Detailed Budget Report: Financial Analysis of Hamble Ltd - QH0320

VerifiedAdded on 2023/06/18

|10

|1471

|185

Report

AI Summary

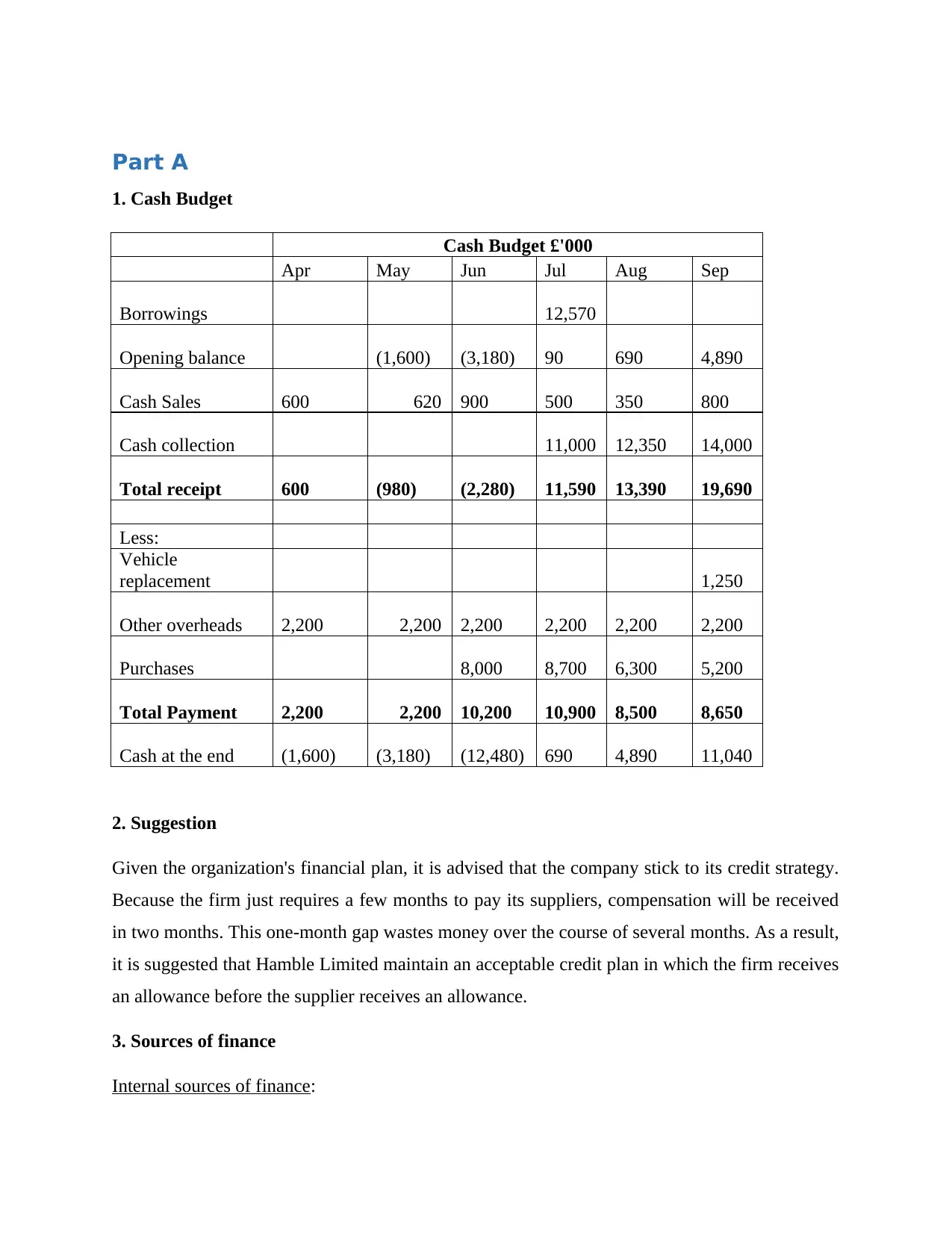

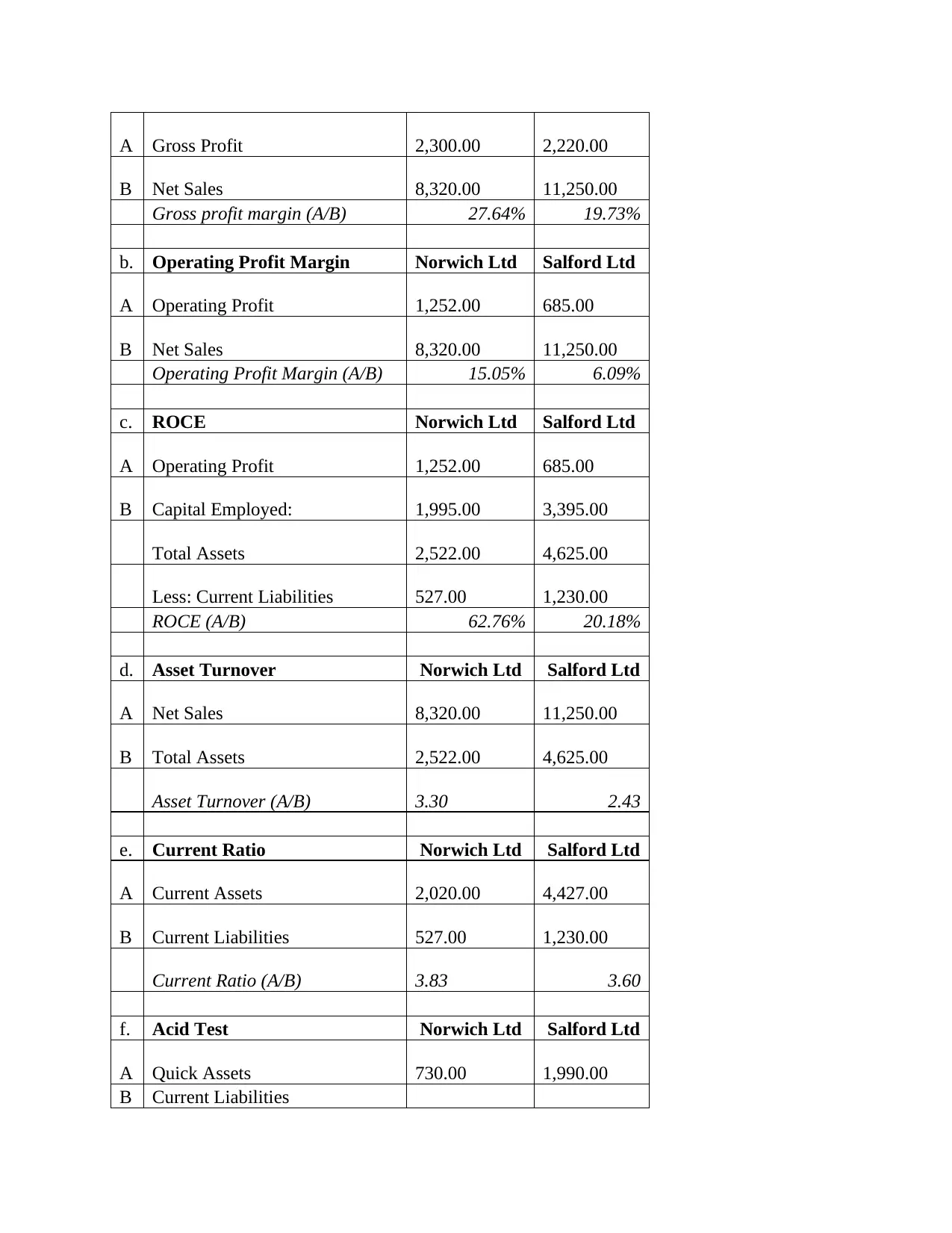

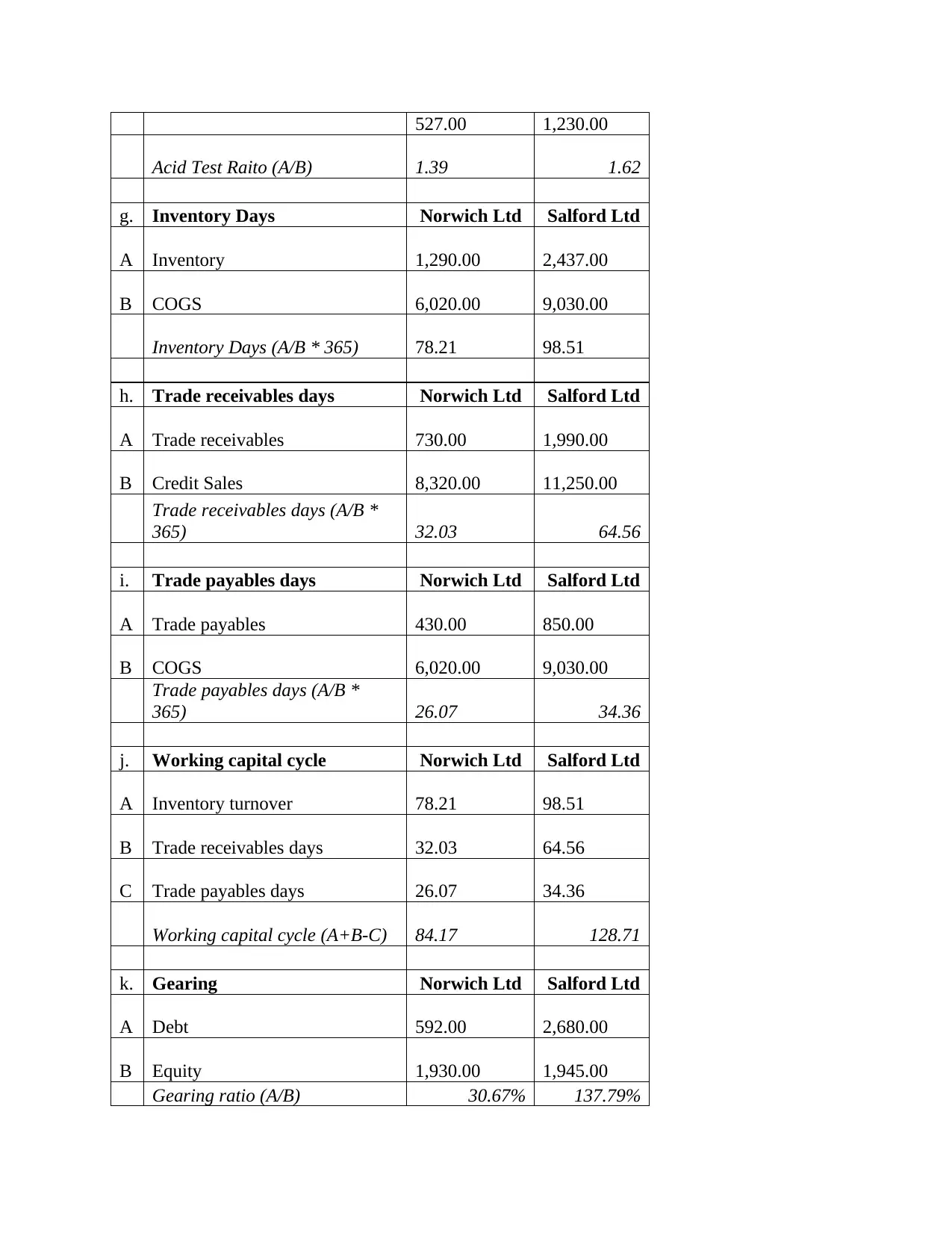

