Q- catering which run nearly five catering and food

service/production centres in Australia. (IBIS, 2017b).

Financial Management

Qantas frequent flyer –One of the imperative program of Qantas which is based on loyalty of

more than 10 million users (IBIS, 2017b).

Analysis of Financial Statements

There are three main financial statements namely the income statement, balance sheet and

cash flow statement which need to be analysed in order to provide a glimpse about the overall

financial position and operational performance of the selected company.

Income Statement

Based on the income statement of the last five years, it is apparent that the revenue growth

has been rather muted due to which there is negligible top line growth. This may be attributed

to the fierce competition that the company faces in both domestic and international flights. In

domestic flights, the company faces high competition from Virgin Australia and hence the

company has actively focused on increasing flight capacity and market share. Going forward

also revenue growth is not expected in this sector. In international travel, the company faces

competition from various international players particularly Emirates which is responsible for

muted topline (Qantas, 2014). With regards to operating profits, it is apparent that 2014 was a

particularly difficult year for the company since the company reported huge losses and also

asked for government support. However, the EBITDA margins of the company have

continuously improved which augers well for the business especially when topline growth is

absent. This improvement in topline may be attributed to the transformation program

undertaken by the company to rationalise costs and because of the declining fuel costs. After

reporting a net loss of $ 2.84 billion in FY2014, the company has turned around to report a

profit after tax of $ 0.58 billion and $ 1.03 billion in FY2015 and FY2016 respectively

(Qantas, 2016).

Balance Sheet

With regards to balance sheet, a noticeable trend has been the decrease in short term and long

term borrowings over the years which augers well for the company especially at a time when

the company is upgrading the fleet to increase capacity and improve services. Also, it is

noticeable that in FY2016, there is a decrease in the share capital caused due to the share

buyback announced by the company (Qantas, 2016). Further, owing to a huge loss in

FY2014, the retained earnings of the company even in FY2016 continue to be negative,

however with high earnings in both FY2015 and FY2016, the losses have been largely

Qantas frequent flyer –One of the imperative program of Qantas which is based on loyalty of

more than 10 million users (IBIS, 2017b).

Analysis of Financial Statements

There are three main financial statements namely the income statement, balance sheet and

cash flow statement which need to be analysed in order to provide a glimpse about the overall

financial position and operational performance of the selected company.

Income Statement

Based on the income statement of the last five years, it is apparent that the revenue growth

has been rather muted due to which there is negligible top line growth. This may be attributed

to the fierce competition that the company faces in both domestic and international flights. In

domestic flights, the company faces high competition from Virgin Australia and hence the

company has actively focused on increasing flight capacity and market share. Going forward

also revenue growth is not expected in this sector. In international travel, the company faces

competition from various international players particularly Emirates which is responsible for

muted topline (Qantas, 2014). With regards to operating profits, it is apparent that 2014 was a

particularly difficult year for the company since the company reported huge losses and also

asked for government support. However, the EBITDA margins of the company have

continuously improved which augers well for the business especially when topline growth is

absent. This improvement in topline may be attributed to the transformation program

undertaken by the company to rationalise costs and because of the declining fuel costs. After

reporting a net loss of $ 2.84 billion in FY2014, the company has turned around to report a

profit after tax of $ 0.58 billion and $ 1.03 billion in FY2015 and FY2016 respectively

(Qantas, 2016).

Balance Sheet

With regards to balance sheet, a noticeable trend has been the decrease in short term and long

term borrowings over the years which augers well for the company especially at a time when

the company is upgrading the fleet to increase capacity and improve services. Also, it is

noticeable that in FY2016, there is a decrease in the share capital caused due to the share

buyback announced by the company (Qantas, 2016). Further, owing to a huge loss in

FY2014, the retained earnings of the company even in FY2016 continue to be negative,

however with high earnings in both FY2015 and FY2016, the losses have been largely

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

nullified and it is expected that in FY2017, a positive retained earnings should be reported

(Qantas, 2016).

Cash Flow Statement

Over the last five years (barring FY2014), there has been an increase in the operating cash

flow which is a positive trend for the company. The cash outflow in investing activities has

shown significant jump in FY2016 as compared to the previous years and $ 778 million is on

account of aircraft refinancing which augers well for the company going ahead (Qantas,

2016). With regards to financing, it is a good sign for the company that the cash flow from

financing activities is negative in all the last five years except in FY2014. This indicates

commitment on the part of the company so as to reduce the debt through various refinancing

arrangements and better earnings (Petty et. al., 2012).

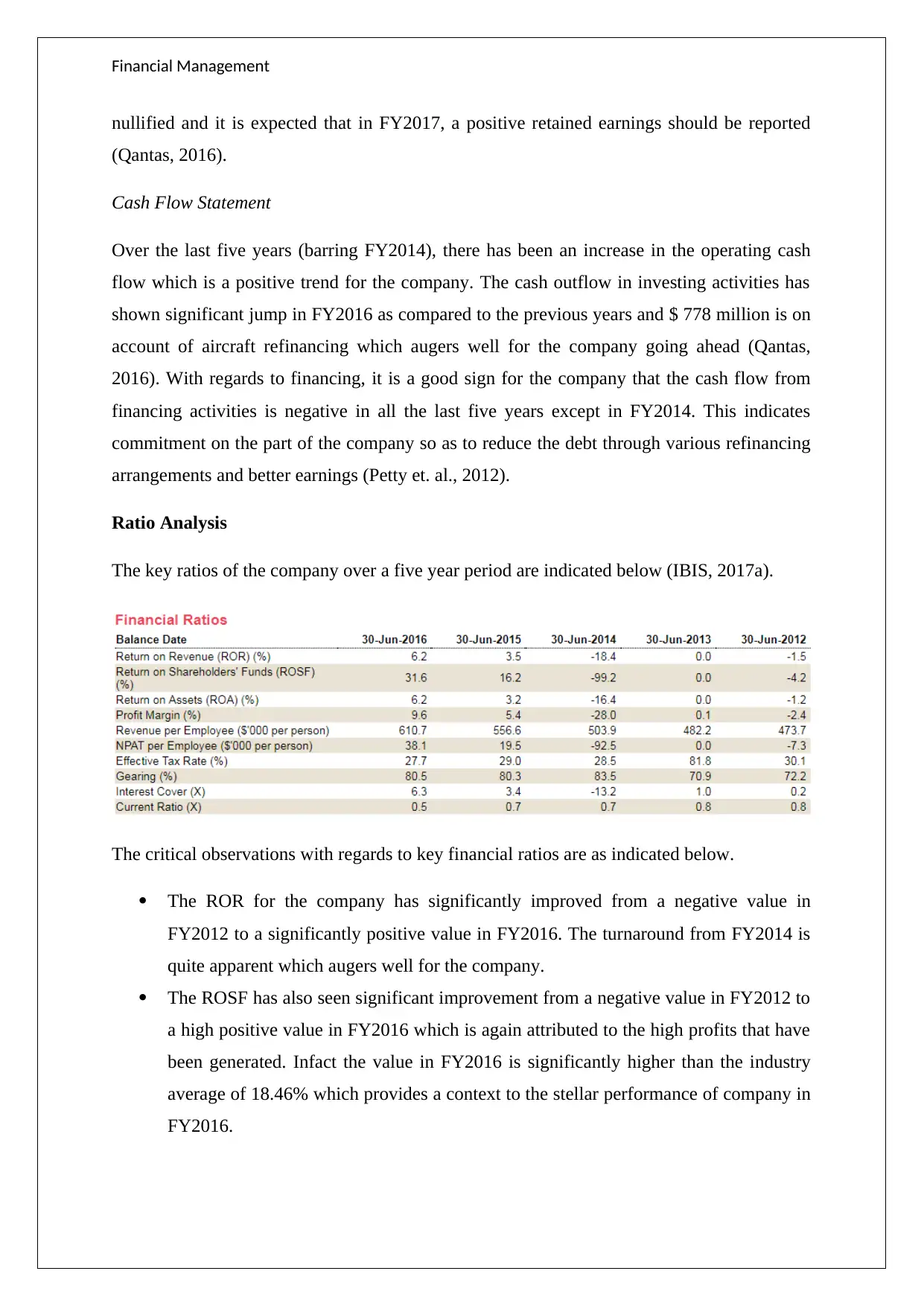

Ratio Analysis

The key ratios of the company over a five year period are indicated below (IBIS, 2017a).

The critical observations with regards to key financial ratios are as indicated below.

The ROR for the company has significantly improved from a negative value in

FY2012 to a significantly positive value in FY2016. The turnaround from FY2014 is

quite apparent which augers well for the company.

The ROSF has also seen significant improvement from a negative value in FY2012 to

a high positive value in FY2016 which is again attributed to the high profits that have

been generated. Infact the value in FY2016 is significantly higher than the industry

average of 18.46% which provides a context to the stellar performance of company in

FY2016.

nullified and it is expected that in FY2017, a positive retained earnings should be reported

(Qantas, 2016).

Cash Flow Statement

Over the last five years (barring FY2014), there has been an increase in the operating cash

flow which is a positive trend for the company. The cash outflow in investing activities has

shown significant jump in FY2016 as compared to the previous years and $ 778 million is on

account of aircraft refinancing which augers well for the company going ahead (Qantas,

2016). With regards to financing, it is a good sign for the company that the cash flow from

financing activities is negative in all the last five years except in FY2014. This indicates

commitment on the part of the company so as to reduce the debt through various refinancing

arrangements and better earnings (Petty et. al., 2012).

Ratio Analysis

The key ratios of the company over a five year period are indicated below (IBIS, 2017a).