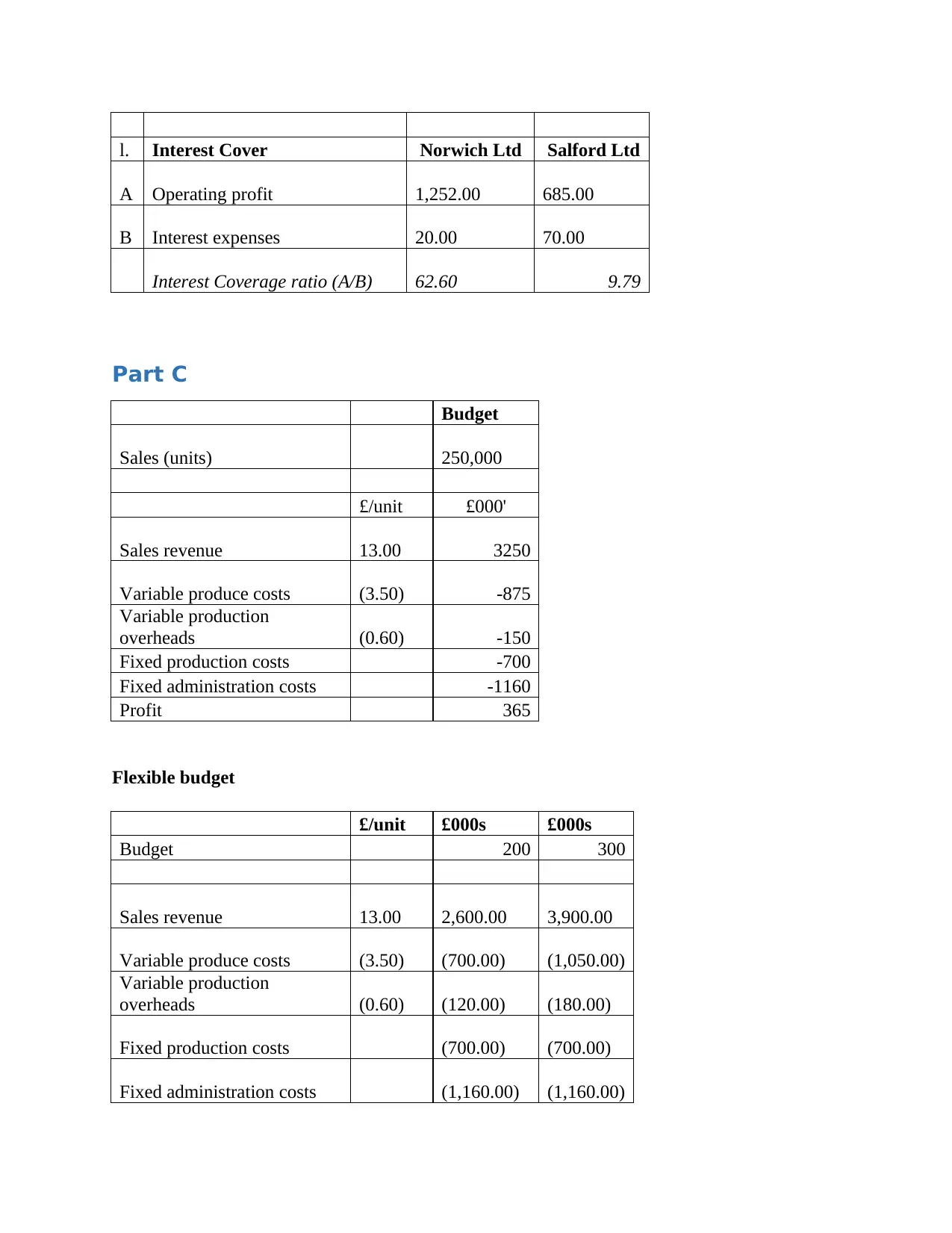

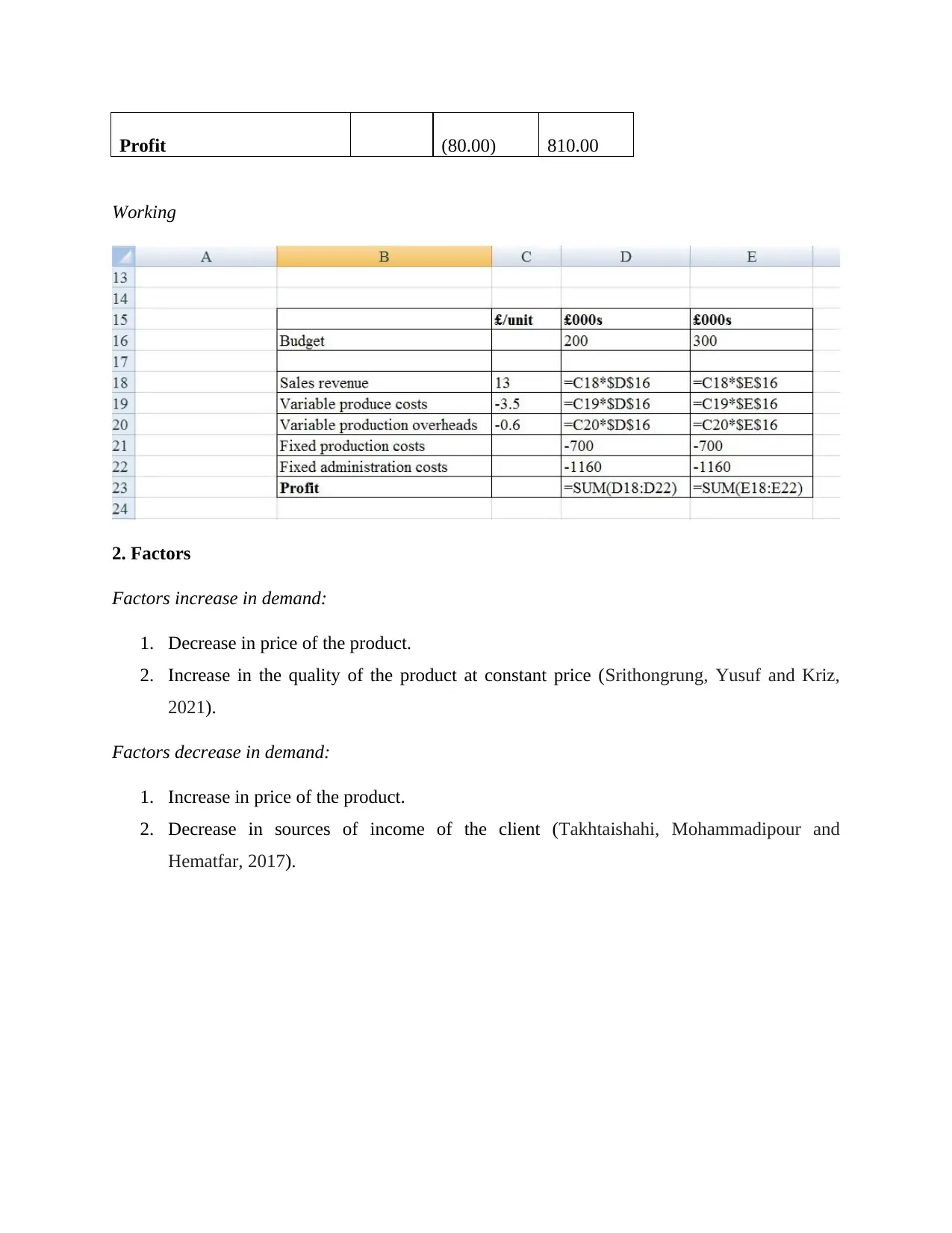

This assignment is a budget report focusing on the financial analysis of Hamble Ltd. Part A includes a cash budget, suggestions for the company's credit strategy, and a discussion of internal and external sources of finance, specifically the issue of shares, along with their respective advantages and disadvantages. Part B presents a detailed ratio analysis of Norwich Ltd and Salford Ltd, covering gross profit margin, operating profit margin, ROCE, asset turnover, current ratio, acid test, inventory days, trade receivables days, trade payables days, working capital cycle, gearing, and interest cover. Part C includes a flexible budget and an analysis of factors that increase or decrease demand for the company's products. The report also includes relevant references to support the analysis and recommendations.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.