The critical observations with regards to key financial ratios are as indicated below.

The ROR for the company has significantly improved from a negative value in

FY2012 to a significantly positive value in FY2016. The turnaround from FY2014 is

quite apparent which augers well for the company.

The ROSF has also seen significant improvement from a negative value in FY2012 to

a high positive value in FY2016 which is again attributed to the high profits that have

been generated. Infact the value in FY2016 is significantly higher than the industry

average of 18.46% which provides a context to the stellar performance of company in

FY2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

The ROA of the company has also undergone significant improvement and at 6.2% in

FY2016, the value exceeds the industry average which highlights the superior

performance of the company which may be attributed to the top management team.

The profit margin has also shown similar improvement as the other parameters

highlighted above. The profit margin for the company in FY2016 is superior to the

industry average of 6.06%.

The company has been able to rationalise the workforce so as to significantly improve

the net profit per employee which in FY2016 stands at $ 38,100 and is significantly

higher in comparison to the industry average of $ 25,340 which highlights the higher

efficiency of processes and productivity of employees.

Gearing ratio of the company is an indication of the capital structure. The gearing

ratio peaked out in FY2014 when the company took a debt in order to restructure and

bring about a turnaround which has led to future savings which have been reaped in

FY2015 and FY2016. In the recent years, there has been a decrease in the gearing

ratio as a result of which this value for the company is close to the industry average of

0.78 as on June 30, 2016. This implies that the balance sheet of the company is not

overleveraged and in this aspect, the company is comparable to the peer group which

is critical considering the outstanding debt concerns in the past (Petty et. al., 2012).

The interest cover has also improved significantly in the recent years which provide

greater comfort to the lenders that the company would be able to meet the interest

obligations (Petty et. al., 2012). The interest cover as on June 30, 2016 is significantly

higher than the industry average of 4 which implies that the company could avail

incremental debt at lower interest rates compared to the peer group.

The trend in current ratio seems worrisome as there is a declining trend which raises

issues over the short term liquidity. Additionally, when seen in the context of airline

industry also, it is apparent that the company’s current ratio as on June 30, 2016 is

inferior to the industry average of 0.62. Thus, it clearly highlights the need to improve

for the company in this regard (IBIS, 2017a).

Future of the business

In order to understand the future of the company, it is imperative to briefly describe the huge

turnaround that the company has witnessed in fortunes since 2014. In 2014, the company was

reeling under debt and was at the verge of closure which forced the company to approach the

Federal government to consider a bailout package which was turned down (Sandilands,

The ROA of the company has also undergone significant improvement and at 6.2% in

FY2016, the value exceeds the industry average which highlights the superior

performance of the company which may be attributed to the top management team.

The profit margin has also shown similar improvement as the other parameters

highlighted above. The profit margin for the company in FY2016 is superior to the

industry average of 6.06%.

The company has been able to rationalise the workforce so as to significantly improve

the net profit per employee which in FY2016 stands at $ 38,100 and is significantly

higher in comparison to the industry average of $ 25,340 which highlights the higher

efficiency of processes and productivity of employees.

Gearing ratio of the company is an indication of the capital structure. The gearing

ratio peaked out in FY2014 when the company took a debt in order to restructure and

bring about a turnaround which has led to future savings which have been reaped in

FY2015 and FY2016. In the recent years, there has been a decrease in the gearing

ratio as a result of which this value for the company is close to the industry average of

0.78 as on June 30, 2016. This implies that the balance sheet of the company is not

overleveraged and in this aspect, the company is comparable to the peer group which

is critical considering the outstanding debt concerns in the past (Petty et. al., 2012).

The interest cover has also improved significantly in the recent years which provide

greater comfort to the lenders that the company would be able to meet the interest

obligations (Petty et. al., 2012). The interest cover as on June 30, 2016 is significantly

higher than the industry average of 4 which implies that the company could avail

incremental debt at lower interest rates compared to the peer group.

The trend in current ratio seems worrisome as there is a declining trend which raises

issues over the short term liquidity. Additionally, when seen in the context of airline

industry also, it is apparent that the company’s current ratio as on June 30, 2016 is

inferior to the industry average of 0.62. Thus, it clearly highlights the need to improve

for the company in this regard (IBIS, 2017a).

Future of the business

In order to understand the future of the company, it is imperative to briefly describe the huge

turnaround that the company has witnessed in fortunes since 2014. In 2014, the company was

reeling under debt and was at the verge of closure which forced the company to approach the

Federal government to consider a bailout package which was turned down (Sandilands,

Financial Management

2014). As a result, the company embarked on an ambitious turnaround plan which involved

cutting down on jobs, dropping unprofitable routes, retiring the old fleet of aircrafts and

deferring the purchase of aircrafts along with cost rationalisation (Park, 2017). This plan has

helped the company to turn around and reap $ 2.1 billion in savings in 2017 alone. Also, the

lower fuel costs contributed immensely to the turnaround for the company (Sheedy, 2016).

Going forward, it is expected that the fuel prices in the short to medium term would be low

only which augers well for not only Qantas but the airline industry as a whole. Also, the

competition between Virgin Australia and Qantas has eased in the recent years owing to

excess capacity generation by both players (Freed, 2016). Further, low cost subsidiary of

Qantas i.e. Jetstar is performing well both in terms of revenue and profitability and going

forward better results may be expected (Chung, 2016). Also, going forward, the company

should look at improving the topline which has been stagnant. Further, the key aspects of the

turnaround strategy must be continued so as to reap cost savings going ahead as well.

Besides, the company must look at improving the services so as to build on the market share

and the brand.

Political competitive environment impact

The political environment tends to have a significant impact on the operation of airlines and

Qantas is no different. One of the recent ways in which the government is impacting the

airline industry is through various environment related taxes owing to the airline emissions

(Kenny, 2014). In Australia also, the scrapping of carbon tax in 2014 has proved to be

positive development for Qantas. Introduction of green taxes can adversely impact the

profitability of the airlines especially against international players based in geographies

where such taxes do not exist (Freed, 2015). Another way in which the government impacts

the airline industry is through the means of taxes which are not only limited to corporate

profits but also on the fuel and the other services. Most of this tax burden is passed on to the

consumers and determines the final cost to be borne by the customer. A lower tax structure

would not only mean higher profitability for the company (Qantas) but also would lead to

higher growth in passengers (Qantas, 2016).

Also, considering that Qantas derives about 40% of the revenue from international flights,

hence the currency rate is also a critical factor which tends to impact the overall competition

(IBIS, 2017b).. Offlate there has been a decline in the value of Australian dollar which has

favoured Qantas and thus it has been able to witness lower competition from international

2014). As a result, the company embarked on an ambitious turnaround plan which involved

cutting down on jobs, dropping unprofitable routes, retiring the old fleet of aircrafts and

deferring the purchase of aircrafts along with cost rationalisation (Park, 2017). This plan has

helped the company to turn around and reap $ 2.1 billion in savings in 2017 alone. Also, the

lower fuel costs contributed immensely to the turnaround for the company (Sheedy, 2016).

Going forward, it is expected that the fuel prices in the short to medium term would be low

only which augers well for not only Qantas but the airline industry as a whole. Also, the

competition between Virgin Australia and Qantas has eased in the recent years owing to

excess capacity generation by both players (Freed, 2016). Further, low cost subsidiary of

Qantas i.e. Jetstar is performing well both in terms of revenue and profitability and going

forward better results may be expected (Chung, 2016). Also, going forward, the company

should look at improving the topline which has been stagnant. Further, the key aspects of the

turnaround strategy must be continued so as to reap cost savings going ahead as well.

Besides, the company must look at improving the services so as to build on the market share

and the brand.

Political competitive environment impact

The political environment tends to have a significant impact on the operation of airlines and

Qantas is no different. One of the recent ways in which the government is impacting the

airline industry is through various environment related taxes owing to the airline emissions

(Kenny, 2014). In Australia also, the scrapping of carbon tax in 2014 has proved to be

positive development for Qantas. Introduction of green taxes can adversely impact the

profitability of the airlines especially against international players based in geographies

where such taxes do not exist (Freed, 2015). Another way in which the government impacts

the airline industry is through the means of taxes which are not only limited to corporate

profits but also on the fuel and the other services. Most of this tax burden is passed on to the

consumers and determines the final cost to be borne by the customer. A lower tax structure

would not only mean higher profitability for the company (Qantas) but also would lead to

higher growth in passengers (Qantas, 2016).

Also, considering that Qantas derives about 40% of the revenue from international flights,

hence the currency rate is also a critical factor which tends to impact the overall competition

(IBIS, 2017b).. Offlate there has been a decline in the value of Australian dollar which has

favoured Qantas and thus it has been able to witness lower competition from international

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

airlines. Thus, various government policies tend to impact the currency rate and in turn the

consumer decisions as explained above (Pash, 2017). Thus, it would be fair to consider that

political factors tend to have a significant impact on the competitive environment of the

company (Qantas, 2014).

Relevant Ethical Considerations

It is well known that insolvency has legal considerations but it also has ethical considerations.

This is because it tends to adversely impact the industry credibility in the eyes of not only the

shareholders but also the suppliers and lenders. In most of the bankruptcies, the role of the

management is pivotal and in most cases there is a fraud with the collusion of the

management especially in case of failure of big companies. This tends to enhance the agency

costs for the remaining firms and dampens the sentiment. If every firm starts acting in this

manner, the participation of these key stakeholders would dwindle and hence even genuine

businesses would face issues (Lubben, 2011).

From a utilitarian perspective also, the businesses should try to extend benefit to the greatest

number of stakeholders through business decisions which is possible when the company is

operational and is professionally managed. Winding up tends to be detrimental to the interest

of the various stakeholders and needs to be avoided. These arguments are further true for a

company such as Qantas which acts as the national carrier of Australia. However, businesses

that are not sustainable due to the faulty business model or inefficient operations must not be

given support by the government and other stakeholders and it is best that these are shut

down as they tend to act as a drag for the resources which could be deployed elsewhere

(Sandilands, 2014).

External factors to be considered

One of the external factors that is pivotal with regards to consolidation is competition. In a

competitive industry such as airlines where there are frequent price wars for customer

acquisition, profitability can be wafer thin especially when the oil prices are high. As a result,

it is imperative to keep the costs down so as to ensure higher profitability margins even when

the topline growth is muted (Posh, 2017). This typically requires economies of scale whereby

the scale becomes pivotal. Further, it is not feasible for too many players to survive in such a

competitive industry as only a few would make profits. Thus, Qantas can potentially look at

airlines. Thus, various government policies tend to impact the currency rate and in turn the

consumer decisions as explained above (Pash, 2017). Thus, it would be fair to consider that

political factors tend to have a significant impact on the competitive environment of the

company (Qantas, 2014).

Relevant Ethical Considerations

It is well known that insolvency has legal considerations but it also has ethical considerations.

This is because it tends to adversely impact the industry credibility in the eyes of not only the

shareholders but also the suppliers and lenders. In most of the bankruptcies, the role of the

management is pivotal and in most cases there is a fraud with the collusion of the

management especially in case of failure of big companies. This tends to enhance the agency

costs for the remaining firms and dampens the sentiment. If every firm starts acting in this

manner, the participation of these key stakeholders would dwindle and hence even genuine

businesses would face issues (Lubben, 2011).

From a utilitarian perspective also, the businesses should try to extend benefit to the greatest

number of stakeholders through business decisions which is possible when the company is

operational and is professionally managed. Winding up tends to be detrimental to the interest

of the various stakeholders and needs to be avoided. These arguments are further true for a

company such as Qantas which acts as the national carrier of Australia. However, businesses

that are not sustainable due to the faulty business model or inefficient operations must not be

given support by the government and other stakeholders and it is best that these are shut

down as they tend to act as a drag for the resources which could be deployed elsewhere

(Sandilands, 2014).

External factors to be considered

One of the external factors that is pivotal with regards to consolidation is competition. In a

competitive industry such as airlines where there are frequent price wars for customer

acquisition, profitability can be wafer thin especially when the oil prices are high. As a result,

it is imperative to keep the costs down so as to ensure higher profitability margins even when

the topline growth is muted (Posh, 2017). This typically requires economies of scale whereby

the scale becomes pivotal. Further, it is not feasible for too many players to survive in such a

competitive industry as only a few would make profits. Thus, Qantas can potentially look at

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial Management

the players that are making losses but have potential to be turned around as possible

acquisition targets.

Further, the industry dynamics is such that an airline business has various verticals and

usually a particular company does not have strong presence in each of these. Hence, it makes

sense for a company like Qantas to make acquisition in one of these verticals in order to

increase market share. For instance in the airline catering business, Qantas has a paltry

market share of 4% and thus can potentially acquire bigger players in this segment so as to

enhance the overall share and reap synergies (IBIS, 2017b).. However, the regulatory

environment would also need to be considered which would be particularly relevant if for

instance Virgin Australia and Qantas decide to merge as it would create a virtual monopoly in

domestic flights and hence may be objected to.

Conclusion & Recommendation

The above discussion indicates that the company has had a turnaround from FY2015 onwards

and it is expected that the company would continue to outperform the industry in the near

future especially till the crude oil prices remain reasonably low. Even though from the low

price of around $ 1.5 seen in FY2014, the Qantas stock has tripled but considering the sound

management in place, increasing tourism in Australia, market leadership in international

flight, lower competition in domestic flights and low price of crude oil, it makes sense to

invest in the company from a medium term perspective. However, the company performance

needs to be carefully monitored since the industry has significant external leverages such as

political environment and crude oil prices.

the players that are making losses but have potential to be turned around as possible

acquisition targets.

Further, the industry dynamics is such that an airline business has various verticals and

usually a particular company does not have strong presence in each of these. Hence, it makes

sense for a company like Qantas to make acquisition in one of these verticals in order to

increase market share. For instance in the airline catering business, Qantas has a paltry

market share of 4% and thus can potentially acquire bigger players in this segment so as to

enhance the overall share and reap synergies (IBIS, 2017b).. However, the regulatory

environment would also need to be considered which would be particularly relevant if for

instance Virgin Australia and Qantas decide to merge as it would create a virtual monopoly in

domestic flights and hence may be objected to.

Conclusion & Recommendation

The above discussion indicates that the company has had a turnaround from FY2015 onwards

and it is expected that the company would continue to outperform the industry in the near

future especially till the crude oil prices remain reasonably low. Even though from the low

price of around $ 1.5 seen in FY2014, the Qantas stock has tripled but considering the sound

management in place, increasing tourism in Australia, market leadership in international

flight, lower competition in domestic flights and low price of crude oil, it makes sense to

invest in the company from a medium term perspective. However, the company performance

needs to be carefully monitored since the industry has significant external leverages such as

political environment and crude oil prices.

Financial Management

References

Chung, F. (2016), Qantas posts record $1.53 billion full-year profit, Perth Now, [Online]

Available at http://www.perthnow.com.au/business/companies/qantas-just-had-its-best-year-

ever/news-story/f19ad5ddc1320591487eec0a5ffab7ab [Available August 25, 2017]

Freed, J. (2015). The five reasons Qantas is back in the black, The Sydney Morning Herald,

[Online] Available at http://www.smh.com.au/business/aviation/the-five-reasons-qantas-is-

back-in-the-black-20150224-13nbws.html [Available August 25, 2017]

IBIS (2017a), Industry Average & Financial Ratios, IBIS World Website, [Online] Available

at http://clients1.ibisworld.com.au/reports/au/enterprisepremium/averages.aspx?entid=32

[Available August 25, 2017]

IBIS (2017b), Segment & Subsidiaries, IBIS World Website, [Online] Available at

http://clients1.ibisworld.com.au/reports/au/enterprisepremium/environment.aspx?entid=32

[Available August 25, 2017]

Kenny, M (2014), Qantas 'pressured on carbon tax', The Sydney Morning Herald, [Online]

Available at http://www.smh.com.au/federal-politics/political-news/qantas-pressured-on-

carbon-tax-20140306-34a8c.html [Available August 25, 2017]

Lubben, S. (2011), Corporate Bankruptcy Raises a Question of Ethics, The New York Times,

[Online] Available at https://dealbook.nytimes.com/2011/12/09/corporate-bankruptcy-raises-

a-question-of-ethics/?mcubz=0 [Available August 25, 2017]

Park, K. (2017), Qantas Turnaround Wizard Joyce Has a One-Word Lesson for Cathay,

Bloomberg Website, [Online] Available at https://www.bloomberg.com/news/articles/2017-

03-16/qantas-turnaround-wizard-joyce-has-a-one-word-lesson-for-cathay [Available August

25, 2017]

Pash, C. (2017), The Qantas turnaround is complete, Business Insider, [Online] Available at

https://www.businessinsider.com.au/the-qantas-turnaround-is-complete-2017-8 [Available

August 25, 2017]

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th edn. NSW: Pearson Education,

French Forest Australia.

References

Chung, F. (2016), Qantas posts record $1.53 billion full-year profit, Perth Now, [Online]

Available at http://www.perthnow.com.au/business/companies/qantas-just-had-its-best-year-

ever/news-story/f19ad5ddc1320591487eec0a5ffab7ab [Available August 25, 2017]

Freed, J. (2015). The five reasons Qantas is back in the black, The Sydney Morning Herald,

[Online] Available at http://www.smh.com.au/business/aviation/the-five-reasons-qantas-is-

back-in-the-black-20150224-13nbws.html [Available August 25, 2017]

IBIS (2017a), Industry Average & Financial Ratios, IBIS World Website, [Online] Available

at http://clients1.ibisworld.com.au/reports/au/enterprisepremium/averages.aspx?entid=32

[Available August 25, 2017]

IBIS (2017b), Segment & Subsidiaries, IBIS World Website, [Online] Available at

http://clients1.ibisworld.com.au/reports/au/enterprisepremium/environment.aspx?entid=32

[Available August 25, 2017]

Kenny, M (2014), Qantas 'pressured on carbon tax', The Sydney Morning Herald, [Online]

Available at http://www.smh.com.au/federal-politics/political-news/qantas-pressured-on-

carbon-tax-20140306-34a8c.html [Available August 25, 2017]

Lubben, S. (2011), Corporate Bankruptcy Raises a Question of Ethics, The New York Times,

[Online] Available at https://dealbook.nytimes.com/2011/12/09/corporate-bankruptcy-raises-

a-question-of-ethics/?mcubz=0 [Available August 25, 2017]

Park, K. (2017), Qantas Turnaround Wizard Joyce Has a One-Word Lesson for Cathay,

Bloomberg Website, [Online] Available at https://www.bloomberg.com/news/articles/2017-

03-16/qantas-turnaround-wizard-joyce-has-a-one-word-lesson-for-cathay [Available August

25, 2017]

Pash, C. (2017), The Qantas turnaround is complete, Business Insider, [Online] Available at

https://www.businessinsider.com.au/the-qantas-turnaround-is-complete-2017-8 [Available

August 25, 2017]

Petty, J.W., Titman, S., Keown, A., Martin, J.D., Martin, P., Burrow, M., and Nguyen, H. (2012)

Financial Management, Principles and Applications. 6th edn. NSW: Pearson Education,

French Forest Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial Management

Qantas (2014), Annual Report 2014, Qantas Website, [Online] Available at

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2014AnnualReport.pdf [Available August 25, 2017]

Qantas (2016), Annual Report 2016, Qantas Website, [Online] Available at

https://www.qantas.com.au/infodetail/about/corporateGovernance/2016AnnualReport.pdf

[Available August 25, 2017]

Sandilands, B. (2014), Qantas strategy runs into political, investor headwinds, Crikey Blog,

[Online] Available at https://blogs.crikey.com.au/planetalking/2014/02/27/qantas-strategy-

runs-into-political-investor-headwinds/ [Available August 25, 2017]

Sheedy, C. (2016), Qantas: The most remarkable turnaround in aviation history?, ICAS

Website, [Online] Available at https://www.icas.com/ca-today-news/qantas-nine-lives-flying-

kangaroo [Available August 25, 2017]

Qantas (2014), Annual Report 2014, Qantas Website, [Online] Available at

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2014AnnualReport.pdf [Available August 25, 2017]

Qantas (2016), Annual Report 2016, Qantas Website, [Online] Available at

https://www.qantas.com.au/infodetail/about/corporateGovernance/2016AnnualReport.pdf

[Available August 25, 2017]

Sandilands, B. (2014), Qantas strategy runs into political, investor headwinds, Crikey Blog,

[Online] Available at https://blogs.crikey.com.au/planetalking/2014/02/27/qantas-strategy-

runs-into-political-investor-headwinds/ [Available August 25, 2017]

Sheedy, C. (2016), Qantas: The most remarkable turnaround in aviation history?, ICAS

Website, [Online] Available at https://www.icas.com/ca-today-news/qantas-nine-lives-flying-

kangaroo [Available August 25, 2017]

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.